Quick Answer

Define one cross-functional event policy before implementation, then enforce it for trials, upgrades, downgrades, and annual prepay in the same sequence every time. For subscription billing saas trials upgrades downgrades annual prepay, the practical pattern is: approve policy, execute change, generate invoice outcome, update entitlements, and reconcile accounting evidence. Treat annual prepay as deferred revenue recognized across the service term, and require idempotent webhook replay tests so retries do not produce duplicate financial effects.

Where Trials and Plan Changes Complicate Billing#

Start with one shared event model#

Treat subscription changes as an operating decision first, not a pricing page edit. The moment a customer upgrades mid-cycle, adds services, or switches to annual prepay, you are coordinating product access, invoicing, and accounting at the same time.

That coordination gets fragile as you scale. Mid-contract upgrades and add-ons create real billing complexity, and manual handling is not just slow; it is error-prone and can hurt customer relationships. A common failure mode is simple: teams update access, billing, and accounting on different timelines, so the records stop matching. You end up with access and invoices out of sync, plus month-end cleanup that should not have existed.

Use this checkpoint before you do anything else. Ask product, finance, and engineering to answer the same four questions for one change event, such as a mid-cycle upgrade. When does the contract state change? When does the invoice change? When does access change? What is the accounting impact? If you get three different answers, you do not have a tooling problem yet. You have a policy problem.

The goal is not to force identical treatment. The goal is to make sure each team is making decisions against the same rules before exceptions pile up.

That shared model matters most where billing and accounting diverge. Revenue recognition means recording revenue when it is earned, not when cash is collected. Annual prepay makes that gap especially visible. Cash receipt and recognized revenue are not the same thing, and ASC 606 gives one model for handling that complexity. If your team talks only about charges and collections, but not contract modification or earned revenue, you are pushing reconciliation work into the close.

The practical recommendation is straightforward: define each change type as a business event with customer-facing, invoice, and accounting consequences. Do not let support, sales, or engineering invent those consequences case by case.

Write the policy before implementation#

Write the policy before you pick implementation details. Billing platform fit depends on your use case, so there is no universal stack pattern to copy. What you can standardize now is the rulebook: what counts as an upgrade, when proration applies, how annual prepay is treated, and which event becomes the source of truth for entitlements.

Once those rules are clear, you can map them into billing automation and your API layer with fewer surprises. A useful verification step is to check whether your stack can represent contract modifications and proration without falling back to manual adjustments. If it cannot, treat that as an early red flag, not an annoyance to absorb later.

The sections that follow help you lock the rules first, then implement them in a way finance can close and engineering can trust.

For a step-by-step walkthrough, see Building Subscription Revenue on a Marketplace Without Billing Gaps.

Decide billing policies before touching code#

Policy ownership must be explicit before implementation, or billing, access, and accounting will drift. Use a clear split: product owns feature-gating intent, finance owns revenue recognition and MRR policy, and engineering owns webhook handlers and system guarantees.

Assign policy owners before you build#

Write and approve policy for four cases before any build starts: mid-cycle upgrades, plan downgrades, proration, and annual prepay. For each case, define when the change is effective, what appears on the invoice, when access changes, and when finance treats it as a contract-modification review item.

Run one upgrade and one downgrade scenario across product, finance, and engineering. If answers differ, pause and resolve policy first, because inconsistent judgment leads to late adjustments, audit notes, and restatements.

Choose the source of truth for contract and invoice state#

Set one source of truth for contract state and one for invoice state, and document both. Do not let CRM-billing sync and app entitlements resolve conflicts independently.

Test this with replay: run one change event and confirm that contract state, invoice state, and entitlements always converge to the same final status.

Decide the audit trail before launch#

Define the audit trail before launch, especially for ASC 606. Keep a record of the approved policy, effective timestamp, pre- and post-plan state, related invoice or credit record, and the reason for contract-modification treatment.

Be explicit on annual prepay: cash collected upfront is deferred revenue on day one, then recognized over the 12-month service term. If that chain is not traceable, close work shifts to manual fixes.

You might also find this useful: Subscription Billing Platforms for Plans, Add-Ons, Coupons, and Dunning.

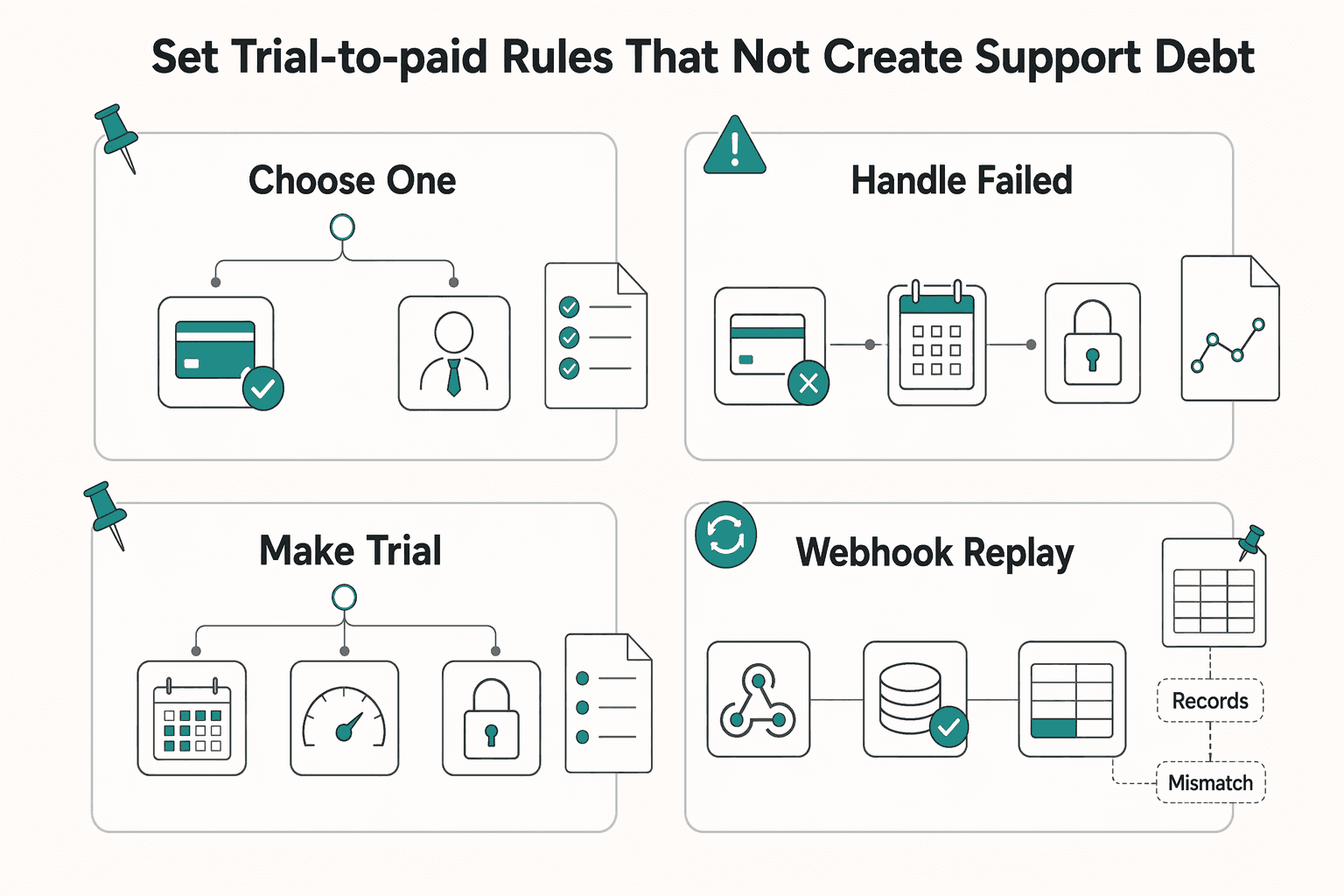

Set trial-to-paid rules that do not create support debt#

Set trial-to-paid rules before launch so conversion outcomes are predictable for customers, support, and finance.

| Order | Step | Sequence note |

|---|---|---|

| 1 | Payment retry | Run first |

| 2 | Customer notice | Run after payment retry |

| 3 | Grace behavior for feature gating | Run after customer notice |

| 4 | Downgrade or suspension | Run after grace behavior for feature gating |

- Choose one conversion path per segment, and define overrides clearly.

Use explicit segment rules for self-serve card capture versus sales-assisted activation, and document who can override trial expiration and where that decision is recorded.

- Handle failed conversion in a fixed order.

Run the same sequence every time: payment retry, customer notice, grace behavior for feature gating, then downgrade or suspension. Repeated payment failures can signal de-prioritization or financial stress, so treat this path as both a recovery flow and an early-risk signal. If you bill through Google Play, handle SUBSCRIPTION_STATE_PENDING before activation.

- Make trial-end billing explicit for monthly vs. annual prepay.

Define which invoice is created at conversion for each plan path so first invoices are unambiguous. For annual prepay, treat collected cash as deferred revenue on day one and recognize it across the 12-month term.

- Verify conversion behavior with idempotent webhook tests.

Test successful conversion, failed conversion, and duplicate webhook delivery through your handlers. You should see one consistent subscription, invoice, and entitlement outcome even when an event is delivered more than once.

Related reading: How to Handle Multi-Currency Pricing for Your SaaS Product.

Choose upgrade and downgrade timing with explicit tradeoffs#

After activation, change timing policies are a common source of billing disputes. Set one default timing rule for upgrades and one for downgrades, and treat exceptions as explicit policy decisions.

Step 1. Pick default timing by risk, not by ticket-by-ticket requests#

For downgrades, choose between two valid defaults and document the tradeoff. Immediate downgrade aligns access and price on the same date, but can increase mid-cycle product friction. End-of-period downgrade preserves continuity through the paid term, but cost relief waits until renewal.

For upgrades, use a clear if/then rule. If overage risk is high, apply the upgrade mid-cycle with proration so billing starts when added access starts; in Stripe, proration_behavior=always_invoice charges now. If contractual commitments or sales terms require a clean boundary, schedule the change at the next bill date or renewal; Stripe subscription schedules and Recurly effective-date options support this timing model.

Use this as a decision aid, not a universal scorecard.

| Policy choice | Customer fairness | Finance close impact | Support volume | Implementation complexity |

|---|---|---|---|---|

| Immediate plan downgrade | Access and charge change together; feature loss can feel abrupt | Fewer future-dated changes; prorated adjustments may need review | More access-loss questions when gating changes immediately | Medium |

| End-of-period downgrade via subscription schedule | Customer keeps current access through paid term | Cleaner renewal boundary; scheduled changes must be tracked | More "when does this take effect?" questions if UI is unclear | Medium to high |

| Immediate mid-cycle upgrade with proration | Customer pays when added value starts | More off-cycle invoices during the month | Lower when preview is clear; higher when charges appear without warning | Medium |

If one segment gets different timing outcomes based on who handled the request, your policy has turned into negotiation.

Step 2. Make base-plan changes and add-ons deterministic#

Define add-on interaction rules before launch so contract changes are consistent. Recurly treats plan, quantity, price, and included add-ons as subscription changes, and under IFRS 15, approved scope/price changes are contract modifications.

| Scenario | Setup | Expected result |

|---|---|---|

| Base-plan upgrade only | Subscription has a base plan plus one add-on | One approved contract-change record, one subscription state outcome, and one invoice or preview outcome at the same timestamp |

| Add-on change only | Subscription has a base plan plus one add-on | One approved contract-change record, one subscription state outcome, and one invoice or preview outcome at the same timestamp |

| Both together | Subscription has a base plan plus one add-on | One approved contract-change record, one subscription state outcome, and one invoice or preview outcome at the same timestamp |

At minimum, define:

- whether add-ons inherit the base-plan effective date or keep their own date

- whether a base-plan downgrade removes incompatible add-ons immediately or leaves them until renewal

- whether the change uses immediate proration, deferred proration, or no proration

Validate this with three test cases on a subscription that has a base plan plus one add-on: base-plan upgrade only, add-on change only, and both together. Expected outcome: one approved contract-change record, one subscription state outcome, and one invoice or preview outcome at the same timestamp.

Step 3. Show the bill before the customer confirms#

In self-serve flows, show billing impact before confirmation. Generate the preview from the exact subscription update or subscription-schedule update, then display the effective date, new recurring amount, any proration amount, and whether billing happens now or at renewal.

Be explicit about proration behavior in the confirmation UI. create_prorations creates adjustments without automatic invoicing, while always_invoice generates an immediate charge.

If you use usage-based billing thresholds, test renewal-edge behavior directly: Stripe does not evaluate thresholds in the final 24 hours before a subscription ends.

Implement proration and invoicing with idempotent event handling#

Treat proration and invoicing as a controlled financial operation, not a set of one-off adjustments. There is no universal proration formula or event order to assume here, so your team needs one documented approach and consistent enforcement.

- Standardize one required change payload and reject incomplete requests rather than inferring missing inputs.

- Make retries replayable by mapping each approved change request to one recorded billing and accounting outcome.

- Enforce one execution sequence across systems so billing, accounting, and access updates do not drift.

- Put a reconciliation gate between invoice outcomes and ledger records before you close the change.

- Keep an audit trail for each change operation so you can review exceptions quickly.

Keep product access and billing state in lockstep#

Keep access and billing tied to the same recorded subscription change so your teams and systems can explain the same customer state. When entitlements and billing records drift, support, finance, and reporting all get harder to trust.

Step 1. Anchor entitlements to one billable state#

Use one billing-side record as the source for each entitlement change, and make that record traceable in logs. Your practical check is straightforward: pick a recent upgrade and downgrade, then verify you can trace each access change back to its billing-side change record and effective time.

If you cannot answer "which billing change caused this access update?" from your logs, you still have drift risk.

Step 2. Define and monitor acceptable delay#

Document what delay between billing updates and entitlement updates is acceptable for your product. The exact window is a business and risk decision, but it should be explicit and measurable.

This is not just a support issue. Billing and metering design affects financial reporting, and invoice timing is not the same as earned revenue because revenue is recognized as service is delivered. Track billing-to-entitlement lag and review exceptions.

Step 3. Treat annual prepay and contract changes as explicit policy decisions#

For annual prepay and contract changes, document how access changes map to your contract terms and service period instead of relying on a blanket "paid means fully active" assumption. A simple policy table reduces one-off overrides and makes edge cases auditable.

This aligns with ASC 606's five-step framework, where revenue is recognized when the customer gains control of promised goods or services; in many SaaS models, that promise is a stand-ready obligation. Use regular drift checks between billing status and entitlement status so mismatches are found and resolved quickly.

Related: Streaming Media Subscription Billing: How OTT Platforms Handle Billing Trials and Churn.

Close the books correctly for annual prepay and contract changes#

Annual prepay should not make operating performance look better than it is. Keep cash, recurring metrics, and revenue recognition as separate views, then close with written rules applied the same way each month.

| View | Treatment | Note |

|---|---|---|

| Cash collected | Keep separate from revenue and recurring metrics | Annual prepay cash and earned revenue are different events |

| MRR | Use a separate view | It does not need to match month to month |

| ARR | Use a separate view | It does not need to match month to month |

| Recognized revenue | Recognize as service is delivered, not when cash is collected | On a 12-month term, annual prepay is recognized evenly over the term |

Step 1. Separate cash from revenue and recurring metrics. Treat annual prepay cash and earned revenue as different events. In SaaS, revenue is recognized as service is delivered, not when cash is collected. On a 12-month term, annual prepay creates deferred revenue on day one, then is recognized evenly over the term.

Use separate views for cash collected, MRR, ARR, and recognized revenue. They do not need to match month to month because they answer different questions. A practical check is to trace one annual contract across all four views and confirm the same account tells one consistent story in finance and analytics.

Step 2. Write normalization rules for credits and refunds before month end. Do not handle credits, partial refunds, and downgrade adjustments case by case during close. Define a short policy for how these events are normalized in recurring metrics and which date controls monthly reporting treatment.

Consistency is the priority. Applying ASC 606 treatment the same way each month makes results steadier and easier to review, while inconsistent treatment creates late close changes, audit notes, and potential restatements.

Step 3. Add ASC 606 checkpoints to contract modifications. Upgrades, downgrades, and cross-sell additions can be contract modification events, not just pricing changes. Use a lightweight ASC 606 checkpoint (five-step framework) tied to the billing event: what changed, when it changed, and how it affects deferred versus recognized revenue.

For each material change, confirm effective date, updated subscription or add-on terms, related credits if any, and whether the service obligation changes now or at renewal. You do not need a long memo for every small change, but you do need consistent evidence that the review happened.

Step 4. Assemble a close evidence pack you can defend. Build a monthly evidence pack that clearly ties billing activity to accounting outcomes. A practical structure is an invoice log, credit memo log, ledger tie-out, and an exception list from billing automation.

Your close check is simple: invoice and credit memo activity should reconcile to deferred and recognized revenue movements, and exceptions should be resolved or explicitly tracked. If a contract change happened outside normal billing flow and is missing here, treat it as a close issue.

Build exception handling for refunds failed charges and cross-sells#

Build exceptions as predefined workflows, not ad hoc ticket decisions. That is how you reduce manual errors, keep customer handling consistent, and avoid reconciliation churn later.

- Define exception classes up front.

Use a short, fixed list: failed collection, disputed prorated invoice, refund after plan downgrade, and late cross-sell activation. For each class, define one billing treatment, one customer communication path, and one accounting review point. Manual mid-contract handling is error-prone, and spreadsheet-heavy fixes become less reliable as complexity grows.

- Assign owner, recovery path, and SLA by class.

Support can own customer communication, billing ops or finance can own credit decisions, and engineering can own event failures or replays. Document the recovery path and SLA for each class so teams do not handle failed collections and disputed prorations the same way by default. Clear roles and a clean process reduce close friction.

- Check CRM-billing sync before credits or refunds.

Before you issue a credit memo or refund, confirm CRM and billing reflect the same contract change. This synchronization is what keeps sales and finance records consistent. If records do not match, pause the case and resolve the mismatch first.

- Publish red flags that trigger escalation.

Escalate cases when you see:

- manual spreadsheet proration * off-cycle edits without a contract modification record * missing webhook audit trails

These signals indicate the case should move out of normal support handling into formal review.

If you want a deeper dive, read A Guide to Dunning Management for Failed Payments.

Wrap up with a copy-paste launch checklist#

Launch only when every item is complete with evidence, not just agreement. A non-streamlined billing process can create revenue leakage risk, so treat this as a go-live gate.

Before you start#

Assign one owner each from product, finance, engineering, and support, and name a billing operations owner for mid-cycle changes.

- Lock written policies.

Confirm one written rule for trial-to-paid conversion, mid-cycle upgrade, plan downgrade, proration, and annual prepay. Each rule should state the approval path, effective timestamp, access timing, and what the customer sees before confirming.

- Verify the event sequence end to end.

Confirm the system flow is consistent: subscription change -> prorated invoice -> ledger posting -> feature-gating update. Replay one upgrade and one downgrade in test/staging and verify those events stay aligned.

- Test retries and CRM linkage.

Confirm webhook handlers are idempotent and duplicate deliveries do not create duplicate outcomes. Confirm CRM-billing sync on the same test cases, since the subscription engine should stay connected to CRM for quoting and handoff continuity. If tooling is still open, choose based on your requirements, not a universal winner. With over 50 subscription billing tools in market discussions, fit matters more than brand ranking: The Best Tools for Managing Subscription Billing.

- Review the monthly close evidence pack.

Confirm close can separate cash collected, MRR/ARR normalization, revenue recognition, and ASC 606 review. Keep records that let finance reconstruct contract changes, invoice/credit outcomes, and ledger tie-outs without ad hoc evidence hunts.

- Assign exception owners before rollout.

Set named owners, SLAs, and customer-facing templates for failed collection, disputed proration, downgrade refunds, and feature-gating mismatches. Treat missing ownership or escalation paths as a launch blocker.

Want a quick next step on subscription billing for SaaS trials, upgrades, downgrades, and annual prepay? Try the free invoice generator.

Frequently Asked Questions

How should SaaS teams handle a mid-cycle upgrade without creating billing disputes?

Use a documented, consistent plan-change workflow, and make the pricing impact clear before confirmation. A common failure is handling upgrades informally and trying to reconcile billing afterward, which can increase frustration and churn risk. Keep plan changes, billing updates, and access changes aligned in one auditable flow.

Should a plan downgrade apply immediately or at period end?

The grounding here does not establish a universal timing rule. Choose one clear policy, make it visible in your plan-change workflow, and apply it consistently.

How do annual prepay, credits, and refunds change Monthly Recurring Revenue (MRR)?

Start by separating invoicing from revenue recognition. Annual prepayment creates deferred revenue on day one, and you recognize it over the 12-month term rather than taking the full invoice immediately when future service is still owed. For MRR, use a consistent internal policy for credits and refunds instead of mixing cash movements and recognition timing in one metric.

What must stay in sync between billing events and feature gating?

Keep billing outcomes and access state aligned so customers get what they paid for, when they paid for it. A practical check is to run real plan-change scenarios and confirm the resulting billing and access states stay consistent.

What is the minimum evidence needed for ASC 606 review of contract modification events?

ASC 606 alignment is essential, but the grounding here does not provide a specific minimum evidence checklist for contract modifications. Keep records sufficient to reconstruct what changed and when, then validate the standard with your accounting team.

How do you prevent duplicate charges when webhook handlers retry?

Handle retries so repeated event delivery does not create duplicate billing outcomes. Validate this with replay tests and confirm the financial outcome remains unchanged.

What should be automated first if we still run proration in spreadsheets?

Automate the step that most often creates inconsistent plan-change outcomes and customer confusion. Even before full automation, enforce one documented workflow and keep invoicing events separate from revenue-recognition reporting.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 3 external sources outside the trusted-domain allowlist.

- cs.princeton.edu/courses/archive/spring18/cos226/assignments/...trusted

- mit.edu/~ecprice/wordlist.100000trusted

- nlp.stanford.edu/~lmthang/morphoNLM/cwCsmRNN.wordstrusted

- sec.gov/Archives/edgar/data/1160951/0001193125202170...trusted

- sec.gov/Archives/edgar/data/1600222/0000950123250030...trusted

- chargebee.com/blog/maximize-billing-process-efficiencyexternal

- dev.to/krlz/android-saas-app-with-subscriptions-com...external

- docs.mixpanel.com/docs/pricingexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Best Tools for Managing Subscription Billing

**Protect cashflow by selecting for recovery and control first, then layering convenience features.**

A Guide to Dunning Management for Failed Payments

If you run recurring invoices, failed payments are not back-office noise. They create cashflow gaps, force extra follow-up work, and increase **Involuntary Churn** when good clients lose access after payment friction.

How OTT Platforms Handle Billing Trials and Churn in Streaming Subscriptions

Start with the monetization model. Choose your monetization path before a product demo starts steering the decision. For a streaming offer, the real question is not which vendor can show subscriptions on a checkout page. It is whether your business is built around recurring access, ad-supported reach, one-off transactions, or a direct-to-consumer mix that may vary by market.