Quick Answer

Use a simple decision sequence: refund when cash must go back, credit invoice or adjustment when value changes without cash movement, and reversal plus rebill when the issued invoice is invalid. Before posting, require the original invoice ID, reason code, approver, and close-period check. Then run the correction with one idempotency key, capture webhook event ID, journal reference, and settlement reference, and close only after GL, AR, and customer balance align.

What a Credit Invoice Does#

Once volume grows, credit invoices, invoice reversals, and invoice adjustments stop being simple billing edits. They become order-to-cash events that affect customer balances, accounts receivable, accounting records, payment matching, and sometimes fund finalization on a different timeline. The practical mistake is treating them like one back-office task when they are really several linked records that have to stay in sync.

That gets harder because order-to-cash already spans multiple teams. Sales, support, billing, and finance operations can all trigger or approve a correction. Accounts receivable and accounting teams typically own different parts of the outcome. In a stack with multiple sources of truth or manual handoffs, a case that looks finished in the billing UI can still be unresolved in the accounting record or unsupported in downstream matching. Close confidence drops fast when each team is looking at a different version of the same invoice story.

The billing object can also behave in ways that catch teams off guard. A credit-note style action can reduce an open or paid invoice, and in some products it can take an open balance to zero and move the invoice status to paid. That may be correct for the invoice state, but it does not mean every downstream view is complete. If finance sees "paid," support sees "credited," and cash application still shows pending activity, you already have the ingredients for a month-end exception.

Fund finalization adds another layer. Payment settlement is the point where funds are finalized and transferred, and for card payments that often completes in one to three business days, not instantly. A correction can be valid in billing and accounting before the cash side has fully caught up. If you do not check that status separately, you can mark a case done while payout exposure or proof of the cash outcome is still incomplete.

This guide is meant to prevent that drift. It gives you decision rules for choosing the right correction, an execution order that avoids new mismatches, and verification checkpoints that keep GL, matching, and cash-status views aligned. Start with a simple rule: do not approve any correction path until the original invoice reference, the customer balance impact, and the expected accounting outcome all tell the same story.

The scope here is operational design inside order-to-cash and accounts receivable. Not every subscription billing platform behaves the same way. Product behavior is configuration-dependent, and some features must be enabled before related modules are available. In practice, confirm in product how your platform handles credit invoices or credit notes, reversal objects, invoice status changes, and related status events before you roll out policy. Recurly, for example, treats a credit invoice as a separate invoice object for credits, while other platforms may expose similar outcomes with different labels or controls.

Define each action before anyone clicks approve#

Define these as five separate approval paths before work starts: Refund, Credit invoice, Invoice reversal, Invoice adjustment, and Rebill. If teams blur those labels, they usually create revenue leakage or unnecessary billing complexity.

Separate the correction types first#

| Action | Typical trigger | Accounting intent | Customer impact | Reconciliation impact |

|---|---|---|---|---|

| Credit invoice | Price concession or service credit where cash stays on account | Record credit as its own invoice object | Reduces what the customer owes or applies to future invoices | Link the credit document to the original charge |

| Invoice reversal | Prior posted invoice accounting must be reversed | Reverse the prior invoice document | Invalidates the prior invoice outcome | Keep a reversal document and journal trail tied together |

| Invoice adjustment | Bill item amount due needs a debit or credit change | Change the amount due for a bill item | Updates the customer account balance | Tie the adjustment to the affected bill item |

| Refund | Completed payment must be returned in whole or part | Return cash after payment succeeded | Customer receives money back | Match refund records to payment and payout records |

| Rebill | Original invoice data is wrong and must be reissued correctly | Credit full invoice, duplicate it, correct data, and resubmit | Customer gets a corrected replacement invoice | Reconcile the full old-to-new document chain |

Apply one hard rule set#

If cash must leave, start with Refund. If cash stays on account and should affect future billing, prefer Credit invoice. If the original document is invalid, use Invoice reversal plus Rebill so the old accounting is unwound and the corrected duplicate creates the replacement accounting.

Check validity and customer outcome before approval#

Before you approve anything, confirm two points: whether the original invoice is still valid, and whether the customer expects cash back or an on-account credit. This is where teams most often drift, such as issuing a credit after support promised a refund, or using an adjustment when the invoice should be replaced.

Also flag any path that depends on manual offsets. Reversal and correction documents often require explicit operator action, and manual negative offsets are where tie-outs become harder to close cleanly.

Prepare the minimum evidence pack before issuing anything#

Before issuing a credit, reversal, or adjustment, require one minimum evidence pack and block execution until it is complete.

| Item | Type | Requirement |

|---|---|---|

| Original invoice reference | Prerequisite | Exact invoice ID being corrected |

| Reason code | Prerequisite | Structured value, not free text, with an optional operator note |

| Approval owner | Prerequisite | Person or role accountable for the decision |

| Close period status | Prerequisite | Confirm the accounting period is open before creating documents |

| Webhook event ID | Reference | Anchor recovery and reconciliation |

| Ledger journal reference | Reference | Anchor recovery and reconciliation |

| Settlement reference | Reference | Anchor recovery and reconciliation |

Step 1. Collect four business prerequisites. Stop if any are missing.

- Original invoice reference: the exact invoice ID being corrected.

- Reason code: use a structured value, not free text (for example

duplicate,fraudulent,order_change, orproduct_unsatisfactory), with an optional operator note. - Approval owner: the person or role accountable for the decision.

- Close period status: confirm the accounting period is open before creating documents, since closed periods can block new receivables activity.

Step 2. Enforce minimum controls on the request.

- Segregation of duties: requester and approver should be different for higher-risk changes.

- Audit trail: log each status change with user, timestamp, and linked document references.

- Idempotency key: assign one unique key per correction intent so retries are recognized as the same operation, not a new issuance.

Use a practical retry test: if the same request arrives twice with the same key, your handler should treat it as the same operation. Also note that some APIs may prune idempotency keys after at least 24 hours, so keep your internal request records longer.

Step 3. Capture the platform references needed for traceability.

- Webhook event ID

- Ledger journal reference

- Settlement reference

These references anchor recovery and reconciliation. Webhooks can retry for up to three days, and undelivered-event recovery can depend on events from the last 30 days.

Step 4. Run one pre-flight checkpoint before execution.

Do not proceed until General ledger, Accounts receivable, and customer-facing balance tell the same story. Reconcile AR to GL before and after posting, then confirm the customer balance reflects the same correction path.

If those three views disagree, fix the mismatch first. Related reading: Subscription Billing Platforms for Plans, Add-Ons, Coupons, and Dunning.

Choose the right action with decision rules, not judgment calls#

Choose the correction based on invoice and payment state, not escalation pressure: use a Refund when cash should return, use a credit note/adjustment when the invoice stands and only value needs to be reduced or reallocated, and use reversal + rebill when the invoice itself is not fit to stand.

| Issue | Use | Condition |

|---|---|---|

| Disputed charge | Refund | If payment succeeded and you need to return funds |

| Pricing mistake | Credit note or line-item adjustment | If customer, invoice identity, and service period are valid but amount is wrong |

| Service credit | Invoice adjustment or line-item credit | Usually for partial service failure, not a full reversal |

| Tax correction | New invoice or credit note | Depending on jurisdiction; do not assume void-and-edit is allowed |

| Duplicate bill | Refund or credit | Choose between returning cash now or offsetting a real future invoice |

| Timing error | Adjust forward or reversal + rebill | Adjust forward if invoice identity is valid; use reversal + rebill if invoice identity is invalid |

Step 1. Classify the issue before you select the document.

- Disputed charge: if payment succeeded and you need to return funds, issue a Refund (full or partial as needed). Record the dispute reason category from the dispute object.

- Pricing mistake: if customer, invoice identity, and service period are valid but amount is wrong, issue a credit note or line-item adjustment. Prefer line-item credits so the correction stays tied to the billed item.

- Service credit: for partial service failure, usually use an invoice adjustment or line-item credit, not a full reversal.

- Tax correction: do not assume void-and-edit is allowed. Depending on jurisdiction, you may need a new invoice or a credit note.

- Duplicate bill: if billed twice, choose between returning cash now (Refund) or offsetting a real future invoice (credit).

- Timing error: if dates or period timing are wrong but invoice identity is valid, adjust forward; if invoice identity is invalid, move to reversal + rebill.

Step 2. On paid invoices, make the trust-versus-predictability decision explicit.

Use a Refund when the customer expects money back now or is contesting the charge. Use a credit when the customer is active and a real upcoming invoice will absorb it. Before issuing credit, verify that a future invoice exists; otherwise you risk stranded balance. Also remember you can issue multiple partial refunds, but not above the original charge amount.

Step 3. Reserve reversal + rebill for invoice-level invalidity, and handle closed periods by rolling forward.

If invoice identity or legal content is wrong after approval or export, reverse and rebill instead of patching. If the Close period is closed, do not backdate just to force a neat report: post a forward adjustment and add an explicit audit note with original invoice ID, reason code, approver, and the closed-period exception. In some accounting systems, this rolls into Period '0' of the next year via balance brought forward handling.

For a step-by-step walkthrough, see How to Issue Compliant Tax Invoices in 50+ Countries as a Global Platform.

Execute the correction in the right order across billing and ledger#

After you choose credit, adjustment, or reversal, keep one correction object as the system anchor and sequence downstream updates from that record.

Step 1. Stabilize the case context before creating the correction. Before posting anything, confirm you have a consistent snapshot: original invoice ID, account or subscription ID, current balance context, period status, and approver. If your platform supports a short-lived hold, use it to reduce mid-process changes while the correction is being created.

Step 2. Create the correction object with retry safety and classification. Create the credit or reversal in the billing platform with an idempotency key so retries do not create duplicates. Keep one key per request (up to 255 characters) and reuse it only for retries of that same request. Persist the reason code at creation time; where supported, use standardized values (for example: duplicate, fraudulent, order_change, product_unsatisfactory).

Step 3. Post ledger and receivables in your required accounting sequence. Do not let projected balance views become your source of truth. Post through the accounting flow your stack requires, and make sure references join cleanly across the correction object, receivables document, and journal entry. If the original period is closed, use a new transaction date for the reversal instead of forcing a backdated post.

Step 4. Treat webhooks as async checkpoints, not guaranteed final state. Webhook delivery can be duplicated, delayed, stale, partial, or out of order. Log processed event IDs, skip duplicates, and use replay-safe handlers. For staged credit-invoice lifecycle events, fetch current object state before posting follow-on actions.

Step 5. Send notices after posting is stable, with traceable references. Send customer and internal notices only when the posted state is settled. Include references that let teams reconcile quickly, typically invoice ID, correction ID, amount, and reason code, and keep internal-only fields in internal channels.

Related: Streaming Media Subscription Billing: How OTT Platforms Handle Billing Trials and Churn.

Reconcile downstream impacts before declaring the case done#

A posted correction is only complete when your billing record, settlement evidence, and payout exposure tell the same story.

| Surface to check | What to verify | Red flag |

|---|---|---|

| Invoice state | Corrected document links to the original invoice and shows the approved amount and reason | The correction exists, but amount or source-invoice linkage does not match |

| Settlement and cash evidence | Transaction-level evidence matches the corrected amount, or clearly shows why cash did not move | Settlement is marked complete, but there is no linked transaction evidence |

| Payout execution exposure | Payout batches already scheduled or sent do not still include the corrected funds | Funds were corrected in billing, but still appear in a queued or paid-out batch |

Step 1. Match the corrected invoice to settlement evidence. Start from the correction record, then verify the cash path at transaction level. Where available, use transaction-level reports rather than summary balances. For example, Adyen's Settlement details report supports transaction-level reconciliation and shows transaction costs.

Your checkpoint is a traceable chain across original invoice ID, correction object ID, settlement or payout reference, amount, and journal reference.

Step 2. Check payout exposure before sign-off. For automatic payouts, reconcile by settlement batch so bank deposits map back to included transactions. Stripe's payout reconciliation model is batch-based, not a loose day-total check.

Use provider timing windows as documented: Stripe defines daily activity as 12:00 am to 11:59 pm. If you query payout balance transactions by API, remember the default 10 results is not the full dataset. For instant or manual payouts, reconciliation against transaction history remains your team's responsibility.

Step 3. Track exceptions and escalate mismatches to named owners. Keep exception handling operational, not informal. Track unresolved exceptions, time to close, and correction rework rate. Route mismatches into explicit queues or worklists so nothing sits unowned.

Two escalation triggers should be explicit:

- Settlement is marked complete, but ledger posting is missing.

- Ledger is posted, but settlement evidence is missing or cannot be matched.

Unreconciled line-level exceptions should block closure until resolved.

Step 4. Define and document your team's completion state. Close the case only after your checklist is fully met and reconstructable by another operator without back-and-forth. A practical checklist usually includes the corrected billing document, matching journal entry, recorded sign-off, and an audit export bundle with supporting reconciliation evidence.

For a deeper look at the billing-engine design behind invoice and credit flows, read How to Build a Subscription Billing Engine for Your B2B Platform: Architecture and Trade-Offs.

Handle the failure modes competitors skip#

The case is not done until you control replay risk and manual workarounds that can create a second financial impact. Prioritize the failures that recur most: duplicate webhook delivery, stale retries after timeouts, and manual back-office edits without reliable change history.

Step 1. Separate duplicate events from safe request retries. Treat inbound events and outbound create or update calls as different risks. Webhook endpoints can receive the same event more than once, so log processed event IDs and skip anything already logged. For create or update calls after a connection failure, retry the same request with the same idempotency key so you do not create a second side effect.

Checkpoint: one approved correction request, one idempotency key, one resulting correction object, and one processed event ID per receipt. A common failure mode is sending a retry with a new key or changed parameters and calling it a replay, which can trigger duplicate credits and duplicate journal postings.

Step 2. Drain stale retries before touching the ledger again. Clear undelivered event backlogs first, then continue with corrections. Stripe supports manual processing of undelivered events while automatic retries can continue for up to three days, and Stripe CLI resend works for up to 30 days after event creation.

If a duplicate posting occurred, reverse only the unintended duplicate entry, not the original approved correction. Then rerun the prior reconciliation sequence: corrected document, journal reference, cash evidence, and payout exposure.

Step 3. Quarantine manual edits that bypass the audit trail. Do not trust manual edits unless actor attribution and change history are complete. The practical test is whether you can show who changed the record, when they changed it, and what the prior value was. Audit-log visibility depends on retained change history in your system.

If you cannot reconstruct the edit path, freeze the case, rebuild the evidence pack, and route for approval. Where approval limits apply, out-of-limit entries can remain in pending adjustment status until someone with the right authority approves or rejects them.

Step 4. Post late-discovered errors into the forward period. When an issue is discovered after month-end, default to a forward-period correction unless approved closed-period handling says otherwise. Closed-books controls should at least warn or require a password prompt for transactions on or before the closing date. Document the original invoice, discovery date, closed-period status, and approval record.

Use post-close change reporting as a verification step. If someone edited the closed period directly, treat it as a control exception and escalate when you see:

- Repeated manual overrides on the same account

- Missing approval artifacts or adjustments still in pending status

- Unresolved cash deltas after reversing the duplicate posting and rerunning checks

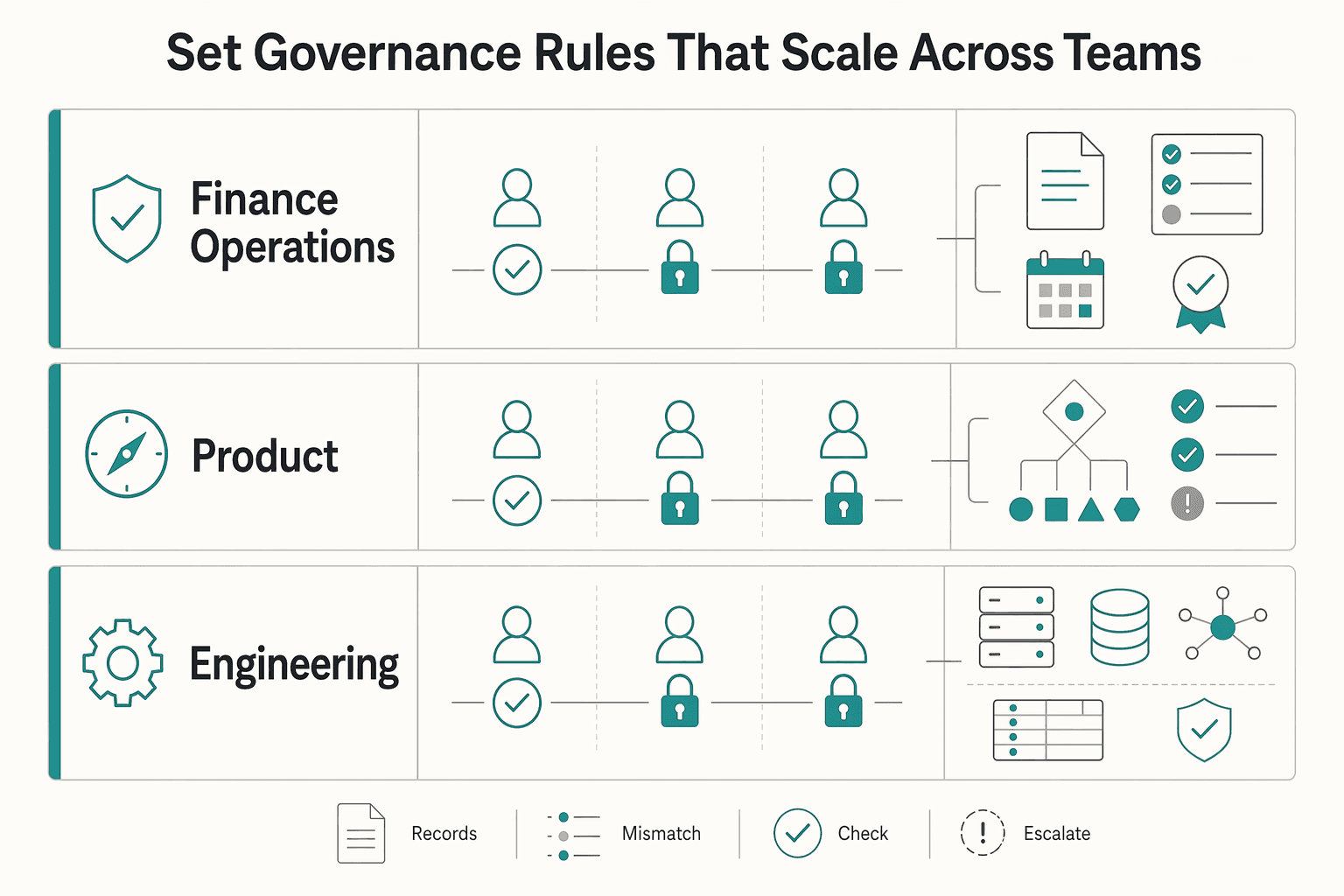

Set governance rules that scale across teams#

Governance scales when role boundaries are explicit, risk routing is policy-based, and control reviews are recurring. The core rule is unchanged: one person should not be able to create, approve, and post a high-impact correction.

| Team | Owns |

|---|---|

| Finance operations | Reason codes, evidence-pack completeness, and close sign-off |

| Product | The rule that determines credit invoice vs reversal vs adjustment vs refund vs rebill |

| Engineering | Permissions, event capture, and audit trail integrity |

Step 1. Assign ownership by correction type and action. Map each correction type to create, approve, and post. Finance operations should own reason codes, evidence-pack completeness, and close sign-off; product should own the rule that determines credit invoice vs reversal vs adjustment vs refund vs rebill; engineering should own permissions, event capture, and audit trail integrity. Validate this with a live role test: conflicting actions must be blocked for the same user under separation of duties.

Step 2. Route by risk, not by team preference. Use approval limits so lower-risk adjustments can auto-route while higher-risk reversals move to pending until an authorized approver acts. For higher-risk cases, enforce a two-person rule: approval must come from a different authorized user before balances update. If your control checks only amount and not actor identity, segregation of duties is incomplete.

Step 3. Run recurring control reviews and close root causes. Use ongoing monitoring plus periodic separate evaluations of control health. Review audit trail quality, reconcile differences across billing, GL, and cash records, and group recurring order-to-cash exceptions by root cause. When the same failures repeat, treat that as a design signal for permissions, event handling, or migration setup, not just an operations issue. Connect those fixes to your billing architecture and your platform migration plan.

This also aligns with B2B SaaS vs B2C Subscription Billing and Churn Differences That Drive Operations.

Conclusion#

If you remember one thing, make every correction a controlled accounting event, not a customer support gesture. Teams stay out of trouble when they standardize definitions, force explicit decision rules, and refuse to call a case done until the GL, matching, and cash-status views agree.

That is what keeps credit invoices, reversals, adjustments, refunds, and rebills from turning into close-period noise. It also keeps you from fixing the customer-facing balance while leaving AR, journal entries, payout references, or disbursement exposure unresolved in the background. A correction is only complete when the document is right, the accounting entries are posted, the exception is matched, and the original history is still preserved in the audit trail.

Use this as a final copy-and-paste check before you close any case.

- Define action type (credit, reversal, adjustment, refund, rebill)

Name the action first and tie it to the accounting intent. If the original issued document is invalid, assess whether it should be handled as a reversal. If cash must leave, route through a refund path. If you are correcting value without sending cash, use the right non-cash correction. The failure mode here is definition drift, where different teams use the same word for different outcomes.

- Confirm approvals, close-period status, and evidence pack

Do not proceed until the request has an approval owner, the original invoice reference, a reason code, and proof that the target period is open or that a forward-period correction is required. Some ERP flows use a real review gate such as Pending Approval before completion. The hard checkpoint is simple: you cannot post transactions to a closed accounting period, so verify period status before anyone posts.

- Execute with idempotency key and webhook-safe processing

Every correction request should carry a unique idempotency key so retries do not create the same correction twice. If your platform follows Stripe-style behavior, that key can be up to 255 characters, and reused retries should resolve to the same request rather than a duplicate. On the async side, store webhook event IDs and reject duplicates before processing.

- Post GL and AR updates in sequence

Use the posting order your platform supports, but make it explicit and consistent. AR correction activity should flow through configured journals and then summarize to GL according to your setup, not through ad hoc balance edits. Verification point: confirm the journal reference exists before you treat the AR side as final.

- Check invoice, cash status, and payout exposure

Match the corrected invoice state to cash evidence and to any payout-level reporting, such as a payout reconciliation report. Red flag: funds show as included in payout, but no journal posting exists, or the journal posted with no cash evidence. Either mismatch means the exception stays open.

- Archive audit trail and close the exception

Preserve the original accounting history alongside the offsetting and new entries. That audit trail is what makes the case defensible after month end, during review, or during migration to a new platform. Close the exception only when the evidence pack, approvals, references, and sign-off are all attached.

Frequently Asked Questions

What is the difference between a credit invoice and a refund in subscription billing?

A credit invoice documents a customer credit as its own invoice object. A refund returns funds to the original payment instrument, such as the card that was charged. If cash is leaving your business, treat it as a refund problem first. If you are recording a non-cash credit against billing, use the credit document.

When should I issue an invoice reversal instead of an invoice adjustment?

Use an invoice reversal when the invoice was already posted and issued and the accounting document itself needs to be reversed. Use an invoice adjustment when you need a correction entry and want to preserve invoice history rather than edit the invoice directly. A simple check is this: if an already issued document needs to be reversed, use a reversal. If the balance or amount needs correction, adjust it.

What minimum controls should exist before anyone can approve a reversal?

At minimum, the person approving should not be the same person who created the reversal request, because segregation of duties is meant to reduce error and fraud risk. You also want a recorded approval step before downstream payment actions continue, since some ERP flows explicitly require approval after an adjustment before payment can proceed. Red flag: if your tool lets one user create and approve the same high-impact correction, the control is too weak.

How do idempotency keys prevent duplicate credits when webhooks are retried?

Idempotency makes repeated API requests retry-safe, so the same request does not create the same correction twice. That matters because webhook endpoints can receive the same event more than once. In practice, pair an idempotency key on the create request with event ID logging on the webhook consumer side, then test by replaying the same event and confirming no duplicate correction is created.

What should finance do if cash data and GL postings do not match?

Do not mark the case complete. First compare the invoice state, cash evidence, and journal reference to identify what is missing or duplicated, then move the exception to manual review if auto-matching failed. Investigate and resolve the mismatch before further corrections are issued.

Can I correct an invoice after close period without reopening the period?

In many systems, yes, but only by posting the correction in an open accounting period if you choose not to reopen the closed one. Do not assume your platform supports backdated fixes after close. The practical checkpoint is to verify close-period status before posting, then document the link to the original invoice so the forward-period correction is easy to audit.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- csrc.nist.gov/glossary/term/Separation_of_Dutytrusted

- docs.stripe.com/api/idempotent_requeststrusted

- docs.stripe.com/reports/payout-reconciliationtrusted

- guides.gaoinnovations.gov/greenbook/2025/principle-16-perform-monitori...trusted

- oacp.upenn.edu/audit/audit101/internal-controls-guidance/op...trusted

- stripe.com/resources/more/payment-reconciliation-101trusted

- stripe.com/resources/more/payment-settlement-explained-...trusted

- billingplatform.com/solutions/subscription-billingexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Build a Subscription Billing Engine for Your B2B Platform

If you are designing a B2B subscription billing engine, get the close and reconciliation model right before you chase product flexibility. A durable sequence is to define recurring billing scope (plans, billing periods, usage, and trials), then map settlement and payout reconciliation to transaction-level settlement outputs, and finally tie that discipline into month-end close controls. The real test is simple: finance should be able to trace invoices, payments, and payouts from source events through settlement records into reconciled close outputs without ad hoc spreadsheet rescue.

How to Migrate Your Subscription Billing to a New Platform Without Losing Revenue

If you need to **migrate subscription billing platform without losing revenue**, treat it as a revenue operations change, not a simple software swap. Billing migrations sit close to renewals, revenue reporting, and payment credentials, so mistakes rarely stay technical. They can show up as duplicate records, inaccurate revenue reporting, failed renewals, or customer-facing downtime.

How OTT Platforms Handle Billing Trials and Churn in Streaming Subscriptions

Start with the monetization model. Choose your monetization path before a product demo starts steering the decision. For a streaming offer, the real question is not which vendor can show subscriptions on a checkout page. It is whether your business is built around recurring access, ad-supported reach, one-off transactions, or a direct-to-consumer mix that may vary by market.