Quick Answer

Yes - use both when spend should be approved before a bill exists: the Purchase Order controls authorization, and the Invoice controls payment release. For low-risk ad hoc spend, invoice-first can work only with compensating controls in place. Put a hard stop on payment when approval history is missing, matching variance is unresolved, or required references are absent. The practical baseline is clear AP ownership, a defined hold-and-release path, and a documented check against Purchase Requisition and PO policy before disbursement.

How Purchase Orders and Invoices Work in Platform P2P#

If you are evaluating purchase order vs invoice procure-to-pay cycle platform design, the hard part is usually not defining the documents. It is deciding who owns each checkpoint, what control exists before money moves, and how cleanly finance, product, and engineering hand off when something goes wrong.

A Purchase Order starts the buying process and records what your business intends to buy. An Invoice comes later and requests payment after delivery or completion. That distinction matters, but teams still struggle once approvals stall, documentation is missing, and someone has to chase exceptions across email, spreadsheets, and payment tools.

This guide treats Procure-to-Pay as an operating chain, not a glossary entry. P2P covers the full path from request and approval through PO creation, receiving or fulfillment, invoice matching, and supplier payment. When the PO side and invoice side are disconnected, visibility drops, approvals slow down, and reconciliation turns into guesswork. In practice, that means more exception chasing and more time spent reconciling records.

The goal is simple: map each stage to a decision checkpoint you can actually use. You will see where a Purchase Requisition matters, when a PO should be mandatory, when invoice-first handling is still workable, and where payment automation adds value only after approval and matching rules are stable. If you own product or engineering, that should help you avoid building payment logic around unclear procurement states. If you own finance or operations, it should help you separate true control gaps from tooling gaps.

The scope is intentionally narrow. The examples lean toward contractor, creator, and marketplace payment operations, where payout flows often sit close to procurement decisions but compliance coverage is not uniform across markets or programs. Verification requirements can vary by country and by account capabilities, and platform-provided verification does not automatically satisfy every independent legal KYC or verification obligation. Treat that as an early red flag. If your payment flow crosses borders or uses connected-account style onboarding, confirm what is actually covered before you automate approvals around it.

So the comparison ahead is not really PO versus invoice as isolated documents. It is about where each document belongs in P2P, which control each one is meant to carry, and how much automation your team can support without creating more exception work than it removes.

For a step-by-step walkthrough, see What Is a Requisition Order? How Platforms Use Internal Purchase Requests to Control Spend.

Want a quick next step? Try the free invoice generator.

PO vs invoice in one view for platform operators#

Use this rule of thumb: treat the Purchase Order as the spend-control document and the Invoice as the payment document. When the invoice has to do both jobs, AP inherits approval, receipt checking, and payment authorization at once. That is where avoidable exceptions usually grow.

| Comparison point | Purchase Order (PO) | Invoice |

|---|---|---|

| Issuer | Buyer side, after an internal request is approved | Supplier side, after goods or services are delivered |

| Trigger event | Approved buying decision, often after a Purchase Requisition | Delivery, completion, or another billable fulfillment milestone |

| Legal or commercial intent | Creates a commitment to spend | Requests payment for delivered goods or services |

| Control purpose | Approval workflow and budget authorization before ordering | AP payment authorization, matching, and posting after receipt |

| Required fields for control | Unique PO reference plus approved line detail needed for later matching | Invoice number and, in PO-based flows, the PO number |

| Downstream owner | Budget owner, requester, procurement, or operations before AP handoff | Accounts Payable, with approver input where policy requires |

| Timing in P2P | Early document, before fulfillment | Later document, after fulfillment and before payment |

| Where PO Flip fits | Source document for a PO Flip | Result of converting a PO into an invoice |

| When to block | Block PO creation if upstream approval is missing | If policy requires PR and PO, hold invoices missing those references unless an approved exception exists |

| Document state and system of record | Records approved spend intent and commitment state | Records supplier claim for payment and payable state |

| Audit Trail requirement | Keep approval history and document changes tied to requisition and PO state | Keep end-to-end traceability from invoice intake through payment approval |

| Ledger Journal posting | A PR can reserve budget without recording actuals; an approved PO alone should not be treated as posted expense or liability | In PO-based flows, posting is typically tied to product receipt and invoice activity; purchase invoice journals record expense debits and liability credits |

| Failure impact if wrong | Unapproved spend, weak budget control, and later matching disputes | Premature or duplicate payment, unmatched liabilities, and close/reconciliation rework |

What matters most in practice#

Timing is usually the row that matters most. A Purchase Requisition is the upstream approval request, and it is the cleanest point to stop bad spend before supplier engagement. It can reserve budget as a commitment without creating actual accounting recognition, so skipping it in policy-driven categories often leaves finance seeing the invoice first, with only approve, dispute, or delay as practical options.

PO Flip sits in the middle of the flow. It is an automated conversion of a PO into an invoice that can reduce rekeying when terms are already agreed. You still need to verify the flipped invoice against PO and receipt data before payment, especially where three-way matching is used.

Blocking rules and posting rules#

If a category requires pre-approval, block invoice processing when PR or PO references are missing unless a named approver documents an exception. If a spend type is truly invoice-first by policy, do not create a backdated PO just to tidy the records; that usually weakens audit chronology.

Posting discipline is the second control point. At the requisition stage, you can reserve budget without recording actuals, and in many PO-based setups GL impact is tied to receipt and invoice activity, not the PO alone. Your ledger should not show expense or liability just because a PR or PO was approved.

For AP, keep the checkpoint narrow: confirm that the invoice includes its own invoice number and the related PO number in PO-based flows, then confirm that billed items were ordered and received before payment approval.

You might also find this useful: Material Procurement for Platforms: How Marketplaces Manage Raw Material Purchases and Supplier Payments.

Where PO and invoice sit in P2P and where O2C hands off#

POs and invoices both sit in Procure-to-Pay (P2P), while O2C covers customer-side receivables and collections. In practice, use this sequence: Purchase Requisition -> PO approval -> supplier fulfillment -> Invoice receipt -> match and approval -> payment execution -> reconciliation.

That sequence keeps controls in the right place. Before PO approval, the question is whether spend should happen. After fulfillment, AP checks whether the invoice matches what was ordered and, where relevant, received. Before payment, the invoice should trace back to the requisition and PO, and forward to payment and reconciliation without audit-trail gaps.

| Process scope | Main purpose | Typical owner focus | Common confusion |

|---|---|---|---|

| Procure-to-Pay (P2P) | Outgoing supplier spend through payment and reconciliation | Procurement, budget owners, AP | Treating invoice intake as the start of approval instead of a late-stage control step |

| Order-to-Cash (O2C) | Customer order handling, billing, collections, and AR | Revenue ops, billing, AR | Mixing customer collections work with supplier settlement work |

| Source-to-Pay (S2P) | Upstream supplier sourcing, negotiation, contracting, then payment | Procurement, vendor management | Labeling supplier-selection or contract issues as "P2P problems" |

If the issue is supplier onboarding, negotiated terms, or contract coverage, treat it as S2P scope. If the issue is invoice matching, AP approval, payment execution, or reconciliation, keep it in P2P. For a related operating example, read How Platform Teams Pay Brazil Contractors with Pix.

Do you need both PO and invoice right now#

Yes, when the spend should be approved before the bill exists. If a purchase is repeatable, budgeted, or policy-gated, require both a Purchase Order and an Invoice. If the spend is truly ad hoc and low-risk, an invoice-led path can work, but only if you add an explicit approval workflow and non-PO checks before payment.

That is the basic split between the documents: a PO commits spend intent, while an invoice requests payment after delivery. In practice, the PO is the budget and policy gate; the invoice is typically the payment trigger. If your team already knows the supplier, category, expected amount, or agreed terms before work starts, skipping the PO can mean approvals happen too late.

For lower-risk categories, a lighter control can still be enough. Two-way matching checks the invoice against the PO only, which is often acceptable for low-risk categories or subscriptions where there is no physical receipt. Where delivery or receipt matters, three-way matching compares the invoice, the PO, and the goods receipt. That extra document helps only if you created the PO first.

| Operating signal | Use now | Defer now | Why it matters |

|---|---|---|---|

| Mostly ad hoc, low-risk purchases | Invoice plus approval workflow | Mandatory PO for every spend item | Non-PO invoices can work in some situations, but they need replacement controls before payment |

| Repeatable supplier spend, known terms, recurring category budgets | PO and invoice together | After-the-fact approval by AP | PO approval is where budget and policy checks belong; matching later helps control price, quantity, and terms |

| Higher volume and more handoffs between requestor and AP | Standardize PO plus invoice for most supplier spend | Informal email or chat approvals | As volume grows, manual handling gets more complex, and clear procurement-to-AP handoffs reduce exceptions and cycle-time drag |

If you stay invoice-led for a while, set a hard checkpoint before payment approval: validated vendor record, supporting-document review, approval routing, GL coding, and duplicate or fraud review. That is a practical compensating-control set for a non-PO path. A common failure mode is that AP discovers missing approval, unclear terms, or supplier data issues only after the invoice lands in queue.

The hidden cost of skipping PO controls rarely shows up on day one. It appears later as disputes, documentation gaps, and AP queue churn. When PO and invoice alignment breaks, errors multiply: overpayments, compliance risk, and strained supplier relationships become more likely. If your AP team is spending more time reconstructing intent than matching documents, that is your signal to require POs for repeatable spend and keep non-PO invoices as a documented exception lane, not the default.

Design approval and matching controls before automating payments#

Automate payment release only after your pre-payment controls are explicit and enforceable. At minimum: a role-based Approval Workflow, a declared 2-way or 3-way matching policy, an exception queue that can hold payment, and written override authority in Accounts Payable (AP) for who can clear a variance and with what evidence.

Once payouts are automated, approval and matching errors move faster too. If AP cannot answer who approved, what matched, and who released a hold, payment should not run unattended.

Choose the matching policy on the spend type#

Two-way and three-way matching serve different use cases. Two-way matching compares the PO and invoice. Three-way matching adds receipt confirmation before payment.

| Criterion | 2-way matching | 3-way matching |

|---|---|---|

| Documents checked | PO + invoice | PO + invoice + receipt confirmation |

| Best fit | Services, subscriptions, or spend with no practical receipt event | Physical goods or purchases where delivery/received quantity matters |

| Payment release condition | Invoice terms and amount align to the PO | Invoice aligns to the PO and receipt confirms what was received |

| Main tradeoff | Less evidence that delivery happened | Stronger control, but more exceptions if receipt capture is weak |

| Common failure mode | Paying for work or quantity that was never confirmed | Invoices stall because receipts were not entered |

If receipts are not captured reliably, forcing 3-way matching across all categories can add noise instead of control. Use 3-way where receipt evidence is meaningful; keep 2-way for service categories and require scope, milestone, or contract evidence in the approval record.

Define the exception path before auto-release rules#

For exceptions, sequence matters. Use a fixed operator flow:

| Step | Action | Note |

|---|---|---|

| 1 | Hold payment | Direct control to prevent payment during review |

| 2 | Request missing evidence | From the requester, receiver, or supplier |

| 3 | Re-match against approved documents | Use the approved documents |

| 4 | Approve or reject from the updated record | Decision comes from the updated record |

| 5 | Log rationale, approver, and hold release | Keep it in the Audit Trail |

Applying an AP hold is a direct control to prevent payment during review, and AP systems can maintain hold/release history as an audit trail. Before go-live, test an end-to-end exception, for example a price variance, missing receipt, or manual override, and confirm the invoice stays blocked until hold release is properly recorded.

Document override authority narrowly. AP may clear coding issues, but not missing approvals or unexplained quantity variances without support.

Add compliance and tax gates before payout release#

Add compliance gates in the same pre-payment lane when your product, market, or banking setup requires them. In U.S. banking contexts, 31 CFR 1020.220 requires risk-based customer identity verification. For legal entity customers at covered financial institutions, 31 CFR 1010.230 requires beneficial ownership identification and verification. AML controls are also risk-based and aimed at mitigating money-laundering and terrorist-financing risk.

| Gate | Purpose | Release note |

|---|---|---|

| 31 CFR 1020.220 | Risk-based customer identity verification in U.S. banking contexts | Use as a pre-payment gate where required |

| 31 CFR 1010.230 | Beneficial ownership identification and verification for legal entity customers at covered financial institutions | Use as a pre-payment gate where required |

| EU VIES tool | Checks whether a business is registered for cross-border trade in the EU | Validate VAT status when it affects invoice treatment |

| Form W-9 | Provides correct TIN data to payers filing information returns | Hold final disbursement until the payee record is complete if required data is missing |

| Form W-8 BEN | Submitted when requested by a withholding agent or payer | Hold final disbursement until the payee record is complete if required data is missing |

| Form 1099-NEC | Used to report nonemployee compensation | Hold final disbursement until the payee record is complete where applicable |

For EU cross-border business payments, validate VAT status when it affects invoice treatment. The EU VIES tool is used to check whether a business is registered for cross-border trade in the EU.

Treat tax artifacts as release gates, not follow-up tasks:

Form W-9: provides correct TIN data to payers filing information returns.Form W-8 BEN: submitted when requested by a withholding agent or payer.Form 1099-NEC: used to report nonemployee compensation.

If required W-9/W-8 BEN data is missing, or 1099-NEC readiness is incomplete where applicable, hold final disbursement until the payee record is complete.

Automate the pass path; keep exceptions on hold until documents, compliance checks, and tax artifacts align, with every release traceable in the Audit Trail.

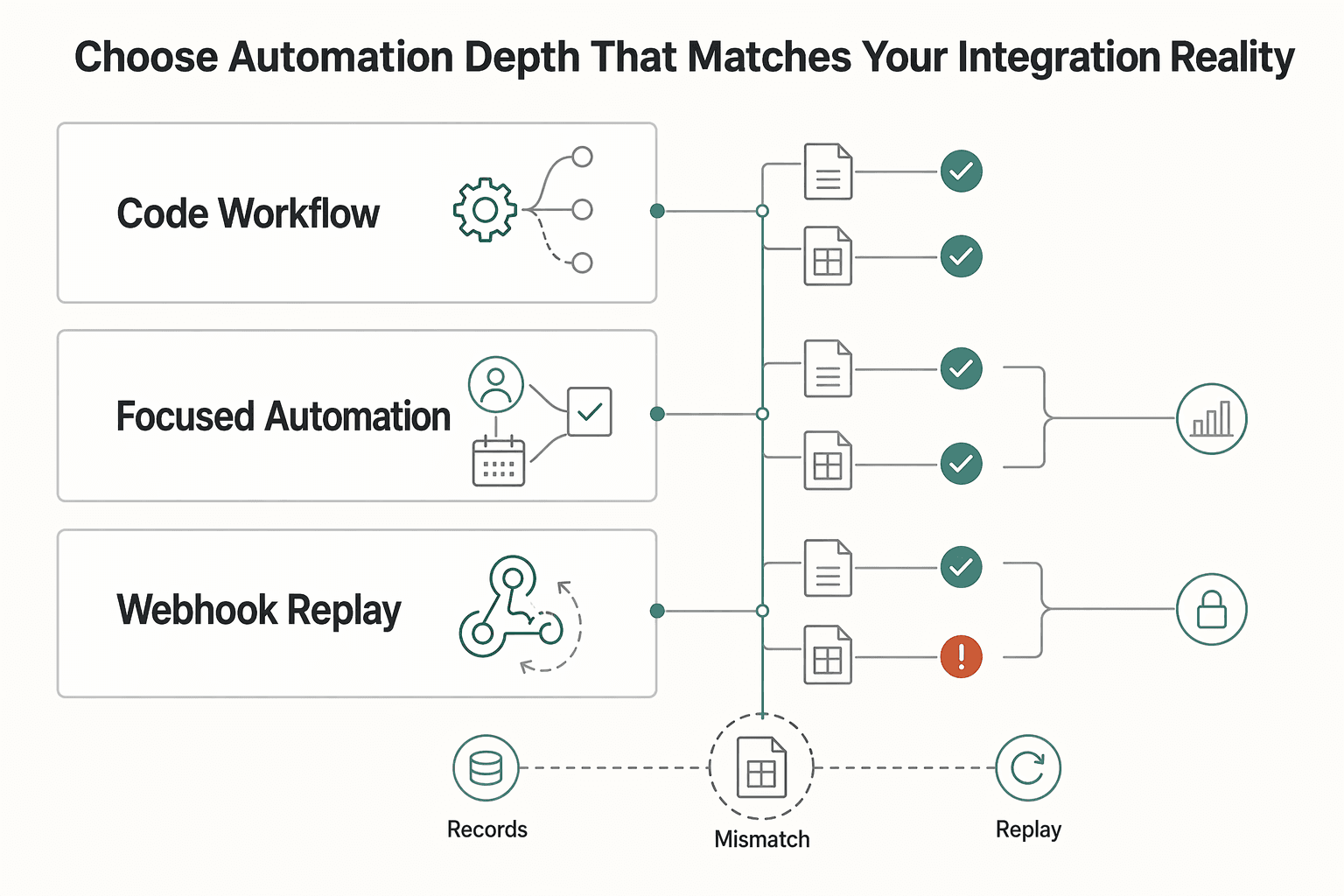

Choose automation depth that matches your integration reality#

Pick the shallowest automation layer that still gives you reliable status sync, reconciliation evidence, and hold control. If engineering bandwidth is limited, start with a constrained Approval Workflow plus webhook-driven status sync. If payout volume is high, prioritize idempotent API submission and batch controls before adding more edge-case automation.

| Option | Best fit | What you get quickly | What can stay weak | Go-live check |

|---|---|---|---|---|

| No-code workflow tool | Early team, low payout volume, finance-led rollout | Faster approval routing, basic invoice intake, less engineering dependency | Payment-state depth, Ledger Journal traceability, and procurement-to-payout state mapping can remain shallow | Confirm approved invoices can be held, and payout status returns to the same record |

| AP-focused automation layer | Finance needs approvals, PO/invoice handling, and 2-way or 3-way matching | Broader P2P control from request and approval through matching and payment handoff | Reconciliation load stays high if payout events and accounting evidence do not map cleanly to AP records | Test one exception case end to end: mismatch, hold, release, status update, posting evidence |

| Integrated payments infrastructure with Payout Batches and Webhooks | High payout volume, platform-led engineering, frequent async state changes | Real-time event sync, bulk disbursement controls, safer retries when implemented correctly | More custom logic and implementation effort to map provider states to procurement states | Verify idempotency keys, batch-level monitoring, and reconciliation against provider reports before scaling |

Start point for low engineering bandwidth#

If engineering capacity is tight, do not start with deep custom payout orchestration. Use a narrow Approval Workflow with clear roles, holds, and exception steps, then sync payout outcomes via Webhooks. Webhooks let providers push event-driven status updates and reduce constant polling for async changes.

Use that as an operating baseline, not your full reconciliation control. Keep a daily reconciliation check against provider evidence, such as recurring balance-change reporting, so late, failed, or mis-mapped events do not silently pass.

What changes at higher payout volume#

At higher payout volume, duplicate prevention and batch containment matter more than UI polish. Idempotency keys support retry safety by returning the original result for repeated requests with the same key, but they do not fix duplicate records created upstream or bad internal state transitions.

| Provider | Batch support | Stated limit or note |

|---|---|---|

| PayPal | Payments per call | Up to 15,000 payments per call |

| Wise Batch Groups | Transfers under one reference | Up to 1000 transfers under one reference |

| Adyen | Batch files | Supports bulk submission through batch files |

Batch capacity also becomes a hard design input. PayPal supports up to 15,000 payments per call, Wise Batch Groups support up to 1000 transfers under one reference, and Adyen supports bulk submission through batch files. At this stage, design around idempotent submission, batch-level monitoring, and explicit failure handling when a payout fails after an invoice is marked ready.

Also avoid a single "paid" procurement status when provider states are more granular. Payment states usually require custom mapping to procurement states, or reconciliation quality degrades quickly.

Platform-specific criteria that change the answer#

Some decisions are architecture-driven, not just AP-maturity-driven. If you accept inbound bank transfers, Virtual Accounts can improve attribution and automate reconciliation. If your model depends on one entity being legally responsible for customer payment processing, Merchant of Record fit is a core design choice.

The non-obvious tradeoffs usually decide outcomes:

- Faster rollout can mean weaker Ledger Journal traceability.

- Flexible exceptions can drift into off-policy handling.

- Lower upfront effort can increase downstream reconciliation load.

For most teams: start narrow and finance-led when volume is manageable, but make webhook sync plus daily reconciliation mandatory from day one. If volume is already high, lead with idempotent APIs, Payout Batches, and clear state mapping, then layer deeper AP automation.

Related: What Is a PO Flip? How Platforms Auto-Convert Purchase Orders Into Invoices.

Build the evidence pack finance and engineering both trust#

Once status sync is live, your next control is evidence. Build one monthly pack that AP and engineering can review without reconstructing each case, and anchor payout truth in provider settlement evidence, not just an internal paid label.

| Evidence artifact | What it answers | What it should link | Failure mode if missing |

|---|---|---|---|

| PO and Invoice linkage report | Was this invoice authorized against the right spend record? | PO number, invoice number, approval state, supplier/payee, amount, final disposition | Paid invoices cannot be tied back to approved spend, so disputes turn into manual record hunts |

| Exception log | What broke, who decided, and what happened next? | mismatch reason, hold/release timestamps, approver, request or retry reference, resolution note | Exceptions get resolved in chat or email and never enter the Audit Trail |

| Payout status file | Did the provider settle, reject, or hold the payout? | provider payout reference, status, amount, payout batch or settlement grouping, timestamp | AP marks invoices paid while provider status is still unresolved or failed |

| Audit Trail export | Can you reconstruct document and decision history later? | approval actions, state changes, overrides, invoice version history | Auditability degrades when records change after the fact |

If your provider offers a payout reconciliation report, use it as the backbone of your payout status file. Stripe frames this report for reconciling transactions included in each payout as a settlement batch. If you run manual payouts, keep explicit operator reconciliation against transaction history in the process.

For asynchronous payout states, set a clear standard for paid or rejected invoices: keep the provider reference ID, the Ledger Journal posting or equivalent funds-movement record, and the webhook event history that changed status. When available, keep the payout Trace ID as well for delayed or missing payout investigations.

A screenshot is weak evidence. A provider reference plus balance-movement record plus event history is stronger and easier to defend.

Preserve the original invoice record. In SAP Ariba's Invoice Reconciliation model, the original invoice remains unchanged for audit, while discrepancies are handled in a separate reconciliation document. Even in lighter stacks, keep that principle: do not edit the source invoice to "fix" reconciliation.

Use cadence as an operating control, not a ritual:

- Daily: triage new exceptions after prior-day provider data is available.

- Weekly: review amount and count variances across AP status, provider settlement output, and Ledger Journal postings.

- Month-end: lock the period evidence pack, carry unresolved exceptions forward explicitly, and sample rejected payouts back to webhook history and provider references.

If you retry payout creation, log the original request identifier in the exception log. Idempotent requests reduce duplicate-operation risk, but keys may be pruned after 24 hours, so later replays are harder to untangle without that record. Related reading: How Platforms Automate Pre-PO Approval with Purchase Requisitions.

Failure modes that create rework and payment risk#

Treat this as a hard rule: if variance, approval history, or payout evidence is unresolved, do not release funds.

| Breakpoint | What to check first | Containment rule |

|---|---|---|

| Unmatched or variant Invoice lines | Check matching holds created by invoice tolerance checks, then review the Matching Hold Detail Report before payment batch runs | Keep the Invoice on hold until variance is resolved; if your team allows release, require a named approver and recorded reason |

| Stale approval states | Compare current approval status with Audit Trail history and latest document version | Do not treat status alone as payment-ready without clear approver and timestamp history |

| Duplicate submission retries or duplicate webhook deliveries | Match request IDs, invoice IDs, and provider event IDs; webhook endpoints can receive the same event more than once | Treat retries and repeated events as duplicate-risk until deduplication or idempotent handling is confirmed |

| PO Flip mapping errors | Recheck PO number, line references, quantities, prices, and supplier mapping from source PO to generated Invoice | Hold as an integration exception until mapping is corrected and the document is revalidated |

Matching failures drive the most rework. Tolerance rules can place matching holds, and one invoice can carry more than one violated match rule, so clear all holds before payout instead of stopping at the first visible issue.

Asynchronous payout flows need separate controls. Webhook updates can be delayed, and undelivered events may be resent for up to three days, so reconcile provider reference, webhook history, and Ledger Journal posting before you mark payout status final.

Held or returned payouts should stay in exception status until destination data, provider status, and ledger impact agree. This includes payouts to virtual accounts, where destination-data quality matters because incorrect destination information is a common cause of returned payouts.

Pause scale-up when failures stop being isolated: the exception backlog keeps growing, held or returned payout exceptions keep recurring, or AP reports and Ledger Journal totals repeatedly fail to reconcile and create period-close blockers.

If you want a deeper dive, read What Is Source-to-Pay? How Platforms Can Automate the Full Procurement Lifecycle.

Conclusion#

The real decision is not choosing between a PO and an invoice. It is matching document controls to the risk you are actually carrying, the maturity your team has reached, and the amount of integration work you can support.

If your spend is repeatable, policy-gated, or sensitive to disputes, require both documents and keep them aligned. If purchases are genuinely low-risk and ad hoc, invoice-first may be workable short term, but only if you keep explicit approval checkpoints and refuse payout release when the record is incomplete or the match fails.

What matters next is traceability. Before you add more automation, make sure a paid or rejected invoice can be followed through the full P2P chain from requisition through payment, with evidence that both finance and engineering can inspect. In practice, that means an audit trail showing invoice actions and decisions, a ledger journal entry showing what was posted, and payment-event history from webhooks so state changes outside your main payment flow are still visible. If you cannot line those up on demand, you do not have a scaling problem yet. You have an evidence problem.

A practical set of checkpoints looks like this:

- Authorization checkpoint

Confirm whether a PO is required, whether the invoice matches what was approved, and whether matching rules are satisfied before payment is even considered.

- Payment checkpoint

Release funds only after the invoice status, approval history, and payment-state events agree. If the payment event stream and the invoice record disagree, hold the payout and reconcile first.

- Close checkpoint

Verify that the final payment has a corresponding ledger posting and retained audit history. If the accounting record exists without the operational history, or the reverse, month-end will turn into exception cleanup.

The main failure mode is rushing into deeper automation because the manual queue feels slow. Faster intake, approvals, PO handling, and invoice handling can help, but only when the underlying controls are already coherent. PO and invoice documents serve different purposes, so treating one as a substitute for the other can create approval and reconciliation issues later.

One final caution: coverage and compliance can vary by region. Do not assume the same controls, payment features, or rollout pattern will be available in every market. Validate region support before launch, pilot with a narrow scope, and scale only after reconciliation stays clean over time. That is the real finish line, not simply getting a payout out the door.

Frequently Asked Questions

What is the practical difference between a Purchase Order and an Invoice in a platform business?

A Purchase Order is buyer-issued and sent before fulfillment. An Invoice is vendor-issued after fulfillment as the payment request. In practice, teams often use the PO as an upfront spend-authorization control and the Invoice as a downstream payment control.

Where exactly do PO and Invoice controls sit in the Procure-to-Pay cycle?

P2P runs across the full spend sequence: requisition, sourcing, purchase orders, receiving, invoicing, and payment. That means PO controls sit upstream, before money is committed, and invoice controls sit later, when AP validates what was actually delivered and whether it should be paid. If your team only controls the invoice step, you may already be late on budget and approval discipline.

Do early-stage platforms need both PO and Invoice workflows, or can they start with one?

You can start invoice-only for smaller, low-risk purchases, because that pattern is common. The catch is scale: once PO and invoice handling are disconnected, error, dispute, and overpayment risk rises. A practical rule is to require both for repeatable, policy-gated spend, and allow invoice-only only where the dollar risk and approval complexity are genuinely low.

What should we automate first in P2P if finance headcount is limited?

Start with the controls that stop bad payments, not the ones that make screens look cleaner. That usually means invoice validation before release, a basic approval path, and retry-safe payout calls using idempotency keys. If you are sending payment API requests, keep a unique idempotency key on each request. Note that Stripe allows keys up to 255 characters, and do not assume a key will persist forever because providers may prune them after at least 24 hours.

How is Procure-to-Pay different from Order-to-Cash for marketplace operators?

P2P governs outgoing spend and supplier settlement. O2C is the sales-side motion: it creates an invoice, manages accounts receivable, processes payments, and manages revenue. For a marketplace, confusing the two usually shows up when teams apply customer billing logic to supplier payout controls.

What are the minimum controls to prevent duplicate or non-compliant payouts?

At minimum, validate the invoice before payment, use three-way matching where goods or receipt confirmation matter, and make retries idempotent so the same request does not create a second payout. For compliance, verify whether your payout provider requires KYC before funds can be paid out. Adyen is explicit that users must be verified before you can process payments or pay out their funds. If verification status, invoice approval, and payout request identity do not all line up, hold the payment.

When does a PO Flip improve operations, and when does it create new failure modes?

A PO Flip helps when your PO data is already clean, because it can create an invoice directly from PO data and enforce buyer business-rule validation. It can create new failure modes when PO data quality or line-level mapping is weak, because those defects can carry into AP. Before you trust it, verify the PO number, supplier, quantities, and prices against the invoice it generates. If those fields drift, treat the flip as an exception source, not an efficiency win.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- docs.stripe.com/connect/identity-verificationtrusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- europa.eu/youreurope/business/taxation/vat/check-vat-n...trusted

- irs.gov/forms-pubs/about-form-w-9trusted

- irs.gov/forms-pubs/about-form-w-8-bentrusted

- 2amagazine.com/the-po-vs-the-invoice-understanding-the-crit...external

- coupa.com/blog/procure-to-pay-automationexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

What Is Source-to-Pay? How Platforms Can Automate the Full Procurement Lifecycle

For platform teams, the pain usually does not sit in one isolated procurement task. It shows up in the handoff between finance, ops, product, and engineering as a supplier relationship moves from evaluation to agreement, purchasing, invoice review, and payout. A credible S2P platform should support that path end to end, not just the last mile of AP. In practical terms, the scope includes strategic sourcing, contract lifecycle management, procurement, invoice processing, and payment. You can frame S2P as four linked decisions:

What Is a PO Flip? How Platforms Auto-Convert Purchase Orders Into Invoices

PO flip only pays off when your purchase order data, controls, and exception paths are strong enough to support it. The conversion itself is straightforward. The operating risk is not. Weak order data, stale changes, or poor duplicate checks can turn a useful shortcut into long-tail reconciliation work.

Material Procurement for Platforms: How Marketplaces Manage Raw Material Purchases and Supplier Payments

For platform teams evaluating **material procurement platforms marketplaces raw material purchases supplier payments**, the real question is whether you can keep control from start to finish. Can your workflow stay intact from internal request to supplier disbursement to ledger-ready evidence? If that chain breaks, finance inherits more manual review, ops inherits supplier friction, and engineering inherits avoidable exception handling.