Quick Answer

Start with a vendor portal requirements checklist that ties every action to control evidence and accounting outcome. Set duty-based permissions with RBAC, require dual control for sensitive payout actions, and define an approval matrix by risk rather than org title. Treat the General Ledger as authoritative, and require linked records across approval logs, provider references, and webhook-driven status updates. If a “paid” state cannot be traced to posted journals and audit records, the requirement is not production-ready.

Tie portal requirements to payment evidence#

A useful vendor portal requirements checklist starts with money movement, not screen mockups. Define which actions can create an obligation, release funds, or only capture data. Then set the control, evidence, and reconciliation rules before finance, ops, and product start building inside the same boundary.

That matters because portal work is cross-functional. Finance, legal, and procurement each need different controls, and ops and product still have to turn those controls into behavior the portal can enforce. Portal workflows can centralize forms and approval tracking, which can reduce manual follow-up. That benefit disappears fast if the design looks good during onboarding and breaks down once payment exceptions start stacking up.

Use this checklist with one question in mind: what must the portal prove for every payment event? The right scope is the full payment lifecycle, not just vendor setup. In practice, that means designing for initiation, processing, clearing and settlement, reconciliation and reporting, plus exception handling and investigation. In portal terms, those stages become the actions your teams see every day: request creation, approval, execution, status updates, exception handling, and close-out evidence. A solid starting structure is:

- Define what the portal is allowed to do

Be explicit about which payment actions can start in the portal, which ones can only be reviewed there, and which ones should never be user-triggered at all. If you cannot say whether a request can create a financial obligation, release funds, or only capture data, the requirement is still too vague.

- Define who can act and who must approve

Do not stop at "finance approves" or "ops reviews." Name the actor, the approval point, and the block condition. For each high-impact action, you should be able to point to one owner, one approval rule, and one expected log entry.

- Define what gets logged and what must reconcile

Treat the General Ledger as the central accounting record, and the portal as the operating surface where requests, approvals, and status changes happen. Every important action needs an audit trail strong enough to connect the portal event to the accounting result, even when related updates are recorded at different times.

The common failure mode is treating status screens as proof. They are not. If a payout shows "paid" in the portal but you cannot trace the approval, execution reference, and resulting GL impact, you have built an ops convenience layer that adds reconciliation risk instead of removing it.

Keep the standard high from the start: if a requirement does not name the action, the approver, the audit evidence, and the GL touchpoint, it is not ready for build.

Set the operating boundary before you list features#

Set the boundary by money movement before feature design: define what each flow can do, what it cannot do, and what proof it must produce. Without that boundary, data capture, fund release, and reconciliation can get mixed into the same workflow.

| Flow | Enable now | Boundary to state up front | Acceptance output |

|---|---|---|---|

| Invoicing | Yes / No | Request capture only, or can it create a payable? | Evidence artifact, owner, SLA target, escalation path |

| Virtual Accounts | Where enabled | Use for tracking and reconciliation, not as a cash-holding view | Deposit evidence, owner, SLA target, escalation path |

| Payout batches | Yes / No | Draft only, approval only, or release-triggering | Batch evidence, owner, SLA target, escalation path |

| Dispute intake | Yes / No | Intake and status only, or can it block settlement actions? | Case evidence, owner, SLA target, escalation path |

Be explicit with Virtual Accounts. A virtual account is a uniquely identified account representation for tracking and reconciliation, and it does not hold funds directly. If supported, state whether the portal is only showing identifiers and matching status, or whether ops can take action on unmatched deposits; keep it marked "where enabled."

Write control objectives in plain language: prevent duplicate payouts, shorten reconciliation cycle time, and make critical actions traceable in the Audit Trail. For each flow, confirm the audit record captures what happened, when and where it happened, the source, and the outcome. If retries can execute again because request IDs or idempotency controls are missing, the boundary is still incomplete.

Set system-of-record rules early: the General Ledger is authoritative, portal balances are operational views, and asynchronous updates are expected when webhook events arrive later. A "paid" screen is operational status, not final proof. If status misses the agreed SLA target, route to a named escalation owner instead of relying on UI state.

For a step-by-step walkthrough, see Are You an Employee or a Contractor? A Self-Assessment Checklist.

Design permissions that survive scale and staff turnover#

After you set the money-movement boundary, design permissions around duties, not titles, and enforce separation on high-impact actions. That is what keeps controls stable through reorgs and staffing changes.

How should you define portal roles?#

Use Role-Based Access Control (RBAC) so access follows the operations each person performs. Department labels and seniority titles change; duty-based roles are easier to test, grant, and revoke.

You can start with role labels such as requester, reviewer, approver, payout operator, compliance reviewer, and read-only auditor, then map each critical action to the smallest role surface possible. If sensitive actions like bank-detail edits are spread across broad admin roles, control quality drops quickly.

Which actions need two-person control?#

For payment actions, split initiation and authorization between two different people with distinct user identities. This Maker-Checker Control is the practical baseline for actions like bank-detail changes, payout release, and approval overrides.

When you test permissions, verify behavior, not UI steps: the same identity should not be able to submit and approve the same item. In the Audit Trail, confirm time-stamped records for create/modify/delete actions, with actor identity captured and prior values preserved when records change.

How should emergency access work?#

Treat break-glass access as an emergency-only path, not an operations shortcut. If emergency access starts handling routine queue pressure, it becomes a standing bypass instead of a resilience control.

A compact permissions test table can help keep this visible across teams and turnover. At minimum, track each high-impact action, who is allowed, who is denied, and the expected Audit Trail events.

Build an approval matrix tied to risk not org chart#

Use the approval matrix to route review by risk, not by title. Keep approval depth tied to impact, reversibility, and compliance exposure, so low-risk edits do not block execution-critical changes.

A common failure in a vendor portal requirements checklist is one blanket rule such as "manager approval required" for everything. Separate by action type and, where needed, by field, because some systems support routing specific vendor-field changes to approval before updates are applied.

| Action type | Risk signal to route | Approval depth | SLA design note |

|---|---|---|---|

| Vendor profile change | Changes that can affect payment execution or compliance posture | Lower depth for low-impact fields; higher depth for payout-relevant or sensitive fields | Set clear owner and escalation so blocked changes do not stall operations |

| Payout batch release | Sensitive or high-risk release conditions | Dual approval can be required; add levels for higher-risk cases | Treat as execution-critical with explicit queue ownership |

| Routing override | Override that changes payout path, destination, or control outcome | Higher-depth approval with compliance visibility | Fast path only if evidence capture remains complete |

| Refund | Destination/path differences and exception patterns | Depth based on risk of the specific refund case | Keep a separate commitment so customer-impact exceptions are not orphaned |

Set conditional rules in the matrix. If a change affects payout method or destination, route to a higher-approval path and require renewed checks before execution; if a change is non-financial, a lighter path may be enough.

Include explicit KYC, KYB, and AML triggers. A manager approval does not replace compliance review when identity, beneficial ownership, or suspicious-activity risk changes. Your matrix should call out events like new legal-entity onboarding, beneficial-owner changes, and activity that requires AML review before release.

Each approval should write evidence to the Audit Trail: actor, timestamp, action, reason, and before/after state tied to the request or transaction. For vendor edits, preserve original and proposed values and show pending status while authorization is incomplete. If high-risk and low-risk edits produce the same trail and same path, the matrix is too blunt.

For the end-to-end build pattern, see How to Build a Vendor Portal for Platforms: Tax Forms Invoices Payouts and Disputes in One Workspace.

Split self-service from admin-only actions with explicit guardrails#

Set the boundary so vendors can submit and track requests, but cannot directly change how money moves or how controls are applied. This is where the approval matrix becomes operational: the self-service line affects AP workload and fraud surface.

Keep self-service for routine, low-risk work. Supplier portals can reduce routine invoice and payment-status inquiries, and common portal patterns include profile updates plus payment visibility. In practice, this usually means invoice submission, status tracking, document upload, and profile edits that go to review instead of applying immediately.

Which vendor actions should stay in review?#

Use RBAC so vendor roles can create requests and submit documents, while higher-impact actions stay restricted. A vendor can upload a Form W-9 when you need TIN data for information returns, and a Form W-8 BEN when requested by the payer or withholding agent. Treat those uploads as review inputs, not final tax determinations by themselves.

| Action | Access | Note |

|---|---|---|

| invoice submission | Vendor self-service | routine, low-risk work |

| payment and invoice status tracking | Vendor self-service | routine, low-risk work |

| upload of Form W-9 and Form W-8 BEN documents | Vendor self-service | review inputs, not final tax determinations by themselves |

| low-risk profile updates | Vendor self-service | submitted for approval |

| payout routing or destination changes | Admin-only | keep out of self-service by default |

| policy or approval-rule overrides | Admin-only | keep out of self-service by default |

| release from a compliance hold | Admin-only | after AML review |

| any action that both proposes and executes a funds-moving change | Admin-only | keep out of self-service by default |

Vendor self-service

- invoice submission

- payment and invoice status tracking

- upload of W-9 and W-8 BEN documents

- low-risk profile updates submitted for approval

Admin-only

- payout routing or destination changes

- policy or approval-rule overrides

- release from a compliance hold after AML review

- any action that both proposes and executes a funds-moving change

If an action can change payee identity, payout destination, or control logic, keep it out of self-service by default. Least privilege and separation of duty are the right control anchors here, and sensitive release steps should not be executed by the same actor who submitted the change.

What statuses should the portal show?#

Show a clear user-facing state for every request: pending review, approved, blocked, needs documents, or paid. This reduces support churn and prevents repeated resubmissions caused by unclear status.

Before launch, test one tax-document flow and one restricted action. Upload a W-9 and confirm it lands in review with the correct label and timestamp, and that the vendor can see pending review but cannot self-approve. Then attempt a payout-routing change from a vendor role and confirm it is denied, logged in the Audit Trail, and available only to the designated admin role.

The tradeoff is straightforward: more self-service lowers AP handling work, but each additional editable field expands risk unless permissions, approval gates, and visible states are tight. If the boundary is unclear, start narrower, keep funds-moving and policy-changing actions admin-only, and expand only after controls are proven.

Related: How to Build a Vendor Self-Service Portal That Reduces AP Workload.

Specify the audit evidence pack finance will actually use#

Finance should be able to prove each money movement end to end without rebuilding the story at close. Set the standard as one traceable chain from internal request to provider outcome to posted General Ledger journal, with approval and event evidence attached.

If that chain cannot be exported by period and entity, reconciliation degrades into manual ticket-and-screenshot work.

What records must every money event link together?#

Treat this as a fixed evidence contract for each payout or routed payment event:

| Evidence item | Why it matters | Verification check |

|---|---|---|

| Internal request ID | Anchor for the originating user or system action | Present on the request and in the audit log |

| Provider reference | External key for tracking and reconciliation | Matches provider-side transaction or Transfer ID |

| Approval record | Proof of authorized decisioning | Includes actor, timestamp, reason, and decision state |

| Webhook events | Evidence of asynchronous status changes | Includes event time, delivery status, and request ID linkage when available |

| Posted General Ledger journal | Close and reconciliation evidence | Journal is posted and includes the reconciliation reference used on related clearing lines |

A reconciliation reference on related journal lines is what makes clearing-account reconciliation faster at scale.

What is the minimum audit log?#

Define an internal minimum and enforce it consistently. Log actor, action, timestamp, entity, old value, new value, reason, and related transaction IDs. Where applicable, align payment-event logging with PCI DSS v3.2.1 event-record guidance (user identification, event type, date/time, success/failure, and event origination).

Use a launch checkpoint that tests one completed payout: the same transaction linkage should appear across request, approval, webhook evidence, and posted journal. A common break is clean provider references with missing journal linkage.

How should finance export evidence?#

Export evidence by legal entity and period range, not as one-off case files. Include linked records plus a readable event timeline, and mask PII where disclosure is not required.

If regulated data is in scope, apply regime-specific checks instead of assuming one control set covers all cases. For HIPAA, 45 CFR 164.312(b) requires mechanisms to record and examine activity in systems that contain or use ePHI. For PCI DSS, verify required payment-event logging fields are present. For Cal ECPA, treat it as a disclosure and access constraint, not as a payments control framework.

Engineer failure handling before you ship#

Treat failure handling as a launch requirement. Your payout flow should stay replay-safe and reconcilable even when status signals are delayed, duplicated, or incomplete.

| Failure mode | Baseline | Handling |

|---|---|---|

| delayed Webhook delivery | "no update yet" is not the same as "nothing happened" | If status is still unknown after your SLA window, pause downstream release actions, open an investigation queue, and assign an owner and due time. |

| duplicate callback | duplicate webhook delivery is normal; some providers may retry non-2xx webhook deliveries up to 25 times over 3 days | Enforce replay safety with an Idempotency Key at every write point. |

| stale FX quote | extended quote locks can be 5 minute, 1 hour, or 24 hour; a quote moves from active to expired after lock_expires_at | If the quote is expired, require a re-quote before release. |

| provider return | define it as an expected failure mode | Hold reissue until the original payout and reversal evidence are linked. |

| unmatched deposit in Virtual Accounts | define it as an expected failure mode | Keep it as an open item with an investigation owner instead of forcing a match. |

Use this pre-ship checklist:

- Define expected failure modes. At minimum, model delayed Webhook delivery, duplicate callback, stale FX quote, provider return, and unmatched deposit in Virtual Accounts. Duplicate webhook delivery is normal, and some providers may retry non-2xx webhook deliveries up to 25 times over 3 days, so "no update yet" is not the same as "nothing happened."

- Enforce replay safety with an Idempotency Key at every write point. Cover payout creation, status writes, and ledger posting, not just the first API call. Test by sending the same POST twice with the same key and confirming the prior result is returned instead of creating a second payout or journal.

- Set your unknown-status rule for your own SLA window. If status is still unknown after that window, pause downstream release actions, open an investigation queue, and assign an owner and due time. This is a control hold, not an automatic payment-failed decision.

- Keep resolution evidence attached to the original event chain. If your Audit Trail supports a single thread, keep investigation notes, retry evidence, provider references, and final disposition there. If not, link exception records back to the original request and transaction IDs.

Handle time-bound states explicitly#

FX is the clearest case: extended quote locks can be 5 minute, 1 hour, or 24 hour, and a quote moves from active to expired after lock_expires_at. If the quote is expired, require a re-quote before release.

Apply the same pattern to exceptions: if a provider return arrives, hold reissue until the original payout and reversal evidence are linked; if a Virtual Accounts deposit is unmatched, keep it as an open item with an investigation owner instead of forcing a match.

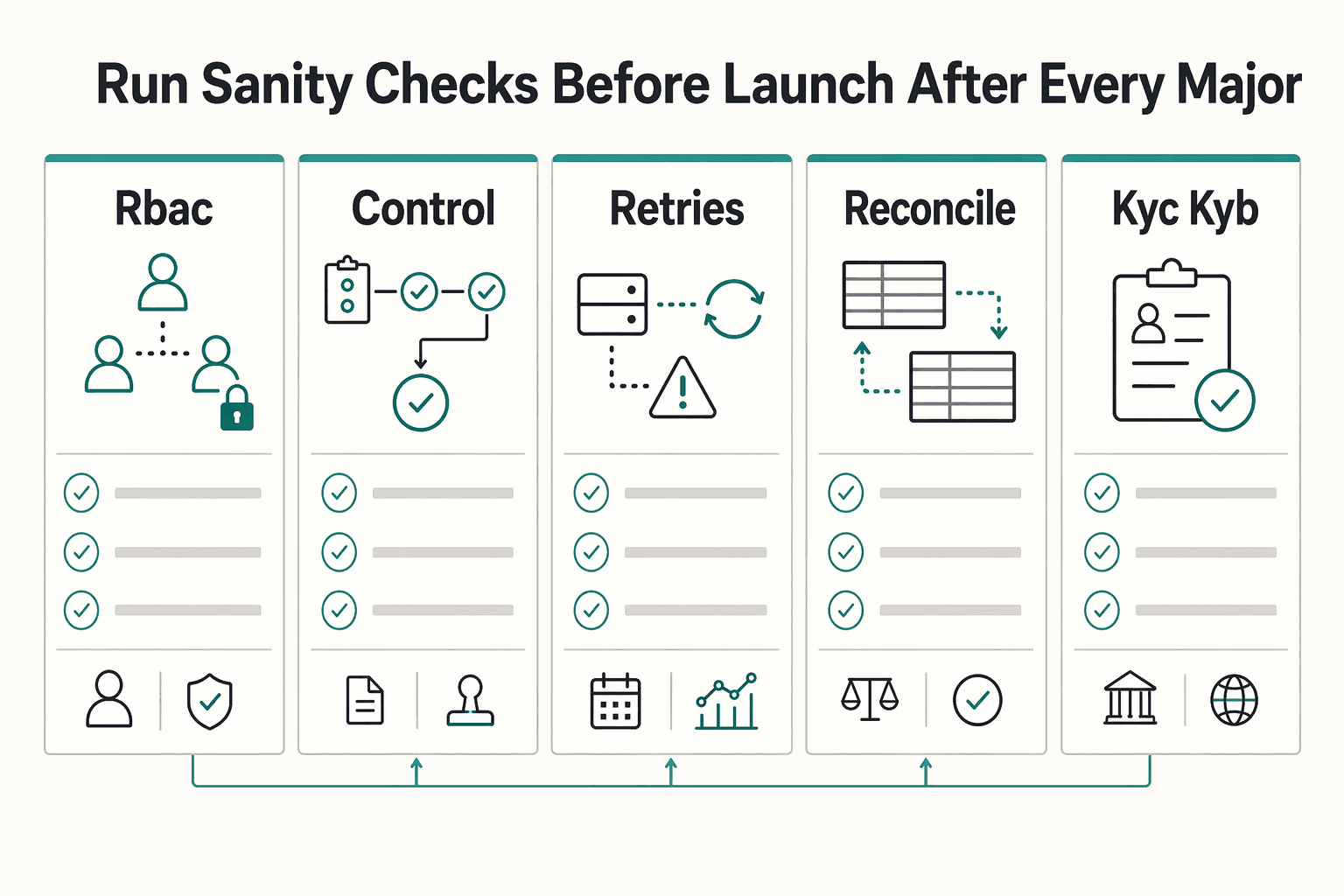

Run sanity checks before launch and after every major change#

Treat this as a release gate: if a change touches roles, approvals, webhook ingestion, payout routing, or export mapping, rerun your control tests before production.

| Check | Test | Pass condition |

|---|---|---|

| RBAC | test denied access for unauthenticated access, horizontal access to another user's record, and vertical access to admin actions | denied access for each path |

| Maker-Checker Control | confirm one user can create but cannot approve the same request | creation and approval stay with separate actors |

| Retries | resend the same POST with the same idempotency key | you get the prior result, not a second payout, second status write, or second ledger effect |

| End-to-end reconciliation | reconcile one sample transaction: portal status -> provider reference -> General Ledger posting -> final export pack | if any hop cannot be matched, treat it as a launch blocker |

| KYC/KYB/AML checks | if checks apply to a legal entity, block account use until beneficial-owner identification and verification are complete | account use stays blocked until those checks are complete |

| Form 1099 output | validate output and filing timing for your supported path | Form 1099-NEC by January 31; Form 1099-MISC by February 28 (paper) or March 31 (electronic) |

| Rollback drill | break an approval policy, stall webhook ingestion, and misroute a payout batch | restore prior policy, recover or replay stuck events, and leave an evidence trail finance can follow |

Use scripted critical-path checks, not only UI happy paths:

- For RBAC, test denied access for unauthenticated access, horizontal access to another user's record, and vertical access to admin actions.

- For Maker-Checker Control, confirm one user can create but cannot approve the same request, so creation and approval stay with separate actors.

- For retries, resend the same POST with the same idempotency key and verify you get the prior result, not a second payout, second status write, or second ledger effect.

Reconcile one sample transaction end to end: portal status -> provider reference -> General Ledger posting -> final export pack. If any hop cannot be matched, treat it as a launch blocker.

Verify compliance and tax gates that are easy to miss in demos:

- If KYC/KYB/AML checks apply to a legal entity, block account use until beneficial-owner identification and verification are complete.

- Where Form 1099 is enabled, validate output and filing timing for your supported path: Form 1099-NEC by January 31; Form 1099-MISC by February 28 (paper) or March 31 (electronic).

Finish with a rollback drill in a controlled test: break an approval policy, stall webhook ingestion, and misroute a payout batch. Pass only if you can restore prior policy, recover or replay stuck events, and leave an evidence trail finance can follow.

For the broader launch-readiness lens, see Digital Product Launch Checklist: Demand, Pricing, Compliance, and Operations.

Conclusion#

A credible vendor portal requirements checklist is a control design, not a catalog of screens. If a requirement cannot be tied to an owner, a verification method, and an audit artifact, it is not ready for launch.

That is the thread running through every section above. The requirements that matter are the ones that still hold up when volume rises, staff changes, requests retry, and a finance reviewer asks for proof. In practice, that means designing around control activities such as approvals, authorizations, verifications, and reconciliations, then making responsibility explicit instead of assuming the team will sort it out later.

Your strongest next move is to turn this into a one-page requirement table for each money flow you support. Do it per flow, not as one giant master sheet, because payout release, vendor profile changes, invoice intake, and exception handling do not share the same risk. Each row should answer five things clearly:

- What is the action or event?

Example: bank detail edit, payout batch release, duplicate callback, unmatched deposit.

- Who owns it?

Name the operational owner and the approver, not just the team. This is where Assignment of Responsibility matters.

- What control applies?

RBAC permission, maker-checker control, compliance review, idempotent write, reconciliation check, or escalation rule.

- How do you verify it?

Add one pre-launch test per row. For example, resend the same payout creation request with the same idempotency key and confirm there is one payout effect and one recorded outcome, not two.

- What is the evidence artifact?

Specify the exact audit record, approval object, provider reference, webhook history, investigation note, or export pack that proves the control worked.

A good checkpoint is to sample one normal case and one broken case for every critical flow. For the normal case, confirm you can trace request to approval to execution to posting. For the broken case, confirm the portal shows the failure state, the owner, and the recovery evidence in the same thread. If your team has to reconstruct the story from chat logs or database queries, the requirement is still too loose.

One red flag to keep in mind: do not treat separation of duties or idempotency as box-checking. A two-person rule is only real if one user cannot both initiate and release a sensitive action, and retry safety only helps when downstream effects are controlled too. The failure mode is subtle: the UI looks controlled while the back end can still allow duplicate or unreviewed effects.

If you want the portal to reduce risk rather than create another ops surface, finish with a control test before launch and after every major change. That is where a design becomes believable.

Frequently Asked Questions

What must a vendor portal include to be audit-ready for payouts and reconciliation?

At minimum, each payout-related event should have traceable structured records: what happened, when, where or from what source, the outcome, and who performed it, plus linked approval and payout status context. If finance cannot trace a transaction across those records without asking engineering to reconstruct it, the portal is not audit-ready. A good checkpoint is to pull one paid item and one exception item and confirm both can be matched from start to finish.

Which actions always require dual approval under a Maker-Checker model?

Use dual approval for actions that can move funds, override a control, or materially change payment routing. That aligns with the separation-of-duties and two-person rule concept, even if the exact approval matrix differs by company. A red flag is letting the same user create and release a payout, or submit and approve a routing override in the same Audit Trail thread.

What should be self-service for vendors versus admin-only for operations teams?

Self-service should cover account-data maintenance and similar lower-risk updates only when access is authorized and controlled. High-risk actions should stay admin-only, especially payout routing changes and control overrides. If you allow profile edits in the portal, put them behind review rather than making them instantly effective.

Which audit log fields are mandatory for finance close and compliance review?

There is no single universal field list for every regime, but structured fields are non-negotiable. For this use case, log the event type, timestamp, source or location, outcome, and actor identity, then link related transaction and approval records. Free-text notes alone are not enough when someone has to prove who changed what and whether the action succeeded or was denied.

How do you prevent duplicate payouts when webhooks retry or users retry submissions?

Use an Idempotency Key on payout/API requests. Then treat retries as a replay of the original request rather than a new instruction. The practical test is simple: resend the same request with the same key and confirm you get one payout effect, not duplicates. If your webhook consumer is not idempotent, duplicate callbacks will eventually create a reconciliation mess.

How should portal teams handle unmatched deposits and returned transfers in Virtual Accounts?

Do not leave them as vague exceptions. Returned and failed outcomes should be explicit statuses, and unmatched deposits should go into a time-bound reconciliation process with a clear owner and supporting evidence. Operators should have enough context to investigate and record final resolution. Unreconciled discrepancies that sit too long can become a control or regulatory issue.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Build a Vendor Portal for Platforms: Tax Forms Invoices Payouts and Disputes in One Workspace

Treat the **vendor portal for platforms** as an operating surface, not a file drop or message inbox. If it cannot support onboarding checks, invoice and payment visibility, clear access boundaries, and a reliable record of status changes, it will not take real work off finance and ops.

How to Build a Vendor Self-Service Portal That Reduces AP Workload

If the portal does not remove AP inbox work, show payment and document status, and preserve a usable AP audit trail, it is not real self-service. This guide is for platform teams that want fewer vendor support loops and cleaner evidence when finance or compliance asks what changed, when, and by whom.

How to Invoice a German GmbH Compliantly

If you want a Rechnung that gets paid without back-and-forth, treat first-pass accuracy as a cash flow task, not admin cleanup. Two failures are common and expensive: sending a duplicate or conflicting invoice, and invoicing while scope or acceptance is still disputed.