Quick Answer

Set up your QuickBooks chart of accounts as a freelancer by starting lean, not broad: create core buckets for income, processing fees, clearing, and owner activity, then map ACH, PayPal, and Venmo with consistent rules. Separate gross, fees, and net deposits, and treat Fiverr.com and Freelancer.com as distinct income streams. Expand only when reporting or workflow needs justify it so your books stay clean and cashflow decisions stay fast.

Your QuickBooks setup should protect cashflow not just track expenses#

Use your Chart of Accounts to expose cash timing, fees, and follow-up actions, not just expense totals. If you're a business-of-one, your books are your cash system, not a scrapbook of expenses.

If you run as a sole proprietor or lean team, control starts here. A cluttered Chart of Accounts slows decisions because your Profit and Loss and Balance Sheet can blend categories instead of surfacing clear operating signals. You may spot issues too late and miss fee or unpaid-invoice patterns.

Start with a durable freelancer baseline in your first setup pass. Keep it minimal, then expand only when a clear trigger appears. That keeps your QuickBooks setup practical for daily use and stable enough for month-end bookkeeping.

- Step 1: Build a lean account map.

Create only the core accounts you need to run the business this month: revenue, processing fees, clearing, and owner activity. In QuickBooks, account type and detail type determine where data appears in reports. Choose names and types you can defend in a review. Outcome: You can open reports and separate performance from cash movement quickly.

- Step 2: Set rail-specific rules before transactions pile up.

Downloaded bank activity needs consistent categorization, so set rail logic now for ACH, PayPal, and Venmo.

| Rail | Operational reality | Rule for your Chart of Accounts |

|---|---|---|

| ACH | Reaches U.S. bank and credit union accounts | Post ACH receipts through a dedicated clearing path, then reconcile to deposit status. |

| PayPal | Domestic transactions occur when both parties are in the same market | Track PayPal gross receipts and PayPal fees separately so market-based fee behavior stays visible. |

| Venmo | Instant transfer typically lands within 30 minutes and charges 1.75% (minimum $0.25, maximum $25) | Log instant transfer fees in a distinct fee bucket so speed decisions do not blur margins. |

- Step 3: Add expansion triggers, not account sprawl.

Add a new account only when you add a new rail, face a repeat dispute pattern, or need a report your current structure cannot produce. For example: you start with direct invoices, then a new client asks for Venmo payouts. You add one rail-specific clearing and fee path, keep naming consistent, and move on. Outcome: You keep the books clean now and scale without rework. Want a quick next step? Try the free invoice generator.

What to prepare before you touch your Chart of Accounts#

Pick your QuickBooks product lane, collect real transaction evidence, and assign review ownership before you change your Chart of Accounts. This prep keeps your setup grounded in real cash movement. You are not expanding categories yet. You are setting inputs so your Chart of Accounts supports decisions, clean reports, and tight financial organization.

| Prep step | What to confirm |

|---|---|

| Choose your product lane first | You choose a path that matches real control needs, not marketing labels. |

| Gather transaction evidence by rail and source | You can explain each transaction by rail, source, and business purpose without guessing. |

| Map income origins before category names | Your Chart of Accounts reflects how money actually enters the business. |

| Assign review cadence and escalation path | Every unclear transaction gets an owner, a due date, and an escalation path. |

Before you start#

- Step 1: Choose your product lane first.

Match your workflow to product capabilities before you touch account structure.

| Product lane | Good fit | What it means for your Chart of Accounts |

|---|---|---|

| QuickBooks Solopreneur | One-person business operations | Keep accounting basics lean and avoid category sprawl early. |

| QuickBooks Self-Employed | Solo business tracking workflows | Use a simplified structure, and if you need onboarding context, review A Guide to QuickBooks Self-Employed for Freelancers. |

| QuickBooks Online Simple Start | You need Chart of Accounts customization | Build a more explicit Chart of Accounts structure from day one. |

Intuit ended new QBSE mobile app downloads after March 24, 2024, so check your current account state before you commit. Outcome: You choose a path that matches real control needs, not marketing labels.

- Step 2: Gather transaction evidence by rail and source.

Pull recent activity from your bank, PayPal, Venmo, and card channels before drafting categories. Connect to PayPal 2.0 imports transactions daily and supports start dates up to 90 days back. Depending on the flow, historical imports can extend further, including references up to 18 months. Export Venmo account statements as CSV, then stage everything in one review sheet. Verification point: You can explain each transaction by rail, source, and business purpose without guessing.

- Step 3: Map income origins before category names.

List direct client invoices separately from marketplace payouts. If a payout bundles fees and earnings, flag it now so your rules can categorize it consistently later. Labeling source first prevents cleanup chaos at month end. Outcome: Your Chart of Accounts reflects how money actually enters the business.

- Step 4: Assign review cadence and escalation path.

Name one owner for final classification decisions, then add a short daily review for rule-applied transactions. When ambiguity appears, escalate through QuickBooks Community, and route complex cases to QuickBooks Live Experts. Verification point: Every unclear transaction gets an owner, a due date, and an escalation path.

What is the safest starter Chart of Accounts for a freelancer?#

Start with a minimal, stable Chart of Accounts, separate income types and collection costs, then expand only when you need clearer reporting. Build a structure you can run consistently. The goal is not perfect theory. The goal is decisions you can trust: where money came from, what it cost to collect, and what is still unsettled.

| Expansion trigger | Action |

|---|---|

| Current reports cannot answer a recurring operating question | Add an account. |

| A new income stream needs separate visibility | Add an account. |

| Fees or unsettled balances are material enough that separate tracking improves decisions | Add an account. |

A Chart of Accounts is an organized list of accounts in the general ledger. Keep it simple early. In QuickBooks, account type and detail type determine where data appears in reports, so structure matters from day one.

- Step 1: Build core buckets before edge cases.

Create only the accounts you need to run this month, then stop. QuickBooks also supports splitting income into separate line items instead of one lump category.

| Layer | What you separate | Starter example in your QuickBooks setup |

|---|---|---|

| Income type | Direct clients vs platform work | Income Direct Client, Income Platform Work |

| Collection costs and unsettled funds | Gross receipts vs fees vs clearing balances | Processing Fees, Payment Clearing |

Verification point: You can read the Profit and Loss and see where money came from, plus what payment handling cost you.

- Step 2: Lock naming rules before growth.

Use one naming pattern and keep it fixed. If you create near-duplicates, QuickBooks can auto-suffix account names with labels like -1 and -2, which weakens reporting clarity fast. Pick one pattern now and enforce it during monthly review.

- Step 3: Add accounts only when reporting needs it.

Treat expansion as a controlled decision, not a reaction. Rules vary by business, so use your reporting needs as the trigger.

- Add an account when your current reports cannot answer a recurring operating question.

- Add an account when a new income stream needs separate visibility.

- Add an account when fees or unsettled balances are material enough that separate tracking improves decisions.

A typical progression: you start with direct invoices, then add a platform channel and one clearing account. You add only the related income and clearing accounts and keep naming consistent.

- Step 4: Use the overengineering warning as a guardrail.

A ProAdvisor-cited warning is straightforward: overcomplicating the Chart of Accounts with too many accounts makes bookkeeping harder and more time-consuming. Make that your policy. Outcome: Your chart stays lean, your reports stay usable, and the system scales without losing control.

How do you map payment rails to cleaner cashflow visibility?#

Map each payment rail to its own clearing flow, fee capture, and status checkpoints so you can see real cash position before reconciliation. A lean Chart of Accounts is only the start. This is where it becomes a system: every rail has a consistent path from receipt to deposit, and fees never disappear inside revenue.

Build your rail map in QuickBooks Online#

- Step 1: Define clearing and fee accounts.

Set Undeposited Funds as your interim holding point for incoming payments, then choose the bank deposit account you want QuickBooks to post into. Use a dedicated processing-fees expense account so fees never hide inside revenue. Verification point: You can trace one payment from receipt to deposit and see fees in a separate expense line.

- Step 2: Split gross, fees, and net at posting time.

Do not post only the net settlement. Record gross receipts first, then record fee withdrawals and final settlement as separate entries so reports stay accurate.

| Rail | Receipt event | Settlement event | Fee handling |

|---|---|---|---|

| ACH | Record payment to clearing | Move to bank when deposit completes | Track bank or processor fees separately |

| PayPal | Record gross payment | Record payout deposit separately | Record fees separately from income |

| Venmo | Record gross payment | Record payout deposit separately | Record fees separately from income |

For third-party processor flows, record final payout deposits and fees explicitly. That discipline keeps your accounting basics intact when rails behave differently.

- Step 3: Standardize status checkpoints.

Use one internal status chain across rails, such as Sent, Pending, Deposited, Held, Returned, Refunded, and map each payment into that chain. QuickBooks lets you view PayPal or Venmo transaction status in the Sales tab. Manual ACH entries can face security-check delays, so your checkpoints must match operational timing. Verification point: Every in-flight payment has one current status and one owner.

Protect your primary income categories#

- Step 4: Create a dispute and reversal path.

When a chargeback notice arrives for PayPal or Venmo, assign action immediately and complete required response steps within 5 calendar days. If you must reverse a payment, void the receive-payment transaction and route dispute activity to dedicated reversal accounts, not primary income categories. Outcome: You preserve cash flow visibility without distorting margin or revenue trends.

Which QuickBooks product setup fits your workflow right now?#

Choose Solopreneur for one-person simplicity, and move to QuickBooks Online when you need more accounting control. Your product choice determines how much control you have over chart setup, reporting, and collaboration as complexity grows.

Control depth means three things: how far you can customize your Chart of Accounts, how much reporting flexibility you get, and how easily you can collaborate with an accountant in Intuit products.

- Step 1: Compare lanes by control depth.

| Product lane | Best fit right now | Control signals to watch |

|---|---|---|

| QuickBooks Solopreneur | One-person operators with simple bookkeeping needs | Start here if you want a lean setup and minimal admin overhead. |

| QuickBooks Self-Employed (QBSE) | Solo workflows that still stay simple | Keep it while your accounting basics stay straightforward; move up when you need more advanced bookkeeping features. |

| QuickBooks Online (Simple Start and above) | Freelancers who need more structure | Choose this when you need Chart of Accounts customization, stronger report depth, or accountant collaboration tools. |

- Step 2: Run a practical decision check before you commit.

- Bookkeeping complexity: If your bookkeeping needs become more advanced, move toward QuickBooks Online.

- Chart of Accounts needs: If you need to customize your Chart of Accounts, QuickBooks Online Simple Start is a practical next step.

- Collaboration needs: If you want an accountant to review books and make corrections directly, QuickBooks Online supports accountant-user workflows.

- Reporting depth: If you need broader reporting and multi-user access, QuickBooks Online tiers scale from lean access to wider team access and larger report libraries.

- Step 3: Set safe defaults and clear upgrade triggers.

Start lean, then upgrade when your workflow asks for control you cannot get in your current lane. For example: if you outgrow basic bookkeeping and need custom accounts plus regular accountant collaboration, upgrading helps keep your books organized and reduces rework. Verification point: You can explain why your current product fits today, and name the exact trigger that will make you switch.

How do you categorize Fiverr.com and Freelancer.com transactions without rework?#

Treat Fiverr.com and Freelancer.com as separate streams, then map gross, fees, and clearing status before you accept net cash coding. Set your platform rules early so new payouts follow the same logic, then review what lands in QuickBooks before you finalize categories.

- Step 1: Separate platform sources in your tracking setup.

Use distinct categories or tags for Fiverr.com, Freelancer.com, and direct client work. In QuickBooks Online, downloaded transactions land in the Pending tab with suggested categories, and you can change them before accepting. Verification point: Your reporting can show platform activity separately from other income activity.

- Step 2: Split each payout into gross income, platform deductions, and net cash.

Do not book only the net deposit. Record the full transaction flow.

| Flow item | Fiverr.com rule | Freelancer.com rule |

|---|---|---|

| Gross service income | Record the full cleared order amount as income | Record full project income before deductions |

| Platform fee | Record platform take separately because freelancers receive 80% of the client's cleared payment | Record project fee separately because fees can be 10% of the bid or $5, whichever is greater |

| Clearing and withdrawal | Track cleared earnings separately from withdrawable cash when timing differs | Track settlement timing separately when payout date differs from earning date |

If a deposit includes mixed items, split lines so service revenue is not overstated.

- Step 3: Automate repeat patterns with rules and tags.

Set bank rules by payee text and transaction pattern, then assign transaction type, category, tags, and payee. QuickBooks supports up to 2,000 bank rules, so you can automate common platform flows and keep coding consistent. Use tags for analysis because tags do not affect the general ledger. Outcome: You reduce manual recoding while keeping control.

- Step 4: Route incomplete items into a weekly exception routine.

When a memo lacks project detail, hold the item for review, add a note explaining why you paused it, and resolve it in your weekly review. In QBSE, mark mixed-use transactions as Split when needed. If ambiguity remains, flag uncertainty and confirm treatment with your accountant using your note history.

A common scenario: a payout arrives without a clear client identifier. Hold it, add context, and clear it during the next review instead of guessing. Verification point: You can read your notes later and follow the reasoning behind each classification decision.

What breaks most freelancer books and how do you recover fast?#

Freelancer books often break when you let account names drift, post net payouts without fee detail, and skip a strict tie-out routine. When the books break, you need a recovery sequence that restores reporting fast and prevents repeat errors.

| Failure mode | What it breaks | Fast recovery move |

|---|---|---|

| Account sprawl and inconsistent naming | Reporting clarity and trend tracking | Merge duplicates, lock a naming standard, and stop ad hoc account creation |

| Miscategorized rail activity | Margin and cashflow visibility | Reclass in batches, then reconcile by rail |

| Duplicate or unclear platform entries | Revenue accuracy and fee tracking | Tie each payout to platform statements before month close |

- Step 1: Standardize names and remove account sprawl.

A common pain pattern is too many near-duplicate accounts and labels that change meaning month to month. Keep one clear naming pattern for income, fees, clearing, and reimbursables. If a new account does not support a new workflow, do not create it. Verification point: You can explain each account in one sentence and classify every new transaction without guessing.

- Step 2: Lock the period and reclass rail errors in bulk.

Run a short lock-and-review pass before you touch old reconciled periods. Use the Reclassify Transactions tool for batch cleanup if you work in QuickBooks Online Advanced or QuickBooks Online Accountant. If you need a full reconciliation rollback, bring in your accountant instead of forcing a full undo yourself.

If your QuickBooks setup lacks batch reclass tools, filter and edit in controlled batches, then reconcile each payment rail line by line. Verification point: Reconciled balances match statements, and uncategorized rail entries drop to zero.

- Step 3: Tie out Fiverr.com and Freelancer.com with payout evidence.

Map each payout to three lines: gross income, platform fee, and net cash. Do not post net cash as revenue. Use Match in bank feeds to link downloaded items to existing records and avoid duplicates, and remember pending bank items will not download until posting completes. Fiverr yearly earnings documents help you confirm period totals. Verification point: Every deposit maps to one platform payout record, with no orphan or duplicate entry.

- Step 4: Add cross-border compliance reminders to your monthly close.

Create a reminder to review foreign account exposure with FinCEN FBAR rules if aggregate foreign account value exceeds $10,000 at any point in the year. Add a second reminder for FATCA-related review, since certain U.S. taxpayers may need Form 8938 when specified foreign assets exceed base thresholds such as $50,000. Form 8938 does not replace FBAR, so verify both obligations where applicable.

If a platform payout looks unclear in one month, park it in clearing, note the reason, and clear it after statement tie-out. That habit protects cash visibility without forcing guesswork. If you want a deeper dive, read Value-Based Pricing: A Freelancer's Guide.

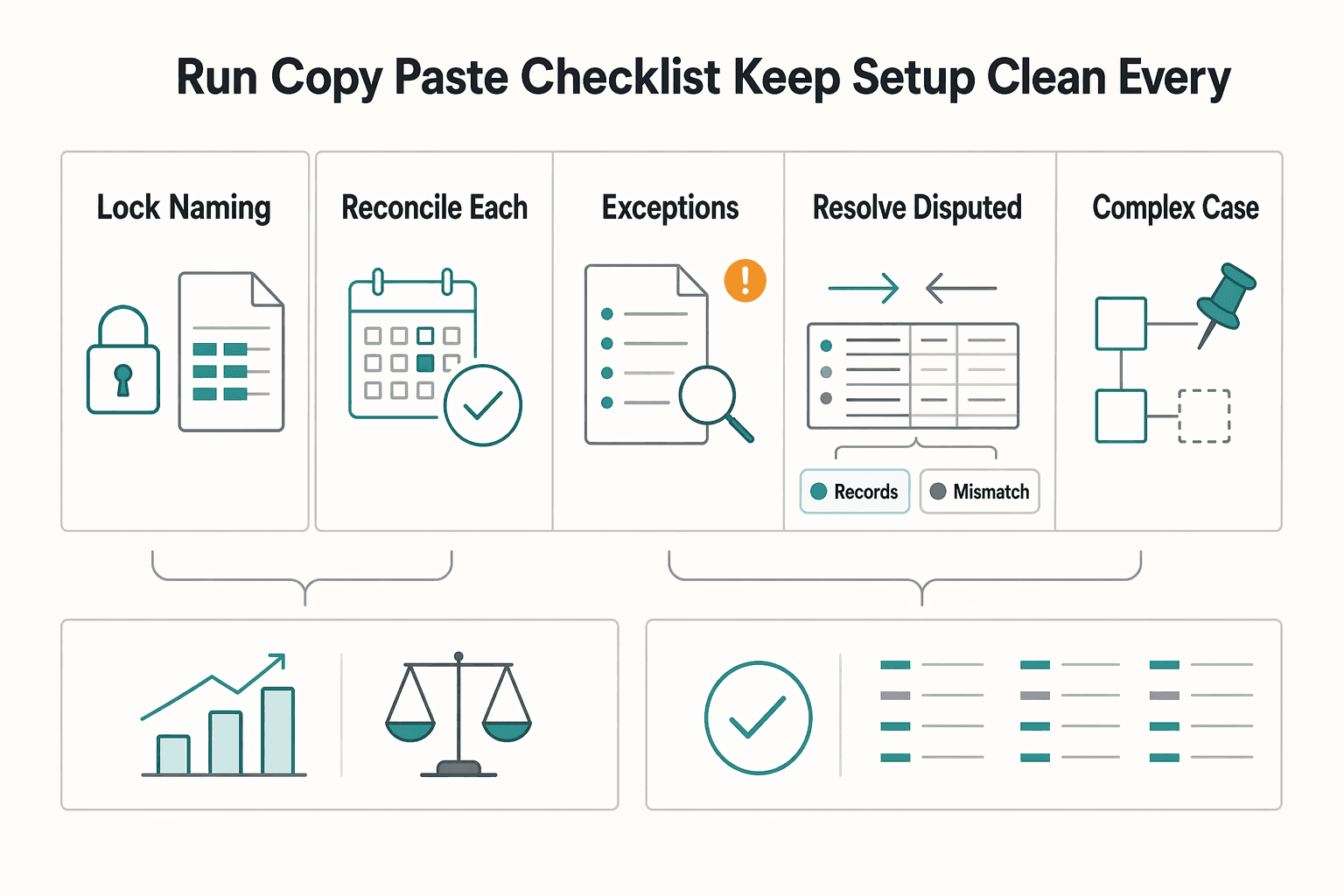

Run this copy paste checklist to keep your setup clean every month#

Run one disciplined close routine each month so your books stay decision-ready, audit-ready, and easy to trust. This is the operational loop. If you run it monthly, your Chart of Accounts stays lean, your rails stay reconcilable, and exceptions stop piling up.

| Monthly check | Verification point |

|---|---|

| Lock your naming standard in the Chart of Accounts | Your Profit and Loss and Balance Sheet show clean, predictable groupings with no duplicate account names. |

| Reconcile each rail separately before you review performance | Statement balances match, and no rail carries unexplained variance into next month. |

| Clear platform payout exceptions before month close | Every platform deposit ties to a documented payout record. |

| Resolve disputed payments with notes | No dispute sits without a documented next action. |

| Reassess product fit as complexity grows | Your current product supports your reporting depth and collaboration needs. |

| Run a cross-border reporting check | You log whether each filing applies, who will file, and what records you need. |

- Step 1. Lock your naming standard in the Chart of Accounts.

Use one naming pattern for income, fees, clearing, and reimbursements, then apply it every month. Keep account types and detail types consistent, because those choices control where numbers appear in reports. Verification point: Your Profit and Loss and Balance Sheet show clean, predictable groupings with no duplicate account names.

- Step 2. Reconcile each rail separately before you review performance.

Reconcile ACH, PayPal, and Venmo as separate flows where you use them. Start with the statement for each account, then confirm all statement-period transactions are added and categorized before reconciliation. If invoice payments came through PayPal or Venmo, confirm deposit behavior and auto-reconciliation timing inside your records. Verification point: Statement balances match, and no rail carries unexplained variance into next month.

- Step 3. Clear platform payout exceptions before month close.

Keep platform entries in a review queue until you can tie them to payout evidence. Use your platform payout records and transaction statuses to resolve unclear timing or status changes. If one payout lands without enough context, park it in clearing, add a short note, and resolve it during close instead of guessing. Verification point: Every platform deposit ties to a documented payout record.

- Step 4. Resolve disputed payments with notes.

Track each issue with owner, status, next action, and expected resolution date. QuickBooks chargeback alerts and Resolution Center details help you move faster, but keep your own notes because PayPal, Venmo, and ACH can follow different dispute-protection treatment. Verification point: No dispute sits without a documented next action.

- Step 5. Reassess product fit as complexity grows.

Review whether QBSE, QuickBooks Solopreneur, or QuickBooks Online still fits your workflow. Existing QBSE subscribers can continue or upgrade, and migration can carry most data including up to three years of transactions. Verification point: Your current product supports your reporting depth and collaboration needs.

- Step 6. Run a cross-border reporting check.

If you hold foreign financial accounts or other specified foreign financial assets, test FBAR exposure at the $10,000 aggregate threshold. Then test Form 8938 thresholds based on filing status, where relevant thresholds can start at $50,000 and can be higher, such as $75,000, $100,000, or $150,000 in specific cases. Evaluate both filings separately, because Form 8938 does not replace FBAR. Verification point: You log whether each filing applies, who will file, and what records you need.

Frequently Asked Questions

What is the simplest Chart of Accounts setup for a freelancer in QuickBooks?

Start with four core buckets: assets, liabilities, income, and expenses. Then add only what you need to keep your records clear. Use clear income names (direct vs platform) and a dedicated processing-fees line so fees do not hide inside revenue.

Do I need a full Chart of Accounts as a Sole Proprietor, or can I start lean?

Start lean. A sole proprietor does not need a long account list to stay organized. If you are using QBSE, full chart-of-accounts capability is not available, so move to QuickBooks Online when you need that deeper setup.

How should I categorize Fiverr.com and Freelancer.com transactions in QBSE?

In QBSE, consistency matters because QBSE maps categories to Schedule C lines. Keep Fiverr.com and Freelancer.com activity distinct in naming. Validate payouts during close using Fiverr yearly earnings statements and Freelancer milestone statuses. If a payout is unclear, park it in review and clear it before month end.

Which is better for my workflow today, QuickBooks Self-Employed or QuickBooks Online?

Choose QuickBooks Self-Employed if you want simple tax-oriented categorization and low complexity. Choose QuickBooks Online if you need full chart-of-accounts capability or accountant collaboration through invited accountant users. If you are deciding between both, use this companion guide: A Guide to QuickBooks Self-Employed for Freelancers.

How does better categorization improve cashflow visibility across ACH, PayPal, and Venmo?

In QuickBooks Online, customers can pay by ACH, PayPal, and Venmo, so categorizing those rails separately makes inflows and fees easier to review than one blended total. Categorization improves clarity, but collection speed and invoicing discipline still determine how fast cash lands in the bank.

When should I add more accounts instead of keeping my setup minimal?

Add accounts when your current structure hides repeat decisions. If a recurring fee pattern keeps getting buried in general expenses, create one dedicated account and keep it permanent. If reports stay clear and review time stays short, do not expand.

What should cross border freelancers know about FBAR, FinCEN, FATCA, and Form 8938 in bookkeeping workflows?

Use reminders so you do not guess at filing time. FBAR (FinCEN Form 114) can apply when aggregate foreign account value exceeds $10,000 during the year. Certain U.S. taxpayers may need Form 8938 when specified foreign assets exceed thresholds such as $50,000. Form 8938 does not replace FBAR, and FBAR is not filed with the IRS, so evaluate both obligations separately.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

A Guide to QuickBooks Self-Employed for Freelancers

**QuickBooks Self-Employed can support basic bookkeeping, but predictable cashflow comes from your payment controls, not invoicing alone.**

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.