Quick Answer

Building payments in house only makes sense if you can fund and staff ownership beyond launch. Teams need a 12-month plan that defines the exact system boundary, names cross-functional owners, budgets for maintenance and on-call, and covers PCI DSS, verification, reliability, incident response, and manual exception handling. If month 6 to month 12 ownership is not explicit, a full custom build is premature.

Building in-house payments can be right, but only with a 12-month ownership plan#

Building payments in house can be the right call, but only if you plan to own months 1 through 12, not just launch day. This guidance is for platform leaders choosing between a custom build, a provider integration, or a PayFac path.

Start with ownership, not a launch estimate#

If you are evaluating the build payment infrastructure in-house engineering cost, treat one-time delivery cost as one input, not the decision. The real question is whether your team can keep up with API changes, compliance updates, card-network rule changes, and fraud-pattern shifts after version one. Use published ranges as directional scope checks, not guarantees:

| Path | Source-stated cost | Source-stated timeline |

|---|---|---|

| Integrate an existing provider | $5,000 to $20,000 | n/a |

| Custom gateway build | $50,000 to $300,000+ | 3-6 months (basic), 6-12+ months (full-scale) |

| PayFac infrastructure | PCI compliance costs cited as $2M+ and ongoing ops/infrastructure cited as $360K/year | 12-18 months minimum |

Recommendation: do not approve an in-house path from a rough build estimate alone. Approve it only when you have named owners, explicit maintenance assumptions, and clear go or no-go checkpoints through month 12.

Who this guidance is for#

This is for teams that need to evaluate payments as an ongoing ownership model, not just an initial build. In that setup, payments are rarely just an engineering project. Ownership often spans product, engineering, operations, and compliance.

Use a simple readiness check: can you already name who owns post-launch operations and compliance handling? If not, the estimate is still early.

The boundary to keep in mind#

Do not use one timeline for every in-house option. Source-stated timelines differ by scope: custom gateway work is cited at 3-6 months for a basic version and 6-12+ months for a full-scale solution, while PayFac infrastructure is cited at 12-18 months minimum.

Set one boundary early: will you directly handle card data? If yes, you move into PCI DSS scope, potentially at Level 1. If you pursue a PayFac model, scope can also expand to KYC and AML responsibility for onboarded merchants, plus bank relationships, underwriting, certification, and ongoing operational requirements.

Before you make a full-build decision, produce a one-page ownership pack. It should define the exact boundary, name cross-functional owners, and cover a month 1 to month 12 budget that includes maintenance and control work. If that pack is missing, you are still defining the job, not choosing the architecture.

For a build-vs-buy comparison, see Total Cost of Ownership Calculator: Build vs Buy Your Payment Stack.

Define the exact system boundary before discussing cost#

If you cannot define the owned boundary clearly, pause estimating. Any estimate for in-house engineering cost is weak until ownership is explicit.

Labels are not scope. For example, PayPal's US business fee documentation separates "Payflow Pro (Payment Gateway)," "Dispute Fees," and "Chargeback Fees." That is a practical signal that payment acceptance and exception handling can sit on different cost surfaces.

Make an early split between basic billing behavior and full financial-infrastructure ownership. If you own the infrastructure layer, the scope has to include ongoing owner and operator work, not just initial delivery. Your boundary note should at least name:

- supported provider and market scope

- transaction classification rules you will price and reconcile, for example domestic vs international treatment, including market-group rules

- exception states you own, including disputes and chargebacks

- the documents and checkpoints you will use when rates, fees, or applicability change

Use explicit verification checkpoints in that boundary note. PayPal points to policy updates for fee and rate changes, provides printable fee artifacts, and shows that market or program treatment can affect whether a transaction is treated as domestic for fees. It also notes that other bank or issuer fees can still apply in some cases. If your boundary note cannot hold up at that level of detail, you are still defining the job, not estimating it.

For a step-by-step walkthrough, see Digital Nomad Payment Infrastructure for Platform Teams: How to Build Traceable Cross-Border Payouts.

Most teams start with checkout and end up owning financial infrastructure#

A hosted checkout is a sensible starting point, but ownership expands once you take responsibility for pricing and payouts, not just payment acceptance. At that point, you need to explain fee outcomes, payout activity, and customer-impacting exceptions in a way product, finance, and support can all use.

You might start with Stripe Checkout or another payment gateway. As ownership expands, the work shifts from simple charge collection to ongoing payout and fee operations across your app and provider events.

The scope jump usually happens at pricing and payouts#

The jump becomes real once you decide who owns pricing and payout behavior. With Stripe Connect, that split is explicit: you can offload maintenance to Stripe, or you can take full control and ownership of payments.

| Connect approach | Who owns pricing/fees | Published cost signals that affect architecture |

|---|---|---|

| Offload maintenance to Stripe | Stripe sets and collects processing fees from users | Less direct pricing ownership by the platform |

| You handle pricing | Platform is responsible for Stripe processing fees and can charge users | $2 per monthly active account (active = month with payouts sent), 0.25% + 25¢ per payout, and billing based on aggregate monthly payouts at month end |

Once you choose "you handle pricing," estimates depend on payout volume and active-account behavior.

Adding processors can add translation and verification work#

A second processor adds another fee model and another set of operational assumptions to reconcile. Even with one provider, you still need to revalidate fee assumptions because gateway costs can change.

On Stripe's public pricing, for example, standard domestic card pricing is 2.9% + 30¢, with +1.5% for international cards and +1% for currency conversion. If you use Managed Payments, the 3.5% Managed Payments fee is stated as in addition to standard Stripe processing fees.

The hidden layer is internal operations#

As ownership grows, this becomes more than API calls. Before you take on more ownership, verify three basics:

- who owns pricing and processing-fee responsibility

- how monthly active accounts and payouts are counted for billing

- how often fee assumptions are revalidated as pricing changes

Build the 12-month ownership model before writing code#

Model the first 12 months of ownership, not the launch sprint. If leadership cannot fund month 6 to month 12 maintenance with named owners, do not approve an in-house build.

For a payment gateway stack, use explicit cost buckets instead of one blended total. Upfront build work matters, but long-term maintenance, support, and changing provider fees are also part of the job.

| Cost bucket | What belongs here | Assumptions that move the number most |

|---|---|---|

| Build | Initial gateway integration, payment-state model, entitlement hooks, internal ops screens, reconciliation exports | Staffing mix, owned boundary, provider count, custom payout logic |

| Hardening | Idempotent webhook handling, duplicate-event protection, retry handling, monitoring, audit logging, failure drills | Provider event behavior, event volume, tolerance for delayed settlement visibility |

| Compliance | PCI DSS scope analysis, security controls, validation work, evidence collection, policy review | Whether you store/process/transmit cardholder data, SAQ A eligibility, projected 12-month transaction volume |

| Incident response | On-call setup, escalation paths, breach-response prep, testing exercises | Business-hours vs 24x7 coverage, primary/backup responders, severity expectations |

| Ongoing maintenance | Fee refreshes, API changes, support escalations, reconciliation breaks, manual exception handling, operational toil | Growth rate, support load, fraud-review volume, exception volume requiring human handling |

Turn this into a budget worksheet, not a planning artifact. If any row has no owner, no assumptions, or no review date, the model is incomplete.

Force the assumptions into the model#

Published ranges are hard to compare because scope and team assumptions differ. Write these down before approving build work:

- Staffing model: who builds, who owns post-launch maintenance, and whether finance ops or support needs dedicated exception and reconciliation coverage

- On-call coverage: business-hours only or a full schedule with named responders and escalation contacts

- Provider count: one provider and two providers can be different operating models, with different reconciliation and exception paths

- Risk controls: whether fraud detection is manual, vendor-assisted, or internal, and your planned PCI DSS scope from day one

PCI scope can change estimates quickly. PCI DSS applies when cardholder data is stored, processed, or transmitted. A fully outsourced account-data model can narrow scope, for example an SAQ A posture, but it does not remove security or operational responsibility. Also test whether your projected 12-month volume could change your compliance posture, for example because Visa merchant levels are determined on a 12-month transaction window.

Budget for post-launch failure modes#

Hardening and incident response are easy to underfund in early estimates. Webhook endpoints can receive duplicate events, and some providers retry undelivered events for up to three days. Budget duplicate-safe processing and replay handling before launch. That carries two real costs:

- investigation capacity for payment-state mismatches when retries arrive after the original event

- monitoring and evidence trails that separate provider issues from endpoint issues and internal idempotency gaps

Use a pre-launch checkpoint. One operator should be able to trace a failed event from provider reference to your internal record and decide whether replay is safe.

Incident response needs the same level of discipline. Breach-response guidance expects immediate-response readiness and at least annual testing. If no one owns on-call scheduling, escalation, exercises, and post-incident fixes, your model is missing real operating cost.

Add opportunity cost, not just vendor and headcount cost#

Include what this work displaces. Undifferentiated payments operations work competes directly with product roadmap work. At minimum, price these line items:

- roadmap delay while engineering handles money-state operations work

- blocked pricing experiments when fee logic or payout exceptions remain manual

- sales friction when enterprise exceptions require engineering intervention

Manual exception handling tied to revenue or payouts can be a warning sign. If support, finance, or sales cannot resolve exceptions without engineering, ownership cost may already be above the initial plan.

Be explicit about uncertainty: provider costs change, fraud-control cost is context-dependent, and estimates are not comparable without clear scope and team assumptions. The decision rule is still simple: no named owners, no funded on-call model, no stated PCI DSS scope, or no month 6 to month 12 maintenance budget means stop the custom build.

Related: How to Build a Gross Margin Model for a Marketplace: Payment Costs FX and Infrastructure.

Compliance and tax work is product work, not back-office cleanup#

Compliance and tax rules need to live inside product logic because they determine onboarding, payout eligibility, and reporting paths. If policy operations are not staffed, your payout system is under-specified.

The controls change by flow, market, and program#

There is no single global checklist for KYC, KYB, AML, and VAT validation. CIP identity verification is risk-based, legal-entity verification varies by entity type and country or region, and requirements can expand when additional financial products are enabled.

| Flow | What varies | What it should gate in product |

|---|---|---|

| KYC / identity verification | Risk profile, jurisdiction, provider program | Activation, withdrawal eligibility, payout release |

| KYB / legal-entity verification | Entity type, country/region, program setup | Business onboarding completion, payout enablement |

| AML controls | Location, size, and nature/volume of activity | Review states, payout holds, exception escalation |

| VAT validation | EU cross-border VAT status, member-state differences | Tax handling and account setup for relevant EU flows |

If a status can block money movement, it belongs in your state model. In provider programs that use webhook notifications, verification is event-driven, and failed verification can block payouts from being enabled.

Tax documents have a lifecycle, not just a file upload#

Tax forms need collection, validation, storage, and a traceable status history. Form W-9 is used to collect a correct TIN, and missing or incorrect TIN data can trigger backup withholding. Form W-8BEN is for individuals, while entities use different W-8 forms, and it is furnished to the payer or withholding agent, not filed directly with the IRS.

| Item | Use | Note |

|---|---|---|

| Form W-9 | Collect a correct TIN | Missing or incorrect TIN data can trigger backup withholding |

| Form W-8BEN | For individuals | Furnished to the payer or withholding agent, not filed directly with the IRS |

| Form 1099-K | Reports card and third-party network transactions | Filed by the payment settlement entity for each calendar year |

Reporting logic also needs to be explicit. Card and third-party network transactions are reported on Form 1099-K by the payment settlement entity, not automatically on 1099-NEC or 1099-MISC. 1099-K is filed for each calendar year, and IRS information-return records are kept for at least 3 years from the due date (4 years for Form 1099-C).

Put policy gates inside payout and withdrawal states#

Do not bolt policy checks onto a "ready" payout flow. Define explicit states such as pending verification, pending tax review, eligible for withdrawal, and payout blocked.

For EU flows, VIES is the VAT-registration check for cross-border validation, and it relies on national VAT databases rather than acting as a single global VAT system. It also has known scope limits, including the UK GB VAT-number service change noted on 01/01/2021.

A practical pre-launch check is simple. Run one individual and one business account through each target-market path. Verify that the correct document route triggers. Confirm block reasons are visible to operations, and confirm failed verification leaves payouts disabled. If compliance ownership is only part-time, treat that as a decision signal and consider MoR or a constrained hybrid model until policy operations have named owners, queue coverage, and evidence retention.

Reliability requirements that finance and engineering both have to sign#

Reliability is the control layer that makes sure money moves once, lands in the right state, and is explainable later. If finance and engineering are not signing the same invariants, you do not yet understand the real cost of owning payments in house.

| Invariant | Requirement | Detail |

|---|---|---|

| Idempotent writes with idempotency keys | Retryable write paths return the original result for the same key | Stripe replays the first result for a key, including 500 outcomes; Adyen supports safe retries that perform the action once |

| Ordered internal state transitions | Do not treat callback timing alone as the source of truth | Webhooks are event signals, and Stripe can retry undelivered events for up to three days |

| Replay-safe webhook handling | Accept, store, then process webhook messages | PayPal's pattern is to fetch the latest order details after webhook receipt and verify current provider state before finalizing internal state |

Finance and engineering should sign the same three invariants:

- Idempotent writes with idempotency keys: Retryable write paths must return the original result for the same key instead of creating a second operation. Stripe replays the first result for a key, including 500 outcomes, and Adyen supports safe retries that perform the action once. This is the primary defense against duplicate posting.

- Ordered internal state transitions: Provider updates are asynchronous, so callback timing alone is not your source of truth. Webhooks are event signals, and Stripe can retry undelivered events for up to three days.

- Replay-safe webhook handling: Accept, store, then process webhook messages. PayPal's pattern of fetching the latest order details after webhook receipt is the right model. Verify current provider state before finalizing your own.

Your financial truth model#

Use ledger journals as the source of truth. A journal entry is a complete, balanced set of debits and credits, which gives finance an auditable record and engineering a stable financial event history.

Treat balances and dashboard views as derived outputs from journaled events plus provider settlement data. Use journal entries and provider reconciliation outputs as the basis for posting, payout release, and month-end close.

Failure modes worth designing for up front#

The highest-cost failures are usually repetitive, not exotic:

- Duplicate posting: Retries or webhook redelivery create extra operations when idempotency is missing or scoped incorrectly.

- Stale FX quotes: The rate at payment time can differ from refund or dispute time. Quote durations like 5 minute, 1 hour, or 24 hour reduce uncertainty but do not eliminate FX exposure.

- Payout state mismatch: Provider callbacks move transfer status, but internal payout state does not follow. You need transition checks on every callback path.

Practical rule: when money movement depends on a callback, verify the latest provider object before you lock internal state.

Verification checkpoints before launch and every month after#

Finance and engineering should agree on recurring checks with owners and evidence:

- confirm reconciliation completeness by tying each payout settlement batch back to full transaction history

- run month-end integrity tests that tie ending balances to journal entries and provider reporting outputs

- track incident recovery with MTTR and review evidence: webhook payloads, retry outcomes, journal entries, and payout reconciliation artifacts

If these checks still require manual spreadsheet repair, the system is not yet operating at production reliability.

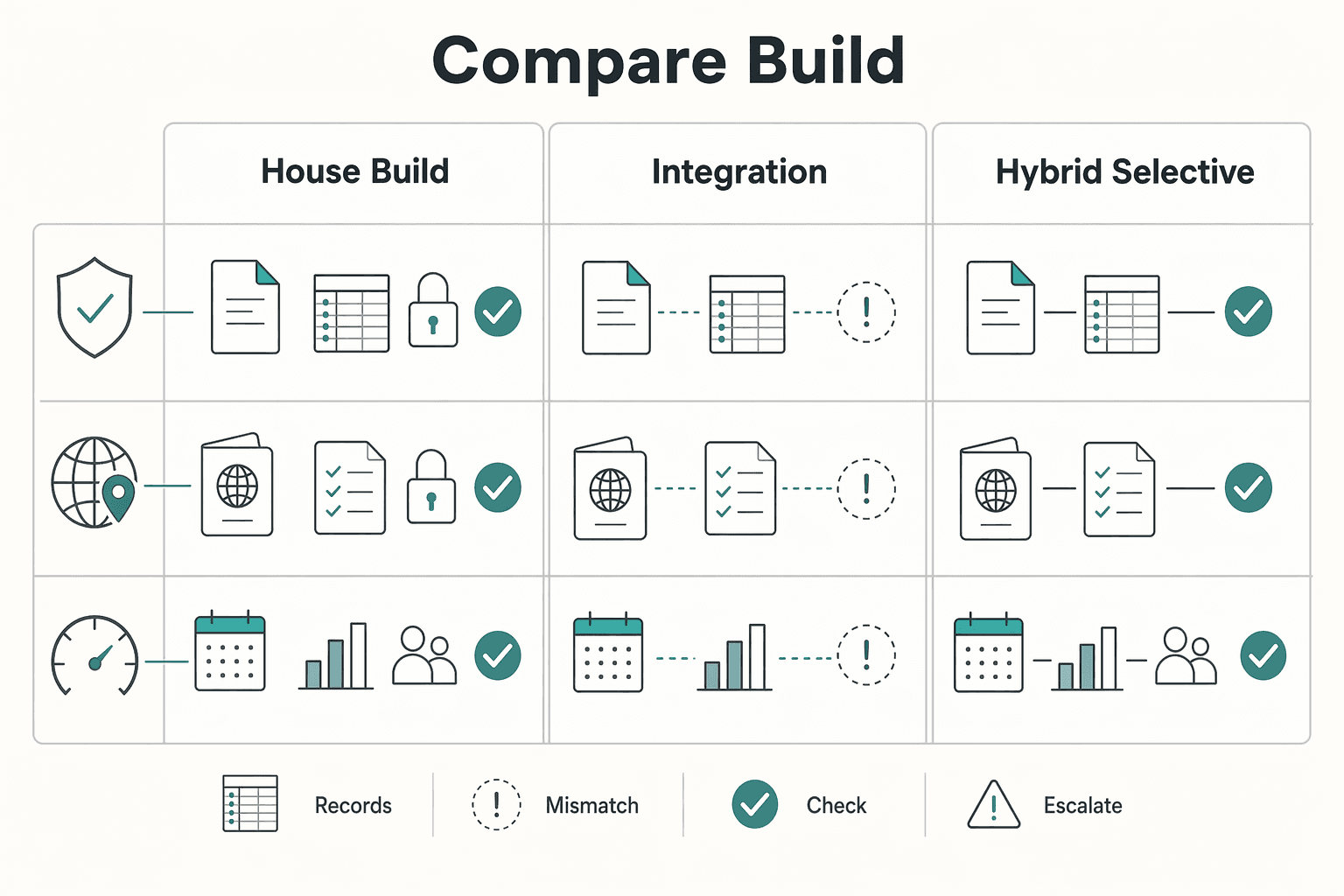

Compare build, buy, and hybrid using explicit decision criteria#

If you need to launch quickly and handle cross-border compliance now, a PSP-led path or selective Merchant of Record (MoR) is often the faster starting point. Full in-house ownership is most defensible when you can name the specific control you need and the team that will run it after launch. The decision is really about operating burden, not feature lists: who owns transaction liability and compliance work.

| Model | Control | Launch speed | Cost risk | Compliance load |

|---|---|---|---|---|

| In-house build | Highest control over routing, internal data model, and provider mix | Slowest, because you own integrations and failure handling | Higher execution risk as complexity grows across countries, providers, and exceptions | Highest, especially if you store, process, or transmit cardholder data and expand PCI DSS scope |

| PSP-led integration | Moderate control for standard flows with one primary provider | Fast for standard acceptance flows | Lower upfront build risk, with later tradeoffs around customization and lock-in | Often lower than full build, depending on provider scope |

| Hybrid (selective MoR + direct ownership where needed) | Targeted control only where it pays back | Typically faster than full build, more flexible than single-provider only | Moderate, because you run multiple models without owning everything | Moderate to lower, based on what the MoR covers by market/product |

Use four scale checks before deciding:

- Country count: Multi-country expansion can raise compliance and tax operations quickly. Selective MoR can reduce that burden where supported.

- Provider diversity: Multiple providers can improve reach, adaptability, or performance, but each new partner adds integration and support overhead.

- Connection footprint: At multinational scale, processor/acquirer/gateway connections can multiply quickly, which increases operating complexity.

- On-call tolerance: Multi-provider stacks increase operational overhead your team must own.

Two practical patterns stand out:

- A large, multi-region merchant may justify selective in-house ownership, for example orchestration, while outsourcing some compliance responsibility.

- An early-stage platform will often prioritize launch speed and operational focus over maximum control.

Decision rule: buy or hybrid is usually stronger when you need speed and compliance coverage now. Build selectively only when the control requirements are explicit, material, and operationally owned.

Related reading: How to Build a Compliance Operations Team for a Scaling Payment Platform.

Set go or no-go checkpoints before sprint 1#

Do not start a full in-house payments build until ownership, operating artifacts, and compliance choices are explicitly defined and signed. If a checkpoint is still unresolved, treat that as a risk signal and consider deferring the full build while launching with Stripe Checkout or a tightly scoped hybrid path.

| Checkpoint | Must exist before sprint 1 | Go test |

|---|---|---|

| Ownership map | Named owners across relevant functions (typically product, engineering, finance ops, and compliance) for payment operations | Each owner can state decision rights and escalation paths for settlement, payout, and compliance incidents |

| Artifact readiness | Usable transaction/ledger journal model, webhook retry/replay policy, and a documented incident escalation plan | Team can trace one payment from provider event to internal records and explain retry, duplicate, and escalation handling |

| Compliance readiness | Chosen PCI DSS approach, documented KYC and related verification policy decisions by market/program, and an evidence retention plan | Team can explain what stays off your servers, what still requires annual PCI attestation, when payouts are blocked pending verification, and what evidence is retained |

Ownership has to cross functions#

This is not just an engineering integration. Payment operations span authorization, processing, settlement and clearing, plus compliance and risk management, so ownership has to be cross-functional before implementation starts.

A practical check is a tabletop incident scenario, for example failed payouts or a provider mismatch. If the team cannot clearly answer who approves customer communication, who investigates ledger impact, and who escalates to the processor, ownership is not ready.

Artifacts must hold up under retries and incidents#

Your artifacts need to work in production, not just look complete on paper. The transaction/ledger journal model should let your team reconcile provider payment events to internal financial records.

Webhook handling should assume retries are normal behavior. Stripe can automatically retry undelivered events for up to three days, so you need replay handling plus idempotent processing to avoid duplicate effects.

Incident response also needs concrete ownership and execution, not just a document. PCI guidance treats incident response planning as a formal control and expects responsible parties to understand it.

Compliance choices cannot stay provisional#

Using a PSP does not remove your PCI obligations. PCI is a shared responsibility, and the business still has compliance duties, including annual attestation. Hosted flows like Stripe Checkout can reduce scope by keeping payment data off your servers.

KYC and related verification decisions also gate payout readiness. Platform flows require onboarding and verification before payouts, and verification requirements vary by country or region, so policy choices need to be made by market and program before scale.

If these checkpoints are not ready, that is a decision signal: ship a constrained path now, then return to full in-house ownership when owners, artifacts, and compliance controls are truly in place.

For the finance ops side, read Accounting for a Payment Infrastructure Business: How to Structure Finance Ops.

Sequence the first 180 days if you choose to build#

Once the go decision is real, sequence for financial correctness first, then expand scope. A practical first 180-day sequence is to prioritize event integrity, payout control, and reconciliation evidence before adding routing complexity.

| Phase | Focus | Gate |

|---|---|---|

| Days 0-30 | Build the ledger and event-handling foundation | Replay tests for duplicates and undelivered events, plus a manual recovery drill |

| Days 31-90 | Add payout controls, reconciliation exports, and baseline fraud controls | Finance-ops reconciliation sign-off on transaction-level exports and payout outcomes |

| Days 91-180 | Expand provider routing in stages and harden monitoring and on-call | Month-end close simulation from reporting outputs, without spreadsheet patching, before widening routing or adding local receiving account details |

Days 0-30#

Build the ledger and event-handling foundation first. Define the minimum journal events you need across payment and payout states, and do not expand scope until finance can map provider events to internal journal entries.

Treat your webhook endpoint as essential but non-deterministic input. Stripe notes that duplicate event delivery can happen and recommends logging processed event IDs. It also retries undelivered events for up to three days. Handlers need to be replay-safe, with a documented undelivered-event recovery flow.

Make idempotency a control, not a convenience. For any retry that could trigger money movement, require a stable idempotency key and enforce deduplication in internal write paths to prevent duplicate side effects after partial failures.

Days 31-90#

Add payout controls only after event truth is stable. Implement payout creation, approval states, and payout batches with explicit duplicate protection in your operating flow.

Ship reconciliation exports in the same phase. Transaction-level settlement outputs help finance verify settled payments, payouts, and costs against your internal journal. Totals alone are often not enough for a reliable close.

Stand up baseline fraud controls now. Start with provider default or AI-backed rules, then add custom rules when you have clear risk patterns, so you avoid both unnecessary loss and avoidable manual-review load.

Days 91-180#

If your first provider path closes cleanly, expand provider routing in stages. Additional providers can add callback, reference, and reconciliation variance, so validate each path before broad rollout.

Introduce local receiving account details only where provider and currency support is confirmed. Treat availability as provider- and currency-dependent, and avoid broad rollout assumptions until compliance and operations validate coverage.

Harden monitoring and on-call for payment creation failures, webhook replay backlog, payout state mismatches, and reconciliation breaks. If replay and finance corrections are still mostly manual, keep scope constrained.

Make phase gates explicit before moving forward.

- After days 0-30: replay tests for duplicates and undelivered events, plus a manual recovery drill

- After days 31-90: finance-ops reconciliation sign-off on transaction-level exports and payout outcomes

- Before widening routing or adding local receiving account details: month-end close simulation from reporting outputs, without spreadsheet patching

Red flags that should stop scope expansion immediately#

Stop scope expansion if any of these signals are red. Freeze new countries, providers, and payout paths until the control gap is fixed, because pushing forward usually turns a contained defect into a finance, compliance, and support problem.

- Broken payment traceability: If finance cannot trace one payment end to end across merchant reference, provider reference, internal ledger journals, and final bank deposit status, do not expand. Reconciliation should tie payout records to bank deposits and reconciliation status, not just totals. If a settled payment, refunded payment, or paid-out balance movement still needs spreadsheet stitching to explain, treat that as a hard stop.

- Manual webhook and duplicate-event repair: If engineering is replaying failed webhooks manually or cleaning up duplicate side effects, event handling is not safe enough to scale. Webhooks can be delivered more than once, so your flow must be replay-safe. Retrying the same operation with the same idempotency key should not create a second journal entry, second payout, or manual correction ticket.

- AML/KYC review bypass: If AML or identity-review steps are skipped to keep payouts moving, stop expansion immediately. In U.S. context, CIP rules require written identity procedures for banks, and AML duties for MSBs can include suspicious-transaction reporting for transactions that involve or aggregate at least

$2,000. - Country rollout without VAT and tax-document controls: Do not add EU countries until you have a defined VIES VAT-validation step, clear handling for valid vs. invalid outcomes, and country-specific follow-up procedures where required. Also define how Form W-9 and Form W-8BEN requests are collected, reviewed, and retained when those forms are required in your tax-document workflow before launch.

Handle country and program variation without creating legal blind spots#

Do not treat country expansion as a config change. Treat it as a policy change, because CDD/AML review points, tax-form handling, and payout-method eligibility can vary by jurisdiction, sector, provider, and program.

The rules are not uniform. FATF standards are implemented locally, not identically, and threshold examples are context-specific. Sector thresholds can vary. U.S. CTR reporting is triggered above $10,000 in currency transactions. EU AML text references cash payments above EUR 10 000 while allowing stricter national rules, and FATF's virtual-asset context uses a USD/EUR 1 000 CDD threshold. Do not reuse one threshold across flows without validating the exact jurisdiction and program.

Use a "confirm safely" workflow before launch and whenever you change market scope:

- document each assumption in one place: country, provider program, payout route, tax form, and the source URL reviewed

- confirm market-specific capabilities with the provider or program owner, since coverage is published by country, region, and currency, not as universal support

- log policy changes with an owner and effective date so support, ops, and compliance are not working from stale rules

Keep tax-form logic precise. Form W-9 is for providing a correct TIN to payers or brokers filing information returns with the IRS. Form W-8BEN is submitted when requested by the withholding agent or payer, not as a universal form for every non-U.S. payee. In your records, store form type, request trigger, and review status.

In internal docs and customer-facing copy, use qualified language such as "where supported" and "coverage varies by market/program." When introducing virtual accounts or a new cross-border payout route, require explicit legal and compliance sign-off so availability is not overstated.

The practical next step is a gated decision, not a bigger estimate#

Choose a full build only if leadership is ready to fund and staff ownership after launch, not just deliver v1. If that commitment is unclear, treat full build as a no-go for now and evaluate a constrained hybrid or Merchant of Record (MoR) path.

This is a tradeoff call, not a default. In-house paths can require higher upfront cost and more time, and ownership continues through long-term maintenance and support. A payment gateway is not finished when the first transaction succeeds.

Make the go or no-go check explicit#

Before approving architecture, complete the checkpoint list and review it with product, engineering, finance, and compliance together. The test is simple: each item needs a named owner, a sign-off date, and evidence. Your minimum evidence pack should include:

- a signed ownership map across product, engineering, finance ops, and compliance

- a PCI DSS scope position if you store, process, or transmit cardholder data

- a country and program assumption list marked

confirmed,needs access, orunknown - post-launch coverage for maintenance, support, and incident handling

If those basics are unresolved, do not ask for a bigger estimate. Reduce scope and choose a lower-risk architecture.

Match the path to your operating capacity#

| Path | When it fits | What you still need to verify |

|---|---|---|

| Full build | You need deep control and can absorb considerable upfront investment plus ongoing maintenance | PCI DSS scope, owner coverage after launch, market-by-market capability checks |

| Constrained hybrid | You want control over selected flows without owning every compliance and operational burden on day one | Clear boundary between your stack and the provider's responsibilities |

| MoR-led acceleration | You need to reduce time-to-launch pressure and want transaction-level tax and compliance responsibilities handled by the MoR for supported flows | Exact MoR scope in your setup, country coverage, and commercial/program approval |

MoR can help when tax collection and remittance and KYC and AML duties are major blockers. But it does not remove every responsibility in every jurisdiction, so you still need clear written boundaries for what stays with you versus the provider in your product design.

Confirm coverage before you commit architecture#

Coverage is not uniform by country or program. Some features are unavailable in certain regions, and some capabilities require explicit access before rollout. For example, one international issuing path requires early access and lists local issuing in 22 countries. Broad availability claims like 200+ countries/regions and 25 currencies still do not confirm your exact flow.

Finish the go or no-go checklist. Run the build vs buy vs hybrid table with leadership. Then talk to sales or request access before locking architecture. Ask for written confirmation of required markets, currencies, and program features. If you do not get that confirmation, assume coverage is not committed and choose the lower-risk path now.

If your team needs to validate market/program fit before committing architecture, talk to Gruv.

Frequently Asked Questions

How much does it cost to build payment infrastructure in-house, and why do published ranges vary so much?

Published costs vary by scope and ownership. The article lists $5,000 to $20,000 for integrating an existing provider, $50,000 to $300,000+ for a custom gateway build, and PayFac infrastructure with PCI compliance costs cited as $2M+ plus $360K/year in ongoing ops and infrastructure. Some estimates cover only an MVP or payment acceptance, while others include payouts, compliance, and post-launch support.

When does building in-house make sense instead of using a payment provider or Merchant of Record?

Building in-house makes sense when control and customization are product requirements, not just preferences. It is most defensible when you can name the specific control you need and the team that will run it after launch. If speed and compliance coverage matter more, a PSP-led path or selective MoR is usually the stronger starting point.

What hidden costs show up after the MVP phase for a payment gateway build?

Hidden costs usually show up in maintenance, support, hardening, compliance, incident response, and manual exception handling. Teams also underestimate fee refreshes, API changes, reconciliation breaks, and duplicate-safe webhook processing. If support, finance, or sales still need engineering to resolve exceptions, ownership cost is already rising beyond the MVP plan.

How long does a basic implementation take versus a full-scale multi-region platform?

A basic custom gateway is cited at 3-6 months, while a full-scale solution is cited at 6-12+ months. PayFac infrastructure is cited at 12-18 months minimum. Multi-region scope takes longer because payouts, tax-document workflows, and market-specific verification add operational and compliance work.

Why do payment infrastructure estimates drift after launch even when the initial scope looked clear?

Estimates drift because the scope keeps moving after launch. KYC, KYB, and verification requirements vary by country, capabilities, and business type, while provider fees, fraud patterns, and network rules also change. Production work continues too, including reconciliation, manual exceptions, and webhook retries that can continue for up to three days.

What is the minimum compliance scope a platform must budget for before scaling payouts?

At minimum, budget for PCI DSS scope review if you store, process, or transmit cardholder data, and for KYC readiness before connected accounts can accept payments and send payouts. If U.S. tax-document workflows are in scope, plan for Form W-9 TIN collection and Form W-8BEN handling when requested. Keep reporting logic current because filing thresholds and reporting treatment can change.

What should founders verify first if they are considering a hybrid build-buy approach?

Start by defining ownership boundaries: the merchant-of-record role by flow, card-data exposure in your stack, and who owns KYC, payout controls, and tax-document operations. Then validate coverage and rules by specific country and program, because support is not uniform across markets. VIES is for EU cross-border VAT validation, not a global validation system.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaaml.ffiec.gov/docs/manual/06_AssessingComplianceWithBSAReg...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- epa.gov/sites/default/files/2017-12/documents/epaccm...trusted

- gao.gov/assets/gao-20-195g.pdftrusted

- irs.gov/forms-pubs/about-form-w-9trusted

- irs.gov/pub/irs-pdf/fw8ben.pdftrusted

- ncua.gov/newsroom/press-release/2026/fincen-issues-ex...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: