Quick Answer

Use a three-path decision table: full cash refund, prorated refund, or travel credit. In covered air cases, route by DOT first, including the June 25, 2024 rule and its timing standards of 7 business days for card payments and 20 calendar days for other payment forms. For pass renewals, keep consent, notice, and cancellation cutoff timestamps tied to the charge reference. Then post the final disposition to journal records so support, finance, and audit review the same evidence.

What Travel and Hospitality Membership Billing Needs to Handle#

If you run a pass or membership program, the hard part is not the charge. It is what happens after the sale. The pressure shows up later: when someone wants to cancel before renewal, asks for a refund, or accepts a credit that does not get redeemed cleanly. In travel and hospitality, those post-purchase events can make reconciliation unmanageable fast if support, finance, and billing are not working from the same record.

- Post-charge decisions create the real operating risk.

A membership or pass program can look clean at checkout. It gets messy later, when one customer wants to cancel before renewal, another qualifies for a refund, and a third gets a credit that never gets redeemed or cleared correctly. That is why this guide focuses less on billing setup and more on the operating model behind each decision. You need one path from customer event to ledger journal posting, or support, finance, and audit will each end up with a different version of the truth.

- Some outcomes are policy choices, but some are not.

A workable model starts by separating business preference from legal obligation. DOT refund regulations are a useful anchor. Under the final rule effective June 25, 2024, automatic refunds are required in certain cancellation or significant-change cases, and refund timing is not open-ended: within 7 business days for credit card payments and within 20 calendar days for other forms of payment. For DOT-covered flight cases, carriers and ticket agents must also inform consumers of their right to a refund before offering credits or vouchers instead. Your billing design should recognize when credit is acceptable and when refund is the only defensible outcome.

- Auto-renewal only works if cancellation evidence is tight.

Public pass programs make the renewal edge cases easy to see. FlexPay examples are useful not because they represent every program, but because they show what you may have to prove later. Universal Studios Hollywood states that auto-renewal begins at the end of the initial 12-month term on a month-to-month basis, and Universal Orlando states a pass will renew month-to-month until canceled, with cancellation requests required 72 hours before the monthly renewal date. The important point is not the renewal rule itself. It is whether you can verify the consent record, the cutoff window, and the exact cancellation timestamp when a dispute lands.

That is the frame for the rest of this article. We are comparing operating models that keep ledger truth intact, reduce auto-renewal disputes, and prevent unresolved credits from lingering as open liability without forcing support teams to improvise case by case.

Selection Criteria That Separate Reliable Billing Systems From Fragile Ones#

Judge a billing model by post-purchase control, not checkout smoothness. If your team cannot explain a disputed transaction from customer request to final journal posting, treat that as a stop signal before you add volume.

| Criterion | What to check |

|---|---|

| Cancellation clarity | Who requested cancellation, when it was received, which cutoff applied, and which terms controlled the outcome |

| Cash refund legality handling | Whether DOT-covered flight scenarios that require automatic refunds are routed away from credit-first handling |

| Travel credit liability aging | Issue date, expiry, redemption status, and reversals |

| Auto-renewal control | Consent evidence, renewal-date logic, cancellation cutoffs, and which terms version was accepted |

| Exception throughput | Whether exceptions are routed by reason code with clear SLA ownership rather than falling into general support queues |

| Close-time effort | Whether the reconciliation pack ties refunds, credits, renewals, and reversals to journal exports without spreadsheet stitching |

This section is for teams that own close, reconciliation, and policy execution across products, not for consumer travel hacks. In travel and hospitality, revenue recognition is often directly linked to billing systems, so post-purchase gaps become finance and audit problems quickly.

- Cancellation clarity

Keep a clear event trail for who requested cancellation, when it was received, which cutoff applied, and which terms controlled the outcome. If support notes, billing events, and renewal jobs conflict, disputes become judgment calls instead of evidence-based decisions.

- Cash refund legality handling

Separate policy preference from legal obligation. In DOT-covered flight scenarios, the rule effective June 25, 2024 requires automatic refunds when a covered carrier cancels or significantly changes travel and the consumer is not offered or rejects alternatives, with timing of 7 business days for credit card payments and 20 calendar days for other forms of payment. If your flow cannot reliably route those cases away from credit-first handling, it is fragile.

- Travel credit liability aging

Credits support liquidity only when liability aging is visible and reconcilable. Track issue date, expiry, redemption status, and reversals so balances clear in monthly close instead of drifting into unresolved liability.

- Auto-renewal control

Recurring charges are not enough. You need consent evidence, renewal-date logic, cancellation cutoffs, and proof of which terms version was accepted, or renewal disputes escalate into refund disputes.

- Exception throughput

Stress shows up during bulk cancellations and provider reversals, where manual reconciliation can become unmanageable. Automated billing helps only when exceptions are routed by reason code with clear SLA ownership rather than falling into general support queues.

- Close-time effort

Include close readiness in your selection, because hospitality teams must collect, analyze, and report high volumes of financial data. The practical test is whether your reconciliation pack ties refunds, credits, renewals, and reversals to journal exports without spreadsheet stitching.

Compare options using the same evidence pack: a policy matrix, an event/state map, a monthly reconciliation pack, and an exception SLA dashboard tied to journal exports.

| Model | Best for | Key pros | Key cons | Required controls | Failure blast radius |

|---|---|---|---|---|---|

| Manual policy plus support decisions | Low volume or temporary programs | Fast to launch, flexible edge-case handling | Agent variance, weak audit trail, slow close | Written policy matrix, case timestamp capture, monthly manual reconciliation pack | High. One dispute can spread across support, finance, and chargebacks |

| Automated billing but finance-decoupled | Teams optimizing checkout first | Less manual intervention, better recurring billing execution | Credits and refunds drift from accounting truth | Event/state map, exception queue, journal export matching | Medium to high. Operations scale, but close and audits stay painful |

| Control-coupled billing with journal-first reconciliation | Teams scaling passes, credits, and refunds across products | Stronger legality handling, cleaner close, better evidence | More setup and governance work | Policy matrix, SLA dashboard, ledger-linked reconciliation, periodic audit review | Lower. Errors are easier to isolate, prove, and correct |

Option 1: Fixed-Term Pass Billing With Explicit Renewal Consent#

Use this model when you sell Annual Pass or Seasonal Pass products with defined validity windows and blockout dates, and you need renewal outcomes to be easy to prove. The core control is to track purchase, activation, renewal notice, consent, and cancellation as separate events.

- Best for: pass programs tied to calendar access rules where term validity and blockout handling must be explicit.

- Pros: clearer term boundaries and a stronger dispute trail when renewal consent and notice records are complete.

- Cons: higher renewal drop-off risk and more lifecycle messaging work than simpler recurring defaults.

- Concrete use-case: a FlexPay-style setup with an initial down payment and the remaining balance spread over 11 months, while keeping purchase date and activation date separate.

In this pattern, the pass can be valid from purchase but not active until first use, so the purchase-to-activation gap is a real lifecycle state, not noise. If your system collapses those states, support and finance will struggle to explain timing disputes.

If you run auto-renew, store explicit consent and notice evidence. For terms of one year or longer in California, reminder timing is 15 to 45 days before renewal. If you enforce a cutoff, store that too; one operational example is a cancellation request at least 72 hours before renewal.

| Policy sentence | System event to store |

|---|---|

| "Pass remains valid through expiry date; blockout dates apply." | pass_term_created, expiry_date_set, blockout_calendar_attached |

| "Pass is valid from purchase date but activates on first entry." | purchase_captured, entitlement_created, activation_on_first_use |

| "Auto-renew continues until canceled by the contract holder." | consent_captured, renewal_notice_sent, cancel_request_received, renewal_executed_or_stopped |

Before scaling, test accounts where purchase and activation dates differ, then confirm support notes, billing events, and journal output align to the same timestamps. If you cannot prove who consented, when notice was sent, and whether cancellation arrived before cutoff, renewal disputes will default to manual refund judgment.

Related: Non-Profit Membership Billing: How to Manage Recurring Donations and Member Tiers.

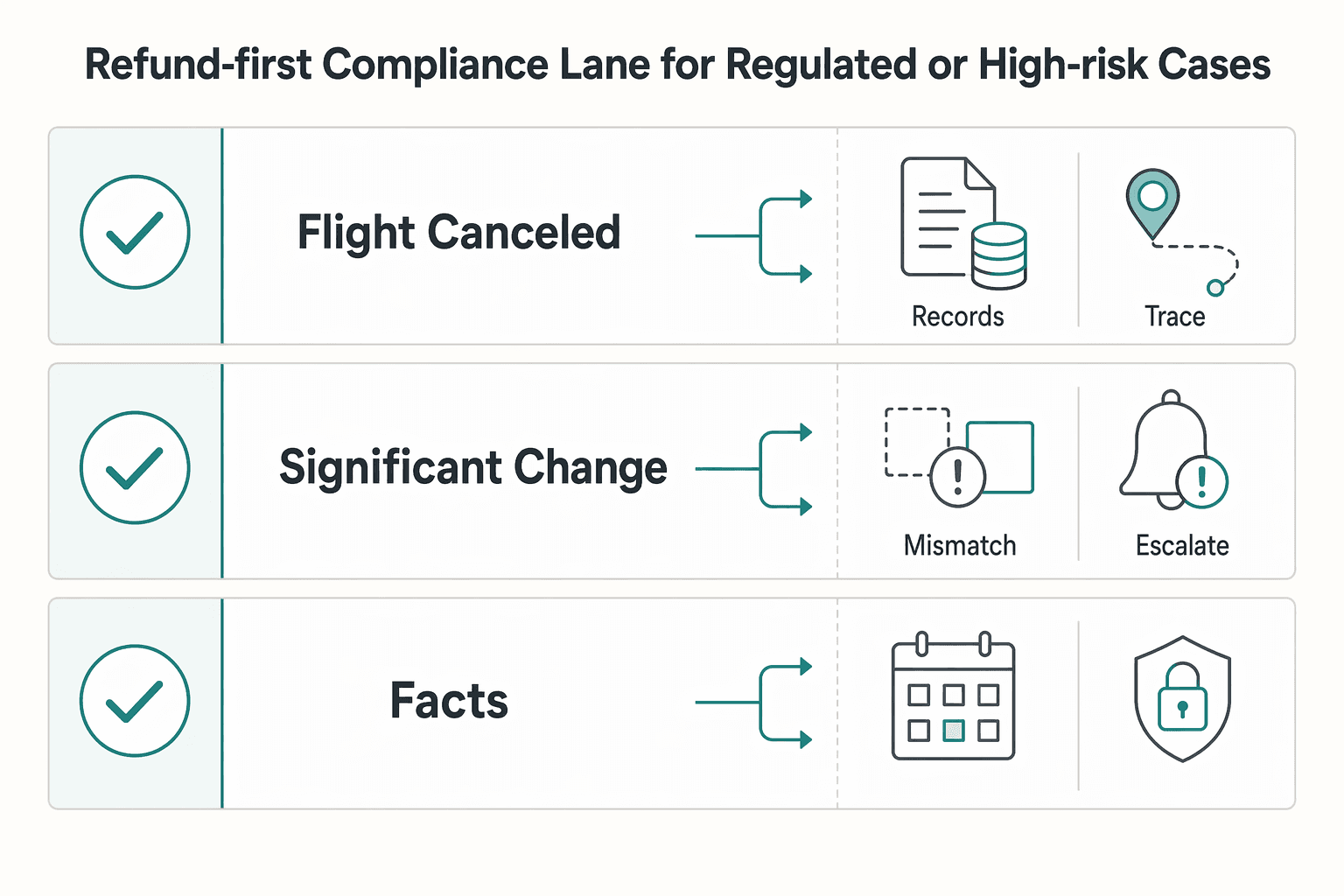

Option 2: Refund-First Compliance Lane for Regulated or High-Risk Cases#

Use this lane when cancellation scenarios can create a legal refund entitlement. For clear covered cases, the safest default is cash refund first. It is most useful in air-travel-adjacent operations where DOT refund regulations can apply, and where forced cancellations often become complaints, chargebacks, or escalations.

- Best for: teams handling frequent forced cancellations with potential regulatory exposure.

- Pros: fewer judgment calls when a cash refund is clearly owed; lower escalation risk.

- Cons: immediate cash-flow impact and heavier refund operations load during disruptions.

Run the lane by separating clear triggers from ambiguous ones. DOT consumer guidance states a traveler is entitled to a refund when the airline cancels a flight, and gives a significant-delay reference point of 3 hours or more for domestic itineraries and 6 hours or more for international itineraries. DOT's 2024 final rule requires automatic refunds for covered canceled or significantly changed flights, and if a passenger rejects rebooking, a voucher, or credit, the refund path remains cash.

| Trigger | Route | Evidence to store |

|---|---|---|

| Flight canceled in a covered air case | Full cash refund | cancellation event, customer notification, payment method, refund journal link |

| Significant change and traveler rejects rebooking, voucher, or credit | Full cash refund | change timestamp, rejection record, agent or self-serve action log |

| Facts unclear or policy scope disputed | Hold for policy review | timestamped decision notes, policy version, escalation owner |

For execution, track the prompt-refund timing standards: 7 business days for credit card payments and 20 calendar days for other forms of payment. In covered scenarios where full fare must be refunded, include taxes and ancillary fees, not only the base charge.

Assign one accountable owner and link every disposition to ledger journal records. Because the Merchant of Record (MoR) is the entity legally responsible for payment processing, including refunds and chargebacks, MoR ownership plus shared journal IDs gives support, finance, and audit one trail to verify.

Before scaling, test one end-to-end case from trigger to settlement and confirm status, amount, and payment method match across customer history, processor output, and journals. Red flag: if agents can still issue credits after a covered cash-refund trigger fires, you have a policy contradiction that will surface in disputes and close.

For a step-by-step walkthrough, see Subscription Billing Platforms for Plans, Add-Ons, Coupons, and Dunning.

Option 3: Credit-First Liability Control for Recoverable Demand#

Use credit first only after you exclude cases with a cash-refund right. This lane fits brands with real repeat intent and clear terms. The upside is near-term liquidity. The failure mode is slower and more expensive: confusion that can sit in liability for months.

That handoff from the refund-first lane matters. If your facts look like a covered air disruption and the traveler rejects rebooking, voucher, or credit, DOT refund rights can still point back to cash. The significant delay reference point remains 3 hours or more for domestic itineraries and 6 hours or more for international itineraries. Your credit offer needs a legal override, not just a customer service script.

Where credit-first earns its keep#

A travel credit is a future-use value instrument, not cash. It works best when customers are likely to return and when the product family is stable enough that stored value can be redeemed without argument. If you run passes, attractions, or bundled inventory, that usually means your terms have to be precise before issuance, not clarified later in a support thread.

The judgment call is simple: use your own redemption history to estimate unexercised-rights (breakage) risk before you default to credit. That does not mean credit is wrong. It means long-tail liabilities and disputes can cost more than expected when customers are unlikely to redeem.

The metadata that makes credits defensible#

Do not issue a generic balance. Attach hard fields to every credit object so support, finance, and the customer all see the same rights.

| Field | Why it matters | Example of what to store |

|---|---|---|

| Expiry | Value can be lost if not used in time | explicit expiration timestamp; public-term reference; example policies range from travel beginning within 1 year from original ticket date to 5 years in qualifying delay or cancellation cases |

| Transfer rule | Some products are locked to the original traveler or account | named passenger or account ID; non-transferable flag |

| Redemption scope | Credits may work only in certain channels or for certain charges | airfare only; bags online only; no cash-out |

| Eligible inventory | Pass and attraction products can exclude specific inventory | explicit included/excluded park or product IDs per pass type |

Universal Orlando Resort is a good example of why inventory flags matter. Public pass entitlements differ by park bundle, including combinations across Universal Studios Florida, Universal Islands of Adventure, and Universal Volcano Bay, so your credit or refund logic cannot assume one park equals another.

Use this checkpoint before you scale the program: redeem one test credit end to end and confirm the customer balance, booking entitlement, and liability journal all match after partial use, full use, and expiry. Red flag: agent-created credits without expiry, transferability, or inventory eligibility fields. Those are the records that turn into breakage disputes, manual workarounds, and month-end balances nobody trusts.

Keep an evidence pack with the policy version shown at issuance, customer acceptance, credit ID, expiry timestamp, scope flags, and every redemption event tied back to the same journal trail.

Option 4: Hybrid Decision Matrix That Switches Between Refund, Prorated Refund, and Credit#

Use a hybrid decision table when the same operation needs consistent outcomes across passes, hotels, and add-ons. Each row should map a defined fact pattern to one of three outputs only: full cash refund, prorated refund, or travel credit.

This is most useful when products share a brand but not the same legal or policy basis. In air-linked cases, DOT refund rules can require cash refunds in covered cancellation or significant-change scenarios. For pass products like an Annual Pass or Seasonal Pass, your published policy usually determines whether the outcome is full refund, prorated refund, or credit.

Publishable routing matrix#

A decision table is a row-based rule format: each row sets conditions and one outcome. If a case does not match a row, route it to exception approval instead of ad hoc handling.

| Trigger type | Product type | Usage status | Legal or policy basis | Output |

|---|---|---|---|---|

| Carrier cancellation, or significant change of 3 hours or more domestic / 6 hours or more international, and customer declines credit | Air-linked booking | Any | DOT refund regulations | Full cash refund |

| Involuntary downgrade | Air-linked booking | Used in downgraded class | DOT refund regulations requiring fare difference back | Prorated refund |

| Carrier cancellation or significant change, and customer affirmatively accepts a voucher or credit | Air-linked booking | Any | Credit allowed only with affirmative acceptance under 14 CFR part 260 | Travel credit |

| Operator cannot deliver contracted access and pass has not been used | Annual Pass | Unused | Your published pass policy | Full cash refund |

| Access reduced after partial use and policy allows partial recovery | Annual Pass or Seasonal Pass | Partially used | Your published pass policy | Prorated refund |

| Recoverable future demand, terms shown before issuance, and customer accepts non-cash value | Hotel stay, attraction add-on, or bundled amenity | Unused or rebookable | Your credit policy and acceptance record | Travel credit |

Keep outputs capped at those three. Do not hide extra paths like "goodwill" or "manager discretion" inside routine handling.

Governance that keeps it honest#

The hard part is preventing drift after launch. Decision tables help you spot overlap and gap defects, so run that check before policy releases. If multiple rows can match, set an explicit hit policy; if no row matches, fail closed to exception review.

For air-linked rows, anchor to the applicable DOT framework. As reflected in the June 25, 2024 final rule timeline, covered automatic refunds have processing timing expectations of 7 business days for credit card payments and 20 calendar days for other payment forms. Credit or voucher outcomes should require affirmative customer acceptance.

Before rollout, replay real cases through the table and confirm support disposition, customer notice, and journal outcome all align. For refund rows, verify timing controls trigger once refund entitlement is clear. For credit rows, verify acceptance record, credit ID, scope flags, and expiry terms captured at issuance.

Option 5: Month-End Reconciliation Design That Survives Scale#

At scale, close is more reliable when the ledger journal is the source of truth and wallet views are treated as projections. Refunds, credits, reversals, and disputes can post out of order, so month-end should confirm journal-backed evidence, not reconstruct history from UI balances.

After you decide whether a case is a refund, prorated refund, or credit, your close process still has to prove where value moved, when it moved, and whether processor and payout records align.

Make the journal the anchor#

Anchor every money or liability movement to journal lines first, then reconcile outward. Charges, completed refunds, credit issuance, and credit expiry should each have explicit posting logic and traceable references to the originating billing event and the settlement or payout record.

| Movement | Journal requirement | Reference |

|---|---|---|

| Charge | Explicit posting logic with a traceable reference to the originating billing event | Settlement or payout record |

| Completed refund | Explicit posting logic with a traceable reference to the originating billing event | Settlement or payout record |

| Credit issuance | Explicit posting logic with a traceable reference to the originating billing event | Settlement or payout record |

| Credit expiry | Explicit posting logic with a traceable reference to the originating billing event | Settlement or payout record |

| Processed payment funds | Reconcile funds to accounts in your balance platform | Virtual Accounts settlement reference or the equivalent payout-rail reference |

Include webhook ingestion in close controls because payment state changes are asynchronous, including disputes. If async events are missing from close, month-end becomes a cleanup exercise instead of reconciliation.

On the cash side, reconcile processed payment funds to accounts in your balance platform. If you use Virtual Accounts, store that settlement reference on the same journal records used for close; if not, use the equivalent payout-rail reference. The goal is one auditable chain from customer event to journal to external money-movement evidence.

Use a daily cadence by default. Reconciliation reporting can run on schedule or on demand, and daily runs make month-end a roll-forward plus exception review.

Use a practical bucket view#

A four-bucket view is a useful operating pattern for membership and pass products, but your labels can vary as long as the evidence standard stays consistent.

| Bucket | What it includes | Evidence that should match | Common break |

|---|---|---|---|

| Billed | Successful charges | Journal posting plus processor settlement reference | Charge captured but journal missing or delayed |

| Refunded | Refunds that completed, including async confirmations | Reversal journal plus return or payout reference | Ticket marked refunded while processor status is still pending |

| Credited | Non-cash value issued | Liability journal plus credit ID and issuance terms | Wallet value created without matching liability entry |

| Expired | Credits that reached stated expiry | Liability release journal plus cohort or policy record | Credit shows expired in UI while liability remains open |

Check these controls before close:

- Unmatched events: billing, refund, and credit events should map to journal lines; money-moving events should also map to settlement or payout references.

- Duplicate retries: mutation retries should use idempotency keys so duplicate operations are detectable and controllable.

- Stale status transitions: one system shows "refunded" or "expired" while processor events or journals do not reflect that state.

- Liability aging by cohort: group credits by issue period, product, or policy cohort so older balances are explainable.

In most scaled setups, close from journals first and then investigate projection drift in wallet surfaces. For lodging operators, keep reporting mappings aligned with USALI where relevant so operational close and external reporting stay consistent.

Exception Controls Most Teams Miss Until an Audit or Outage#

After you anchor close on journal entries, most breakage comes from exception-control gaps, so treat these controls as mandatory before scale.

| Exception area | Required evidence or gate | Article note |

|---|---|---|

| Retry and timing conflicts | Original charge reference, final cancellation timestamp, and related journal IDs before posting a second refund or a credit-expiry release | If those records conflict, freeze the case as unresolved |

| Payout release | Required verification complete and disputed reversal exposure cleared | KYC is required before connected accounts can accept payments and send payouts; onboarding commonly includes KYC and KYB |

| High-risk escalation | Policy version, customer consent snapshot, event timeline, ledger journal IDs, and support actions | Use one review bundle |

| Tax and reporting consistency | Verify downstream records after refund and credit changes before close | Form W-9 for U.S. TIN collection, Form W-8BEN when requested by a payer or withholding agent, Form 1099-K for card and third-party network payments, and the FBAR trigger when aggregate balances exceed $10,000 at any point in the calendar year |

- Route retry and timing conflicts to manual review

Send duplicate refund retries, conflicting auto-renewal cancellation timestamps, delayed provider reversals, and expired travel-credit edge cases to an exception queue instead of auto-resolving them. Require the original charge reference, the final cancellation timestamp, and related journal IDs before posting a second refund or a credit-expiry release. If those records conflict, freeze the case as unresolved.

- Gate payout release on verification and dispute exposure

If funds can be released to connected accounts, hold payouts until required verification is complete and disputed reversal exposure is cleared. KYC is required before connected accounts can accept payments and send payouts, and onboarding commonly includes both KYC and KYB procedures. If your provider or jurisdiction also requires AML checks, keep them in the same gate and expect requirements to change over time.

- Standardize the escalation evidence pack

For high-risk cases, require one review bundle: policy version, customer consent snapshot, event timeline, ledger journal IDs, and support actions. This keeps triage fast when support, finance, and payments show different statuses by proving who acted, in what order, under which policy text.

- Run a tax and reporting consistency check after refund/credit changes

Refunds and credits can change settled flows, so verify downstream records before close. Keep payer data aligned with Form W-9 for U.S. TIN collection and Form W-8BEN when requested by a payer or withholding agent. For card and third-party network payments, use Form 1099-K (not 1099-MISC or 1099-NEC), and if foreign financial accounts are in scope, remember the FBAR trigger begins when aggregate balances exceed $10,000 at any point in the calendar year.

Conclusion#

The durable answer is not refunds versus credits. It is an internal-control approach that produces the right outcome consistently, supports reliable reporting, and leaves enough evidence that an external reviewer can see what happened without guessing.

-

Choose the model by risk exposure, not team preference. If your product mix includes regulated travel scenarios, forced cancellations, or high complaint risk, lean toward the refund-first lane from the options above. DOT's 2024 rule matters when it applies: if a consumer is entitled to a refund, they must be informed of that right before you offer a credit or voucher, and the timing clock is concrete at 7 business days for credit card payments and 20 calendar days for other forms of payment. If repeat use is genuinely likely and your written terms are clear, a credit-led path can still work, but only when you can defend expiry, scope, and redemption rules from the policy text.

-

Treat reconciliation as the real scale test. Reconciliation is not a back-office cleanup step. It is the control that checks accuracy, completeness, and validity by comparing records and resolving discrepancies. In ledger-based workflows, a practical close pattern is to anchor on journal records, then use customer-facing balances, wallets, and support views as projections that tie back to journal lines and settlement references. The checkpoint is simple and strict: for any disputed membership charge, you should be able to trace the policy trigger, customer action, decision outcome, payment movement, and final journal posting in one chain. One failure mode is a case that looks closed in the UI but still has an open liability because a duplicate refund retry, stale status transition, or missing reversal never reached the books.

-

Build the exception evidence pack before volume exposes the gaps. The minimum pack should include the governing policy version, consent or cancellation timestamps, event timeline, disposition reason, settlement reference, and journal IDs. If the case involved an annual or installment-style renewal, keep the exact renewal terms shown and the disable or cancel timestamp tied to the charge reference. The differentiator here is proof, not speed: completion should be clear to an external reviewer. If your team can explain a disputed transaction end to end, from policy trigger to final journal entry, you have a much stronger billing foundation than a platform that only knows the customer-facing outcome.

For related reading, see The Best Business Travel Insurance for Digital Nomads and Executives.

Frequently Asked Questions

What is the operational difference between a cash refund and a travel credit?

A cash refund returns money to the original payment flow. A travel credit keeps value available for later use under your written product terms. The key difference is immediate return of funds versus retained value under policy.

When should a platform force a refund instead of offering credit?

If the case falls under a legal refund entitlement, refund first. In the air-travel context, DOT requires automatic refunds when a carrier cancels or makes a significant change and the traveler rejects alternatives, and consumers must be told about that refund right before credits or vouchers are offered. For covered cases, timing matters too: 7 business days for credit card payments and 20 calendar days for other payment forms under the 2024 rule.

How should auto-renewal for an Annual Pass be billed and canceled to avoid disputes?

Treat consent and cutoff evidence as part of the billing record, not just a UX event. In one documented Annual Pass example, Universal Studios Hollywood says auto-renewal is standard for new FlexPay contracts and the customer must disable it at least 24 hours before the renewal date. Your verification checkpoint is simple: keep the renewal terms shown, the consent timestamp, and the exact cancel or disable timestamp tied to the charge reference.

When is a prorated refund the right middle ground?

There is no universal proration rule. Use proration only when your written policy allows it and a full refund is not legally required. If you prorate, store the policy version and calculation basis used for that case.

What controls prevent expired or orphaned credits from distorting liabilities?

Start with policy version control, because credit treatment should follow written program terms. Public terms can explicitly state that participation is governed by written terms and conditions and that changes must be made in writing. Use that written record to decide whether value expires, remains open, or is otherwise handled.

Which monthly checkpoints prove that credits and refunds are fully reconciled?

There is no single checkpoint set that applies to every platform. Use your documented reconciliation process to verify refunded, credited, redeemed, and still-open balances tie back to journal entries and settlement references, and treat unexplained exceptions as unresolved.

How should teams handle unknowns when community anecdotes conflict with written policy?

Published terms win. Public program terms can explicitly say participation is governed by written terms and conditions and cannot be changed except in writing, so forum posts should never override your case decision. If the customer may raise a card billing error, preserve the written record early because Regulation Z ties billing-error notices to a 60 day window from the first statement showing the alleged error.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- ecfr.gov/current/title-14/chapter-II/subchapter-A/par...trusted

- federalregister.gov/documents/2024/04/26/2024-07177/refunds-and-...trusted

- federalregister.gov/documents/2024/08/12/2024-17602/refunds-and-...trusted

- finance.cornell.edu/controller/internalcontrols/unitlevelactivit...trusted

- gao.gov/greenbooktrusted

- irs.gov/forms-pubs/about-form-w-9trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

- law.cornell.edu/cfr/text/12/1026.13trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Health and Wellness Platform Billing: How to Manage Memberships Trials and Insurance Integrations

A common rollout mistake is treating `membership billing`, `insurer billing`, and `employer-sponsored benefits` as one workflow. They are not. Membership billing is automatic, recurring billing after someone subscribes. Insurer billing runs through claims, with payment moving through payer channels. Employer-sponsored benefits are different again, because coverage or reimbursements are funded through employer-backed structures such as a group health plan or an individual coverage HRA (ICHRA).

Non-Profit Membership Billing for Recurring Donations and Member Tiers

Billing usually breaks before volume looks dangerous. The real problem is that membership programs often grow faster than their controls, so tiers, recurring donations, and membership dues start following different rules depending on who last touched the record. What you want is simpler than most billing documentation suggests: charges, renewals, and exceptions should be traceable and handled consistently, with ownership finance can explain without guesswork.

Subscription Billing for SaaS Teams Handling Trials and Plan Changes

Treat subscription changes as an operating decision first, not a pricing page edit. The moment a customer upgrades mid-cycle, adds services, or switches to annual prepay, you are coordinating product access, invoicing, and accounting at the same time.