Quick Answer

Start by confirming your municipal registration position for January 1, then classify your status under Japan’s resident versus non-resident rules before mapping income. For japan tax residency, the article’s core sequence is status first, income-scope mapping second, and local-tax timing checks third. It also stresses monthly recordkeeping because residence tax (juminzei) can surface later through municipal billing cycles. If your facts point to two countries, escalate for treaty review instead of relying on day-count shortcuts.

Start Here If You Want Fewer Tax Surprises in Japan#

If you want fewer tax surprises in Japan, follow one sequence and keep it current: confirm your registration timeline, map what income is in scope, check local timing triggers, and keep proof organized.

For globally mobile freelancers and consultants, it is easy to focus only on national tax planning. Resident tax (juminzei) is a local tax at the municipality and prefecture level, and many foreign professionals only notice it when a bill arrives about a year after work starts.

Treat this as a year-round discipline, not a filing-season scramble. If you can explain your timeline, income labels, and local registration facts in one read, you are less likely to get surprised or spend weeks rebuilding records.

Use this sequence from day one.

- Determine your local registration timeline before you optimize anything.

Track where you are registered, where you are actually living, and which year each income stream belongs to.

- Map income the same way every month.

Tag each payment consistently so you are not reclassifying transactions under deadline.

- Check local timing triggers early.

A key rule is whether you were registered as a resident on January 1 and had taxable income in the prior year. Resident tax is commonly described as a 10% income-based portion plus an approximately JPY 5,000 fixed per-capita amount, with prefectural items such as a JPY 1,000 Forest Environment Tax in that local layer.

- Build evidence continuously.

Keep registration records, contracts, invoices, and municipality notices together, and update your timeline whenever facts change.

One checkpoint prevents a lot of surprises: confirm your registration status before January 1, then confirm your prior-year taxable income summary. Do not assume a visa label or nationality changes this local treatment. This structure is described as applying the same way to Japanese citizens and foreign residents.

A monthly log works because it forces consistency before pressure starts. When a payment or move date looks unclear, mark it that week, attach the document you have, and note what is missing. That is much easier than rebuilding facts months later.

If you only do one thing this week, start a monthly tax log with four columns: location, registration status, income tag, and document proof. If you want a quick next step, Try the tax residency day counter.

Build the Mental Model Before You Decide Anything#

Tax residency and immigration status can point in different directions. Treat them as separate tests from the start.

Tax residency here is your status for Japan income tax, not your visa label. A Japan digital nomad visa describes entry permission, but it does not by itself determine tax status.

For income tax, the first split is resident versus non-resident. A person is generally treated as a resident if domiciled in Japan or if they have lived there continuously for more than one year. OECD summary language uses the same one year or more continuous-residence test.

Domicile is where most edge cases turn. A practical lens is your center of living. Presumptions can point toward domicile in Japan when your occupation normally requires living in Japan continuously for one year or more and other core ties line up there. Presumptions can also point away from Japan when your occupation normally requires living abroad continuously for one year or more.

Two people can share a similar visa profile and still land in different tax treatment because their living facts differ. One has occupation and living ties centered in Japan. Another has occupation and living ties centered abroad. The visa label is the same, but the filing analysis is not.

Residents are then divided into permanent and non-permanent groups, while non-residents remain separate. These labels can affect income-scope analysis later. One commonly cited threshold is that non-Japan citizens who have resided in Japan for more than five out of the last ten years are treated as permanent residents.

To reduce reclassification risk later, tag each revenue line and keep one supporting record per line:

- Residency-factor tag: facts tied to domicile (center of living) or continuous residence duration.

- Evidence tag: one document that supports your classification.

- Time tag: when the income was earned and where you were living at that time.

Run this tagging monthly and review any line item that changes category. If your facts are mixed or your records are thin, pause and get advice before filing. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

Use the Legal Test in the Right Order#

When facts get messy, use this order: OECD for orientation, Japan domestic law for your filing position, then treaty prep if your facts point to more than one country.

| Checkpoint | What to document | Next step |

|---|---|---|

| Residence pattern in Japan | Build a dated timeline of where you lived and for how long | Confirm whether your pattern supports residence in Japan and the one-year threshold |

| Domicile indicators | Test whether your occupation, family or household ties, and business-location ties point more strongly to Japan or abroad | If indicators are mixed, keep supporting records and a short memo for each indicator |

| Status before income-scope mapping | Lock likely resident or non-resident treatment first | Then map income scope |

| Treaty escalation for mixed facts | If the same period shows strong ties to two countries, prepare treaty tie-breaker analysis | Do not rely on day-count shortcuts |

The OECD residency page is a starting point, not the decision. Your filing position should be based on Japan domestic law: domicile, or continuous residence in Japan for one year or more.

Run these checkpoints in order and document each one before mapping income:

- Residence pattern in Japan

Build a dated timeline of where you lived and for how long. Confirm whether your pattern supports residence in Japan and the one-year threshold.

- Domicile indicators

Test whether your occupation, family or household ties, and business-location ties point more strongly to Japan or abroad.

- Status before income-scope mapping

Lock likely resident or non-resident treatment first, then map income scope. This avoids classification errors later.

- Treaty escalation for mixed facts

If the same period shows strong ties to two countries, treat risk as higher and prepare treaty tie-breaker analysis instead of relying on day-count shortcuts.

Domicile can be fact-intensive. If your indicators are mixed, write a short memo for each one and keep the supporting records so your position is traceable. For dual-residency risk, prepare a compact file before adviser review: timeline, occupation terms, household facts, and source and remittance records.

Keep the memo format simple. Write one paragraph on what supports your position and one paragraph on what points the other way. Then add one line stating what evidence would settle the point. This keeps the discussion factual and speeds up adviser review.

Classify Your Taxpayer Type and Scope of Income#

Classify taxpayer type first, then map income scope against that category.

For individual income tax in Japan, people are classified as residents or non-residents. For income-scope analysis, residents are then split into non-permanent residents and other residents. A non-permanent resident is a non-Japanese resident with domicile or residence in Japan for five years or less within the preceding ten years. If you do not meet the resident criteria, you are treated as a non-resident taxpayer.

| Likely category | Scope to map first |

|---|---|

| resident (other than non-permanent resident) | Worldwide income |

| non-permanent resident taxpayer | Japan-source income, plus foreign-source income depending on whether it is paid in Japan or remitted to Japan |

| non-resident taxpayer | Japan-source income only |

Do not equate payment location with income source. Salary for work performed in Japan is treated as domestic-source income even if paid from outside Japan.

Before you file, use this rule: if you cannot clearly separate Japan-source and foreign-source cash flows, fix your bookkeeping first. Then run this verification checkpoint for each revenue stream:

- Source tag: Japan-source or foreign-source.

- Payment rail tag: how funds were paid.

- Remittance path tag: paid in Japan, kept abroad, or remitted to Japan.

- Evidence tag: record supporting your source and remittance treatment.

If one stream cannot be tagged cleanly, do not bury it in a broad category. Mark it unresolved, tie it to the underlying document gap, and carry it into adviser review. That keeps one weak line item from contaminating the full filing position.

Use this log consistently and tie it to the January 1 to December 31 tax year. If your facts may support treatment in more than one country, escalate for treaty review rather than forcing a confident classification from incomplete records. Related: Taxes in Italy for Expats and Freelancers.

Handle Local Tax Timing Early So January 1 Does Not Blindside You#

Local tax exposure is driven first by your January 1 municipal registration status and your prior-year income, so treat it as a separate local-tax check each year.

| Check | What to confirm | Timing note |

|---|---|---|

| January 1 municipality ledger entry | Confirm your January 1 entry in the local municipality ledger and keep proof | January 1 registration status drives local tax exposure |

| Prior-year income totals | Reconcile prior-year income totals for the January 1 to December 31 period | Local inhabitant tax is based on income from January 1 to December 31 of the previous year |

| Move dates and municipality | Record move dates and which municipality administered your address on January 1 | If you move after January 1, that municipality may still be the one you must pay |

| Forest Environment Tax and reserve | Add Forest Environment Tax at JPY 1,000 annually to your local-tax estimate and set reserve funds before June | Payment notices are often sent around June, and some municipal guidance says around mid-June |

Local inhabitant tax (residence tax or juminzei) is levied by city and prefecture based on income from January 1 to December 31 of the previous year. Municipal guidance also states the January 1 trigger applies regardless of nationality.

In practice, the municipality ledger is the key checkpoint. If you move after January 1, the municipality that administered your address on that date may still be the one you must pay.

Timing is the common execution risk. Payment notices are often sent around June, and some municipal guidance says around mid-June. Build your reserve before notices are issued, then confirm exact timing with your municipality.

Include Forest Environment Tax in the same plan. It is described as a national tax introduced in 2024 and collected in the local inhabitant-tax context, with a fixed annual amount of JPY 1,000.

Use this verification pass each year so local timing does not surprise you:

- Confirm your January 1 entry in the local municipality ledger and keep proof.

- Reconcile prior-year income totals for the January 1 to December 31 period.

- Record move dates and which municipality administered your address on January 1.

- Add Forest Environment Tax at JPY 1,000 annually to your local-tax estimate and set reserve funds before June.

Reserve planning is easier when you spread it across the year. Set a monthly reserve check in your income log, then compare the running estimate to your expected local burden before notice season. You are not trying to predict the bill perfectly. You are trying to avoid a cash surprise when notices arrive.

Stop Using the 183-Day Shortcut as Your Primary Rule#

Use day count as a quick signal, not your primary rule.

Classification should be based on continuity and domicile facts, not a single 183-day cutoff. The OECD summary for Japan points to Income Tax Act Article 2(iii). It says the resident definition includes an individual who has had a residence in Japan continuously for one year or more. It also cites the Order for Enforcement of the Income Tax Act, where Article 14 and Article 15 set opposing domicile presumptions.

| Test | Legal anchor | What to verify now |

|---|---|---|

| Continuity of residence | Income Tax Act Article 2(iii) | Timeline and records showing continuous residence in Japan for one year or more |

| Presumption toward domicile in Japan | Order for Enforcement of the Income Tax Act Article 14 | Whether your occupation normally requires residing in Japan continuously for one year or more |

| Presumption toward domicile abroad | Order for Enforcement of the Income Tax Act Article 15 | Whether your occupation normally requires residing abroad continuously for one year or more |

This two-part check is practical in mixed-tie years. If your facts point both ways, do not force a quick classification.

Before you file, run a hard evidence pass: travel log, contract dates, and documents stating expected work location and duration. Test those records against the one-year continuity standard and the Article 14 or Article 15 presumption that best fits your occupation. If records conflict, document your position and what remains uncertain.

Do not cherry-pick the day count that gives you the result you want. Start with the full timeline, then test continuity and domicile presumptions against that timeline. If one document contradicts another, keep both in the file and note why the conflict matters.

The tradeoff is simple: shortcuts feel faster, but mixed-tie years can create cleanup risk. If your result may depend on treaty residence outcomes, escalate treaty residence review early rather than relying on memory.

Stress-Test Common Edge Cases Before You File#

Edge cases are where filing positions break, so make decisions from documents first and treat uncertainty as a task to close before returns are drafted.

Start by comparing two timelines that may look similar but carry different review risk:

- Mid-year arrival with ongoing contracts and open-ended living arrangements.

- Short assignment with a defined end and clear return plans outside Japan.

If those records point in different directions, do not force a clean answer from memory. Flag it for treaty-level review early, especially when family location, work location, and major assets are split across countries.

Use this pre-filing stress test before drafting returns:

- Build a dated timeline for arrivals, departures, contracts, and housing periods.

- Mark where work was actually performed during each period.

- Note where family and major assets were centered during each period.

- Write one line for your current position and one line for what could overturn it.

One risk is claiming non-resident treatment because travel was intermittent, while the full file supports a resident-treatment position. Document the conflict and escalate before filing.

Another problem is using contract labels as a shortcut for where work happened. If your contract language and your actual work-location evidence are not aligned, review risk rises fast. Reconcile that mismatch before your return is drafted.

For U.S. persons, run a separate U.S. return red-flag check. U.S. citizens and resident aliens abroad are taxed on worldwide income and generally keep the same U.S. filing requirements as those living in the United States. Benefits like the Foreign Earned Income Exclusion or Foreign Tax Credit still require filing a U.S. return, and an automatic two-month extension may apply while interest can still accrue from the regular due date on unpaid tax.

If your outcome depends on cross-border residence treatment, escalate with a complete packet: timeline, contracts, housing records, and a short issue summary. The U.S.-Japan convention includes Residence and General Treaty Rules articles, which is enough to trigger review but not enough to self-confirm an outcome.

Build a Defensible Evidence Pack You Can Hand to an Adviser#

Build one evidence pack for the tax year so an adviser can verify your timeline, income records, and filing readiness quickly before submission.

Use one folder with five tabs so your adviser can check facts quickly:

| Folder tab | Put these records in it | What your adviser can verify fast |

|---|---|---|

| Timeline | Entry and exit dates, contract start and end dates, housing start and end dates | Whether your fact pattern is consistent across the year |

| Contracts and work proof | Signed contracts, scope changes, invoices, and work logs | Whether your business records line up with your timeline |

| Income and remittance | Payment records, transfer notes, and consistent internal labels | Whether your cash-flow mapping is internally consistent |

| Official correspondence | Tax-related notices and correspondence you received | Whether notice dates and details align with your main timeline |

| Filing identity | My-Number details and identification documents | Whether filing can proceed without identity-related delay |

Anchor the pack to the filing calendar for 2025 taxable income. Cover January 1 to December 31, 2025, file from February 16 to March 16, 2026, and complete payment before March 16, 2026. If you expect a refund, the tax office may accept final returns before February 13, 2026. Put these dates at the top of your index.

Treat My-Number as an early readiness item. If you have a My-Number, enter it on the return and keep the related identification documents in the same folder as your draft return.

A clean index saves time in adviser review. Put a one-page index at the front with document name, period covered, and why the document matters. Use consistent file names so timeline, income, and remittance records can be cross-checked quickly.

A monthly close helps keep evidence current and usable:

- Update travel, contract, and housing timeline entries.

- Add new payments and apply the same internal labels.

- Append remittance notes while details are easy to confirm.

- Save new tax-related correspondence and note the relevant period.

- Track missing documents with an owner and retrieval date.

If the file cannot explain the full year in one read, pause and close evidence gaps before finalizing.

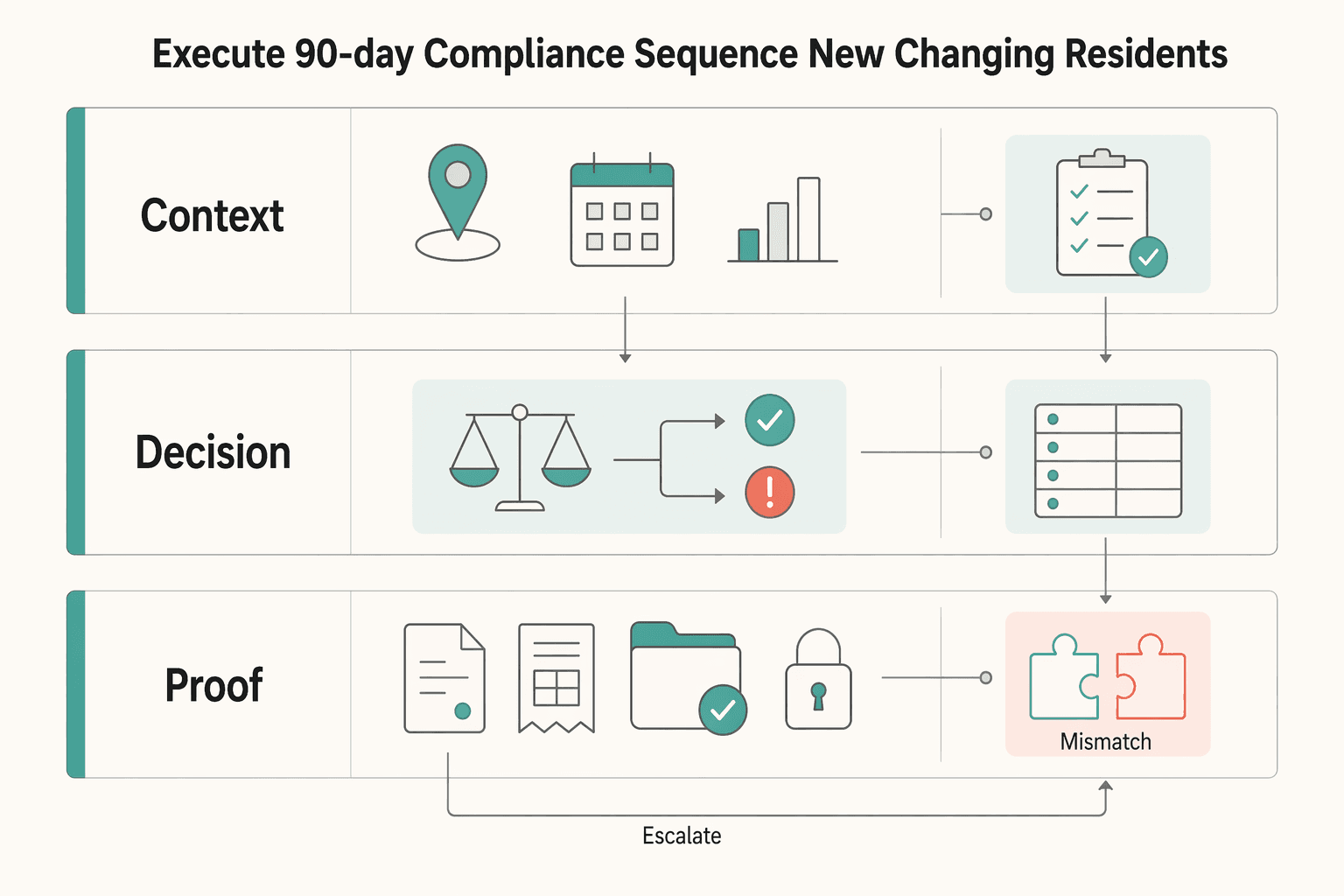

Execute a 90-Day Compliance Sequence for New or Changing Residents#

Use this 90-day sequence as a planning cadence, not a legal deadline. The objective is to reduce ambiguity early so your filing position is based on consistent records, not memory.

| Day range | Main task | What to produce |

|---|---|---|

| Days 1-15 | Confirm facts and registration posture | Short fact memo with move dates, living arrangement, work-location pattern, and registration steps |

| Days 16-45 | Split income and estimate likely exposure | Income map, provisional taxpayer-category view, and working estimate of likely exposure |

| Days 46-75 | Reconcile records while details are fresh | Income totals tied to statements after documented adjustments and a short exception log with issue, owner, due date |

| Days 76-90 | Escalate unresolved risk with a focused adviser brief | Fact memo, income map, reconciliation exceptions, relevant correspondence, and written decisions on open points |

Days 1-15 confirm facts and registration posture#

Create a short fact memo with move dates, living arrangement, work-location pattern, and any ties that could affect how your situation is interpreted. Track registration steps already completed and anything still pending. By day 15, a third party should be able to follow your timeline without filling in gaps.

Keep this memo plain and specific. If a date is uncertain, mark it clearly as pending verification instead of writing around it.

Days 16-45 split income and estimate likely exposure#

Tag each payment by source, where work was performed, how it was paid, where it landed, and whether funds were remitted. Use that map to draft a provisional taxpayer-category view and a working estimate of likely exposure. If any stream is unclear, mark it as unresolved and carry it into adviser review instead of forcing a weak assumption.

At this stage, consistency matters more than perfect precision. The goal is a defensible draft position that can be reviewed, not a polished final conclusion built on missing records.

Days 46-75 reconcile records while details are fresh#

Reconcile invoices, receipts, account statements, and remittance notes as one chain. Assign an owner and target date to every mismatch so unresolved items do not drift. By day 75, your income totals should tie to statements after documented adjustments.

Use a short exception log with three fields: issue, owner, due date. That single log prevents unresolved mismatches from disappearing between reviews.

Days 76-90 escalate unresolved risk with a focused adviser brief#

If cross-border risk or category ambiguity remains, run a pre-filing review. Share a concise brief with your fact memo, income map, reconciliation exceptions, and relevant correspondence, and request written decisions on open points.

Frame adviser questions so they can be answered directly. Ask for a position, the evidence needed to support it, and what could change the answer.

Keep one policy watch item in that brief. Public reporting has described proposed measures that could require incoming tourists to carry private health insurance, potentially deny entry without proof of insurance, and eventually tie some visa renewals to proof of insurance and tax compliance, with possible re-entry consequences for defaulters. Treat this as a monitoring item until official rules are confirmed. You might also find this useful: How to Create a Secure Backup Strategy for Your Freelance Business.

Know Exactly When to Bring in a Professional#

Bring in a professional when your facts still support more than one filing position after your 90-day cleanup. If key points remain ambiguous, waiting usually increases risk and rework.

Escalation Triggers That Should Not Wait#

Escalate when dual-country facts are in play and you cannot defend one residence position cleanly from your records. When residence and source questions are both open, this is a technical issue, not a paperwork detail.

Use a simple test: if two competent reviewers can read the same timeline and reach different conclusions, pause filing prep and get adviser input. Bring the documents behind the disagreement, including your timeline, municipality records, and fact memo.

Category and Source Mapping Red Flags#

Escalate if your resident vs nonresident classification is still unsettled after reconciling dates and ties. You do not need to solve every edge case first, but you should clearly show where evidence conflicts.

Escalate if you cannot confidently split source-based income treatment, for example Japan-source vs foreign-source, at the transaction level. Each material payment should have source tagging, work-location support, and remittance notes that match statements.

When you escalate, do not send raw files without context. Include a short cover note that states your current position, your competing position, and exactly which records support each view.

U.S. Filing Overlay and the Adviser Packet#

If you are a U.S. person, include U.S. filing context even when your Japan position looks stable. U.S. guidance states that citizens and resident aliens abroad are taxed on worldwide income, and a filing requirement can still apply even when exclusions or credits may reduce liability. It also notes that an automatic extension for eligible taxpayers abroad does not remove interest exposure from the regular due date.

Bring one complete packet so decisions can be made in one pass:

- Timeline with move dates, housing, and work-location facts

- Source tagging sheet for each income stream

- Remittance history tied to statements and transfer notes

- Municipality correspondence and registration records

- Open-issue log, including possible tax treaty residence and source-rule questions

- U.S. filing context, including whether a U.S. return filing requirement may apply

If one review cycle still does not produce a conclusion, treat that as a high-risk signal. Narrow the open questions, gather missing proof, and re-review before filing.

Take the Low-Stress Path and Document as You Go#

Use a simple hierarchy: anchor decisions in controlling legal text, use guidance as support, and escalate early when facts do not line up cleanly.

For residency and treaty-position questions, treat each conclusion as a documented test, not a filing-season guess. Keep your timeline, income tagging, and filing position aligned so someone else can follow your logic from records alone.

A practical guardrail from OECD MAP materials is that MEMAP is process guidance, not binding law. It does not change treaty rights or obligations, and it is not a substitute for controlling convention or higher guidance. If guidance and controlling text conflict, follow controlling text.

Turn this into a personal checklist tied to your own situation:

- Track move and address facts in one timeline.

- Keep income-source and remittance notes current for material payments.

- Keep a filing calendar and flag unresolved assumptions in plain language.

When facts stay mixed, take the conservative path and escalate before filing on assumptions. If a treaty dispute may arise, ask early whether MAP should be considered and what documentation is needed now.

Before next month starts, run one practical check: can someone else read your file and reproduce your current position without asking you to fill gaps from memory? If the answer is no, focus on closing that gap first.

Frequently Asked Questions

What makes you a tax resident in Japan?

A practical baseline is address-based: one source describes a resident as someone with an address in Japan or a residential address there for more than one consecutive year. Residency is determined by your actual facts, not just labels. Use your timeline and address records to support the position you file.

How are permanent, non-permanent, and non-resident taxpayers taxed in Japan?

Tax scope depends on resident-status classification. For residents other than non-permanent residents, the described scope includes all income, including foreign-sourced income. A non-permanent resident is described as a non-Japanese resident with an address or residential address in Japan for 5 years or less in the past 10 years, and tax-purpose status should not be confused with immigration-law permanent residence.

When do I owe local inhabitant tax or residence tax in Japan?

A key trigger shown in guidance is whether you have a residential address as of January 1 of the year. Keep municipality records consistent with your move timeline. Also align that with the January 1 to December 31 income-tax period when reconciling filings.

Do foreigners pay a different residence tax system than Japanese nationals?

Guidance states that foreign nationals residing in Japan are included. The materials here do not show a separate basic structure based only on nationality. Classification and records still drive the outcome.

Is 183 days enough to determine Japan tax residency?

No, not on its own. A universal 183-day pass or fail rule is not supported here. If your address facts and income facts conflict, treat it as a professional-review case.

What tax treatment applies if I have Japan employment income but think I am non-resident?

In SOFA-status situations, Japan-source income can still create Japanese income tax liability even when someone is treated as non-resident. In practice, source analysis is still required before filing. If your records do not support one clear position, escalate before filing.

When should I use treaty tie-breaker rules and talk to a professional?

Use treaty-level review when two countries may both claim residency or when your residence and source conclusions do not line up cleanly. For U.S.-Japan cases, the Technical Explanation is an official guide to interpreting the Convention. Bring complete records so advice is based on documents, not memory.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Taxes in Italy for Expats and Freelancers

Start with one objective: make filing choices you can defend with records, not assumptions. As a freelancer or consultant, you do not need to predict every line item on day one. You need a position that stays consistent from client onboarding to invoicing to return prep. The avoidable mistake is signing work or claiming a benefit first, then trying to explain the tax result later. You are aiming for a position that holds together all year, not a best-case assumption that falls apart when forms and bank records have to match.

How to Create a Secure Backup Strategy for Your Freelance Business

Build backup for recovery speed, not storage volume. Your setup should let you keep delivering and getting paid after equipment failure, cyberattack, human error, natural disaster, or other data-loss events. A reliable baseline matters, but the real test is whether it stays usable when stress is high and decisions need to happen fast.