Quick Answer

Build a vendor onboarding roi calculator around task-level labor, exception handling, and downstream cleanup, then compare manual review, automation-first, and hybrid paths. Use concrete checkpoints such as W-9/W-8 completeness, TIN/EIN validation, ACH/SWIFT verification, OFAC dispositions, ERP vendor-master quality, and GL mapping accuracy. The article’s core recommendation is to default to hybrid when failure cost is meaningful, then validate projected gains with a controlled pilot before scaling.

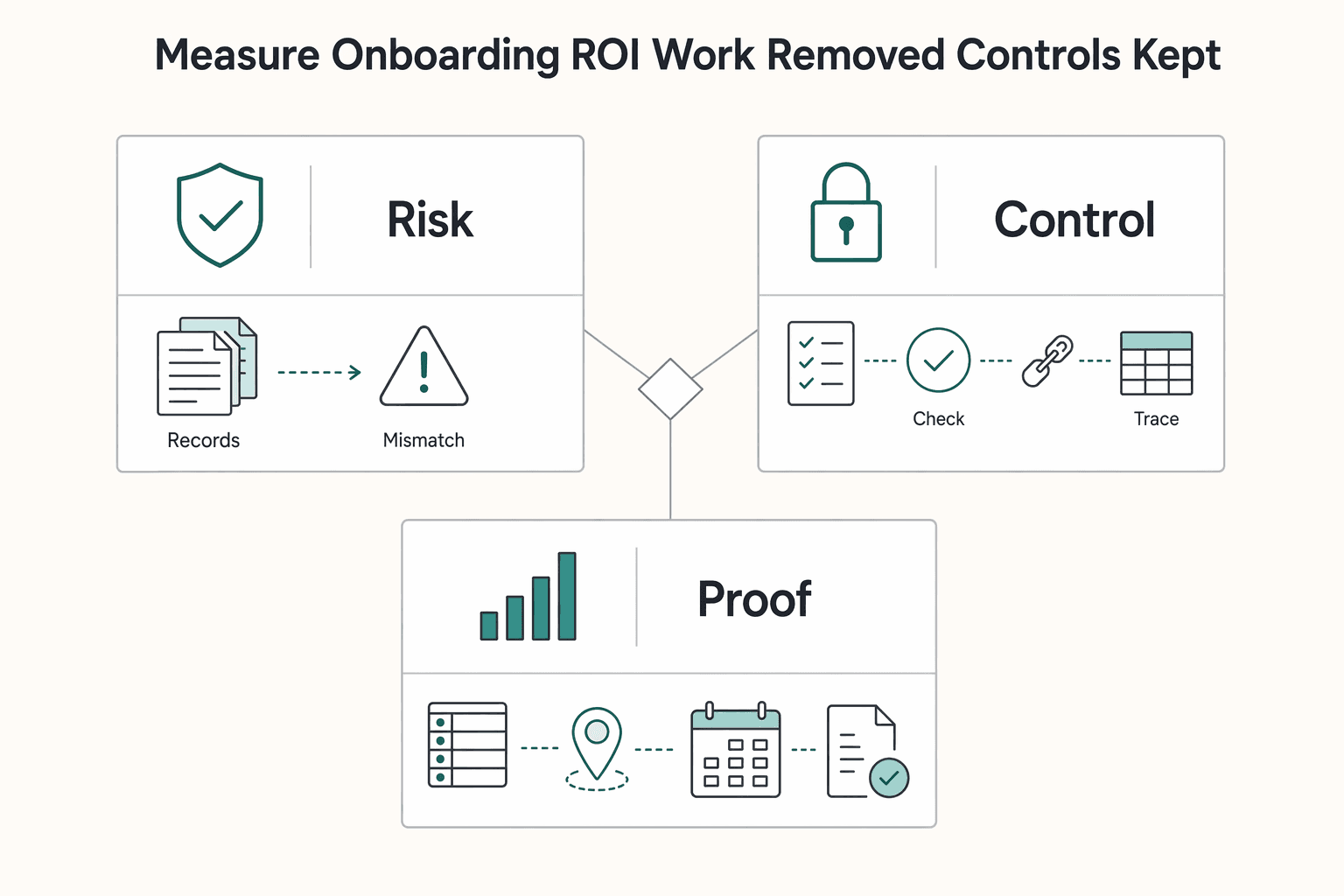

Measure onboarding ROI by work removed and controls kept#

A credible vendor onboarding roi calculator should answer one question clearly: does automation remove enough real work, without weakening controls, to justify the spend? That's the case you need to make to finance and ops. The real comparison is simple to state and harder to model well. It is manual review across onboarding data, banking, compliance, and ERP setup versus automated verification that still routes exceptions to a human.

That distinction matters because manual onboarding cost is usually spread across teams instead of showing up as one obvious line item. The time drain can sit in email follow-ups, spreadsheet tracking, document review, bank detail checks, approval chasing, and vendor master creation. Industry messaging around automation usually points to lower cycle time, less admin effort, and broader compliance coverage. That is directionally useful, but not enough to support a defensible ROI case on its own.

A better operator lens is not "How fast can we approve a vendor?" Ask instead: "What work disappears, what work merely moves, and what control risk changes afterward?" An automation-first approach can replace manual email and spreadsheet intake with a centralized portal and sync approved vendor data directly into ERP vendor master records. That can reduce repetitive handling, but it does not remove the need to review exceptions, confirm bank account details before money moves, or check whether approved data lands cleanly in the right downstream records.

That last handoff is where many ROI models get too shallow. Faster onboarding only matters if it improves payout readiness and does not create more reconciliation cleanup later. If your team approves vendors quickly but bank-detail or verification issues still surface downstream, the saved onboarding minutes can be offset by payment failures, rework, and correction entries. In practice, verify one concrete handoff: whether approved vendor data is actually usable for payment setup and ERP posting without manual repair.

For platform teams, the scope should extend beyond intake and approval screens. Your model should connect onboarding effort to control quality in ledger journals, reconciliation, and payout readiness. Reconciliation adjustments are recorded through journal entries in the general ledger, so weak onboarding controls can reappear later as discrepancies someone has to investigate and correct. That is why this article treats ROI as a comparison of operating models, not just a time-saved estimate. Manual review, automation-first, and hybrid automation with human exception handling each shift cost, risk, and auditability in different ways.

If failure cost is meaningful, start from the hybrid assumption and make the math prove otherwise. That usually gives finance a cleaner case because it ties speed gains to evidence your team can actually verify. For a step-by-step walkthrough, see Client Onboarding Blueprint for Freelancers from Proposal to Kickoff.

Manual review vs automated verification at a glance#

If you need to model cost and control together, start with a hybrid baseline: automate standard checks, then review exceptions. Manual review is usually slower and harder to keep consistent at scale, while automation-first can move faster but push failure cost downstream when policy gates are weak or late.

| Criteria or task | Manual baseline | Automation-first | Hybrid |

|---|---|---|---|

| Data inputs | Collected across email, PDFs, portal uploads, and spreadsheets | Centralized intake with structured fields and document capture | Same structured intake, plus reviewer checkpoints on risky records |

| Cycle time impact | Slower due to follow-ups, handoffs, and rekeying | Faster for standard cases | Faster than manual, without assuming touchless for every case |

| Control coverage | Depends on checklist quality and staff consistency | Broad when rules are configured early and applied consistently | Broad automated checks plus human judgment on edge cases |

| Exception handling | Often handled ad hoc in inboxes and shared sheets | Can bottleneck if routing is weak | Clear queue for mismatches, sanctions matches, tax gaps, and bank anomalies |

| Audit evidence | Fragmented across threads and attachments | Better when tools store status, timestamps, and submitted docs | Strong when automation logs steps and reviewers record dispositions |

| Integration effort | Lower upfront, high ongoing rekey work | Higher upfront ERP/data-mapping effort | Similar integration effort, with explicit review states |

| Model transparency | Labor is visible; hidden rework is not | Savings can look overstated if exception cost is excluded | Easier to defend when touchless and reviewed paths are separated |

| W-9/W-8 and TIN/EIN capture | Staff request forms, read fields, and chase missing data | Required fields and uploads can be enforced by rules | Automation collects data; reviewer resolves missing/inconsistent tax fields |

| ACH/SWIFT checks | Staff verify routing/account details manually; SWIFT can be misread as settlement readiness | Fast field validation, but bad source data can still pass | Automation validates first; reviewer confirms high-risk or cross-border details |

| OFAC screening | Manual checks are slower and harder to evidence | Screening can run early and consistently | Screening runs automatically; potential matches get human disposition |

| ERP vendor master setup | Manual ERP entry after approval | Approved records can sync to ERP vendor master | Auto-sync clean records; hold incomplete records for review |

| GL mapping | Often assigned during or after ERP entry | Can be defaulted by rules | Rule defaults plus review when posting profile assignment is unclear |

Tax and banking work drives more downstream rework than most ROI models capture. A W-9 is used to provide a correct TIN, and for many non-individual entities that identifier is the EIN; for foreign beneficial owners, Form W-8BEN is submitted when requested by the payer or withholding agent. ACH is a U.S. batch transfer network, while SWIFT is a messaging network rather than settlement, so a record that looks complete can still fail payout-readiness for the intended rail.

Sanctions, ERP sync, and GL mapping are where control quality becomes visible. U.S. persons are prohibited from transactions involving property interests of parties on the OFAC SDN list, so consistent screening and documented disposition matter. ERP sync can remove rekeying, but AP posting setup still determines which summary account posts vendor balances to the general ledger.

Recommendation: If failure cost is high, choose hybrid automation with strict exception review over full touchless onboarding. Use automation to collect W-9/W-8 data, run OFAC and bank checks early, and sync clean records to ERP, while requiring human review for sanctions matches, tax mismatches, cross-border banking details, and unclear GL mapping.

One tradeoff to model explicitly: faster onboarding can increase rework when KYC/KYB/AML gates are weak or late. In some platform flows, unverified information can pause charges or payouts once required-information thresholds are hit, so speed only counts when approval also means payment-ready, ERP-ready, and audit-ready.

Define the minimum viable ROI model before picking a tool#

To make the calculator defensible, define your minimum model before comparing tools. If a comparison counts labor savings but omits exceptions, rework, or control quality, treat the result as incomplete.

| Type | Model item |

|---|---|

| Input | vendor volume |

| Input | analyst effort by task |

| Input | labor cost assumptions |

| Input | exception rate |

| Input | rework path when OFAC or bank verification checks fail |

| Output | current cost |

| Output | future cost |

| Output | net savings |

| Output | ROI percent |

| Output | time to onboard |

| Output | control quality indicators tied to SLA performance and error leakage |

Make these inputs explicit up front:

- vendor volume

- analyst effort by task

- labor cost assumptions

- exception rate

- rework path when OFAC or bank verification checks fail

Then lock the outputs before vendor pages start shaping your assumptions:

- current cost

- future cost

- net savings

- ROI percent

- time to onboard

- control quality indicators tied to SLA performance and error leakage

For ROI percent, use the plain formula: benefits minus costs, divided by costs, times 100. Some calculators show this structure clearly. For example, one page shows sample inputs of 1,000 vendors per year and $60,000 salary per FTE, with outputs of $300,000 current cost, $134,769 future cost, $165,231 net savings, and 55% ROI. Use figures like these as model-structure examples, not universal benchmarks.

| Calculator context | Typical inputs | Why it is not directly comparable |

|---|---|---|

| Supplier onboarding ROI calculator | Supplier volume, processing effort, time and cost savings | Focuses on supplier setup, not merchant funnel economics |

| Merchant onboarding ROI calculator | Volume, costs, conversion rates | Built for merchant acquisition and approval flow, not vendor master and AP readiness |

| Platform vendor operations model | Vendor volume, task effort, exception rate, rework, SLA, control leakage | Must connect onboarding speed to payment readiness and downstream ops quality |

Keep a short "known unknowns" block in your model. Trust Your Supplier and Clustdoc emphasize interactive estimates in visible page copy, and may not expose full formulas or exclusions there. Treat that as a signal to model exception staffing, review effort, and error leakage explicitly on your side.

If you want a deeper dive, read AP Automation ROI Calculator: How to Build the Business Case for Your Finance Team.

Break the onboarding job into tasks where ROI is won or lost#

ROI is won when you automate deterministic checks and protect judgment-heavy risk decisions with human review. Do not model onboarding as one block of effort. Split intake-to-approval work into task-level checkpoints so you can separate removable effort from exception effort.

Use a practical order of operations: document collection, tax validation, bank verification, sanctions/compliance screening, approvals, then ERP vendor-master creation. This order helps surface issues before payout enablement, where fixes are usually more expensive.

| Task | Automate first | Keep human review for | Failure mode if missed |

|---|---|---|---|

| Document collection | Request and capture required forms/fields consistently | Unusual entity context or foreign payee edge cases | Incomplete files and stalled approvals |

| Tax validation | Presence/format checks for Form W-9 or Form W-8BEN-E, plus TIN/EIN rule checks | Name-tax ID mismatches, foreign-status edge cases, unclear withholding treatment | Incomplete tax profiles and downstream reporting breaks |

| Bank checks | ACH/SWIFT detail checks and micro-deposit validation steps where used | Legal-entity/account-owner mismatches and cross-border exceptions | Failed payments, manual correction, payout delays |

| Sanctions/compliance screening | OFAC list screening plus duplicate/address anomaly flags | Potential matches and other cases needing due diligence | False clears, false positives, approval delays |

| Approvals + ERP creation | Multi-level routing, vendor-master creation, prefill for category/tax region/GL mapping | Policy exceptions and nonstandard coding paths | Duplicate vendor records, bad GL mapping, reconciliation cleanup |

What should stay automated, and where do you still need judgment?#

Automate comparisons of known fields; keep people on ambiguous context. Checking that required tax forms exist, validating submitted identifiers against your rules, and running list-based screening are good automation targets. Deciding whether a near match is truly the same entity, or whether edge-case foreign documentation fits your payout setup, is where analyst review protects quality.

This is where ROI models often overstate savings: approval and exception effort is usually reduced, not eliminated. Automated onboarding flows still include manual reviews, comments, and approval steps for judgment cases.

When should compliance gates happen?#

Run identity and compliance gates (for example, KYC/KYB/AML controls) before final payout enablement as an operating design choice, then map legal sequencing to your jurisdiction-specific policy. The operational point is simple: catch issues before payment-ready status to avoid late rework.

Treat OFAC list search as one input, not the full control. OFAC states its sanctions search tool is not a substitute for appropriate due diligence, so your model should include review and documentation time for potential matches.

Duplicate vendor records, bad GL mapping, and incomplete tax profiles are the failure paths that erode ROI after go-live. Price those paths explicitly in your calculator, or your savings estimate will be inflated.

Related: Vendor Onboarding Automation: How to Collect Bank Details Tax Forms and Compliance Docs at Scale.

Hidden costs competitors understate#

Headline ROI usually shows gross savings, not savings you can safely budget. The misses are typically integration upkeep, exception handling, and evidence work that remains after automation goes live.

| Cost or risk | What headline ROI often assumes | What you should actually model |

|---|---|---|

| Integration maintenance | One-time setup, then low-touch operations | Ongoing connector maintenance, plus implementation and training costs |

| Exception queue staffing | Alerts are rare and mostly auto-resolved | Rework rate, manual review time, and queue coverage for bank, tax, and sanctions edge cases |

| Policy tuning and false positives | Screening stays cheap after launch | Analyst investigation time for false positives, rule tuning, and approval-note cleanup |

| Async event timing | Approval instantly updates downstream systems | Webhook delays, duplicate-event handling, and eventual consistency before ledger journals reflect changes |

Use a quick sanity check: if a calculator does not ask about implementation, training, rework percentage, or investigation time, it is presenting a partial case. Treat that as capacity released, not cash saved, until your own operating data proves otherwise.

Control debt is easier to create than to see. If intake is automated without durable audit artifacts, you can create support gaps later for 1099 workflows, and for FBAR or FEIE-related processes where onboarding data is reused. Form 1099-NEC requires a statement to the recipient, FBAR is due April 15, and FEIE applies only when specific requirements are met. A record that only says "approved" is usually not enough when evidence is requested later.

Timing assumptions also need to be explicit. Webhooks are asynchronous and can deliver the same event more than once, and eventual consistency means writes may not be visible immediately. In practice, teams often wait for downstream updates and visible journal state before treating onboarding as complete.

What counts as a red flag in calculator claims?#

When reviewing Hyperbots Agentic AI-style calculators against your own data, treat these as warning signs:

| Claim area | Red flag |

|---|---|

| Input scope | It asks only for vendor volume, labor rate, and cycle time |

| Exception handling | It ignores rework percentage and exception queue staffing |

| Sanctions handling | It treats sanctions alerts as pass/fail with no false-positive investigation cost |

| Event processing | It assumes webhook events are unique and downstream updates are immediate |

| Audit evidence | It cannot show how audit evidence is retained or exported for 1099, FBAR, or FEIE-related support where relevant |

| Evidence basis | It relies on assumptions and anecdotes instead of measured before-and-after operating data |

Only count savings as bankable when you can tie them to observed queue time, retained evidence, and actual downstream posting behavior.

Choose by scenario, not by marketing claims#

Once you price hidden costs honestly, the right choice is the onboarding model that matches risk, complexity, and ownership boundaries, not the one with the biggest automation claim. If vendor volume is high and variance is low, prioritize automated verification with exception handling. If the population is mixed, cross-border, or high impact, use hybrid controls with stricter manual approval gates.

| Operating scenario | Recommended model | What matters most |

|---|---|---|

| High vendor volume, low variance in requirements | Automation-first with exception handling | Small inefficiencies compound quickly at scale, so manual effort should focus on failures and mismatches |

| High complexity, mixed risk tiers, critical vendors | Hybrid with stricter manual gates | Review depth should be commensurate with risk profile, complexity, and activity criticality |

| Merchant of Record setup or shared payment ownership | Boundary-aware hybrid | Define ownership for tax, compliance, disputes, refunds, approvals, and evidence retention before rollout |

A practical rule for the ROI model is: if count is high and variance is low, automate more; if complexity and risk diversity are high, keep stronger human controls. Do not treat touchless onboarding as a default when risk tiers differ materially across vendors.

Who should the tool be built for after launch?#

Choose for the operator, not the demo buyer. If you are a finance leader, optimize for auditability and reconciliation first: routed approvals, timestamped decisions, and exportable evidence should be non-negotiable. If the system can approve a vendor but cannot clearly show who approved what and when, savings are not yet defensible.

If you are a product owner, optimize for integration behavior and state visibility. Use webhooks for asynchronous updates, but pair them with a status surface that shows where each request sits and what is blocking completion. A webhook event alone is not proof that the full onboarding chain is complete.

How are direct payables and Merchant of Record different?#

These are different operating models, so evaluate them separately. In direct payables flows, your team typically owns more of the control chain end to end. In a Merchant of Record setup, core tax, compliance, and dispute responsibilities shift into the MoR boundary, so ownership lines must be explicit.

Do not approve rollout until exceptions, approvals, and evidence exports are mapped end to end across the lifecycle. Run a live trace from intake through final status and confirm the audit trail is complete before treating ROI as bankable.

Build the evidence pack your CFO and auditor will accept#

If your ROI claim cannot be traced to onboarding events, approvals, and downstream payment evidence, it is not budget-ready. Treat the evidence pack as part of the operating model, not post-launch cleanup.

A defensible ROI model needs baseline assumptions, a task-level time model, an exception taxonomy, approval logs, and monthly forecast-versus-actual variance tracking. Summary dashboards help, but auditors and finance leaders also need records they can examine.

| Evidence area | Demo-grade proof | CFO and auditor acceptable proof |

|---|---|---|

| Baseline and savings logic | One blended "hours saved" assumption | Task-by-task baseline with owner, minutes per task, volume assumption, exception rate, and labor cost basis |

| Approval and control history | Final status only | Timestamped approval log with approver, reviewed items, comments, and linked documents |

| Downstream traceability | "Payout ready" screen or export | Trace from onboarding request ID to payout readiness, payout batch status evidence, and related ledger journals |

| Policy gate evidence | Pass/fail label | Stored decision evidence for KYC, KYB, AML, VAT validation, and tax-form completeness, including reason codes or review notes |

Traceability is where credibility often breaks. You should be able to pick one completed vendor and one exception case, then produce the request record, approval history, payout status evidence, and journal reference without engineering reconstruction.

Apply the same standard to policy gates. Keep what was checked, what matched or failed, who reviewed it, and when the decision was made. If beneficial-owner review is part of your process, keep the identification and verification evidence tied to the legal-entity review; if EU cross-border VAT checks are required, retain the VIES outcome record from the time of review.

Treat tax forms as completeness evidence, not a box check. For W-9 or required W-8 documentation, retain both the form and the review trail showing completeness and approval for payment and reporting. A common failure mode is having a file but no evidence that anyone confirmed it was complete enough to use.

Close the loop monthly: compare projected cycle time, exception rate, and rework savings to actuals, then explain variance. More broadly, CFOs are now expected to be strategic drivers of financial and digital transformation, so traceable controls usually carry more weight than headline savings alone.

Validate the model in a pilot before full rollout#

Run a controlled pilot cohort before broad launch, and treat it as a pass/fail decision rather than a soft preview. If actual results miss the limits you defined up front, stop and fix before scaling.

| Pilot control | What to verify |

|---|---|

| Continue/no-go gates | Keep exposure small and use explicit continue/no-go gates |

| Duplicate creation | Do not scale up if duplicate creation exceeds your own threshold |

| OFAC handling | Confirm the team can document how a potential match was triaged and whether it was cleared or escalated |

| Reconciliation breaks | Do not scale up if reconciliation breaks exceed your own threshold |

| Pause authority | Define who can pause automation before processing the first record |

| Failure triage | Define who triages failures before processing the first record |

| ERP and ledger corrections | Define who posts corrections in ERP and ledger journals, and validate this with at least one failed-case drill |

Compare forecast versus actual on the few metrics that drive the decision:

| Checkpoint | Forecast in the model | What to verify in the pilot |

|---|---|---|

| Cycle time | Expected reduction from request to approval or payout readiness | Timestamped start-to-finish performance for the pilot cohort, including waits from manual review |

| Exception rate | Expected share of cases requiring human handling | Duplicates, sanctions reviews, and rework volume by reason code |

| Rework cost | Assumed labor and correction effort after failures | Actual analyst effort, correction tickets, and downstream fixes in ERP and ledger journals |

Keep exposure small and use explicit continue/no-go gates. Do not scale up if duplicate creation, OFAC handling failures, or reconciliation breaks exceed your own threshold. For OFAC handling, confirm the team can document how a potential match was triaged and whether it was cleared or escalated.

Define rollback ownership before processing the first record: who can pause automation, who triages failures, and who posts corrections in ERP and ledger journals. Validate this with at least one failed-case drill so you know corrections can be made cleanly without ad hoc spreadsheet work.

Conclusion#

The model worth backing is the one you can defend task by task. A credible vendor onboarding roi calculator is not a glossy savings number. It is a comparison between your current manual effort and an automation path that still prices in controls, exceptions, rework, and evidence.

That is why most calculator outputs are only directional until they meet live operating data. If a tool cannot show which assumptions drive the result, treat it as a scenario, not a decision. The stronger case starts with the status quo. Then it tests the upside of automation using explicit inputs like vendor volume, current process effort, labor cost, and correction work tied to downstream operations.

The practical move is small and disciplined. Pick one scenario, build the minimum viable model, run a pilot on a defined vendor cohort, and compare forecast to actual. Your checkpoint is not just faster onboarding. It is whether cycle time, exception rate, and rework cost improve without introducing new control failures that later block payment.

Post launch, verify ROI with operational evidence, not memory. Keep the baseline assumptions, time samples, approval logs, and exception reason codes, then connect them to real status signals from your payment stack where available. Payout webhooks are useful here because they show progress and status changes of transfers, but they are not enough on their own. If those events are not retained, reconciled, and tied back to the onboarding record, you still have a proof gap.

This is also where reconciliation should come back into the buying decision. If your operation uses or plans to use Virtual Accounts, remember what makes them useful: they are sub-ledger accounts linked to a physical account, each with a unique identifier. That structure can help you trace money movement and simplify reconciliation, but only if your onboarding controls, account setup, and payout evidence are connected end to end. The failure mode is common: teams optimize intake speed, then discover they cannot reliably match approvals, beneficiary setup, and payment activity later.

So the closing recommendation is simple. Choose by scenario, validate with a pilot, and only scale what you can prove in production. If you are assessing Gruv or any similar platform, ask one concrete question: how do your onboarding controls connect to Virtual Accounts, payout status evidence, and audit-ready reconciliation where those capabilities are supported? Related reading: The Ultimate Checklist for Onboarding a New Freelance Client.

Frequently Asked Questions

What inputs do I need to build a credible vendor onboarding roi calculator?

Start with annual onboarding volume, analyst effort by task, fully loaded hourly labor cost, and the share of cases that need rework. If you do not model rework, you can overstate savings, especially where missing or incorrect documents, data mismatches, duplicate records, or extra approvals are common. A good checkpoint is to sample recent onboarding files and time the actual steps instead of relying on team memory.

How should I compare manual review and automated verification without hiding exception costs?

Compare both paths at the task level: document collection, tax validation, bank verification, compliance screening, approvals, and ERP setup. Put exception handling in both models, not just the manual one, and keep a separate line for retries and analyst review on compliance and bank-check exceptions. If your automated case assumes straight-through processing for nearly every vendor, it is probably too optimistic.

Which onboarding tasks usually deliver the biggest ROI gains first?

Common early candidates are tax validation, bank verification, and compliance screening. In practice, TIN or EIN and W-9 or W-8 checks, ACH or SWIFT verification, and OFAC or sanctions screening are often measurable places to start. Keep human review for high-risk mismatches, because reversals can erase projected gains.

Why do ROI numbers differ so much across calculators like Trust Your Supplier, Ballerine, and Hyperbots?

Because ROI is not one fixed formula, and calculator scope changes the answer. Trust Your Supplier positions a supplier onboarding calculator, while Ballerine explicitly frames a merchant onboarding ROI calculator with volume, cost, and conversion rate inputs, so those outputs are not apples to apples. Hyperbots also shows example assumptions such as 5 FTEs, 1,000 vendors per year, and $60,000 salary per FTE, which alone can drive very different results.

What assumptions must finance teams validate before presenting ROI to leadership?

Finance should verify how ROI is measured, what costs are included, and what is excluded from the savings line. Check the baseline cycle-time range: supplier onboarding examples can vary widely from about 1 day to 40+ days. Also confirm labor rates, exception frequency, and who owns correction work in downstream systems. If the calculator output does not show the underlying assumptions, treat it as a scenario, not a business case.

How do I prove post launch ROI with audit ready evidence instead of one time projections?

Use the same measures from the model after launch: cycle time, exception rate, and rework cost, with monthly forecast-versus-actual tracking. Keep an evidence pack with baseline assumptions plus task-level time logs, exception reason codes, and review or escalation records for compliance checks. Watch for one failure mode in particular: a savings claim that cannot be tied back to actual onboarding events and corrections.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- fdic.gov/news/financial-institution-letters/2023/fil2...trusted

- federalregister.gov/documents/2023/06/09/2023-12340/interagency-...trusted

- federalreserve.gov/paymentsystems/fedach_about.htmtrusted

- guides.gaoinnovations.gov/greenbook/2025/principle-10-design-control-a...trusted

- irs.gov/forms-pubs/about-form-w-9trusted

- irs.gov/newsroom/how-to-report-foreign-bank-and-fina...trusted

- occ.gov/news-issuances/bulletins/2023/bulletin-2023-...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

AP Automation ROI Calculator: How to Build the Business Case for Your Finance Team

If you need a CFO-ready case for AP automation, start with transparent math and explicit assumptions. A defensible model is more useful than a bigger headline ROI claim.

Vendor Onboarding Automation: How to Collect Bank Details Tax Forms and Compliance Docs at Scale

**Vendor onboarding automation for bank details, tax forms, and compliance documents works best when the control points are explicit.** If you cannot define what must be collected, what gets validated, what triggers manual review, and what blocks payout, automation can scale bad decisions faster.

How to Write an Engagement Letter for a Bookkeeping Client

Your engagement letter is not a formality. Treating it as the last administrative step before the real work starts is a mistake. A generic template does more than leave gaps. It weakens your authority, blurs expectations, and exposes your business to avoidable risk.