Quick Answer

Yes, a platform can sometimes launch payouts without its own Money Transmitter License (MTL), but only when the operating model, partner boundaries, and retained obligations are documented and tested. The article recommends deciding model choice before build, mapping licensing-trigger activities by jurisdiction, and assigning named owners for AML, KYC, sanctions, and exceptions. It also requires a signed evidence pack and pre-launch failure testing before first third-party payouts.

How Platforms Handle Payouts Without Holding Funds#

Fast payouts are not the hard part. The hard part is deciding, early enough, whether your product and fund flow create money transmission risk before you scale contractor, seller, or creator payments.

Step 1. Name the real tension#

If you own compliance, legal, finance, or risk, you are usually balancing two valid pressures. Product wants a fast launch and broader payout coverage. The business may also see embedded payments as a revenue stream. But once your platform starts facilitating transfers for other parties, weak licensing assumptions can create compliance risk and partner friction as banks or processors review the flow more closely.

That tension gets sharper because a money transmitter is generally understood as an entity that facilitates fund transfers, including across borders. For a platform, the real mistake usually starts earlier, before anyone says, "we should have gotten a license." It starts when you build the flow before anyone pins down who receives funds, who holds them, who instructs movement, and which party in the chain is the regulated one.

This guide is here to help you launch with the right operating model for now, instead of jumping too early to a full Money Transmitter License (MTL) path or assuming a partner integration solves the issue by itself. Many platforms are weighing those same two broad options: becoming money transmitters themselves or partnering with regulated institutions.

So the working question is not "how do we avoid licensing forever?" It is "how do we make a documented, defensible first decision?" Then set clear triggers for when that decision has to be revisited. If you are trying to build a payout network without your own license, use that standard. You want speed, but you also want explicit escalation points for new jurisdictions, new payout types, cross-border routes, or any change in who touches funds.

Before design starts, use one simple checkpoint. Make sure someone can state, in one sentence, your current licensing assumption and the exact partner-role boundary. If no one can do that, you are not ready to treat the payout flow as low risk.

Step 2. Draw the boundary#

This is an operator guide to decision quality and control ownership, not legal advice. That limit matters because outcomes vary by jurisdiction, product design, and partner structure, especially once you move beyond a single domestic use case. These laws can feel intimidating, which is exactly why undocumented assumptions tend to fail later.

Use this article to tighten classification, evidence, and launch controls. For the final call on licensing position, rely on qualified counsel and your regulated partners. Then keep the assumptions in writing so you can test them as the product changes.

Related: How to Get a Money Transmitter License State by State Without Cost Surprises.

What to prepare before you design payout flows#

Do the classification work before product design, not after. If you launch a payment rail before legal assessment, you create enforcement and launch risk that is much harder to unwind, so reduce ambiguity before anyone starts wiring payout logic.

| Prep step | What to capture | Key note |

|---|---|---|

| Define use-case mix in writing | Document each flow, payer, payee, and jurisdiction | State where the current licensing assumption applies |

| Map every funds-movement touchpoint | Record who receives funds, holds them, instructs movement, and can pause, reroute, or return funds | Do not let documentation say a partner controls funds if your operating flow gives your team intermediary-like control |

| Collect partner model facts early | Confirm partner terms, onboarding requirements, and exact control boundaries | If roles and responsibilities are unclear, pause before launch planning |

| Assign approval owners now | Legal approves classification assumptions; Compliance owns control scope; Finance owns reconciliation and reporting evidence | Verify web-summary conclusions against an official edition before treating them as launch-ready |

- Define your use-case mix in writing. Separate flows where payments are an add-on to your product from flows where moving money is the core service, and document each payer, payee, and jurisdiction.

Checkpoint: one page stating what each flow does and where your current licensing assumption applies.

- Map every funds-movement touchpoint. For each step in your payment rail, record who receives funds, who holds them, who instructs movement, and who can pause, reroute, or return funds.

Failure mode: your documentation says a partner controls funds, but your operating flow gives your team intermediary-like control.

-

Collect partner model facts early. Confirm partner terms, onboarding requirements, and exact control boundaries before design is finalized. If roles and responsibilities are unclear, pause and resolve them before you plan the launch.

-

Assign approval owners now. Legal should approve classification assumptions, Compliance should own control scope, and Finance should own reconciliation and reporting evidence. If anyone relies on web summaries for legal research, verify conclusions against an official edition before treating them as launch-ready.

For a step-by-step walkthrough, see A Deep Dive into Florida's Money Transmitter License Rules.

Decide your operating model before product build#

Decide the operating model before you ship payout logic, because this choice sets where control, regulatory exposure, and execution burden sit.

Step 1. Choose between partner-led and license-led based on where you want risk and control to sit#

The core decision is where the regulated perimeter sits now: with a sponsor-bank partner structure, often with an FBO account and a Stripe Connect-type setup, or with your own entity through an MTL or EMI path.

| Decision criterion | Partner-led model (sponsor bank + FBO + provider setup) | License-led model (MTL or EMI path) |

|---|---|---|

| Control ownership | More control is set by partner program boundaries and contracts | More control sits with your internal policies and operations |

| Onboarding burden | Partner program requirements are front-loaded | You carry more direct onboarding and monitoring responsibility |

| Speed to market | Often faster when your use case fits an approved partner program | Often slower because licensing and control build-out come first |

| Regulatory exposure concentration | A larger share is concentrated in the partner relationship, with retained obligations for you | More exposure is concentrated in your entity and operating decisions |

| Partner dependency risk | Higher dependency on partner geography, product scope, and exceptions handling | Lower partner dependency, but higher internal capability requirements |

If you choose a partner-led model, do not treat it as obligation-free. FinCEN's May 9, 2019 guidance is interpretive and does not create new requirements, and it is not exhaustive, so models outside listed examples may still carry BSA obligations. Build a model memo that names who owns AML, KYC, sanctions screening, monitoring, exceptions, and returns in real operations.

Step 2. Start partner-led if your controls are not yet mature enough to stand on their own#

If you cannot yet run mature AML, KYC, and sanctions operations across your target markets, start partner-led and set explicit escalation checkpoints before you expand.

Use a practical readiness test: can you evidence policy ownership, case handling, reconciliation, and audit-trail quality without relying on a partner dashboard as your only record? If not, treat a license-led roadmap as premature.

For US expansion, re-check state analysis early. State definitions of money transmission are fragmented, and multi-state growth can create costly registration and reporting burdens. See State Money Transmitter Licenses: Which US States Require a License for Marketplace Payouts.

Step 3. Re-run the licensing decision when your model changes#

Reopen the model decision when facts change, not just when volume increases.

- You add geographies, including cross-border payout scope.

- You add payout types, for example moving beyond current B2B or third-party assumptions.

- You change who receives, holds, or can redirect funds, including FBO design changes.

- You shift approval or onboarding logic from partner-enforced to internally run controls.

- You add rails or stored-value-like features that change the control perimeter.

Expected output: a dated decision memo stating the current model, why it fits now, partner boundaries, and explicit legal/compliance escalation triggers. If the model changes, escalate to specialist counsel rather than extending an old assumption.

Map activities that trigger licensing risk by jurisdiction#

Map licensing risk by what your platform does with funds in each jurisdiction, not by labels like "marketplace payouts" or "B2B payments."

Step 1. Build the matrix around activities, not product labels#

Build one row per jurisdiction and one column per activity: receiving funds, holding funds, routing funds, and initiating third-party payouts. Add columns for who performs each activity in practice and what evidence proves that split.

Make the evidence specific enough that Legal can verify it without guesswork: sequence diagrams, sample ledger entries, payout state transitions, and contract sections assigning responsibility to the sponsor bank, processor, or your platform. If you use a For Benefit Of account, record who can release funds, delay settlement, and reroute or reverse payouts.

Two readiness checks:

- If the matrix does not show who receives funds and who decides when funds move, it is not ready for sign-off.

- Do not mark a jurisdiction as cleared based only on federal registration; FinCEN MSB registration does not replace state money transmitter licensing.

Step 2. Score each activity with a red, amber, green launch rule#

Use a red/amber/green status to separate low-ambiguity flows from flows that need counsel review.

| Status | Activity pattern | Launch rule |

|---|---|---|

| Green | A regulated institution or approved partner receives and holds funds, and your platform passes instructions within documented limits | Keep the memo, partner boundary map, and product evidence on file; recheck on feature changes |

| Amber | Your platform can delay release, route between payees, handle returns, or initiate third-party payouts where control split is less clear | Mandatory Legal review before launch; document assumptions, partner boundaries, and rollback steps |

| Red | Your platform receives funds, holds them in platform accounts, controls release to third parties, or the flow resembles direct user-to-user transmission | Treat launch as blocked until specialist analysis is complete; evaluate whether state money transmitter licensing or a different structure is required |

State exposure is state-specific, including single-state operations. If you need a deeper pass, use State Money Transmitter Licenses: Which US States Require a License for Marketplace Payouts.

Step 3. Test scenario contrasts before you assume one answer travels#

Do not assume one approved flow covers the whole product. The same movement of funds can be treated differently when the parties or routes change.

A practical contrast:

- A true B2B payment from your own operating funds to your vendor is a different pattern from receiving customer funds and paying sellers.

- If a "B2B" flow includes third-party funds moving through your platform, classify it as third-party payouts.

Treat P2P with extra caution. In New York, Cash App is described as a peer-to-peer money transmission service for sending and receiving fiat currency, and the same company held both money transmission and virtual currency authorization. For matrix purposes, user-to-user fiat transfer is a licensing fact pattern, not a naming choice.

Give cross-border paths their own rows even if domestic paths scored green. Then enforce one launch rule: no new jurisdiction goes live until Legal signs a dated memo documenting assumptions, partner-role boundaries, and contingency actions if interpretation changes.

For fee design, see How to Structure Platform Fees Without Violating Money Transmission Laws.

Define control ownership with your bank and program partners#

Your licensing position is only as strong as your actual control split. After you complete the jurisdiction matrix, turn it into a written control-ownership record with your bank, processor, and other regulated partners. If contract language and day-to-day operations do not match, treat that as a launch blocker.

Step 1. Assign each control to one named owner#

Make ownership explicit for sanctions screening, KYC, AML transaction monitoring, suspicious case review, and escalation. Avoid vague language such as "partner supports compliance" or "platform assists."

For each control, document:

- Decision-maker

- Evidence reviewed

- Action authority

- Escalation deadline

A usable matrix should include control, primary owner, backup owner, trigger event, retained evidence, and who can freeze or release funds. FinCEN's guidance says it does not create new requirements, and models not explicitly covered may still have BSA obligations, so "novel setup" is not a reason to leave ownership unclear.

Use one end-to-end scenario as a hard check. If a payee changes bank details after passing KYC, who re-screens, who reviews alerts, and who can block the next payout?

Step 2. Collect counterparty artifacts before onboarding#

Before onboarding a key payout counterparty or program partner, require clear eligibility artifacts instead of relying on assurances. A practical baseline can include UBO disclosure, a current SOC 2 report, sanctions and AML policy summaries, and an escalation contact list.

These are not universal legal requirements in the excerpts here. They are due-diligence controls that make ownership and control maturity visible. If a partner resists basic beneficial-ownership or control-attestation requests, treat that as a red flag.

Step 3. Define sponsor boundaries in FBO and processor setups#

In sponsor-led FBO or processor models, define what your team can configure and what the sponsor has to enforce. Be explicit about payout timing changes, beneficiary edits, fund holds, failed-payout retries, and rule overrides, because these actions can shift real control boundaries.

Assumed ownership gaps are common. A sponsor may own formal screening while your team controls intake, customer messaging, manual retries, or exception routing. OCC payment guidance includes third-party risk management as a risk-management component, so partner oversight cannot be implicit.

A practical red flag: if the agreement says the sponsor owns monitoring but your team is first to see suspicious payout patterns and no escalation path is documented, the model is not ready.

Related reading: Account Takeover in Payout Platforms and How to Stop Payee Hijacks.

Build the minimum evidence pack before go live#

You are only ready for first production third-party payouts when your go-live pack is complete enough that reviewers can verify controls and outcomes without verbal backfill.

| Evidence area | Include | What it proves |

|---|---|---|

| Signed compliance record | Signed control matrix, AML and sanctions procedures, scoped KYC policy, written compliance attestations from the regulated financial institutions in your flow | A reviewer can identify ownership for screening, monitoring, escalation, and hold or release decisions from the documents alone |

| Rail-level traceability | Payout event logs, idempotency behavior for retries, exception-handling paths, and reconciliation outputs | Logs and reconciliation show execution, not just policy intent |

| Governance record | Approval memo, escalation tree, and a dated assumptions register for licensing interpretation and market coverage | Market scope, role boundaries, and re-review triggers are documented in dated form |

| Pre-launch failure tests | Tests for failed payouts, held funds, returned funds, and duplicate requests, plus the resulting logs, reconciliation outputs, and escalation records | If Finance, Compliance, and Ops cannot independently reach the same conclusion from the record set, stop launch and close the evidence gap first |

Step 1. Gather the signed compliance record. Include the signed control matrix, AML and sanctions procedures, scoped KYC policy, and written compliance attestations from the regulated financial institutions in your flow. The pass/fail test is simple: a reviewer should be able to identify ownership for screening, monitoring, escalation, and hold/release decisions from the documents alone.

Step 2. Add rail-level traceability, not just policy files. Include payout event logs, idempotency behavior for retries, exception-handling paths, and reconciliation outputs tied to the payment rail you are launching. Validate one sample payout end to end so each state change maps to a timestamp, actor or service identifier, and finance-reconcilable reference.

Industry payfac guidance separates onboarding and compliance setup from ongoing process management; your evidence pack should reflect both. Policy documents show intent, while logs and reconciliation show execution.

Step 3. Record governance decisions in dated form. Include the approval memo, escalation tree, and a dated assumptions register for licensing interpretation and market coverage. If your launch depends on a partner-led structure, document market scope, role boundaries, and explicit re-review triggers. Keep whitepapers and industry guides as context, not as a substitute for internal sign-off.

Step 4. Run pre-launch failure tests and store the evidence. Test failed payouts, held funds, returned funds, and duplicate requests before go live, then save the resulting logs, reconciliation outputs, and escalation records in the same pack. If Finance, Compliance, and Ops cannot independently reach the same conclusion from that record set, stop launch and close the evidence gap first.

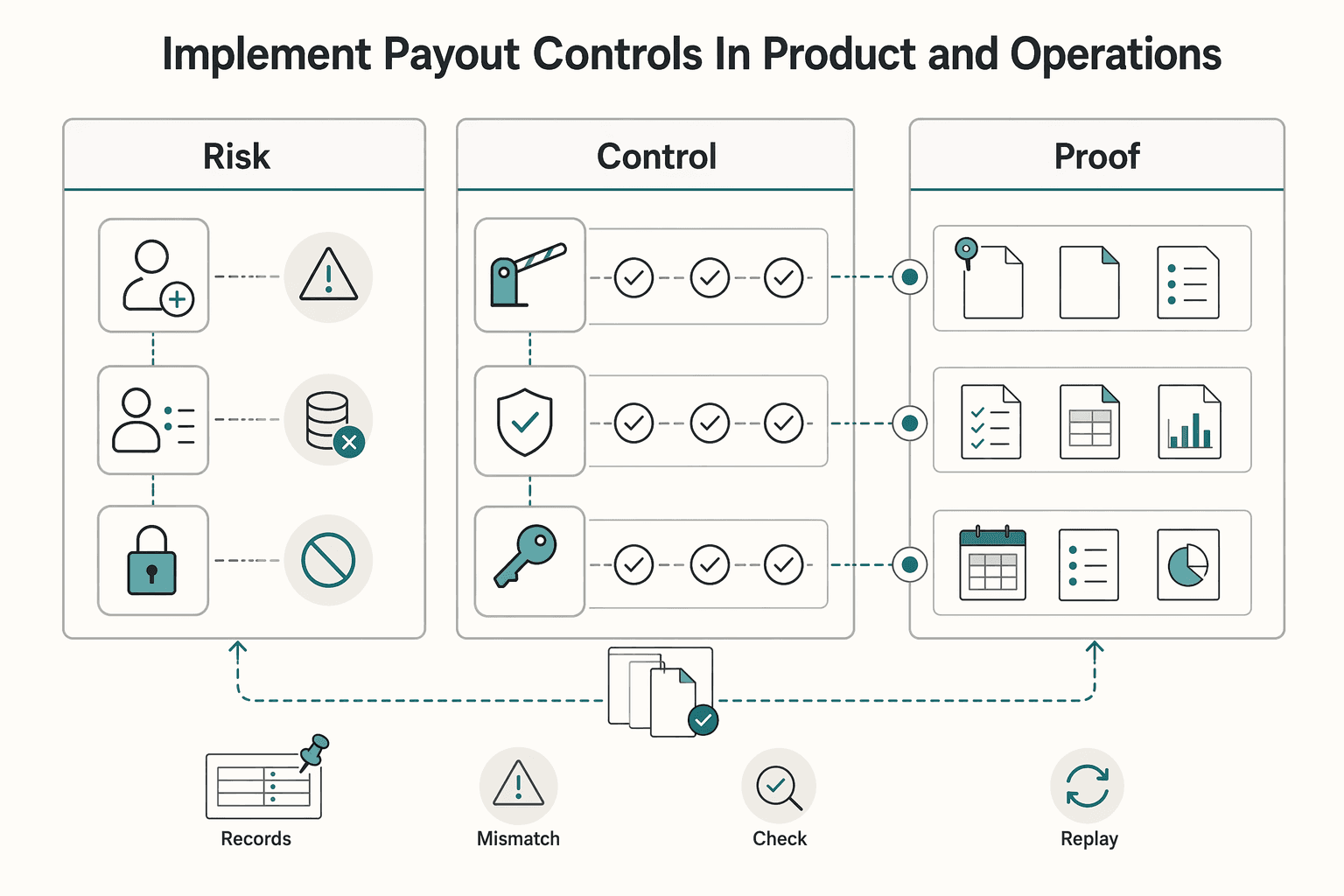

Implement payout controls in product and operations#

After your evidence pack is complete, implement controls in product and operations in the same sequence: activation gates, KYC and sanctions outcomes, then payout permissions.

Step 1. Gate account activation before payout access. Keep account creation, review, and payout enablement as separate states. Users can register and complete profile setup, but payout access should stay off until required KYC and sanctions checks are completed and recorded in a form both Ops and Compliance can review.

The checkpoint is not just that a check ran. You need a dated status, a traceable decision record, and controls that prevent accidental or workaround-based enablement. If admin tools can bypass review logic, require named approvers, reason codes, and audit logs in the same trail as standard approvals.

Step 2. Apply policy controls to initiation, velocity, and exceptions. In online marketplaces, post-onboarding payout behavior is where control gaps often appear. Define who can initiate payouts, raise limits, release holds, and resolve exception queues, with clear Ops and Compliance ownership.

Make those rules enforceable in product with role- or segment-based limits, controlled overrides, and required hold or return reason capture. If sanctions-related exceptions can be cleared without Compliance review, ownership is not actually clear. For deeper rule design, see Transaction Monitoring for Platforms: How to Build AML Rules Without Slowing Down Payouts.

Step 3. Make the integration replay-safe and auditable. Treat idempotency, webhook reconciliation, and mismatch alerting as production controls, not implementation details. Replayed requests should produce one commercial outcome, and delayed, duplicated, or out-of-order webhooks should still resolve to the same final internal state.

If your platform reports "paid" while a partner reports "failed," your escalation and reconciliation records should explain exactly why and how it was resolved.

Step 4. Add extra controls before enabling alternative rails. Do not treat USDC or Circle Payments Network (CPN) as a simple rail toggle. FinCEN's May 9, 2019 guidance says it does not create new requirements and does not address every fact pattern, so model-specific review remains necessary where digital asset flows may raise BSA or MSB questions.

For CPN-specific rollout, Circle describes onboarding as intentionally rigorous, with eligibility standards and configurable operational risk controls. Where CPN is in scope, require the additional eligibility and control documentation before production, including legal registration, UBO disclosure, licensing evidence, AML/KYC and sanctions documents, and SOC 2 reports. If that package is incomplete or control deltas are not mapped, keep the rail disabled in production.

If you run an affiliate or publisher model, see Affiliate Network Payout Structures for Publisher Commissions.

Common failure modes and recovery actions#

Treat these as stop signals, not cleanup items. When an old assumption is stretched to fit a new payout model, the root issue is usually stale classification, weak third-party evidence, or both.

| Failure mode | Recovery action | Checkpoint |

|---|---|---|

| Add a partner and assume obligations transferred | Re-document control ownership in writing, then compare contract language with real product behavior, exception queues, and who can release or stop payouts | For each control, assign one named owner, one escalation path, and one system of record for decisions |

| Add a geography, payout type, or funds-flow model | Pause onboarding for that market and rerun jurisdiction analysis before volume builds | Keep an updated assumptions register and fresh legal sign-off naming the jurisdiction, activity tested, partner-role boundaries, and changed controls |

| Evidence is incomplete while scaling | Treat the gap as a scale blocker until required documents are current, approved, and mapped to the exact partner and market in production | Examples include missing beneficial-ownership documentation, outdated SOC 2, or incomplete partner attestations |

Step 1. Re-open retained obligations when you add a partner#

A Stripe Connect or sponsor-bank integration is not, by itself, proof that AML, sanctions, or monitoring responsibility is fully transferred. The recovery move is to re-document control ownership in writing, then compare contract language with real product behavior, exception queues, and who can release or stop payouts.

Checkpoint: for each control, assign one named owner, one escalation path, and one system of record for decisions. This aligns with the OCC handbook's treatment of Third-Party Risk Management as a distinct payment-systems risk area.

Step 2. Freeze new-market onboarding until classification is refreshed#

If you add a geography, payout type, or funds-flow model, pause onboarding for that market and rerun jurisdiction analysis before volume builds. Do not rely on an earlier memo just because the new rail appears similar.

Checkpoint: maintain an updated assumptions register and fresh legal sign-off that names the jurisdiction, activity tested, partner-role boundaries, and changed controls.

Step 3. Enforce evidence thresholds before scaling back up#

When evidence is incomplete, treat that as a scale blocker. In practice, this often shows up as missing beneficial-ownership documentation, outdated assurance reports such as SOC 2, or incomplete partner attestations where your policy expects them.

Be especially careful when counterparties or pricing models change. Stripe Connect offers different commercial models, including "Stripe handles pricing" and "you handle pricing," but pricing ownership is not a legal-classification shortcut. Check that required documents are current, approved, and mapped to the exact partner and market in production.

Conclusion and copy paste launch checklist#

The goal is not to avoid a Money Transmitter License at all costs. It is to choose the operating model that fits your current product, then set hard escalation triggers for the moment your jurisdictions, payout types, or control over funds change. Use this checklist as a final pre-launch pass, not as a substitute for the earlier analysis.

- Step 1. Confirm your activity map and jurisdiction assumptions are signed off.

Your legal sign-off should name the actual activities in scope, such as receiving funds, holding funds, routing funds, and initiating third-party payouts, not just describe the product at a high level. Verify that the memo or approval packet also names the jurisdictions covered and the partner-role boundaries. If you have added a new rail or new market since that sign-off, treat the approval as stale and rerun the analysis before launch.

- Step 2. Confirm your model choice and re-evaluation triggers are documented.

State clearly whether you are launching partner-led, licensed, or through another model, and document the exact triggers that force re-evaluation, for example changes in jurisdictions, payout types, control over funds, or partner-role boundaries. Assign an owner and review cadence so those triggers are checked before launch and after material product changes.

Frequently Asked Questions

Can a platform run payouts without its own Money Transmitter License (MTL)?

It depends on the exact facts and jurisdiction. A money transmitter facilitates fund transfers between locations, including across international borders; there is no blanket yes/no exemption rule.

What is the practical difference between using an FBO account and obtaining a state-level money transmitter license?

Treat account structure and licensing status as separate questions, and avoid assuming one substitutes for the other without jurisdiction-specific analysis.

When should we escalate to specialist counsel instead of relying on internal compliance review?

Escalate when the legal basis is unclear for your specific product flow or jurisdiction. New York is the clearest example: DFS regulates virtual currency activity under 23 NYCRR Part 200 (issued in June 2015) and under limited purpose trust company provisions of New York Banking Law. Also, avoid relying on the Ohio resource listed here for guidance content, because the captured page returned a 404.

Which controls are non-negotiable before first third-party payouts go live?

Document control ownership and escalation paths clearly enough that legal and compliance reviewers can verify them before launch.

How should we compare partner-led models against an eventual EMI license or MTL path?

Run a jurisdiction-by-jurisdiction legal analysis instead of applying one default model across all markets when comparing partner-led models against an eventual EMI license or MTL path.

What documents should be ready for partner due diligence and internal approvals?

The sources here do not prescribe a fixed document packet. Keep a clear, reviewable record of your legal position, role boundaries, and operational controls so reviewers can test how decisions are made and logged.

What are the most common mistakes marketplaces make when they add a payment rail?

A key error is assuming an intermediary automatically ends money transmission liability. The NMLS MSB Call Report FAQ states liability remains outstanding until funds are paid to the beneficiary, refunded, or escheated, and is not extinguished simply by transmitting funds to third-party paying agents.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- chicagounbound.uchicago.edu/cgi/viewcontent.cgitrusted

- com.ohio.gov/wps/portal/gov/com/divisions-and-programs/fi...trusted

- congress.gov/crs-product/R46486trusted

- congress.gov/bill/119th-congress/house-bill/3633/texttrusted

- dfs.ny.gov/virtual_currency_businessestrusted

- dfs.ny.gov/industry-guidance/enforcement-discipline/ea2...trusted

- federalregister.gov/documents/2023/08/29/2023-17565/gross-procee...trusted

- fincen.gov/system/files/2019-05/FinCEN%20Guidance%20CVC...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Platform Transaction Monitoring That Doesn't Slow Payouts

Strong Anti-Money Laundering (AML) controls only help a payout platform when they reduce risk without slowing legitimate payouts. In practice, that means controls need to work during payment execution, support consistent decisions, and leave a clear record of what was released, held, or escalated.

State Money Transmitter Licenses: Which US States Require a License for Marketplace Payouts

If your platform pays sellers, creators, or contractors in the United States, treat licensing as an operating decision from day one, not a label to clean up later. The core issue behind **state money transmitter licenses us states marketplace payouts** is this: federal status and state licensing answer different questions, and teams get into trouble when they treat one as a substitute for the other.

The Best Community Platforms for SaaS Businesses

Start by classifying the job. If you want access to other people's audience, ideas, or conversations, you are choosing a community to join. If you want a place your customers or members use under your brand, with your rules and structure, you are choosing software you will need to operate every week.