Quick Answer

B2B SaaS and B2C subscription billing differ most in who buys, how payment is collected, and how churn should be read. B2B often needs invoicing, purchase orders, admin ownership, and stronger exception handling, while B2C usually works best with low-friction recurring card charges. Churn also behaves differently: B2B can show stable logo counts while revenue churn worsens, and B2C often exposes risk first through failed-payment recovery.

How B2B SaaS and B2C Subscription Operations Differ#

Treat B2B SaaS and B2C subscription as different operating models, not just two versions of recurring revenue. Both rely on repeat payments, but when you choose between charges on saved payment methods, recurring invoices, or a mixed collection setup, you also choose a different level of billing effort, ledger reconciliation work, and churn risk.

A more useful question is not which model looks simpler on paper. It is which model gives you cleaner records and fewer exceptions for how customers actually buy. If you are evaluating b2b saas subscription vs b2c subscription billing churn differences, start with the collection rail and the evidence trail behind it. Those choices shape everything that follows in reporting and renewal handling.

B2C subscriptions can use recurring card billing for low-friction activation. B2B SaaS can use the same rail, and some teams also add invoice-based collection. Invoice operations bring their own collection and reconciliation requirements. The commercial motion may still look like subscription billing, while the back office manages more handoffs, more exceptions, and more ways for billing records and ledger entries to drift out of sync.

The churn picture also changes once you look past a single headline number. Customer churn tells you how many accounts left. Revenue churn tells you how much revenue left. When revenue is unevenly distributed, those metrics can diverge sharply, so a stable customer count can still hide meaningful revenue risk. If you only track one, treat it as a warning light, not a final answer.

A practical checkpoint early on is simple. Can you verify the billing event, confirm the first successful charge or invoice settlement, and tie that outcome back to the ledger without manual detective work? A practical red flag is just as clear. Failed payments are a leading cause of involuntary churn, where a subscription is lost because the payment process broke rather than because the customer chose to leave. One vendor-cited estimate says close to 35% of transactions fail, but treat that as directional context, not a benchmark to copy across segments.

The aim of this comparison is straightforward. You should come away able to choose B2B controls, B2C defaults, or a hybrid with open eyes, then set the right reconciliation checks and churn signals before an avoidable billing problem becomes real revenue churn. If your current model forces one recurring billing motion across unlike customer groups, that is usually the first place to look for preventable loss.

B2B SaaS and B2C subscription differences at a glance#

Start with operating reality, not labels: use a B2B motion when buying, billing, and renewal ownership sit across an organization; use a B2C motion when one person can activate and keep paying with minimal admin. Use a hybrid when both patterns are real in your customer base. Forcing one motion across both usually shows up first as reconciliation exceptions and renewal ownership confusion.

| Criterion | B2B SaaS | B2C subscription | Ops impact | Default recommendation |

|---|---|---|---|---|

| Buyer structure | Often a buying group rather than one decision-maker. Forrester reports an average of 13 people involved, with 89% of purchases spanning two or more departments. | Often fewer stakeholders in the decision and payment path. | More approval evidence, more handoffs, and more chances billing contact, admin contact, and renewal owner are different people. | Use B2B controls when procurement, finance, or IT approvals are in path. Use B2C defaults when one person can discover, buy, and renew without internal routing. Hybrid fits when self-serve starts the deal but larger accounts add approvals later. |

| Billing rail | Recurring invoices, charges on saved payment methods, or both. Purchase orders can be part of the flow. | Usually recurring charges on saved payment methods. | Invoice-plus-PO flows add exception handling because invoice records may need PO references and matching checks. Card-first flows reduce manual touch but increase failed-payment recovery pressure. | Favor B2B setup when invoice approval, PO linkage, or negotiated billing terms matter. Favor B2C when activation speed matters more than invoice formality. Hybrid is justified if enterprise accounts require invoices while smaller customers renew by card. |

| Entitlement model | More likely to include multi-user management and account-level administration. | More often simple single-user or lightweight household-style access. | Multi-user access adds reconciliation touchpoints between who is billed and who has access. Renewal risk increases when admin ownership is unclear. | Treat as B2B when seat ownership, admin permissions, or account-wide access must be managed centrally. Keep B2C when billing and access can stay tied to one person. |

| Pricing model | Commonly uses per-seat pricing or usage-based billing. Per-seat maps seat count to user units; usage-based bills measured consumption. | Often simpler recurring price points, though usage elements can exist. | Seats and usage create variable invoice lines, mid-cycle changes, and heavier audit trails for billed amounts. Fixed consumer plans are easier to post and explain. | Choose B2B when value tracks users or consumption and you can support metering plus invoice detail. Choose B2C when predictable pricing and low support burden matter more. |

| Churn profile | Customer churn and revenue churn can diverge sharply when revenue is concentrated. | Customer churn and revenue churn may track more closely when account values are more uniform. | B2B renewal review should track both account count and revenue exposure. B2C teams can often detect risk from payment-failure and cancellation patterns, while still checking revenue mix. | Use B2B reporting depth when a few account losses can move revenue materially. Use B2C reporting emphasis when broad customer behavior matters more than any single contract. Hybrid fits when you run both a long tail and a meaningful enterprise tier. |

Two operating checks matter most. First, verify the evidence trail for the rail you run: in card-first flows, confirm the billing event and first successful charge; in invoice flows, make sure the invoice includes the correct PO reference where required so billing ties back to approved order evidence.

Second, separate failure ownership. In B2C, failed recurring charges can be collection failure rather than true product-driven churn. In B2B, payment delays can come from invoice matching friction, including invoice, PO, and receipt records that do not align or discrepancies outside tolerance.

Treat public churn benchmarks as context, not targets. Headline rates vary by churn definition, recognition timing, and sample design. One dataset may aggregate over 3,500 respondents across seven years, while another uses different churn-recognition rules. The practical check is whether your own customer churn and revenue churn tell the same story, or whether your billing model is hiding risk in one of them.

If you want a deeper dive, read SaaS Subscription Billing Benchmarks: Churn MRR Expansion and Payment Decline Rates.

Buyer structure changes your billing risk before churn shows up#

Buyer structure is usually the earliest signal of billing risk, before churn metrics move. If procurement, finance approval, and IT admin are all in path, operate the account with B2B controls from the start, even if checkout begins online.

This is operational, not just commercial. B2B purchases often involve a group rather than one buyer. CEB material cited by Salesforce reports an average of 5.4 stakeholders, and Challenger describes finance, IT, procurement, and other functions joining decisions. In self-service B2C flows, activation is typically tighter: Microsoft's self-service guidance states a user signs up and uses the subscription for themselves.

That split should shape your onboarding design immediately. Self-serve flows optimize for quick activation and minimal admin steps. B2B onboarding usually needs clear role ownership and identity controls: RBAC for permissions, SAML SSO for company-managed authentication, and provisioning/deprovisioning tied to the customer's identity system so access changes are not handled ad hoc.

Before marking an account as fully onboarded, confirm three named owners: billing contact, access admin, and renewal owner. If ownership is missing or unclear, handoff gaps often show up later as renewal delays, support friction, or avoidable churn risk.

Handoff risks worth checking every renewal cycle#

| Handoff risk | What to verify |

|---|---|

| Owner changes | Verify whether the original buyer still owns budget and approval, not just whether the CRM contact still exists. |

| Access revocation | Confirm deprovisioning follows the customer's identity source where possible; manual-only removal paths can drift. |

| Renewal ownership gaps | Check that renewal notices route to someone who can act, not only the original purchaser. |

| Admin continuity | Confirm a backup admin exists for multi-user access so one departure does not stall operations. |

Design for the real owner chain, not the checkout surface. When RBAC, SSO, and admin-managed provisioning are required, self-serve entry is best treated as initial activation, not proof the account behaves like B2C.

When to use card-first recurring billing vs invoicing and purchase orders#

Use card-first recurring billing when renewals can run without a human approval step, and use invoicing plus PO controls when approvals or matching checks are required before payment.

| Decision point | Card-first recurring billing | Invoicing plus purchase orders |

|---|---|---|

| Cash collection speed | Automatic collection at the start of each billing cycle; card settlement is commonly cited at 1 to 3 business days. | Slower by design, with payment on terms such as Net 30, Net 60, or Net 90. |

| Approval path | Minimal routing when the saved payment method is already authorized. | Built for approval workflows that route to identified approvers and record approval actions. |

| Dispute / exception profile | Main risk is the card-dispute path; a chargeback can reverse a processed payment. | Main risk is approval or matching failure before payment; discrepancies can be routed for human review. |

| Reconciliation complexity | You still need to tie charge success, settlement, disputes, and refunds to the ledger. | You need a heavier evidence chain: invoice states, PO validation, and sometimes three-way match evidence. |

The tradeoff is straightforward. Card billing reduces delay, but only when the customer can authorize automatic charges each cycle. Invoice and PO rails add friction on purpose because some buyers require recorded approval and matching controls before payment is released.

A practical launch check is simple: can this customer renew without a human approval event? If yes, card-first is usually a strong fit. If no, set up invoicing and define what proof is required before an invoice is sent or treated as collectible. For PO-backed accounts, that typically includes the PO reference, approval evidence, and match results that confirm bill-to-PO alignment and, where relevant, receipt or service-entry alignment.

Many SaaS teams run both rails in parallel, such as immediate-payment self-serve accounts and enterprise accounts on terms. Keep those as separate exception queues. Card queues focus on failed charges, retries, disputes, and expired payment methods. Invoice queues focus on invoice status changes, missing PO details, approval holds, and mismatch review. Keep operator artifacts distinct by rail:

- For invoicing: track invoice statuses: draft, open, paid, uncollectible, and void.

- For PO flows: store PO references and validation evidence, and route failed match checks for review.

- For card flows: reconcile charge success to settlement, then monitor disputes and refunds separately so cash and revenue do not drift.

If you need a simple operating rule, use card-first for velocity and invoice plus PO for mandatory approval environments. For a step-by-step walkthrough, see Building Subscription Revenue on a Marketplace Without Billing Gaps.

Plan design choices create different churn drivers#

After you choose a billing rail, retention risk shifts to plan design. In per-seat plans, expansion and contraction usually show up as seat-count changes; in usage-based plans, they show up as consumption changes. That is why revenue churn can move even when logo churn looks stable.

| Plan design choice | Typical expansion path | Churn risk to watch |

|---|---|---|

| Per-seat pricing | Added users, teams, or departments | Seat reductions can shrink recurring revenue without a full logo loss |

| Usage-based pricing | More consumption or new workloads | Revenue can contract quickly when usage drops, even if the account remains active |

| Enterprise feature set (SSO, API access) | Deeper deployment into customer identity and internal systems | Missing admin/integration fit can stall rollout and raise renewal risk |

For B2B SaaS, admin, integration, and security needs are often part of the buying requirement, not optional polish. Enterprise customers commonly expect SSO and API access so they can integrate your product into internal systems. In B2C subscriptions, those same controls often add setup overhead, so fast activation and low-friction access usually matter more.

Read logo churn and revenue churn together, especially when a few large contracts carry most recurring revenue. Logo churn tracks account loss, while revenue churn tracks recurring revenue loss, and those can diverge materially when account sizes differ. A ChartMogul example shows 33% customer churn and 50% revenue churn in the same period, which is why concentrated enterprise books need both metrics in renewal reviews.

A practical finance signal is expansion quality, not just headline churn. As one finance-leader example put it: "net revenue retention rate was 128% for the trailing twelve months, highlighting our ability to expand existing customer relationships through increased consumption and new workloads."

Related reading: Best Lead Generation Tools for B2B SaaS Operators.

Failure modes that teams mislabel as churn#

Do not label every non-payment or renewal delay as lost demand. A meaningful share of these cases are billing-operations failures first: payment failure (involuntary churn), invoice disputes, PO-invoice mismatch holds, blocked invoices, or onboarding and activation gaps that delay renewal decisions.

The distinction matters because ownership changes. Demand churn is a product-value problem; billing and collections failures are an operations problem across finance, collections, and cross-functional handoffs.

| Failure mode | Where it appears first | Verify before calling it churn | Common misread |

|---|---|---|---|

| Failed card or banking issue | Failed collection events, then dunning emails | Customer payment attempt, retry execution, recovery outreach | Treated as cancellation when it may be involuntary churn |

| Invoice dispute | Billing/support/AP dispute queue | Dispute reason, ticket age, service status | Treated as non-renewal when it is delayed collection |

| PO mismatch or blocked invoice | Match hold, blocked invoice status, reconciliation break | PO number match, quantity/price mismatch, block/hold status | Treated as refusal to pay when payment is operationally blocked |

| Delayed onboarding | Onboarding/support queue, then renewal delay | Go-live status, active usage, promised setup completion | Treated as weak demand before activation is complete |

In B2B SaaS, PO mismatch and blocked-invoice paths are often misclassified. If invoice and PO do not match within defined tolerances, the invoice can be held; if blocked, it cannot be paid until resolved. When reconciliation shows open receivables and AP shows blocked or held status, treat it as document and workflow repair, not churn evidence.

In card-first B2C flows, the first signal is usually failed charge activity followed by dunning. Check retries, message timing, and post-failure usage before you classify the account. If usage continues and payment recovery fails, start with collections operations.

Escalation timing is a retention tradeoff. A harder collections posture may protect near-term cash, but poorly timed pressure can damage customer sentiment and make retention harder, especially when dispute, blocked-invoice, or onboarding issues are still unresolved.

Weekly red-flag review for finance and product:

- Failed collection events with continued product activity

- Disputed, blocked, or PO-held invoices

- Renewal delays with unresolved onboarding or activation gaps

- Reconciliation breaks where invoice status and cash status disagree

- Dunning accounts without a clear follow-up owner

Before you call churn, require evidence from both sides: payment status and product activation status.

Decision checklist for choosing B2B SaaS, B2C subscription, or hybrid#

Route by buying motion, not by channel: enterprise procurement signals point to B2B SaaS controls, low-friction individual signup points to B2C defaults, and mixed signals call for a deliberate hybrid.

| Decision question | If yes | If no |

|---|---|---|

| Is the buyer/payer different from the end user? | Use B2B SaaS controls (billing owner, admin ownership, and account-level handling). | Keep B2C-style self-serve defaults for single-user signup and usage. |

| Does the deal require invoicing, purchase-order flow, or negotiated pricing/terms (including private offers)? | Treat as enterprise contract motion and route to B2B handling. | Keep standard self-serve checkout terms. |

| Does the account need admin-led entitlements (multi-user management, role control)? | Use B2B entitlement and admin-control patterns. | Keep activation lightweight for individual users. |

| Are approvals or procurement systems part of the purchase path? | Plan for approval workflow burden and stronger finance/ops handling. | Prioritize low-friction activation to protect conversion. |

| Will this segment create frequent billing exceptions that need tracking and ownership? | Stand up stronger reconciliation and exception-management controls. | Keep operations lean with lightweight dunning management. |

Use this as an internal policy heuristic: if two or more enterprise signals are present, for example PO/invoicing requirements, multi-user admin needs, or enterprise contract terms, default to B2B SaaS controls even when entry starts as self-serve. This is a practical routing cutoff, not a universal external rule.

If both motions are real in your business, run a hybrid model on purpose: separate policy, pricing, and support lanes rather than forcing one model across all segments. In practice, that usually means a self-serve lane and an enterprise lane with invoicing, approvals, and admin-controlled entitlements. Related: The Best Tools for Managing Subscription Billing.

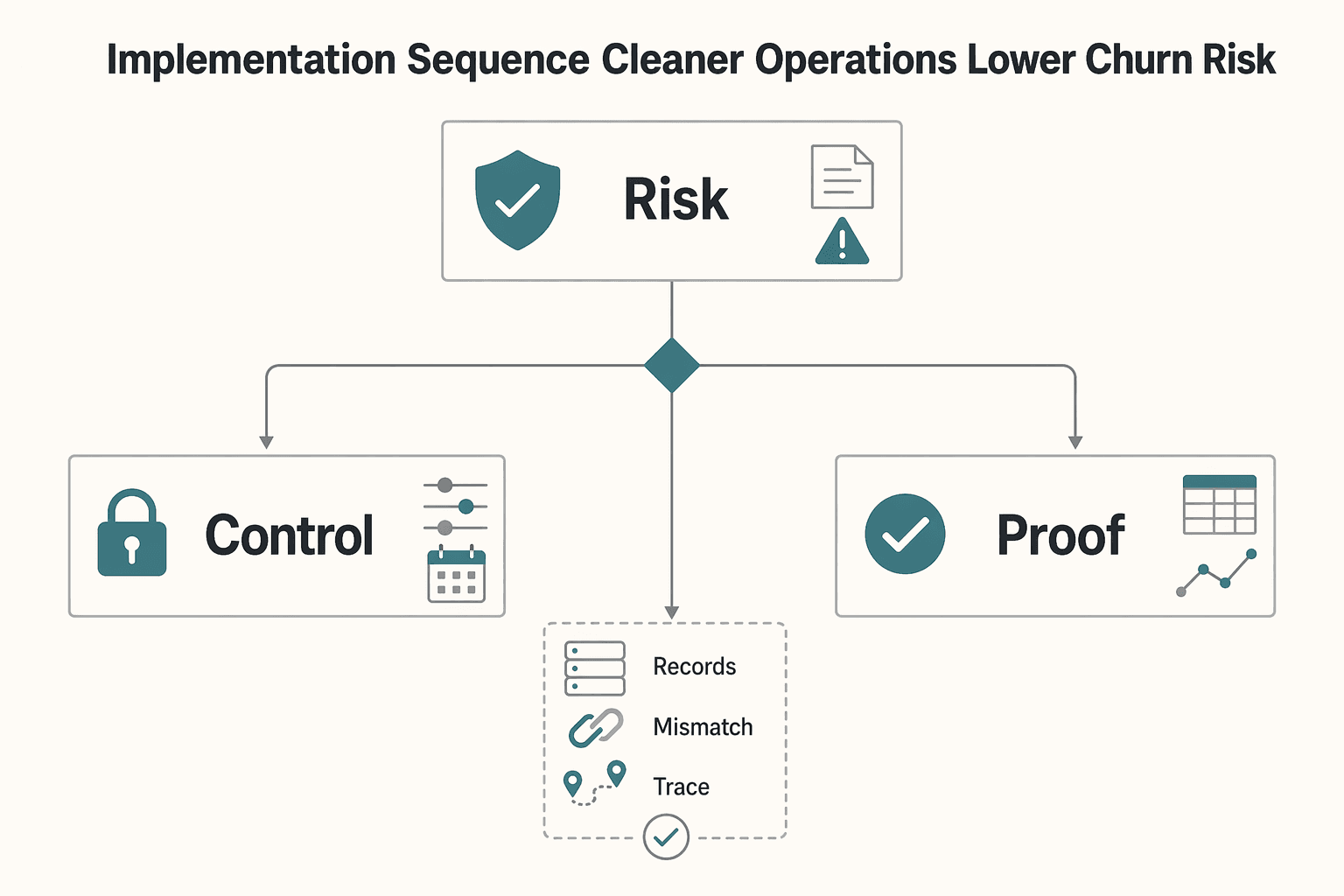

Implementation sequence for cleaner operations and lower churn risk#

Run the rollout in this order: segmentation, billing rails, entitlement model, then reconciliation and churn monitoring. That sequence keeps operational failures from being misread as churn and gives you usable checkpoints before scale adds exceptions.

| Stage | Decision | Verification checkpoint | Failure to prevent |

|---|---|---|---|

| 1. Segmentation | Route accounts to B2B SaaS controls, B2C defaults, or hybrid lanes | Confirm payer, user, admin owner, and billing path match the lane | Enterprise exceptions hidden inside self-serve flow |

| 2. Billing rails | Choose card-first recurring billing, invoicing, or both | First successful charge or confirmed invoice settlement by lane | Retry duplication, delayed invoicing, unclear exception ownership |

| 3. Entitlement model | Set single-user access or RBAC/SSO/API access | Onboarding and admin ownership confirmed before renewal risk is assessed | Paid account with incomplete activation or no valid admin owner |

| 4. Controls and monitoring | Define reconciliation outputs, dunning recovery, renewal review | Track recovery rate, invoice-state checkpoints, and renewal readiness | Ops defects labeled as churn without an evidence trail |

Start with the lane, then wire the money path#

Lock the lane before you ship checkout. If an account needs invoicing, approvals, or admin-managed access, route it to the B2B lane early. If one user can self-serve and pay directly, keep the B2C path lighter. After lane selection, set billing rails, then attach entitlement rules. This order avoids adding enterprise access complexity where it is not needed.

Define the evidence pack before exceptions multiply#

Each transaction flow should produce a minimum evidence pack:

| Evidence item | Included detail |

|---|---|

| Originating billing event | charge, invoice, or payment-attempt record |

| Approval trail where required | procurement or internal release approval in invoice-led flows |

| Ledger reconciliation output | ties fees and outcomes to lifecycle status changes and events |

For invoice-led flows, checkpoint invoice timing explicitly. Stripe documents that new invoices start in draft, waits 1 hour after successful invoice.created webhook responses before attempting payment, and can still finalize/send after 72 hours if responses are not received. If those gates are not monitored, delayed invoicing can appear later as collection risk or false churn signals.

Make API ownership explicit#

Require idempotency keys on write operations. Stripe supports safe retries with idempotency and documents a 24 hour retry window for clients using the same key, which helps prevent duplicate financial side effects. Use webhooks for asynchronous status handling, but plan for replay and duplicates. Stripe can resend undelivered webhook events for up to three days, so make ownership explicit for replay handling, duplicate protection, and final failure-state resolution.

| Control | Operational note |

|---|---|

| Idempotency keys | Require idempotency keys on write operations. |

| Safe retries | Stripe documents a 24 hour retry window for clients using the same key, which helps prevent duplicate financial side effects. |

| Webhooks | Use webhooks for asynchronous status handling, but plan for replay and duplicates; Stripe can resend undelivered webhook events for up to three days. |

Use operational checkpoints, not intentions: onboarding completion, first successful charge or settled invoice, recovery rate from dunning management, and renewal readiness review confirming billing owner, admin owner, and access state alignment.

We covered this in detail in How to Calculate and Manage Churn for a Subscription Business.

Conclusion#

The right answer is not choosing a winner in the abstract. It is matching your billing architecture, entitlement model, and churn controls to how each customer segment actually buys, pays, and renews. If your enterprise accounts need invoicing and contract-level controls, treat them that way from the start. If your growth motion depends on fast activation and recurring card collection, keep that lane simple instead of forcing heavier controls onto it.

That choice shows up quickly in operations. Accounts receivable management is not just sending invoices. It is invoicing, tracking, and collecting payments. Payment reconciliation is not a back-office afterthought. It is the process of matching transaction records to accounting records for accuracy. A practical checkpoint is simple: can you trace every successful charge or settled invoice back to the right customer, contract or subscription record, and accounting entry without manual guesswork? If not, you do not just have reporting noise. You may also have renewal risk hiding inside collections and reconciliation work.

Teams often do better when they separate lanes early. They run card-first flows where speed matters, and they keep invoice and contract controls where buyer complexity demands them. That does not mean making every flow stricter. There is a real tradeoff here. More control can improve cash-flow discipline and make reconciliation cleaner, but it can also add activation friction and a worse customer experience if you apply it to the wrong segment.

For churn control, keep the same discipline. Failed-payment recovery is worth tightening because stronger recovery programs are linked to lower involuntary churn, but do not stop there. Retention in SaaS should be read through multiple views, not one headline number, so your benchmark tracking should sit beside your own segment data rather than replace it. Peer datasets can be useful, but only when you overlay them with your own metrics and segment definitions. Even refresh cadence matters operationally, so set your review rhythm around when your benchmark source updates instead of comparing stale snapshots.

A practical next step is to rerun the decision checklist against your current customer segments, then tighten two things in your existing subscription billing stack: failed-payment recovery and benchmark review discipline. If you do that well, the differences between B2B SaaS and B2C subscription billing stop being theory and start turning into cleaner ledger reconciliation, fewer preventable failures, and more durable retention.

Frequently Asked Questions

How is B2B SaaS subscription billing operationally different from B2C subscription billing?

B2B SaaS billing usually has more approvals, negotiated terms, and document handling than B2C subscription billing. It often needs invoicing, purchase orders, and clear exception ownership. A practical check is whether you can identify the payer, admin owner, and payment document trail before renewal.

Why can lower logo churn still hide higher revenue churn risk in B2B SaaS?

Logo churn counts lost accounts, while revenue churn measures recurring revenue lost. In B2B, one canceled account can remove far more revenue than several smaller cancellations. If account sizes vary, read both metrics together.

When should a team use invoicing and purchase orders instead of recurring credit card billing?

Use invoicing and purchase orders when approvals are required, payment terms are negotiated, or finance needs document-backed settlement. These flows are heavier because billing often must match the invoice to the purchase order and related records before payment. Forcing a PO-driven buyer into card-first renewal can create delays that are operational, not true churn.

Which churn signals should billing ops track first for B2B SaaS vs B2C subscription?

For B2C, start with logo churn and failed-payment recovery because payment failure is a common preventable loss path. For B2B, track revenue churn, invoice reconciliation exceptions, payment delays, and failed-payment recovery on card accounts. If you cannot separate cancellation from collection failure, churn reporting is distorted.

How do per-seat pricing and usage-based pricing change retention and expansion behavior?

Per-seat pricing expands or contracts through seat adds and seat removals. Usage-based pricing moves with consumption, so revenue can change even if the account stays active. Check seat changes or usage trends before labeling the account as churned.

What should be in a practical decision checklist before choosing a hybrid model?

Ask whether some customers need purchase orders or invoicing, multi-user admin, negotiated terms, both card and invoice collections, or document matching instead of only charge events. If several answers are yes, split the lanes early. A hybrid works best when self-serve and enterprise motions are both real.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- docs.stripe.com/billing/subscriptions/usage-basedtrusted

- docs.stripe.com/subscriptions/pricing-models/per-seat-pricingtrusted

- stripe.com/en-li/resources/more/what-is-a-po-number-on-...trusted

- stripe.com/gb/resources/more/what-are-net-payment-terms...trusted

- txst.edu/gao/ap/resources/disputing-invoices.htmltrusted

- a.sfdcstatic.com/content/dam/www/ocms/assets/pdf/misc/The-Cha...external

- atlassian.com/licensing/purchase-licensing/howtopayexternal

- challengerinc.com/blog/more-b2b-decision-makers-want-inexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

A Guide to Dunning Management for Failed Payments

If you run recurring invoices, failed payments are not back-office noise. They create cashflow gaps, force extra follow-up work, and increase **Involuntary Churn** when good clients lose access after payment friction.

How to Compare SaaS Billing Benchmarks Before Expansion

For expansion decisions, treat payment decline rate, churn, and expansion as one system, not three separate metrics. That gives product, finance, and GTM a view they can defend before rollout resources are committed. If you own the budget call, you need that view before your team starts treating one good month as a trend.

The Best Tools for Managing Subscription Billing

**Protect cashflow by selecting for recovery and control first, then layering convenience features.**