Quick Answer

Start with AEAT, then move to Social Security: submit Modelo 036/037, confirm acceptance, and only then file alta en el RETA with matching data. For become freelancer spain autonomo 2026 decisions, the article’s core rule is sequencing plus evidence, not just signup completion. Build prerequisites first (NIE, bank domiciliation readiness, filing inputs), keep receipts for each submission, and run an owned calendar for monthly cuota, quarterly forms, and annual Renta. Also treat VERI*FACTU as a live compliance area that needs periodic re-checks.

Why Spain autónomo setup is an operator decision, not just a freelancer task#

Step 1#

Spain setup is a multi-system launch, not a profile-completion task. If your internal brief is become freelancer spain autonomo 2026, you are managing at least three moving parts that affect launch speed and support load: AEAT registration, RETA onboarding through Importass, and invoicing rules that are still shifting around VERI*FACTU.

Each part tends to land on a different team. Tax registration starts with AEAT census onboarding through Modelo 036. The RETA step then runs through Importass in its own autónomo flow for alta en el Régimen de Autónomos. Separate from both, your invoicing setup has to track Spanish compliance closely enough that finance and ops are not left cleaning up avoidable errors once users start billing.

The practical rule is simple. If your product can only help someone "sign up" but cannot support filing sequence, record retention, and invoicing configuration, you do not have a Spain launch motion yet. You have a lead-gen problem dressed up as onboarding.

Step 2#

As of 2026, the core structure is clear, but parts of the invoicing picture are still moving. Public guidance confirms the basic setup. AEAT census filing exists for starting activity. RETA registration exists as a separate step. VERI*FACTU is a real invoicing compliance track with phased dates. AEAT's own material states 1 de enero de 2026 for taxpayers subject to Corporate Tax, and AEAT has also published notices extending invoicing-system adaptation timelines.

What you should not assume is that every autónomo will face identical, fully settled VERI*FACTU obligations on the same terms across 2026. AEAT's public FAQ page was still being updated on 5 de diciembre de 2025, which is a strong signal to treat invoicing guidance as live, not final. If a billing product or partner tells you Spain invoicing is fully settled, verify that claim before rollout.

Your verification checkpoint should be practical. Keep a dated proof file for every rule you rely on, including the exact AEAT or Importass page, the filing receipt, and the product setting that implements it. That saves time when legal, finance, or support asks why a launch decision was made.

Step 3#

This guide is meant to get you to a clear go-or-no-go view, the right filing sequence, and a checklist another team can execute without guessing. By the end, you should know what gets filed with AEAT, what is handled in RETA, where invoicing uncertainty still needs review, and what proof to retain.

If you cannot hand that packet to legal, finance, and ops with named owners and expected submission evidence, do not promise Spain onboarding yet. The setup itself is manageable. The real risk is launching before someone owns the exceptions.

For more background, see A Guide to the 'Autónomo' System for Freelancers in Spain.

Decide whether Spain fits your expansion thesis#

Spain fits your expansion thesis only if you can run the compliance cadence, not just onboard users. If you cannot support ongoing Social Security payment operations plus recurring tax steps, defer launch until ownership is clear.

Step 1 Weigh market access against recurring admin#

The deciding factor is recurring operational load. RETA is not a one-time task: Social Security contributions can be paid by bank direct debit, so you need day-one support for payment status, account changes, and reconciliation.

AEAT adds recurring tax work that often drives support volume. For many self-employed users in direct estimation, Modelo 130 has filing windows of 1 to 20 April, July, and October, and 1 to 30 January. Modelo 303 adds VAT self-assessment, including a Q4 window from 1 to 30 January, and AEAT also publishes monthly VAT windows for applicable taxpayers. Annual income tax is separate through Modelo 100, and AEAT shows the Renta 2025 campaign starting 8 de abril de 2026.

| Touchpoint | Operational impact | Common failure point |

|---|---|---|

| RETA contributions | Ongoing bank direct debit handling | Failed debits, bank-account changes, payment-status questions |

| Modelo 130 | Recurring IRPF touchpoints for many self-employed users | Deadline spikes in April, July, October, and January |

| Modelo 303 and Modelo 100 | VAT cadence plus annual Renta obligations | January compression and annual document collection |

Step 2 Stress-test your support design#

Before launch, stress-test support around three predictable blockers: NIE, Tax Agency registration, and alta en el RETA. The NIE is the foreigner identifier used for economic and professional dealings in Spain, and Social Security guidance states users need a Social Security number before requesting affiliation and active contributor status.

Map each stall point and assign an owner before go-live. If you defer filing support design, the gap usually shows up first during January deadline overlap.

Step 3 Set a hard go or no-go checkpoint#

Proceed only when ownership is documented for filing guidance, exception handling, payment support, and record retention. In practice, that means named owners for AEAT questions, RETA issues, and a single evidence location.

Keep this checkpoint auditable. Store the exact AEAT or Importass page used, filing receipts, and relevant bank direct debit confirmations. If those records do not have clear ownership, Spain is still a pilot, not launch-ready.

If you want a deeper dive, read The Best Bank Accounts for Freelancers in Spain.

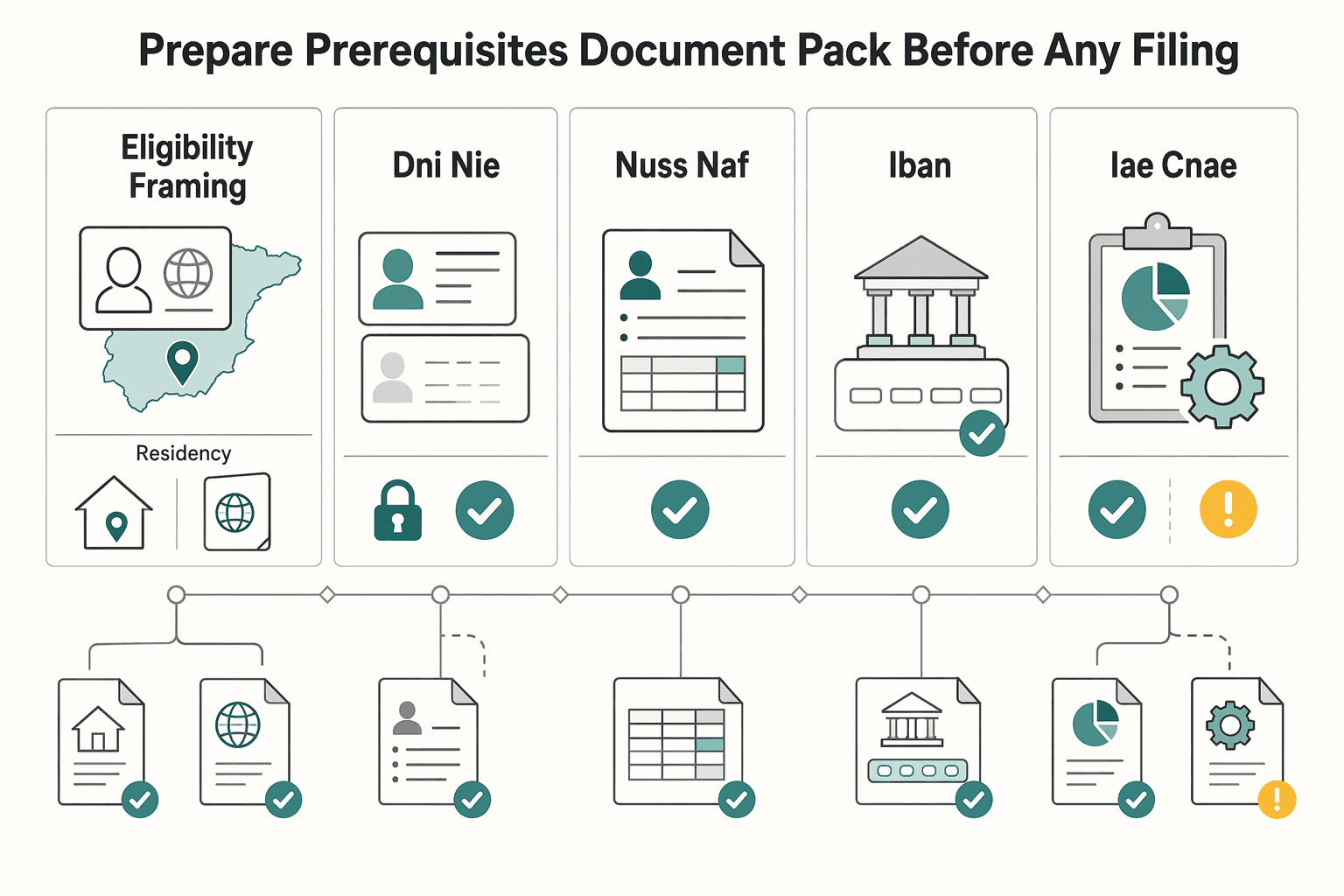

Prepare prerequisites and a document pack before any filing#

Do not file anything until identity fields, payment details, and filing inputs are verified end to end. Most setup failures come from trying to correct core data after submission.

| Item | Stage | Detail |

|---|---|---|

| Eligibility framing | Before any filing | Confirm the user is a Spanish resident in Spain or a foreign national with work authorization |

| DNI or NIE | Before any filing | Verify the exact field match; NIE mismatches can cause the alta to be rejected |

| NUSS or NAF | Before any filing | Verify the exact field you will submit |

| IBAN | Before any filing | Used for payment domiciliation; if a Spanish bank account is required, confirm it is open and debit-ready |

| IAE and CNAE codes | Before opening Modelo 036/037 | Prepare them with the activity start date and estimated monthly net income |

| Activity start date | Before opening Modelo 036/037 | The alta can be filed the same day work starts or up to 60 days before |

| Estimated monthly net income | Before opening Modelo 036/037 | Prepare it in one pass with the other filing inputs |

Step 1 Verify identity, eligibility, and payment prerequisites. Confirm the user matches the basic eligibility framing (Spanish resident in Spain, or foreign national with work authorization). Then verify the exact fields you will submit: DNI or NIE, NUSS or NAF, and the IBAN for payment domiciliation. If your onboarding requires a Spanish bank account, confirm it is already open and debit-ready. Treat exact field matching as a hard gate, especially for NIE, because mismatches can cause the alta to be rejected.

Step 2 Assemble the Hacienda payload before opening Modelo 036/037. Pull the filing inputs together in one pass: IAE and CNAE codes, activity start date, and estimated monthly net income. Draft your first invoice template at the same time so activity description, dates, and taxpayer details stay aligned with what is filed. Assign tax-calendar ownership now, before signup. Keep the filing window in view: the alta can be filed the same day work starts or up to 60 days before.

Step 3 Build a proof file support can use under pressure. For each submission, store what was submitted, where, by whom, and when, plus the acknowledgment or receipt. Keep the filed data, the domiciliation IBAN, and any justificante generated for account-domiciliation requests. Also log bank-detail change timing: requests made between days 1 and 13 apply that same month, while requests from day 14 apply the following month.

For a step-by-step walkthrough, see Portugal NHR vs Spain Beckham Law for High-Earning US Expats in 2026.

Register with the Tax Agency first using Modelo 036/037#

File the AEAT census alta first, then submit alta en el RETA. In practice, this is the cleanest sequence: complete Modelo 036/037 with Hacienda, confirm it is accepted, and then move to Social Security. It aligns with practitioner guidance and with Importass guidance that the Social Security alta should coincide with the Hacienda alta and be completed before, or on, the activity start date.

Step 1 File the census alta with Hacienda first#

Your first live filing should be the Tax Agency census registration via Modelo 036/037. In practice, the fiscal side starts with this alta. Treat RETA as the second move, not a parallel guess, so your start date, activity profile, and identifiers are already fixed in an accepted tax filing.

Step 2 Confirm the Hacienda acknowledgment before RETA#

Do not move forward on "submitted"; move forward on "acknowledged." Save the Hacienda receipt or acknowledgment with timestamp and filed data in your proof file, then verify the start date and identifiers match what you will use for RETA.

This checkpoint matters because proof of Hacienda alta is commonly requested on the Social Security side, especially for in-person handling.

Step 3 Submit alta en el RETA only after proof exists#

If RETA is attempted before the Tax Agency setup is in place, you can create avoidable rework, including possible rejection or correction loops. Keep the timing rule in view: both altas should be completed before or on the activity start date, and filing late can mean losing quota benefits and possible surcharge risk.

If you are close to launch, keep the order tight: Hacienda alta, acknowledgment check, then RETA.

You might also find this useful: A Deep Dive into Spain's 'Autónomo Tarifa Plana' for New Freelancers.

Complete alta en el RETA with Social Security within the allowed window#

After your tax alta is filed, complete alta en el RETA with matching data and within the official timing window so your registration stays compliant and operationally clean.

Step 1 Submit alta en el RETA with matching data#

Use your accepted Modelo 036/037 filing as the reference when you submit RETA. Keep the start date, NIE, activity details, and bank account data aligned across both filings.

Treat mismatches as a stop signal, not a minor edit. If the tax filing and RETA data do not line up, correct the draft before submission.

Step 2 File inside the allowed timing window#

The timing rule is strict: RETA can be processed up to 60 días in advance, and both altas should be completed before or on the same day the activity starts.

| Timing point | What the article says |

|---|---|

| Up to 60 days before start | RETA can be processed in advance |

| Before or on the activity start date | Both altas should be completed before or on the same day the activity starts |

| After activity start | The alta is treated as the first day of that month, and late filing can mean losing quota benefits and possible surcharges |

| After 30 days from start | The request must go through Registro Electrónico |

If filing happens after activity start, the alta is treated as the first day of that month. Late filing can mean losing quota benefits and possible surcharges, and after 30 días from start, the request must go through Registro Electrónico.

Step 3 Set up cuota direct debit and plan month-one cash#

Once RETA is active, you are required to pay a monthly cuota. Payment is handled by domiciliación, so a usable IBAN is required for direct debit setup.

Operationally, this is a cash-timing control, not just paperwork. The linked account needs enough balance from the first billing cycle to avoid preventable payment issues.

If first-time completion starts dropping at this step, route users into assisted flows before you scale acquisition.

Keep location-led planning separate from the autónomo launch checklist: immigration, banking, and tax setup all need their own evidence trail.

Model year one and year two costs before you promise launch dates#

Do not price Spain from the first RETA debit alone. Model year one and year two together, because the tarifa plana changes only the RETA cuota and does not remove VAT, IRPF installments, or annual Renta work.

Step 1 Separate Social Security from tax filings#

Split obligations into separate lines from the start: Social Security contributions on one side, tax filings on the other. For new autónomos, the tarifa plana baseline is 80 € al mes for the first 12 months, and that belongs only in the RETA line.

Tax obligations still run in parallel. Modelo 303 (VAT) is filed quarterly in April, July, October, and Q4 in January. Modelo 130 (IRPF installment for direct estimation) follows the same quarterly cycle, with the January window through 30 January. Renta remains annual, with the 2025 campaign starting 8 April 2026.

Use this control check: if your reduced-rate assumption lowers VAT or Renta burden, the model is wrong.

Step 2 Build two year two scenarios, not one#

Year two should always be modeled two ways.

The extension path: you can request a 12-month prórroga if the tarifa plana was used after 1 January 2023 and expected net returns are below the SMI. In that case, the 80 € monthly cuota may continue during the extension period if requested and applicable.

The non-extension path: if extension conditions are not met or not asserted, year two moves to general cuota logic, where the cuota de autónomos is a percentage of the contribution base. Do not publish a specific year-two euro amount without the exact official 2026 table line for that case.

| Line item | Year 1 baseline | Year 2 if extension is requested and applicable | Year 2 if no extension |

|---|---|---|---|

| RETA cuota | 80 € per month for first 12 months | 80 € per month for up to 12 more months | General cuota applies based on contribution base |

| VAT filing overhead | Modelo 303 quarterly | Modelo 303 quarterly | Modelo 303 quarterly |

| IRPF installment overhead | Modelo 130 quarterly if in direct estimation | Modelo 130 quarterly if in direct estimation | Modelo 130 quarterly if in direct estimation |

| Annual income tax | Renta still applies | Renta still applies | Renta still applies |

| Admin support assumption | Standard onboarding plus filing reminders | Higher eligibility and evidence review load | Higher pricing and objection-handling load |

Step 3 Verify extension evidence before you message price#

Do not treat prórroga as automatic. Keep proof for first alta timing, post-1 January 2023 framing, and the basis for the expected below-SMI return used in the request. If that file is incomplete, message the non-extension path by default.

The common failure mode is simple: teams market Spain as low cost from year-one 80 €, then users hit year two with unchanged VAT, IRPF, and Renta obligations and potentially higher RETA cost. Do not publish low-cost positioning unless your forecast, support scripts, and help content all cover post-reduced-rate behavior.

We covered this in detail in Spain vs Portugal Digital Nomad Visa for a Confident 2026 Move.

Build an ongoing compliance cadence for VAT, Renta, and recurring filings#

Treat compliance as a system, not a reminder list: assign owners for the monthly RETA debit, quarterly tax filings, and annual Renta before you scale.

Step 1 Assign the recurring calendar before the first invoice. Set three live cycles and named ownership for each. RETA contributions can run by direct debit, and the monthly charge is shown for the last business day of the month. For taxes, Modelo 303 (VAT) is filed on a quarterly period as a general rule, and Modelo 130 belongs on that same quarterly rhythm when direct estimation applies. For the annual cycle, map Renta explicitly, with AEAT listing 8 April 2026 as the start of the Campaña de Renta 2025.

| Cycle | What must happen | Owner | Required data | Proof to retain | Escalation path |

|---|---|---|---|---|---|

| Monthly | RETA quota charge is monitored | Finance or ops owner | Bank account on file, expected cuota amount | Bank debit evidence and monthly check log | Failed debit, missing charge, or unexpected amount triggers finance review |

| Quarterly | Modelo 303 filed, and Modelo 130 filed if direct estimation applies | Tax owner, gestor, or supervised finance lead | Invoice totals, expense support, quarter mapping | Filing acknowledgment and working papers | Missing invoices, unclear expense treatment, or total mismatches trigger tax review before filing |

| Annual | Renta prepared and submitted in campaign window | Tax owner with user signoff where needed | Full-year income and expense records, prior quarterly filings | Submission receipt and year-end reconciliation file | Material mismatch or incomplete records trigger qualified review |

Step 2 Build an execution checklist, not just reminders. For each cycle, define: who files, how the due date is confirmed, which dataset is final, where proof is stored, and who takes over if records are incomplete. A task is complete only when the filing is submitted, acknowledgment is saved, and the numbers are still explainable later. For RETA, confirm the debit landed and matches expectation. For quarterly filings, freeze invoice and expense inputs before filing starts.

Step 3 Reconcile invoiced activity against what was declared to Hacienda. At quarter end, reconcile invoices, cancellations or refunds, and expense support to the figures filed in Modelo 303 and, when relevant, Modelo 130. Store that reconciliation with the filing proof. AEAT's retention frame is 4 years for invoices and justifications, so your records should let another operator rebuild the quarter without depending on memory.

Step 4 Set a scale gate after the pilot. If compliance still depends on manual spreadsheets, deadline memory, or document chasing by email, pause expansion until tooling or partner coverage is in place. That is an operator rule, not a legal requirement, but it prevents avoidable filing misses and weak audit trails. Use at least one full quarter plus one verified month-end debit as the minimum readiness check.

Related reading: FTC Non-Compete Rule Status in 2026 and Freelancer Contract Risk.

Common setup failures and how to recover fast#

Most setup problems are recoverable if you treat them as a sequencing and evidence issue, then correct the record before moving on.

| Failure | Recovery | Reference |

|---|---|---|

| Social Security filed ahead of AEAT | Restart with the AEAT census registration step (Modelo 036) clearly documented before RETA handling | Save the AEAT acknowledgment and log what was corrected, by whom, and on which accepted dates |

| Tarifa plana promised too broadly | Escalate year-two eligibility before promising pricing | Keep messaging narrow: the reduced cuota regime includes an initial 12-month period for qualifying new registrations |

| A quarter cannot be explained | Rebuild it from invoice records, expense support, bank movements, and filing receipts already submitted | AEAT requires preserving invoices and supporting documents for 4 years |

| VERI*FACTU assumed settled | Require Spain-specific checks before rollout | AEAT's VERI*FACTU FAQ set shows updates as of 5 December 2025 |

Step 1 Restart the sequence when Social Security was filed ahead of AEAT. If filings were misordered, rebuild the trail with the AEAT census registration step (Modelo 036) clearly documented before you proceed to RETA handling. Setup guidance also flags timing mismatches and notes Social Security alta can be filed up to 60 days before activity start, but not the reverse. Do not continue until the AEAT acknowledgment is saved, then log what was corrected, by whom, and on which accepted dates.

Step 2 Escalate tarifa plana eligibility before promising pricing. Keep product messaging narrow: the reduced cuota regime includes an initial 12-month period for qualifying new registrations. Do not promise year-two outcomes tied to SMI without case-level review. If support or sales gets this question, route it to qualified tax review before the user commits.

Step 3 Rebuild VAT and Renta evidence from source systems, then lock retention. When a quarter cannot be explained, reconstruct it from invoice records, expense support, bank movements, and filing receipts already submitted. AEAT requires preserving invoices and supporting documents for 4 years. The real failure is not just missing documents, but declared totals that cannot be reproduced later.

Step 4 Require Spain-specific checks before rollout, especially for VERI*FACTU. Generic freelancer playbooks are not enough for Spain. AEAT's VERI*FACTU FAQ set shows updates as of 5 December 2025, and the rule family requires billing systems to generate and store or send records to AEAT at invoice issuance. Before production, confirm your invoicing flow can meet those mechanics and that filing steps follow Spain-specific forms and timing.

This pairs well with our guide on How to Set Up Chart of Accounts in QuickBooks for a Freelancer.

Conclusion and copy-paste launch checklist#

Use this as your go-or-no-go gate. If you cannot pass every item below with a named owner and saved proof, you are not ready to launch Spain as an autónomo flow.

-

Verify identity and bank readiness before any filing. Confirm the user's DNI or NIE is valid for the process, and the bank account used for direct debit is active. Guidance expects a bank account for domiciling payments and, if needed, refunds.

-

Use Tax Agency registration as an internal handoff point, while keeping dates aligned. Use Modelo 036 or 037 for censal registration with Hacienda, and save the receipt. Official guidance stresses timing alignment: the AEAT start date and the RETA start date should coincide, and both registrations should be completed before, or on, the activity start date.

-

Submit alta en el RETA within the allowed window and check the dates twice. Importass states the alta must be requested before starting the activity, and it can be filed up to 60 días in advance. The verification step is simple but important: compare the activity start date on the tax filing with the RETA start date before submission.

-

Test the payment path and track the first operational signals. RETA is not done when the form is sent. It is operational when the payment route is working and someone is checking it. Save the bank proof, the registration acknowledgment, and any first debit or exception notices once they appear.

-

Turn the tax calendar into a live obligation, not a note in onboarding. Your baseline should include quarterly IRPF installments via Modelo 130 on 1 to 20 April, July, and October, plus 1 to 30 January. For VAT, your checklist should include Modelo 303 and at minimum the published Q4 window of 1 to 30 January. For annual filings, keep the 2026 online Renta window in view: 8 April to 30 June 2026 for the 2025 return.

-

Log open compliance unknowns with review dates. Keep a dated open-issues log for moving items such as VERI*FACTU, because AEAT has already published adaptation updates and that is your signal to review again before scale-up.

Frequently Asked Questions

What is the correct registration order to become an Autónomo in Spain in 2026?

Coordinate Tax Agency registration through Modelo 036 and alta en el RETA through Importass so both start dates coincide. Official guidance says the RETA alta must coincide with the AEAT alta and must be requested before you start activity. The working checkpoint is simple: save the tax filing receipt and make sure both start dates match.

How long can the freelancer reduced rate under RETA last, and what affects extension eligibility?

The confirmed starting point is 80 € per month for the first 12 months for eligible new registrations. A further 12-month period may apply if expected net income stays below the vigente SMI threshold. The red flag is promising that second-year rate too early, because it turns on an income condition, not just on being newly registered.

Does the reduced Social Security rate replace VAT or Renta obligations?

No. The cuota reducida only affects your RETA contribution. IVA filings such as Modelo 303 and IRPF installment payments such as Modelo 130 remain separate obligations, so a low RETA cost does not mean low tax admin.

What is alta en el RETA, and when should it be filed around Modelo 036?

Alta en el RETA is the registration into Spain’s self-employed regime. It must be filed before activity starts, and Importass states you can process it up to 60 días in advance. In practice, coordinate both filings so the dates line up cleanly, and make sure direct-debit details are ready.

What are the minimum prerequisites before filing, including NIE and bank account readiness?

You need an identity document accepted for the process, including NIE, and a bank account to domiciliar the cuota. Before filing, verify that the bank account is active for direct debit and that the account-holder details match the filing record. If you skip that check, you can run into issues with cuota collection or refund processing.

Should operators recommend DIY filing, a Gestor, or a managed platform for new entrants?

There is no universal winner. DIY is reasonable for a simple case if the person can keep receipts, align AEAT and RETA dates, and handle follow-up. If your users are first-time entrants, non-Spanish speakers, or likely to ask tarifa plana edge-case questions, route them to a gestor or managed option before they commit.

What is still unknown from public guidance, including parts of VERI*FACTU, and how should teams handle that uncertainty?

Treat VERI*FACTU as an active compliance area, not a settled checkbox. AEAT has published adaptation notices, which is the clearest sign that details can still move. The practical response is to keep an open-issues log, verify the latest AEAT update before launch, and avoid product claims that assume every 2026 invoicing scenario is already final.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- portal.seg-social.gob.es/wps/portal/importass/importass/Categorias/Al...trusted

- portal.seg-social.gob.es/wps/wcm/connect/importass/importass_contenid...trusted

- sede.agenciatributaria.gob.es/Sede/iva/sistemas-informaticos-facturacion-v...trusted

- sede.agenciatributaria.gob.es/Sede/procedimientoini/G322.shtmltrusted

- expatwires.com/spain/money-work/autonomo-spain-guideexternal

- legalitas.com/actualidad/como-darse-alta-autonomoexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Freelancer Bank Accounts in Spain: Choosing a Primary and Backup Setup

Choose your setup as a risk decision, not a brand ranking. Pick one primary account for daily inflows and keep one backup account active in the same planning session.

Spain Autonomo System for Freelancers Who Want Compliance Control

Low-stress compliance comes from predictable execution, not tax-shortcut bets. Keep filings clean, document decisions, and set escalation triggers before deadlines.

Spain’s Autónomo Tarifa Plana for New Freelancers in 2026

Use the tarifa plana to buy compliance control, not lifestyle drift. The discounted phase, often around **€80/month**, gives you room to set up the unglamorous parts properly. That matters because your social security cost later moves into a more normal **€230 to €530/month** range.