Quick Answer

Start with credits when AI usage is volatile and you need to launch fast, then treat the model as temporary until a clearer value metric emerges. Define one credit in customer terms, not infrastructure terms, even if you map it internally (for example, 1 credit = 1,000 tokens). Before scaling, lock zero-balance behavior, overage handling, expiration, and rollover, then confirm usage events reconcile to both the credit ledger and invoices.

When Credit-Based Billing Makes Sense#

Credit-based pricing can be a useful launch model for AI, but it is not a pricing identity. Customers prepay for a pool of credits and consume them as they use the product. That works especially well in AI, where LLM consumption can swing wildly and cost is easier to observe than customer value early on. The advantage is straightforward: you get a predictable prepayment layer for an unpredictable workload. The catch matters just as much. For many teams, credits are a bridge model, not the thing that should define pricing forever.

This guide is for the people who have to carry the tradeoffs inside a SaaS business: founders, revenue leaders, product teams, and finance operators. Those groups are often balancing the same three pressures at once: growth, buyer trust, and unit economics. Credits can help when you need to launch several AI capabilities under one commercial unit instead of inventing separate pricing for each feature on day 1. The decision is rarely just commercial. It can affect packaging, metering, invoice clarity, and cash flow at the same time.

The goal is not to make credits look clever. It is to choose a model you can meter cleanly, explain in plain English, and control when usage spikes or costs drift. A direct mapping such as 1 credit = 1,000 tokens can be useful internally. It only works if buyers can also understand which actions consume credits and what balance changes to expect. The right first version protects margin now while leaving room to move later toward a clearer value metric once customer behavior stabilizes.

Examples from vendor and operator write-ups are useful as signals, not templates. Your final design should be validated against your own metering and customer behavior, not copied from someone else's packaging. One early checkpoint matters more than most teams expect: make sure usage events can be reconciled to credit burn and then to invoices before you scale the model.

A common failure mode is building a credit unit that mirrors infrastructure cost so closely that finance likes it, while customers still cannot tell what they are buying. When that happens, teams can spend months on billing work without improving customer understanding. Some vendors report poorly scoped implementations stretching into 6-12 months of custom infrastructure effort. That is exactly the kind of pricing debt you want to avoid.

Selection criteria before you pick any credit model#

Use credits when usage is volatile and value is still hard to price directly; if you already have a stable outcome-based metric, price on that outcome instead.

| Criterion | What to check | Why it matters |

|---|---|---|

| Value metric clarity | Can buyers understand what they are paying for without learning tokens, GPU time, or inference calls? | A metric can be fully measurable and still be poor pricing if it does not map to customer value. |

| Metering readiness | Can you reliably log credit-burning actions and tie them to accounts, features, and invoices? | Reconcile sample usage events to a credit ledger before launch, or disputes will shift to support and finance. |

| Margin protection | Can the model absorb volatile cost-per-token and usage spikes without constant repricing? | Credits only help if you pair them with ongoing cost monitoring and explicit controls such as quotas. |

| Buyer transparency | Can customers predict usage from common actions instead of reverse-engineering billing behavior? | If pricing reads as infrastructure language, commoditization risk rises. |

| Operational overhead | Can your team handle overages, exceptions, and contract edge cases without heavy manual work? | A simpler model often wins if operations can run it cleanly. |

Use the table as your pre-launch checklist. If any row is shaky, treat that as a launch blocker rather than something to patch later.

Set three non-negotiables in writing up front: overage behavior, credit expiration clarity, and credit rollover rules. Keep it to one page, but make sure it answers what happens at zero balance, whether unused credits expire, and whether credits carry into the next billing period.

Use one final checkpoint: if finance can explain GPU time and inference calls but sales cannot explain customer value in plain language, treat credits as a temporary model and time-box them.

If you want a deeper dive, read Credit Invoices Explained: How to Issue Reversals and Adjustments in a Subscription Billing Platform.

Best credit-based billing models for AI SaaS teams#

If you need the shortest path to launch, start with a cost-plus credit model and treat it as a bridge while you validate a stronger value metric. For other priorities, pick the model that best matches your main constraint: budgeting, packaging, messaging, or value visibility.

- Cost-plus credit model

Best when launch speed matters most and your value metric is still immature. Customers prepay for credits, consume them as they use features, and you apply margin over underlying cost. This is a common first move because AI cost signals are often clearer than value signals early on. Main upside: speed and familiar prepayment. Main risk: opacity for buyers, even when finance is comfortable with the math. Set an early review point so this does not become a permanent default by inertia.

- Seat-based credit pools

Best when you sell to teams with uneven usage across users and features. A shared pool can simplify budgeting at the account level. Main upside: one team balance instead of per-seat micromanagement. Main risk: entitlement and fairness friction if pool-draw rules are unclear.

- Hybrid pricing with subscription plus credits

Best when you already have a stable core subscription and need a variable layer for AI-heavy usage. Main upside: a base revenue floor plus usage upside. Main risk: packaging confusion if included usage, credit burn, and zero-balance behavior are not explained consistently.

- Usage-based billing with a credit wrapper

Best when your internal economics depend on detailed usage, but customers do not want to buy tokens, GPU time, or model calls directly. Credits act as a prepaid wallet tied to those underlying usage components. Main upside: you keep internal cost fidelity while simplifying the external bill. Main risk: two-layer complexity (raw usage + credit abstraction) that can confuse buyers.

- Output-anchored credit design

Best when credits can map to visible, countable deliverables. Main upside: clearer value perception for customers. Main risk: margin drift when one "output" can hide different underlying compute costs.

Simple rule: use cost-plus for speed, then move toward the model customers can predict most easily from the actions they take in your product.

Related: Fair Credit Billing Act for a Business-of-One: How to Dispute Credit Card Billing Errors.

Compare models fast and choose with explicit rules#

Pick the model you can both measure and explain. If your costs are variable but buyers still need predictable budgets, start with hybrid pricing, and only use pooled credits if your team can explain and operate them clearly. If customer value is already measurable in plain terms, move toward usage-based or output-anchored pricing.

| Model | Best for | Primary value metric | Metering dependency | Margin risk | Buyer transparency risk | Migration difficulty |

|---|---|---|---|---|---|---|

| Cost-plus credit model | Early launches when pricing is anchored to cost signals | Cost proxies (for example tokens, model calls, or GPU time) | Depends on reliable cost and usage tracking | Higher if underlying costs move faster than credit pricing | Higher when buyers cannot map credits to outcomes | Medium |

| Seat-based credit pools | Team plans that want one shared budget envelope | Team access plus shared credit consumption | Depends on seat-level and period-level usage visibility | Depends on pool design and usage concentration | Depends on how clearly pool rules are communicated | Medium |

| Hybrid pricing | Products needing both budget predictability and variable-revenue coverage | Base subscription plus variable usage or credit spend | High, because fixed and variable components must reconcile cleanly | More controlled when variable usage is priced explicitly | Usually clearer than pure credit-only pricing when plan terms are explicit | Low to medium |

| Usage-based billing with a credit wrapper | Products already metered at raw usage level but sold with simpler packaging | Raw usage translated into a prepaid credit wallet | High, because wrapper and underlying meter must stay aligned | Depends on conversion design between usage and credits | Medium if conversion logic is opaque | Medium |

| Output-anchored or outcome-based pricing | Products with visible, countable deliverables | Completed outputs or tasks | High, because outputs must map consistently to usage and cost | Depends on output variability and edge cases | Lower when buyers can easily predict what they are paying for | High |

Use three rules before launch. First, do not pick a model before you understand your cost structure; teams often fail by choosing pricing first and economics second. Second, match the model to your value proposition, cost structure, and customer preferences rather than forcing one template onto every segment. Third, treat hybrid as the default when you need subscription predictability plus consumption fairness, and remember that examples like $99/month including 10,000 calls plus $0.01 overage are design patterns, not market benchmarks.

AI pricing is still in an experimentation phase, so treat your first model as a decision you can revise, not a permanent identity.

Design a credit unit customers can trust#

If a buyer cannot quickly explain what one credit buys, your unit is still telling your internal cost story instead of the customer's value story.

- Define credits in customer language first

Start with a customer-visible action, then map it internally to GPU time, inference calls, or API requests. AI credits are usage-based units tied to AI actions, so lead with the action and keep infrastructure math in the background. Direct mappings like 1 credit = 1,000 tokens processed or time-based mappings like 1 credit = 1 minute of compute time, GPU access, or agent runtime are useful examples, not universal templates.

- Make burn logic visible for major actions

Customers should not have to reverse-engineer billing. Publish a short burn table for the actions that consume most credits, and keep the wording simple enough for finance, sales, and procurement to use consistently. Validate that usage events, balance views, and billing descriptions show the same deduction logic.

- Add guardrails before balance hits zero

Trust drops when credits disappear without clear visibility. Show remaining balance in-product, send pre-overage warnings, and state overage terms in plain language. Be explicit about what happens at zero balance and whether usage stops, moves into overage, or triggers top-up.

- Do not let internal cost mapping become the customer story

A credit unit can match your internal costs and still feel arbitrary to buyers. A single metric such as tokens or API calls often misses real differences across actions, so explain the task being purchased, not just the meter being charged. If customers can predict outcomes, credits are easier to trust. If they only see infrastructure proxies, move toward clearer usage-based billing or output-based framing.

Set policy controls before launch day#

Lock the policy stack before the first contract goes live. If you leave these rules to support judgment or sales promises, the same issue gets different answers and customer trust drops.

| Control area | What to define | Why it matters |

|---|---|---|

| Lock one policy package | State whether credits expire, whether unused balance rolls into the next billing period, whether credits are pooled at account or user level, and which features can draw from that balance. | Customers experience one reality: what they can use, when they can use it, and who can use it. |

| Define exception paths like accounting entries | Define who approves each case, what evidence is required, whether the fix restores credits, refunds cash, or adjusts future usage, and how the reason is recorded. | Handle disputes, reversals, and goodwill credits with explicit workflows, not one-off favors. |

| Draw hard transfer boundaries | Be explicit about when credits can move across users, features, and billing periods, and when they cannot. | Clear boundaries keep balances fair and predictable. |

1. Lock one policy package#

Treat credit expiration policy, credit rollover policy, credit pooling, and entitlement management as one package, not separate toggles. Customers experience one reality: what they can use, when they can use it, and who can use it.

Publish a short policy matrix by plan or contract. State whether credits expire, whether unused balance rolls into the next billing period, whether credits are pooled at account or user level, and which features can draw from that balance. Keep the language consistent across the order form, in-product balance view, and invoice description.

Make this a launch checkpoint. Run real-time test usage, check balances before compute is allowed, and confirm the live balance and usage report follow the same policy logic.

2. Define exception paths like accounting entries#

Handle disputes, reversals, and goodwill credits with explicit workflows, not one-off favors. Define who approves each case, what evidence is required, whether the fix restores credits, refunds cash, or adjusts future usage, and how the reason is recorded.

Record exceptions in append-only ledgers for auditability, and enforce idempotency so retried events do not apply the same credit adjustment twice. Support should be able to point to the ticket, usage event IDs, invoice reference, and timestamped ledger entries that explain exactly what changed.

3. Draw hard transfer boundaries#

Be explicit about when credits can move across users, features, and billing periods, and when they cannot. This matters most in seat-based pools or hybrid pricing, where teams often assume different entitlement rules.

Define ownership first, then movement. Decide whether credits belong to a named user, a workspace, or the full account, then test edge cases like seat adds/removals, feature downgrades, renewals, and billing-period changes. Clear boundaries keep balances fair and predictable.

This clarity is also a trust control. Finance teams may like credits because they map cleanly to spend and cash flow, while customers often find credits unclear. Short, visible, consistently enforced policy rules make the model easier to defend.

You might also find this useful: Subscription Billing Platforms for Plans, Add-Ons, Coupons, and Dunning.

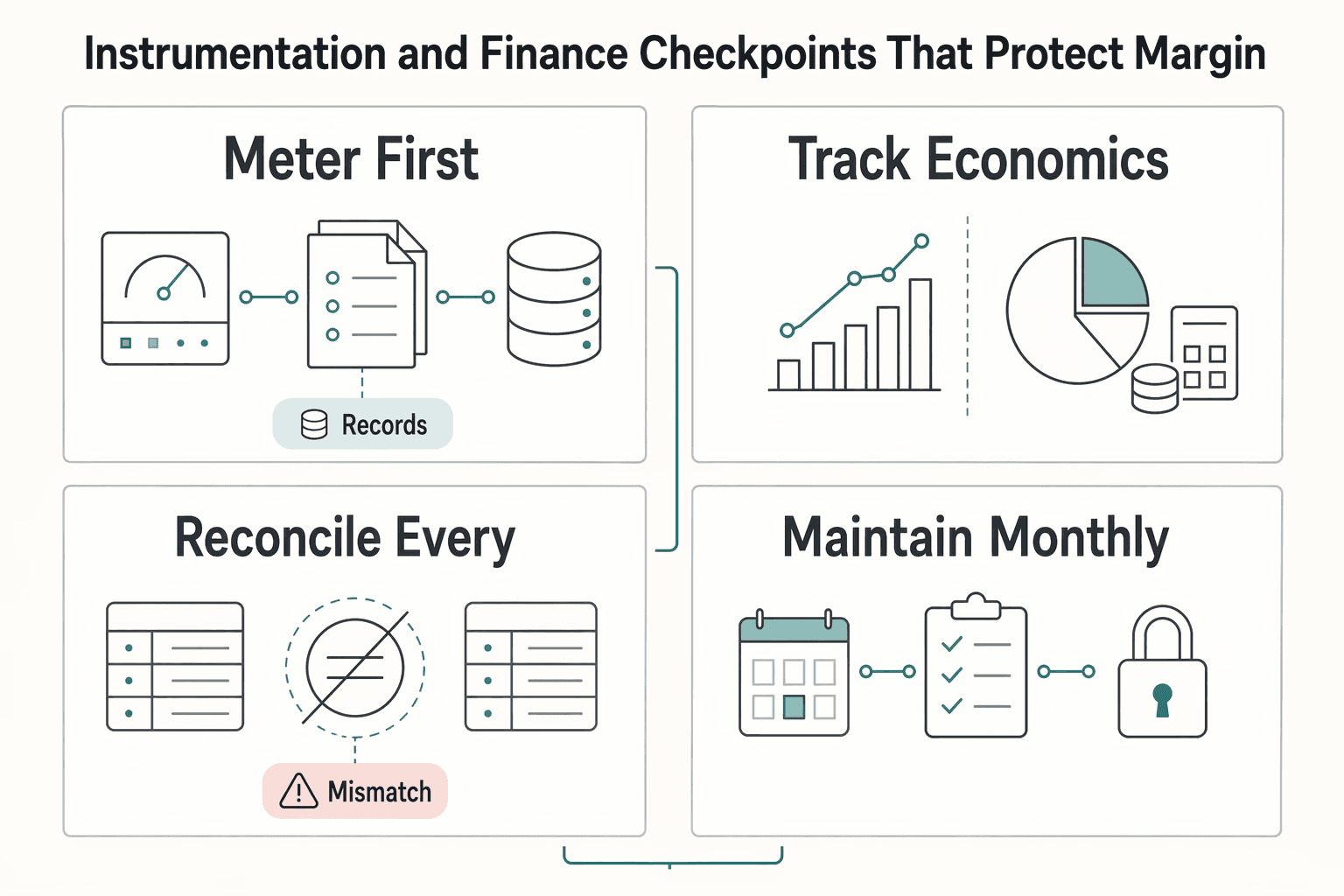

Instrumentation and finance checkpoints that protect margin#

Once policy is set, margin protection comes down to control consistency: instrument first, reconcile second, automate last. In AI billing, accuracy alone is not enough. Finance, compliance, and leadership still need to understand how outcomes were produced and why decisions were made.

| Checkpoint | What to do | Why it matters |

|---|---|---|

| Meter first, automate second | Instrument credit-burning actions before automated billing posts invoices or enforces balances, then validate reconciliation, then enable automation. | If you invert that order, you end up debugging billing outcomes after money movement and trust drops fast. |

| Track economics at feature level | Break out usage and billed credits by feature or major action so drift is visible early. | Account totals can hide margin pressure in a single AI workflow. |

| Reconcile every cycle | Verify that metering totals, invoice totals, and credit-ledger movements align. | If variance is unresolved, pause release decisions until you can explain which record is correct and why. |

| Maintain a monthly pricing health pack | Keep burn patterns, top credit-consuming actions, exception volume, dispute themes, and model-change recommendations. | Watch for rising overage disputes, a widening gap between LLM consumption and billed credits, frequent manual adjustments, and Shadow AI. |

- Meter first, automate second.

Instrument credit-burning actions before automated billing posts invoices or enforces balances. Get the metering records consistent enough to explain what happened, validate reconciliation, and only then enable automation. If you invert that order, you end up debugging billing outcomes after money movement and trust drops fast.

- Track economics at feature level, not only account level.

Account totals can hide margin pressure in a single AI workflow. Break out usage and billed credits by feature or major action so drift is visible early. If one workflow consumes more LLM capacity without matching billed credits, adjust that workflow directly before blended reporting hides the issue.

- Reconcile metering, invoices, and credit ledgers every cycle.

Make reconciliation a formal checkpoint each billing cycle. Verify that metering totals, invoice totals, and credit-ledger movements align, and check that controls were applied consistently across systems. If variance is unresolved, pause release decisions until you can explain which record is correct and why.

- Maintain a monthly pricing health pack and treat red flags as early warnings.

Keep a recurring operator artifact with burn patterns, top credit-consuming actions, exception volume, dispute themes, and model-change recommendations. Watch for rising overage disputes, a widening gap between LLM consumption and billed credits, and frequent manual adjustments in billing operations. Also watch for Shadow AI (unapproved internal AI usage), because undocumented tool usage can weaken explainability, documentation, and governance in billing workflows.

Related reading: How Independent Experts Use France's CIR Tax Credit Without Overclaiming.

Plan the migration from launch credits to durable value pricing#

Launch credits should stay temporary unless customers still find them clearer than the value they are buying. Plan migration triggers early, then move by segment instead of forcing a single cutover.

- Set migration triggers before pressure builds.

Use your monthly pricing health pack as the checkpoint. Practical triggers include stable usage cohorts across billing cycles, a value metric your team can explain clearly, and repeated customer feedback that credits feel opaque. If finance can reconcile usage but buyers still cannot predict bills, that is a strong signal to revisit the model.

- Transition by segment, not all at once.

Keep legacy credit terms for existing contracts that already budget around credits, and test value-linked packages with new cohorts first. This lowers contract friction and gives cleaner reads on conversion, expansion, and dispute rates. Avoid changing segment and packaging at the same time, or you will not know what caused the result.

- Shift toward the metric buyers understand best.

Usage-based pricing charges after consumption and tends to fit simpler products with one clear metric, while credit-based pricing can fit more complex multi-feature products. If credits still improve spend clarity for part of your base, keep them there. If not, a hybrid model can combine credit-driven predictability with usage-based flexibility during the transition.

- Frame the change as clarity and trust, not extraction.

Show side-by-side bill examples for the same behavior under the old and new models, including assumptions. This is especially important in a market where monetization fit is still unsettled: in one cited survey of 614 CFOs, 68% said their current pricing model no longer works. Buyers move faster when they can see how the change improves predictability and fairness.

For a step-by-step walkthrough, see A Deep Dive into the Foreign Tax Credit (Form 1116).

Conclusion#

Use credits to launch quickly, but do not mistake them for your final pricing identity. They often work best as a bridge: useful early, and worth keeping only if trust, margin, and metering stay healthy.

-

Start with credits when speed matters more than pricing purity. A credit model gives you a middle ground between flat-rate packaging and pure pay-as-you-go, which is why early teams often use prepaid credits to get usage monetization live with more predictability and some upfront cash flow. The discipline is what matters. If you cannot explain one credit as a defined unit of value in plain customer language, you can still launch, but you should label the model as temporary and set a review point every billing cycle.

-

Earn buyer trust with controls, not messaging. Credits are deducted in real time as services are consumed, so the customer experience can break when usage feels invisible. Put in real-time tracking, pre-compute balance checks, and an append-only ledger before volume climbs, then verify each cycle that metering totals, invoices, and the credit ledger reconcile cleanly. Transparency is not optional. Poor visibility is a known trust failure mode, especially when credits seem to disappear faster than customers expected.

-

Decide in advance what would make you leave the model. Credits help when the product is young, but even supporters of prepaid credits note that the simplicity can strain at enterprise scale. Your migration triggers should be explicit: repeated complaints that credits are opaque, recurring trust issues tied to unclear usage visibility, or ongoing reconciliation strain between metering and billing. The point is not to wait for a pricing crisis. Watch metering accuracy, feature-level margin, and buyer confidence on a fixed cadence, then move new cohorts first when a clearer value metric is ready.

If you are still unsure, use one simple rule. When your team cannot yet explain the value metric cleanly, use credits deliberately, instrument deeply, and make burn logic clear for major actions. When customers understand outcomes better than credits, start testing alternatives and keep legacy credit terms where they still reduce friction.

That is the real test. It is not whether credits are clever. It is whether they buy you time to learn without hiding the signals you will need to price better later.

Frequently Asked Questions

What is credit-based billing in AI, and when does it make sense?

Credit-based billing uses credits as the core usage and billing unit. Netlify, for example, publishes a dedicated FAQ for billing on its credit-based pricing plans. It can make sense when AI actions have uneven compute and you need one simpler unit buyers can understand. Postman, for example, says every AI-powered action in Agent Mode uses credits based on the amount of compute required. Teams often use it early when internal cost signals are clearer than long-term value metrics.

Why do AI SaaS teams start with a cost-plus credit model?

Many teams start here because it can ship faster than pricing each feature or outcome directly. You can package volatile AI costs into simple plan allowances, such as 50 credits per user/month on Postman Free or 400 on Solo, without exposing internal infrastructure detail. The tradeoff is that a model built around cost can become harder to explain once customers want bills tied to visible value.

How do seat-based credit pools work in practice?

A seat-based pool gives each seat an allowance, then lets the team consume from one shared bucket. Postman Enterprise (v12) shows the pattern with 800 per user/month, pooled across the team, then $0.035 per credit once included usage is exhausted. Watch entitlement rules and alerting closely, because one heavy user can burn through shared credits before the rest of the team notices.

Are credits better for buyers or vendors?

Neither side wins by default. Buyers can benefit when credits make budgeting easier or when some actions are billed at discounted credit rates, while vendors can benefit when paid plans automatically move to pay-as-you-go billing after included credits are used. If neither side can predict what a normal month should cost, credits are probably masking a pricing problem rather than solving one.

Should credits expire, and how should rollover be handled?

There is no universal expiration or rollover rule in the sources here, so do not treat any one policy as standard. The practical requirement is clarity: define expiration, rollover, pooling limits, and whether credits can move across users, features, or billing periods before launch. If you cannot explain those rules cleanly in your pricing page and order form, expect disputes.

How do you make credit usage transparent enough to avoid billing surprises?

Make usage visible where the customer already works. Postman gives teams a concrete path, Team Settings → Resource Usage → AI Credit Details, to view AI credit usage and accrued pay-as-you-go costs, and it deducts credits when an AI action completes. Publish burn logic for major actions, add remaining-balance and pre-overage alerts, and verify each billing cycle that the usage view matches the invoice and credit ledger.

When should a company move from credits to usage-based billing or outcome-based pricing?

Move when customers trust the direct metric more than the wrapper. Good triggers are repeated complaints that credits feel opaque, or stable usage cohorts that make a clearer value metric forecastable. If that is where you are, test the new model on new accounts first and keep legacy credit terms for existing contracts. A Guide to Usage-Based Pricing for SaaS is a useful next step.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- congress.gov/117/bills/hr7900/generated/BILLS-117hr7900pc...trusted

- ecfr.gov/current/title-12/chapter-II/subchapter-A/par...trusted

- occ.gov/news-issuances/news-releases/2026/nr-ia-2026...trusted

- scholarship.law.gwu.edu/cgi/viewcontent.cgitrusted

- scholarship.law.umn.edu/cgi/viewcontent.cgitrusted

- blulogix.com/ebooks-whitepapers/50-financial-intelligence...external

- finops.org/wg/finops-for-ai-overviewexternal

- flexprice.io/blog/how-to-implement-credit-based-billing-f...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

SaaS Usage-Based Pricing for Predictable Cashflow and Fewer Disputes

If you are considering **saas usage-based pricing**, treat it as an operations and collections decision first. Pricing works best when the usage unit can be measured, shown on the invoice, and explained by someone outside your product team.

Credit Invoices Explained: How to Issue Reversals and Adjustments in a Subscription Billing Platform

Once volume grows, credit invoices, invoice reversals, and invoice adjustments stop being simple billing edits. They become order-to-cash events that affect customer balances, accounts receivable, accounting records, payment matching, and sometimes fund finalization on a different timeline. The practical mistake is treating them like one back-office task when they are really several linked records that have to stay in sync.

Usage-Based Billing for B2B SaaS Platforms That Teams Can Operate

Usage-based billing works best when customer value rises with measurable consumption rather than with a fixed license. It can improve pricing fit, but only if pricing logic, billing data, and finance controls are designed together from the start.