Quick Answer

Map the payout path first, then expand only where it is auditable. Start at Affiliate Onboarding, pass identity and tax checks, execute through Payouts API, and close with Commission Reconciliation that matches payable, provider result, and ledger posting. Use one market-and-rail matrix before launch sign-off, and run a dry run that proves who is eligible, who is held, and how returned payouts are resolved. If that chain still depends on spreadsheet stitching, defer rollout.

Where Payout Automation Changes Affiliate Network Decisions#

Affiliate network payout automation only works if you define it as the full commission-to-cash path, not the moment a transfer succeeds. In practice, that path starts with affiliate onboarding, runs through commission logic and contract terms, and ends only when payouts are recorded in a way your team can reconcile.

That distinction matters because affiliate programs create more than payout files. You are expected to track leads, calls, downloads, and sales across channels, along with the contracts and payouts tied to partner performance. At small scale, teams often patch that together with manual checks. As volume grows, those workarounds lead to inefficiencies, errors, and missed opportunities, with month-end close still dependent on spreadsheet stitching.

For founders, the better question is not, "How do we pay affiliates faster?" Ask instead, "Which markets and commission models can we operate cleanly, with control and transparency for both finance and partner teams?" That is the real scope here. The transfer step matters, but it is only one layer. The harder work is keeping partner enrollment, payout instructions, commission approvals, and records connected well enough that you can explain each payment after the fact.

A practical early checkpoint is simple. Can you trace one paid commission from the affiliate's onboarding record to the agreed payout terms and final payout record without rebuilding the story by hand? If that chain breaks anywhere, you do not yet have reliable automation. You have partial automation wrapped around manual risk.

As you add markets, operational complexity usually rises before demand catches up. Processes that look straightforward in one setup can become harder to track and reconcile in another. A common failure mode is treating instant or embedded payouts as the goal, then discovering required partner data is incomplete and the payout cannot clear cleanly.

So the decision lens for the rest of this guide is deliberately conservative. Expand where your payout path is visible and repeatable. If a market looks attractive but your team cannot reliably onboard partners, validate payee data, generate the right payout records, and reconcile disbursements back to source activity, that market is not launch-ready yet.

If you are evaluating payout network structure and compliance boundaries, see How to Build a Payout Network Without a Money Transmitter License for Platforms.

What affiliate network payout automation actually includes#

At an operating level, this is end-to-end work, not just a successful transfer. In practice, it starts when a partner enrolls and submits payout details, and it is only complete when finance can match the payable, payment result, and close records without rebuilding the trail manually.

The clearest operating model is three layers:

- Partner-facing layer: Payout links collect beneficiary details and required partner information.

- Execution layer: Payouts API or payouts automation applies release logic and sends payment instructions. Those rules often use triggers such as signup, approval, sales, refunds, or refund rate, with lookback windows like 7, 14, 30, 60, 90 days, or all time.

- Finance control layer: Commission reconciliation checks whether earned, approved, sent, and posted amounts still agree.

Policy gates still apply across all three layers. KYC verifies identity before opening an account or providing financial services, and affiliate payment programs may require verified contact and tax information for fraud prevention and compliance controls. That means an "instant" payout flow can still stop when required identity or tax data is incomplete or inconsistent. A practical checkpoint is to treat commissions as payout-ready only after earned status, payee details, and tax status all pass review.

For a more detailed look at operational payout design, read Affiliate Network Payouts: How to Pay Publishers and Partners Automatically at Scale.

Match commission structures to payout operations before market entry#

Choose the commission model your payout operations can support, not just the one you want to test. That choice changes dispute handling, invoicing flow, retry risk, and close effort.

PPC pays for clicks, while PPA pays for a lead or sale outcome. In practice, those structures create different payout workloads for publisher partners, especially as payout frequency increases.

Modern affiliate platforms can support flexible commission models, fraud detection, and automated invoicing. That flexibility helps only if each payable can be traced cleanly from source event to approval, invoice, payout instruction, and ledger outcome.

| Commission structure | Payout workload shape | Likely exception pattern | Reconciliation load | Automation priority |

|---|---|---|---|---|

| PPC (click-based) | Higher event volume | More review pressure around click validity and duplicates | Higher, because many small events must still reconcile | Strong event validation, fraud checks, and automated invoicing/commission reconciliation |

| PPA (lead/sale-based) | Lower event volume than click-heavy models | More focus on approval and attribution decisions | Moderate to high, based on approval lag and reversals | Clear approval states, payable-release rules, and end-to-end traceability |

| Monthly consolidated partner payouts | Fewer transfer events per period | Fewer transfer-time exceptions, with period-end adjustments | Lower transfer complexity, but close matching still matters | Reliable batch controls and exception handling during reconciliation |

If you raise payout frequency, deepen controls before launch. Weak controls make unauthorized or duplicate activity harder to catch.

Use one full-path prelaunch check with realistic records. You should be able to trace each payable through:

- source event record (click, lead, or sale)

- approval decision, including hold/reversal status

- invoice line or automated invoicing record

- payout request identifier and provider reference

- final settlement or failure status tied to ledger posting

Do not rely on manual approvals and fragmented compliance checks as a long-term fallback. They create friction early, and that friction compounds once a payout cycle reaches hundreds of transactions across multiple countries.

Related: Mass Payouts for Affiliate Networks: How to Pay Publishers Partners and Creators at Scale.

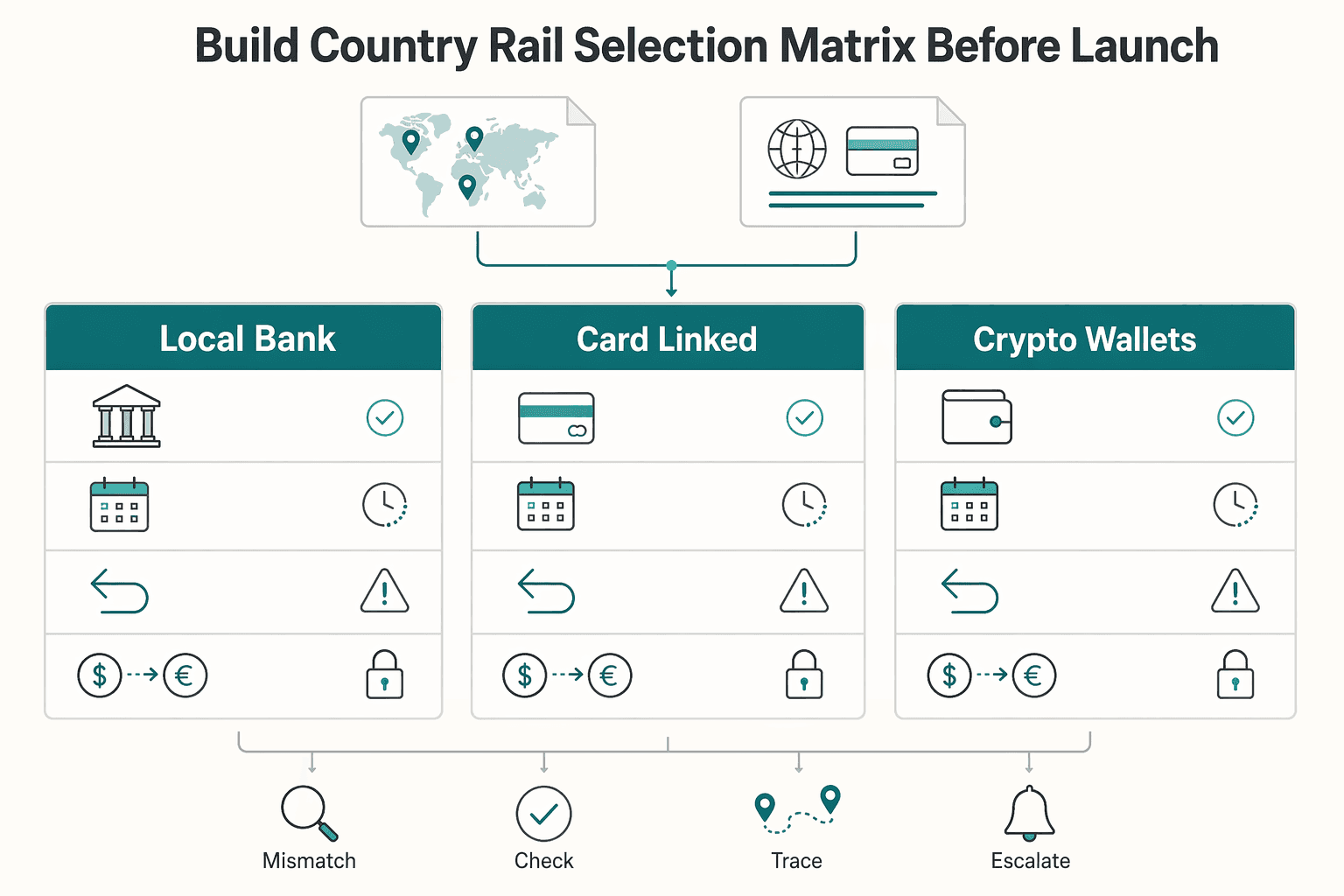

Build a country and rail selection matrix before launch#

Build the market matrix before you commit to local payouts, because rail fit determines whether a market runs predictably or becomes exception-heavy. Start with two inputs, your provider's Coverage Map and International Payments view, and use them to separate "can send funds" from "can run this corridor reliably."

For each target market, compare four items side by side: available payout rails, expected settlement behavior, return behavior, and currency-conversion requirements. Some cross-border routes may support same-day or next-day settlement, but treat that as a route characteristic to validate, not a launch promise.

| Route option | What to verify before launch | Main failure mode to plan for | When it usually makes sense |

|---|---|---|---|

| Local bank transfer via bank portals | corridor availability, beneficiary data requirements, funding currency vs. local currency, return-handling path | returned payouts that require rework | default route for repeat publisher payouts when bank data is validated early |

| Card-linked payout | corridor support, settlement predictability, conversion steps when currencies differ | failed payouts when the card or corridor is not eligible | useful when partners prioritize faster access and corridor support is clear |

| Crypto wallets where supported and compliant | provider support, policy approval, accounting and tax handling, conversion path back to fiat when needed | compliance or reconciliation gaps if launched without explicit controls | only where this path is approved end to end |

Add policy columns, not just payment columns#

A launch-ready matrix needs policy fields per market: onboarding evidence, payout gating, and tax-document readiness. Evaluate those alongside payout methods, global reach, engineering lift, compliance risk, and operating cost so go-to-market decisions map to executable operations.

Before sign-off, each country row should show what makes a partner payout-eligible, what can block release, and what document set finance needs in place before first payout. Run one end-to-end dry run per market and route so you can verify coverage evidence, onboarding requirements, tax readiness, payout activation, and the exception path for returned transfers.

Use a hard defer rule#

If a target market needs manual intervention in more than one critical step, defer launch until controls are automated. If onboarding requires manual review and returned payouts also need manual repair, the market is not operationally ready yet.

Design onboarding, compliance, and tax document flows that scale#

After market and rail decisions, make payout eligibility a controlled gate: standardize onboarding intake, validate in order, and keep policy ownership internal. That is the fastest way to reduce avoidable exceptions and keep decisions auditable as volume grows.

Use one consistent onboarding pattern for affiliates and payees, then apply the same eligibility checks every time. Variation by operator or program creates downstream ambiguity about who is actually payable.

Set the validation order before payout eligibility#

A practical sequence is:

- Create the payee record and capture required onboarding data.

- Run identity and compliance checks required by your policy.

- Collect tax documents/profile data and verify completeness.

- Mark the partner payout-eligible only after those checks pass.

This keeps compliance, tax management, and liability in a single release gate instead of scattered approvals. It also gives finance a clear audit trail for why a partner is approved, pending, or blocked.

Keep the policy logic in house#

Vendor onboarding, tax, and payout modules can automate workflow steps, but they should execute your rules rather than replace them. Keep one internal eligibility status model as the source of truth, with explicit review checkpoints and reason codes.

For each approved partner, you should be able to retrieve the onboarding submission state, compliance/tax status, payout method, and eligibility-change timestamp from one place.

Be strict about sensitive data handling#

Keep sensitive-data controls explicit across onboarding and payouts: masked views, encrypted storage, and minimal PII in logs and events. Automation helps reduce manual operations, but governance still depends on your internal controls and traceability.

Instrument reconciliation and status visibility from API to ledger#

Traceability is the requirement: you should be able to follow one payout from the Payouts API request through provider response, final status, and ledger posting. If that chain breaks, close drifts back to manual matching and spreadsheet repair.

This gets harder with multiple rails or providers because report formats, identifiers, and timing differ. Without one internal record that survives those differences, finance can spend hours or days matching entries across systems. In practice, that anchor should be your own payout object rather than any single vendor response.

Build one auditable event trail#

Use one event trail that ties together four fields: internal request ID, provider reference (when returned), payout status history, and ledger entry ID. That gives you a single auditable source of truth and proof of settlement: what happened, where it happened, and when it settled.

A simple check is whether finance can answer, "Why was this publisher paid, not paid, or reversed?" without stitching exports across systems. If you run multiple programs or entities, a ledger hierarchy helps keep balances and postings attributable at the right level instead of pooling liability into one opaque bucket.

Treat Commission Reconciliation like a shipped feature#

Commission Reconciliation should run as a daily close process, not month-end cleanup. Define explicit checks, mismatch buckets, and named owners so exceptions are routed and aged in queues instead of hiding in inboxes.

A workable daily close usually checks:

- commissions approved vs payouts created

- payouts created vs provider-accepted transactions

- provider-accepted transactions vs settled or failed outcomes

- settled payouts vs ledger postings or reversals

Define mismatch categories before launch (for example: amount mismatch, missing provider reference, status timing lag, duplicate-submission suspicion, posted-to-ledger-before-final-outcome), then assign each to finance, payments ops, or engineering.

Make retries safe and status visible#

Set idempotency as an internal rule for all payout-triggering calls, even when a vendor does not require it. Retries from timeouts, partial responses, or operator replays are normal; without idempotency tied to your internal payout request, a transient failure can become a duplicate disbursement and later reconciliation break.

Expose one shared operational status view for finance and ops, including API status and the underlying event log. A single status trail keeps incident triage evidence-based instead of split across teams.

For a step-by-step walkthrough, see Stopping Affiliate Payout Abuse From Fake Clicks and Fake Signups.

Set payout cadence, instant payout, and exception rules by segment#

Use segmented payout rules, not one global cadence, and treat instant payout as an earned state based on control reliability. Segment partners by volume, dispute or reversal risk, onboarding completeness, and payout-detail quality, then set approval depth by segment before cash moves.

Keep the decision path auditable in one payout record: segment label, approver, qualification reason, and final outcome. If you cannot show those fields together, keep the slower cadence for that segment.

Instant payout through Dots Payouts or a similar option can improve partner confidence, but only when compliance gating and status tracking are already stable. If beneficiary validation is still failing or outcomes are not reliably reflected in your records, instant payout compresses the time between error and loss.

Define exception handling before rollout:

- Stale FX quote: reprice before retry, and log the original quote timestamp plus replacement-rate decision.

- Failed beneficiary details: stop auto-retries on hard validation failures and route to manual correction with missing fields identified.

- Returned payout: reopen the payable, attach the provider return reference or reason, and require manual approval before resubmission.

As a governance baseline, review segment rules and provider performance at least annually, including commission rates and each provider's ability to fulfill commitments.

Execute a 90-day rollout with hard verification checkpoints#

Run this as a gated 90-day rollout: each phase should stay narrow, measured, and easy to stop if verification quality drops.

| Phase | Scope | Verification focus |

|---|---|---|

| Days 1 to 30 | Pilot one commission model in one market with one onboarding flow, one approval path, and one payout route | Check that onboarding completion, payout success, and reconciliation close align in payout telemetry, and confirm there are no hidden manual handoffs |

| Days 31 to 60 | Add only one new variable: a new rail or a new currency path | Check whether conditional logic still routes correctly under higher volume and verify finance close under that same load; pause if manual review grows or unresolved exceptions roll into the next close cycle |

| Days 61 to 90 | Expand market coverage only after predefined go/no-go checks pass for accuracy, exception aging, and close-cycle reliability | Keep vendor evaluation evidence side by side with live operating metrics and prioritize pilot evidence before scaling |

Days 1 to 30#

Pilot one commission model in one market with one onboarding flow, one approval path, and one payout route. The goal is to prove that onboarding completion, payout success, and reconciliation close align in your payout telemetry, even when execution spans onboarding tools, a CRM, banking APIs, and compliance systems.

Your first checkpoint is simple: can a partner move from enrollment to payout eligibility without hidden manual handoffs? If bank verification is in scope, use risk-adaptive logic by transaction size, customer type, and regional compliance need instead of one method for everyone. Instant Account Verification can show lower drop-off than micro-deposits in cited examples (~5% vs up to 20%), but treat that as directional, not a universal benchmark. Keep human-in-the-loop checkpoints for exceptions from day one.

Do not call the pilot healthy just because transfers went out. Review every held or failed payout and confirm the reason is clear, assigned, and traceable to the partner record.

Days 31 to 60#

Add only one new variable: a new rail or a new currency path. Do not add both at once.

This is the stress phase. A single payout cycle can involve hundreds of transactions across multiple countries, each with different banking rules and verification layers. Check whether your conditional logic still routes correctly under higher volume, then verify finance close under that same load. If manual review grows or unresolved exceptions roll into the next close cycle, pause here and fix those controls before expanding.

Days 61 to 90#

Expand market coverage only after your predefined go/no-go checks pass for accuracy, exception aging, and close-cycle reliability. Define those checks before rollout and keep them tied to your own operating evidence.

Keep vendor evaluation evidence side by side with live operating metrics for every option (for example, Payouts.com, i-payout, Dots, Affise Pay), using the same evidence pack each time:

- market and rail assumptions tested

- pilot telemetry for onboarding completion, payout success, and exception volume

- finance close notes showing where manual intervention was still required

- failed-case examples and resolution path

If evaluation looks strong but the pilot still depends on manual cleanup, prioritize pilot evidence before scaling. Related reading: Building a Virtual Assistant Marketplace with Operable Payout and Tax Controls.

Conclusion#

The right choice is rarely the vendor or setup with the most features. It is the mix of market, commission model, and controls your team can actually verify, govern, and close without manual rescue work. That is the real standard for affiliate network payout automation.

Taken together, the decision rule is simple: do not expand based on partner demand alone. Expand only when a partner can move from onboarding to payout eligibility to payment status to close through a path your team can explain end to end. If you still need side spreadsheets to answer who was eligible, who was held, who was paid, and what returned, you are not ready to stack a new country on top of a new payout model.

That matters more as you scale. The case for automation is not just speed. It is that managing hundreds or thousands of affiliate relationships manually creates inefficiencies, errors, and missed opportunities. Good automation improves onboarding, tracking, communication, and performance analysis, but those gains only matter if your controls hold up under volume. In practice, the most useful checkpoint is not a dashboard screenshot. It is whether finance and ops can trace one payout from request ID to provider reference to final posting without guessing. A strong launch decision should pass three tests:

- Clear eligibility rules

You should be able to show what makes a partner payable, what documents or reviews can block payout, and who owns exceptions.

- Traceable payout states

Pending, held, failed, returned, and paid should mean something operationally, not just look clean in a UI.

- Repeatable close with low exception drag

Your month-end should not depend on staff memory or manual matching between payout activity and commission records.

If one market needs manual review in more than one critical step, treat that as a red flag. The same goes for commission changes that increase payout frequency before you have stable reconciliation visibility. A common failure mode is thinking the transfer layer is the hard part, then finding that bad onboarding data, unclear holds, or unresolved returns can slow finance close.

The next move should be disciplined, not broad. Start with your market and model decision matrix: payment volume, integrations, compliance needs, testing scope, and monitoring requirements. Then run a constrained pilot, ideally one market and one commission model, and require hard evidence before expanding. That evidence pack should include onboarding completion quality, payout status traceability, exception aging, and proof that close can be repeated without spreadsheet stitching.

If you want a deeper compare of commission choices before you pilot, this breakdown on Affiliate Network Payout Structures: Performance-Based Commission Models for Publisher Partners is the right next read.

Frequently Asked Questions

What is affiliate network payout automation in practical terms?

In practice, it is the operating layer between partner signup and a reconciled payout, not just the transfer itself. It usually includes affiliate onboarding, payment-detail collection, payout triggering, status tracking, and finance checks across systems. If you still need manual checks to confirm who was eligible, paid, held, or returned, the automation is only partial.

What should founders evaluate before expanding affiliate payouts to a new country?

Check whether you can support the full path in that market: onboarding evidence, payment-detail quality, payout route, and finance verification readiness. A good test is whether a partner can move from enrollment to payout eligibility without hidden manual steps. If manual verification in your current process is still taking too long, adding a new country can add delay before it adds revenue.

How do commission structures change payout complexity and reconciliation workload?

The more often you calculate and release earnings, the more pressure you put on approval logic and reconciliation. A commission-based CPA model may be simple conceptually because you pay only on confirmed sales, but operational workload still depends on payout cadence. If you move from consolidated payouts to more frequent disbursements, reconciliation can pile up fast without clear payout states.

When is instant payout worth the added compliance and control overhead?

Instant payout is worth it only when your eligibility gates already work cleanly and your status visibility is reliable in real time. Fast disbursement does not remove compliance, KYC or KYB, fraud checks, or finance review where policy requires it. If you cannot quickly explain why a payout is pending, held, failed, or returned, adding instant payout usually turns a trust feature into an ops problem.

What are the most common payout failure points in affiliate networks?

The usual breaks are bad onboarding data, incorrect payout details, manual review bottlenecks, and weak reconciliation. Incorrect bank details are a direct cause of failed transactions and delays, so verify what was collected before blaming the rail. Manual review and inefficient reconciliation can also delay resolution after money is sent.

What can be fully automated, and what usually remains policy-gated or manual?

You can automate much of the routine work: data capture, payout scheduling, status updates, and parts of the payout flow itself. Some stacks also expose real-time system status, which helps ops and finance triage from the same event trail. What usually stays gated is document review, compliance decisions, edge-case exceptions, and any payout that fails validation or needs human approval.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- comptroller.tn.gov/content/dam/cot/la/advanced-search/2026/educ...trusted

- das.nebraska.gov/materiel/purchasing/6677/RFP%206677%20Z1%20M...trusted

- dmv.ca.gov/portal/handbook/vehicle-industry-registratio...trusted

- ecfr.gov/current/title-17/chapter-II/part-230trusted

- fdic.gov/bank-examinations/section-3-asset-management...trusted

- federalreserve.gov/publications/files/cbem-7000-202602.pdftrusted

- insight.dickinsonlaw.psu.edu/cgi/viewcontent.cgitrusted

- patreasury.gov/transparency/e-library/ContractFiles/477341_...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Affiliate Network Payout Structures for Publisher Commissions

Commission design is an operating decision, not a pricing footnote. The structure you choose affects what behavior you reward and the economics of the program. It is easy to announce rates. It is much harder to define a model that still holds up once reversals, edge cases, and partner questions start showing up.

Automating Affiliate Network Payouts for Publishers and Partners at Scale

Automating affiliate payouts is worth doing, but only after you decide what has to stay controlled. As programs grow, payouts become a real operational burden, and payout reliability affects whether partners stay engaged. If you automate the payment motion before you clean up approvals, tax data, and reconciliation, you usually do not remove work. You just move it into exceptions that are harder to unwind.

Mass Payouts for Affiliate Networks Paying Publishers, Partners, and Creators at Scale

Treat affiliate payouts as infrastructure, not as a payment feature. Once you are paying publishers, partners, and creators in volume, the hard part is often not the send button. It is everything around it: commission calculation, recipient onboarding, approval controls, rail selection, status handling, reconciliation, and close.