Quick Answer

Define the operating boundary first: name the contracting entity, the party that issues payout instructions, and the partner that actually moves funds. Then test that design against Exchange Business Regulation C 7/2025 and Article (65) before committing build or GTM scope. Use WPS and SIF as internal control references for data quality and traceability, not as automatic contractor-payment permission. If UAEFTS or AMLSCU coverage is not confirmed for your exact flow, mark it unknown and restrict launch to documented cases only.

Know when WPS applies and when it does not#

Before You Start#

Write down the exact flow you want to launch in the United Arab Emirates: who contracts with the worker, who holds funds, who instructs the payout, and where the money actually moves. If you cannot explain it on one page, you are not choosing a payout feature yet. You are still defining a regulated operating model.

Step 1 Define the decision as compliance plus operations#

The fastest way to make a bad UAE expansion call is to treat contractor payouts like a vendor feature comparison. Start with a simpler question: does your proposed flow stay inside a narrow contractor-payment scope, or does it start to look like employee payroll, money transfer, or another regulated activity?

That matters early because the Central Bank of the UAE requires exchange business activities in the UAE to be subject to a licensing regime. Under the Exchange Business Regulation, licensed financial activities under Article (65) include currency exchange and money transfer services. If your model starts to look like you are providing the transfer service yourself, or operating beyond a software role, that is a threshold issue, not a later implementation detail.

Use one quick check: identify the legal entity that contracts with the worker, the party named on the payout instruction, and the partner that actually moves funds. If any of those three are unclear, pause the launch decision.

Step 2 Anchor your plan in what is known, not what sales decks imply#

This guide uses Wage Protection System, or WPS, as a payroll compliance reference point because it helps expose where contractor flows may look employee-like. It does not assume WPS defines contractor payout rules, and it does not treat a WPS-shaped process as automatic permission to pay contractors that way.

Use the same caution with UAEFTS and AML language. Public material confirms that the UAE Funds Transfer System is the national RTGS system operated by the Central Bank. It also confirms that the Central Bank's Standards for the Regulations Regarding Licensing and Monitoring of Exchange Business set baseline requirements for exchange houses, which are required to comply with those Standards at all times. Version 1.20 from November 2021 includes an Anti-Money Laundering Compliance section. What those sources do not do is fully specify your platform requirements for UAEFTS or confirm AML obligations for your exact contractor model.

A common failure mode is promising "UAE-ready" coverage because a bank partner or vendor mentions local rails. That is not enough evidence for product scope, customer claims, or launch timing.

Step 3 Use the rest of this guide to make a go or no-go call#

The goal here is practical: decide whether you can launch now, what must be built first, and what should stay explicitly out of scope. By the end, you should have a documented boundary between contractor payouts and payroll, a short evidence pack for vendor and legal review, and a list of open questions that block launch until verified.

If that sounds narrower than your initial plan, that is usually a good sign. In the UAE, disciplined scope beats optimistic coverage.

We covered a similar operator workflow in How Platform Operators Pay Contractors in Colombia with PSE Nequi and DIAN Controls.

Set the legal scope before building payout flows#

Step 1 Separate contractor payouts from payroll before you promise anything. If your launch plan in the United Arab Emirates starts to look like employee pay, pause product and go-to-market commitments and get legal review first. This is not just a labor-label question. The Central Bank of the UAE's Exchange Business Regulation, C 7/2025 (effective 26/6/2025), treats money transfer services as a licensed financial activity, so scope drift can become a licensing question too.

Use a simple checkpoint for each payout use case: who hires the worker, who approves the amount, who instructs the payment, and whether the payment is framed as payroll or a contractor invoice settlement. If that chain is muddy, you do not have launch scope yet.

Step 2 Use Central Bank licensing boundaries as your reference, not as proof your contractor flow is allowed. The Central Bank framework covers license decisions, ongoing supervision, examinations, and sanctions for licensed persons, and it may impose additional requirements beyond listed minimums. Your job is to document where your model stays outside regulated exchange-business scope and where it starts to resemble it.

That memo should name the exact features that stay out of scope for now and the triggers for legal re-review. The common failure mode is simple: a team says it can pay contractors because it supports bank transfers, then quietly builds payroll-shaped controls around those transfers.

Step 3 Escalate employee-like patterns early and write the boundary memo. If role design, platform control, or payment cadence starts to look employee-like, escalate before launch. Do not wait for vendor onboarding.

Your internal memo should list:

- allowed use cases that run through bank transfers

- excluded cases pending review

- jurisdictions and entities in scope

- the owner for legal and compliance signoff

If you cannot keep that memo current, your scope is not stable enough to build.

Related: How to Pay Contractors in Mexico: SPEI CoDi and SAT Compliance for Foreign Platforms.

Prepare the UAE evidence pack before vendor demos#

Build this evidence pack before provider demos. Otherwise, you risk choosing a vendor before your launch scope is defensible.

Step 1 Build the minimum pack around scope, not vendor features#

Start with what you are operating, not what a provider can demo. Under the Central Bank of the UAE Exchange Business Regulation C 7/2025 (effective 26/6/2025), Exchange Business activities are in a licensing regime, and Article (65) includes money transfer services among licensed financial activities.

Include, at minimum:

- entity setup context for each UAE entity and free-zone presence in scope

- target user types, including who is treated as a contractor and which employee-like cases are excluded

- contract templates or template families you plan to use

- payout methods in scope now (for example, bank transfers) and any methods explicitly excluded or escalated

- exception paths for returned payments, identity mismatches, amount disputes, and holds pending review

A useful check: an outside reviewer should be able to tell who is paying, on what contractual basis, and through which method without a meeting.

Step 2 Assign one owner per artifact#

Assign clear ownership across Product, Payments Ops, and Compliance for every artifact. The Standards in force as N 35/2018 are legally binding, and the Central Bank may impose additional requirements beyond listed minimums, so ownership gaps can turn into audit gaps.

Keep ownership practical and explicit:

- Product: user-type definitions, onboarding fields, payout state labels

- Payments Ops: payout method setup, exception handling notes, reconciliation evidence

- Compliance: contract-template approval, escalation criteria, and the scope rationale for included vs excluded flows

Each artifact should show version date, owner, and latest legal/compliance signoff.

Step 3 Set stop rules before onboarding starts#

Define no-go rules before onboarding starts. If required onboarding data, contract documentation, or payout instruction details cannot be captured reliably at the start, pause rollout instead of relying on manual fixes later.

Set one strict traceability rule: every payout state change must be explainable from request to final status. Your records should make it possible to trace the request, approval, instruction, any return or hold, and final disposition.

Compare payout path options and where compliance load sits#

Choose the payout path only after ownership is explicit. When onboarding fails, a classification call is disputed, or a payout is held, you should be able to name who does the work and who can prove it. If ownership is unclear, do not move to build.

Step 1 Map ownership before comparing speed#

Start with accountability, not feature lists. A direct model and an EOR-supported model can distribute work differently, but the Central Bank sources here do not define that split for you. Your team has to define it in writing.

Use the same regulatory anchor for either path. Under Exchange Business Regulation C 7/2025 (effective 26/6/2025), Exchange Business activities in the UAE are under a Central Bank licensing regime, and Article (65) lists licensed financial activities. The Standards N 35/2018 are legally binding, and Exchange Houses operating in the UAE must comply with all Standards requirements at all times.

Use this as an internal scoring table, not a legal allocation table:

| Decision area | Direct platform model | EOR support | What to verify now |

|---|---|---|---|

| Onboarding and contract records | Your team carries more of the process design and evidence handling | Partner may carry more worker-facing process steps | Exact data fields, document set, and cure path for incomplete records |

| Classification and scope decisions | More internal control over edge cases | More reliance on partner process definitions | Who approves edge cases and where that decision is recorded |

| Payment exceptions | More internal handling of returns, holds, retries, and changes | More partner handling of day-to-day exception flow | A real exception trace from request to final disposition |

| Review-ready evidence | More internal burden to maintain full trails | Evidence may be split across systems | Export access, retention expectations, and named owners |

Step 2 Score control against speed#

Treat this as a capability decision, not a preference decision. A model with more internal control also requires stronger internal ownership for evidence, approvals, and escalation handling. A model that accelerates entry usually depends more on partner process boundaries.

Set one checkpoint before go/no-go: if your team cannot consistently reconstruct who approved what, when a payout changed state, and how a hold was resolved, your compliance load is not operationally contained yet.

Step 3 Gate launch scope by confirmed jurisdiction#

For Dubai and each free zone in scope, require separate written confirmation of operating ownership. The sources used here do not provide free-zone-specific carve-outs, and they do not define MoHRE process ownership details for your model choice.

Use a hard gate: if you cannot name the contracting entity, the payment-operating entity, and the evidence owner for each jurisdiction in scope, pause expansion and launch only where ownership is fully documented.

Build the WPS data layer as if audits will happen#

Build this layer as an audit record from day one, not as a disposable import step. For UAE payout flows that may touch exchange-business activity, that posture is safer because Exchange Business Regulation C 7/2025 (effective 26/6/2025) sits inside a Central Bank licensing regime, and Standards N 35/2018 are legally binding and can be supplemented with additional requirements.

Step 1 Model a controlled internal record, not a pass-through file#

Translate each WPS/SIF input into a canonical internal record you control, version, and can explain later. For every value you keep, store provenance: where it came from, when it entered the system, and who changed it through an approved path. If you cannot trace an outbound value back to a specific input version and actor, your data layer is not audit-ready.

Step 2 Enforce sequence: validate, approve, release, reconcile#

Use a strict order of operations: validation first, approval gating second, payout instruction third, reconciliation and exceptions last. This is an internal control design choice, not a published CBUAE or MoHRE workflow mandate. If a payload fails your validation rules, block release and route it to named owners. Do not patch around failures in production.

Step 3 Make each run exportable as evidence#

Require a per-run evidence bundle that ties approved inputs to final outputs, plus validation outcomes and operator actions. That discipline matters because the Central Bank framework allows additional requirements beyond minimum listed items, and the Standards require ongoing compliance for Exchange Houses in scope. Operational checkpoint: if your team cannot export one complete run quickly, including failed records and ownership history, you still have an audit gap.

Close UAEFTS and AMLSCU uncertainty with explicit launch gates#

Do not turn unverified acronyms into product promises. For UAE launch decisions, treat UAEFTS and AMLSCU as unknowns until you have current, named confirmation for your exact payout flow.

Step 1 Separate confirmed rules from missing confirmation#

Start by separating confirmed regulatory posture from unconfirmed feature coverage. From the materials in hand, you can confirm that Exchange Business in the UAE is under a Central Bank licensing regime, Regulation C 7/2025 is in force from 26/6/2025, Standards N 35/2018 are legally binding, the Standards include "D. Anti-Money Laundering Compliance," and the Central Bank may impose requirements beyond listed minimums.

| Area | What is stated | What is still unverified |

|---|---|---|

| Licensing posture | Exchange Business in the UAE is under a Central Bank licensing regime; Regulation C 7/2025 is in force from 26/6/2025 | Whether your exact contractor flow stays outside regulated exchange-business scope |

| UAEFTS | UAE Funds Transfer System is the national RTGS system operated by the Central Bank | Current UAEFTS requirements for contractor payout flows |

| AML standards | Standards N 35/2018 are legally binding and include "D. Anti-Money Laundering Compliance" | AMLSCU obligations or thresholds |

| Coverage claims | Mentions of local rails or "supported" statements are not enough evidence for product scope, customer claims, or launch timing | Coverage for any specific platform, bank, exchange house, or processor without a dated source and named confirmation |

What current guidance does not confirm is just as important. Current UAEFTS requirements for contractor payout flows, AMLSCU obligations and thresholds, and UAEFTS/AMLSCU coverage for any specific platform, bank, exchange house, or processor all require direct verification with the relevant authority.

Use a blunt checkpoint: if a claim in your sales narrative has no dated source and named confirmation, mark it as unknown.

Step 2 Build a verification track before go to market#

Create one reviewable verification log before any external claim goes live. Track: claim tested, date captured, internal owner, external party asked, exact answer received, evidence location, and recheck date.

Assign clear ownership: Product for scope wording, Compliance for interpretation risk, and Payments Ops for operational feasibility. If a partner says "supported," require the exact scope in writing rather than treating the statement as universal coverage.

Do not treat demos, marketing one-pagers, or older report references as launch confirmation.

Step 3 Gate launch on materiality, not optimism#

Apply a hard rule: if UAEFTS or AMLSCU obligations materially affect the target flow and confirmation is missing, launch a restricted scope or defer entry.

In practice, that means enabling only flows already validated through your licensed path and excluding flows that depend on unconfirmed assumptions. Your launch memo should list excluded cases and the reason for each exclusion.

If a control is unknown, state that directly.

Step 4 Mark roadmap controls as policy-gated#

Label controls as either available now or policy-gated "when enabled." Use the same label in product notes, ops procedures, and customer-facing materials so roadmap intent is not mistaken for current compliance coverage.

Keep one line clear: current capability versus future dependency. If UAEFTS or AMLSCU handling is not verified for your model, do not sell through that gap.

Implement operational controls that prevent silent payout risk#

Once you have gated scope and unknowns, make silent payout failure impossible to ignore. In the UAE, exchange-business activity sits under CBUAE supervision, and the in-force framework (including binding Standards N 35/2018 and Regulation C 7/2025 effective 26/6/2025) covers risk management, AML compliance, and customer protection. The excerpts here do not prescribe exact payout-control mechanics, so define them explicitly in your operating model before full-volume launch.

Step 1: Make retries safe by design. Set one stable payout identifier per intended transfer and require replayed requests to return the original outcome rather than create a second transfer. Validate this with timeout-and-replay testing across your ledger and provider records.

Step 2: Define operator-owned payout states. Use clear states (for example: credited, held, returned, under investigation) with a named owner and next action for each non-final case. If a state has no owner, exceptions will age silently.

Step 3: Place AML checks at release points and keep auditable records. Where your policy stack supports AML controls, apply them before withdrawal release and before payout submission. Keep decision logs that are reviewable while masking sensitive fields in routine operational views.

Step 4: Reconcile on a fixed cadence before close. Match payout events to ledger records on a named schedule with visible exceptions for Finance and Operations. Your readiness test is simple: trace one payout end-to-end from request to final state using your own records only.

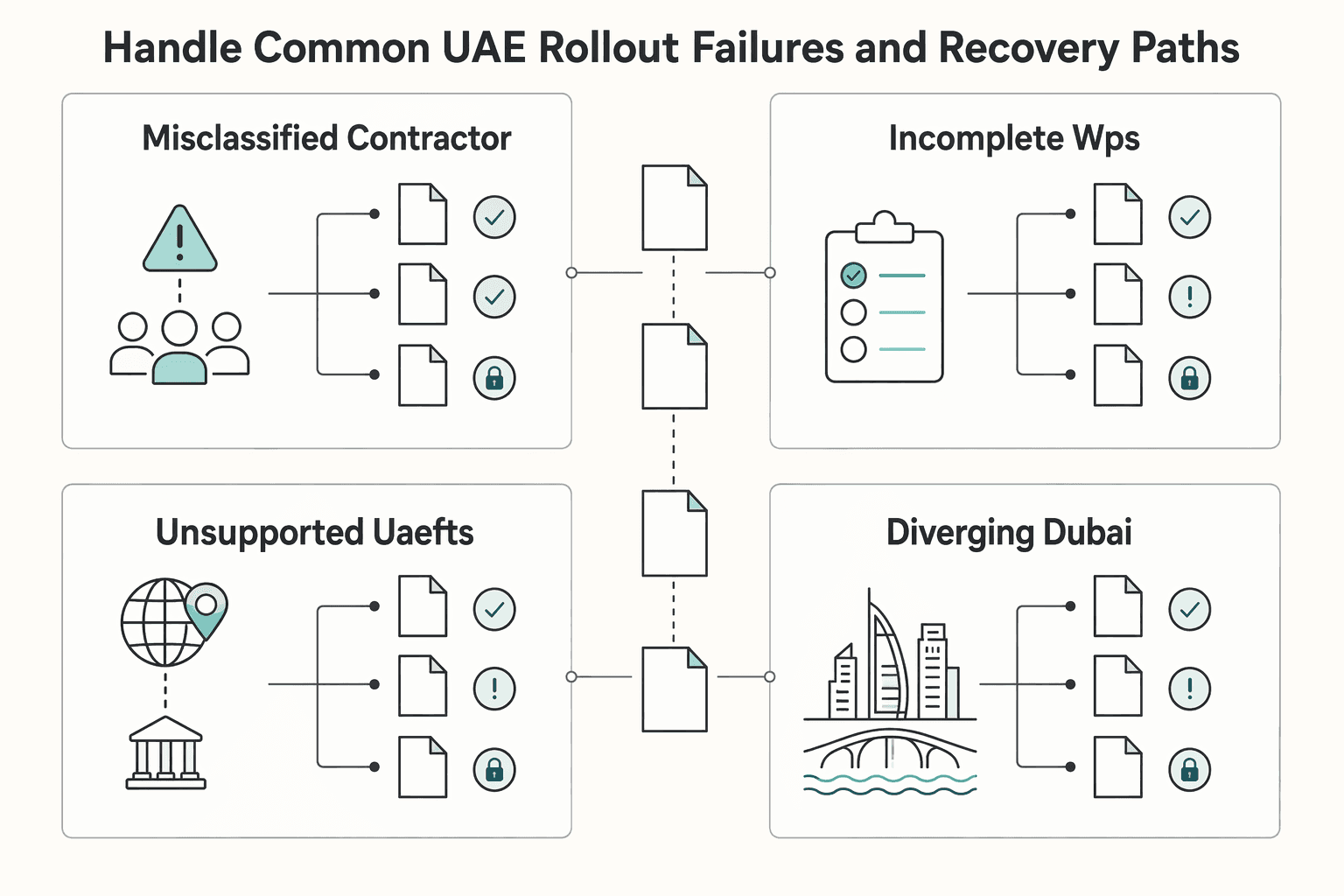

Handle common UAE rollout failures and recovery paths#

When a UAE rollout issue changes classification, submission basis, or jurisdiction logic, pause the affected flow first and repair the underlying records before you resume payouts. CBUAE materials support a strong supervision context, including examination and sanctions powers over licensed persons, but they do not provide a contractor-payout rescue script, so your recovery path needs explicit internal rules.

| Issue | Immediate action | Record to keep |

|---|---|---|

| Misclassified contractor group | Stop that group's payouts, mark related items as on hold, and send the full set for Legal and Compliance review | A record of what changed and who approved it |

| Incomplete WPS or SIF input data | Reject before submission, fix source records, and rerun through a controlled approval path tied to the corrected input version | The original extract and corrected version in the same audit trail |

| Unsupported UAEFTS or AMLSCU readiness claim | Pull it from launch materials and log it as a known unknown with owner, verification target, and decision date | The known-unknown entry with owner, verification target, and decision date |

| Diverging Dubai and free-zone logic | Route them separately and assign distinct ownership, approval, and escalation paths | A record that shows which path applied and why |

Step 1 Freeze misclassified flows and re-approve the affected population. If a contractor group appears misclassified, stop that group's payouts, mark related items as on hold, and send the full set for Legal and Compliance review. Clear only the payouts tied to the reviewed and approved classification outcome, with a record of what changed and who approved it.

Step 2 Block incomplete WPS or SIF submissions at pre-submit validation. If your process uses WPS/SIF files and required input data is incomplete, reject before submission, fix source records, and rerun through a controlled approval path tied to the corrected input version. Keep the original extract and corrected version in the same audit trail rather than patching rows ad hoc.

Step 3 Remove unsupported UAEFTS or AMLSCU readiness claims. If a readiness claim cannot be evidenced, pull it from launch materials and log it as a known unknown with owner, verification target, and decision date. This is a risk-control step: the Exchange Business Regulation (C 7/2025, effective 26/6/2025) allows the Central Bank to impose additional requirements beyond listed minimum items.

Step 4 Split handling when jurisdiction logic diverges. If one operating policy no longer fits both Dubai and free-zone cases, route them separately and assign distinct ownership, approval, and escalation paths. The key test is operational clarity: from the record alone, an operator should be able to tell which path applied and why.

Make the go or no-go call with a copy-paste checklist#

Use this as a hard gate: if any item is still assumed, treat launch as no-go or narrow scope to what you can prove today.

- Confirm scope boundaries are documented and approved.

Keep a dated legal boundary memo that states which flows you treat as contractor payouts, which flows are excluded, and when to escalate for review under UAE Labor Law. Do not rely on product assumptions to define this boundary.

- Confirm your jurisdiction map is explicit for Dubai and each in-scope free zone.

Write down where you are launching now, where you are not, and who approved that scope. If coverage is partial, keep customer-facing claims equally specific.

- Confirm WPS/SIF handling is modeled, validated, and auditable.

These materials do not provide a field-level WPS/SIF spec, so avoid guessing required fields. Use your approved spec, validation rules, approval record, and retained outputs as the control baseline.

- Confirm UAEFTS and AMLSCU status is either verified or clearly unknown.

For exchange-business exposure, validate against the Exchange Business Regulation C 7/2025 (effective 26/6/2025), Standards N 35/2018, and Article (65) on Licensed Financial Activities. These sources confirm licensing, supervision, and enforcement for exchange business, and that the Central Bank may impose additional requirements; they do not, by themselves, confirm platform-specific UAEFTS or AMLSCU obligations.

- Confirm the operating model and escalation ownership are named.

Whether you run direct or via an EOR path, assign owners for classification issues, payout approvals, exception response, and customer communications. If ownership is unclear, the model is not launch-ready.

- Confirm payout controls exist for retries, exceptions, reconciliation, and audit exports.

You should be able to show what changed, who approved it, and where the record lives for each state change. Launch only the cases your current controls can support.

- Confirm launch scope, exclusions, and claims are aligned.

Your launch file, ops playbook, and go-to-market language should match the same verified reality, with unknowns labeled as unknown.

Related reading: How Platform Teams Pay Contractors Across UAE, Saudi Arabia, and Egypt.

Frequently Asked Questions

Is WPS mainly for employee payroll, and how should platforms treat contractor payouts differently?

These materials do not establish whether WPS treatment for employee payroll extends to contractor payouts. Use a classification-first check, and if a payout flow looks employee-like in control, cadence, or obligation, pause and route it for legal review instead of forcing it through a contractor setup.

What fields from a Salary Information File matter most when designing payout data models?

The public materials used for this section do not provide a field-by-field Salary Information File (SIF) specification, so do not build from assumptions. Build from your approved file specification, and keep a versioned extract, approval record, and final output for each run.

Who reviews WPS-related payroll information in the UAE process context?

These sources do not identify a named reviewer for WPS payroll files, so avoid claiming that a specific agency or team checks each file in a defined way. What is confirmed is broader. The Central Bank framework includes licensing, ongoing supervision, examination, and sanctions for licensed persons. The 2021 annual report also references supervision of AML and CFT measures as well as supervision of payment systems and exchange houses.

What is actually confirmed versus still unclear about UAEFTS requirements for platforms?

Confirmed: under the Exchange Business Regulation, C 7/2025 effective from 26/6/2025, exchange business activities in the UAE are subject to a Central Bank licensing regime, and the legally binding Standards N 35/2018 supplement that regulation. Not confirmed from these materials: whether your platform’s contractor payout model triggers UAEFTS-specific requirements, or what exact platform obligations would apply. If you cannot show dated external confirmation, mark UAEFTS as unverified in launch materials.

How should operators handle AMLSCU-related uncertainty before committing go-to-market claims?

Do not promise AMLSCU support without documented confirmation, because AMLSCU-specific obligations, thresholds, and approval steps require verification with the relevant authority. Keep a known-unknown log with owner, question, evidence target, and decision date, and require written confirmation before Sales or Partnerships uses AMLSCU language. The checkpoint is simple: can you attach a dated document to the claim?

When should a platform choose an Employer of Record (EOR) path instead of direct local operations?

These sources do not answer that choice directly, so do not present EOR as regulator-endorsed or required based on this material alone. As an operating rule, evaluate EOR when you cannot clearly assign responsibility for classification, payroll-adjacent data handling, local approvals, and exception response. If ownership is fuzzy, a direct model is not ready.

What evidence should be ready before launching in Dubai or across multiple free zones?

Have a jurisdiction-specific evidence pack ready before launch: contract templates, classification memo, payout method, approval owners, exception handling, and any dated confirmations tied to UAEFTS or other claims. Dubai and free-zone implementation rules require direct verification with the relevant authority, so your internal record has to do the work. A good verification test is whether an operator can show, from the file alone, which jurisdiction path applied and why.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 5 external sources outside the trusted-domain allowlist.

- centralbank.ae/media/gizhn4zk/cbuae-annual-report-2021.pdfexternal

- centralbank.ae/media/um1brhvo/cbuae-annual-report-2016-en.pdfexternal

- financialprofessionals.org/docs/default-source/default-document-library...external

- rulebook.centralbank.ae/sites/default/files/en_net_file_store/CBUAE_...external

- rulebook.centralbank.ae/en/entiresection/100external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Pay Contractors in Peru with Yape, PLIN, and SBS Checks

Treat Peru as a posture decision, not just a rail decision. If you choose a local wallet-style method first, then sort out contractor status, tax data, and evidence later, you may get a smoother payout experience. You also raise launch risk in areas that are much harder to fix once money starts moving.

Pay Contractors in Mexico: SPEI, CoDi, SAT, and CFDI Decisions for Platforms

Mexico contractor payouts usually break for a simple reason: teams launch from a generic Latin America plan, then discover that payout rail choices, tax steps, and operating structure cannot be separated in practice. If you are evaluating multiple rails and operating models at the same time, you need Mexico-specific decisions before you send the first live payout.

How to Pay Contractors in Kenya with M-Pesa, PesaLink, and KRA Controls

Kenya is worth serious consideration for contractor payouts, but you should not greenlight a launch just because M-Pesa is familiar and PesaLink is on the shortlist. The real decision is practical. Confirm which rail fits your contractor base, put local compliance and tax controls in place before money moves, and keep enough evidence to explain each payout later.