Quick Answer

Opening an Estonian OÜ with e-Residency starts with two baseline state fees: €150 for the e-Residency application and €265 for online company registration. Beyond those charges, plan for provider-priced services such as a contact person and accounting, plus banking setup controls and clear tax and reporting ownership from day zero. e-Residency is a digital identity, not tax residency or citizenship.

Separate e-Residency access from company formation cost#

If you need to assess open estonian company e-residency costs without creating a control gap, start by separating identity access from company formation. Estonian e-Residency is a government-issued digital identity for access to Estonia's business infrastructure. It is not traditional residency, and it does not grant tax residency or citizenship.

This guide is for compliance, legal, finance, and risk owners setting up an Estonian private limited company (OÜ) through e-Residency. The real risk is not the filing itself. It is weak ownership, thin evidence, and no clear escalation path when tax or legal questions come up.

Before you start#

Treat the first phase as a control exercise, not a shopping exercise. Official materials position e-Residency as a way to establish a company online and access e-services, with tax compliance as a core objective. "Fully online" does not remove the need for ownership, evidence retention, and approvals.

If anyone treats e-Residency as a substitute for tax, legal, or citizenship analysis, correct the scope before approving spend. That misunderstanding can surface later in banking, invoicing, and ownership reporting.

Define the card's role first#

Start by defining what the card does, and what it does not do. The digital identity card is the first thing your team will actually use in this process. The application is online, and the card is issued by the Estonian Police and Border Guard Board.

Verification point:

- Name the person who will hold the digital ID.

- Name the internal owner who tracks the application.

- Store application confirmation and payment proof in a controlled folder.

Without those basics, you do not have a clean starting point for company filing or later audit support.

Assign responsibility before the application#

Assign responsibility before anyone clicks "apply." A practical minimum is one accountable setup owner, one finance owner for payment evidence, and one backup approver. This helps avoid a common failure mode: one person submits alone, the receipt stays in a personal inbox, and later no one can show what was paid, by whom, or under which approval.

A minimum evidence pack at this stage:

- Online application confirmation

- Payment receipt

- Payer record, if someone else paid

- Internal approval note

Keep names consistent with how the future OÜ will appear in your internal entity register.

Compare providers only after ownership is clear#

Only after that should you compare setup costs and providers. If a quote bundles statutory items with service fees, treat it as non-comparable until the line items are split.

Cost alone is not enough. You also need a retained evidence trail, a named owner for each recurring obligation, and a clear escalation point when treatment or filing approach is unclear. So before you commit to an application or package, build the pre-filing dossier first. For a related workflow, see How a Freelance Video Editor in Mexico Can Work Compliantly With a California Company.

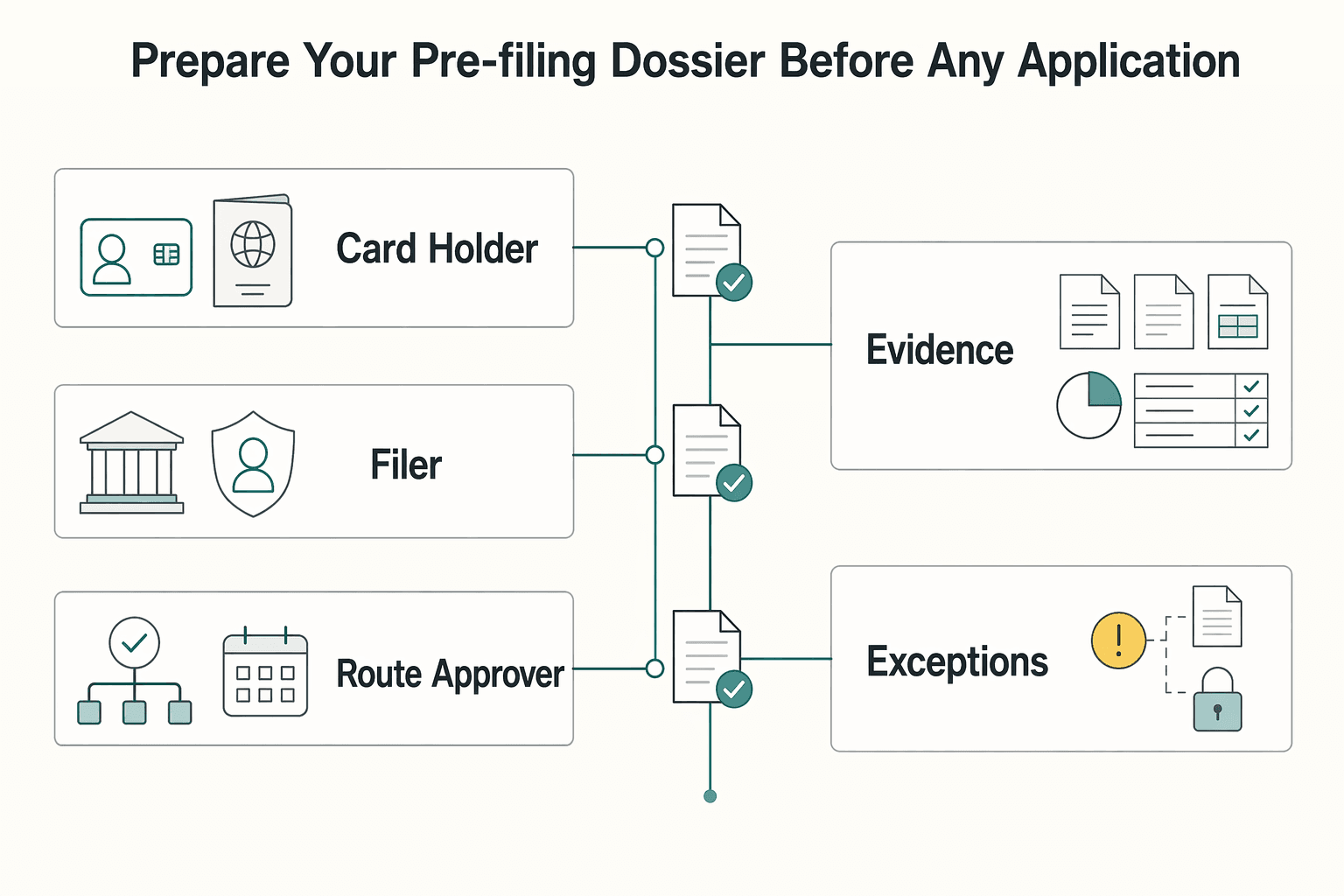

Prepare your pre-filing dossier before any application#

Before anyone pays or files, lock down ownership and evidence in one dossier. Registration can be completed online through the e-Residency service and the e-Business Register. A common internal risk is unclear responsibility, even when online access is available.

| Dossier item | What to record | Verification |

|---|---|---|

| Card holder | Who holds the e-Residency digital ID card | One document clearly answers who holds the card |

| Filer | Who executes filings in the e-Business Register | One document clearly answers who files |

| Route approver | Who approves the filing route | One document clearly answers who signs off |

| Payment evidence owner | Named internal owner of the payment receipt | The dossier contains the receipt and approval record |

| Payer record | Payer identity when different from the applicant | The dossier contains payer identity when different from the applicant |

| Operational escalation owner | Who handles application issues with the relevant authority | Operational escalation is recorded separately from legal escalation |

| Legal escalation owner | Who handles company setup legal questions | Legal escalation is recorded separately from operational escalation |

| Filing verifier | Assigned verifier after submission | Confirms the filing appears in the Estonian company register |

Name the core roles#

Name roles before the application starts. Record who holds the e-Residency digital ID card in your process, who is expected to execute filings in the e-Business Register, and who approves that filing route. Do not assume those roles are held by the same person.

Verification point: one document should clearly answer who holds the card, who files, and who signs off.

Assign payment-evidence ownership#

Assign ownership of payment evidence, not just payment approval. Keep the payment receipt with a named internal owner, and if someone else pays, record that payer at the same time with the related approval note.

Verification point: the dossier contains the receipt, payer identity when different from the applicant, and the approval record.

Pre-approve payment controls#

Pre-approve payment controls before attempting payment. If your team plans a specific payment method, record that as an internal plan, not as a guaranteed acceptance path for this flow.

Set an internal contingency path in advance: who can approve a retry, who can approve a different payer, and when to pause instead of improvising. This is one of the easiest places to lose audit clarity if multiple payment attempts happen ad hoc.

Separate operational and legal escalation#

Separate operational escalation from legal escalation. Record who handles application issues with the relevant authority, and separately record who handles company setup legal questions. Final checkpoint: after submission, the assigned verifier confirms the filing appears in the Estonian company register.

For a step-by-step walkthrough, see Australia Tax Residency for Digital Nomads With GST and ABN Checkpoints.

Separate fixed fees from variable operating costs before you pick a provider#

Use one table to separate statutory fees from provider services before any approval. If costs are bundled, you cannot compare quotes or explain variance later.

| Cost item | Mandatory vs optional | Fixed vs variable | Evidence required |

|---|---|---|---|

| State fee for Estonian e-Residency application | Statutory filing item (confirm current applicability) | Statutory item set by the authority at filing time | Filing/application receipt + dated official fee source, and corresponding official PDF record where available |

| Company registration fee for OÜ filing | Statutory filing item (confirm current applicability) | Statutory item set by the authority at filing time | Registration/finalization receipt + dated official fee source, and corresponding official PDF record where available |

| Contact person service | Conditional | Variable service cost | Itemized quote/contract, scope, renewal terms, internal owner |

| Accounting services | Optional to outsource | Variable service cost | Quote/SOW, billing basis, scope, renewal terms, internal owner |

| Provider package pricing | Optional managed-service route | Variable bundled service cost | Itemized quote, version date, contract terms, explicit split between statutory and service fees |

| Share capital contribution | Caveat, case-specific | Uncertain/conditional | Incorporation documents, internal legal note if needed, payment proof if contributed |

| Business license | Caveat, activity-specific | Uncertain/conditional | Regulatory assessment, applicable guidance, application/approval records if required |

| Card pickup travel/location-related charge | Caveat, location-dependent | Variable incidental cost | Confirmed pickup location + travel estimate/receipt |

For statutory lines, do not rely on non-official web renderings alone. Verify against an official legal edition, keep the corresponding official PDF record you relied on, and date-stamp it.

For provider lines, require the same categories across all quotes: statutory pass-throughs, one-time service fees, recurring services, and auto-renew add-ons. If a provider will not separate statutory and service fees, treat the quote as non-comparable and do not approve it.

Keep uncertain items out of your fixed baseline until applicability is confirmed. For example, card pickup travel depends on location, so track it as a caveat row rather than a universal filing cost.

If you want a deeper dive, read Xolo Go vs. Xolo Leap: A Strategic Choice for Solopreneurs.

Choose the incorporation route with explicit decision triggers#

Lock the incorporation route early. Use the e-Business Register when your team can complete identity and filing digitally with a clearly assigned filer, and move to notary support when signing ownership is unclear.

| Route | Practical trigger | Timeline stance | Presence check | Operational burden |

|---|---|---|---|---|

| e-Business Register | You already have Estonian e-Residency credentials and a named filer | Do not assume an official SLA | Confirm the signer has the e-Residency digital ID card and PINs | Can reduce provider dependency when filing ownership is clear |

| Notary | Digital signing or filing ownership is unclear, or you want guided support | Providers may market ~1-2 weeks or ~2 weeks vs 4-6 weeks; treat those as claims, not guarantees | Providers may market remote handling; verify whether any in-person step applies to your case | Can require more provider coordination |

Confirm the digital path before you choose it#

Choose the e-Business Register only after the actual filer has collected the e-Residency starter kit, meaning the digital ID card and PIN codes. Background checks by the Estonian Police and Border Guard Board sit upstream, so your timeline should account for that gate before incorporation starts.

Escalate to notary support when digital ownership is weak#

Use a notary route when your team cannot clearly assign who will authenticate, sign, and submit from end to end. It is not automatically faster, but it can reduce process friction when language, document handling, or filing responsibility is unclear beyond basic forms.

Require pre-approval for any route change#

Treat any route switch as an internal control event, not an admin tweak. If you switch after quote approval, recheck timeline assumptions, document requirements, and whether legal or provider support scope has changed. In your internal file, mark a route change live only after the owner, approver, and revised evidence list are updated.

Related reading: How Platforms Reduce Cross-Border Payout Costs.

Set up local presence correctly and avoid bundled-service confusion#

Treat local presence as a separate control point once the filing route is set. A common risk is scope confusion: a bundled package may not fully cover contact-person support, legal-address support, or ongoing handling after setup. Exact legal triggers, mandatory service standards, or fixed fee ranges are not established here, so treat those as case-specific checks.

Map obligations to named tasks#

Have your legal or compliance owner confirm what applies in your case under current Estonian requirements, then convert that into named tasks. Keep the decision record explicit: what is required, who owns it, what the provider covers, and what stays with your team.

| Task area | Internal owner | External provider | Evidence to retain |

|---|---|---|---|

| Contact person, if required in your case | Legal/compliance | Named provider | Contract or order confirmation, provider details, renewal terms |

| Legal address, if required in your case | Legal/operations | Named provider or landlord | Address-use agreement, renewal terms |

| Official mail handling | Operations | Named provider | Handling terms, escalation contact, acknowledgment method |

If ownership or evidence is still unclear, do not treat setup as complete.

Compare service scope before package labels#

Compare providers on scope first, then price. Bundled offers can work, but only if contact-person support, legal-address support, and ongoing handling are clearly separated in writing.

Verify scope in listings and in the contract#

If you use the e-Residency Marketplace to build a shortlist, confirm final scope in the contract. Do not approve based on listing language alone when contract terms say something different.

Before approval, retain:

- The listing or provider page used for scoping.

- The final contract or order form showing included services and renewal handling.

- A named service contact and escalation mailbox.

Set acceptance criteria before purchase#

Set acceptance criteria in writing before you buy: correspondence acknowledgment, document handling flow, and renewal continuity. Ask direct questions about who receives official mail, how documents are forwarded and logged, and how time-sensitive notices are escalated.

If you need more context on the role itself, use this explainer on the contact person role. For broader context, read How Foreign Professionals Can Decide Tax Residency in Japan.

Plan banking and money movement controls before first revenue#

Do not wait for first revenue to discover banking friction. Set your account-opening path, approval ownership, and fallback before OÜ registration is complete, where possible.

Decide the account-opening sequence early#

Treat onboarding as a parallel workstream, not a post-registration admin task. Estonian e-Residency gives access to online services, but bank onboarding may still include offline or in-person steps.

Document in advance:

- your primary provider

- who can submit the application

- who approves payouts once the account is live

- your fallback if onboarding is still pending after OÜ registration

Define your evidence checkpoint up front as well. If you are asked for local economic ties, be ready to show real business activity such as customers, staff, contracts, or office presence in Estonia.

Set fallback and approval controls before go-live#

Define a written fallback rule before the first invoice is issued: if the primary account is not approved by go-live, either delay collection or use a pre-reviewed alternative. Do not improvise after money starts moving. That helps keep ownership, payer intent, and transfer history clear from the start.

Make bank-to-ledger evidence a day-one control#

Once the account is open, accounting and tax handling are the next compliance areas. If transaction evidence is weak in month one, cleanup later can be harder.

| Checklist item | What to record |

|---|---|

| Inbound source record | Who paid, why, and which contract or invoice supports it |

| Payout approval | Who approved release of funds and where that approval is stored |

| Reconciliation owner | Who matches bank movement to invoice or liability |

| Exception queue | Where unmatched, reversed, or unclear items are logged and resolved |

Use those same four fields as your first-transaction checklist for each payment flow.

Add a scale trigger for cross-border, high-volume flows#

If payments are cross-border and high-volume, add a review gate before scaling. Expand only when your team can trace material bank movements to ledger entries and supporting documents.

Run a recurring checkpoint: can your team trace each material inbound and outbound transaction from bank record to ledger entry to supporting document? If not, pause expansion and fix the evidence trail first. Related: How to Open a Business Bank Account for Your Estonian Company.

Define tax and reporting obligations at day zero#

Set tax ownership before the first invoice. Do not run an Estonian OÜ on a vague "the accountant will handle it later" model.

Assign named owners for tax assessment, reporting, and records#

Assign clear ownership for tax-registration assessment (including VAT, if relevant), declaration coordination, and day-to-day recordkeeping hygiene. In a small team, one person can hold multiple roles, but each responsibility still needs its own checklist and review point.

Before launch, each owner should be able to state in writing:

- what triggers action

- where supporting documents are stored

- who reviews exceptions

Your day-zero evidence pack should include:

- OÜ incorporation documents

- a short tax-registration status memo with re-check ownership

- the accounting services contract, if outsourced

- a document repository for invoices, contracts, receipts, and bank records

- a reporting calendar for tax-payment and declaration deadlines

Separate recurring duties from event-driven obligations#

Track recurring and event-driven obligations separately from day one. Recurring work includes recordkeeping upkeep, declarations and payments as applicable, and EMTA tax-calendar monitoring. Event-driven work includes changes in activity, cross-border expansion, profit distributions, and reassessment of foreign tax exposure.

This split matters because an e-resident-formed company is an Estonian resident company for income-tax purposes, but foreign-country tax can still apply where activities are carried on. Estonian tax residency is not, by itself, an exemption from tax obligations elsewhere.

Set a hard escalation rule for uncertainty#

If tax treatment, tax nexus, permanent-establishment risk, or company obligations are unclear, stop process design and escalate to specialist review. Do not finalize invoicing or payment logic while tax ownership remains unresolved.

This matters most in cross-border activity. Estonia applies double-taxation prevention mechanisms, and if permanent-establishment profit is taxed abroad, later Estonian treatment of distributions can differ.

Match accounting scope to the risk you are actually taking#

Choose accounting scope based on operational risk, not just budget. A lighter setup may be workable when operations are simple and internal document control is consistently strong. If you expect cross-border payments, many counterparties, contractor spend, or recurring tax uncertainty, consider broader accounting services with ongoing controls.

Use one practical test: can your team produce the contract, invoice, payment record, and booking support for any material transaction on request? If not, filing-only support is too thin.

Deferred Estonian income-tax timing until profit distribution does not reduce day-zero control needs. It changes timing for one part of the tax picture, not the need for clear ownership, records, and escalation from the start.

We covered this in detail in How to Get a Tax Residency Certificate as a Digital Nomad.

Build first-year budget scenarios with escalation thresholds#

Build three first-year scenarios now, not one flat estimate, and define what automatically triggers re-approval. For Estonia-related setup and e-Residency costs, use documented assumptions for each line and treat unknowns as explicit sensitivities.

Build three scenario rows instead of one total#

Use the same core lines in each scenario: state fee (if applicable), company registration fee (if applicable), contact person, and accounting services. Populate each amount from a dated receipt, signed order form, or provider quote.

| Scenario | Assumption | Core cost lines | Sensitivity items | Governance minimum |

|---|---|---|---|---|

| Lean | Simple activity, low transaction volume, minimal outsourcing | State fee, company registration fee, basic contact person, minimal accounting services | Potential share-capital item, possible licensing item, provider markup not finalized | Approver named, evidence attached, renewal date recorded |

| Standard | Recurring operations with some cross-border exposure | State fee, company registration fee, contact person, ongoing accounting services | Share-capital timing, possible license review, provider markup under review | Approver + tax owner sign-off, contract version saved, renewal date set |

| Managed | Higher reporting risk and ongoing control needs | State fee, company registration fee, contact person, broader accounting services | Share-capital treatment still open, license/legal review, provider markups and add-ons separated | Finance approver, legal/tax reviewer, evidence pack complete, renewal/rebid date set |

If a line cannot be tied to a document, treat it as an assumption.

Add sensitivity lines where budgets usually fail#

Keep potential share-capital, licensing, and provider markup items as separate sensitivity lines. Mark each as not needed, pending review, or expected.

Also budget for VAT-reporting scope risk. Since 1 July 2021, EU VAT rules for cross-border B2C e-commerce changed, and online marketplaces or platforms have record-keeping requirements. If you may use OSS, plan for added reporting effort because OSS returns are additional and do not replace regular VAT returns. Depending on scheme, returns are quarterly or monthly, and supplies in that scheme must be fully declared.

If VAT treatment is complex, include a specialist-review contingency. Taxable persons can request a VAT Cross-border Ruling, and Estonia is among participating countries.

Add governance fields to every recurring line#

For each recurring line, record the following:

- Approver: who can approve initial spend and changes.

- Evidence artifact: the exact file proving scope and price.

- Renewal date: when repricing or renewal can occur.

A usable budget row shows amount source, scope, owner, and renewal timing in one place.

Set a hard escalation rule before spending starts#

Set the variance threshold internally before launch, then make escalation automatic: if actuals exceed approved variance, or key assumptions change, require re-approval plus legal and tax review.

Common triggers include moving into cross-border activity, entering the EUR 10 000 threshold context, adopting OSS, identifying a licensing issue, or vendor rebundling that obscures statutory versus service-cost changes. The scenario budget is a control tool because it tells finance, legal, and tax when the operating model needs another look.

You might also find this useful: ASC 340-40 for Platforms: How to Account for Contract Acquisition Costs and Commissions.

Execute in order with verification checkpoints#

Run setup in sequence, not as parallel guesswork. Move forward only when proof from the prior step is stored, reviewed, and consistent across your records.

Apply for Estonian e-Residency and lock the payment trail#

Start this workflow by applying for Estonian e-Residency, then capture the state fee evidence immediately. Store the payment receipt, payer record if someone else paid, submission confirmation, approval record, and key correspondence in one case folder.

Set your document standard at this stage. Use a single intake channel and capture the same metadata each time: transaction date, currency, counterparty, and business purpose. This avoids the "ask later" pattern that often turns into corrections in declarations or reports. Checkpoint: the receipt and submission proof can be found in five minutes.

Register the Estonian private limited company and reconcile entity data#

If your next step is registering an Estonian private limited company (OÜ), save the filing confirmation as a formal artifact. Record which source is the final accounting proof when card charges, platform confirmations, and provider invoices appear in different systems.

Before treating the OÜ as operational, reconcile core entity data across filing records and internal tracking notes. If company or owner fields differ, resolve them now to prevent downstream errors. Checkpoint: one consistent entity record across all systems before proceeding.

Designate contact persons and store the full service evidence#

Once the company filing evidence is complete, designate the contact persons for the workflow and archive the full service proof. If you use a contact-person service, keep the provider contract, order form, scope, renewal terms, and internal sign-off, not just payment receipts.

For international services, keep the contract plus documents that confirm work results. If scope is unclear across accounting, legal, and operations, pause and clean up the paper trail before launch. Checkpoint: service scope is explicit and auditable across teams.

Activate accounting controls before first transaction#

Set controls before the first transaction, not after. Assign one owner for document intake, define scheduled checkpoints, and set a final-proof-source rule for multi-system expenses.

Require regular checks that each transaction links to supporting evidence, and tag board-decision-related expenses separately. Add a hard go or no-go launch gate: no missing proof and no unclear approval or reporting ownership. Verify requirements against EMTA resources for non-residents and e-residents before filing, then recheck before the first tax-relevant activity. Checkpoint: if ownership, proof, or record consistency is incomplete, launch is a no-go.

Handle common failure modes and recover quickly#

When the process breaks, recover by pausing new commitments, preserving evidence, and reopening only after the blocking fact is verified.

| Failure mode | Immediate response | Next check |

|---|---|---|

| e-Residency application declined | Pause new setup spend, log the decision date, and keep application-fee evidence | Do not treat digital setup as ready without the e-Residency ID card, card reader, and pickup confirmation from an embassy or collection point |

| Opaque provider bundle | Confirm which lines cover the legal address and contact person before approval | Record each confirmed item and its related contract or filing artifact |

| Filing route changes | Treat prior assumptions as unverified and recheck any in-person steps and launch timing | Also recheck banking because some account-opening paths still require branch attendance and onboarding can fail without clear local business ties |

| Key artifacts missing | Stop before the first live transaction and rebuild the file from original senders or platforms | Reconcile names, dates, payer details, and final proof sources across company records |

Freeze spend if Estonian e-Residency is declined#

A declined e-Residency application is a real branch, not a minor delay. Log the decision date, keep application-fee evidence, and rework the timeline before approving new setup spend.

Use one hard readiness check. If you do not have the e-Residency ID card, card reader, and pickup confirmation from an embassy or collection point, treat digital setup as not ready.

Break apart opaque provider bundles#

If a provider package mixes required and optional services, confirm which lines cover the legal address and contact person required for local setup before approval.

Record each confirmed item and its related contract or filing artifact before you proceed.

Revalidate assumptions if the filing route changes#

If your route changes, treat prior assumptions as unverified. Recheck any in-person steps and launch timing before moving forward.

Do the same for banking. Some account-opening paths still require branch attendance, and onboarding can fail without clear local business ties.

Pause launch and rebuild the evidence file#

If key artifacts are missing, stop before the first live transaction. Rebuild the file from original senders or platforms, then reconcile names, dates, payer details, and final proof sources across your company records. That keeps banking and reporting from starting on inconsistent data.

Know when to escalate to specialist advice#

When obligations, filings, or evidence ownership are unclear, escalate immediately and define the question narrowly before work continues.

Escalate legal questions that affect company obligations#

Escalate to legal counsel when you cannot map an Estonian legal obligation to a named owner and required proof. Do the same when business license scope is unclear from the materials you have.

Use one checkpoint: can you state the obligation, who performs it, and what evidence closes it? If not, treat it as an open legal risk and escalate.

Escalate tax questions before you design around assumptions#

Escalate to a tax specialist when VAT treatment, cross-border sales or service handling, or reporting obligations are unclear. In Estonia, VAT is administered by EMTA, and registration becomes mandatory once taxable turnover exceeds €40,000 in a calendar year.

Escalate when your team cannot clearly explain why registration is or is not required, or whether payroll, board fees, or contractor payments trigger TSD review. Late registration or incorrect assumptions increase compliance risk.

Escalate finance control gaps early#

Escalate to a finance specialist when bookkeeping evidence is incomplete, reconciliation ownership is unclear, or annual report readiness depends on memory. All registered Estonian businesses, including e-resident companies operated from abroad, must submit annual reports.

Treat the first 90 days as a controlled setup phase. Confirm who prepares each filing, who approves it, and that monthly and quarterly deadlines sit in one internal calendar.

Record the outcome as an operating decision#

Document every escalation outcome as an operating decision record, not just an email thread. Capture the question, decision date, owner, specialist consulted, documents reviewed, and next control action. If the decision changes the filing route, VAT setup, or evidence ownership, update ownership and the record location the same day.

Copy-paste launch checklist#

Use this as a launch gate: if ownership, filing route, or evidence is unclear, pause the OÜ launch.

Confirm route and signer ownership#

Confirm who will hold and use the e-Residency digital ID card, who will submit the OÜ filing, and who approves the route. Before proceeding, verify the named owner can log in to Estonian online portals and complete a legally valid electronic signature. Do not treat e-Residency as citizenship, physical residency, or a travel visa, and do not assume it will be accepted across all EU public systems.

Approve budget lines and evidence rules#

Split spend into fixed state charges and provider-priced services, then assign an approver, payment record, required evidence, and review date for each line.

Minimum evidence pack per line item:

- payment receipt or confirmation

- signed provider contract or order form

- filing confirmation, where applicable

- named internal follow-up owner

If a provider quote bundles multiple items and cannot be unbundled, treat it as non-comparable until scope and pricing are clear.

Contract and verify contact person and accounting scope#

If you use a contact person, confirm contract scope, renewal terms, escalation contacts, and handling of official correspondence before launch. Apply the same scope check to accounting support so responsibilities are explicit, including what is out of scope.

Provider support can reduce operational burden, but do not assume bundled support means full compliance ownership. For role detail, see The Role of a 'Contact Person' for an Estonian e-Resident Company.

Assign tax and reporting owners from day zero#

Assign one accountable owner each for Estonian VAT number assessment, bookkeeping, and annual report obligations. Set an escalation rule for unclear VAT treatment or entity obligations, and pause process design until specialist advice is obtained where needed. Keep one point explicit in approvals: e-Residency is not a way to avoid tax in the person's actual country of residence.

Run the final go/no-go archive review#

Archive receipts, filing proofs, provider contracts, owner assignments, and escalation decisions in one place. Run a final consistency check so company name, route, and responsibility records match across documents. Launch only if another finance or compliance owner can reconstruct what was approved, who owns each obligation, and what evidence supports it without chasing missing records.

If you want to operationalize these controls in a cross-border payment flow, contact Gruv.

Frequently Asked Questions

What are the mandatory baseline costs to open an Estonian company with e-Residency?

For the standard online route, the baseline state charges are €150 for the e-Residency application and €265 for online OÜ registration. A contact person is required for most e-residents, but that cost is provider-priced rather than a fixed state fee.

Are there annual maintenance fees for the e-Residency digital ID card?

No. The e-Residency digital ID card has no annual or maintenance fee. The card is valid for 5 years, so track the validity date so signing access does not lapse unexpectedly.

Which recurring costs are usually required after company registration?

The most common recurring costs are contact person service and accounting support. The material shows about €200-400 per year for a contact person and accounting from €50 per month. Annual report filing is mandatory for all Estonian companies, including inactive ones, and business-license needs can add extra costs.

What costs are fixed by law vs set by service providers?

The €150 e-Residency application fee and €265 online OÜ registration fee are fixed state fees. Contact person, accounting, and bundled service packages are set by providers and can vary by package. Compare provider quotes carefully because package scope is not always like for like.

Can the e-Residency state fee be refunded if the application is rejected?

No. If issuance is declined, the state fee is not refunded. Keep follow-on spending decisions separate until the application outcome is confirmed.

When should we choose notary registration instead of the e-Business Register?

There is no universal rule, fee schedule, or timeline for choosing notary registration over the e-Business Register. Treat route selection as case-specific, and confirm it with your legal adviser or incorporation provider before committing additional fees.

Which documents should finance and compliance retain for audit readiness?

Keep the payment-service receipt for the e-Residency state fee, because no invoice is issued for that payment. If someone else paid on the applicant's behalf, retain that payer record and confirm payment was made through the application environment. Also retain company registration and annual-report filing evidence, plus service agreements used for ongoing compliance support.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: