Quick Answer

Build a withholding tax calculator international workflow as a controlled decision path: verify payee classification, confirm W-8 or W-9 status, choose the approved branch, and execute payout posting from that approved record. Use Publication 515 and Notice 1392 boundaries so nonresident contractor files are not handled with W-4 estimator assumptions. When documentation is stale or conflicting, send the case to exception review instead of forcing a rate.

Estimate withholding on international contractor payments#

International withholding is an operating process, not a one-step rate lookup. A withholding tax calculator international workflow your team can rely on should connect classification, document checks, rate logic, payment timing, and reporting so each decision is traceable.

Start with classification before any rate decision. Identify foreign individuals, then separate resident and nonresident groups before applying withholding rules. If that classification is wrong, the rate result is wrong too.

This guide gives you a practical structure for deciding when default withholding applies, when treaty treatment may apply, and when treaty treatment should wait until documentation is reliable. It also keeps withholding and reporting as separate controls, because reporting can still apply even when withholding is reduced to zero.

For a related breakdown, read Self-Employment Tax Calculator: How Much Will You Owe on 1099 Income?.

What this calculator is and what it is not#

In this context, this calculator should handle foreign-person withholding for contractor payouts, not employee or pension withholding. That boundary matters from the start.

| Lane | Applies to | Named forms or reporting |

|---|---|---|

| Employer withholding | Employer (W-2) | IRS Tax Withholding Estimator; Form W-4 |

| Pension or annuity withholding | Pension or annuity | IRS Tax Withholding Estimator; Form W-4P |

| Foreign-person contractor payouts | Many U.S.-source payments to foreign persons | IRC 1441 to 1443; Form 1042 and Form 1042-S |

The IRS Tax Withholding Estimator is for employer (W-2) and pension withholding, and it helps users complete Form W-4 or Form W-4P in that lane. IRS guidance also says people with nonresident U.S. tax status cannot use that estimator. If you apply W-4-style logic to a foreign contractor file, you put the payout in the wrong regime before you even get to the rate.

For many U.S.-source payments to foreign persons, withholding falls under IRC 1441 to 1443, often called NRA withholding. The IRS describes a general 30% baseline for most U.S.-source income received by a foreign person, with possible reduced or exempt treatment in some cases. It also ties this regime to Form 1042 and Form 1042-S reporting.

Use one intake checkpoint before approval: confirm the withholding lane first, then calculate. If your process mixes employee withholding, NRA withholding, and other regimes, the output may look precise but still be wrong. IRS guidance is clear that NRA withholding is its own regime and does not include IRC 1445 withholding.

The minimum input set before you calculate anything#

Once the withholding lane is confirmed, use one operating rule: if the record is incomplete, do not calculate. A guessed output may look final, but you will not be able to defend it later.

The IRS Tax Withholding Estimator is a useful contrast here. It is designed to help complete Form W-4 or Form W-4P for federal withholding adjustments tied to a job, pension, or annuity. It cannot be used by people with nonresident U.S. tax status, and it cannot estimate withholding on future income before pay starts. For nonresident cases, IRS guidance points to Notice 1392 instead of the estimator. That is why contractor workflows should start with verified file status and actual payment-record data, not payroll-style assumptions.

Start with identity and tax-status evidence, not math#

Before entering amounts, confirm who the payee is and the current tax-document state in your system.

Use statuses your team can act on, not just "document uploaded": submitted, validated, rejected, or pending review, plus reviewer attribution.

Capture transaction facts from the payment record#

Keep the core transaction fields on the same record used for settlement, not only in notes or attachments.

For withheld-tax inputs, use IRS-style checkpoints: the pay-period withholding entry should include only that pay period, and the year-to-date withholding entry should be the total withheld so far for the year. IRS guidance also flags bad withheld-tax inputs as a common reason results look inaccurate.

Save a reusable evidence pack and enforce stop-gates#

If a calculation cannot be explained after the fact, it is not production-ready. For each calculation attempt, store the proof fields showing why calculation was allowed: document status, reviewer decision, and timestamped approval.

Add explicit "cannot calculate" gates in your workflow. Common examples:

- document status is incomplete or unvalidated

- there is no job, pension, or annuity with federal income tax withholding for estimator use

- the user has nonresident U.S. tax status or only future income before pay starts

- withheld-tax entries are missing or inconsistent between pay-period and year-to-date values

When a gate triggers, route the case to exception handling instead of returning a fallback number.

For a step-by-step walkthrough, see US-UK Tax Treaty Withholding Controls for Contractor Payment Platforms.

Rate selection logic your ops team can execute consistently#

Once intake gates are working, rate selection should follow three branches: default withholding, treaty-reduced withholding, or blocked payout. If the record does not clearly support one branch, do not invent a fourth outcome.

| Branch | Use when | Required support in file | Action |

|---|---|---|---|

| Default withholding branch | No supported treaty reduction is available, but policy allows payout to proceed | Valid payer and payee record, required transaction facts, no approved treaty claim | Apply the default branch and store a reason code |

| Reduced treaty branch | Treaty claim is present and supported | Valid W-8 record, treaty-claim support, any required beneficial-ownership support where applicable, reviewer approval | Apply the treaty branch and tie it to the evidence pack |

| Blocked payout branch | Eligibility cannot be confirmed or required support is missing | Missing, stale, inconsistent, or unvalidated documents, or missing treaty or beneficial-ownership support | Follow policy: hold payout or apply the documented fallback, then route to exception handling |

Use one enforceable if/then rule#

Give reviewers a rule they can enforce: if the W-8 record is valid and the treaty claim is supported, use the treaty branch. If documents are stale, inconsistent, or missing support, apply your documented fallback branch or hold the payout based on policy.

For treaty cases, verify the claim itself, not just the presence of a form. The Form W-8BEN instructions include "Line 10, claims of tax treaty benefits," so "W-8 on file" alone is not enough for reduced withholding. Reviewers should be able to point to the treaty-claim element and the supporting records.

A practical check is to align three fields before approving treaty reduction: treaty-claim element on the W-8 path, supporting records, and payment record facts. If they do not align, treat it as a rate-selection failure.

Treat stale or inconsistent records as active risk#

Document presence is not the control; document state is. W-8BEN instructions include checkpoints such as expiration and changes in circumstances, so your status model should surface usable states like validated, expired, pending revalidation, and rejected for inconsistency.

If policy allows fallback when records are stale, require a recorded reason for proceeding. If policy requires a hold, make the block reason specific enough that support or tax teams know what evidence to collect next.

If you want deeper form and treaty controls, Tax Withholding for International Contractors: W-8 Forms and Treaty Benefits is the adjacent topic.

Do not let Foreign Tax Credit logic leak into payout decisions#

Keep contractor payout withholding separate from Foreign Tax Credit workflows. The IRS treats FTC as a different mechanism. Taxpayers may take a credit or itemized deduction for qualifying foreign taxes, individuals figure the credit on Form 1116, and corporations file Form 1118.

FTC also has its own structure and limits. Form 1116 uses separate filing by income category and one category selection per form, credit amounts are limited by FTC rules, and treaty rules can affect outcomes. Those rules do not decide whether a contractor payout qualifies for treaty reduction today.

Apply the same separation to GILTI, FDII, BEAT, and Subpart F references. If they appear in payout review, route the case to corporate tax and keep payout decisions anchored to contractor record status, W-8 status, treaty support, and payment facts.

Allow overrides, but make them expire#

Overrides should be narrow and temporary, not a quiet second policy. Each override should capture reason, approver identity, date, and revalidation date so one-off decisions do not become permanent defaults.

Your override record should include submitted form version, validation status at decision time, reviewer attribution, approval timestamp, selected branch, and the exact mismatch or gap that triggered the exception. If that chain is missing, the override is not auditable.

We covered this in detail in Withholding Tax Rate Lookup for Treaty Decisions Across 100+ Country Pairs.

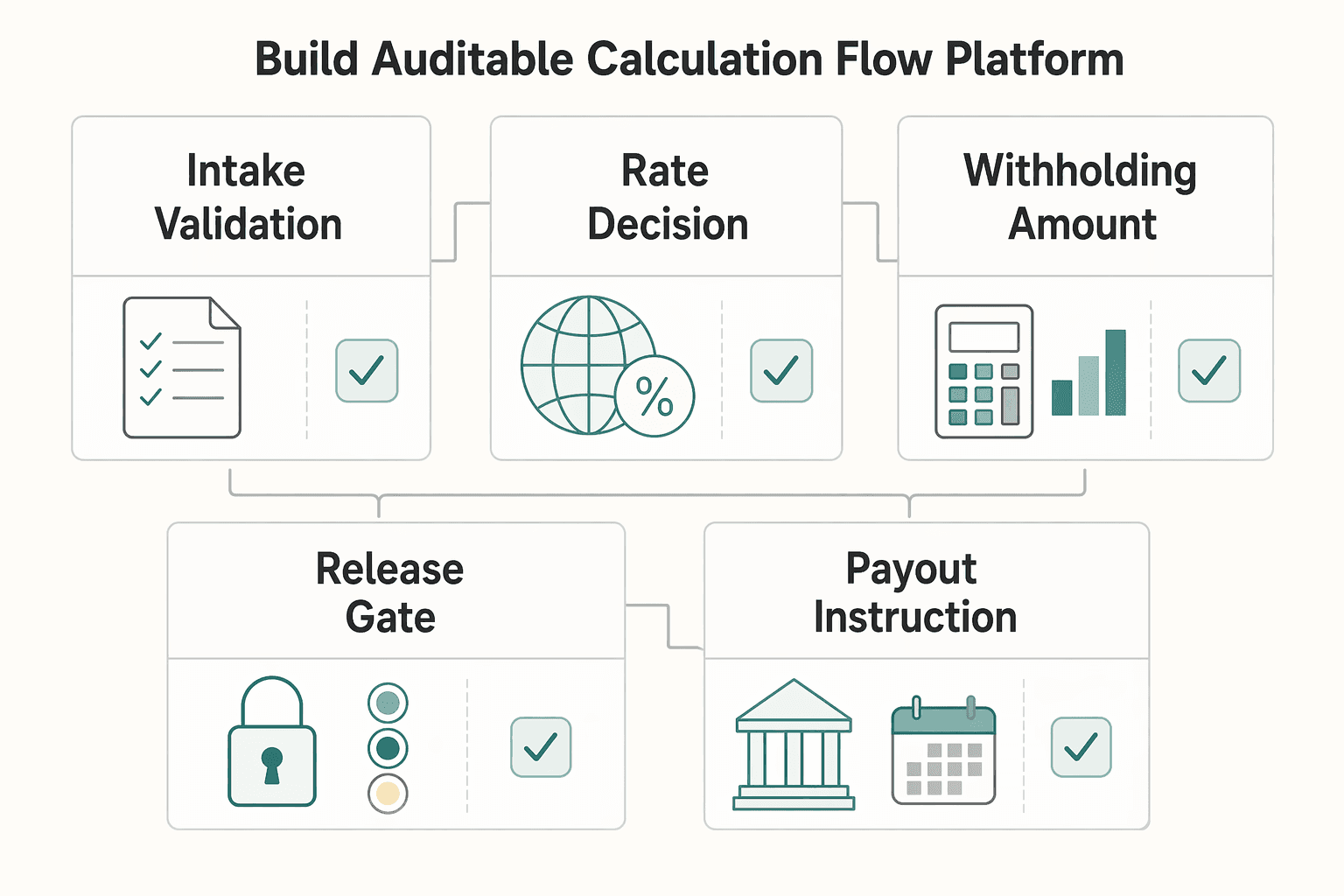

How to build an auditable calculation flow in your platform#

Build this so one approved withholding decision carries through payout and reconciliation. This control pattern can reduce incorrect withholding and preserve an audit trail, especially because cross-border tax logic can vary by country, transaction type, and business structure.

A workable control sequence is intake validation, rate decision, withholding amount calculation, approval, payout instruction, ledger posting, then reconciliation export. This is a control pattern, not a legal requirement. It helps because each step leaves an artifact you can review later.

| Step | What should be fixed at this point | What to verify before moving on |

|---|---|---|

| Intake validation | Payer/payee record and transaction facts | Required tax documentation is present, current, and consistent |

| Rate decision | Default, treaty-reduced, or blocked branch | Reduction claims are supported by current documentation |

| Withholding amount calculation | Gross amount, selected rate, withheld amount, net payout | Calculation points to the approved decision artifact |

| Approval | Reviewer identity, timestamp, reason, and any exception details | Reviewer can point to the supporting record set |

| Payout instruction | Payment request details and internal payment ID | Payout matches the approved net amount |

| Ledger posting | Gross, withheld, net, payable, and tax liability entries | Entries tie back to the approved decision artifact |

| Reconciliation export | Settlement status and processing context | Export traces request to settlement line by line |

Make retries reuse the same decision artifact#

If your platform supports retries, callbacks, or reruns, do not recalculate from mutable live data by default. Prefer reusing the same approved decision artifact for the same payment context. If replay checks fail, for example because key values changed, stop and route the case to review. Exact replay and idempotency behavior depends on your stack design.

Persist the IDs that connect decision, payout, and books#

Store a stable join path across decision, payout, and ledger records. In many platforms, this includes a withholding decision ID and internal payment ID, with provider or batch references when available. If those links are fragmented across systems, audit and month-end reconciliation often fall back to manual reconstruction. Keep the linkage strong enough to support detailed compliance reporting with full audit trails.

Keep logs useful while protecting sensitive tax data#

Operational logs should prove control execution without becoming a second tax-record store. In practice, keep only the minimum metadata needed to trace control execution and status transitions, and keep full tax-document content in the governed record system. That preserves incident visibility without duplicating sensitive records.

Related: Tax Reporting for Creator Platforms: 1099s W-8s and International Withholding.

Exception handling when documents are missing or conflicting#

Exceptions should move through a defined control lane, not ad hoc reviewer judgment. Put unknown eligibility cases in a dedicated queue, and require a written decision path before final tax treatment is approved. A compact matrix helps keep actions consistent under batch pressure and makes later approvals auditable.

| Issue | Main risk | Required action path |

|---|---|---|

| Missing W-8 forms | Eligibility and reporting branch may be unsupported | Route to exception review; follow your documented policy for hold vs. fallback treatment and record approver rationale |

| Conflicting residency claim | Wrong withholding and reporting treatment | Pause automated handling until one residency position is approved in the governed record |

| Expired form | Prior decision may no longer be supportable | Remove auto-reuse and require revalidation per policy before release |

| Inconclusive beneficial ownership review | Treaty handling may be unsupported | Escalate per policy before applying treaty treatment |

| Unsupported treaty claim | Underwithholding and reporting errors | Escalate to a policy owner and apply only an approved path with logged rationale and approver |

Publication 515 gives you checkpoints to anchor this: Withholding Agent, Determination of amount to withhold, and Forms 1042 and 1042-S Reporting Obligations, with Form 1099 reporting and backup withholding treated separately. If an exception record cannot show which checkpoint was satisfied, stop and review before processing.

Treaty-rate percentages, detailed beneficial-ownership evidence standards, and SLA timing thresholds are not defined here. Treat those as policy-defined items and route ambiguous cases to specialist review.

Keep exception aging visible, with explicit ownership and escalation triggers, so unresolved cases do not sit in payout batches indefinitely. This lines up with the caution-oriented handling in Publication 515 and the control focus in IRM 20.1.9 (Penalty Case Controls).

Related reading: How to Build a Global Tax Withholding Engine: W-8 W-9 and Treaty Rate Automation.

Reconciliation checkpoints from gross amount to final payout#

Once an exception is cleared, treat payout as complete only when key values, for example gross amount, withheld amount, net payout, and settlement confirmation, reconcile in one ledger trail. This is where a withholding decision becomes durable evidence instead of a month-end repair.

Match each payment at line level#

Keep those key values in one record path for each payout line, not split across separate exports and journals. In practice, keep a traceable link across the payment record, withholding decision record, payout batch, settlement reference, and posted ledger entry, plus the documentation status that supported the withholding path.

A practical check is whether the same withholding decision can be traced from calculation to payout instruction to ledger posting. If that chain breaks, cash may still move, but confidence in how the settled amount was produced goes with it.

Tie payout records to reporting outputs#

Cash reconciliation alone is not enough. Link each withholding record to the reporting artifacts it supports, such as Form 1042-S and, in a Section 1446 context, Form 8805 (with related payment-voucher records like Form 8813).

Precision here affects downstream outcomes. In one cited IRS matching process, 18 fields on Form 1042-S were compared, and any discrepancy could reject a refund claim. The same flow also froze Chapter 3 and Chapter 4 refund requests for up to one year or longer, with an average 26-week delay in the cited population.

Check batch totals before and after posting#

One internal control is to run two batch checks: compare the sum of line-item withheld amounts to the withholding total expected in the payout batch file, then compare that same line-item sum to the withholding journals posted to the ledger.

If the totals do not match, isolate the affected lines before release instead of forcing parity with a manual plug. This catches mismatch-driven failures early, while they are still diagnosable.

Correct with a reversal-and-repost history#

When you need to correct withholding, a reversal-and-repost pattern can preserve a clear timeline from original settlement to corrected posting and make downstream reporting adjustments easier to explain and verify.

How to evaluate calculator tools without buying the wrong one#

Start with scope clarity before country coverage. A tool is risky for live payouts if it cannot explain what inputs it used, what assumptions it applied, and how to reproduce the result later.

Use category comparisons only as a starting point. You will see both broad calculators and enterprise suites in this space. Then test workflow fit, not brand positioning.

Screen scope first#

Use the IRS Tax Withholding Estimator as a baseline scope check. It estimates withholding from income and helps users complete Form W-4 or Form W-4P.

- It is not for users with nonresident U.S. tax status.

- It is not usable when the person has no job, pension, or annuity with federal income tax withholding.

If a tool follows that same scope, treat it as employee- or pension-withholding oriented, not automatically fit for international contractor payout decisions.

Verify reliability with real cases#

A practical test is to run a real record you can rerun. Evaluate with actual cases and confirm that the same inputs produce a traceable repeat result.

| Checkpoint | What you need to see | Rejection signal |

|---|---|---|

| Input sensitivity | Output changes are explainable when key inputs change | Big result shifts with no clear explanation |

| Assumption visibility | Jurisdiction and classification assumptions are explicit | A single number with hidden assumptions |

| Reproducibility | You can rerun a case and track what result was produced and when | No reliable way to reproduce prior outputs |

The IRS notes that common input mistakes can greatly affect estimator results. In adjacent cross-border tax calculations, country and classification assumptions can also change outcomes, and errors can trigger holds and unexpected costs. That is not direct proof for contractor withholding, but it is a practical warning against black-box outputs.

Use a hard rejection rule#

Prefer tools that disclose rule assumptions and preserve enough result history to explain corrections later. If special documentation paths are central to your process, test those paths directly during evaluation rather than relying on product naming.

For a deeper view on those inputs, see Tax Withholding for International Contractors: W-8 Forms and Treaty Benefits.

If you want a deeper dive, read Cross-Border Invoicing: How to Handle VAT GST and Withholding Tax on International Invoices.

Country and program variation you must confirm before production#

Do not launch a new payout corridor because a tool says a country is "supported." Treat that as a preliminary signal. Make withholding inputs explicit and reviewable before production, including payment-type and contractor-residency facts.

| Pre-production item | What to confirm or retain |

|---|---|

| Payment types | Confirm which payment types the corridor will process |

| Residency facts and forms | Confirm which residency facts and forms are required to reach a withholding result |

| Reporting track | Confirm which downstream reporting track applies, for example 1042/1042-S or another track |

| Decision record | Retain the signed decision memo, sample evidence pack, and effective date |

A frequent mistake is treating withholding and reporting as the same decision. Publication 515 separates these tracks, including Forms 1042 and 1042-S reporting obligations, Form 1099 reporting and backup withholding, and Form 8966 reporting. Keep FATCA-related reporting and adjacent filing contexts in their own lane. They may matter for compliance, but they are not a substitute for payout-side withholding logic.

Apply the same separation to taxpayer return items. FEIE applies to qualifying individuals with foreign earned income who file a U.S. return reporting that income, and it is claimed on Form 2555 or Form 2555-EZ. The physical presence test is time-based: 330 full days during any period of 12 consecutive months, and missing the day count fails the test regardless of reason. So FEIE outcomes and housing exclusion calculations should not replace your payer withholding decision process.

Before enabling any new corridor at scale, require a final legal-confirmation gate on those same points: payment types, required residency facts and forms, downstream reporting track, and the signed decision memo with sample evidence pack and effective date.

If legal cannot sign off on those points, keep the corridor in test or hold payouts by policy rather than guessing.

A 90 day rollout checklist for finance ops and product owners#

Roll this out in phases with explicit review and control checkpoints, rather than switching every payout path at once. This is an internal operating plan, not a regulator-mandated sequence.

| Week range | Primary focus | Key details |

|---|---|---|

| Weeks 1 to 2 | Define required intake fields, your evidence-pack schema, and documented decision policies | Set Program Management and Review ownership and Program Controls checkpoints up front so decisions are auditable before build starts |

| Weeks 3 to 6 | Implement approved decision logic across product and operational workflows | Keep clear approval states and control points so exceptions are measurable and policy changes can be applied without losing decision history |

| Weeks 7 to 10 | Run parallel testing on historical cases, validate reconciliation outputs, and track exception patterns | Confirm that decision outputs stay traceable through payout and reporting flows |

| Weeks 11 to 13 | Launch in phased corridors, starting with lower-exception lanes | Monitor payout failures, override rates, and resolution time, then tighten controls before expanding coverage |

Staging matters because international tax rules are changing on dated milestones. The One Big Beautiful Bill Act (OBBBA) is presented as a major change to U.S. international tax regimes, including a disposition-timing change after June 16, 2025 that may affect 2025 FDDEI outcomes, with additional changes for tax years starting Jan. 1, 2026. With 2026 implementation deadlines, early modeling, cross-functional coordination, and strategic planning should be part of delivery, not a post-launch task.

Use the week ranges below as planning bands, not mandated deadlines.

Weeks 1 to 2#

Define required intake fields, your evidence-pack schema, and documented decision policies with tax, compliance, finance, and product owners. Set Program Management and Review ownership and Program Controls checkpoints up front so decisions are auditable before build starts.

Weeks 3 to 6#

Implement approved decision logic across product and operational workflows, with clear approval states and control points. Keep controls explicit so exceptions are measurable and policy changes can be applied without losing decision history.

Weeks 7 to 10#

Run parallel testing on historical cases, validate reconciliation outputs, and track exception patterns. Use this phase to confirm that decision outputs stay traceable through payout and reporting flows.

Weeks 11 to 13#

Launch in phased corridors, starting with lower-exception lanes. Monitor payout failures, override rates, and resolution time, then tighten controls before expanding coverage. Use an internal success checkpoint: teams can tie withholding decisions to payouts and reports without ad hoc reconstruction.

Before rollout, pressure-test your intake-document paths with the W-8 form generator to catch missing fields before payouts are queued.

Conclusion#

Treat international withholding as a controlled payment operation, not a one-click estimate. If you cannot show who the payee is, why the rate was chosen, when withholding was applied, and how it maps into reporting, the process is not production-ready.

Publication 515 frames withholding as a workflow with checkpoints, including Identifying the Payee, Determination of amount to withhold, When to withhold, and Forms 1042 and 1042-S Reporting Obligations. Your operating design should mirror that workflow, whether execution happens in a product UI, an API, or a review queue.

To scale this safely, standardize four controls early:

- required inputs and evidence standards

- explicit rate decisions, including when treaty-reduced treatment is applied

- a defined exception path for incomplete or conflicting records

- reconciliation from gross amount to withheld amount to net settlement, tied to reporting outputs

Use a simple rule: if the stored evidence cannot support the rate, do not force a payout through optimistic calculation. Route the case to exception review or apply the fallback your written policy allows.

Expand coverage only after controls are stable. Statutory and treaty-reduced outcomes can differ, and quick-chart values are not complete without territory-level detail. Start with one corridor, prove clean month-end traceability, then scale in controlled additions. That is what a reliable international withholding calculation process should deliver: fewer judgment gaps, cleaner evidence, and growth that does not outrun controls.

If you need this withholding workflow to run with policy gates, safe retries, and batch status tracking where enabled, review Gruv Payouts.

Frequently Asked Questions

What inputs are required for an international withholding tax calculator for contractors?

This guide does not establish one definitive required input list for contractor withholding. It does show that input mistakes can materially change results, so define and validate your field set through policy and legal review rather than inferring it in-product.

How is contractor withholding different from payroll tools like the IRS Tax Withholding Estimator?

The IRS Tax Withholding Estimator is for employer withholding on W-2 wages and for pension or annuity withholding. Its output is intended to help complete Form W-4 or Form W-4P for an employer or pension provider. IRS guidance also says nonresidents for U.S. tax purposes cannot use that estimator and should use Notice 1392.

What should we do if a contractor has not submitted valid W-8 forms or W-9?

This guide does not provide a single required hold-versus-fallback rule for missing tax forms. It does establish that most U.S.-source income paid to a foreign person is generally subject to 30% U.S. tax, with potential reduced rates or exemptions where Code provisions or treaty rules apply. Operationally, treat missing or unclear documentation as an exception path with a recorded decision basis.

When should we hold a payout instead of applying fallback withholding?

This guide does not define a universal trigger for hold versus fallback. Use your written policy when the legal basis for a rate is not supportable from available records. Keep that decision auditable so exceptions can be reviewed consistently.

How do we apply tax treaty benefits without creating audit risk?

Treat reduced rates as conditional, not automatic. IRS guidance says a reduced rate, including exemption, may apply where Code provisions or a tax treaty allow it. Use a documented internal review process that ties the treaty claim to available documentation and payment facts before applying treaty treatment. Also note IRS international FAQ responses are informational and not citable legal authority.

How do we reconcile withheld amounts across payout batches and ledger records?

There is no full reconciliation procedure to work from. There is a reporting checkpoint, though: where NRA withholding applies under IRC 1441 to 1443, reporting includes Form 1042 and related Form 1042-S. If you design a reconciliation process, keep each withholding decision traceable into those reporting outputs.

Which matters more when choosing a tool, broad country coverage or transparent decision logic?

This guide does not support a strict ranking of coverage versus transparency. It does support that input mistakes can significantly affect outcomes, which makes visible assumptions and repeatable decision outputs operationally important. In practice, evaluate coverage and decision transparency together, and avoid tools whose assumptions or outputs you cannot explain.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: