Quick Answer

Platform wallets do not have one universal U.S. float rule, and interest-bearing balances usually require more legal review, controls, and state-by-state analysis than transit-only balances. Teams should decide early who holds funds, how long balances sit, whether value accrues, and which federal and state review lanes remain unresolved. Launch where assumptions are documented and approved, and pause states or features that are still open.

How Float, Interest, and State Rules Affect Platform Wallets#

Wallet balances can improve speed and cost outcomes, but once those balances can sit as float or generate interest-like value, compliance scope can get heavier. That is the core design tension in 2026. Product teams want faster, smoother money movement, while legal, compliance, and finance need controls for how funds are held, monitored, and handled when something goes wrong.

That risk is not theoretical. GAO has noted both the upside, including faster transactions and potential cost savings, and that major harms have already occurred, including a case where a substantial portion of platform assets might be missing or stolen. So the practical question is not just whether to add a wallet. It is which wallet model you are actually building, and what obligations come with it.

Use this article as a decision framework before requirements harden. Define these points early:

- Who holds the funds

- How long balances are expected to sit

- Whether balances can generate or pass through value

- What sanctions controls and monitoring are required

- Which issues still need jurisdiction-specific legal review

Set one boundary up front. In June 2023, GAO said no single federal financial regulator has complete authority over nonsecurity crypto spot markets.

Also verify rule status before treating any item as a design anchor. The OCC entry posted on 03/02/2026 is a proposed rule, not final text. The Federal Register listing also states it does not provide legal notice. If your team references it, confirm current status, including the 05/01/2026 comment-period checkpoint, before locking assumptions.

Read the rest of this piece as product-scoping guidance, not legal advice for every jurisdiction. The goal is to help you choose the right wallet path early. Where relevant, that includes sanctions, because OFAC says sanctions obligations apply equally to virtual-currency and fiat transactions and expects a risk-based compliance program.

Define the terms before you design the product#

Start by treating product terms as internal labels, not compliance conclusions. Define them clearly in your PRD, then keep the legal conclusion open until it is tied to a specific form, rule, or notice.

The only items in the provided materials that come with that kind of concrete document anchor are these:

| Item | What is supported here |

|---|---|

| Form 1116 | IRS form used to claim the foreign tax credit |

| Form 1116 by category | A separate Form 1116 is required for each listed income category |

| Foreign tax credit limit | Credit is capped by a U.S.-tax-liability fraction formula |

| FBAR filing notices | FinCEN publishes FBAR due-date notices, including disaster-related extension updates |

In these materials, terms like "platform wallet," "float," and "interest-bearing" are not defined with regulator-backed meanings. Use them as working labels, document exactly what the product does, and do not treat the label itself as a settled compliance category.

Apply that same standard in wallet scoping. If a term is not tied to a concrete form, rule, or regulator notice, treat it as shorthand, not a finished compliance position.

Build the regulatory surface map before writing a single feature spec#

Map money-movement functions to evidence-backed compliance checkpoints before you name features in the PRD. If you lead with labels like "wallet," "instant payout," or "yield," it becomes easy to bury the real compliance work inside UX decisions.

Start with verbs, not product names#

Build a function inventory first. Collect, hold, convert, and pay out. For each function, record the operating facts that drive review:

- who sends funds

- who can direct movement

- how long funds can sit

- whether balances are pooled

- whether value can change while held

- whether payout is rule-based or user-directed

Then add likely authority tags as provisional markers. FinCEN can be grounded from these materials. OFAC, CFPB, and state regulators can stay on the map as open review paths, not resolved conclusions.

Use "same activity, same risk, same regulation" as an internal escalation heuristic, not a cited rule. Bundled functions can expand review scope faster than teams expect.

Separate known federal signals from unknown state treatment#

The strongest concrete federal signals in these materials are FinCEN artifacts and filing mechanics:

- FBAR (FinCEN Form 114)

- $10,000 maximum-value trigger for certain foreign-account reporting

- April 15 due date with automatic extension to October 15

- maximum-value handling details, including item 15a for "amount unknown"

- XML filing mechanics where required missing elements can cause rejection

- Section 311/BSA administration delegated to FinCEN, with docketed NPRM process (FINCEN-2023-0016)

These details show how specific obligations are framed. They do not, by themselves, settle domestic-only wallet design choices. A practical map format:

| Function | Likely authority lane | Evidence artifact | Open question |

|---|---|---|---|

| collect / hold / convert / pay out | FinCEN, OFAC, CFPB, state (as applicable) | form, threshold, notice, docket, or rule text | what is still unresolved |

If the evidence artifact is blank, treat that row as unresolved. In these materials, state-by-state float and interest treatment stays in the unknown column.

Split mixed use cases early#

If your roadmap includes both consumer and contractor flows, split them into separate compliance tracks before you lock one shared account model. One balance construct may look efficient early, but it can make controls, disclosures, and exception handling harder to defend later. At minimum, separate:

- product assumptions and terms

- ledger flags and reporting views

- unresolved regulator questions and counsel memos

Related: How to Pay Contractors in Vietnam: VietQR Napas and State Bank FX Rules for Platforms.

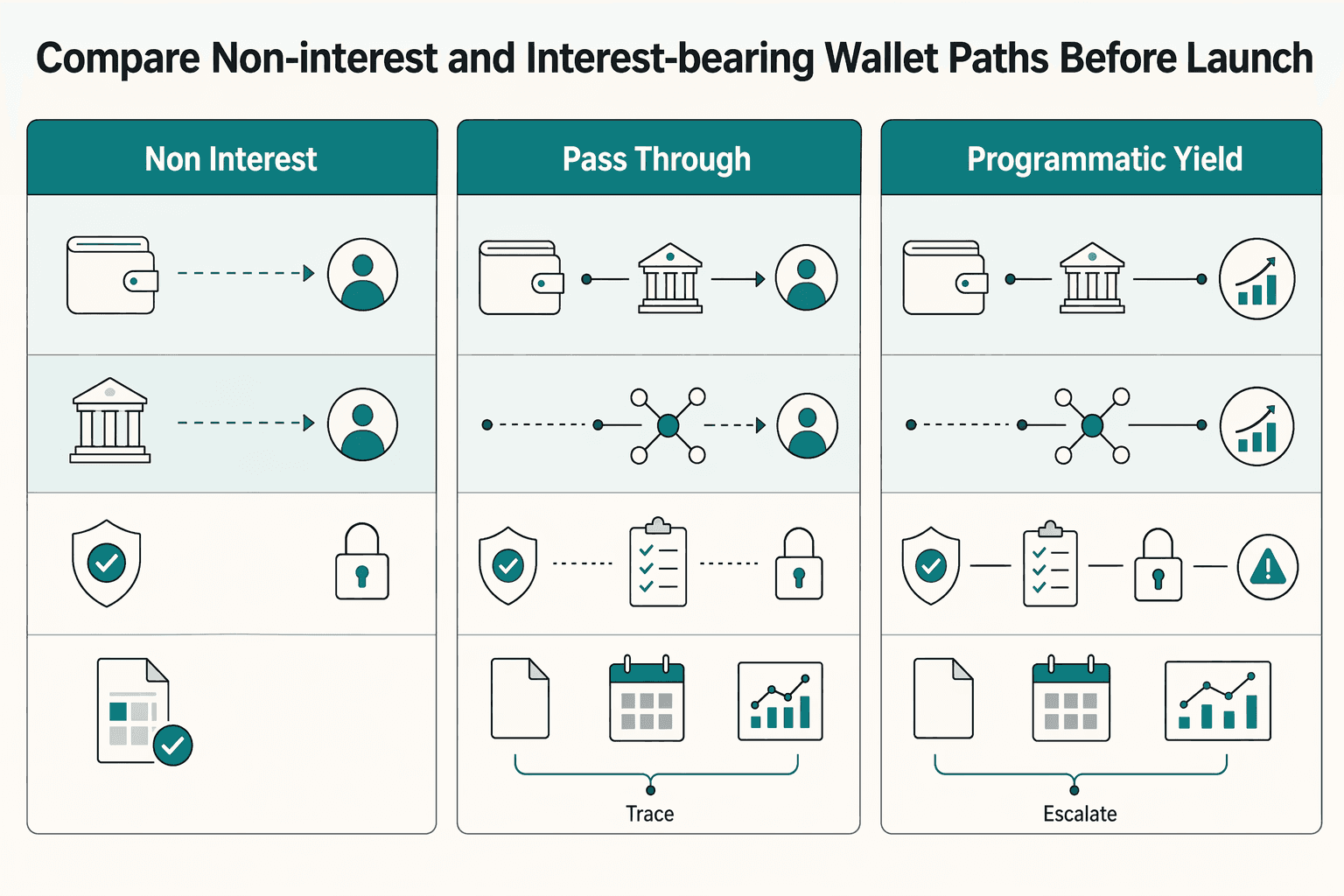

Compare non-interest and interest-bearing wallet paths before launch#

If transit-only balances can meet your product goal, choose that path first. Once balances can accrue value, legal review, controls, and operating overhead can increase, so test assumptions before you assume upside.

This is a launch decision, not a pricing toggle you can casually add later. In these materials, CFPB remittance context is concrete for consumer international electronic transfers. Exact EFTA, 12 CFR Part 1005, and state treatment for these wallet variants remain unresolved here and need case-specific review.

| Path | Product upside | Regulatory complexity | Required controls | Operational cost |

|---|---|---|---|---|

| Non-interest, transit-only balance | Potentially faster payout experience and simpler balance expectations | Potentially lower, but still requires fact-specific review if consumer or cross-border flows are possible; review CFPB remittance context plus EFTA, 12 CFR Part 1005, and state interpretations with counsel | Payout traceability, hold-time/aging rules, reconciliations, clear funds status | Potentially lower |

| Pass-through interest | Potentially stronger value story for held balances | Higher and more fact-specific; these materials do not settle classification or obligations | Principal vs accrued-value reconciliation, disclosure/process review, correction and exception handling | Medium to high |

| Programmatic yield | Potentially highest value story | Highest and most unsettled; broadest legal and state-level analysis burden | Value-change calculations, customer communications, incident handling, reporting workflows | Highest |

Use simple decision rules early#

A few early rules can reduce expensive redesigns later. If balances are strictly transit-only, optimize for payout speed and traceability. If balances accrue value in any form, escalate legal review and control design before rollout.

If consumer international transfers are in scope, treat CFPB remittance-rule analysis as an early launch review lane. The Bureau frames remittance transfers as covering almost all international electronic transfers of consumer money. Remittance-rule assessment materials also include disclosure, cancellation, and error-resolution workflow areas.

Hidden costs usually land outside product#

The engineering lift is only part of the cost. Interest features can add work in four places: disclosure and process design, deeper reconciliations, reporting overhead, and incident-response and support complexity.

These materials do not provide exact wallet-specific EFTA or 12 CFR Part 1005 thresholds. They do indicate that consumer-protection controls include operational workflows, so budget for process ownership in finance, support, and compliance, not only feature build time.

Tie path choice to named review lanes#

Before launch, log CFPB remittance context, EFTA/12 CFR Part 1005 questions, and state money-transmission interpretations as review lanes for the path you chose.

If your flow may qualify as remittance activity, also flag the cited safe-harbor reference point of 100 or fewer remittances for counsel to test against your actual entity and program facts. Do not treat that threshold as a blanket wallet answer.

Freeze the path before you freeze the API#

Set one internal checkpoint before API contracts are final: product, legal, and finance align on the selected balance model and operating assumptions. At minimum, confirm:

- whether balances are transit-only or value-accruing

- whether consumer international transfers are in scope

- which disclosure, cancellation, and error workflows should exist at launch for your chosen flow

- how principal and any accrued value are reconciled and corrected (if applicable)

If you want to turn this path comparison into implementation requirements, map it to API flows and control events in the Gruv docs.

Map federal touchpoints by function and control owner#

Build a federal touchpoint map with named owners, and label each row as either concrete now or unresolved. In these materials, only FinCEN and IRS items are concrete. OFAC, CFPB and EFTA, SEC, and CFTC stay open review lanes.

| Function or question | Authority or document | What is concrete here | Status | Legal | Compliance | Payments Ops | Engineering | Finance | Verification artifact |

|---|---|---|---|---|---|---|---|---|---|

| Sanctions exposure review | OFAC | These materials do not establish wallet-specific sanctions obligations or controls | Unresolved review lane | Lead | Lead | Support | Support | Monitor | Open-issues log with owner and counsel questions |

| FBAR update monitoring | FinCEN FBAR page | FinCEN posts dated update notices (example: "Additional Extension Due to Hurricane Milton (10/11/2024)") | Concrete monitoring signal | Support | Lead | Support | Monitor | Support | Dated check record and change log |

| Consumer transfer interpretation | CFPB, EFTA | These materials do not settle wallet treatment under CFPB or EFTA | Unresolved review lane | Lead | Support | Support | Monitor | Monitor | Scope memo listing open interpretation points |

| Market-function overlap | SEC, CFTC | These materials do not establish jurisdiction triggers for this wallet design | Unresolved review lane | Lead | Support | Monitor | Support | Support | Feature inventory tied to legal review |

| Foreign-tax-credit workflow | IRS, Form 1116, Form 1118 | Individuals, estates, and trusts claim via Form 1116; corporations via Form 1118 | Concrete filing-artifact lane when foreign taxes are relevant | Support | Monitor | Support | Monitor | Lead | Tax memo with form path and assumptions |

Treat unknowns as explicit lanes#

Do not leave unresolved rows as "someone will handle it." If a row has no clear lead owner, it is unowned, and it should block launch readiness for that scope. Use the concrete signals you do have, even when bigger classification questions remain open.

FinCEN gives you an operational monitoring signal through dated FBAR page updates. IRS gives you concrete filing artifacts for foreign tax credit workflow, including the form split by filer type.

"File Form 1116, Foreign Tax Credit, to claim the foreign tax credit"

If you use the simplified election (when eligible foreign taxes are not more than $300, or $600 if filing a joint return, and other conditions are met), note the tradeoff. Unused foreign tax cannot be carried back or carried over. Under the full limit process, unused amounts may be carried forward to the next 10 tax years.

Related reading: How to Write a Payments and Compliance Policy for Your Gig Platform.

Sequence state-regulation work when there is no universal float rule#

If your review does not produce one rule you can apply across every state, do the work in waves instead of trying to clear every jurisdiction at once. Start with the states tied to near-term launch scope, then expand after product behavior is fixed and changes are documented.

This is an operating choice, not a claim about state law. The goal is to avoid redoing broad state analysis every time wallet behavior, interest handling, or payout timing changes.

Build a state matrix you can actually use#

Use a matrix that supports go or no-go decisions, not a placeholder that just says "pending legal."

| Field | What to record |

|---|---|

| State | Jurisdiction under review |

| Launch wave | Wave 1, Wave 2, or later |

| Float treatment assumption | Current working assumption (or unknown) |

| Interest restriction assumption | Current working assumption for the variant in scope (or unknown) |

| Licensing posture | Current counsel view, including provisional views |

| Federal assumption touched | Which federal lane from your map could be affected (for example FinCEN) |

| Unresolved counsel questions | Exact open questions in plain language |

| Owner and last review date | Named owner and date |

| Evidence artifact | Memo, approval note, issue log, or equivalent |

Make the gating rules explicit#

Write the internal gates before expansion pressure starts. A practical internal baseline is simple: hold launch on a state row that still has unresolved classification questions. Hold interest-feature expansion until assumptions for that exact product variant are documented and approved.

Treat non-interest and interest-bearing variants as separate review rows when assumptions differ. Reusing one generic row across both usually hides real scope differences.

Keep one escalation path back to the federal map#

When a state interpretation changes a federal assumption, escalate immediately and update both records.

- State counsel flags the changed assumption or conflict.

- Legal updates the state row and opens a cross-functional issue.

- Compliance checks whether FinCEN-related reporting or recordkeeping assumptions are affected.

- Product and finance decide whether to pause launch scope, narrow the feature, or redesign.

For data-readiness checks, keep at least one concrete FinCEN checkpoint in the flow. Confirm your records can support FBAR logic when relevant. That includes a reasonable approximation of maximum account value, recorded in U.S. dollars and rounded up to the next whole dollar.

Design the controls stack so audits are survivable#

Once scope is defined, controls become the stable part of the product. The practical goal is simple: every balance change should be explainable, reproducible, and reviewable.

Make the ledger the core record#

Treat your ledger as the core record, and treat dashboards, webhook payloads, and UI balances as views of that record. As an internal baseline, define clear policy gates, sanctions checks, consistent event handling, and a durable journal for financial state changes.

This is not a claim that one regulator prescribes one exact wallet stack. It is a design choice that makes reviews and audits survivable.

Lock one order of operations before scale#

Set and enforce one operating sequence for your system: intake checks, ledger posting, balance projection, payout eligibility, and webhook-driven status updates. Keep webhooks downstream of the journal, not as the source of truth.

A related settlement pattern appears in SEC disclosure practice: paid amounts are confirmed before corresponding settlement actions, and short payment can follow an exception path rather than forcing a matched action.

Define failure branches up front#

Do the failure design before traffic scales. Document how the system behaves for key exceptions, for example when:

- deposits are unmatched

- FX quotes are stale

- webhook events are duplicated

- payout is attempted during an AML hold

The key is consistency. Each branch should produce a controlled outcome, a ledger-visible state, and a traceable resolution path.

Require evidence for every control family#

For each control family, keep evidence artifacts with the control itself: policy docs, named owners, test logs, and reconciliation exports. The CRS framing is a useful reminder that supervision is its own review dimension, separate from broader regulatory analysis.

Design for that reality by making it easy to produce records quickly, explain exceptions clearly, and show ownership at each control point.

Handle blocked property and sanctions incidents without improvising#

Sanctions handling should be as fixed as ledger handling. If funds may be blocked property, use one documented sequence that can stop movement quickly, route the case to a named owner, and preserve an investigation trail.

Use one incident path and make it explicit#

For wallet products, use detect -> freeze movement -> internal escalation -> reporting workflow -> periodic follow-up as your standard operating sequence. This is an operating design choice, not a claim that U.S. law mandates that exact wording or order.

It also keeps product behavior aligned with OFAC under the U.S. Department of the Treasury. OFAC administers and enforces U.S. sanctions. Many programs require blocking property and interests in property of specific persons or entities, and dealing in that property is prohibited. OFAC also states sanctions obligations apply equally to virtual-currency and fiat transactions.

Freeze movement in the product, not just in policy#

A sanctions hold should be a system state, not a ticket note. When an alert creates a potentially blocked-funds scenario, controls should stop outbound movement across payout initiation, internal transfers, balance release, and automated retries.

The checkpoint is simple. Funds are not released or rerouted until the case has a documented disposition tied to the ledger event and approved by the named sanctions owner. OFAC expects participants to avoid prohibited transactions directly and indirectly, so design for indirect paths too, including partner-triggered flows and manual overrides.

Keep sanctions handling distinct and program-aware#

Do not bury sanctions cases in a generic queue. Name OFAC in the workflow, because OFAC explicitly calls out recordkeeping, reporting, licensing, and enforcement processes that teams should be ready to handle.

Also avoid one canned decision path for every hit. OFAC notes prohibitions vary by program, so case records should support program-specific review of what was flagged, what property was affected, who controlled it, and what actions were blocked while review was open.

Build queryable records, not just policy PDFs#

Recordkeeping should be built into the product, not left to policy documents. Investigation history should be queryable and exportable so teams can reconstruct what happened without manual cleanup. Useful case artifacts include:

- alert match details

- linked ledger events and freeze state

- actions taken or prevented after detection

- reviewer decisions and escalation approvals

- follow-up entries until final resolution

Prevent accidental consumer-account exposure in mixed-use products#

Mixed-use drift can create classification risk, and it is worth addressing before scale. If a contractor wallet can plausibly function for personal, family, or household spending, that may warrant CFPB analysis tied to electronic fund transfers and 12 CFR Part 1005. That does not automatically mean every mixed-use wallet is covered.

A central boundary in the proposal is account purpose. In Docket No. CFPB-2025-0003, CFPB posted a proposed interpretive rule on electronic fund transfers through accounts established primarily for personal, family, or household purposes using emerging payment mechanisms. Because this is a proposed interpretive rule with a comment process, use it as a triage signal, not a final test for every mixed-use wallet.

Use a flagging checklist, not wishful labeling#

Do not rely on a "business" label alone. As an internal triage heuristic, not a CFPB-mandated checklist, flag the account for legal review when the product shows consumer-facing signals such as:

| Signal area | Indicator |

|---|---|

| Onboarding language | Does not clearly limit use to business or contractor activity |

| Terms | Allow broad lawful use without excluding personal, family, or household activity |

| Balance features | Position the wallet as day-to-day stored money |

| Help-center or marketing copy | Suggests everyday spending, bill payment, or general money storage |

| Transaction patterns | Show repeated personal-use behavior after launch |

If multiple signals are present, treat the classification question as active before expanding distribution.

Segment early if personal use is plausible#

If personal use is plausible, consider segmenting early. Keep contractor or business wallets distinct from any consumer-purpose experience in product copy, eligibility rules, terms, and internal reporting.

Consider setting an evidence checkpoint: retain onboarding screens, terms versions, approval records, and sampled transaction-purpose data mapped to the "personal, family, or household purposes" risk. A common failure mode is launch drift. Exceptions and growth pressure can gradually turn a scoped wallet into a de facto consumer balance product without a deliberate CFPB and 12 CFR Part 1005 review.

Plan for cross-border variance without breaking your core architecture#

Cross-border variance needs to be part of the design, not an afterthought. A wallet model that works in the U.S. will not always port cleanly to other markets.

Your U.S. model may lean on FRB framing and other U.S. regulatory materials, while other jurisdictions can require different product boundaries and approval paths. This is an architecture decision, not a policy memo. The FRB describes cross-border payments as a critical part of global economic and financial integration, and global coordination through the FSB and CPMI still targets the same pain points: cost, speed, access, and transparency. That is a good design signal that one-rule-fits-all implementations usually fail.

Use a portability test before opening a new market#

Before you open a new market, ask one hard question: can your control model adapt by market without changing core ledger, payout orchestration, and sanctions components?

A portable design keeps the ledger as the source of truth and moves market variance into configuration and policy layers. If a new market forces basic posting-logic rewrites or custom sanctions code instead of parameterized controls, refactor before launch. Otherwise, each jurisdiction becomes its own product branch.

Make market support a technical state#

"Where supported" should be enforced in product config, not only in terms or sales copy. Keep explicit flags for:

- wallet balance holding allowed or blocked by market

- accrual or interest features enabled, disabled, or approval-gated

- payout rail availability, hold periods, and required review steps

Drive onboarding, API behavior, UI copy, and ops queues from those flags, and fail closed in code when a market is unsupported.

One verification checkpoint is easy to miss. If you map U.S. dependencies from rulemaking pages, do not rely on the FederalRegister.gov XML view alone. Use the linked official PDF on govinfo.gov for your evidence pack and verify against an official Federal Register edition, since the XML rendition is informational and does not provide official legal or judicial notice.

For a step-by-step walkthrough, see Cross-Border Streaming Rights and Billing: How EU Portability Rules Affect Your Platform.

Use a launch checklist that forces go or no-go decisions#

Make launch approval binary. If the wallet is not clearly understood, owned, tested, and documented, do not ship. A launch checklist is a decision gate, not a project tracker.

Before go-live, require proof that authority mapping is complete, state assumptions are documented, sanctions controls are tested, incident handling is rehearsed, and reconciliation works in failure paths, not only the happy path.

Anchor the checklist to evidence, not confidence#

Use the OCC Payment Systems booklet as a structure for your launch file. It is examiner guidance for bank supervision, not a universal wallet checklist, but its control model is practical: risk management, policies and procedures, internal controls, and risk assessment.

Your evidence pack should include at least:

- legal memos on product structure, authority mapping, and open state assumptions

- control test outputs for sanctions screening, ledger and reconciliation checks, and payout eligibility logic

- an owner matrix for Legal, Compliance, Engineering, Payments Ops, and Finance

- escalation contacts for sanctions incidents, customer incidents, provider outages, and reconciliation breaks

- release approvals with named approvers and dates

If a legal conclusion depends on a Federal Register item, do not rely on FederalRegister.gov XML alone. Treat that view as informational and verify against an official Federal Register edition before it enters your evidence pack.

Rehearse the failures that create regulatory exposure#

Require scenario tests for the paths most likely to fail under pressure. For example, test:

- blocked-party or sanctions hits that freeze movement and route to the right escalation path

- delayed provider webhooks arriving after ledger posting and balance projection

- return and chargeback flows that reverse prior payout assumptions cleanly

- payout retries that prove idempotency and prevent duplicate movement

This keeps controls aligned with a practical FinCEN posture: reduce money-laundering risk without unnecessarily stalling new payment-system operations.

Set explicit no-go triggers#

Write no-go triggers into the approval sheet and require named owners to clear them before launch. Use zero-tolerance triggers for:

| Area | No-go trigger |

|---|---|

| State interpretation | Unresolved state interpretation on float or interest treatment in any launch state |

| Sanctions incidents | No documented sanctions escalation path for sanctions incidents |

| CFPB or EFTA scope | Controls touching possible CFPB or EFTA scope without a clear owner |

Do not treat IRS bulletin highlights or synopses as authoritative legal interpretation. If your product touches covered digital-asset flows, confirm whether Form 1099-DA readiness is in scope. That includes gross-proceeds reporting for covered transactions on or after January 1, 2025, and certain basis reporting on or after January 1, 2026.

After product path selection, hand off tax consequences to the right team. See How to Handle Tax on Platform Wallet Interest: FDIC Pass-Through and Income Reporting.

Conclusion#

The durable decision here is operational: choose a wallet design that matches your risk appetite, then prove your controls still hold as guidance, product scope, and launch geography change.

Build a function-to-regulator map early, before code and contracts harden. FinCEN says it has examined emerging payment mechanisms since 1995 and describes an approach that aims to reduce financial-crime risk without inhibiting growth. For any wallet that can receive funds, hold them, restrict movement, or release them later, assign owners up front for FinCEN analysis, sanctions controls, and expansion approvals.

A costly mistake is shipping fast and rebuilding later. OFAC sanctions programs can require blocking property and interests in property, and some OFAC prohibitions also apply to certain non-U.S. persons. If your ledger, payout logic, and case management cannot freeze and preserve funds end to end, that is a product design gap, not just a policy gap.

Treat source checking as a control. For the OCC item dated 03/02/2026 on FederalRegister.gov, with a comment period ending 05/01/2026, use the linked govinfo PDF as the official-source checkpoint when you need the legal reference text. FederalRegister.gov states its web version is not an official legal edition and does not provide legal or judicial notice.

For state float and interest treatment, these materials do not support a universal U.S. answer. Launch where interpretation is closed, and keep unresolved states as no-ship. At minimum, preserve a dated legal memo, state assumption matrix, owner assignments, control-test outputs, release approvals, and copies of official notices relied on.

If interest is still on the roadmap, treat it as a separate approval event rather than a default extension of the wallet. Once the base wallet is controlled, move tax and reporting implications into a dedicated track. See How to Handle Tax on Platform Wallet Interest: FDIC Pass-Through and Income Reporting.

Teams that avoid rebuilds are usually the teams that can show, on a specific date, what the product did, which official sources they relied on, who owned each control, and why they paused when an answer was still open.

When your team is ready to confirm coverage and compliance dependencies for your target markets, contact Gruv.

Frequently Asked Questions

Do platform wallets have one universal float rule across U.S. states?

No supported evidence here establishes a single float rule across all U.S. states. Treat any national default claim as unverified until state-by-state interpretations are documented and approved. Launch where interpretation is closed and pause expansion where it is still open.

When does a platform wallet start looking like a regulated account product?

There is no supported bright-line trigger here based on balance, hold time, or user count. The materials do not define a wallet-specific trigger test, so changes in scope should go to legal review instead of guessed thresholds.

Can wallet balances be interest-bearing by default for all users?

Do not assume a blanket yes. The materials do not support default-on interest across all jurisdictions or user types. If interest is planned, treat it as a controlled feature with explicit approvals, segmented rollout, and documented state assumptions.

What changes operationally when interest is added to wallet balances?

The materials do not establish wallet-specific operational requirements when interest is added. They do show that adjacent tax workflows can require concrete filing artifacts, such as Form 1116 for individuals, estates, and trusts, separate Form 1116 filings by income category, and Form 1118 for corporations. That does not prove those forms apply to your wallet, but it supports planning for documentation scope to expand when requirements change.

Which federal bodies matter first for wallet compliance scoping: **OFAC**, **FinCEN**, **CFPB**, **SEC**, or **CFTC**?

These materials do not support one universal ranking. They do show that FinCEN's FBAR page includes dated update notices, so reporting calendars can change through event-driven notices. Assign ownership to monitor live updates rather than freezing a one-time priority order.

How should teams handle unknown state interpretations without stalling product delivery?

Treat unknown state interpretations as explicit decision items, not silent approvals. Keep a state review matrix with status, counsel question, decision owner, and ship or no-ship flag. Launch only where the issue is closed.

What is the minimum evidence package to defend a launch decision in an audit or regulator inquiry?

There is no regulator-defined minimum in the provided materials. A practical internal baseline is a legal memo, state assumption matrix, named owners, control-test outputs, release approvals, and dated copies of official notices relied on for timing decisions. Preserve the exact artifacts used because timelines and exception notices can change.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- federalregister.gov/documents/2026/03/02/2026-04089/implementing...trusted

- federalreserve.gov/mediacenter/files/financial-inclusion-panel-...trusted

- files.consumerfinance.gov/f/documents/bcfp_remittance-rule-assessment_...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- fincen.gov/reporting-maximum-account-valuetrusted

- gao.gov/assets/830/827878.pdftrusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: