Quick Answer

Use a multi-currency FX calculator as planning input, then approve and execute from a controlled record. Visa’s own calculator language shows why: it is an indication and final billing can differ by bank fees, conversion path, or processing context. For platform payouts, the safe approach is to capture source, quote time or exchange date, fee assumptions, and transaction linkage before release, and reject incomplete inputs rather than reconciling guesses later.

Where FX Calculation Fits in Platform Payout Controls#

A multi-currency FX calculator is useful for planning, but it is not a guaranteed source of truth for what will settle. In practice, issues often appear when the rate source, fee assumption, and effective timestamp used for a payout batch do not match the facts later referenced in approvals, ledger journals, or reconciliation.

That distinction matters because some calculators are explicitly indicative. Visa's Exchange Rate Calculator says it gives an indication of the rate you may receive for international card use, and it also notes that a bank may use a different rate and add foreign transaction fees. If a merchant or ATM operator performs the conversion, the calculator rate does not apply at all. For operators, the takeaway is simple: calculator output can support planning, but it cannot replace settlement evidence.

The real control point is not the conversion screen. It is the moment you decide which rate source is allowed for a given job, who approved it, and which exact facts must travel with the transaction into payout batches and ledger journals. At minimum, store the source name, quote or lookup timestamp, fee logic, base and target currencies, and the internal batch or transaction ID that ties the conversion to the payout release. If those fields are incomplete, reconciliation gets harder than it needs to be.

A common mismatch is small, not dramatic. One team models a batch with an indicative rate and no bank fee. Another books the journal using the same pair with a fee assumption. A third compares the settled amount against a later lookup done on a different date. Even when the currency pair is the same, the context is not, so the variance can look mysterious when it is actually process drift. Visa's calculator UI shows how sensitive this is by allowing a bank-fee input, including an example of 2%. That does not make 2% a default or universal fee, but it does show why fee assumptions must be captured, not guessed.

You should also expect source behavior to change over time. Visa notes a VisaNet currency conversion enhancement as of April 2021. The practical lesson is to keep the source, version context when available, and lookup date in your evidence pack instead of relying on memory or screenshots with no identifiers.

The goal of this article is a repeatable operating approach. Pick the right rate type for the job, execute conversions in the right order, and leave an audit trail that survives review. If your current process cannot replay a completed conversion from request to journal to payout batch without manual stitching, that is a red flag to fix.

Build the right FX mental model first#

Keep three buckets separate or you will manufacture variance. The useful question is not "what rate did we use?" but "what job was that rate meant to do?"

| Rate bucket | Use it for | Do not use it for |

|---|---|---|

| Indicative rate | Planning, scenario checks, and pre-approval estimates | Treating it as settlement evidence |

| Method-specific estimate | Understanding how one conversion method behaves versus another | Assuming it transfers cleanly to a different payout method |

| Reporting rate | Consistent reporting and normalization across periods | Real-time payout execution decisions |

A conversion-method estimate can drift from your payout result because the method can differ on both exchange rates and fees. If you compare methods, keep that distinction explicit instead of collapsing everything into one "FX variance."

For reporting, Federal Reserve H.10 data is updated every Monday at 4:15 p.m. and is available through Friday of the previous business week. It is useful for consistent reporting context, including formal uses, but it is not a real-time execution feed for payout release decisions.

If one team plans with an indicative rate, another normalizes with a reporting rate, and ops validates against a different method estimate, reconciliation noise is predictable, not accidental. Pick one rate type per job and record that purpose beside the number.

For payout architecture details, see How Platforms Build Multi-Currency Sub-Wallets for Contractors.

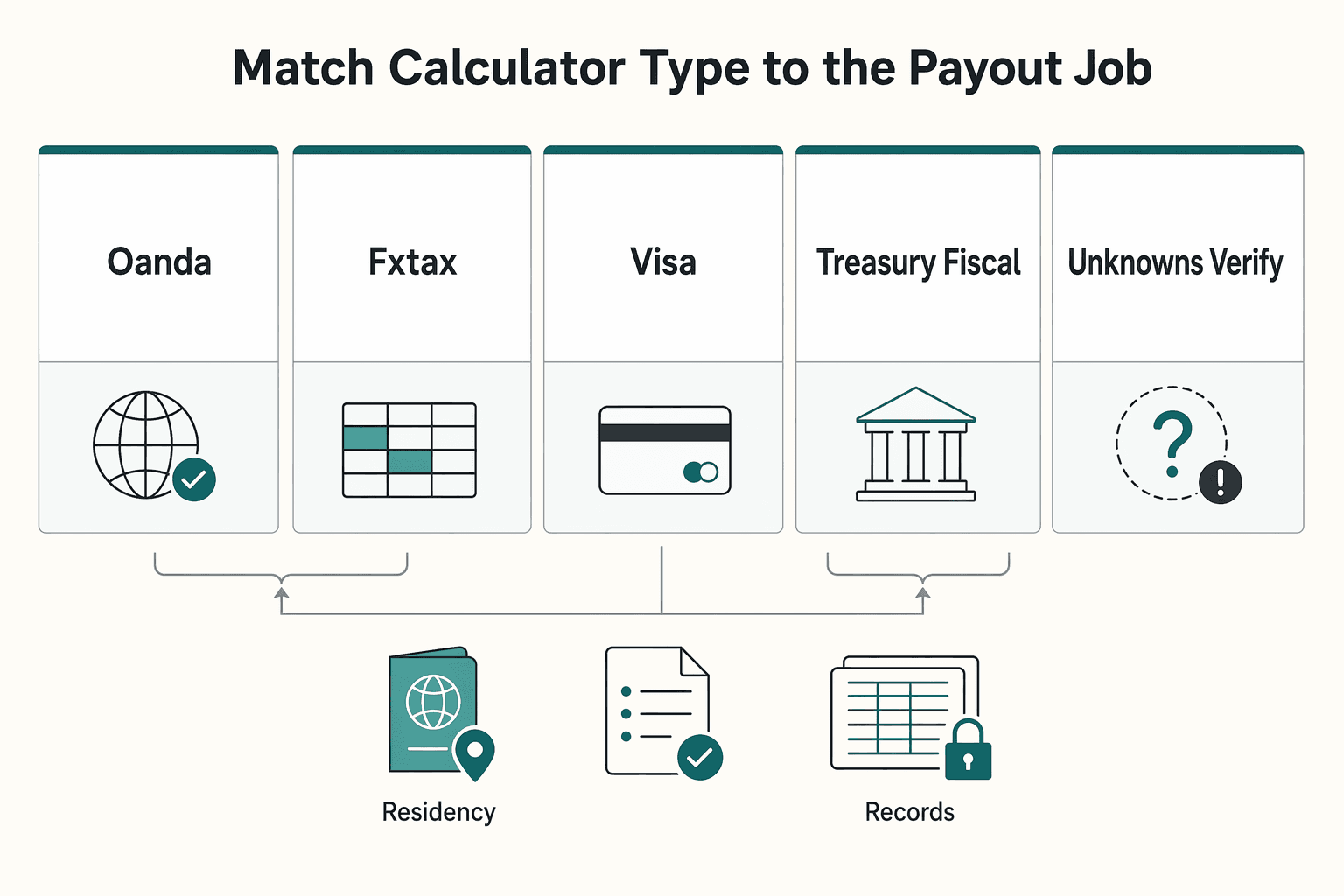

Match calculator type to the payout job#

Pick the calculator by payout job, then document that purpose before anyone uses the number downstream. In this section's evidence set, the capabilities of OANDA, FXtax, Visa Exchange Rate Calculator, and Treasury Reporting Rates of Exchange are not independently verified, so treat the table below as a routing policy template, not proof of tool behavior.

| Source | Source purpose | Execution fit | Caveats | Auditability |

|---|---|---|---|---|

| OANDA | Use only if your team has verified its role in your policy (for example, planning-only input). | Do not treat as settlement truth unless your execution source controls say so. | Confirm methodology, update cadence, and export/API behavior with the provider. | Capture source name, pair, amount, purpose label, and lookup timestamp. |

| FXtax | Use for pre-payout scenario planning across many corridors only if your team has verified matrix-style fit. | Planning fit only; do not promote directly into settlement assumptions. | Matrix behavior and data method are not evidenced here; verify before relying on it. | Store assumptions, owner, timestamp, and approval context. |

| Visa | Keep in a card-estimate bucket only, subject to your internal verification. | If used outside card contexts for settlement assumptions, stop and reclassify as non-settlement guidance. | Verify non-card settlement fitness with the provider. | Label as card-context guidance; do not file as payout rate of record. |

| U.S. Treasury Fiscal Data | Use for reporting consistency if your policy explicitly assigns that role. | Reporting-normalization fit only; not a substitute for live execution inputs. | Confirm update cadence, method detail, and technical access limits with the provider. | Reference the named reporting source in policy and workpapers. |

| Unknowns to verify | Source methodology, update cadence, and export/API limits when not disclosed. | Treat as unresolved until verified from provider documentation or controlled internal testing. | Unverified details can create false variance across teams. | Add a gap note; unlabeled outputs are not audit-ready evidence. |

Decision rule: if the task is pre-payout scenario planning across many corridors, route it to the planning bucket (for example, a verified matrix-style tool such as FXtax). If the task is reporting consistency, route it to your reporting-rate bucket (for example, Treasury Reporting Rates of Exchange) and keep that choice explicit in policy.

Before approval, require five fields on every calculator pull: source name, purpose label, currency pair, amount, and lookup timestamp. If any field is missing, reject the input and rerun.

Define conversion checkpoints before payout release#

Lock a fixed conversion sequence before release, and treat any post-approval change as a full re-approval trigger. Use the same order every time: rate source selection, quote timestamp or exchange date validation, fee assumption lock, approval, then conversion and release into payout batches.

Make the exchange date and quote time explicit#

Record the field that determines which rate applies. In Deltek's terms, the exchange date identifies the rate used from the daily table, and that same date's rate is used across currencies for that run. Operationally, do not let exchange date or quote timestamp live only in a provider screen.

Store that field with source name, currency pair, amount, and purpose label in the approval record. If conversion happens on different quote timing than what was approved, stop and requote instead of pushing it through as normal variance.

Treat pre-conversion checks as mandatory gates, not optional courtesy steps. If required checks are missing, fail closed and hold release.

| Checkpoint | Owner | Required evidence | Reject condition | Escalation path |

|---|---|---|---|---|

| Rate source selection | Finance ops or treasury | Named source, purpose label, currency pair, amount, selected exchange date or quote timestamp | Source is unlabeled, not approved, or mismatched to the job | Treasury lead or finance controller |

| Quote timestamp validation | Payout ops | Captured quote time, approval time, internal tolerance check | Timestamp missing or quote age exceeds internal tolerance | Requote with treasury or provider ops |

| Fee assumption lock | Finance ops | Fee logic/version used in approval and batch reference | Fees missing, changed after approval, or not aligned with conversion input | Finance controller and product owner |

| Approval | Designated approver | Approval record tied to source, timestamp, fee assumptions, and batch ID | Approval does not match conversion facts or lacks traceability | Controller or delegated approver |

| Conversion and batch release | Payout ops | Conversion reference, payout batches ID, posting link to ledger journals | Conversion executed on different facts than approved, or batch linkage missing | Hold batch and investigate |

Keep the same facts through approval and posting#

A checkpoint only works if the same approved facts carry into records and downstream events. For each payout, verify that source, exchange date or quote timestamp, fee assumptions, and internal reference match across approval evidence and ledger journals.

If a release input arrives without conversion context, hold it for review before posting. There is no universal stale-quote threshold in the source material, so define your own internal tolerance in policy and enforce it consistently: if quote age exceeds tolerance, reject and requote.

If you use any third-party method in this flow, validate it before using it as an approval input. The FDIC-linked comment points to principles for validating selected third-party approaches; your record should show why the source was chosen, what job it is allowed to answer, and who approved that use.

Related reading: How to Handle Currency Gain and Loss Reporting for a Multi-Currency Platform.

Prevent reconciliation drift across systems#

Drift starts when conversion context is split across systems instead of recorded once and reused. If source, timestamp or exchange date, fee logic, rounding treatment, and payout batches linkage are not stored with ledger journals, reconciliation turns into fragmented reconstruction, and those process gaps are a common cause of persistent errors.

Small mismatches also compound quickly. In high-volume operations, minor data-entry gaps and inconsistent rounding steps can become material risk, and even a one-cent mismatch can trigger payment failures and manual cleanup. Your control objective is deterministic output: the same inputs should produce the same cents everywhere.

Keep one canonical conversion record#

Use one canonical conversion record per execution path, and have downstream systems reference it instead of rebuilding values from fresh screens or later rate pulls. At minimum, keep:

| Record element | What to keep |

|---|---|

| Rate source | Rate source name |

| Timing field | Quote timestamp or exchange date |

| Currencies | Currency pair and amounts |

| Fee logic | Fee logic or version used at approval |

| Rounding rule | Rounding rule applied |

| References | Provider reference, internal conversion ID, and payout batches ID |

- rate source name

- quote timestamp or exchange date

- currency pair and amounts

- fee logic or version used at approval

- rounding rule applied

- provider reference, internal conversion ID, and

payout batchesID

Carry that same reference through API writes, webhooks, and posting into ledger journals. A practical check is parity on one completed payout: compare the API payload, the webhook event used by your consumer, and the journal support. If cents differ, investigate rounding or transformation logic; if IDs are missing in one layer, replay and auditability will still break.

Separate collection-side and payout-side FX context#

If your workflow has both collection and payout legs, keep their FX context separate rather than blending them into one record. Store each leg with its own timestamp, source, amount basis, and journal linkage, then connect them with a shared transaction or account reference.

That separation makes variance diagnosable. If you collapse both legs into one early "effective rate," you lose visibility into whether differences came from intake timing, payout timing, or rounding, and drift can stay hidden until close.

For a step-by-step walkthrough, see How to Reconcile Multi-Currency Payouts Across Multiple PSPs in One Ledger.

Apply compliance and tax gates before funds move#

Before any conversion or release into payout batches, confirm the payout is allowed for that lane. If a payee, business, or tax profile is not in an approved state under your program policy, stop early rather than unwinding amounts later.

Block before conversion, not after#

Use a policy-first gate for items like KYC, KYB, AML, VAT validation, W-8, and W-9 where your country, program, and counterparty rules require them. Coverage is not universal, so keep a machine-readable lane policy owned by legal and compliance instead of relying on memory.

| Checkpoint | Required state |

|---|---|

| Beneficiary or business status | Approved for that payout lane |

| Screening status | Clear or dispositioned per policy |

| Required tax profile | Complete for that lane, including W-8 or W-9 when required |

VAT validation | Recorded when that lane depends on it |

| Decision timestamp and reviewer/service reference | Stored with the same transaction record that posts to ledger journals |

A practical pre-release checkpoint is:

- beneficiary or business status is approved for that payout lane

- screening status is clear or dispositioned per policy

- required tax profile is complete for that lane, including

W-8orW-9when required VAT validationis recorded when that lane depends on it- decision timestamp and reviewer/service reference are stored with the same transaction record that posts to

ledger journals

This prevents a common failure mode: converting first, then discovering a hold and forcing funds into suspense while rates, fees, and settlement timing shift.

Tie tax treatment to transaction IDs#

Keep tax treatment tied to the same transaction identifiers used in ledger journals, not a separate spreadsheet keyed by names or emails. That matters for later review across topics like FEIE, FBAR, and 1099.

For FEIE, treat eligibility as conditional and year-specific. Under the physical presence test, eligibility requires 330 full days during any period of 12 consecutive months, and the days do not need to be consecutive; if 330 days is not met, the test is not met. Also, excluded foreign earned income is still reported on a U.S. return. IRS maximum exclusion amounts listed are $130,000 for tax year 2025 and $132,900 for 2026 per qualifying person.

Do not treat an IRS Practice Unit by itself as binding authority; it is instructional and not an official pronouncement of law. Final gate logic should be confirmed with legal/compliance owners for each program and country context.

Design failure handling for stale quotes and async provider events#

After compliance and tax gates, the core control is straightforward: handle failures in a way your team can explain, trace, and safely replay. Treat stale quotes, timeouts, duplicate retries, and settlement mismatches as different failure classes so each one gets the right next action.

Classify failures before you automate retries#

Use separate failure classes in the transaction record instead of one catchall status.

| Failure class | Required response |

|---|---|

| Stale quote rejection | Pause execution, requote, and reapprove if your policy requires it |

| Provider timeout | Resolve status first because outcome is unknown |

| Duplicate retry attempt | Stop re-submission and confirm whether the original intent already processed |

| Post-conversion settlement mismatch | Investigate why settled amounts or fees differ from stored conversion context |

Before any retry, confirm the payout intent ID, quote timestamp, quote/rate reference, and current provider status are all present on the same record. If any part is missing, resolve the record first.

Make retries replay the same intent#

Keep planning outputs from your multi-currency FX calculator separate from execution, then make execution retry-safe with one idempotency key carried across conversion and payout calls. One business intent should keep one key on safe retries, with the same amount, currency pair, and beneficiary details.

Store your intent ID with the provider request ID, webhook event ID, retry count, and final journal reference. If an API call times out after submission, do not immediately resubmit; first query by your own key or provider reference. If you cannot confirm failure, treat the request as pending and wait for status via webhooks.

Treat Virtual Accounts as state changes#

For Virtual Accounts, model delayed credits, returns, and late notifications as asynchronous state changes tied to the original payout intent. Do not treat them as new transactions with reconstructed context.

Keep each event linked to the intent ID, conversion record, and ledger journals entry. If a delayed return arrives, post it as its own event against that same ID chain so operations can trace funding, beneficiary-detail, or settlement-timing issues cleanly.

Set the minimum evidence pack for audit replay#

Your evidence pack is only good enough if another operator can replay a completed conversion end to end without manual reconstruction.

Use a compact record plan and inventory for each conversion, and keep an indexed chain that includes:

- the source reference used for the rate decision and its timestamp

- explicit status tracking, plus any validity window fields your workflow uses

- stable IDs that link request, execution, posting (

ledger journals), and export artifacts

Keep this organized like a bank record index plus a status log: each step should show where the record lives and how to traverse to the next one. If key links are scattered across unindexed payloads or side channels, replay breaks when you need it most.

Run a periodic replay sample on completed conversions from request to posting to export. If a sample still requires manual stitching, your evidence pack is too thin.

For reconciliation workflows, see Xero Multi-Currency for Payment Platforms: How to Reconcile Foreign Currency Payouts.

Conclusion#

A strong multi-currency FX calculator process is usually won by classification, not by tool shopping. The practical question is not "which calculator is best?" It is "which rate type belongs to this decision, and what evidence do we keep with it?" Once you separate planning rates, execution context, and reporting rates, much of the noise that shows up later in reconciliation becomes predictable and preventable.

That distinction matters because not every visible rate is built for the same job. OANDA states that its converter tools use OANDA Rates compiled from leading market data contributors, and that displayed values represent daily average Bid and Ask rates from many data sources. That is useful context for planning and comparison, but displayed converter output should not be treated, on its own, as proof of an executed settlement rate. If your team cannot point to the source class, quote timestamp, fee assumptions, and approval record, the number is not ready to drive a payout release.

The operational win comes from connecting calculator choice to the rest of the payout path. In Gruv workflows, your conversion checkpoint should use the same facts that later reach payout batches, ledger journals, and exports. A simple verification rule goes a long way: before release, confirm that the stored source name, captured timestamp, pair orientation, and fee logic all match the approval record. If any one of those is missing, stop and requote or reapprove instead of trying to explain the mismatch after settlement.

There is also a quieter risk that teams miss when they document their process. On the same OANDA page, the history length is presented both as "Over 31 years" and "over 32 years," so if you are writing policy notes or internal controls, verify the exact wording before copying it into documentation. That sounds minor, but inconsistencies like this can make process documents drift away from the tools operators actually use.

The next move should be concrete. Put the checkpoint table and evidence requirements into your current payout flow, even if you start with one corridor and one approval path. Pick a high-volume currency pair where timing or fees often create variance, run the new controls there first, and replay a few completed transactions end to end. If the same conversion record can be traced from decision to posting to export without hand stitching, you are in a much better position to scale the calculator, the approvals, and the reconciliations together.

Frequently Asked Questions

Which multi-currency FX calculator type should platform payout teams use for planning versus reporting?

Use a multi-currency FX calculator with indicative market rates for planning, scenario checks, and corridor comparison before approval. For reporting, use the source your finance policy names so month-end and audit views stay consistent. Keep those jobs separate, because planning output should never be treated as settlement evidence.

What is the practical difference between indicative rates, card-network estimates, and government reporting rates?

An exchange rate is the relative price of one currency in terms of another, but the source changes the purpose. Calculators can help compare market rates with bank, card, and airport rates, but those outputs are still estimates rather than guaranteed settlement outcomes. Keep reporting-rate usage aligned to your internal policy, and avoid mixing source types inside one approval or reconciliation path.

Why can final settled amounts differ from calculator outputs even when teams used the same currency pair?

The biggest reasons are provider choice and fees or markups applied outside the calculator. MultiPass explicitly notes that the provider affects the rate you actually exchange at, so matching the pair alone does not guarantee matching results. A basic check that catches real mistakes is pair orientation: in a pair like EUR/USD, the first currency is the base and the second is the quote. If the pair is reversed or the rate is copied incorrectly, the amount can be distorted immediately.

What are the minimum controls to approve FX inputs before releasing payout batches?

Require one record that holds the named source, the quote timestamp captured at decision time, the fee assumptions used in approval, and the approver or approval reference. If the quote is older than your internal tolerance, reject it and requote rather than pushing it into payout batches. Before release, verify that the same rate context will flow through to ledger journals, not just sit in an approval spreadsheet.

How can teams compare multiple currencies at once without introducing reconciliation drift?

Use one source class and one capture window for the whole comparison. Then bind every corridor in that comparison to the same internal intent ID or approval record. If you need a matrix view, export all rows from the same tool at the same time instead of stitching one rate from a market calculator, another from a card quote, and another from a reporting table. The common failure mode is mixed-source comparison followed by single-source reconciliation.

Which exact fields must be logged to make FX decisions audit-ready and replayable?

At minimum, log the selected source, timestamp, fee assumptions, approver name or reference, payout batch ID, internal intent ID, provider request or transfer reference, conversion record ID, ledger journal reference, and export file or report ID. If the number came from a planning tool, label it as planning evidence so nobody reuses it as executed-rate proof. A replay test should let another operator trace request to posting to export without opening Slack or reconstructing context by hand.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cameroncountytx.gov/wp-content/uploads/2021/07/DCICN-200-150.pdftrusted

- fdic.gov/resources/regulations/federal-register-publi...trusted

- federalreserve.gov/releases/h10/histtrusted

- hartford.edu/about/offices-divisions/finance-administrati...trusted

- irs.gov/individuals/international-taxpayers/figuring...trusted

- irs.gov/individuals/international-taxpayers/foreign-...trusted

- newhaven.edu/faculty-staff-profiles/brian-marks.phptrusted

- ojp.gov/pdffiles1/Digitization/174809NCJRS.pdftrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How to Handle Multi-Currency Pricing for Your SaaS Product

**Treat SaaS multi-currency pricing as a get-paid system, not a checkout feature.** If you only localize the price label, you miss the points where margin and cash timing break. As the CEO of a business-of-one, your job is to make "getting paid" boring and predictable, even when you sell globally. Start by linking presentment, settlement, and payout so your setup can absorb delays and FX movement as you expand.

Intacct vs. NetSuite for Payment Platforms: Which ERP Handles Multi-Currency and High-Volume AP Better

Treat this as an integration-debt decision first, and an ERP comparison second. For payment platforms, multi-currency accounting and higher-volume AP risk usually shows up at the seams between product behavior, finance controls, and integrations, not in top-level feature lists.

Let Clients Pay in Local Currency with Multi-Currency Payment Links

Multi-currency payment links can speed up international collection, but the harder decision is operational: will your FX, settlement, and reconciliation setup produce the outcome finance and ops expect after payment?