Quick Answer

Choose the setup your team can operate under failure, not the one with the broadest marketing claim. For iban number platforms european payouts, start by matching each corridor to SEPA or SWIFT, then confirm what IBAN validation happens before submission and what appears only at bank processing. If you need fast attribution, a Virtual IBAN model can help, but only after provider evidence confirms onboarding scope, payout coverage, and machine-readable failure reporting.

Why IBANs matter for European payouts#

If you are evaluating iban number platforms european payouts, skip the glossary. The real decision is which payout setup will keep money moving, exceptions visible, and reconciliation manageable as volume grows. This guide is for platform founders, finance ops leads, and engineering owners who need to ship reliable European payouts, not for readers looking for a basic banking explainer.

This guide stays close to the choices you actually have to make: which rail fits the corridor, what kind of IBAN setup gives you enough control, and what to verify before you commit code or operating effort. An IBAN is a standardized account identifier, and it is required to clearly assign recipients for international payments and payments within Europe. But that definition does not tell you whether SEPA, SWIFT, or a Virtual IBAN model is the right fit for your payout stack.

- Operator-first lens

If you are handling contractor, creator, seller, or supplier payouts, failure handling matters as much as send capability. That raises the bar. "Supports Europe" is not enough. You need to know whether the provider gives you enough status detail, beneficiary validation, and region or currency coverage to support your own controls. This guide treats payout operations as an execution problem, not a terminology problem.

- Decision-ready, not definition-heavy

You will move quickly from IBAN basics into selection criteria, tradeoffs, and implementation checkpoints. That matters because the rails are not interchangeable. SEPA is a standardized euro payments area covering 41 countries and territories, while SWIFT is an international transfer path that is typically slower and costlier than local rails. It may also require extra configuration to avoid delays and unnecessary fees. The goal is not to memorize acronyms. It is to decide what to use, when to use it, and what extra work each choice creates for finance and engineering.

- Scoped to the messy parts providers often gloss over

The focus here is SEPA, SWIFT, and Virtual IBAN decisions, because public provider pages are often too high level to support architecture choices on their own. A vIBAN has the same format and functionality as a standard IBAN but links back to a master account. The EBA noted in its 2023/2024 fact-finding work that the definition of vIBANs is still not uniform across the market. Treat that as a warning sign. When you compare options, confirm capabilities directly by region and currency instead of assuming the headline page tells the whole story.

By the end, you should have a short list of option types, the tradeoffs behind each one, and a clear set of checkpoints to validate before rollout.

How to choose an IBAN payout platform and who this list is for#

When you are comparing IBAN payout platforms for European payouts, the right shortlist starts with your operating shape, not the provider homepage. If payout exceptions, status tracking, and reconciliation are part of your day job, you need a deeper evaluation than "supports Europe."

| Criterion | What to check | Why it matters |

|---|---|---|

| Rail fit | Select the transfer method per region and currency pair, typically LOCAL or SWIFT | The choice affects speed, cost, and failure handling |

| IBAN validation controls | Ask what checks happen before submission versus only at bank processing | Banks do check the IBAN during payment processing |

| Onboarding and coverage constraints | Confirm capabilities directly because they can vary by region and currency | Provider docs explicitly warn that capabilities can vary and may require direct confirmation |

| Exception visibility | Verify status changes through API responses, dashboard views, and webhook events | Do not rely only on a final success or failure |

- Teams this list is built for

This comparison is built for teams running contractor, creator, or marketplace payouts into France, Germany, Austria, or the United Kingdom. Those countries appear in current SEPA scheme materials, and SEPA itself covers 41 countries and territories, so the question is not whether Europe is broadly supported. The real question is whether a provider gives you enough control to send repeat payouts cleanly across those corridors while keeping payout state changes and failures visible.

- Teams that may not need this level of selection work

If you only send occasional one-off transfers, have no API roadmap, and do not expect meaningful reconciliation load, a full platform evaluation may be more than you need right now. You still need basic beneficiary accuracy, because banks do check the IBAN during payment processing, but you may not need deep event streams, custom routing, or provider normalization work yet. In that case, simpler bank tooling or a narrower provider review can be reasonable.

- What to score first before features or pricing

Start with four criteria, in this order. First, rail fit. Some providers require you to select the transfer method per region and currency pair, typically LOCAL or SWIFT, and that choice affects speed, cost, and failure handling. Second, IBAN validation controls. Ask what checks happen before submission versus only at bank processing. Third, onboarding and coverage constraints. Provider docs explicitly warn that capabilities can vary by region and currency and may require direct confirmation. Fourth, exception visibility. Verify whether you get status changes through API responses, dashboard views, and webhook events, not just a final success or failure.

- The decision rule that usually matters most

When payout failure handling and reconciliation are strategic, prioritize platforms with strong operational status surfaces over the lowest front-door pricing claim. A cheaper route is not cheaper if your team has to inspect logs manually every time a payout stalls or comes back with a missing reason. Ask for proof that the provider exposes machine-readable failure details such as a failure code and failure description, plus payout state changes through webhooks or reporting. A practical red flag is any platform where you cannot trace a failed payout from request to final state without support tickets, especially when SWIFT transfers can take up to three business days to arrive.

If you want a deeper dive, read What is an IBAN and How is it Different from a SWIFT Code?.

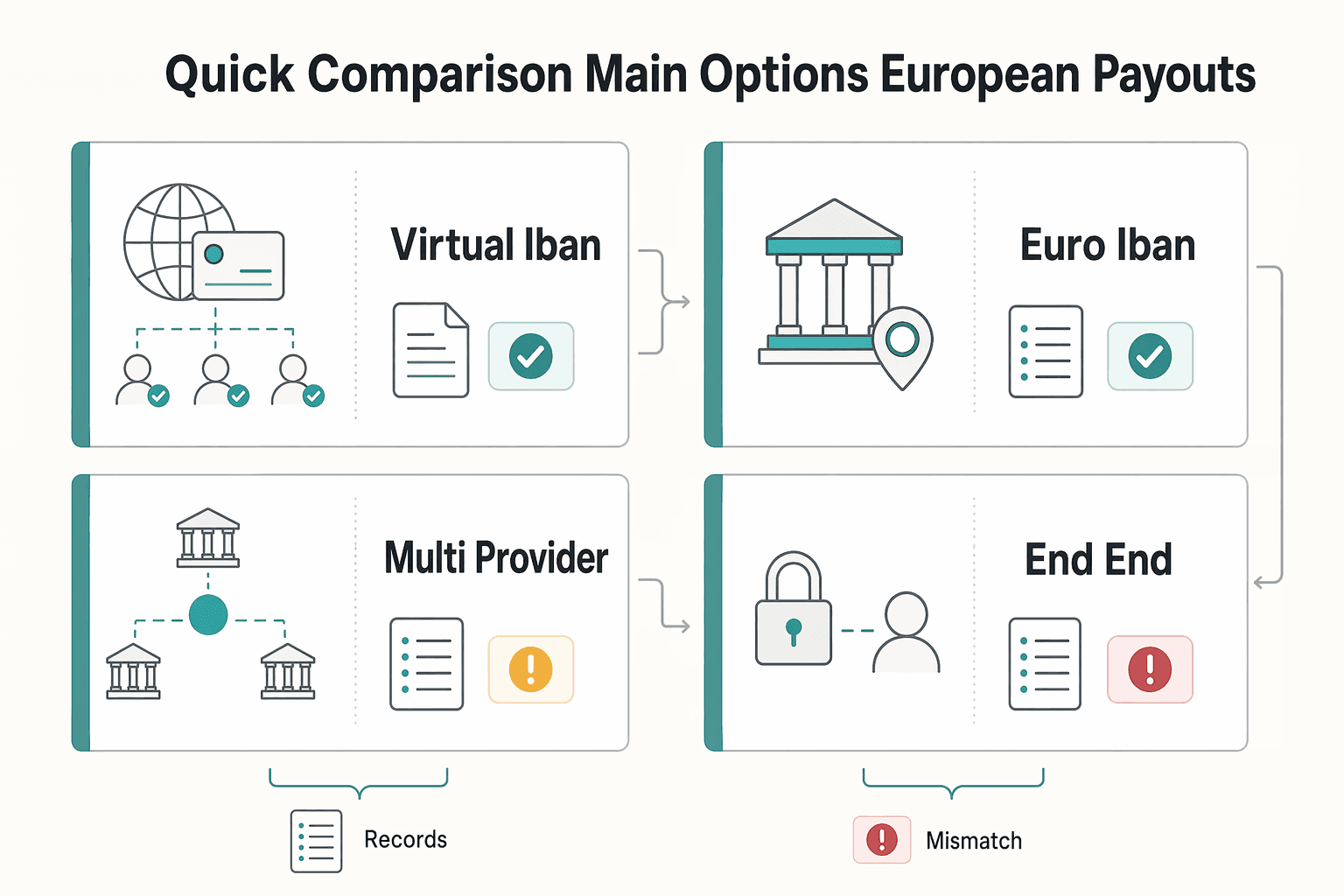

Quick comparison of your main options for European payouts#

Choose the route your team can actually operate when something goes wrong, not the one with the broadest homepage claim. In practice, the expensive choice is the one that creates payout rework your team cannot absorb.

The earlier section narrowed the decision to rail fit, onboarding constraints, validation controls, and exception visibility. This table compares the four main operating models against those realities and calls out the missing pieces on purpose.

| Option type | Best for | Setup effort | Control depth | Operational burden | Known unknowns to validate |

|---|---|---|---|---|---|

| Virtual IBAN provider route | Teams that need fast account allocation and cleaner payment attribution without building multi-bank logic first | Medium | Medium | Medium | Whether the vIBAN is linked to a master account in reporting, whether outbound payouts are supported or the product is stronger for inbound collection, SEPA and SWIFT availability by entity and corridor, onboarding eligibility. Airwallex marketing claims local bank details including UK IBANs in 60+ markets, but that does not answer those questions for your case. |

| Euro IBAN account route | Finance teams with mostly euro payouts and a stable payee base | Low to medium | Low to medium | Low | Whether the dedicated Euro IBAN supports your full payout flow, not just account opening; whether SWIFT is available when a corridor falls outside euro-only flows; what reconciliation detail is included. Genome and Sharpay excerpts are high level, so eligibility and operating depth still need direct confirmation. |

| Multi-provider stack | Larger teams that need fallback routing, corridor control, or provider concentration risk reduction | High | High | High | How you will normalize status models, IBAN checks, return reasons, and reporting across providers; who owns incidents; how contract and onboarding differences affect go-live timing. This route breaks fast when one provider reports final failure and another reports reversals differently. |

| End-to-end platform route | Teams that want payout execution and more of the audit and reconciliation surface in one place | Medium to high | Medium to high | Medium | Which controls are actually included for your program, what markets and entity types are supported, whether SEPA and SWIFT are both available where you need them, and how much failure detail is exposed through API, dashboard, or exports. Public claims can look broad: Narvi markets reach to 100+ countries and 75+ currencies, but also says incoming payments currently support EUR, USD and GBP and asks prospects to confirm onboarding directly. |

The biggest divider is still rail scope. SEPA Credit Transfer is for payments in euro, and the scheme materials currently cover 41 SEPA scheme countries. If your payouts are mostly euro and stay inside that footprint, a dedicated Euro IBAN route can be the lowest-friction answer. If you expect non-euro corridors, SWIFT fallbacks, or more account-level segmentation, that simplicity can become a constraint quickly.

A Virtual IBAN route deserves a closer look when attribution matters. The European Banking Authority describes vIBANs as linked to a master account, and notes that third parties may not distinguish them from standard IBANs. That is operationally useful. Before signing, verify one concrete point: can the provider show, in reporting or webhook payloads, how each vIBAN maps back to the underlying account and then to your internal beneficiary or ledger object? If not, returns and attribution gaps can turn into manual investigation work.

The known unknowns matter because current public excerpts from Airwallex, Narvi Payments, Sharpay, and Genome are directional, not architecture-grade. They show the product shape, not the full answer on eligibility, compliance scope, market-by-market support, or failure-event depth. Ask for a short evidence pack before you commit. Get onboarding confirmation for your entity, inbound versus outbound scope, a corridor list by rail, sample payout lifecycle statuses, and one failed payout example with a machine-readable reason.

Use this checkpoint to make the final call: choose the option that minimizes payout rework under your current team capacity. If your finance ops function is small and engineering cannot normalize two providers yet, do not start with a multi-provider stack. If your team can already manage exception queues and you need routing control, the added complexity may be justified. Make that call only after a corridor-level pilot proves the status and reconciliation surfaces are good enough.

We covered this in detail in Mass Payouts for Gig Platforms That Teams Can Actually Operate.

Option 1 use a virtual IBAN provider for faster launch#

If speed to launch and cleaner payment attribution matter more than having every routing option on day one, start here. A Virtual IBAN route is often a strong first move for a marketplace launching euro payouts, as long as you verify actual rail coverage, onboarding eligibility, and failure reporting before you commit.

- Best fit

This option suits teams that need fast account allocation without opening a separate bank account for every seller, creator, or merchant. In a virtual IBAN pattern, multiple IBAN identifiers map to one underlying account while preserving attribution. That is the real operational win. You keep beneficiary-level visibility without building multi-bank account logic first. If your finance ops team is small, that simplification can buy you time.

- Why launch can be faster

Providers market virtual IBANs as a way to centralize cross-border collections and payouts, with incoming and outgoing funds handled in one place. The benefit is not just account creation speed. It can also mean less reconciliation mess early on, because payment references and account mapping can stay tighter from the start. Before signing, ask for one concrete proof point: a sample report or webhook payload that shows how each virtual IBAN maps back to the master account and then to your internal seller or ledger record.

- What to pressure-test hard

The main risk is assuming broad coverage from a homepage that only describes the product shape. Coverage can vary by currency, direction, and rail. Narvi, for example, states that incoming payments currently support EUR, USD and GBP, and it explicitly asks companies to confirm onboarding directly. Rail behavior matters too. Narvi notes that if SEPA Instant is not possible, the payment is sent as a normal bank transfer, and its page gives a €100,000 per payment SEPA Instant limit. If payout timing or status expectations matter to your users, get that fallback behavior spelled out in the provider's status model, not buried in support copy.

- A practical rollout pattern

Use this route when your real goal is to get the first reliable euro lane live, then widen coverage after you learn from production. A sensible sequence is to launch one euro corridor, monitor failure reasons and delays, then add countries only after the provider confirms which payouts use SEPA, which need SWIFT or other local methods, and what failures look like in exports or API responses. Ask for an evidence pack with onboarding confirmation for your entity, inbound versus outbound scope, a corridor list by rail, sample lifecycle statuses, and one failed payout example with a machine-readable reason. That last item matters because exceptions still create manual work, and manual review is exactly what turns a fast launch into a finance ops burden later.

Related: Virtual IBANs for Platforms: How to Give Every Seller Their Own Dedicated Bank Account Number.

Option 2 use a Euro IBAN account with SEPA and SWIFT support#

If Option 1 feels too account-structure heavy for your first live lanes, this is the cleaner route. A standard Euro IBAN setup is usually the right choice when your payout pattern is stable, your beneficiaries are known, and you do not need per-user account identifiers from day one.

| Evidence item | What it should cover | Section detail |

|---|---|---|

| Supported outbound rails | Currency and beneficiary country | Ask for supported outbound rails by currency and beneficiary country |

| Successful SEPA payout sample | Status or reconciliation export | Request one sample status or reconciliation export for a successful SEPA payout |

| Returned or rejected payout sample | Failure example | Request one sample for a returned or rejected payout |

| Non-SEPA handling | Route used when a payment does not meet SEPA conditions | Get confirmation of what happens when a payment does not meet SEPA conditions and must use another route |

Best fit#

This option works best for finance teams paying a predictable supplier base in places like France and Germany on a monthly cycle. You are not trying to assign a separate account reference to every seller or creator. You just need a reliable euro account, clear payout files, and a straightforward way to send bank transfers without adding virtual-account logic too early.

The rail detail that matters is SEPA Credit Transfer (SCT). SCT is for euro payments where both accounts are located in the SEPA area. The EPC says the SCT scheme can be used across 41 SEPA scheme countries, which is why a plain Euro IBAN model can cover a lot of European payout volume without much structural complexity.

Why this route is simpler#

A standard IBAN uses a defined international account-number structure, so the operating model is familiar to banks, finance teams, and ERP tooling. For straightforward payables, that familiarity matters. Treasury and AP processes can be easier to explain, reconcile, and audit when they run through one Euro IBAN account instead of a master account plus mapped virtual identifiers.

Where SWIFT helps is outside pure SEPA conditions. If some cross-border flows require it, SWIFT can support the messaging side between financial institutions. The catch is operational. SWIFT is not the clearing and settlement system itself. So treat "SWIFT support" as a compatibility question, not proof that every outbound payment path, fee pattern, or timeline will behave the same.

What to verify before you commit#

Do not assume that having a Euro IBAN automatically means you have both outbound SEPA and outbound SWIFT for every use case. That is the first checkpoint to clear with your bank or provider in writing. Ask for an evidence pack that includes:

- supported outbound rails by currency and beneficiary country

- one sample status or reconciliation export for a successful SEPA payout

- one sample for a returned or rejected payout

- confirmation of what happens when a payment does not meet SEPA conditions and must use another route

The main tradeoff versus a Virtual IBAN model is not that a standard Euro IBAN cannot segment anything at all. It is that segmentation and attribution often become more manual. The EBA notes that virtual IBANs keep standard IBAN format and functionality while linking back to a separate master account. If you think you will soon need beneficiary-level account mapping, automated attribution, or more routing control, that future requirement is your red flag. Start with the simpler Euro account only if your payout base is stable enough that one-account reconciliation will stay manageable.

For a step-by-step walkthrough, see What is a Virtual IBAN and How Do Platforms Use It to Collect Payments Globally?.

Option 3 build a multi-provider stack for routing control#

Choose this path only when routing control is worth the extra ownership. If your team cannot explain payout failures, reconcile exceptions, and run incidents across two providers, do not add a second one yet.

| Use case | How it works | Operational note |

|---|---|---|

| Fallback recovery | Retry on another provider if the primary provider fails a payment | Avoids waiting for manual intervention |

| Rule-based routing | Send eligible euro SEPA corridors one way and reserve other flows for a different provider based on country, currency, or amount | Routing logic cannot stop at SEPA first and SWIFT second because SWIFT is messaging between institutions, not the settlement layer itself |

| Provider risk management | Keep an alternative if one provider has an outage, policy change, or coverage gap | Monitor success rates and accepted payout volume across providers from day one |

A multi-provider setup is the point where you stop buying a single payout lane and start managing routing logic yourself. In practice, that means using one provider as primary and defining fallback behavior when a payment fails, or sending payments to different providers based on explicit conditions like country, currency, amount, or account type. That control can be valuable, but it moves a lot of operational responsibility onto your side.

Best fit#

This option fits larger teams with real concentration-risk concerns or corridor-specific needs. You may have euro payouts that should go over SEPA Credit Transfer when both accounts are in the SEPA area, but also need a non-SEPA path or a backup route when that primary path fails. A second provider can give you more room to recover payments instead of just queueing exceptions.

The rail rule that matters most is still simple: SCT is for euro payments where the accounts are located in the SEPA area, and the scheme can be used across 41 SEPA scheme countries. That makes SEPA the obvious first route for many European lanes. The mistake is assuming everything else cleanly drops into "SWIFT" as a fallback. SWIFT is messaging between institutions, not the settlement layer itself, so your routing logic has to be more precise than "SEPA first, SWIFT second."

Why teams accept the extra load#

Teams accept this complexity for one reason: control. A multi-provider stack lets you route by corridor or payment attributes, retry on another provider after a failure, and reduce the risk that one provider issue stalls all payouts. That is the operational version of payment orchestration, with multiple processors or providers managed through one control layer instead of hardwiring your whole payout book to a single vendor. That control is useful in a few specific cases:

- Fallback recovery: if the primary provider fails a payment, you can define a retry on another provider rather than waiting for manual intervention.

- Rule-based routing: you can send euro payouts in eligible SEPA corridors one way and reserve other flows for a different provider based on country, currency, or amount.

- Provider risk management: if one provider has an outage, policy change, or coverage gap, you are not starting from zero.

The tradeoff is that you now own the consistency problem. Provider A and Provider B may not expose the same payout states, rejection reasons, return events, or IBAN validation behavior. Assume they differ until your own tests prove otherwise.

What breaks first if you rush it#

Reporting drift is one of the first things that can break. One provider might call a payment "submitted" while another calls a similar state "processing," and your finance team starts counting both as final when neither is. Define one canonical payout status model before onboarding a second provider. If you skip that step, your dashboards, exception queues, and success-rate reporting stop being decision-grade almost immediately.

Reconciliation sprawl is usually next. Returned payouts, reversals, and rejected beneficiary details can arrive in different formats across providers. Before go-live, ask each provider for the exact reconciliation export, status payloads for successful and failed payouts, and at least one sample return or reject event. You need to know how a failed payment is identified, how a reattempt is linked, and which identifier remains stable across providers.

Use this as your checkpoint: monitor cross-provider performance from day one, not after launch. If you cannot compare success rates and accepted payout volume across providers, you will not know whether your routing logic is helping or just creating noise. Among the options in this guide, this one gives you the most control, but only if you treat status normalization, rail rules, and reconciliation evidence as core product work, not cleanup for later.

Option 4 use an end-to-end platform with compliance and reconciliation built in#

If Option 3 felt like too much ownership, this is usually the stronger choice. Pick an end-to-end platform when you want payout execution, policy checks, and reconciliation reporting in one place. It is especially useful if finance and engineering are already spending time stitching together tax, payout, and reconciliation evidence by hand.

Where it fits#

This route is best for teams that need more than a bank rail. You want the platform to centralize payout execution alongside policy and reconciliation checks, not just transmit it after the fact. That matters when your controls include VAT-related checks or country-specific policies, because EU tax rules are not uniform. The practical test is whether the platform can apply country-aware logic, not whether it simply advertises "VAT support."

The operator detail that matters most is the reporting link between the original transaction and the payout it lands in. Some platforms support automatic payouts in a way that preserves the association between each transaction and the payout batch, and that is what makes reconciliation materially easier. If that link is missing in exports or reports, your month-end close still ends up depending on spreadsheet joins and exception chasing.

This is also the better fit when your team is already paying the cost of fragmented tooling. Research based on nearly 300 CFOs and corporate treasurers described complexity and fragmentation as a burden on finance. That does not mean one platform fixes everything, but it is a real reason to prefer fewer handoffs when you are scaling European payouts.

What to verify before you commit#

Coverage is the catch. Do not assume a platform's Europe story means the same payout methods, timelines, or account behavior in every country or program. Public docs explicitly note that payout methods and transfer timing can vary by country or region and by payout account type. Before signing off on architecture, ask for these three items:

- a country-by-country coverage view showing which payout types are available for your markets, including SEPA and international payout types where relevant, plus cut-off times and estimated delivery windows

- confirmation that your specific account or program is enabled for the payout types you need, since some providers require explicit enablement rather than turning every method on by default

- a sample reconciliation export that shows the transaction-to-payout association, plus at least one failed payout and one returned payout record

A good use case is a marketplace or platform that wants one control point for payout execution, VAT-aware policy checks, and settlement-batch reconciliation. The red flag is buying this model for "simplicity" without validating market coverage first. If your lanes depend on both SEPA and SWIFT behavior, confirm those paths with your target countries and account setup before you commit the integration.

You might also find this useful: VAT and SEPA: How European Platforms Combine Tax Compliance with Automated Euro Payouts.

Implementation checkpoints that prevent payout errors#

If you keep one rule from this guide, make it this: validate and decide before money moves, then prove you can explain failures without digging through raw logs. That is the difference between a payout flow that scales and one that quietly turns finance ops into an exception desk.

- Lock the order of operations before you write retry logic.

Start with beneficiary capture, then run IBAN format validation, then choose the rail, then execute the payout with an idempotency key. That sequence keeps avoidable input problems from looking like rail or provider failures. If you let retries fire before validation and routing checks are settled, you create duplicate investigation work instead of faster recovery.

- Confirm corridor rules in writing, not from a headline page.

Get provider confirmation for outbound rails by currency and beneficiary country, plus what happens when a payment does not meet SEPA conditions and must use another route. This matters because public pages are often directional. You need to know which payouts actually go through SEPA, which need SWIFT or another local method, and how those cases appear in status updates and reconciliation exports.

- Test the status surface before launch.

Ask for sample lifecycle statuses, one successful payout example, one failed payout example with a machine-readable reason, and one returned or rejected payout record. Then check the same states across API responses, dashboard views, webhook events, and exports. Do not accept a setup where the only clear signal is final success or failure. You need enough detail to tell whether a payment is delayed, rejected, returned, or reversed.

- Make reconciliation proof part of the vendor review.

If you are using Virtual IBANs, verify how each vIBAN maps back to the master account and then to your internal beneficiary or ledger object. If you are using an end-to-end platform, verify the transaction-to-payout association in exports or reports. If you are using more than one provider, define one canonical payout status model before the second integration goes live. Different setups create different failure modes, but the underlying rule is the same: you should be able to trace a payout request to its final state without opening a support ticket.

- Pilot one live corridor before expanding coverage.

Launch one euro corridor first, monitor failure reasons and delays, and only then add countries or a second provider. This is the fastest way to find gaps in onboarding eligibility, rail coverage, or exception reporting while the payout book is still small enough to inspect closely. A narrow pilot also tells you whether your finance team can actually work from the exported data you receive, not the data you assumed would be there.

- Do not add a second provider until the first one is observable.

If you cannot compare accepted payout volume, success rates, and failure reasons inside one provider, you are not ready to normalize two. A multi-provider stack is useful when you need routing control, fallback recovery, or provider risk management. It becomes expensive fast when the first integration is still opaque. Fix the visibility problem in one lane before you spread it across a second contract.

That checkpoint list is not glamorous, but it prevents the most common rollout mistake: buying payout capability before you prove you can operate payout exceptions.

Frequently Asked Questions

What is an IBAN number in payout operations?

An IBAN is the structured bank account identifier used across many European payout flows to route money to the right beneficiary account with fewer formatting errors. For platform operations, it is most useful when beneficiary capture, validation, and rail selection all use the same canonical account record.

When should a platform use SEPA instead of SWIFT?

Use SEPA when the beneficiary account and payout corridor meet SEPA conditions and your provider supports the currency-country pair operationally. Use SWIFT or another rail when the corridor falls outside SEPA rules, when the beneficiary country is not in the supported footprint, or when settlement requirements differ. The European Payments Council SEPA Credit Transfer overview is a useful operational reference.

What should teams validate before the first euro payout run?

Validate beneficiary account capture, IBAN format checks, currency-country support, failure codes, and the provider status flow before the first live batch. A strong launch test proves one successful payout, one rejected payout, and one returned payout all map back to clean internal references.

Do virtual IBANs replace local payout rails?

No. Virtual IBANs can simplify inbound collection and account referencing, but they do not automatically replace the local payout rail you use to send money out. Teams still need to confirm how the provider maps the virtual IBAN, ledger object, beneficiary record, and outbound rail for each corridor.

Why start with one euro corridor before adding more providers?

A single-corridor launch is the fastest way to expose onboarding gaps, weak failure handling, and reconciliation blind spots before complexity multiplies. Once one corridor is stable, you can compare success rates, exception reasons, and provider behavior with much less operational noise.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- congress.gov/crs-product/R46843trusted

- docs.stripe.com/global-payouts/manage-payoutstrusted

- eba.europa.eu/sites/default/files/2024-05/612f03de-965a-41...trusted

- ecb.europa.eu/paym/retail/sepa/html/index.en.htmltrusted

- ecb.europa.eu/paym/retail/instant_payments/html/index.en.htmltrusted

- stripe.com/gb/resources/more/ibantrusted

- airwallex.com/docs/accounts/supported-regions-and-currenciesexternal

- airwallex.com/uk/blog/virtual-iban-providersexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

What is an IBAN and How is it Different from a SWIFT Code?

For people handling high-stakes international payments, uncertainty is expensive. Not knowing whether a wire will arrive on time, or at all, pulls attention away from the work and adds avoidable risk. The fix is not another generic template. It is a repeatable process that tells you which details matter, where to get them, and how to check them before money moves.

Virtual IBANs for Platforms: How to Give Every Seller Their Own Dedicated Bank Account Number

If you want to give each seller their own receiving bank details without opening a separate traditional account per seller, start by treating this as an account-mapping and controls decision, not just a UI feature. In common setups, a virtual IBAN looks like a standard IBAN but points to an underlying master payment account rather than a standalone account.

VAT and SEPA: How European Platforms Combine Tax Compliance with Automated Euro Payouts

The hard part is not VAT on one side and SEPA on the other. It is keeping tax treatment, beneficiary checks, and euro payout execution aligned when your platform pays across multiple European markets at speed.