Quick Answer

Start with operating ownership before vendor selection: use MoR when faster cross-border launch and narrower customer-payment liability are the main goals, and use PSP plus in-house payouts only if your team can run verification, duplicate-safe webhooks, and payout failure handling. For payments on-demand service platforms delivery rideshare, require written proof of settlement timing, exception ownership, and country coverage before rollout.

On-Demand Platform Payments as a Two-Sided System, Not a Single Checkout Flow#

On-demand platform payments are a two-sided system, not a single checkout flow. You have to make customer collection and worker or contractor payouts line up end to end, or the mismatch shows up later as verification blocks, payout delays, or reconciliation issues.

That matters in rideshare, delivery, and on-demand labor and repair services, which fall within the IRS digital platform scope. In practice, your stack has to onboard users, process payments, and pay out funds, so payment architecture is also an operating decision about verification, settlement timing, and reporting. Use that lens as you read the rest of this guide. Treat each area as a launch gate, not cleanup work after rollout. Related: Airline Delay Compensation Payments: How Aviation Platforms Disburse Refunds at Scale.

- Customer checkout is only half the job

A smooth purchase flow does not mean you are ready to launch if payout operations are weak. You still need clear ownership of how funds become available, who can receive payouts, and what happens when payouts are delayed or blocked. If your team cannot trace funds from checkout to payout state, you are not operationally ready.

- Verification is a hard gate, not a background task

KYC checks are a prerequisite for payment processing and payouts, and requirements vary by country and account attributes. Country rollout is not copy and paste. Before you enter a market, confirm what each user type must provide, who handles failed checks, and what support and finance can see when an account is blocked.

- Settlement timing shapes worker experience and support load

Payout speed is constrained by settlement configuration and by industry and country payout availability. Stripe notes an initial payout is typically scheduled 7-14 days after the first successful live payment. If your supply-side promise assumes near-immediate access to funds, that timing can break it.

- Reconciliation is where weak designs surface

Webhooks are useful for asynchronous events, but they do not replace payout-level reporting. You still need a reliable way to match bank credits to payout batches and internal records. Before launch, verify which reconciliation exports or reports you will receive and how they map to your records. Uber Direct is a white-label delivery service, Roadie is a UPS-owned logistics network, and DailyPay is an earned wage access provider. Use examples like these to choose an operating model your team can support as rollout expands across markets.

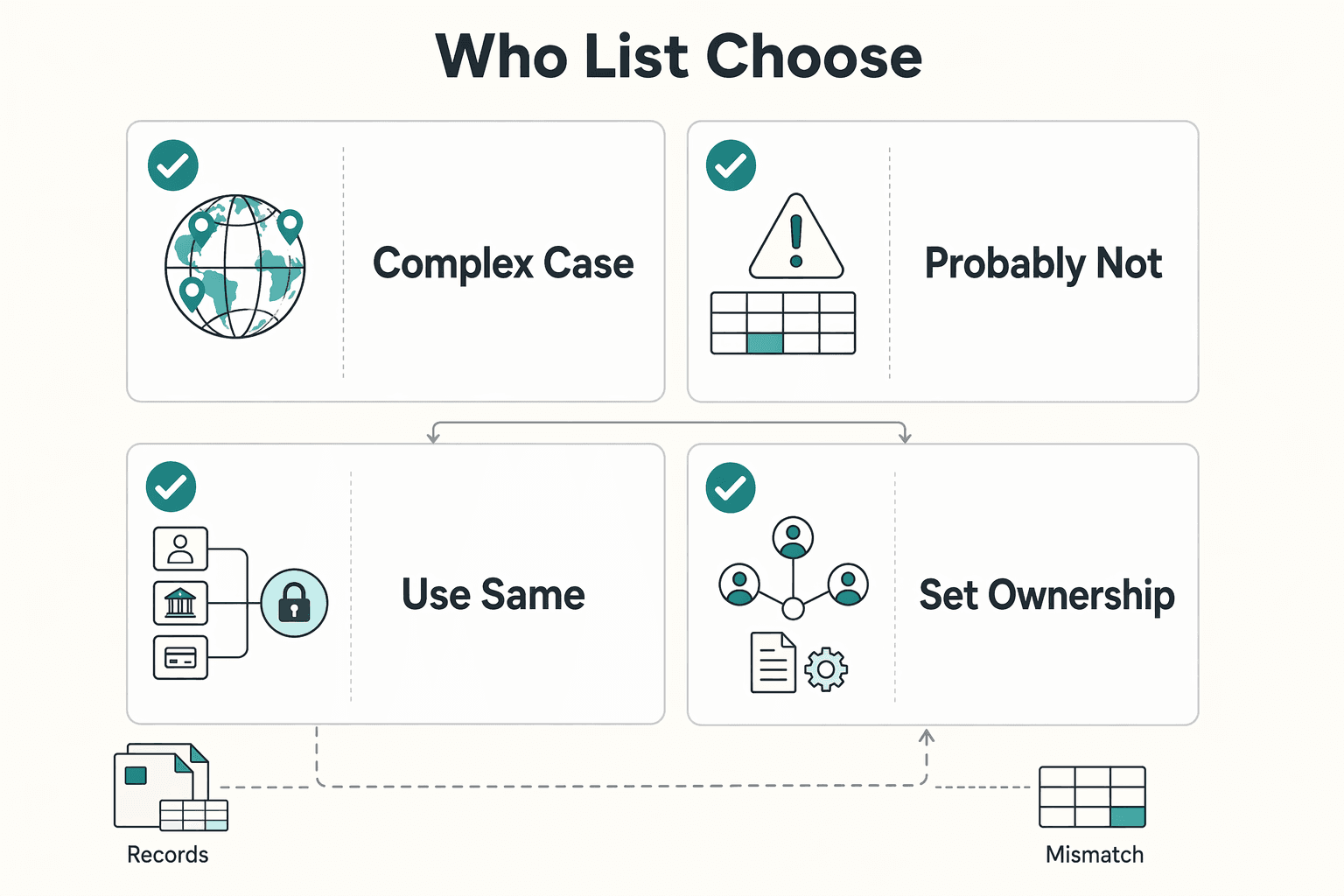

Who This List Is For and How to Choose#

Use this list as an operating filter rather than a feature checklist if you are choosing a stack across countries. If you cannot explain how identity checks, payout states, and reconciliation records work market by market, you are not ready to expand.

- Best fit: teams managing cross-country compliance and payout complexity

This guide is for platform founders, Payments Ops, and Finance Ops teams dealing with different KYC-style identity checks, KYB-style beneficial ownership checks, AML controls, and VAT conditions across markets. AML controls are risk-based, beneficial ownership checks for legal entities can apply in covered contexts, and EU VAT rules can be applied differently by country. The main decision is not checkout polish. It is whether your model can handle country variance without constant manual work.

- Probably not for: early, single-country builds

If you are still operating in one market with basic checkout and manual weekly payouts, this may be more stack than you need right now. Multi-country options can add integration, exception-handling, and reporting overhead before they deliver much value.

- Use the same four filters on every option

Compare each stack on payout reliability, reconciliation clarity in your internal records, API and webhook maturity, and where compliance ownership sits. Ask for the exact payout status model and how failed, returned, or delayed payouts are handled. A payout can show as posted while funds are still delayed at the recipient bank. Some payout flows can take 1-2 business days to confirm, plus another 3 business days for bank arrival.

- Set ownership before day one

Make ownership explicit for KYC or KYB failures, payout exceptions, and support escalation. If ownership is unclear, pause expansion. Webhooks are asynchronous and can include duplicate events, while finance still has to match internal records against external transaction and bank records.

Side-by-Side Comparison of the Main Stack Options#

The core choice is how much payment, compliance, and reconciliation ownership you keep in-house. MoR often reduces transaction liability, PSP plus in-house can give you the most payout control, and the other options are usually add-ons or hybrids that address specific operational gaps.

| Option | Best-for scenario | Compliance burden (KYC/KYB/AML) | Payout control | Reconciliation effort | Integration load (API + Webhooks) | Contract checks before launch |

|---|---|---|---|---|---|---|

| Merchant of Record (MoR) | Fast cross-border entry when speed matters more than custom payout logic | Lower on customer payment liability because the MoR is legally responsible for processing payments; some managed models also cover tax, fraud, and disputes in more than 80 countries | Medium | Medium | Medium | Confirm fee schedule and FX treatment, settlement timing by country, failed or returned payout ownership, and actual country coverage for your model |

| PSP + in-house payouts | Teams with strong Payments Ops and engineering that need custom routing and policy logic | High. Platform-led onboarding can leave KYC or KYB collection with you, and requirements can change over time | High | High | High | Confirm required onboarding data, how requirement changes are communicated, webhook retry behavior, and what payout status means operationally in your flow |

| Dispatch-network add-on | Platforms that need last-mile coverage quickly | Medium. Ownership can split across payment and courier parties | Low to medium | Can be high if data sits in separate partner portals or files | High. Dispatch APIs plus real-time webhooks | Confirm delivery event payloads, exception ownership, and region or country availability before rollout |

| Earned wage access add-on | Teams evaluating on-demand pay as a worker cash-flow option | Medium to high. Product treatment can shift over time and depends on scope conditions | Low for core marketplace payouts, medium for worker cash-access flows | Medium to high | Medium | Confirm eligibility scope (employees, contractors, or both), worker fee visibility, export treatment, and how records stay separate from ordinary payouts |

| Hybrid Virtual Accounts + Payout Batches | Multi-country platforms needing inbound collection plus controlled outbound payout runs | Medium. Collection accounts support inbound reconciliation, while AML and onboarding ownership still needs to be explicit | Medium to high | Medium | Medium to high | Confirm virtual account type, including payout restrictions, supported regions and currencies, duplicate batch ID handling, and batch failure or retry behavior |

Settlement timing is the contract lever to lock down early. Provider docs say payout schedules vary by country and industry, so market-by-market timing should be written into contracts instead of accepted as a generic promise.

A hidden cost during expansion can be reconciliation drift, not happy-path authorization. As Drew Edmond puts it, a core workload driver is "the level of effort required to reconcile payment activity."

With that tradeoff in mind, the next sections break down where each model earns its keep and where it tends to fail.

Before signing vendors, run your expected volumes and payout patterns through the payment fee comparison tool to stress-test margin impact by model.

Option 1 MoR-Centric Stack for Fast Cross-Border Entry#

Choose an MoR-centric stack when your first goal is faster cross-border launch, not custom payout logic. A Merchant of Record (MoR) is the entity legally authorized to process customer payments and is liable for the legal, financial, and compliance aspects of those transactions, including KYC and AML. Treat that as a scoped transfer of responsibility, not a blanket handoff.

Why teams choose it first#

This model can shorten time to market. It is strongest when activation speed is the constraint. It gets weaker when your model depends on highly customized payout states, routing, or exception handling from day one.

Where the tax boundary helps#

Tax responsibility can shift by flow and jurisdiction, so the contract has to say exactly where that line sits. In the EU, platforms can be treated as deemed suppliers for VAT purposes in specific scenarios, and cross-border B2C VAT rules changed on 1 July 2021.

A practical check is to confirm the provider's legal model in writing. Some marketplaces document both an MoR model, where the marketplace is seller and MoR, and an agency model, where the vendor remains MoR. Do not rely on generic wording like "we handle compliance."

The control you give up#

A common tradeoff is less flexibility on edge-case payout behavior. MoR also does not automatically settle ownership of payout exceptions outside the customer checkout leg. In connected-account setups, platform exposure can still return to you if an account balance goes negative.

The label is not a liability shield. Card networks enforce MoR rules, and violations can lead to significant fines. Regulators also evaluate conduct, not labels, as shown by the FTC's 2025 action that included a $5 million settlement.

Practical pattern for home services#

A workable pattern for home services is MoR for customer checkout, with separate payout rails for provider disbursements. In some implementations, that can support faster entry while keeping provider onboarding and payout controls explicit. Before launch, lock down three items in the contract:

| Contract item | What to confirm |

|---|---|

| Customer vs provider compliance | Ownership of customer-side KYC and AML versus provider-side onboarding and compliance checks |

| Payout status meaning | Whether payout status means submission, bank acceptance, or funds arrival |

| Reconciliation evidence pack | Settlement exports, transaction references, and country-level tax treatment |

For a step-by-step walkthrough, see How to Structure a White Label Service Agreement for Cross-Border Delivery.

Option 2 PSP and In-House Payouts for Maximum Control#

Choose this model when custom payout logic is core to your business and you can operate the compliance and exception-handling load that comes with it. A PSP plus in-house payouts can give you direct control over payout settings, timing, and reconciliation, but it also puts more failure-handling responsibility on your team.

Why teams pick this path#

The main benefit is API-level control. In a custom connected-account setup, the platform can change account settings through the API, including bank-account details and payout schedules. That matters when your payout and risk logic has to be tailored by market or flow.

You can also design ledger journals around your own reconciliation model instead of a provider default. If you go this route, webhook operations and idempotent retries become core controls, not implementation details.

What you own once you take control#

More control means more operational burden on the platform. In custom account setups, the platform can be responsible for collecting verification information, and KYC or KYB requirements vary by country or region, legal entity, and product setup.

Liability settings matter early. Where platform liability applies, responsibility for identity verification can shift to your platform, and connected-account disputes can also become your responsibility. If balances stay negative long enough, reserve impacts can return to the platform. One documented threshold is 180 days in the relevant setup.

The failure modes to plan for early#

A lot of breakage shows up in asynchronous flows, not just at checkout. Webhooks carry later events such as payment confirmations and disputes, so your ledger logic has to handle delayed signals.

Treat payout reversals as conditional, not guaranteed. A paid reversal can later be refused by the bank and move to failed, so reconciliation should tie together the payout ID, reversal reference, webhook events, and journal movements.

Practical decision rules#

This can be a strong fit when you run a rideshare or delivery platform that needs its own payout scheduler and compliance checks after validating market requirements. It is weaker when the priority is speed of country launch over custom control.

Before you commit, verify these points:

- Confirm negative-balance liability and dispute ownership in the PSP configuration and contract.

- Test webhook delivery handling, retries, and idempotency against duplicate and delayed events.

- Validate KYC, KYB, and VAT requirements market by market.

- Align payout promises with the actual provider setup. Initial payout scheduling can typically begin in the 7-14 day range after the first successful live payment.

- For EU rollout, validate VAT country by country. Member States implement the Directive nationally, and the standard VAT rate floor in the framework is 15%.

Use this architecture when custom payout control is a business requirement, not just a preference.

Option 3 Dispatch Network Add-On for Local Delivery Expansion#

If your bottleneck is courier coverage rather than payout logic, this can be one of the fastest expansion paths. Use a dispatch network for last-mile fulfillment, but keep financial truth in your payment and ledger systems so delivery status and cash movement still reconcile at month end.

Why teams choose it#

This model fits platforms that already own the customer order channel and need local delivery quickly. Uber Direct is positioned for orders placed through a business website, app, or phone, with options for under-2-hour, same-day, or scheduled delivery up to 30 days in advance. That can speed go-to-market when you need a delivery promise before building your own courier network.

Roadie is a similar add-on when the goal is coverage, not payout control. It promotes nationwide same-day reach, including deliveries up to 100 miles, and provides API workflows for shipment management. If your core question is whether you can cover a metro or region fast enough to test demand, this option can be a strong fit.

The MediaMarktSaturn example with Uber Direct, 90-minute express delivery in over 100 cities across Germany, is useful evidence of rollout speed, not evidence that finance operations become simpler.

The real tradeoff#

Dispatch events are not settlement records. Uber Direct sends webhook POST updates, and Roadie documents webhooks plus status, cancellation, and error surfaces. Those are useful for customer updates and exception handling, but they do not replace payout reconciliation or transaction-level settlement reporting.

A common operational risk is split visibility: operations may see delivery, support sees exceptions, and finance sees payout batches. Before launch, make sure the commercial review and integration review spell out what reconciliation files or exports you receive, who owns exceptions, and how delayed or failed callbacks are handled.

Keep the ledger in one place#

The cleanest setup is to use the dispatch partner for fulfillment while keeping customer payments, payouts, and ledger journals in one finance-owned system. Use reconciliation artifacts that map payouts to settled transactions, such as payout reconciliation reporting or transaction-level settlement details.

For each order, keep one internal record with:

- order ID

- dispatch delivery or shipment ID

- webhook events with timestamps

- payment processor charge or transfer reference

- settlement batch or payout ID

- bank payout reference

That single record helps resolve "delivered" orders that are still unreconciled in finance.

Decision rules before you sign#

Choose this option when speed to local delivery matters more than custom courier economics. Do not assume this model also covers KYB, KYC, AML, tax handling, or marketplace payout rails based on the retrieved material.

Before you commit, verify:

- Coverage versus your delivery promise, for example Uber Direct availability claims and Roadie same-day radius claims

- Integration constraints, including Roadie's published rate limit of 10 requests per second

- The reconciliation path from delivery IDs to payout batches through your payment reports

- Failure handling for duplicate, delayed, and missing webhook events

This can be the right expansion tool when logistics is the gap, as long as dispatch is not treated as your source of financial truth.

Option 4 Earned Wage Access Layer for Worker Retention#

Use this option when retention is sensitive to payout timing, and keep it separate from your marketplace payout rails. Earned Wage Access (EWA) is advance access to wages already earned but not yet paid on the normal schedule. It is a pay-timing layer, not a replacement for contractor disbursement operations.

Why it can help#

Flexible access to earned pay can improve worker supply and retention signals. Uber-linked research found that moving from weekly pay to flexible pay increased driver work time, and Harvard Business School cites evidence that EWA usage is associated with higher retention. Worker expectations are also visible in market behavior: Uber Instant Pay advertises cash-out up to 6 times a day.

Where teams get burned#

The main risk is product-boundary confusion. Employer-partnered wage access, contractor instant cash-out, and marketplace settlement are different flows, and treating them as one can create compliance and finance-logic errors.

US policy context shows why this needs tight scoping. CFPB treatment changed during 2025, and at least 20 states had pending EWA legislation in that legislative year. Classification also matters because employee and independent-contractor treatment differ for pay and tax handling.

How to structure it safely#

The safest pattern is to separate the rails on purpose. Keep contractor payouts on your standard payout flow, and offer earned access only where the model is supported for that worker category and jurisdiction. That preserves one stable settlement path while limiting earned access to a clearly governed scope.

Set one hard gate before launch: can you prove the offered amount does not exceed accrued earnings for that worker type in that jurisdiction? If not, stop and narrow the scope.

Set transfer expectations clearly. "Instant" can still be delayed by bank rails, so treat delay handling as a planned support process. Keep one shared record across the accrual snapshot, eligibility timestamp, cash-out request, payout reference, and bank transfer reference so finance and support are working from the same facts.

Option 5 Hybrid Stack with Virtual Accounts and Payout Batches#

Choose this when you need better inbound payer identification across countries, but still want to control when funds are released outbound. Virtual Accounts can improve inbound matching, and payout batches keep outbound release decisions centralized. It works best when finance and engineering share one event model and one ownership model before launch.

Why this option earns its keep#

This model fits platforms with many inbound payment sources and high-volume outbound payouts to workers, providers, or partners. In multi-market expansion, collection and disbursement often stop behaving like one linear flow, so separating identification from release becomes operationally useful.

The core identifier is the Virtual Account. In Virtual Account Management, providers combine a core deposit account with virtual subledger views, and unique virtual account numbers per payer can improve identification even when remittance details are poor. That reduces anonymous-looking deposits, but it does not eliminate reconciliation work.

On the outbound side, ACH is batch-based for both collections and disbursements. Design your release process around grouped processing, settlement timing differences, and later exceptions, not line-by-line instant finality.

What the operator burden really is#

Use a simple release rule. Release from payout batches only after inbound funds are matched to the right payer, posted to the correct internal records, and cleared through your hold logic for compliance or operational exceptions.

The hard part is asynchronous events. Webhooks can be delivered more than once, and undelivered events may be retried for up to three days. Your consumer has to prevent duplicate business effects, not just accept requests. If a duplicate event can post a second journal entry or trigger a second release, the design is incomplete.

Two checks can prevent many avoidable failures:

- Verification checkpoint: For each inbound credit, trace payer identifier, provider reference, internal payment object, and resulting ledger journal entry without spreadsheet stitching.

- Failure-mode checkpoint: Define one canonical status model for late identification, retried webhooks after manual intervention, and compliance hold states.

Where teams get burned#

The main risk is false confidence from cleaner inbound references. Better identification improves matching, but it does not prove amount accuracy, timing correctness, or release eligibility. Exceptions can still break settlement logic even when matching rates improve.

Sanctions blocking is another hard edge. In the US context, institutions that receive and block payments have explicit reporting duties, and the initial report is due within 10 business days after property becomes blocked. That timing should not be generalized to every jurisdiction, but your records should still be audit-ready: payer details, provider references, hold reason, timestamps, journal entries, and approver trail.

ACH timelines can also create long-tail exposure. Nacha cites a one year warranty-claim limit for entries to non-consumer accounts. Regulation E-related consumer error windows can run 60 days from the statement showing the first error. These are ACH-context reminders that exceptions can surface long after a batch appears complete.

Concrete use case#

A home-services marketplace is a practical fit when customer collection and provider payout are decoupled in time. One internal pattern is to post inbound payment events to ledger journals first, then move through your own review and hold states before approving provider release.

In this setup, Virtual Accounts improve who-paid identification and payout batches control when funds move out. Webhooks update lifecycle state, but they should not be the sole source of truth. Ledger postings, provider references, and batch release records should line up before disbursement.

Recommendation#

If expansion pain is mostly inbound identification, this is often the right next step. If you cannot yet prove idempotent webhook handling, batch-level reconciliation, and documented hold procedures for returned or blocked funds, keep the stack simpler. Its value comes from control, and that value depends on every delayed, duplicated, held, or returned event resolving into one consistent accounting story.

Vertical-Specific Decision Rules for Rideshare Delivery and Home Services#

Choose by failure pattern, not feature count. Rideshare is often most sensitive to payout delays and event handling, delivery is often most sensitive to settlement and exception or claims-data clarity, and home services is often most sensitive to entity, tax, and evidence traceability.

1. Rideshare should prioritize payout reliability over feature breadth#

If support volume is delay-sensitive, make webhook robustness and idempotent retries your first requirement. Uber states drivers can cash out up to 6 times a day, and Lyft supports five times every 24 hours, so duplicate or delayed payout events quickly become support incidents.

Use idempotency keys for payout-triggering API requests, and design webhook consumers to handle duplicate and out-of-order events. Also account for undelivered webhook retries for up to three days. A practical check is to replay the same payout event twice and confirm one accounting effect and one payout state transition.

2. Delivery should require settlement and exception clarity before partner-led rollout#

If delivery margins are tight, require contract-level clarity on settlement timing, billing artifacts, and exception or claims handling before committing volume to partner-led networks such as Uber Direct or Roadie.

Uber Direct says dashboard deliveries are billed daily in a single invoice. Uber for Business also provides reconciliation and compliance reporting, plus monthly CSVs generated on the first of every month for prior-month transactions. Roadie documentation references webhooks, status, return and cancellation codes, and its claims flow includes complete loss, partial loss, and damage. Before launch, verify that daily billing, periodic reporting, and exception or claims data can be joined to your internal payout reconciliation records.

3. Home services should prioritize KYB, VAT handling, and evidence traceability#

When your model depends on legal-entity onboarding and post-service documentation, prioritize KYB, VAT invoicing handling, and traceable evidence records. In the US, beneficial-owner verification for legal-entity customers is required under 31 CFR §1010.230 for covered financial institutions. In the EU, VAT-registered businesses follow a common baseline of VAT invoicing rules.

Your control check should tie together the provider legal-entity record, beneficial-owner verification result where applicable, invoice or VAT artifact, service evidence, payment object, and ledger entries. Transaction-level settlement reporting should support adjustment tracing when disputes or corrections appear later.

| Vertical | Dominant pressure | KYC/KYB depth to prioritize | Payout cadence to design for | Reconciliation checkpoint |

|---|---|---|---|---|

| Rideshare | Delay-sensitive worker support | Identity and payout-eligibility controls | Multiple same-day cashout requests | Deduplicate webhook events, enforce idempotent retries, and confirm one payout action maps to one ledger outcome |

| Delivery | Settlement clarity and exception handling | Eligibility and partner-responsibility controls | Daily billing plus periodic reporting cycles | Match operational events to daily invoices, monthly CSVs, and exception or claims records |

| Home services | Entity, tax, and evidence traceability | KYB for legal entities, including beneficial-owner procedures where required | Controlled release after evidence and tax checks | Tie entity records, VAT or invoice artifacts, service evidence, settlement detail, and ledger entries into one traceable chain |

When you compare options, ask which stack gives you the controls your exception pattern requires, then validate with real retries, real reporting files, and real evidence records before launch. Related reading: Merchant of Record for Platforms and the Ownership Decisions That Matter.

Implementation Sequence for the First 90 Days#

Use this sequence as your default operating order: set ownership first, automate second, pilot third, and have finance certify last. That order helps you avoid going live with payout volume you cannot explain when a webhook fails, a tax form is missing, or a hold appears while funds are still pending.

| Phase | Key control | Checkpoint |

|---|---|---|

| Phase 1 | Assign owners for Form W-9, Form W-8BEN, beneficial-owner verification under 31 CFR §1010.230, and VAT by market | Sample five worker or provider records and verify which form applies, who reviewed it, and whether payout is blocked if required documentation is missing |

| Phase 2 | Use idempotency keys on payout-triggering POST requests; for providers with this documented window, a retry with the same key is safe within 24 hours; account for funds moving from pending to available | Replay the same event twice and confirm one accounting effect and one state transition; include undelivered-event recovery for up to three days |

| Phase 3 | Treat the batch ID as a control object; one API may support up to 15,000 payments per call and reject reused sender_batch_id values seen in the last 30 days | Explain unmatched inbound funds, held balances, and returns after payout creation |

| Phase 4 | Use a payout reconciliation report, implement the Form 1099-NEC workflow where applicable, and escalate FBAR and FEIE fact patterns | Trace a payout through the reconciliation report, confirm the tax form on file, and determine whether it belongs in a 1099-NEC workflow where applicable |

1. Phase 1 sets the responsibility map#

Phase 1 is complete only when each control has a named owner and a documented dependency on a vendor, bank partner, or internal team. For platform businesses, worker classification and tax reporting or withholding obligations are core operating controls, not month-end cleanup.

Keep the onboarding split explicit. Collect Form W-9 for U.S. payees and handle Form W-8BEN for foreign beneficial owners. If legal entities are involved, contract-map who handles beneficial-owner verification where a regulated institution requires it under 31 CFR §1010.230. Do not assume that responsibility always sits with the platform.

Treat VAT the same way. Define responsibility market by market, not as one global rule. EU cross-border B2C VAT rules changed on 1 July 2021, which is a practical reminder that jurisdiction can change ownership and process design.

Checkpoint: sample five worker or provider records and verify, from the record alone, which form applies, who reviewed it, and whether payout is blocked if required documentation is missing.

2. Phase 2 makes asynchronous flows trustworthy#

Phase 2 should make asynchronous payout operations reliable under retries, delays, and duplicate events. Build around API requests, webhook endpoints, and ledger posting rules.

Use idempotency keys on payout-triggering POST requests from day one. For providers with this documented window, a retry with the same key is safe when it happens within 24 hours, and a modified request needs a fresh key. This is a control, not an optimization.

Map payout state transitions before ledger wiring. Where balance timing matters, account for funds moving from pending to available instead of assuming immediate availability.

Checkpoint: replay the same event twice and confirm one accounting effect and one state transition. Include undelivered-event recovery. Some providers resend for up to three days, so deduplication and queue-based recovery should be in scope.

3. Phase 3 pilots scale mechanics, not just happy paths#

Phase 3 should validate settlement behavior and exception handling, not just successful payout creation. Keep pilots narrow enough that you can inspect each failure path.

If you use Payout Batches or another payout rail, run it in a controlled lane first. For batch payouts, treat the batch ID as a control object. One API may support up to 15,000 payments per call and reject reused sender_batch_id values seen in the last 30 days. Even when provider rules differ, you still need traceability for included, failed, returned, and unresolved payments.

For any new payout rail, test matching and exception handling before broad rollout. Your team should be able to explain unmatched inbound funds, held balances, and returns after payout creation.

4. Phase 4 certifies finance outputs and document hygiene#

Rollout is not complete until finance can reconcile and report without manual investigation. A payout reconciliation report should let finance match transactions in each settlement batch and tie them to internal ledger journals and payout states.

If contractor or nonemployee payouts are in scope, implement the Form 1099-NEC workflow in this phase. For cross-border users, keep routing guidance clear. FBAR and FEIE are fact-pattern dependent, but teams should know when to escalate. For example, FBAR can apply when aggregate foreign account value exceeds $10,000, and FEIE physical presence includes 330 full days during 12 consecutive months in a foreign country.

Final checkpoint: finance should be able to pick a payout, trace it through the reconciliation report, confirm the tax form on file, and determine whether it belongs in a 1099-NEC workflow where applicable.

Red Flags That Should Pause Expansion#

Pause expansion if finance cannot trace and explain payouts from system records alone. Small control gaps can become recurring payout, tax, and support issues as volume grows.

| Red flag | Pause when | Check |

|---|---|---|

| Broken transaction traceability | A single payment cannot be traced from the original request to the provider reference and into your ledger journals without spreadsheet stitching | The API request identifier, webhook event, payout or transfer reference, and journal entry align in your records |

| Silent ownership in partner contracts | Contracts do not clearly assign ownership for payout failures or delayed settlement across partner rails | Settlement timing, escalation paths, and who makes the customer whole are written in the contract or operating appendix |

| Tax and identity records that do not survive scale | Records mix up Form W-9 and Form W-8BEN, or Form 1099-K readiness depends on cleanup later | Sample five records and confirm form type, reviewer, and missing-document behavior; do not treat the $20,000 and 200 transactions Form 1099-K threshold as a hard binary |

- Broken transaction traceability. Pause when a single payment cannot be traced from the original request to the provider reference and into your ledger journals without spreadsheet stitching. Reconciliation depends on preserving the transaction-to-payout link, and provider reporting often includes transaction-level IDs to support that control.

Test one live payment end to end. The API request identifier, webhook event, payout or transfer reference, and journal entry should align in your records. If they do not, you are likely to rely on manual investigations for delays and disputes. Webhook drift is a known failure mode because events are asynchronous, undelivered events are retried, and missed events may need to be queried later. Weak duplicate-safe posting can create two ledger effects for one payout state.

- Silent ownership in partner contracts. Pause when contracts do not clearly assign ownership for payout failures or delayed settlement across partner rails. Oversight expectations still apply for service-provider relationships, and third-party risk can apply by contract or otherwise, so vague language does not remove accountability.

Confirm exception ownership is written, not assumed. Check the contract or operating appendix for settlement timing, escalation paths, and who makes the customer whole when funds are stuck between parties. If support asks why a payout is missing and ops can only say "we are waiting on the partner," you are not ready to add markets.

- Tax and identity records that do not survive scale. Pause when records mix up Form W-9 and Form W-8BEN, or when downstream Form 1099-K readiness for U.S. reporting depends on cleanup later. Form W-9 provides taxpayer identification data for IRS information returns, and Form W-8BEN is submitted by foreign beneficial owners when requested by the payer or withholding agent.

Validate that onboarding enforces payout blocking and reporting readiness. Sample five records and confirm form type, reviewer, and missing-document behavior. For U.S. reporting, do not treat the $20,000 and 200 transactions Form 1099-K threshold as a hard binary, because a payee may still receive Form 1099-K below that level.

Conclusion#

The stack that holds up is the one your team can operate and audit under stress, not the one with the strongest demo. A practical starting point is a deliberately scoped architecture that keeps compliance ownership, payout execution, and reconciliation explicit from day one, then expands only after pilot testing exposes real failure paths.

1. Put ownership in writing before feature scope#

Decide who is legally and operationally responsible before you buy features. If you choose a Merchant of Record, confirm the contract names the entity legally responsible for processing customer payments. If you use a PSP with your own payout layer, verify how charge type and negative-balance responsibility determine dispute handling and account-level financial impact, including who is debited.

If legal, finance, and payments teams would answer "who responds, who is debited, and who absorbs the loss?" differently, that route is not scale-ready.

2. Keep KYC, KYB, AML, and exception handling visible#

Treat verification and compliance gating as explicit launch controls. In some platform setups, users must be verified before payments are processed or funds are paid out, and AML assumptions should be rechecked per market rather than copied forward. FATF recommendations change over time, shown as amended in October 2025, so date-checking policy assumptions is part of rollout discipline.

Operationally, you should be able to point to the exact document, field set, or status that blocks payout release. If you cannot, exception ownership is still too implicit.

3. Treat reconciliation and async events as launch gates#

Reconciliation is a control for transaction accuracy, not just accounting cleanup. Keep a trace from request and provider reference through webhook-driven state changes to reconciliation outputs and payout records. Where available, use a payout reconciliation report to match bank payouts to included transaction batches.

Webhook events and idempotency are reliability mechanisms in asynchronous payment flows. Pilot testing should include undelivered events, retry paths, and negative-balance scenarios so you validate operations beyond the happy path.

Build a vertical-by-market decision matrix that names, for each route, the compliance owner, payout cadence, reconciliation artifact, and failure owner. Then pressure-test a pilot route and use the results as input, not proof, before broader rollout.

If you are finalizing a multi-market rollout plan, review Gruv's Payouts overview to map batch controls, status tracking, and reconciliation into your operating model.

Frequently Asked Questions

What does on-demand payments mean for delivery and rideshare platforms in practice?

In practice, on-demand payments are asynchronous operations, not just checkout logic. You are often managing customer payment acceptance and worker payouts at the same time, with status changes arriving through webhook events. To keep operations reliable, maintain a clear trace from the original API request through payout or transfer records and into reconciliation records.

What are the minimum payment capabilities required before entering a new country?

At minimum, your onboarding flow must collect verification data based on legal entity type and operating country because payout eligibility is country-specific. Teams usually pair that with duplicate-safe retries via idempotency keys, webhook handling for asynchronous updates, and transaction-level reconciliation outputs such as a settlement details report. If KYC requirements are incomplete, the market is not launch-ready.

How do delivery and rideshare payout operations differ day to day?

The operational differences usually show up in payout cadence and fee mechanics. Public program examples show cash-out availability up to 6 times each day for Uber drivers and delivery people in the US, while DoorDash Fast Pay is positioned as daily cash-out for a $1.99 fee. For operators, that means payout configuration and support workflows should be tuned by model and market, not copied across both.

When should a platform choose Merchant of Record (MoR) instead of building in-house controls?

Choose MoR when you want a single entity to be legally authorized to process payments and carry core transaction compliance responsibility. MoR can simplify responsibility placement, but it is not a blanket escape from operational oversight. Before you commit, verify contract ownership for payouts, refunds, chargebacks, and reporting boundaries.

What should founders verify in vendor contracts before committing roadmap and GTM spend?

Confirm who is liable for chargebacks and related costs, since marketplace structures can still leave the platform liable. Verify settlement timing, whether flows are netted weekly or handled separately, what reconciliation files or reports are delivered, and who owns payout failures or delayed settlement. If those controls are vague in the contract, rollout risk is higher than it looks in a demo.

Which payment details are usually missing from partner landing pages and demos?

Common gaps include implementation details: retry behavior, rate-limit handling, webhook redelivery behavior, payout failure states, and reconciliation depth. Some docs explicitly require clients to honor Retry-After headers, and webhook deliveries can be retried for up to three days when delivery fails. If a demo cannot show duplicate-safe retries and recovery for undelivered events, you are still looking at marketing-level detail rather than production readiness.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- consumerfinance.gov/compliance/advisory-opinion-programtrusted

- consumerfinance.gov/about-us/newsroom/cfpb-proposes-interpretive...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- ecfr.gov/current/title-31/subtitle-B/chapter-X/part-1...trusted

- federalregister.gov/documents/2025/12/23/2025-23735/truth-in-len...trusted

- files.consumerfinance.gov/f/documents/cfpb_earned-wage-access-advisory...trusted

- files.consumerfinance.gov/f/documents/cfpb_ao-rescinding-earned-wage-a...trusted

- irs.gov/businesses/small-businesses-self-employed/re...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Contractor Advance Payments for Platforms Without Taking Credit Risk

For platform operators, the real decision is control quality, not payout speed. Paying before delivery only works when each release is tied to verified approval evidence and a complete document trail.

Airline Delay Compensation Payments for Customer Experience and Control

If you are evaluating an `airline compensation payments customer experience delays platform`, split the work into three lanes first: legally owed refunds, discretionary compensation, and outsourced claims recovery. Vendor pages often blur these together, but they lead to different policy choices, ledger treatment, and customer outcomes.

When BNPL Helps B2B Services Platforms and When It Hurts Margin

Treat BNPL as a unit-economics decision first, not a checkout feature. For B2B services platforms, faster closes may help, but fees, disputes, and risk-management work can wipe out the upside if you do not model them up front.