Quick Answer

Choose SCF when preserving cash to invoice maturity matters most, and choose Dynamic Discounting when you can deploy internal cash for timing-based discounts. For a dynamic discounting vs supply chain finance platform decision, test by supplier cohort instead of setting one default. Confirm who funds early payment, whether the payable stays due to maturity, and how DPO and contribution margin move after real participation and exception handling.

How each model affects cash timing and margin#

When you compare Dynamic Discounting and supply chain finance for a platform, the real question is funding mechanics, not whether suppliers can get paid faster. Both models can accelerate payment and support cash flow, but they do it in different ways, with different effects on cash deployment, working-capital posture, and economics.

This decision cuts across treasury, product, and go-to-market. You are not just choosing an early-pay feature. You are deciding how the value is funded, where the value is captured, and how much flexibility you keep as the program grows.

The split is straightforward. Dynamic Discounting is a buyer-led model where suppliers can receive early payment at a timing-based discount, funded by the buyer's own cash. Supply Chain Finance, also called payables finance or reverse factoring, is also buyer-led. Suppliers access financing, typically through a third-party-funded program, while the buyer payable remains due at maturity.

That creates the core tradeoff. Dynamic Discounting can improve buyer profitability through COGS reduction, but it uses internal cash for early payment. In SCF, buyers can preserve payment timing to maturity and may improve working-capital posture by paying later, while suppliers still get faster access to cash.

Problems start when teams treat the two models as interchangeable. Before you commit, pressure-test the funding path behind the supplier promise and the operating model behind approvals, payment timing, and reconciliation.

Use three checks up front:

- Confirm who funds acceleration in your target model and whether it fits your current cash position.

- Confirm whether the buyer payable stays outstanding to due date or is settled early from buyer funds.

- Confirm which delivery mechanics fit your operating context, since the broad goal is similar but not delivered the same way.

There is no universal winner. The right choice depends on your operating context. This guide gives you a direct comparison, scenario-based decision rules, and an implementation checklist to help you choose Dynamic Discounting, SCF, or a hybrid approach with fewer execution surprises.

Related: Two-Sided Marketplace Dynamics: How Platform Supply and Demand Affect Payout Strategy.

At-a-glance comparison for platform operators#

Start with the funding path. Use Dynamic Discounting when you can fund early payment from your own cash and want to capture early-payment economics. Use SCF when preserving buyer cash to maturity matters more.

| Criteria | Dynamic Discounting | Supply Chain Finance / Reverse Factoring |

|---|---|---|

| Funding source | Buyer funds early payment with its own cash. | Suppliers access funding from banks, funds, or other financiers in a buyer-led program. |

| Cash impact on buyer | Buyer cash leaves before the original due date when early settlement is approved. | Buyer cash outflow stays at invoice maturity, or another agreed due date, and is paid to the finance provider. |

| DPO effect | Can pull payment earlier than contractual maturity because settlement happens before due date. | Payable remains due to due date, so timing is closer to original maturity. |

| Margin mechanics | Buyer captures variable early-payment discounts tied to how early settlement happens. | Economics center on financing cost, typically aligned with buyer credit risk. |

| Who carries the funding risk | Buyer balance sheet and cash position. | Third-party capital funds supplier acceleration; buyer still owes at maturity. |

| Who captures economics | Buyer captures early-payment discounts when suppliers opt in. | Economics include a financing cost typically aligned with buyer credit risk; buyer benefit is usually cash preservation and payable timing. |

| Implementation burden | Supplier opt-in flow, discount-term setup, and payable extinguishment handling after early settlement. | Provider coordination, supplier participation, maturity-date payment to provider, and reporting visibility. |

| Best fit signals | Buyer has available cash and wants to deploy it for early-payment discounts. | Buyer prioritizes preserving cash to maturity while enabling supplier liquidity through external providers. |

| What to verify before signing | Supplier opt-in flow, discount-term logic, payable treatment after early settlement, and reporting outputs. | Contract terms and conditions, maturity payment path, supplier participation readiness, and reporting depth, including liability position, due-date ranges, and liquidity-risk visibility. |

The biggest misunderstanding is where the funding risk sits. In Dynamic Discounting, early payment is funded by the buyer and the payable is extinguished at payment. In SCF, suppliers can be paid early by a provider while the buyer obligation stays due at maturity.

Read DPO carefully instead of assuming the answer. DPO is the average days to pay accounts payable, often tracked as (Average Accounts Payable / Cost of Goods Sold) x Number of Days in Accounting Period. Dynamic Discounting can pull timing earlier, while SCF more often keeps due-date timing intact, but neither effect is automatic in every setup.

Commercial terms are only part of diligence. You also need to review the reporting outputs. For supplier-finance diligence, verify terms and conditions, where liabilities sit on the balance sheet, ranges of payment due dates, and liquidity-risk visibility.

Participation risk matters too. Dynamic discounting is optional for sellers, so supplier invitation flow and acceptance behavior can determine whether projected economics show up in practice.

The model difference that actually matters#

The difference that matters is funding control, not the shared promise of faster cash access. With Dynamic Discounting, you fund early invoice payments from your own balance sheet and take variable early-payment discounts based on how early you settle versus the original due date.

With SCF, suppliers receive early invoice payments from third-party capital. Your payable remains due until maturity, or another agreed due date, and is then paid to the finance provider.

That changes the operating tradeoff in a very practical way:

- With Dynamic Discounting, you control cash deployment, timing, and discount mechanics, but you use your own cash earlier.

- With SCF, you can preserve cash until the agreed due date and supplier financing is typically linked to your credit risk, but you add provider dependency.

So it is not enough to say both improve cash flow. You still need to decide who funds the acceleration, who controls settlement timing, and which cost-of-capital path and dependency risk you are willing to carry.

Get the settlement path in writing before you sign. For SCF, verify that the payable stays outstanding to due date and that payment goes to the provider at maturity or another agreed date. For Dynamic Discounting, verify that the discount is truly timing-based against the original due date, not a fixed early-pay fee.

A key SCF red flag is provider withdrawal risk. If the financial institution exits the arrangement, your ability to settle liabilities when due can be affected.

Where each model changes margin economics#

For margin decisions, treat SCF mainly as a cash-flow lever and Dynamic Discounting mainly as a yield or profitability lever. Both can support monetization, but they affect net economics through different paths.

SCF lets suppliers get paid early without immediate buyer cash outflow, and the buyer repays at maturity to the finance provider. Dynamic Discounting is usually funded with your own cash, and the economics vary invoice by invoice based on how early each payment is made.

| Economic lens | SCF | Dynamic Discounting |

|---|---|---|

| Monetization path | Usually indirect unless you explicitly price the program | More direct through captured early-payment discounts |

| Contribution margin | Cash preservation can support operations, while net impact depends on funding/provider costs | Discount capture can improve profitability when it lowers purchase cost (COGS) |

| Net economics after funding cost | Can be stronger when third-party funding is competitive versus deploying internal cash | Can be stronger when excess internal cash is available for early-payment discounts |

| Working capital | Preserves near-term cash and can support extended DPO | Uses internal working capital earlier |

| Key risk | Provider dependency and potential cash pressure if funding is withdrawn | Consumes internal cash capacity and requires liquidity discipline |

Do not set one platform-wide default too early. Make the decision at cohort level and compare your internal cash posture with the all-in external funding path; fit can vary by supplier cohort.

Run a simple sensitivity check before you commit:

- Supplier spend visibility: confirm where the payable base sits.

- Invoice volume visibility: confirm where payment activity is concentrated.

- Payment-term visibility and discount timing: realized yield changes with invoice-level payment timing.

The tradeoff is simple even when the modeling is not. SCF can protect near-term cash but adds provider dependency. Dynamic Discounting can improve yield but consumes internal cash capacity.

Choose by supplier cohort and invoice profile#

Do not force one funding model across your entire supplier base. Segment first, then route by how each cohort actually behaves. Payables finance is buyer-led and supplier participation is optional, while Dynamic Discounting lets suppliers select individual invoices for early payment.

A practical starting split is strategic suppliers, long-tail suppliers, seasonal vendors, and high-variance invoice cohorts. Use those groups to test participation mechanics and execution reliability, not to assume one model is always best for each group.

| Cohort | What to check first | Better first test | Why |

|---|---|---|---|

| Strategic or top-spend suppliers | Recurring approved invoices and clean settlement at maturity | SCF (payables finance) | Traditional bank-funded SCF is often targeted to a concentrated top-supplier group, for example top 50-100 suppliers |

| Long-tail suppliers | Payment terms, payment method, payment currency, and low-touch targeting | Dynamic discounting campaign | Dynamic discounting campaigns can be segmented by terms, method, and currency, and suppliers can choose invoice by invoice |

| Seasonal vendors | Whether approval, confirmation, and settlement flow stays stable for this cohort | Separate test cohort | No single funding route is always ideal; validate behavior before broad rollout |

| High-variance invoice cohorts | Inconsistent confirmation and settlement flow | Hold out until process quality is stable | Supplier-finance disclosures highlight buyer confirmation, early payment, and maturity settlement as key checkpoints |

The long tail needs explicit design. In many supplier bases, 80% of suppliers represent about 20% of spend, so a manual operating model built for the top 10-20% can be hard to scale across everyone else.

Use one guardrail across all cohorts: do not flatten supplier behavior into a single adoption assumption. In payables finance, suppliers independently decide whether to use the program. In Dynamic Discounting, they can opt in at the invoice level. Participation will vary by cohort and invoice class.

Before you route a cohort, validate a short evidence pack on real invoices. Check:

- approval-to-confirmation reliability

- supplier participation signals, based on actual or pilot behavior rather than platform-wide assumptions

- settlement reliability at maturity

- average payment term for participating suppliers, since longer terms can increase Dynamic Discounting acceptance

If you need a clean rollout path, start with one concentrated, operationally clean cohort for SCF and one tightly targeted invoice campaign for Dynamic Discounting. Expand only after participation and settlement behavior match your model.

Use hybrid routing when one model is not enough#

Use hybrid routing when cash constraints and due-date mechanics vary across invoice lanes. Treat flexible funding as operating logic. For each approved invoice lane, route to SCF or Dynamic Discounting based on current cash position, payable timing, and invoice-level rules.

Hybrid routing works because the two lanes behave differently after early payment. In Dynamic Discounting, you use your own cash for early payment, and the payable is extinguished when you pay early. In SCF, a bank, fund, or other financier pays the supplier early, while your payable stays due until maturity. That difference is a key input for DPO and cash planning.

Route by constraint first#

Start with the constraint you are actually trying to manage. If cash is tight, shift eligible lanes to SCF. If you have surplus cash, expand Dynamic Discounting where supplier participation and invoice approvals are already reliable. GSCFF guidance supports switching between self-funded discounting and third-party payables finance based on buyer cash position, and flexible models can run both at the same time.

| Situation | Better lane | Why | Verify before routing |

|---|---|---|---|

| Cash-tight month | SCF | Supplier gets early payment without immediate buyer cash outflow; payable remains due to maturity | Invoice is approved, supplier is eligible, maturity date is clear |

| Surplus-cash period | Dynamic Discounting | Buyer deploys own funds for early payment, including excess cash | Cash cap is set, payment schedule is open, no blocked days prevent early payment |

| Mixed supplier base in one period | Hybrid by invoice lane | No need to force one funding route across all invoice classes | Invoice-level rules can be applied to selected invoices |

Keep the order of operations boring#

Once you decide to run both, keep the operating sequence simple and explicit:

| Step | What to do |

|---|---|

| Evaluate Eligibility Rules | Check approval status, supplier participation, and lane compatibility at invoice level |

| Score the funding option | Compare available cash with the need to keep payables due to maturity; include DPO and cash effects |

| Assign the lane | Route each invoice class to SCF or Dynamic Discounting and keep the assignment explicit in payment and reconciliation records |

| Monitor DPO and cash-impact deltas | Track lane-level differences so the payable-timing effect is visible in reporting |

If you cannot explain which rule put an invoice into a lane and what happened after that, the routing logic is still too loose.

Switch at clean checkpoints#

Only move a supplier or invoice class at stable checkpoints, such as after approved invoices have run through early payment and settlement at maturity. Avoid switching based on short-term noise or disputed invoices.

Use repeated operating evidence, not a universal threshold. If a lane consistently meets approval, scheduling, and settlement expectations, move it into self-funded discounting during surplus-cash periods. If cash tightens, move it back to SCF. Keep the supplier experience stable and keep lane assignment explicit in your invoice payment records.

Product and data prerequisites before launch#

Do not launch either lane until you can prove invoice state, acceptance, discount terms, and reconciliation mapping at invoice level.

Start with records both lanes can defend#

Use one shared model for approved invoices, then track lane-specific payment behavior explicitly in the records below.

| Required object | Dynamic Discounting | SCF / Payables Finance | Launch check |

|---|---|---|---|

| Invoice state | Approved invoice triggers early payment eligibility | Approved invoice triggers eligibility, but buyer payable remains due at maturity | Status transitions are explicit, not inferred |

| Acceptance event | Supplier acceptance of early payment terms is recorded | Supplier participation and financing acceptance are recorded | You can show who accepted, when, and for which invoice |

| Discount terms | Store discount date and discount amount per invoice | Keep financing or discount terms linked at invoice level | Terms are not only stored at supplier level |

| Reconciliation mapping | Early payment and accounting outcome map to the invoice | Financier early payment and buyer maturity payment both map to the same invoice | Payment and discount entries reconcile to reporting outputs |

| Settlement evidence | Execution timestamp and paid amount | Financier payment event plus buyer due-date settlement | You can trace invoice-level request, payment, and due-state outcomes without spreadsheet patchwork |

Run one invoice end to end before launch. If you cannot show approved state, acceptance, discount terms, payment event, and accounting output in one trace, month-end risk is still high.

Build retry-safe integrations, not just listeners#

Money movement and state changes will not stay clean unless the plumbing is built for retries and asynchronous events. Use APIs and webhooks for changes such as acceptance, initiation, delivery, and settlement. For webhook-based updates, support POST, use HTTPS when public, acknowledge with 2xx, store the event, then process it durably.

| Control | Article guidance | Reason |

|---|---|---|

| Change events | Use APIs and webhooks for changes such as acceptance, initiation, delivery, and settlement | Money movement and state changes will not stay clean unless the plumbing is built for retries and asynchronous events |

| Webhook handling | Support POST, use HTTPS when public, acknowledge with 2xx, store the event, then process it durably | Providers can retry events for days |

| Idempotency | Make money and state transitions idempotent | Duplicate-safe handling is required to avoid duplicate settlement or discount recognition |

| Audit trail | Answer four questions clearly: what was requested, what was accepted, what was paid, and what remains due | The audit trail does not need one universal schema, but it should answer those questions clearly |

Make money and state transitions idempotent. Providers can retry events for days, so duplicate-safe handling is required to avoid duplicate settlement or discount recognition. Your audit trail does not need one universal schema, but it should answer four questions clearly: what was requested, what was accepted, what was paid, and what remains due.

Treat finance controls as launch gates#

Treat approval gates, exception queues, and month-end reconciliation outputs as launch prerequisites, not cleanup work. Exception handling needs to be visible enough that finance can resolve posting blockers in system instead of reconciling around the product.

Tie outputs to Working Capital review with lane-level visibility. At minimum, you should be able to explain:

- DPO impact, using a consistent DPO calculation approach.

- Cash-flow impact by lane.

- Failure handling and unresolved exceptions.

Also confirm that reporting can separate buyer-funded early payment from third-party-funded payables finance, so disclosure and liquidity-risk reporting remain defensible. If product and finance operations cannot explain those lane outcomes clearly, keep the rollout in pilot.

You might also find this useful: Supply Chain Finance for Marketplaces: How Early Payment Programs Can Attract and Retain Sellers.

Vendor diligence questions that change outcomes#

This is where outcome risk concentrates. If a provider cannot clearly show who gets paid, when cash moves, and how outputs map to your finance disclosures, pause the contract.

| Diligence point | Dynamic Discounting | SCF / Payables Finance | What to verify |

|---|---|---|---|

| Funding source | Buyer funds early payment with its own cash | Third party funds supplier early payment | Contract language matches the real cash path |

| Fee economics | Economics are reflected in supplier discount terms and buyer cash usage | Economics can include financing spread plus provider/platform fee layers | Get a full fee waterfall, not only a headline rate |

| Settlement path | Early payment is made from buyer cash | Buyer typically pays at maturity into the finance provider's remit-to account | Trace one invoice from approval to maturity settlement |

| Operating model control | Buyer-led program design and offer structure | External finance provider and platform involvement are typical | Confirm who can change pricing logic, terms, and exceptions |

| Reporting duty | Treasury cash usage and discount outcomes are central | Outstanding confirmed amounts, terms, and liquidity-risk transparency are central | Request sample monthly and quarterly outputs before signing |

Ask the contract-critical questions early: payment timing logic and whether any assets or guarantees are pledged as security. For SCF, confirm that maturity payment goes to the provider account and that the buyer obligation remains due at maturity. For Dynamic Discounting, test treasury controls more deeply because the buyer is using its own funds.

Use the same discipline on economics definitions. Do not accept Cost of Capital as a label on its own. Ask how the program calculates it, where spread is captured, which fees are inside or outside the quoted rate, and which setup, legal, reporting, or operational charges are excluded.

If you report under US GAAP or IFRS, require disclosure-grade reporting support during diligence. FASB's ASU 2022-04 (September 29, 2022) and IASB's supplier-finance disclosure updates (issued 25 May 2023, effective for annual periods beginning on or after 1 January 2024) both increase focus on terms, payment timing, outstanding confirmed amounts, and liquidity-risk transparency. Ask for a sample rollforward, balance-sheet mapping, and interim outstanding amount output before contract execution.

For a step-by-step walkthrough, see Real-Time Reporting Metrics Platform Finance Teams Can Actually Control.

Failure modes to catch in the first 90 days#

In the first 90 days, do not judge success by launch optics alone. The fastest signals are adoption friction, cash-use exposure, and provider dependency.

Adoption breakdowns differ by funding model#

The failure mode is different in each model, so monitor them differently from day one.

In Dynamic Discounting, supplier participation is optional, so low uptake is a core risk to catch early. If invitations are high but accepted early-payment offers stay low, review the offer design and enrollment flow before you scale volume.

In SCF, onboarding friction is a documented failure mode. In one DBS supplier-finance webinar, 55% of attendees said onboarding was a significant barrier and 41% said it could be better. ICC also highlights supplier onboarding as the largest challenge, with legal-structure negotiation slowing implementation. A practical fix reported in that DBS case was simplifying onboarding documentation and data extraction, which cut onboarding time to three days.

Track the onboarding funnel directly: invited, started onboarding, approved, first early payment. Where suppliers stall is where the rollout is actually breaking.

Execution drift can hide behind volume growth#

Funded volume can look healthy while rollout friction builds underneath it. Track volume alongside onboarding conversion and exception trends so execution issues are visible early.

Treat eligibility and process settings as control levers to test early. If a cohort repeatedly generates holds, disputes, or manual intervention, fix that lane before adding more volume.

Treasury risk and dependency risk are different, but both need early controls#

These risks do not show up the same way, so they need different controls. Dynamic Discounting is buyer-funded, so higher uptake means greater use of your own cash.

| Cadence | What to review |

|---|---|

| By cohort | invitations, onboarding progress, first-use, and repeat-use |

| By lane | dispute or exception trendline and fallback-payment readiness |

| Periodically | how the company would be affected if supplier-finance arrangements were no longer available |

SCF, including reverse factoring, shifts early payment to a financial institution, which introduces dependency risk if that provider becomes unavailable. IFRS has explicitly framed this risk: if the institution withdraws the arrangement, the entity's ability to settle liabilities when due can be affected.

Supplier-finance disclosure updates issued on 25 May 2023 and applied in the EU for financial years starting on or after 1 January 2024 also require companies to assess how they would be affected if arrangements were no longer available.

If one lane starts degrading, do not force growth through it. Reduce exposure, fix the bottleneck, and keep a fallback path for approved invoices. Related reading: ARR vs MRR for Your Platform's Fundraising Story.

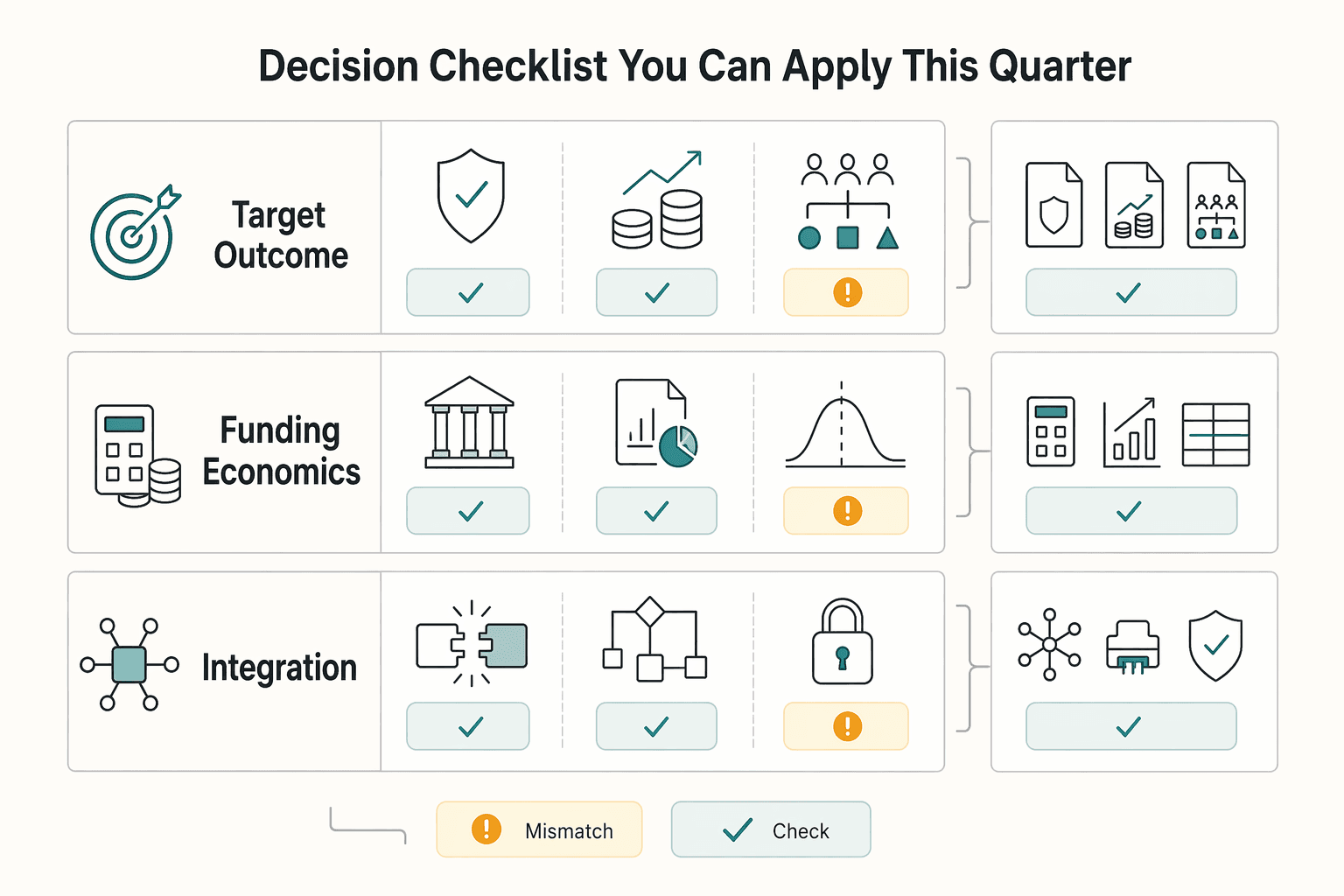

Decision checklist you can apply this quarter#

Start with the outcome you need this quarter, then validate execution risk before launch. If the priority is working-capital protection and DPO optimization, SCF is usually the better starting point. If you have excess cash and want to capture discounts directly with buyer-funded early payment, Dynamic Discounting is usually the better starting point. If goals differ by supplier cohort, use a hybrid design instead of forcing one model.

| Decision lens | What to score now | Direction it usually supports |

|---|---|---|

| Target outcome | DPO optimization, working-capital protection, or a balanced mix | DPO and cash protection tend to favor SCF; discount yield on buyer cash tends to favor Dynamic Discounting; mixed goals tend to favor hybrid routing |

| Funding and economics | How discount or financing economics flow into your program | Buyer-funded discount capture aligns with Dynamic Discounting; third-party funding with buyer payment still due at original maturity aligns with SCF |

| Working-capital posture | Treasury capacity to fund early payments through payout-heavy periods | Tight cash tends to favor SCF; surplus cash can support Dynamic Discounting; uneven cash capacity often supports cohort-based hybrid routing |

Before you launch, define a clear internal gate across finance, product, and operations. Finance should confirm cohort economics, including discount capture, effective APR for buyer-funded lanes, DPO impact, and provider costs where relevant. Product should confirm ERP integration, onboarding flow, and transaction transparency. Operations should confirm the controls needed to run the lanes consistently.

Set the first-quarter scorecard in writing before go live. Track adoption by cohort and lane-level performance. For buyer-funded lanes, include discounts captured and effective APR. For SCF lanes, include onboarding completion and payment-term impact. If the proposal cannot show assumptions, cash-use view, integration dependencies, and a fallback path, pause approval until that is complete.

Before choosing a lane, model your own adoption and discount assumptions with the pricing calculator.

Conclusion#

Choose the model based on net economics, operating effort, and control requirements, not the headline.

Dynamic Discounting uses buyer cash for early payment in exchange for a variable discount, so it fits when you have excess cash and enough discount capture. Payables finance lets suppliers access financing on approved receivables, typically priced to buyer credit risk, while the buyer payable remains due at maturity, which may preserve near-term cash flexibility.

Start narrower than your ambition. Pick one high-confidence cohort, validate the economics, and validate the controls before you scale. If you cannot clearly show when payment is triggered, who funds it, and how exceptions are handled, you are not ready to expand either model.

Before rollout, confirm three things with evidence and keep the proof together:

- Economics: net discount capture or funding cost after fees, settlement work, and exception handling.

- Controls: a clear audit trail from invoice approval to early payment to final settlement, with clear dispute and reconciliation ownership.

- Reporting readiness: if supplier finance arrangement disclosure is in scope, make sure your data supports it. IASB amendments issued in May 2023 apply for annual reporting periods beginning on or after 1 January 2024, and US teams should review FASB ASU 2022-04 from September 2022.

Once one lane is stable, a hybrid approach may be appropriate. Run Dynamic Discounting and SCF side by side only with explicit eligibility and routing rules, and switch cohorts based on cash position, economics, and execution reliability.

Align finance, product, and operations on the decision checklist, then move into vendor diligence and pilot design focused on net economics, operational proof, and reporting readiness. If you want a practical read on controls, payout operations, and integration scope for your rollout, talk to Gruv.

Frequently Asked Questions

What is the practical difference between Dynamic Discounting and SCF for a platform?

The practical difference is who funds early payment and when you release cash. Dynamic Discounting is buyer-led and funded with your own cash, and the discount typically increases when payment happens earlier. SCF, also called payables finance or reverse factoring, is also buyer-led, but supplier early payment is funded by a third party and you typically pay at maturity.

Which model is better if our platform has limited cash on the Balance Sheet?

If your balance sheet is tight, SCF is often the better starting point. It allows early supplier payment without requiring you to deploy your own cash immediately, and it is often used to support working-capital goals, including DPO extension. Before launch, confirm that your agreement preserves the payment timing you expect.

Can we run Flexible Funding with both Dynamic Discounting and Supply Chain Finance at the same time?

Yes. Flexible Funding can mean switching between the two models or running both at the same time.

When should we switch an invoice cohort from SCF to Dynamic Discounting?

There is no universal numeric trigger. Move a cohort when you have enough internal cash for the period and the expected discount capture justifies moving from third-party funding to buyer-funded early payment.

How does each option affect Days Payable Outstanding and Contribution Margin?

DPO is the average number of days it takes to pay accounts payable. SCF can support longer DPO because suppliers may be paid by a finance provider while your payable remains due at the agreed maturity date, though outcomes depend on program design and execution. Dynamic Discounting uses buyer cash earlier, so it may not extend DPO in the same way, but discount capture can improve profitability, including through lower cost of goods sold.

What contract terms matter most before we launch an Early Payment Solution?

Start with the key program terms: payment terms, any guarantees, who funds early payment, and how due dates work in practice. If supplier-finance disclosure is in scope, make sure reporting can cover due-date ranges and liquidity-risk information; IFRS amendments apply for annual periods beginning on or after 1 January 2024, and US teams should review FASB ASU 2022-04 (September 2022).

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 6 external sources outside the trusted-domain allowlist.

- bsaaml.ffiec.gov/manual/RisksAssociatedWithMoneyLaunderingAnd...trusted

- eur-lex.europa.eu/eli/reg/2024/1317/oj/engtrusted

- fasb.org/page/getarticleexternal

- iccwbo.org/news-publications/guests-blog-speeches/suppl...external

- ifc.org/content/dam/ifc/doclink/2023/supply-chain-sm...external

- ifc.org/en/interviews/2025/scaling-up-supply-chain-f...external

- ifrs.org/news-and-events/news/2023/05/iasb-increases-...external

- ifrs.org/content/dam/ifrs/project/supplier-finance-ar...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

What Is Reverse Factoring? How Supply Chain Finance Lets Platforms Pay Contractors Early at Low Cost

The core decision is not what you call the model. It is whether you can run a buyer-led financing program on invoices the buyer has confirmed as valid, with approval controls a finance provider can rely on.

How Supply and Demand Dynamics Should Set Your Marketplace Payout Strategy

In a two-sided marketplace, payout strategy is not back-office plumbing. It can shape whether sellers stay active, whether transactions complete reliably, and whether buyers can find supply that is ready to transact.

Supply Chain Finance for Marketplaces: How Early Payment Programs Can Attract and Retain Sellers

Treat an Early Payment Program as both a funding decision and a payout-control decision. In a marketplace, it can shape seller experience, payout reliability, exception volume, and who carries cash and credit exposure when payment happens before standard terms.