Quick Answer

PCI scope reduction comes from architecture, not a vendor feature. Platforms reduce scope by keeping PAN on the shortest provider-controlled capture path, making other services token-only, and tightly limiting any PAN retrieval. Hosted fields, iframes, and provider-hosted checkout can help only when raw card data goes directly to the provider and does not leak into app services, logs, analytics, or routing.

How Hosted Fields and Tokenization Reduce PCI Scope#

PCI scope reduction is an architecture boundary decision, not a vendor feature. Decide exactly where PAN is allowed to appear, and block it everywhere else.

Under PCI DSS scoping guidance, any system that stores, processes, or transmits cardholder data or sensitive authentication data is in scope, and systems that can impact the Cardholder Data Environment (CDE) may be in scope as well. For platform teams, this is not only a checkout concern. If PAN reaches adjacent systems, or those systems can materially affect PAN-capable components, your CDE boundary expands.

The practical goal is simple: keep PAN on the shortest possible path and make token-only handling the default everywhere else. Payment tokenization replaces sensitive payment data with a token that holds no payment information, while the original data is stored in the tokenization service's vault. In practice, this typically changes scope only when the capture path is designed correctly from the start.

Step 1#

Map data boundaries before you choose UI components. iFrames or hosted payment pages can shape the capture path, but scope outcomes still depend on the full architecture and responsibility split. Use a simple checkpoint: know every place cardholder data can appear. If you cannot identify every place PAN can show up, you are not ready to claim scope reduction.

Step 2#

Sequence the decisions so you do not build in rewrite-heavy debt. Define the capture pattern first, then the token model, then routing and reporting. When tokenization is added after PAN has already flowed through app services, PAN assumptions can stay embedded in surrounding workflows.

Step 3#

Treat control and responsibility as a tradeoff, not a slogan. PCI SSC e-commerce guidance notes that merchants can choose different levels of control and responsibility. Aim for a narrow, intentional boundary: a small set of justified PAN-capable components, with token-only handling everywhere else.

For the PCI DSS 4.0 changes behind this shift, see PCI DSS 4.0 for Platform Operators: What Actually Changed.

What to prepare before you touch checkout code#

Before you shortlist vendors or build UI, lock your PCI boundary in writing. Define exactly where Cardholder Data (CHD) and Sensitive Authentication Data (SAD) are allowed, and where they are never allowed. That is what prevents accidental paths into the Cardholder Data Environment (CDE) that are hard to unwind later.

Step 1#

Write a one-page target state and get it approved across security, platform, and product. Under PCI DSS 4.0, any system that stores, processes, or transmits CHD or SAD is in scope, and systems that can impact the CDE can be pulled in too. Be explicit in how you label components: checkout capture components and any service that can handle raw PAN are PAN-capable. App APIs, analytics, support tooling, and exports should stay token-only.

Use a hard checkpoint: every service gets one label only, PAN-capable or token-only. If a service needs an exception, record the business reason before implementation starts.

Step 2#

Inventory every current PAN step, not just the payment form. Review web checkout, mobile SDKs, support screens, retry jobs, email templates, BI exports, observability tools, error payloads, and browser telemetry. Include systems that can impact the CDE, such as admin workstations, jump hosts, and CI/CD paths tied to checkout releases.

Do not assume hosted fields solve exposure on their own. According to the PCI SSC hosted payment page FAQ and the merchant-script FAQ, your site still has responsibilities when scripts can influence the payment page. If payment data is still visible in the browser, malicious client-side scripts can read it, so review client-side scripts and browser instrumentation before rollout.

Step 3#

Set ownership before build starts. Decide who operates the tokenization service and vault, and who is accountable for compliance evidence and architecture records. When ownership is split without a clear approver, detokenization access and audit evidence can drift.

Verification point: for PAN retrieval or vault-adjacent APIs, confirm every call is authenticated, authorized, and logged.

Step 4#

Enforce one release rule: no new raw card-data pathway outside approved boundaries. For token-only services, require token-only payloads and reject any API that accepts raw card data. This is how you keep scope boundaries intact as features, processors, and support workflows change.

Related: What Is an Audit Trail? How Payment Platforms Build Tamper-Proof Transaction Logs for Compliance.

- An approved data-flow diagram for web, mobile, and support-assisted payment paths

- A service inventory labeled

PAN-capableortoken-only - Evidence that logs, analytics, and telemetry stay out of raw card-data handling

- A named owner for every detokenization or PAN-capable exception

Set scope boundaries before vendor selection#

Do not let vendor demos redefine your boundary. Start with the PCI DSS 4.0 scoping baseline: any system that stores, processes, or transmits CHD or SAD is in scope, and systems that connect to or can impact the Cardholder Data Environment (CDE) can be in scope too.

Step 1#

Anchor vendor evaluation on scope first, not feature breadth. Ask every vendor exactly where PAN can appear and which connected systems can affect that zone. If the answer is unclear, you do not have a credible scope-reduction path yet.

Expected outcome: you can name where raw card data exists and which adjacent systems could pull scope back in.

Step 2#

Use a simple system map in design reviews, for example PAN-capable or token-only. It is an internal rule, but it forces clear decisions across services, admin surfaces, integrations, and data paths.

When a vendor claims scope reduction, verify that the architecture actually removes PAN from your services and constrains pathways into and within the CDE, rather than just changing documentation. Save a PCI scope checklist with this map and review it with product, security, and payments before you approve a shortlist.

Step 3#

Set your PAN retrieval rule before you compare providers. If a service can request PAN from a tokenization service, treat that path as potentially in scope and require a business-critical justification.

Late decisions here usually lead to retrofitted controls and slower delivery. Use a blunt test: if a claimed scope-reduction design still leaves multiple PAN access paths under your control, question the claim.

For a deeper technical look at tokenization and vault design, see How Platforms Handle PCI-Compliant Tokenization: Card Vault Architecture and Implementation.

Compare capture patterns and pick one on purpose#

Choose your capture pattern based on cardholder-data exposure first, then on UX flexibility. If faster delivery and lighter PCI burden are the priority, start with a provider-hosted checkout pattern and verify that card data stays in the provider capture path rather than your systems.

Step 1#

Compare options using the same questions every time:

| Pattern | Where card data can appear | Operational tradeoff | PCI scope risk |

|---|---|---|---|

| Provider-hosted checkout or redirect | Primarily on the provider-controlled capture path | Often faster to launch, but you still need trace and script reviews | Lower when card data stays out of your systems |

| Hosted fields or iframe capture | Inside the browser surface you control plus the provider-controlled field or frame | More UX control, but stronger client-side and script governance is required | Medium unless you prove PAN never crosses into app services or logs |

| Custom capture where your services handle card data | Across your checkout, APIs, logs, support tooling, and adjacent systems unless tightly constrained | Highest integration and compliance overhead | High if your systems store, process, or transmit cardholder data |

According to the PCI DSS e-commerce guidelines, redirect, iframe, and merchant-script models all need explicit review of where cardholder data and supporting scripts live. So the first question is always the same: where can raw card data appear?

Do not let bundled offerings blur responsibilities. Even when one provider sells both, the Stripe PCI guide and the PCI SSC redirect FAQ still push you back to the same review question: where can PAN appear, and who controls that path?

Step 2#

The tradeoff is straightforward: more capture control usually means more integration and compliance complexity. This is not only a scope discussion. It affects delivery speed and checkout outcomes too.

Poor payment form implementation can increase abandonment, and performance can matter at checkout. Keep HTTPS and clear trust and 3DS messaging as baseline checkout quality checks.

Step 3#

Set a decision rule before build starts. If scope reduction and speed are your primary goals, prefer a provider-hosted capture path and require a concrete business justification before choosing a path where your systems handle cardholder data.

Use three checks in design review:

- Does any code you own read, store, or forward raw card values?

- Do any systems you operate receive card-form payloads?

- Can connected systems affect the capture path enough to expand scope?

If any answer is yes, document that as intentional exposure, not "scope reduction."

Step 4#

For hybrid businesses, keep web and in-person payment decisions separate. The online capture choice and in-person processing path should be reviewed as different paths, with separate evidence and diagrams.

If in-person channels exist, document their controls separately so teams do not mix web capture assumptions with card-present assumptions.

Choose your token model and vault boundaries#

Choose a token model that keeps PAN access exceptional and contained. Keep detokenization rare and tightly bounded around your tokenization service and card data vault, and make key ownership explicit.

Step 1#

Decide and document your token approach up front, then tie each choice to a real product need. Record architecture reasons for any PAN-recovery path rather than treating PAN recovery as a default capability.

If you cannot name a clear PAN-recovery use case, do not design for broad PAN recovery. In your diagrams, keep services clearly split into PAN-capable or token-only, and keep CHD flows inside the tokenization and vault boundary.

Step 2#

Separate token issuance, CHD storage, and key management so one component does not become a shadow vault. Put token issuance in the tokenization service, keep PAN and other retained CHD in the card data vault, and make key ownership explicit.

This is the boundary that controls scope: systems that store, process, or transmit CHD or SAD are in scope, and systems that can affect CDE security can expand scope as well. Tokenization helps reduce retained PAN, but it does not remove vault-hardening obligations.

Step 3#

Define and document detokenization controls before implementation spreads, including which systems are allowed to request PAN and for what business need.

Keep this path narrow and treat PAN-capable callers as high risk. According to the PCI DSS standard, card-data transport on public networks should stay on approved encrypted paths, and you should keep audit records for PAN retrieval activity.

Step 4#

Treat PAN retention as an architecture decision, because it changes both risk and PCI scope. If you can avoid storing PAN, you lower security risk and reduce PCI compliance scope.

Keep token-only services outside PAN handling wherever possible, and keep PAN recovery exceptional.

Related reading: How Platform Operators Should Plan PCI DSS Level and Cost.

Sequence the implementation to avoid platform debt#

Plan the sequence before you code, then enforce it with rollout gates. A practical target state is to set the capture boundary early, then token-based API contracts, then gateway routing, and then reporting surfaces. Skipping planning usually creates security gaps, duplicate-charge failure modes, and cleanup work across APIs, events, and dashboards.

| Step | Focus | Gate or evidence |

|---|---|---|

| Step 1 | Lock the capture boundary first; keep the backend contract token-first | Trace a real checkout and save an architecture diagram, a redacted request sample, and logging review notes |

| Step 2 | Build APIs and webhooks around token identifiers and transaction IDs | Test retry and webhook redelivery behavior so one business action does not produce duplicate submissions |

| Step 3 | Define ownership before MoR or multi-entity expansion | Pause expansion until it is explicit which entity and provider credentials govern a payment |

| Step 4 | Gate each phase with scope checks | Keep evidence as part of normal delivery records during rollout, not only at Self-Assessment Questionnaire (SAQ) time |

| Step 5 | Run a brief dual path, then decommission legacy capture on a date | Record the cutover date, owner, paths to retire, and a post-cutover check showing legacy traffic is zero |

Step 1 Lock the capture boundary first#

If checkout uses Hosted Fields or an iFrame, decide that early and keep it stable before payment APIs spread. The backend contract should be token-first: receive a payment method token with fields such as amount and currency.

Use a concrete gate: trace a real checkout and confirm the server-side payment-create request contains the token, amount, and currency fields you expect. Save lightweight evidence for approval, including an architecture diagram, a redacted request sample, and logging review notes.

Step 2 Build APIs and webhooks around token identifiers#

Once capture is fixed, design payment APIs and webhooks around token identifiers and transaction IDs. Keep responses centered on the downstream integration artifacts other systems need, such as transaction ID and status like succeeded or failed.

Test retry and webhook redelivery behavior so one business action does not produce duplicate submissions.

Step 3 Define ownership before MoR or multi-entity expansion#

If you run Merchant of Record (MoR) or multi-entity flows, make ownership and access expectations explicit before adding regions. Document those rules so teams can determine which entity and provider credentials govern a payment.

If that is unclear, pause expansion until it is explicit.

Step 4 Gate each phase with scope checks#

Treat security and scope checks as release gates at every phase across logs, events, and analytics outputs. This aligns with broad PCI scope risk across the card-processing network, including service-provider and acquirer-operated systems.

Keep evidence as part of normal delivery records during rollout, not only at Self-Assessment Questionnaire (SAQ) time.

Step 5 Run a brief dual path, then decommission legacy capture on a date#

If direct PAN capture still exists, keep fallback temporary and explicitly dated. A short dual path can validate behavior, but only if it comes with a defined shutdown plan.

At minimum, record the cutover date, owner, paths to retire, and a post-cutover check showing legacy traffic is zero. Then disable the old path and related credentials so the fallback does not become a permanent second architecture.

Before rollout, map your token-based APIs, webhook retries, and routing checkpoints against Gruv implementation patterns in the developer docs.

Apply controls that still matter after tokenization#

Tokenization lowers exposure, but it does not remove control obligations for the CDE or for systems that can connect to or impact it.

| Control area | Required action | Evidence or check |

|---|---|---|

| Token-only and PAN-capable paths | Keep a hard boundary between token-only services and anything that stores, processes, transmits, or can impact systems handling cardholder data | Validate with real network-path and permission checks across admin workstations, jump hosts, and CI/CD paths |

| Secure transport and PAN retrieval | Use TLS 1.2 or TLS 1.3 for calls carrying card data over public networks; treat PAN retrieval endpoints as a named exception with clear ownership and approval | Review who can call those endpoints, and remove temporary migration access once the use case ends |

| Operational access to the card data vault | Limit access by role and purpose; if a team only needs payment status and token references, do not give it a path to PAN-capable tools | Export current role assignments, compare them to approved responsibilities, and track removals and exceptions |

| Key-management controls | Treat cryptographic key management as an operational control | Confirm changes do not reintroduce raw PAN into less controlled storage, and save those results with your access and network-path evidence |

Step 1 Separate token-only services from PAN-capable paths#

Keep a hard boundary between token-only services and anything that stores, processes, transmits, or can impact systems handling cardholder data. The CDE is where cardholder data or sensitive authentication data is stored, processed, or transmitted, and systems that can connect to or impact the CDE can still be in scope.

Treat any service that can connect to or materially affect a PAN-capable service as potentially in scope. Validate that with real network-path and permission checks across admin workstations, jump hosts, and CI/CD paths, then keep the evidence with rollout records.

Step 2 Enforce secure transport and tightly controlled PAN retrieval#

Use TLS 1.2 or TLS 1.3 for calls carrying card data over public networks. Keep transport controls strict for token operations too, since connected service paths can become a route into more sensitive components.

If your design includes PAN retrieval endpoints, treat access as a named exception with clear ownership and approval. Review who can call those endpoints, and remove temporary migration access once the use case ends.

Step 3 Restrict operational access to the card data vault#

Broad admin or support access to the card data vault can expand connected scope. Limit access by role and purpose, and review what each role can actually do in vault-connected systems.

Use evidence-based checks: export current role assignments, compare them to approved responsibilities, and track removals and exceptions. If a team only needs payment status and token references, do not give it a path to PAN-capable tools.

Keep the storage rule explicit too: sensitive authentication data must not be stored after authorization, even if encrypted.

Step 4 Validate key-management controls and keep evidence#

Treat cryptographic key management as an operational control, and document how tokenization and vault controls are validated.

Confirm changes do not reintroduce raw PAN into less controlled storage, and save those results with your access and network-path evidence.

Keep control while routing across processors#

If you want processor flexibility while limiting PCI scope growth, keep your routing architecture token-only from end to end.

Step 1 Define a token-only routing boundary#

Set one hard rule: routing services select processors using tokens and transaction metadata, not raw card data. Your router, retries, failover, and provider-selection logic should not store, process, or transmit CHD or SAD.

This is a scoping control, not a style preference. Systems that store, process, or transmit CHD or SAD are in scope, and systems that can connect to or impact the CDE can be pulled in as well.

Verification point: trace a payment request and confirm card data posts directly to the payment provider, not through backend services or logs.

Step 2 Isolate raw-PAN exceptions#

If a gateway feature requires raw PAN, isolate that path and document why it exists. Do not let a provider-specific exception become the default contract for upstream services.

Keep that exception behind separate service boundaries, access approvals, and release review. This helps prevent the common failure mode where card data spreads into logs, analytics tools, support tickets, or data lakes and expands scope.

Step 3 Keep platform functions token-driven across providers#

Keep routing, reconciliation, and payout logic based on token references and transaction metadata rather than card details. That supports multi-gateway orchestration without reintroducing PAN handling into app services.

Before adding or switching processors, review internal APIs and event schemas for raw-card assumptions or wholesale provider payload storage. If token and vault responsibilities are still unclear, use How Platforms Handle PCI-Compliant Tokenization: Card Vault Architecture and Implementation as a companion.

Step 4 Document ownership and access for PAN-capable paths#

For any PAN-capable exception path, document service ownership, data boundaries, and who can approve access. Keep this with your architecture evidence so token-only and PAN-capable paths stay explicit during processor changes or incident response.

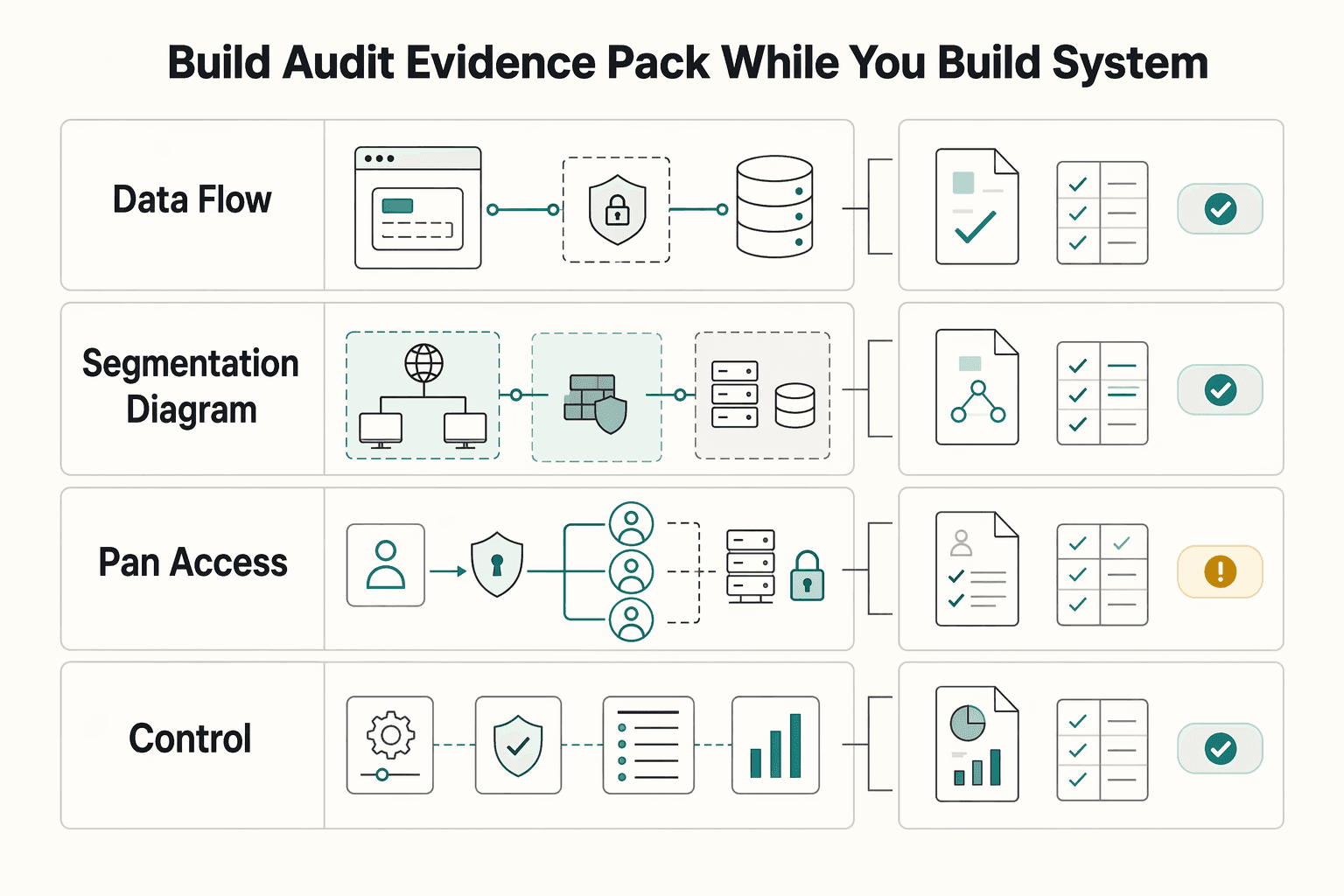

Build the audit evidence pack while you build the system#

Treat the evidence pack as part of implementation, not post-launch paperwork. If a PAN path is added, removed, or denied, update the evidence at the same time.

| Artifact | Scoping focus | Review note |

|---|---|---|

| Data-flow diagram | Where PAN can flow | After each payment release, trace one successful flow and one failure flow to confirm the documented boundary still matches production behavior |

| Segmentation diagram | What is segmented from the CDE | Use it as part of the operator-first map of what is inside or outside the CDE |

| PAN access policy | Who can request detokenization | If a PAN path is added, removed, or denied, update the evidence at the same time |

| Control ownership matrix | Who owns each control | Build SAQ inputs continuously instead of reconstructing evidence at the end |

Step 1 Create a living artifact set tied to PCI DSS requirements#

Keep four artifacts current: a data-flow diagram, a segmentation diagram, a PAN access policy, and a control ownership matrix. Use them as an operator-first map of what is PAN-capable, what is token-only, and what is inside or outside the CDE.

A practical checkpoint is to map this set to PCI DSS's 12 requirements as you implement and review controls. After each payment release, trace one successful flow and one failure flow to confirm the documented boundary still matches production behavior.

Step 2 Tie proof to the standards language you actually use#

Label each artifact with the scoping question it answers: where PAN can flow, who can request detokenization, what is segmented from the CDE, and who owns each control. That is usually faster to review than a pile of disconnected screenshots.

Use consistent PCI DSS terminology and keep tokenization terms precise. Vault tokens can reduce merchant scope, but they still carry portability and lifecycle tradeoffs, so your evidence should show the boundary controls you rely on, not just that tokens exist.

Step 3 Build Self-Assessment Questionnaire inputs as releases happen#

Build SAQ inputs continuously instead of reconstructing evidence at the end. As changes ship, store architecture decisions, test evidence, and approved exceptions with the same artifact set.

This matters operationally because PCI scope is tied to storing, processing, or transmitting cardholder data, even if you handle only one transaction per year. Continuous records reduce rework when reviewers ask how a hotfix, retry path, or exception was controlled.

Step 4 Write a one-page scope rationale for every major service#

For each major service, keep a one-page "in scope vs out of scope" rationale. State what data the service receives, whether it stores, processes, or transmits cardholder data, whether it can impact the CDE, and what it is explicitly blocked from doing.

Make the verdict explicit and testable against current network paths, permissions, and logs. If those checks and the one-pager diverge, fix the system first, then update the document.

Common mistakes and how to recover fast#

The fastest recovery path is to treat any unexpected PAN or CHD path as a release blocker until you confirm where cardholder data is actually flowing.

Step 1 Check for PAN leakage outside the checkout boundary#

A common mistake is assuming tokenization automatically keeps telemetry and logs clean. Inspect browser telemetry, front-end error payloads, server logs, and downstream log sinks for PAN or CHD, then redact at collection and storage points before you scale traffic.

Your verification point is a fresh trace that shows token values in analytics, errors, and events, plus confirmation that any card-data path on public networks uses TLS 1.2 or 1.3. If sensitive authentication data was captured, treat it as urgent because it must not be stored after authorization, even if encrypted.

Step 2 Restrict PAN retrieval access to approved callers only#

The failure mode here is broad access to PAN retrieval, which can expand practical PCI scope all over again. List every caller that can retrieve PAN, document the business reason and owner, and remove access that is not clearly required.

Keep the recovery evidence simple and current: PAN retrieval policy, current access list, and a documented storage pattern for the vault, key store, token table, and endpoint encryption.

Step 3 Stop new processors from creating side-door PAN paths#

Another common mistake is onboarding a processor or feature that bypasses token-based flows. Treat any request for raw card data as an architecture exception, not a standard integration.

Before launch, verify what identifier crosses service boundaries, what retries send, and whether routing still runs on non-reversible payment tokens. Trace one successful authorization and one retry. If PAN or CHD appears where it should not, isolate or reject that flow.

Step 4 Move evidence updates into each release#

The operational mistake is waiting for periodic assessment prep before updating documentation. Update evidence during each payment release so scope decisions stay tied to production behavior.

At minimum, keep the data-flow diagram, segmentation diagram, PAN access policy, and control ownership matrix current as changes ship. If artifacts and production diverge, pause rollout until the boundary is accurate again.

For a step-by-step walkthrough, see How Platform Operators Should Plan PCI DSS Level and Cost.

Conclusion and copy-paste launch checklist#

Treat launch as a go or no-go decision on card-data boundaries, not a tokenization feature toggle.

In 2025 and 2026, validate the approved path with three concrete cases: a 1 USD test authorization, a 25 USD subscription retry, and a 2,500 USD manual exception. If any of those routes leak PAN into logs, support tooling, or retries, your scope-reduction story is not ready for sign-off.

- Map every card-data path and verify it with real traffic.

Document where card data could appear across capture, token creation, retries, webhooks, exports, logs, events, and analytics. For each hop, label it token-only or PAN-capable, then confirm observed behavior matches the label.

- Lock the capture pattern and token boundary before release.

Freeze the approved flow so new direct card-data paths are not introduced through fallbacks or operational tooling. Make the token model explicit: payment tokens replace sensitive credentials such as PANs and bank account numbers, vault tokens can reduce PCI DSS scope for merchants, and network tokens are described as adding domain controls, automatic lifecycle updates, and dynamic cryptograms.

- Choose token model tradeoffs deliberately.

If provider portability matters, decide early how you will handle it. Vault tokens are presented as a scope-reduction option, but with weaker network-wide lifecycle intelligence and portability than network-token approaches. Network tokens are also described as improving fraud and authorization outcomes, especially for card-on-file and subscriptions.

- Check for leakage outside the core payment flow.

Review logs, error payloads, event streams, exports, and support surfaces with test transactions to confirm token-only handling where expected. Any unclear or mixed boundary should be treated as a release blocker.

- Make launch conditional on a complete evidence pack.

Keep one shared package with current data-flow mapping, token-boundary decisions, and verification results from real transaction tests. If any boundary or behavior is unverified, pause rollout and fix the architecture first.

For a broader view of how PCI DSS fits alongside SOC 2 and ISO 27001, see How to Evaluate PCI DSS, SOC 2, and ISO 27001 for Payment Platforms.

If you need a second pass on PAN boundaries and multi-processor rollout risk, request a practical architecture review with Gruv.

Frequently Asked Questions

Does tokenization alone remove PCI scope for a platform?

No. Tokenization reduces exposure by replacing payment account data with a token, but it does not remove scope on its own. Systems that store, process, or transmit cardholder data, or can impact CDE security, still matter for PCI DSS review.

Which pattern usually reduces scope more in practice, `Hosted Fields`, `iFrame`, or direct card capture?

Provider-hosted capture patterns can reduce scope when card data goes directly to the provider and your app receives only a token. Do not treat Hosted Fields versus iFrame as a universal ranking. Validate the actual browser flow, and keep iframe scripts updated and secure.

What systems remain in scope even when we use a `tokenization service`?

Tokenization services and token-vault paths still require strong security controls. Systems that can affect CDE security can also remain in scope, including admin workstations, jump hosts, and CI/CD systems. A practical check is whether a system can impact CDE or token-vault security.

Do we still need segmentation and strict PAN retrieval controls after tokenization?

Yes. Tokenization lowers exposure, but it does not eliminate security obligations. Where PAN retrieval is possible, those paths still need tight access control and ongoing hardening, and any card-data transport over public networks should use TLS 1.2 or 1.3.

Can we keep processor flexibility with `multi-gateway orchestration` without expanding the `CDE`?

Yes, in some architectures. Processor flexibility can be preserved when routing stays token-based instead of requiring raw PAN in app services. Treat any new processor flow that asks for raw PAN as an explicit exception to review because it can expand scope.

What is the minimum architecture and evidence set to review with security and a QSA?

There is no universal minimum package here, so use a review starting point instead of a final checklist. Document the real card-data boundary, including what stores, processes, transmits CHD, or can affect CDE security. Verify that capture flows send card data to the provider and return tokens to your app, and include provider compliance artifacts such as an available AOC.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- developer.paypal.com/braintree/docs/guides/hosted-fields/overview...trusted

- docs.stripe.com/security/guidetrusted

- stripe.com/guides/pci-compliancetrusted

- docs.adyen.com/online-payments/tokenizationexternal

- gruv.ai/blog/pci-compliant-tokenization-card-vault-a...external

- pcisecuritystandards.org/standards/pci-dssexternal

- pcisecuritystandards.org/pdfs/PCI_DSS_v2_eCommerce_Guidelines.pdfexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: