Quick Answer

Pick one tax-resident country you can defend, then apply only after every claim in your file maps to evidence. For a tax residency certificate nomad case, keep visa status separate from tax status, run a CRS mismatch check across account declarations, and save a full submission trail with the form set, receipt, timestamp, and acknowledgment. If U.S.-linked filings apply, treat the certificate as support while continuing required return and disclosure work.

You are not trying to pay zero tax, you are trying to stay provably compliant#

The lowest-stress path is a tax position you can prove, not a zero-tax narrative you cannot defend later. If you are a freelancer or consultant, choose one defensible tax home, document it clearly, and keep filings consistent across jurisdictions.

Tax residency is the legal link that decides where your global income is taxed. A visa may allow you to live somewhere, but it does not automatically resolve your tax position. A low-tax move also does not automatically end reporting duties elsewhere, and OECD CRS coordination across banks, fintechs, and governments can surface mismatches.

Disputes often start with small inconsistencies, not dramatic errors. One form says one country, a bank profile says another, and your supporting files do not explain the difference. Then you spend time proving intent instead of finishing filing. The practical goal is to make your position easy to understand and hard to misread.

Think in sequence, not shortcuts. First pick the country you can defend. Then gather the documents that support that claim. Then test for conflicts before filing. That order is less exciting than tax-hack content, but it prevents a lot of avoidable rework when deadlines are close.

Before You Start#

Use this setup check before you start any certificate application:

- Write one sentence naming your intended tax-resident country and why your claim is defensible.

- Build one evidence folder with your draft application and the identity, address, and filing records you plan to rely on.

- Add a short risk note listing places that could still question your position.

Checkpoint: if you cannot state your tax home clearly in one sentence, do not file yet. This article does one specific job: help you choose one residency path you can defend, build the supporting document trail, and know when to escalate before errors compound. If you want broader prep, pair this with The Ultimate Digital Nomad Tax Survival Guide for 2025.

- Step 1: Choose one defensible path. Pick the country where your facts and records align best, not the one with the loudest marketing.

- Step 2: Map each claim to evidence. Every statement in your application should have one retrievable supporting file.

- Step 3: Set escalation triggers early. Escalate when facts suggest competing residency claims, unresolved filing duties, or conflicts with prior filings.

The tradeoff is simple: aggressive tax stories may look attractive upfront, but weak documentation usually creates more friction later. A strong certificate strategy favors proof, consistency, and early clarification.

If you want a deeper dive, read The Freelancer's Guide to India's Outward Remittance Rules (LRS).

What a tax residency certificate actually proves#

A tax residency certificate supports your claim that you pay taxes in a specific country and may support treaty or DTAA positions. It does not, on its own, settle every question about taxing rights.

Tax Residency Certificate and Tax Domicile Certificate can refer to the same core document. Labels, issuing authorities, and validity periods vary by jurisdiction, so follow local requirements rather than a generic template.

Keep immigration status separate from tax status. Immigration status or a digital nomad visa may explain where you can stay, but it does not automatically establish tax residency.

Another practical boundary: IRS international FAQ content is general guidance, not citable legal authority. Use it to frame your questions, then anchor filings in formal instructions and applicable law.

Treat the certificate as one input, not a complete legal conclusion. If your records conflict, resolve that before submission.

Step-by-step check before filing#

- Step 1: Define your country claim in one sentence. Write: My intended tax-resident country is X because Y. If you cannot state this cleanly, stop before applying.

- Step 2: Confirm the local certificate name and issuer. Verify whether your jurisdiction uses Tax Residency Certificate or Tax Domicile Certificate, and confirm the issuing authority.

- Step 3: Tie the certificate to your use case. State whether the document supports a treaty or DTAA position.

- Step 4: Escalate early if facts conflict. If your facts support competing claims or conflict with prior filings, resolve that before submission.

Before you move on, run one quick sanity check: read your one-sentence claim, then list the three documents that prove it fastest. If you cannot do that without guessing, your draft is not ready.

Before you apply, build your evidence pack#

Treat your evidence pack as a claim map, not a document dump. Each document should support one specific claim you plan to make in the application.

| Lane | What to include | Note |

|---|---|---|

| Core categories | Identity records; current address proof; stay-pattern evidence such as entry and exit history; income trail records tied to the same person and period; filing history that supports your residency position | Treat your evidence pack as a claim map, not a document dump |

| US-linked cases | Federal income tax return records; relevant IRS filings; U.S. status records that are relevant to your filing position, if applicable | Keep a separate US file set |

| Cross-border disclosures | FinCEN Form 114 (FBAR) support files; FATCA-related records; Form 8938 support files and workpapers | Add only where relevant |

Start with core categories that fit your facts:

- Identity records.

- Current address proof.

- Stay-pattern evidence such as entry and exit history.

- Income trail records tied to the same person and period.

- Filing history that supports your residency position.

For US-linked cases, keep a separate US file set:

- Federal income tax return records.

- Relevant IRS filings.

- U.S. status records that are relevant to your filing position, if applicable.

Add cross-border disclosures only where relevant:

- FinCEN Form 114 (FBAR) support files.

- FATCA-related records.

- Form 8938 support files and workpapers.

For Form 8938, keep these checks explicit in your notes:

- Form 8938 is attached to the annual income tax return.

- Filing Form 8938 does not replace FBAR obligations.

- If no income tax return is required for that year, Form 8938 is not required.

- Thresholds vary by profile (including joint filing status and whether you reside abroad), so confirm the right threshold set before marking your pack complete.

Give each file a clear name that includes what it proves and the period it covers. That small habit reduces confusion when you revisit the pack months later. It also makes it easier to confirm whether a document is current or stale before submission.

Keep a simple index with three columns: claim, supporting file, and date range. This is where gaps often show up early. If a claim has no file, either collect the file or remove the claim. If a file has no claim, move it out of the core set so your packet stays focused.

Verification checkpoint before you apply: pick any claim in your draft and pull the matching file immediately. If you cannot map a document to a claim, the pack is not complete.

One common failure mode is mixing local residency files with U.S. disclosure files until no one can tell which record supports which filing lane. Keep those lanes separate from day one, then cross-reference only where needed.

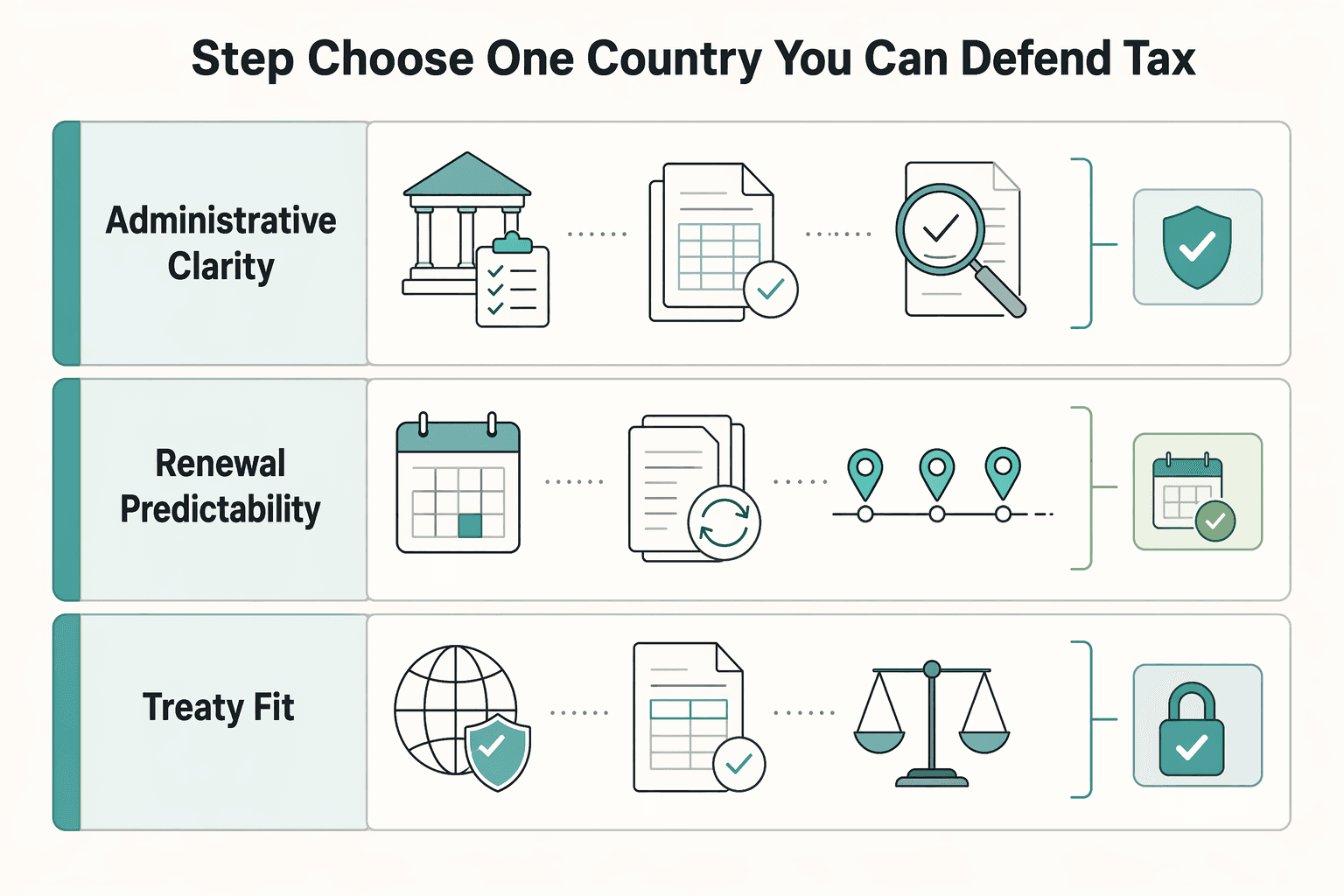

Step 1 choose one country you can defend as your tax home#

Choose the country your records can defend under review, not the one with the most attractive tax marketing. Your tax home should be the place where documents, timelines, and filings still make sense when a bank or tax authority compares records. Tax residency is not the same as visa or residence-permit status.

Use three filters before you compare tax rates: administrative clarity, renewal predictability, and treaty fit.

| Filter | What to confirm before you choose |

|---|---|

| Administrative clarity | Issuing authority, current forms, and required documents are easy to identify |

| Renewal predictability | Where applicable, validity window, renewal timing, and recheck triggers are clear |

| Treaty fit | Treaty network is useful for where your clients, payers, and accounts are |

Match your choice to how you actually operate. If your client and banking footprint is stable, prioritize documentation reliability. If your travel pattern is volatile, prioritize jurisdictions with clearer tax-residency tests.

One practical tie-breaker helps when two options look similar: pick the country where your files already tell a cleaner year-round story. The better choice is usually the one that needs less explanation later, not the one that looks best in an online comparison.

Use this short validation sequence:

- Score administrative clarity. Confirm issuer, form set, and application path.

- Test renewal predictability. Check any stated validity and renewal timing against your filing calendar.

- Stress-test residency rules against your travel pattern. Use only country-specific tests and day-count rules.

- Compare treaty fit with evidence strength side by side. Pick the country your records can prove.

Red flags include assuming a digital nomad visa automatically creates tax residency, assuming a new bank account by itself creates tax residency, or assuming a move to a low-tax jurisdiction ends reporting obligations elsewhere. If two countries still look equally plausible, choose the one with stronger evidence.

Before finalizing, write a short decision note and save it with your pack. Include why you selected that country and why you rejected the closest alternative. That note becomes useful if you need to explain your judgment later.

Step 2 pressure-test residency conflicts before filing#

Before filing, test where your tax-home claim could collide with other jurisdictions. Cross-border activity can create overlapping tax exposure, including situations where the same income stream is taxed in two places.

Tax residency decides where worldwide income may be taxed. Marketing or mobility labels do not determine tax residency on their own.

Do not stop at listing countries. For each one, link one specific exposure reason and one specific evidence item. That forces clarity and helps you avoid assumptions based on travel alone.

Run this conflict check:

- List credible claim countries. Include your intended tax home and any other country that could plausibly claim taxing rights based on your situation.

- Map one exposure reason and one evidence item per country. Use document-backed items such as travel history, address records, payer location, or prior filings.

- Label each link clearly. Mark each connection as immigration only, tax only, or both.

- Run a CRS consistency check. Confirm country declarations and tax ID details align with account records.

- Decide file or fix. If two countries can still credibly tax the same income stream, resolve that conflict before you file.

Use one decision rule: pick the path with fewer unresolved conflicts. Consistency across declarations helps reduce mismatch risk when data is compared across jurisdictions.

If you find a mismatch, fix the root cause before filing, not after. Rework gets heavier once forms are submitted and records start circulating across institutions.

Step 3 handle treaty positioning and US exceptions correctly#

Set treaty posture with a simple rule: a treaty can help coordinate double-tax relief, but it does not remove filing duties by default. A foreign residency certificate may support your position, while returns and forms carry the compliance burden.

| Item | Role | Limit |

|---|---|---|

| Treaty | Can help coordinate double-tax relief | Does not remove filing duties by default |

| Foreign residency certificate | May support your position | Treat it as additive evidence, not a substitute for U.S. compliance |

| FEIE | Applies only if you are a qualifying individual with foreign earned income | That income is still reported on a U.S. return |

| FTC / Form 1116 | Handled on Form 1116 | Each income category requires a separate form |

For U.S. filers, this is the key point. U.S. citizens and resident aliens are taxed on worldwide income, even after foreign tax residency is established. Treat treaty use as coordination, not substitution.

Keep FEIE and FTC in one review lane. FEIE applies only if you are a qualifying individual with foreign earned income, and that income is still reported on a U.S. return. FTC is handled on Form 1116, and each income category requires a separate form.

Do not treat FEIE and FTC as purely mechanical form choices. The sequence matters: classify income first, then evaluate the relief method by income stream, then document why that method fits your facts for that year.

Use this sequence before filing:

- Classify income streams first, then choose the lead relief method for each one.

- Prepare Form 1116 by category, not as one pooled filing.

- Validate FEIE timing assumptions early, including whether one of the limited minimum-time exceptions may apply.

- Treat the foreign certificate as additive evidence, not a substitute for U.S. compliance.

When FEIE is part of your plan, keep the qualifying logic with your travel and income records so your file tells one coherent story. When FTC is part of your plan, keep Form 1116 categories and related support files grouped together to avoid cross-category confusion.

If your plan depends on a certificate alone to end U.S. filing duties, treat that as a red flag. Keep a compact evidence set with the certificate, FEIE workpapers, Form 1116 package, and a short treaty note describing what changed and what did not.

One more guardrail: do not rely on internal practice materials as binding legal authority. They can help you understand process, but your filing position should still be anchored to formal legal sources and instructions.

Step 4 submit the certificate application and track renewal#

Once your position is clear, execute submission in a strict sequence: confirm the authority, confirm the form set, submit, preserve proof, and set renewal reminders before you close the task.

- Confirm the competent authority and exact document name first. Verify the official document name used in your jurisdiction before filing.

- Confirm prerequisites and path before filing. In Spain guidance, for example, an N.I.E. is required before a telework visa application, while foreigners already legally in Spain may apply directly for a telework residence permit without a prior telework visa.

- Submit once and preserve a complete trail immediately. Save the final form set, receipt, timestamp, and acknowledgment reference in one retrievable folder.

- Set renewal logic from official validity text. In the same Spain guidance, telework visa validity is up to 1 year and telework residence permit validity can be up to 3 years.

- Archive the issued document with the decision notice. You should be able to retrieve the full chain from application to issuance in minutes.

Avoid fragmented storage. If the form PDF is in one place, the receipt in another, and the issued document only in email, renewal and audit prep become harder than necessary.

Do not mark this step complete until both items exist: the issued document and the submission trail. At the end of submission, add one short renewal note to your calendar entry with where the files live and what must be rechecked before renewal.

Step 5 keep an audit-ready records system after approval#

After approval, your job is consistency over time. Keep residency documentation, return files, and foreign-asset reporting records aligned year by year so your position stays coherent.

- Link residency proof to the same-year return file. Store your residency documentation with that year's return package. If Form 8938 applies, include it with that return and keep supporting foreign-asset records in that annual file set.

- Run Form 8938 and FBAR as parallel tracks. Filing Form 8938 does not replace FBAR, so maintain separate support files and reconcile them quarterly.

- Apply filing-status rules before year-end. Do not assume one threshold fits all cases. IRS materials include a $50,000 aggregate trigger for certain taxpayers and note higher thresholds in other cases, including some joint filers or taxpayers residing abroad. If no income tax return is required for the year, Form 8938 is not required for that year.

- Keep payouts, invoices, and ledger exports on one timeline. Quarterly bundles make it easier to trace entries from transaction records to tax workpapers.

Quarterly reviews help catch drift early. Account ownership labels can change, profile country settings can be updated, and old assumptions can carry forward unless you check them. Small corrections in quarter one are easier than a full reconstruction at filing time.

Add a repeating review checklist with four questions: Did any account profile change? Did any filing lane gain or lose a document? Did any date range stop matching? Does your residency story still match your declared tax profile? If one answer is unclear, mark it for follow-up before the next filing cycle.

A short quarter-end review catches missing statements, stale records, and profile mismatches before filing deadlines. When a filing position is close, rely on formal legal authorities, not FAQ summaries.

Common mistakes that create residency trouble and how to recover#

Most residency trouble starts with inconsistent positions across filings, not one missing file. Recovery starts by restating your position in plain language, then making each filing lane match it.

| Mistake | Why it creates trouble | Recovery |

|---|---|---|

| Treating one document as the whole answer | A single document can support your claim, but it does not end filing obligations by itself | Map each income stream to required filings and keep one written note showing both claimed relief and remaining duties |

| Assuming Form 8938 and FBAR are interchangeable | They are separate filing lanes | Keep distinct support files for each; Form 8938 is attached to your tax return, and filing it does not remove an otherwise required FBAR filing |

| Applying one Form 8938 threshold to every profile | Thresholds vary by filing profile | Confirm the threshold that applies each year; IRS materials include a $50,000 aggregate trigger for certain taxpayers and higher thresholds in some cases, including some joint filers or taxpayers residing abroad |

| Filing with mismatched values across records | Small inconsistencies can create avoidable filing friction | Reconcile account ownership and values line by line across return workpapers, Form 8938 support files, and FBAR support files; for FBAR, convert non-U.S.-currency values to U.S. dollars and round up to the next whole dollar |

A useful recovery pattern is to fix order before content: first align profile data, then align forms, then align supporting files. If you do the reverse, you often rewrite documents twice.

Another common error is carrying prior-year assumptions forward without review. Even when your country choice does not change, document timing and filing obligations can change. Use annual refresh notes to confirm what stayed the same and what changed.

If no income tax return is required for the year, Form 8938 is not required for that year. Use that rule, then run one final consistency check before filing. If you want a quick next step, Try the tax residency day counter.

When to escalate to a tax professional#

Escalate before filing when your facts support more than one defensible position. Good records help, but they do not resolve legal conflicts on their own.

- Escalate when two countries may both credibly claim tax residency or tax the same income.

If both positions still look valid after you write one legal basis per country, stop self-filing and get filing-sequence guidance.

- Escalate when U.S. worldwide-income rules overlap with FEIE and FTC decisions.

For U.S. citizens and resident aliens, worldwide income can still be in scope. FEIE applies only if you qualify, and the income is still reported on a U.S. return. For 2026, the maximum FEIE is up to $132,900 per qualifying person. FTC handling also requires separate Form 1116 filings by income category.

- Escalate when disclosure scope is unclear across required filings.

The main risk is mismatch across filings, not a single missing form. If you cannot map each account or asset to one reporting path and one responsible filer, get help before submission.

- Escalate before filing if prior-year positions were inconsistent or relied on exception assumptions you cannot support now.

Waivers of minimum time requirements for bona fide residence or physical presence are limited to specific adverse conditions and IRS-published country and effective-date lists. Presence in a foreign country in violation of U.S. law is not treated as bona fide residence or physical presence for these tests.

Use this rule: if two moving parts interact, escalate early. Escalation is not failure. It is a timing decision to avoid locking in a weak filing order, and the goal is to leave the first paid session with one sequence you can execute.

Bring this packet so the first advisor session can be diagnostic:

- Last two federal tax return copies and any amendments

- FEIE calculations and travel-day log for qualification tests

- Draft Form 1116 set, separated by income category

- Current tax residency evidence pack, including certificate files

- Draft international reporting workpapers tied to the return, plus supporting records

Add one page that lists unresolved decisions you need answered. That keeps the session focused and helps you capture a concrete filing order before the call ends. Expected outcome: one filing order, one correction sequence, and one consistent record trail.

Start with one defensible position and a copy-paste execution checklist#

Start with one defensible residency position and keep every filing record aligned to it. If your facts point to two equally plausible outcomes, pause and get filing-sequence advice before you submit.

Use this as your final pre-filing pass. If one checkbox stays open, note the reason and fix it before you send anything.

- Choose one intended tax-residency country and write a one-sentence basis for the exact tax year and period.

- Build an evidence pack that maps each claim to one document and one date range.

- Run a conflict check across travel pattern, immigration or residency status, and potential overlap across jurisdictions.

- If you are U.S.-linked, lock filing posture before submission: U.S. citizens and resident aliens are taxed on worldwide income; FEIE applies only to qualifying individuals and still requires reporting the income on the return; for 2026, the FEIE maximum is $132,900 per qualifying person; if you claim FTC, file a separate Form 1116 for each income category and check only one box per form.

- Submit, archive the full filing packet, and calendar any follow-up dates tied to your filing.

- Run periodic consistency checks so residency documents and filing positions tell one story. Minimum-time exceptions are limited and may apply when you must leave a foreign country because of war, civil unrest, or similar adverse conditions; internal IRS practice units are not legal authority.

Final check before you close: your country claim, filings, and evidence pack should describe the same facts in the same period without contradiction. If they do, you are in a defensible position.

Frequently Asked Questions

What is a tax residency certificate for digital nomads, in practical terms?

In practice, it is documentation used to support a residency position for a specific jurisdiction and period. Treat it as supporting evidence, not a blanket override of every filing obligation.

Is a Digital Nomad Visa the same thing as Tax Residency?

No. Visa status and tax residency are separate, so do not assume one automatically proves the other. If immigration status and tax position point in different directions, resolve that before filing.

Can I live in multiple countries and still hold one Certificate of Residence?

This guidance does not provide a universal rule for that scenario. If more than one country can credibly claim you as resident, pause self-filing and get filing-sequence advice.

Do US citizens and Green Card holders still file with the IRS after getting foreign Tax Residency?

A foreign certificate should be treated as supporting documentation, not an automatic end to U.S. filing exposure. Confirm duties using current IRS filing instructions and your facts. IRS international FAQs can help with orientation, but they are not citable legal authority.

How often does a Tax Residency Certificate need renewal?

A universal renewal cycle is not established in this guidance. Confirm validity and renewal timing with the issuing authority for your document.

Does a Tax Residency Certificate eliminate all taxes?

No. It does not erase all tax or filing duties. California is a clear example: residents are taxed on all income regardless of source, part-year residents are taxed on worldwide income while resident plus California-source income during nonresident periods, and nonresidents are taxed on California-source income.

When is it worth paying for professional advice instead of self-filing?

Pay for advice when residency classification is unclear, because California treats residency as a facts-and-circumstances determination. Classify each year as resident, part-year resident, or nonresident before filing, then map income by source and period. If you are near filing-table cutoffs, remember thresholds vary by filing status, age, and dependents.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

The Freelancer's Guide to India's Outward Remittance Rules (LRS)

Run your outward remittance like an operations process: clarify intent, keep supporting proof, confirm fees, then archive what happened in a reusable folder. If you are the CEO of a business-of-one, this is part of keeping your cashflow predictable. You do not need more theory. You need a system you can repeat every time you send money abroad under LRS in India.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.