Quick Answer

Yes. Easy cancellation can raise long-term value, but only when you run it as a measured monetization change instead of a trust-only gesture. The article ties this to Federal Trade Commission click-to-cancel enforcement pressure and a practical proof rule: track saved cohorts over a defined window, such as 90 days, and keep the change only if reactivation, net churn, and NRR quality improve.

Why easy cancellation is a growth decision not a surrender#

Easy cancellation is not a concession if you treat it as an active retention choice, not a passive churn policy. It can improve Customer Lifetime Value, but only when the exit is paired with better saves, cleaner segmentation, and a way to measure whether the customers you kept were worth keeping.

That distinction matters because different teams read cancellation through different lenses. Founders and revenue leaders see near-term Monthly Recurring Revenue at risk. Product teams worry about friction, trust, and brand damage. Finance cares about margin quality, not just headline save rate.

If you force people through extra steps to stop paying, you may preserve some MRR this month. You may also create the kind of "endless hoops" friction the FTC has warned about, which can damage trust and raise compliance risk.

There is now a hard floor under this discussion. The Federal Trade Commission announced its final click-to-cancel rule on October 16, 2024. The Negative Option Rule took effect on January 14, 2025, with key cancellation compliance due by May 14, 2025. The standard is simple: cancellation must be as easy as signup. So "make it harder to leave" is no longer just a questionable retention tactic. It is also a compliance and enforcement risk. The FTC has framed hard cancellation UX as making people "jump through endless hoops," and its September 25, 2025 announcement of a $2.5 billion Amazon settlement tied to alleged cancellation friction shows the risk is not theoretical.

What is clear today is the direction, not the size of the effect. Public case-style sources report anything from roughly 20% LTV improvement to claims of doubled LTV. That range is too wide for a CFO to underwrite blindly, but it still tells you something useful: easier exits can support better economics in some contexts. What it does not tell you is whether your users, pricing, and save tactics will produce the same result.

Use a simple decision rule. If you make cancellation easier, test it as a monetization change, not a trust gesture alone. Set up a cohort test before rollout and read more than cancel completion. The checkpoint is whether saved users retain, reactivate, and contribute margin over a defined window such as 90 days, not whether fewer people made it to the final cancel screen.

The failure mode is expensive. Teams remove dark patterns, see an initial rise in completed cancels, panic, then reintroduce friction or blanket discounts without learning which customers were actually high fit. A better path is a CFO-safe retention strategy. Comply with cancellation parity, keep the exit clean, and use the cancellation moment to make smarter choices about who should be saved, who should pause, and who should leave with a good enough experience to return later.

Related reading: Freelance Client Retention: Weekly Systems for Repeat Work and Long-Term Relationships.

The retention math leaders should align on first#

Align on retention math before debating UX, or the same cancellation change will look like both a win and a failure across teams.

Start with the two definitions that matter most:

- Customer Lifetime Value (LTV): cumulative gross profit from a customer over the relationship, not just billed revenue.

- Net Revenue Retention (NRR): revenue retained from existing customers after expansion and churn are counted together.

NRR = (Starting MRR + Expansion MRR - Churn MRR) / Starting MRR

If you discuss churn without expansion, or LTV without gross profit, you are making monetization decisions on softer terms than they appear.

What easier cancellation can change#

A lower-friction cancellation flow can reduce the "trapped" experience and improve the quality of how customers leave. That matters in recurring models where billing forgetfulness is common: one survey found 74% of consumers said recurring charges were easy to forget, and 42% said they had stopped using a subscription but kept paying. In that context, forcing saves can protect this month's MRR while reducing the odds of a clean return later.

Research on long-commitment decisions also suggests that clear cancel options can reduce commitment pressure and increase purchase intent. Treat reactivation and referral effects as measurable hypotheses, not guaranteed outcomes.

The tradeoff leaders need to model together#

The rule is simple: a higher save rate is only good if saved cohorts hold value after the save. If saves rely on deep discounts, add support burden, or keep low-fit customers who churn again next cycle, headline retention can rise while LTV quality falls.

Use cohort retention analysis, not aggregate reporting, to verify results. Compare cohorts by offer type, segment, and start month, then review retained gross profit, reactivation, support burden, and NRR movement. Set the review window before launch, for example a 90-day quality gate for monthly subscriptions. If save rate rises but retention quality worsens in that window, treat it as a failed monetization change and rework it.

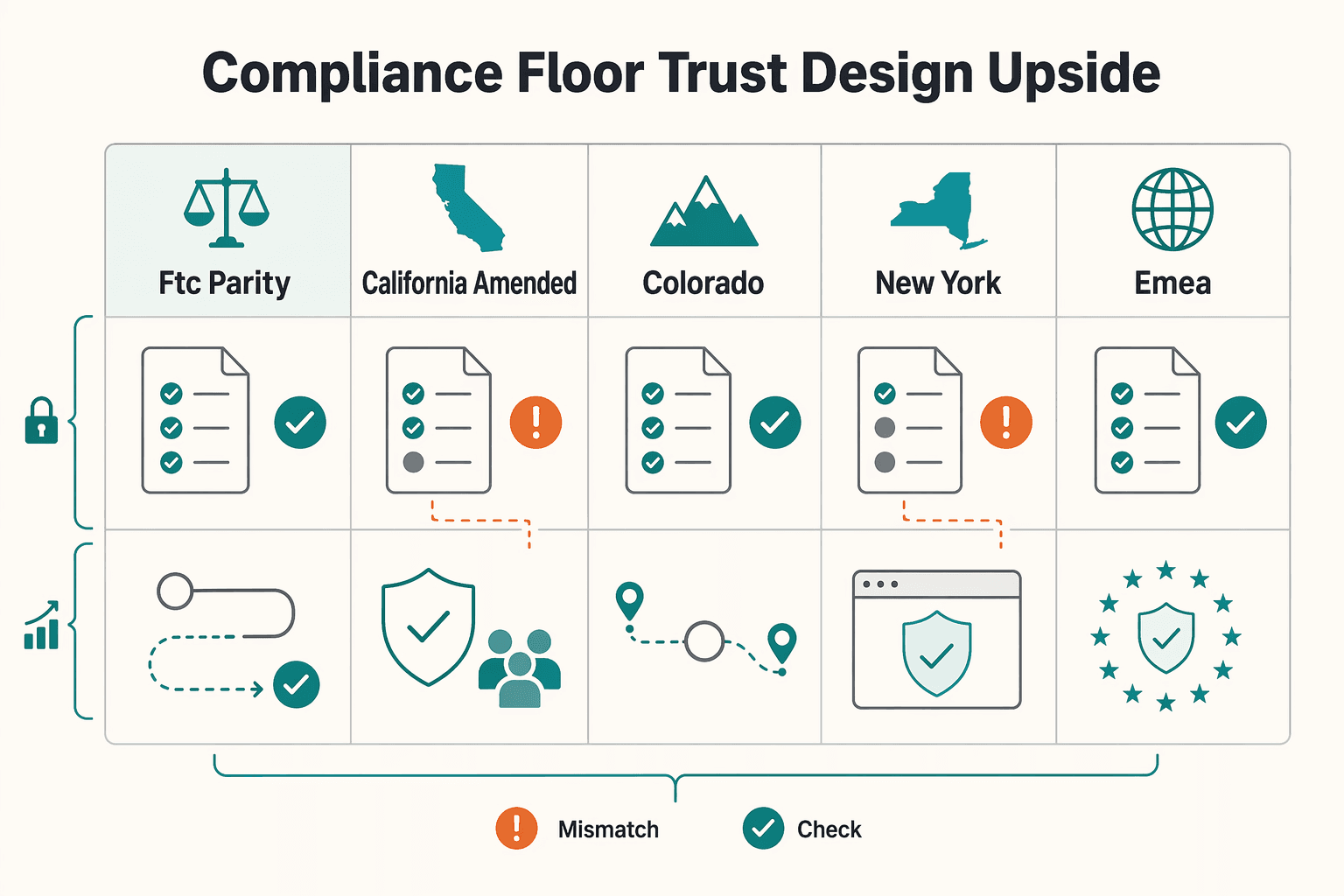

Compliance is the floor and trust design is the upside#

Compliance is the baseline. Trust design is where you create retention upside. Easy cancellation is no longer a brand extra; it is a market expectation shaped by federal pressure and jurisdiction-specific consumer rules.

| Area | Timing/scope | Stated rule |

|---|---|---|

| FTC parity principle | October 16, 2024 framing; recodified effective February 12, 2026 | Cancellation should be as easy as signup |

| California amended ARL | Effective July 1, 2025 | Clear and straightforward cancellation method |

| Colorado | One-step online cancellation | Simple, timely, easy-to-use mechanism |

| New York | Price-increase handling in scope cases | At least a 14-day post-charge cancellation window |

| EU / EMEA | Qualifying distance or off-premises purchases | Can include a 14-day cooling-off period; country implementation and UK rules differ |

The FTC's October 16, 2024 click-to-cancel framing set a clear parity principle: cancellation should be as easy as signup. That principle is still useful for product design, even though the FTC recodified the Negative Option Rule text to its pre-2024 amended version effective February 12, 2026 after court outcomes. Build to the markets you serve, not a vague national average, and get counsel sign-off on the actual flow.

Jurisdiction variance is the operator reality. California's amended ARL, effective July 1, 2025, requires a clear and straightforward cancellation method. Colorado defines one-step online cancellation and requires a simple, timely, easy-to-use mechanism. New York includes cancellation rights tied to price-increase handling, including at least a 14-day post-charge cancellation window in scope cases. In EMEA, do not assume one rulebook: EU consumer contracts can include a 14-day cooling-off period for qualifying distance or off-premises purchases, while country implementation and UK rules differ.

| Area | Regulatory minimum behavior | Trust-building behavior |

|---|---|---|

| Exit parity | Cancellation is as easy to start as signup | Put cancel in account settings, not behind support |

| Reminders | Send required renewal or charge notices where applicable | Remind early enough for a real decision, with plan details |

| Confirmation clarity | Confirm cancellation in plain language | State effective date, last bill date, and what access remains |

| Post-cancel path | Honor required rights and timelines | Offer reactivation, data export, or downgrade without pressure |

Use one release checkpoint: legal reviews the flow first, then product reviews labels, error states, and confirmation copy for hidden friction. Teams often fail here with technically compliant language that still creates confusion through guilt framing, unclear dates, or vague outcomes.

Build a cancellation decision path by segment not one generic screen#

Treat cancellation as a decision path, not a single screen: keep immediate cancel available, then branch only where an alternative is actually relevant.

Once the exit flow is easy and compliant, the next question is commercial: who should see an alternative, and who should exit with no extra friction?

Start with reason codes that drive action#

Reason codes should change what happens next, not just log feedback. Use them to route by intent, value tier, tenure, and usage, then pair each route with a clear success metric.

A practical taxonomy can stay simple:

- temporary constraint

- price mismatch

- low or no usage

- product fit problem

- support or billing issue

- switching away permanently

If a reason code has no owner, no branch, or no metric, it is survey clutter.

Branch by user state, not by hope#

Make branching logic explicit. Low-fit users should get fast cancellation plus clean reactivation hooks. Higher-fit users with temporary constraints can see a pause offer or a tightly scoped save offer.

Pause is useful because it creates a middle state between active and lost. In one operator case, pause was used by 20% of users who clicked to cancel. Treat that as evidence that pause can convert some cancellation intent, not as a universal benchmark.

Use this operating rule:

- engaged but constrained users: test value-preserving alternatives first

- persistent low-usage or repeated low-fit users: prioritize graceful exit and clean return paths

For cost-sensitive but engaged users, plan-rightsizing can be a first test before discounting. For persistent low-usage users, repeated save prompts often add friction without changing the outcome.

Use a compact decision table and maintain it as product logic#

| Reason code | Offer type | Eligibility guardrail | Success metric |

|---|---|---|---|

| Temporary pause in need or timing | Pause offer | Show only to users with recent engagement or clear prior value | Pause acceptance and later reactivation |

| Price too high but still engaged | Plan-rightsizing or narrow save offer | Limit by value tier, tenure, or prior offer usage | Retained revenue quality, not just acceptance |

| Persistent low usage | Immediate cancel with clean reactivation prompt | No extra save screen after repeated low-fit signals | Cancel completion and later reactivation |

| Product fit or service issue | Immediate cancel or support resolution path | Route only if issue is actually fixable in-session | Support contacts, cancellations avoided without friction |

Keep separate decision tables for consumer subscriptions and supply-side cohorts instead of forcing one logic model across both.

Final check before launch: review any cancellation eligibility settings, including processed-charge requirements, with legal, then QA every branch so hidden rules do not make cancellation harder than policy intends.

Related: Bad Payouts Are Costing You Supply: How Payout Quality Drives Contractor Retention.

Instrument the funnel so finance and product read the same truth#

You do not have a retention strategy until product and finance are reading the same cancellation story from the same funnel definition.

Define ordered events first, then build a compact scorecard that separates raw behavior from business outcomes. Ordered funnel analysis only works when the sequence is explicit and stable across releases, so document your event path, for example initiated, offer shown, offer accepted, canceled, reactivated, and keep names consistent.

Start with event definitions, not dashboard tiles#

Treat events and metrics as different objects. Events are actions that happened; metrics are rollups computed from those actions. If that line blurs, dashboard drift follows.

For this funnel, run a basic but strict QA check: each event should fire once in the correct order for a single cancellation path. The common failures are duplicate firings, looped paths, or a reactivation trigger that does not reflect an actual return.

Reactivation should also be defined the same way across teams. Product may track user-level reactivation rate, while finance may track reactivation MRR, but both sides should agree on population, trigger, and time window.

Use a compact scorecard with one primary metric and real guardrails#

Each release should have one primary metric to decide win or loss, plus guardrails to catch side effects.

| Metric | What it tells you | Why it matters |

|---|---|---|

| Cancel completion rate | Whether users can finish cancellation | Surfaces friction in the flow |

| Save acceptance quality | Whether accepted saves hold up after the click | Filters out low-quality saves |

| Reactivation rate | Whether canceled users return | Captures return behavior over time |

| Net churn | Revenue loss after retention effects | Keeps focus on business impact |

| Net Revenue Retention | Retained and expanded recurring revenue from existing customers | Includes churn and expansion together |

| Support contacts per cancellation | Whether the flow creates confusion or cleanup work | Exposes operational cost |

For finance, NRR is a key anchor because it captures more than cancellations alone: NRR = (Starting MRR + Expansion MRR - Churn MRR) / Starting MRR.

Track the risks that can make a "win" look better than it is#

Do not treat a higher acceptance rate as enough on its own. Define a false-save rate internally before launch, for example saved users who still churn inside your review window, so quality is measured, not assumed.

Also track involuntary churn rebound and discount dependency by segment. Otherwise, a short-term lift can hide weaker revenue quality or behavior you do not want to train.

Require one short evidence pack for every release:

- Hypothesis and primary metric

- Cohort test design and population

- Metric window for immediate and delayed outcomes

- Pre-agreed stop/go thresholds and guardrails

This keeps product and finance aligned on what counts as a real win before results arrive.

Use save offers with guardrails so margin quality does not erode#

Use save offers, but put price cuts last. Start with value-preserving moves like plan-fit changes or a pause offer, and treat discounts as a narrower tool for specific segments. If an offer reduces near-term churn but weakens contribution margin in your defined review window, including a six-month window if that is your standard, remove it even when top-line retention looks better.

This follows the scorecard logic from the prior section: a save only counts if revenue quality holds up. Contribution margin is the right lens because it focuses on sales revenue minus variable costs, not just whether an account stayed one more cycle. Discount-led saves lower realized revenue per unit sold, so they should clear a higher bar than pause or downgrade paths.

Set an offer order that protects value first#

A practical hierarchy:

| Move | Use when | Guidance |

|---|---|---|

| Fix fit before price | The customer still has core value but is on the wrong plan | Try rightsizing or feature fit first |

| Pause offer | Temporary constraints are driving the cancellation | Surface pause clearly in the cancellation flow |

| Discounts | The account still looks healthy at the lower price | Reserve price cuts for high-fit cases |

In practice, run that sequence top to bottom: fix fit before price, use pause for temporary constraints, and reserve price cuts for accounts that still look healthy at the lower price.

There is directional evidence that pause deserves real placement. Recurly guidance reports subscription pause usage up 68% year over year in 2024 and 51.7% retention for businesses offering pause instead of outright cancellation. Use that as signal, then validate with your own cohorts.

Put eligibility rules in writing and watch for drift#

Guardrails matter because offers train behavior. If everyone gets the same discount, some users will learn to trigger cancellation to get a lower price. Define eligibility rules you can defend, such as tenure, prior offer usage, and segment behavior.

Keep those rules in your evidence pack and review drift on a regular cadence, such as quarterly. Watch repeat offer usage, discount concentration by segment, and where margin erosion clusters. The failure mode is rarely acceptance alone; it is repeat discount capture or quick churn after accepting a lower-price save.

Keep the exit path clean and honest#

Saves are allowed, but they cannot block cancellation. The FTC announced its final Click to Cancel rule on October 16, 2024, and stated that most provisions take effect 180 days after Federal Register publication. The framing requires cancellation to be as easy as sign-up, with a simple, easy-to-use cancellation mechanism.

Keep copy plain, avoid dark patterns, and keep a clear cancel path on every offer screen. If a user declines a pause or save offer, the next step should be cancellation completion, not another detour.

Community can reinforce retention when cancellation stays easy and trust stays high. See How to Use a Community to Reduce Churn and Increase LTV.

Common failure modes that make easy cancellation backfire#

Easy cancellation backfires when teams optimize for short-term saves instead of long-term retention quality. The pattern is consistent: a save is not a win if those users churn soon after, never reactivate, or only stay at a margin-damaging price.

| Failure mode | What it looks like | Why it backfires |

|---|---|---|

| Wrong metric focus | Save rate or total accepted offers becomes the main readout | Can hide delayed churn or weaken pricing power |

| Compliance-only implementation | The flow meets legal requirements but still feels like users must jump through hoops | Can still fail commercially if the experience feels evasive |

| Billing-only ownership | Cancellation sits only with billing ops instead of product, finance, and lifecycle marketing | Breaks the loop between exit reasons and packaging, pricing tests, and win-back strategy |

False wins from the wrong metric#

Save rate is a diagnostic, not the goal. In a Monthly Recurring Revenue model, it can hide whether you retained real product fit or just delayed churn with a generic offer.

Recurly's point is operational: cancellation reasons are specific, and generic saves produce generic results. If your flow treats every exit the same, your dashboard can reward the wrong behavior.

Generic discounts are the biggest trap. They can hide weak segmentation and, over time, weaken pricing power by training customers to ask for price cuts at cancellation.

A practical check: track saves by reason code and segment, not only total accepted offers. If outcomes look flat across very different reasons, your instrumentation is too blunt.

Compliance can still miss the trust problem#

Meeting a legal requirement is necessary, but it is not enough to protect trust. The FTC has documented dark-pattern cancellation flows, including cases where users had to handle a maze of screens, and consumer reporting still describes people having to jump through hoops to cancel.

The fatigue signal is also clear: 74% of consumers said recurring subscription charges are easy to forget, and 42% said they stopped using a service but forgot they were still paying. So a compliance-only implementation can still fail commercially if the experience feels evasive.

Billing admin ownership slows learning#

Cancellation should not sit only with billing ops. When product, finance, and lifecycle marketing are not jointly accountable, teams lose the loop between exit reasons and better packaging, pricing tests, and win-back strategy.

Use a release-level evidence pack to keep that loop tight:

- reason-code distribution before vs. after changes

- save and cancel outcomes by segment, not just totals

- reactivation and discount reuse over your chosen review window

Use stories from Chargebee or Recurly as hypotheses, not proof. Their patterns are useful inputs, but your audience, product, and unit economics decide what actually works.

For the operational side of save offers, see Build a Cancellation Flow That Saves the Right Subscribers.

Execute a 30-day rollout with explicit owners and checkpoints#

Run this as a controlled 30-day rollout with clear ownership, explicit artifacts, and a hard decision gate before scaling. The goal is not a temporary save-rate lift, but stronger cohort-quality signals after cancel, pause, or save decisions.

| Week | Lead owner | Main output | Checkpoint |

|---|---|---|---|

| 1 | Product with legal, lifecycle marketing, and finance | target outcomes, jurisdiction constraints, baseline scorecard | signed metric definitions and release scope |

| 2 | Product and data | cancel reason taxonomy, event instrumentation, decision logic | event QA and branch-level verification |

| 3 | Finance or analytics with product | first cohort test and review cadence | hypothesis sheet, sample status, adverse-selection and delayed-conversion checks |

| 4 | Cross-functional owner | shared decision doc with keep, change, remove | next experiment queue and scale-or-pause call |

Week 1 alignment#

Define success metrics before changing the flow. Predetermined business-success metrics keep you from choosing whatever metric looks best after launch.

Set owners by function: product owns test design, legal confirms jurisdiction scope, finance signs off on the economic scorecard, and lifecycle marketing defines what happens after cancel, pause, or save. Freeze a pre-change baseline for cancel initiation, cancel completion, offer acceptance, completed cancellations, and reactivation, and record the exact current cancellation copy and screen order.

Week 2 shipping decision logic#

Ship the measurement layer before you optimize outcomes. That means structured cancel reasons, event-level instrumentation, and explicit branch logic for cancel now vs pause offer vs save offer.

Keep the test clean by changing one primary element at a time. Before launch, verify each branch logs exposure, acceptance, and final outcome in the right sequence. If any branch is missing event truth, do not start the test.

Week 3 cohort test and Week 4 decision gate#

Run week three with written hypotheses, a primary metric, a review window, and a stop rule, then evaluate in a cohort retention view instead of relying on same-day save rate. This is where you check whether retention quality improves across lifecycle outcomes such as revenue and conversion behavior.

Include explicit checks for adverse selection, involuntary churn, and delayed conversion effects, and avoid frequent peeking that can inflate false positives. If you are using Amplitude uniques guidance, wait until each variant reaches at least 100 exposures and 25 conversions before reading p-values or confidence intervals.

Week four ends with an operating record, not a vanity uplift slide. Document hypothesis, change, metric window, legal notes, sample status, and a keep/change/remove decision for each branch. If early wins do not improve Customer Lifetime Value quality indicators, pause rollout and fix segmentation before scaling.

Make cancellation easy and retention decisions smarter#

The durable win is not choosing between hard cancel and easy cancel. It is an easy exit paired with segmented stay paths and a strict proof standard for revenue quality.

Treat the cancel flow as a retention decision point, not a billing cleanup screen. Friction can raise short-term saves, but it can also backfire on trust, so the better tradeoff is simple cancellation with relevant alternatives for the right customer.

That means using segmented cancellation logic instead of one generic flow. High-fit customers with temporary pressure may respond to pause, downgrade, or plan-fit options; low-fit or chronically low-usage users should be able to cancel cleanly and return later through a clear path back.

Keep the quality bar tight:

- Track a consistent event chain: cancellation initiated, offer shown, offer accepted, canceled, reactivated.

- Evaluate outcomes with NRR so you measure retention and expansion from the existing base, not just headline saves.

- Pair NRR with Reactivation Rate using the operational test that matters: did the saved customer pay at least one invoice afterward?

Use vendor save benchmarks as directional context, not a decision rule. A reported 17% to 24% save range can inform hypotheses, but your flow only earns rollout if cohort evidence shows better post-save payment behavior and stronger long-term LTV quality.

The practical next step is to run your rollout sequence, validate each branch with cohort evidence, and scale only what improves long-term value quality. For a step-by-step walkthrough, see Freelancer Decisions Under the EU Platform Work Directive.

Frequently Asked Questions

Does easy cancellation really increase LTV?

Sometimes, but not as a universal rule. The safer claim is that lower-friction cancellation can improve the customer experience, while LTV impact is only proven by your own cohort data after the flow change. If you cannot show stronger reactivation rate, cleaner net churn, or better NRR 30 to 90 days later, treat the win as unproven.

What should every cancellation flow include?

At minimum, include a clear path to cancel, concise reason capture, relevant alternatives such as pause or plan fit, immediate confirmation, and a simple path back if the customer returns. One practical check is whether users see final status clearly and receive a confirmation notice. Also instrument final outcomes, not just offer exposure, so finance and product can measure what actually happened.

Which metrics matter most to prove this strategy works?

Do not stop at save rate. Pair top-line retention with quality metrics: reactivation rate, net churn, Net Revenue Retention, and margin impact from discounts or credits. The best checkpoint is whether saved customers "pay at least one invoice after being saved," because post-save revenue behavior is the quality signal, not headline acceptance.

How do we balance compliance and retention goals?

Treat compliance as the floor, not the optimization target. FTC attention on negative-option practices is still active in 2026, with more than 100,000 complaints in the past five years. The prior rule text was recodified effective February 12, 2026, and further amendments are open for comment through April 13, 2026. For operators, that means you should get legal sign-off on the flow, then compete on transparency, relevant offers, and clean confirmation instead of hidden friction. If you want the current regulatory context in more detail, see Click-to-Cancel After the FTC Rule: Why Easy Cancellation UX Still Matters for Subscription Platforms.

When should we show a pause offer versus letting users cancel?

Use pause when the reason points to temporary constraints such as budget pressure, subscription fatigue, or shifting priorities, especially for otherwise engaged users. Let users who do not want an alternative exit immediately with a clean cancellation path. A simple rule is: temporary constraint, offer pause; otherwise, allow a clear cancel experience.

What is the biggest mistake teams make?

They optimize short-term save rate and ignore whether those saves create long-term value. That is how this turns into a vanity-metric exercise instead of a sound retention decision. Require an evidence pack for each release with the hypothesis, cohort window, and stop or go threshold, or you will end up defending discounts that never improved NRR or reactivation quality.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- content.leg.colorado.gov/sites/default/files/documents/2025A/bills/20...trusted

- digitalcommons.bryant.edu/mark_jou/195trusted

- europa.eu/youreurope/citizens/consumers/shopping/retur...trusted

- federalregister.gov/documents/2024/11/15/2024-25534/negative-opt...trusted

- federalregister.gov/documents/2026/03/13/2026-04952/rule-concern...trusted

- ftc.gov/news-events/news/press-releases/2024/10/fede...trusted

- ftc.gov/news-events/news/press-releases/2026/03/ftc-...trusted

- govinfo.gov/content/pkg/FR-2026-02-12/pdf/2026-02866.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Click-to-Cancel Subscription UX After the FTC Rule for Platforms

If you run recurring billing, your cancellation path is no longer a design side project. It is a revenue decision with legal exposure attached, so product, finance, and legal need to treat it as part of how the business operates.

How to Use a Community to Reduce Churn and Increase LTV

If you run community as an engagement channel, you can rack up activity and still miss churn. Run it as a retention loop instead: detect risk early, intervene by segment, and verify whether the action changed retention outcomes. That is how community starts affecting churn.

Bad Payouts Are Costing Your Supply in Two-Sided Platforms

Payout issues are not just an accounts payable cleanup task if you run a two-sided marketplace. They shape supply-side trust, repeat participation, and fill reliability. They can also blur the revenue and margin signals teams rely on.