Quick Answer

Start with a controlled model: define payout-ready rules, release through scheduled Payout Batches, and scale only after reconciliation is stable. In this edtech marketplace payout case study, the practical sequence is prerequisites, model choice, end-to-end money mapping, compliance gates, phased rollout, and close evidence. The article stresses that payout timing affects margin and exception load, and uses the FTC’s Chegg enforcement as a warning to connect cancellation and refund behavior directly to release logic.

Why instructor payouts became a scaling issue#

Step 1. Start from the real tradeoff#

Fast instructor payouts help only if you can still protect margin, controls, and trust. This case study looks at how an EdTech marketplace can expand instructor access to earnings with Gruv without turning refunds, compliance holds, and reconciliation work into finance pain later.

That is the tension most teams feel in practice. Instructors want quicker access to earned funds, product wants a stronger supply story, and finance wants proof that money was collectible, refundable when needed, and released under the right rules. Move too fast on payout timing and you can end up fronting working capital, increasing exception handling, or paying out before a cancellation or refund is reflected in the ledger. Move too slowly and supply trust erodes, making payouts a drag on growth.

Step 2. Bound the evidence honestly#

The evidence base in edtech is not as clean as many case studies suggest. A Stanford source reports edtech investment grew by more than forty-fold over the last decade. Yet only 11% of education decision makers were looking at any type of evidence when purchasing tools, and only 7% of global edtech tools had any form of rigorous evidence. That is a useful warning for this piece. Expect grounded operator logic, not invented certainty.

So the scope here is deliberately narrow. We use the public signals above and what the Federal Trade Commission said in its September 15, 2025 announcement involving Chegg. We avoid product-specific architecture, payout metrics, and internal outcome claims that are not publicly established. Where a detail is unknown, it stays unknown.

Chegg matters here for one practical reason. Payout design cannot be separated from subscription, cancellation, and refund behavior. In that 2025 announcement, the FTC said Chegg would pay $7.5 million to settle allegations tied to cancellation practices, including allegations that it failed to provide a simple mechanism to cancel auto-renewing subscriptions. The practical takeaway is simple: do not design instructor release timing as if downstream reversals and consumer protection obligations belong to some other team.

Step 3. Follow the build order#

The rest of this guide follows the order a careful operator would use in production. First, define prerequisites such as current payout cadence, refund lag, compliance checks, and ownership boundaries. Then choose the payout model that fits your margin profile, map the money movement path end to end, and set release gates before any funds go out.

From there, we move into implementation order, failure recovery, and the evidence pack finance should require before scale. As you read, focus on two things: the rules that prove an instructor is actually payout ready, and the failure modes that force returns, holds, or manual review. The article ends with a copy-and-paste launch checklist you can turn into a real rollout plan.

What to prepare before changing payout logic#

Treat payout speed as a finance-and-controls decision, not only a product decision. Before you change logic, align on four basics: a baseline pack, an early policy-and-market review, clear ownership, and a strict definition of when an instructor account is payout ready.

Step 1. Measure your baseline. Capture your current payout cadence, failed payout rate, refund lag, and the effort finance spends on close. Keep it operational: one source of truth, one date range, and one owner per metric. If product, payments ops, and finance cannot point to the same numbers, a payout-logic change is likely to mask issues instead of fixing them.

Step 2. Do the research before build. Run a needs assessment and map where KYC, KYB, AML, and VAT checks may apply across your markets before touching integrations. Keep the goal practical: identify where extra review may be needed, which account types may need more documentation, and who approves go-live by corridor. This is the stage teams often skip; procurement guidance warns against jumping straight to a preferred option, and Johns Hopkins research reported needs assessments were rarely conducted.

Step 3. Assign ownership across systems. Name owners for integrations, webhooks, payout exceptions, and finance-facing evidence. Make escalation explicit so failed payouts and replayed webhooks have a clear investigation and sign-off path.

Step 4. Lock non-negotiables up front. Define required audit-trail depth, acceptable idempotent retry behavior, and the exact account-level checks behind "payout ready." Keep manual overrides controlled and documented so you do not create reconciliation debt from day one.

Need the full breakdown? Read How EdTech Platforms Pay Instructors Globally: Compensation Models, Payout Controls, and Reconciliation.

Choose the payout model that fits your margin profile#

Choose your payout model based on margin tolerance and control maturity, then optimize for speed. The goal is to improve instructor experience without quietly increasing reversal, exception, and reconciliation risk.

Step 1. Compare the three payout models before you promise speed#

Use a side-by-side view to make the tradeoffs explicit before launch.

| Payout model | Margin pressure | Ops burden | Instructor experience | Better fit when |

|---|---|---|---|---|

| Instant payout | Can be higher because funds may leave before some issues surface | Can be higher due to faster exception handling | Fastest access to earnings | Controls are mature and edge-case handling is already stable |

| Scheduled Payout Batches | Often more controlled because release happens on a set cadence | More predictable review and reconciliation flow | Predictable if cadence is clear | You want consistency and review time before release |

| Thresholded Payout Batches | Can reduce frequent low-value disbursements | Adds rule and support complexity | Mixed, depending on rule clarity | You want fewer small payouts and can explain thresholds clearly |

A practical check: finance, product, and ops should each be able to explain why a payout was released, held, failed, or returned without relying on ad hoc spreadsheets.

Step 2. Set release criteria before you expand faster options#

If payout outcomes are still noisy, use a controlled release pattern first and tighten eligibility criteria. Then test faster release on a narrow cohort rather than changing every instructor at once.

Keep the evidence trail explicit: batch approvals, included accounts, and status history for held, released, failed, or returned amounts. Faster payouts can support growth, but they also move timing risk and exception work into daily operations.

Step 3. Align take-rate decisions with payout timing risk#

Payout timing affects unit economics, not just user experience. When release happens earlier, your pricing may need to absorb additional review effort, exception handling, and temporary funding exposure.

On Gruv, teams usually segment who gets faster release and who stays on standard Payout Batches until outcomes are more predictable. Keep the rollout tied to controls and traceability, not just demand for speed.

Design the money movement path end to end#

Lock the sequence before you add speed: collect funds, post ledger records, confirm payout eligibility, then release through Gruv and track status. When that order breaks, reconciliation turns into manual cleanup.

Step 1. Map the release path in the same order money and evidence move#

Treat payouts as four controlled stages, not one action:

- Collect learner funds.

- Post internal ledger entries for received funds, platform revenue, and instructor-payable amounts.

- Validate payout readiness and market-specific gates.

- Release via Gruv and record outcome updates.

For every instructor payment, keep one traceable chain: source transaction, ledger entry IDs, eligibility decision, and release record. If you use Virtual Accounts or routing features where supported, keep collection and disbursement records distinct so retries, returns, and reconciliation stay explainable.

Step 2. Define statuses and retry rules before launch#

Use a short shared state model and assign clear ownership per state. A practical set is: credited, held, returned, paid, failed. Map inbound events into those states instead of letting each webhook create new business meanings.

Handle retries and replays as normal operating conditions. Use idempotency on release requests, and only update balances when events match known transactions or payout instructions. Test this before go-live by replaying the same request and webhook and confirming balances and ledger outputs do not duplicate.

| Lifecycle stage | Event source | System owner | Evidence output | Reconciliation checkpoint |

|---|---|---|---|---|

| Funds collected | Checkout or payment provider | Payments ops | Provider transaction reference, collection timestamp | Total collected matches open learner orders |

| Ledger posted | Internal ledger service | Finance engineering or product | Entry IDs for gross amount, fee, and instructor payable | Ledger payable matches collected less platform revenue and holds |

| Eligibility validated | Compliance and payouts logic | Payments ops | Approval or hold record, account status, review timestamp | Only payout-ready balances move to release queue |

| Payout released and updated | Gruv plus inbound event handling | Payments ops and finance | Release ID, provider reference, final status, return or failure record if any | Total released plus held plus returned equals approved payable balance |

Step 3. Insert Australia checkpoints before cross-border release#

For Australia, add tax-readiness checks before scaling release. If GST registration is required, registration is due within 21 days. For non-resident businesses, the ATO lists multiple GST registration pathways, including standard registration for entities entitled to or holding an ABN; under standard registration, BAS lodgment and GST payment are monthly or quarterly.

Before broad rollout, confirm three items in your process: whether Australian GST registration is required, which pathway applies, and whether your evidence is complete. Also plan for the operational constraint that non-residents may not be able to lodge electronically from outside Australia and may need an Australian registered tax agent. If that dependency is unresolved, keep rollout controlled.

Do not base tax-flow decisions on archived community threads that may be outdated. Related reading: How EdTech Platforms Pay Tutors: Tax and Payout Architecture.

Set compliance and trust gates before payout release#

Treat payout release as blocked by default until compliance checks, refund exposure checks, and tax-onboarding checks are complete and recorded. That keeps payout decisions defensible later, not just operationally convenient in the moment.

Step 1. Encode payout readiness as explicit machine rules#

Do not keep "ready to pay" in spreadsheets or inboxes. Store a small, explicit set of release checks in your application and require all of them to pass before funds move.

For every released payout, keep the status values and decision timestamp that were true at release time. If you cannot reconstruct that state, your gate is not reliable, and manual exceptions can become audit risk.

Step 2. Tie cancellation and refund policy to payout holds#

Your payout timing should match what learners were promised at checkout and in support policy. If a valid cancellation or refund is still open, hold the related payable until that exposure is resolved.

Make the hold reason visible in your ledger, and keep traceability from refund to original order, payable adjustment, and affected payout release.

Step 3. Document market and education obligations before enabling release#

If a corridor depends on education or privacy obligations, turn that policy position into concrete release flags before broad launch. EdTech operates in a multi-stakeholder environment that often includes regulators, so policy ambiguity quickly becomes payout risk.

The Utah EdTech investigation also frames oversight through "Regulations, Policies, Contracts, and Agreements," which is a practical reminder to map obligations before scale.

Step 4. Keep tax readiness and classification review in the same release gate#

Collect required tax records during onboarding and store completion status in the same gate used for other release checks. This avoids year-end reconstruction and reduces preventable payout exceptions.

Keep classification review separate and explicit. Misclassifying a worker as an independent contractor creates legal and audit risk, and while contractors are generally responsible for their own payroll taxes, your release logic should still require complete tax and classification checks before payout. Related: How a Legal Marketplace Modernized Trust Accounting Compliance.

Implement in phases without breaking finance operations#

Roll out payout changes in narrow phases so issues stay diagnosable and finance can reconcile cleanly.

Step 1. Launch one corridor and one instructor segment#

Start with one payout corridor and one instructor segment using Gruv APIs and conservative Payout Batches. Keep the first cohort simple enough that your team can clearly trace release decisions, batch membership, and ledger outcomes.

Keep a manual review fallback active from day one. If a status is unclear, route it out of the batch and resolve it before release.

Step 2. Expand only after the pilot produces clear operating evidence#

Expand only after the pilot is stable in production, not just successful in a short test window. The same pattern appears in edtech adoption guidance: start small with supportive partners, then expand, and rely on operating evidence rather than assumptions.

Before widening access, confirm webhook handling, retry safety, and exception routing are consistently managed by named owners. If exceptions still depend on ad hoc chat or spreadsheet cleanup, hold expansion.

Step 3. Automate finance evidence before scale#

Automate finance exports before broader rollout so month-end close does not depend on manual reconstruction. Keep payout approvals, batch traces, timestamps, hold context, and ledger links easy to retrieve.

Do not expand rails and geographies in the same sprint. Sequence one risk dimension at a time so failures remain diagnosable and finance operations stay controlled.

For a step-by-step walkthrough, see Embed Financing Options in Your Marketplace with Instant Payout Economics.

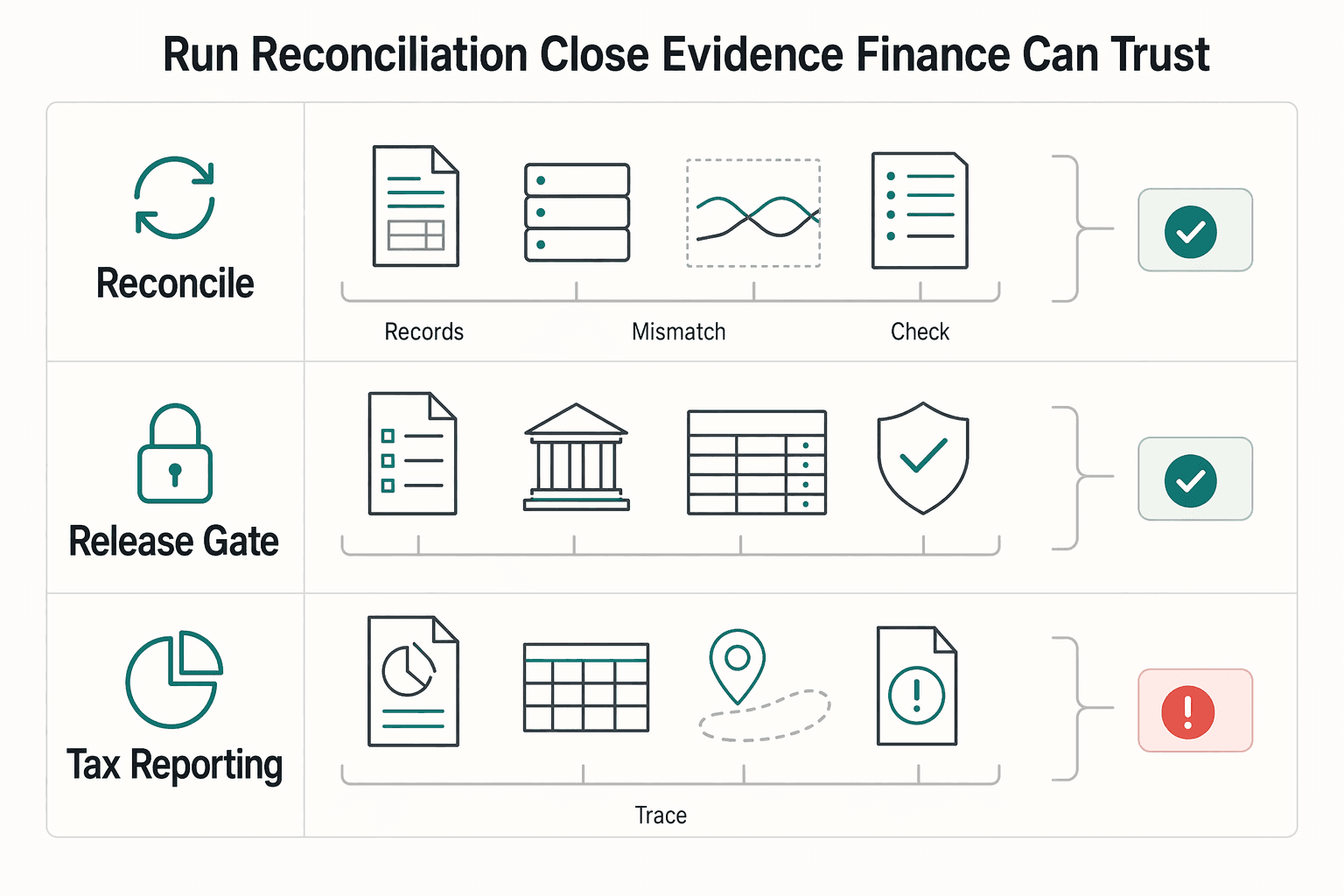

Run reconciliation and close with evidence finance can trust#

Close is production-ready only when finance can trace every batch from approval to final status without engineering intervention.

| Close control | What to confirm | Evidence kept |

|---|---|---|

| Weekly reconciliation pack | Keep one weekly reconciliation pack per payout batch | Submitted payout file, provider reference/transaction ID, ledger postings before and after release, unresolved exceptions tied to that batch |

| Three-way reconciliation | Reconcile total collected vs total payable vs total paid at batch level and confirm the roll-up to the ledger | Held and returned items explicit, not buried in net numbers, if Virtual Accounts are used |

| Dual sign-off | Payments ops signs event integrity; finance signs accounting completeness | Complete outcomes, safe retries, no duplicate effects, clear final state for credited/held/returned/paid/failed items, postings present, exceptions disclosed, audit trail sufficient |

| Tax/reporting continuity | Protect tax/reporting continuity where enabled | Preserve payout dates, amounts, payee identity, and corrections so reporting does not break on returns, reissues, or partial holds |

- Keep one weekly reconciliation pack per payout batch.

For each batch through Gruv, keep a single evidence set with the submitted payout file, provider reference/transaction ID, ledger postings before and after release, and unresolved exceptions tied to that same batch. The standard is simple: starting from a batch ID, finance and ops can trace every line item end to end without log digging or chat archaeology.

- Run a three-way reconciliation and isolate held/returned items.

Reconcile total collected vs total payable vs total paid at batch level, then confirm the roll-up to the ledger. If you use Virtual Accounts, held and returned items should be explicit, not buried in net numbers, so finance can explain why collected funds did not become paid funds in-period.

- Require dual sign-off before close.

Payments ops signs event integrity: complete outcomes, safe retries, no duplicate effects, and a clear final state for credited/held/returned/paid/failed items. Finance signs accounting completeness: postings present, exceptions disclosed, and an audit trail that is sufficient. One approver for both creates a control gap.

- Protect tax/reporting continuity where enabled.

Support for FEIE, FBAR, and Form 1099 depends on durable records, not payout-engine tax decisions. FEIE applies only to qualifying individuals who report the income on a U.S. return, and qualification can depend on tests such as 330 full days in a 12-month period; your data path should preserve payout dates, amounts, payee identity, and corrections so reporting does not break on returns, reissues, or partial holds.

Common mistakes and how to recover fast#

Fast recovery starts with one principle: do not treat disclosure as a substitute for real protections in your payout rollout decisions.

- Mistake: relying on a notice-and-choice approach as the primary control.

Recovery: put substantive protections first, and keep disclosures as supporting context.

- Mistake: assuming user-facing messaging is enough when flows can still steer behavior.

Recovery: review for manipulative dark patterns and remove them before scaling.

- Mistake: treating risk as resolved because disclosures were shown.

Recovery: test decisions against unfairness risk, not just whether terms were displayed.

If a process is hard to defend without pointing to disclosures, it is not ready. The Stanford Law Review feature describes a shift away from disclosure-only frameworks toward substantive protections, including recent FTC action targeting manipulative dark patterns.

Conclusion#

If the failure paths are clear, the launch decision gets much simpler: expand payouts only when product, finance, and compliance are working from the same rules. In education, that matters more than teams often admit. The Utah EdTech investigation frames review around regulations, policies, contracts, and agreements, including COPPA and FERPA, so payout expansion cannot be treated as a product-only speed project.

The education sources behind this piece support that governance point, and they also warn against weak evidence discipline. In a Johns Hopkins procurement study covering stakeholders from 54 school districts and vendors from 47 ed-tech companies, decisions were often made on pilot tryouts and peer references, while needs assessments were rare. That is a useful closing warning for payout work too: do not scale because one batch looked fine once.

The checklist below is for internal payout operations validation; it is not a set of payout mechanics established by the education studies.

- Confirm the payout model and unit-economics assumptions by instructor segment.

Write down which segments get scheduled payout batches, which stay on hold-based release, and where refunds or reversals may change economics. Your verification point is simple: for each segment, someone in finance can explain collected, payable, and paid timing without opening a chat thread.

- If your program requires KYC, KYB, AML, and refund or cancellation release rules, lock them before go-live.

The exact rule design is jurisdiction-specific and should be approved internally, not improvised during rollout. A red flag is any launch plan that says you will "handle exceptions manually for now" without a written override path and decision log.

- Validate API idempotency and webhook replay handling in production-like tests.

These controls are implementation checks you need to prove in your own environment, not something the education sources validate for you. The checkpoint is that a retry or replay does not create an extra payout event.

- Run a reconciliation dry run with real payout batches and the evidence outputs you expect at close.

Use a batch large enough to include normal items, held items, and at least one exception path. If your team cannot tie the batch back to internal records, approvals, and unresolved exceptions before launch, you are not ready to promise broader coverage.

- Expand by corridor only after stability and policy adherence are verified.

Add one corridor, observe it through real operating cycles, then decide whether the controls held under normal load and edge cases. If a new market also changes compliance interpretation, tax handling, or customer contract terms, sequence that separately so you can still diagnose what caused a break.

That is the real takeaway from this case study: speed is useful, but only after you can prove control, evidence, and policy fit at the same time.

Frequently Asked Questions

What should an edtech marketplace payout case study include to be credible?

A credible case study should show evidence, not just a smoother user story. In edtech more broadly, evidence use is thin: one Stanford report said only 11% of education decision makers looked at any evidence, and only 7% of global tools had rigorous evidence. For payouts, document your baseline and post-launch results clearly so reviewers can verify what changed.

How do instructor payout timing choices affect margin and cash conversion?

Treat timing as a tradeoff to validate with your own data, and compare collected, payable, and actually paid amounts by batch before promising faster release.

Which payout model is usually best for cross-border instructor payouts?

There is no universal winner, and the source pack does not support a single ranked answer. In a marketplace model, transactions occur between learners and multiple instructors. Beyond that model definition, these sources do not validate one cross-border payout approach as best.

What compliance controls are table stakes before releasing instructor payouts?

One grounded principle is clear: for online course payments, privacy, compliance, and risk management are not optional extras. Any release controls should be defined with your legal and compliance owners.

How should refunds and cancellations flow back into instructor balances?

Keep the process auditable: record the adjustment in your system of record and ensure it can be traced back to the original earning event.

What is the minimum reconciliation evidence pack finance should require?

A practical baseline is to retain payout exports, provider references, internal postings, and exception/override records so collected, payable, and paid totals can be reconciled without guesswork.

When should a team use scheduled Payout Batches instead of faster payout options?

The sources here do not rank scheduled batches versus faster options. They do distinguish marketplace behavior from subscription model behavior, where regular payments for access to a course library differ from transactions between learners and multiple instructors, so model structure should inform your payout design and reconciliation checks.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ato.gov.au/businesses-and-organisations/international-t...trusted

- ato.gov.au/businesses-and-organisations/gst-excise-and-...trusted

- community.ato.gov.au/s/question/a0J9s0000001Dmq/p-00029303trusted

- files.eric.ed.gov/fulltext/ED458210.pdftrusted

- files.eric.ed.gov/fulltext/ED603521.pdftrusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- ftc.gov/news-events/news/press-releases/2025/09/ed-t...trusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How a Healthcare Staffing Platform Improved Payout Reliability with Gruv

Treat this as a monetization and operations question first. The question is whether a staffing platform could make payouts more dependable with Gruv while keeping margin intact after support load, exception handling, and reconciliation work are counted.

How a Legal Marketplace Modernized Trust Accounting Compliance

Trust accounting is often treated as a compliance topic, but for a legal marketplace it is also an economic decision. When money movement and control are unclear, operating friction rises and pricing pressure gets harder to manage.

How a Logistics Platform Scaled Driver Payouts Across Southeast Asia

Redesigning driver payouts is rarely just a payments project. For a logistics platform, it is often a margin decision hiding inside an ops problem. Do you fix driver uncertainty first, settlement speed first, or manual finance work first?