Quick Answer

Use days payable outstanding dpo marketplace working capital as a constrained operating decision, not a blanket instruction to delay payments. Start with a stable DPO formula, then split payables by type so seller obligations are not mixed with discretionary vendor AP timing. Approve cadence changes only when settlement, compliance, and dispute status are explicit, and confirm movement in posted Ledger Journals. Keep the change only if cash retention improves without increasing payout exceptions or unresolved items.

Why DPO Works Differently in Marketplaces#

Use Days Payable Outstanding as a timing tool, not a blanket instruction to pay later. You only get a real working-capital benefit if you can hold cash longer without creating operational problems.

DPO measures the average number of days it takes a company to pay invoices and bills. It is a working capital ratio, usually measured on a quarterly or annual basis. That makes it useful for finance, but easy to misuse when teams assume every payable can be delayed the same way.

That difference matters because the cash argument is real. Holding cash longer can improve your working-capital position on paper. But slower payment timing does not automatically produce a better outcome. The treasury upside matters only if payment operations stay reliable and delays are clearly understood.

So this is not a generic finance refresher on formulas. The useful questions are operational. Which obligations can absorb timing changes? Which ones should be treated as protected flows? What has to be true before you hold cash longer?

If you change payment cadence, you should be able to verify the result in the records that actually matter. That includes accounting and payment records showing obligations were processed as intended.

A common failure mode is reporting a cleaner DPO number while the operation underneath gets messier. You retain more cash, but you also create more exceptions or unresolved items. That is why this article stays focused on control points, ownership, and checkpoints you can test, not abstract definitions.

One expectation up front: this guide does not rely on a universal benchmark range. If you are looking for a single "good DPO" number, treat it cautiously and set targets from your model, your payment commitments, and your operating reality.

What to prepare before changing payout timing#

Before you change payout timing, build a single view of where delays happen now and who owns each delay. Focus on your own operating records so decisions reflect your actual cash-flow lag.

Step 1. Build one repeatable evidence pack across recent closes#

Use the same evidence pack for each recent close and review the periods side by side to spot timing patterns, not just ending balances. This matters because payout delays are often tied to payout schedules, reserve policies, and upfront costs, and those delays can create real financial strain.

Verification point: trace a small sample of delayed payouts from obligation to release state. If teams cannot agree on the current state for the same payout, fix visibility before you change cadence.

Step 2. Define which records settle disagreements#

Agree in advance which records answer three questions: when an obligation is recognized, what state a payout is in, and what management reporting summarizes. If summary reporting looks cleaner while unresolved payout exceptions remain, treat that as a control gap, not a working-capital improvement.

Step 3. Separate hold queues from timing decisions#

Map policy and operational hold queues in your flow, and assign clear owners before any cadence change. Keep hold-driven delays separate from payout-timing performance so you can see whether timing mismatches are growing. Persistent cash gaps are often bridged with borrowing, so this separation is a practical risk control.

If you are evaluating financing options alongside payout timing, Embedded Working Capital for Platforms: Invoice Financing Factoring and Cash Advance Compared compares the main models.

Build a DPO baseline that reflects marketplace reality#

Build a baseline you can audit month after month. Until a DPO change ties back to posted Ledger Journals and closed breaks, treat it as noise.

Step 1. Calculate the core measure and freeze the rules#

Start with one formula and keep it stable across periods:

DPO = (Average Accounts Payable / Cost of Goods Sold (COGS)) × days in period

Then lock the definitions behind it: what is included in payables, what is excluded, how period length is set, and which policy-driven holds are tracked outside DPO. Use monthly cuts, not occasional snapshots.

For a defensible baseline, use clean, segmented historical data and keep at least two years when available. If your history is shorter, still baseline it, but label it lower confidence and avoid setting aggressive timing policy from that series.

Verification point: for any month with a material move, prove whether payment timing changed or reporting logic changed. If it is reporting logic, reset the baseline.

Step 2. Segment the baseline by payable type and pair it with companion metrics#

A single blended DPO number is not enough for operating decisions. Maintain a monthly table by payable type, then track companion signals next to each type.

| Payable type | What belongs in the monthly baseline | Companion signals to track | Minimum evidence source |

|---|---|---|---|

| Vendor AP | Supplier and platform vendor payables booked as AP | Accounts Payable Turnover Ratio, late-settlement incidents where relevant | Posted Ledger Journals, closed matching items |

| Partner payouts | Amounts owed to commercial partners under payout terms | Failed Payout Batches, late-settlement incidents | Posted Ledger Journals, payout status logs, closed matching items |

| Seller obligations | Amounts owed to sellers under published payout timing | Failed Payout Batches, late-settlement incidents, exception counts | Posted Ledger Journals, payout status logs, closed matching items |

| Merchant of Record (MoR) obligations | MoR-related obligations treated as payable obligations in reporting | Failed Payout Batches, settlement delay counts, exception aging | Posted Ledger Journals, settlement records, closed matching items |

If two payable types behave differently in operations, do not collapse them into one control number.

Step 3. Verify movement before you call it progress#

Call improvement only after you can trace each DPO movement to posted Ledger Journals and closed matching items. That check filters out gains caused by stale exceptions, reclassification, or unresolved payout backlog.

Also avoid over-reading a single strong month. In a 2012-2016 analysis of 147 retailers, 54 percent improved working capital for only one year, which is a useful caution that short-term improvement may not hold.

For a payments-focused view of DPO controls, see Days Payable Outstanding (DPO): How Payment Platforms Help Finance Teams Optimize Cash Flow.

Segment obligations before you optimize terms#

Do not optimize terms from one blended payable pool. Segment obligations first so DPO changes reflect real payable decisions, not mixed operational effects.

Step 1. Separate obligations by reversibility, not just by account code#

Start with buckets that behave differently: supplier invoices, platform service vendors, contractual seller payouts, and review-gated disbursements. Use one rule for classification: can this payment-timing choice be reversed cleanly in the next cycle without breaking a contract or process commitment?

| Obligation | Lane | Operational note |

|---|---|---|

| Supplier invoices | Primary term-optimization lane | Optimize where timing is actually discretionary |

| Platform service vendors | Primary term-optimization lane | Optimize where timing is actually discretionary |

| Contractual seller payouts | Protected lane | Defined by your own commitments and controls |

| Review-gated disbursements | Protected lane | Defined by your own commitments and controls |

Treat supplier and vendor AP as your primary term-optimization lane. Keep seller payouts and review-gated disbursements in protected lanes defined by your commitments and controls, then optimize where timing is actually discretionary.

Verification point: sample items per bucket and confirm mapping against posted Ledger Journals, payout status logs where relevant, and the governing contract or policy note. If one obligation lands in different buckets across reports, fix mapping before you change terms.

Step 2. Use cash-cycle metrics for context, not as a substitute for payout constraints#

Use the cash-cycle view to interpret term changes, then test the result by segment. CCC = DIO + DSO - DPO, where DIO is average days inventory is held, DSO is average days to collect after a sale, and DPO is average days to pay suppliers.

This helps you see whether a DPO move improves the broader cycle or just shifts pressure. If improvement cannot be tied to supplier or vendor segments, do not treat it as clean AP progress.

Step 3. Tag compliance-dependent holds so they are not counted as AP efficiency#

Label compliance-dependent holds separately from treasury-driven payment timing. If your flow includes VAT validation, KYC/KYB, or AML review gates, track them as distinct hold reasons instead of folding them into AP efficiency reporting.

At minimum, keep the hold flag, hold start date, clear date when available, and ledger-posted status. If payable days increase alongside more compliance-held items, optimize in reversible supplier/vendor lanes first.

Related: Accounts Payable Days (DPO) for Platforms: How to Measure and Optimize Your Payment Cycle.

Set payout timing policies with hard decision rules#

Treat payout timing as a policy system, not a case-by-case treasury choice. Use a small set of payout bands with explicit release rules tied to statuses your team can verify: settlement, compliance, and dispute state.

Step 1. Define three payout bands by release confidence#

| Policy band | When to use it | Cash retained | Seller trust risk | Ops workload | Free Cash Flow impact |

|---|---|---|---|---|---|

| Standard cadence | Settlement is confirmed, compliance is clear, no active dispute, and the obligation matches your normal payout promise | Moderate | Low when consistently met | Low to moderate | Steady and predictable |

| Accelerated cadence | Funds are settled and clear, and you have an approved reason to pay earlier than normal | Low | Lowest for affected sellers | Moderate due to added approvals and monitoring | Usually limited for near-term cash retention |

| Exception cadence | An unresolved hold exists (for example, settlement uncertainty, compliance review, or a live dispute) | Highest in the short term while the hold is valid | High if reasons are unclear or delays drift | Highest because the queue needs active ownership | Can help near-term cash position, but may create operational and trust tradeoffs |

Do not optimize this table for maximum delay. In general DPO examples, longer payment timing can look stronger from a cash-flow perspective, but seller-facing obligations carry different trust and operational risk than trade-creditor AP.

Step 2. Write if/then release logic in plain operational language#

DPO is typically calculated on a quarterly or annual basis, but payout decisions happen continuously. Make the decision path explicit so finance, payments ops, and support interpret it the same way.

- If settlement is confirmed, compliance is clear, and there is no unresolved dispute, release on standard cadence.

- If the same item qualifies for an approved early-release reason, move it to accelerated cadence and record approval.

- If any unresolved hold exists, route to exception cadence with a named owner, a hold reason, and an ETA field.

Verification check: sample each band and confirm cadence assignment matches recorded settlement status, compliance flag, dispute state, and release timestamp. Then reconcile the sample to posted Ledger Journals so reported DPO movement is not coming from mislabeled holds.

Step 3. Put contractual and product promises ahead of convenience#

Before rollout, test your payout policy against governing commitments and published promises, then apply treasury goals inside those boundaries. If your configured release logic, seller-facing payout window, and support language do not align, the working-capital benefit is fragile.

Prioritize timing changes where they are more reversible and easier to audit, and treat seller-delay gains against published promises as high-risk until reviewed by the right owners.

For a step-by-step walkthrough, see Working Capital Management for Freelancers Who Invoice Clients.

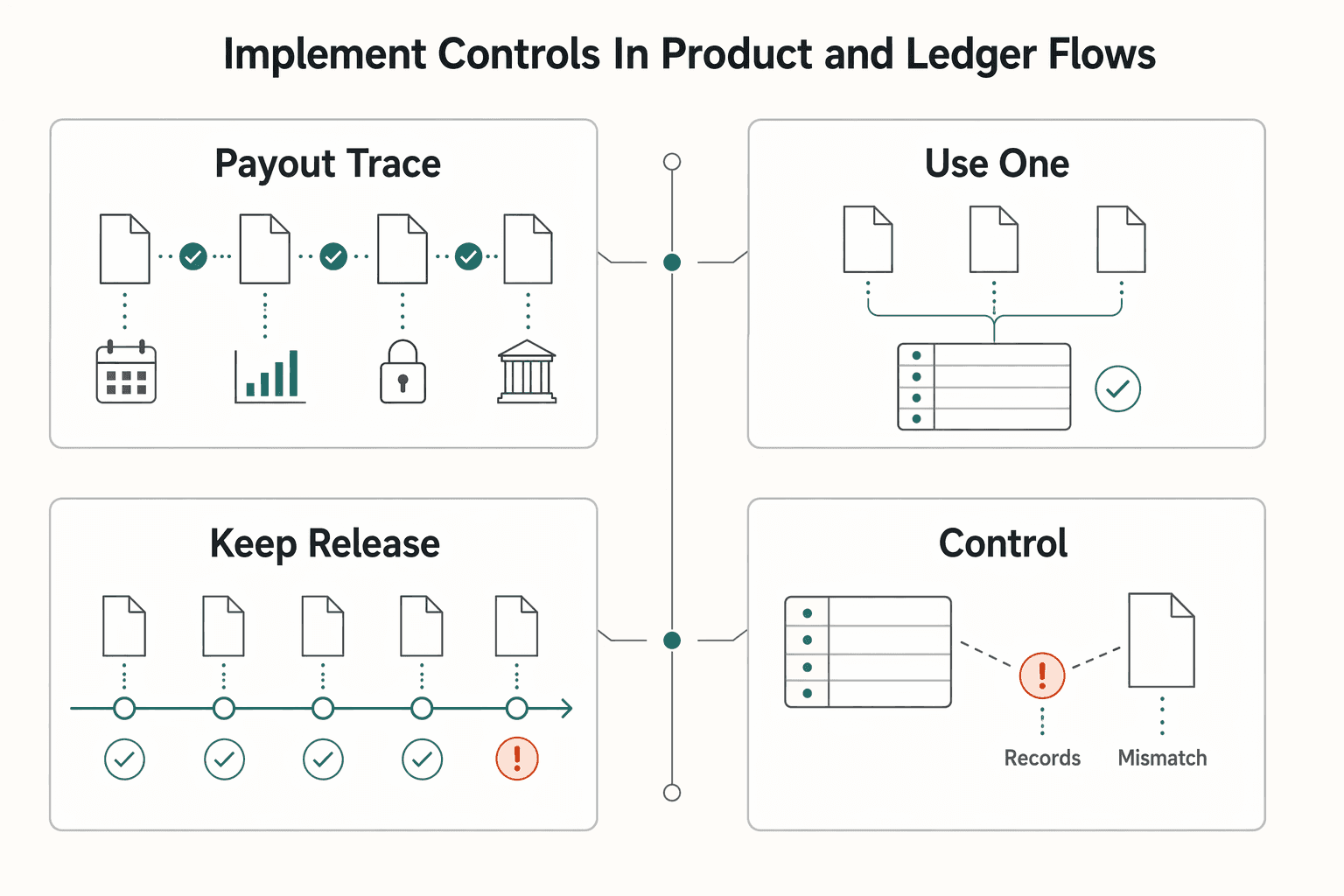

Implement controls in product and ledger flows#

Your controls should make payout timing auditable end to end, so DPO movement reflects a deliberate cash decision rather than AP process noise.

| Control point | Required record or rule | Practical check |

|---|---|---|

| Make each payout action traceable | Stable internal identifier, who or what initiated it, and the resulting status | One clear business outcome, not conflicting attempts |

| Use one internal status path for release decisions | One internal decision flow before release, reporting, and accounting updates are finalized | One consistent trail from status change to release timing and ledger outcome |

| Keep release eligibility explicit | Define the exact release-ready state in policy and enforce it consistently | Do not treat every incoming cash event as automatic release approval |

| Validate controls with regular reconciliation drills | Confirm reconciliation closes from recorded events and posted journals | Not manual after-the-fact fixes |

Step 1. Make each payout action traceable#

Record each payout action with a stable internal identifier, who or what initiated it, and the resulting status. The practical check is simple: when an action is retried in testing, your records should still show one clear business outcome, not conflicting attempts.

Step 2. Use one internal status path for release decisions#

Run payout status changes through one internal decision flow before release, reporting, and accounting updates are finalized. For any sampled payout, finance and ops should be able to follow one consistent trail from status change to release timing and ledger outcome without reconstructing events manually.

Step 3. Keep release eligibility explicit#

Do not treat every incoming cash event as automatic release approval. Define the exact release-ready state in policy and enforce it consistently so payout timing stays aligned with the decision rules set in your payout bands.

Step 4. Validate controls with regular reconciliation drills#

Test controlled payout runs and confirm reconciliation closes from recorded events and posted journals, not manual after-the-fact fixes. Higher DPO can free cash for operations, but an extremely high DPO can also signal payment difficulty, and late payments can damage relationships and add fees.

Monitor red flags and escalate early#

If DPO rises while the AP exception queue grows and seller payouts are delayed, treat it as a control risk until the records prove otherwise. In marketplaces, those delays often come from the interaction of payout schedules, reserve policies, and cash-flow lag, and they can disrupt sellers' day-to-day operations.

Step 1. Track the risky pattern as one signal, not three separate metrics#

Review DPO, exception-queue volume, and delayed payouts together each week. A finance-side gain only counts if payout reliability stays stable. If DPO improves while the other two worsen, you are probably shifting operational risk into working capital instead of improving it.

Step 2. Run weekly control checks that can be verified quickly#

Check unmatched ledger movements, stale payout statuses, and repeated retry storms, even with Idempotency Keys in place. For sampled payouts, confirm the payout state, settlement state, and final ledger journal are consistent. If support sees "processing" while finance sees "released," escalate ownership immediately.

Step 3. Escalate on triggers, not on who argues hardest#

Escalate when reconciliation breaks persist across review cycles, compliance holds repeat for the same payout population, or settlement extends beyond your published payout window. Sellers experience those delays before finance closes the period, so delay in escalation compounds the risk.

| Trigger | Escalate when | Note |

|---|---|---|

| Reconciliation breaks | Persist across review cycles | Delay in escalation compounds the risk |

| Compliance holds | Repeat for the same payout population | Delay in escalation compounds the risk |

| Settlement | Extends beyond your published payout window | Sellers experience those delays before finance closes the period |

Step 4. Keep one shared scorecard for Finance and Ops#

Use one scorecard that includes DPO movement, AP backlog, delayed payout count, and settlement-delay incidents. Review working-capital gains and payout reliability together every cycle. This is the fastest way to catch a paper win before it becomes a seller-trust issue.

If buyer billing and seller payouts need to stay aligned, Recurring Billing for Marketplaces: How to Charge Buyers and Pay Sellers on the Same Cycle covers the operating tradeoffs.

Fix common failure modes without rolling back everything#

When one metric breaks, do not unwind the full change set by default. Restore protected payout segments first, verify the break in Ledger Journals and matching views, then retest AP segments in isolation.

Step 1. Restore protected segments before you touch treasury timing again#

If longer cycles were pushed globally, restore protected payout segments to their prior cadence first. Keep less sensitive AP segments on the new timing so you can test results without mixing failure sources.

Use a simple control: if a flow has a published payout-window commitment, treat it as protected first. If you cannot report outcomes by segment, pause and split the measurement before you make more timing changes.

Step 2. Recalculate the gain against COGS and Ledger Journals#

Treat any DPO gain as provisional until it ties back to COGS scope and posted Ledger Journals. If KPI movement depends on lagging, netted, or manually adjusted reporting views, you do not yet have an operational gain.

Run a sample trace from reported movement to the included payable population, then to posted and closed journals. If the gain disappears after removing manual timing fixes or reclassifications, classify it as reporting-only and rework the metric logic.

Step 3. Separate compliance and tax holds from true payable-cycle time#

Keep compliance hold time and payable-cycle time on separate clocks, with clear processing and suspense states. This avoids counting operational holds as AP-cycle improvement.

Apply the same split to tax-readiness gates where your workflow uses them: W-8, W-9, and downstream Form 1099 status should be tracked separately from payable timing. If payouts sit in a single generic pending state, you lose root-cause visibility.

Step 4. Freeze policy changes until Reconciliation debt is cleared#

If batch changes increase unmatched items or manual fixes, freeze further timing-policy changes until Reconciliation backlog is controlled. Internal controls are only reliable when procedures are documented and responsibilities are clear.

Verify with sampled batches, not trend lines alone: payout status transitions, settlement state, and final Ledger Journals should align, and related items should be closed rather than parked. If backlog keeps rising, fix the break and retest one segment at a time.

Related reading: Accounts Payable Automation ROI for Platforms That Need Defensible Results.

Conclusion#

Treat DPO as a useful cash-outflow metric, not a win by itself. A higher number can free cash for operating needs and short-term investments, but an excessively high DPO can also signal bill-paying strain and supplier relationship risk. Before you broaden any policy change, do one final pass that checks cash benefit and operational risk side by side.

- Document the math before you defend the result.

Confirm your Days Payable Outstanding calculation, including the period used and which obligations sit inside or outside the metric. The check is simple: someone outside Finance should be able to read the note and understand why supplier, vendor, or other payable categories were segmented the way they were. If that explanation is fuzzy, the reported improvement is easy to misread.

- Protect key payment relationships before you optimize anything else.

Identify which supplier/vendor payments are most sensitive to delay and make those guardrails explicit. The failure mode is common: a cash-management change is applied too broadly, then relationship damage appears later as late or disputed payments. If delay creates trust risk, keep that flow protected and look for improvement elsewhere first.

- Test the process points that can make operational issues look like finance gains.

Confirm obligation-to-payment timing is tracked consistently and exceptions are visible early. Your checkpoint is a traceable path from obligation to payment status, without relying on last-minute manual fixes to close the books. If that process is not stable, do not treat the policy as rollout-ready.

- Review one scorecard that shows both upside and risk.

Track the cash case next to payment-risk signals, not in separate meetings with separate owners. At minimum, use one view that compares DPO movement with late-payment exceptions and unresolved items. If DPO improves while exceptions rise, treat that as a red flag.

- Define rollback before rollout.

Write down what would force you to stop or narrow the change, who can make that call, and which payment segments get restored first. This matters because an excessively high DPO can be a sign of bill-paying problems and relationship risk, not stronger discipline. If you cannot state the rollback trigger in one or two sentences, the rollout is still too early.

If you want one simple closeout rule, use this: keep the change only if the cash improvement does not come with bill-paying strain or supplier-risk side effects.

Frequently Asked Questions

What is Days Payable Outstanding (DPO) for a marketplace operator, not just a textbook definition?

DPO measures how many days it takes a company to pay its obligations, but a marketplace operator should treat it as an operating signal, not just a finance ratio. A reported improvement can reflect intentional payment-timing changes or process friction, so the number is most useful when you understand which obligation categories moved.

How do you calculate DPO when payout obligations and supplier AP behave differently?

Start with the standard DPO calculation, typically reviewed on a quarterly or annual basis. Then split your analysis by major payable categories instead of relying on one blended result, so you can see what actually changed in payment timing.

Is a higher DPO always better for working capital?

No. A higher DPO can free up more short-term cash, but an extremely high DPO can also signal difficulty paying bills and create supplier-relationship risk. Treat sustained increases as a tradeoff to validate, not an automatic win.

What are the first warning signs that DPO optimization is hurting sellers?

Watch for signs that payment timing is drifting beyond intended policy, such as more overdue obligations, repeated payment exceptions, or visible relationship strain. If those signals rise while DPO rises, the change may reflect payment friction rather than healthier operations.

How should teams use DPO with DSO, DIO, and Accounts Payable Turnover Ratio in one operating view?

Use DPO for outflow timing and DSO as the corresponding view of cash inflows. Add DIO and Accounts Payable Turnover Ratio only when they are relevant to your operating model, and avoid forcing one headline conclusion when the metrics move in different directions.

What should be in the minimum evidence pack before changing payout timing policy?

At minimum, include the period definition for DPO (typically quarterly or annual), the payable and invoice data used in the calculation, and the documented assumptions behind the KPI. Add a recent trend view so teams can tell whether movement is stable or abrupt; in faster environments, AP teams may also monitor payables daily using automation and AI.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- digitalcommons.du.edu/cgi/viewcontent.cgitrusted

- downloads.regulations.gov/USTR-2024-0015-0040/attachment_1.pdftrusted

- irs.gov/irm/part3/irm_03-011-006rtrusted

- labor.ca.gov/wp-content/uploads/sites/338/2024/08/AB2849-...trusted

- occ.gov/publications-and-resources/publications/bank...trusted

- oecd.org/derec/49755570.pdftrusted

- sec.gov/Archives/edgar/data/1131227/0001193125252832...trusted

- sec.gov/Archives/edgar/data/1816815/0001493152240408...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Payment Platforms Use DPO to Improve Cash Flow Without Reconciliation Risk

Treat DPO as an operating control only when your ledger, reconciliation, and payout states agree on what "paid" means. If you run AP on a payment platform, you need one paid-state rule your finance, ops, and treasury teams can all defend. On a platform, a better-looking metric that hides settlement lag, pending payouts, or unreconciled items is not real cash-flow improvement.

Accounts Payable Days (DPO) for Platforms in the Real Payment Cycle

Treat **Days Payable Outstanding** as an operating control, not a vanity KPI. It measures average supplier payment timing. For platform teams, the real question is whether cash outflows are being delayed on purpose or whether payment problems are being found too late.

Embedded Working Capital: Factoring, Financing, or Cash Advance

Treat this as a product design choice first and a funding feature second. The model you pick changes who controls the invoice asset, who collects repayment, what your support team has to explain, and how the economics hold up once disputes and exceptions show up. That is the real lens for embedded working capital.