Quick Answer

Use a staged close sequence: freeze payout batch inputs, reconcile instruction records before status events, then tie settlement evidence to general ledger and ERP postings. For monthly payout reconciliation 1000 contractors, require item-level keys (internal payout ID, provider reference, idempotency key) and keep one close pack per batch with statement exports, webhook history, and sign-off. If terminal states conflict or evidence is missing, hold that item from reporting and route it to exception ownership.

Monthly Payout Reconciliation at Scale Is an Operating Control, Not Clerical Cleanup#

Monthly payout reconciliation at this scale is an operating control, not clerical cleanup. When you are paying a large contractor base every month, the hard part is not exporting totals. It is deciding which record counts as truth, proving that each payout state is backed by evidence, and stopping unresolved breaks from bleeding into finance reporting.

Treat month-end close as an operating process#

Month-end close is an operating process, not bookkeeping cleanup. It finalizes the previous month's activity, and payment reconciliation is the matching work that checks transaction records against accounting records and bank-side evidence. Together, they answer three basic questions: what did you intend to pay, what actually happened, and what did finance record?

That framing matters because scale creates ambiguity quickly. A payout can be initiated in one tool, acknowledged by a provider in another, and posted into the general ledger or ERP later. If you cannot trace a single payout from internal payout ID to provider reference to ledger result, you do not have a reliable close. You have partial records that happen to line up some of the time.

Build the close around evidence#

Run the close on evidence, not assumptions. A practical approach is ledger-first: the general ledger is the accountable financial record, and provider statuses, statements, and event exports are supporting proof. That gives finance, ops, and product a shared basis for review instead of forcing each team to argue from dashboards built for different jobs.

A practical checkpoint is simple. For every finalized payout batch, you should be able to find a provider acknowledgment, a status trail that explains where the payout ended up, and a corresponding ledger outcome. Keep that evidence pack together. In practice, that usually means the batch file, provider statement or export, status-event export, and sign-off record live in one review set instead of being scattered across email threads and screenshots.

Separate timing differences from real exceptions#

Not every mismatch is an error. Payment reconciliation helps surface irregularities, but timing gaps can come from asynchronous status updates, settlement delays, or compliance and eligibility checks. Those need a defined path, not panic.

A failure mode to watch for is forcing a manual override because month-end is approaching. If a provider view says a payout is complete but the ledger has no matching journal, hold reporting output for that item and route it into exception review. Do the same if the ledger shows a payout without external evidence. A close that is slightly slower but well supported is more useful than fast numbers you cannot defend later.

This guide is for finance, operations, and product owners who need predictable payment reconciliation at scale. The goal is decision-ready monthly close data that is accurate enough to trust, documented enough to audit, and structured enough to improve month after month.

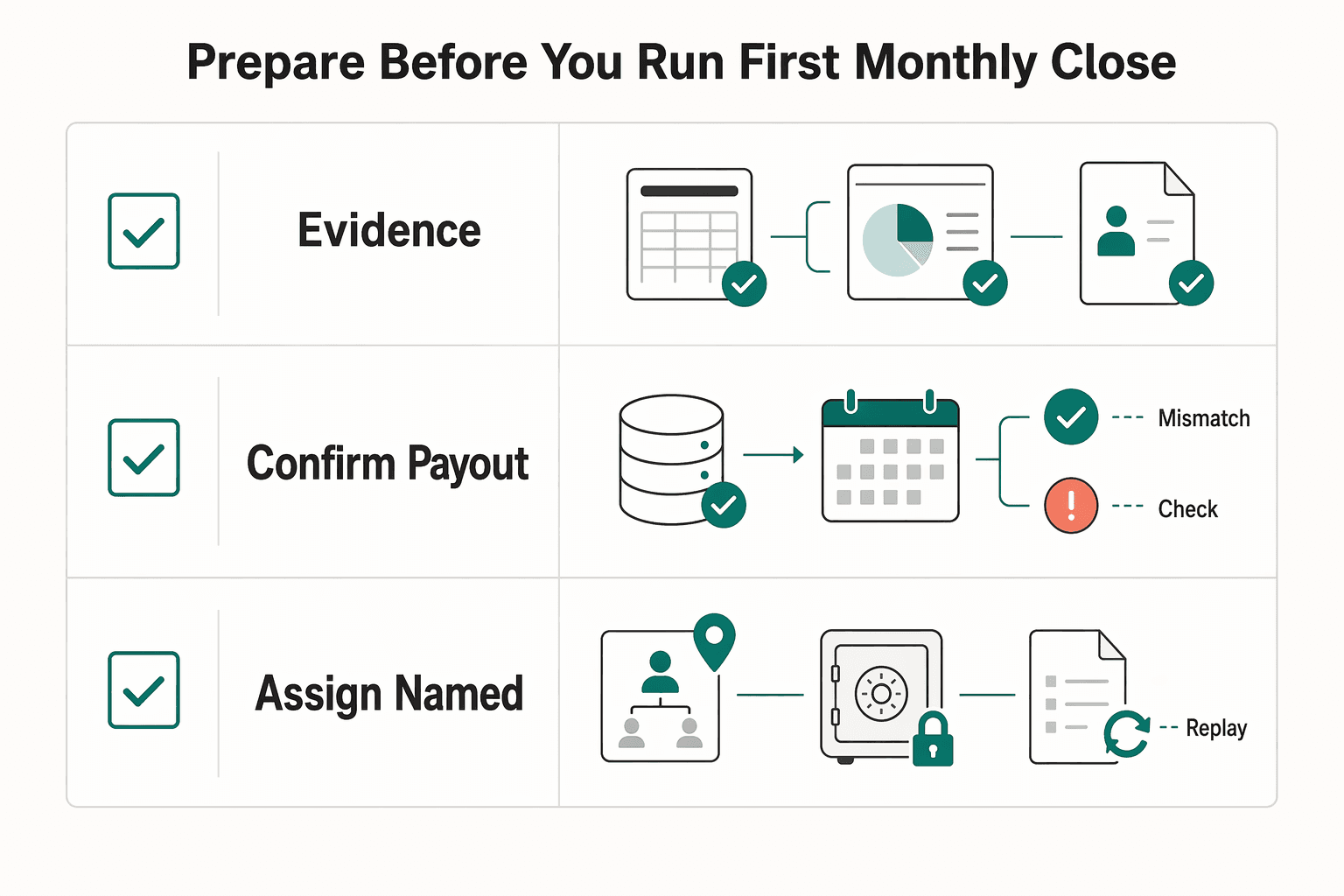

What to prepare before you run the first monthly close#

Your first monthly close will only hold up if boundaries, eligibility inputs, cutoff evidence, and ownership are fixed before month-end pressure starts.

| Step | Focus | Key control |

|---|---|---|

| Define record boundaries | Set the general ledger as the accountable financial record, the ERP as the reporting surface, and provider statuses as external evidence | Confirm subledger transactions are imported and period journal entries are posted |

| Confirm payout eligibility inputs | Verify KYC and AML checks, and confirm Form W-9 or Form W-8BEN where needed | Treat missing compliance or tax documentation as eligibility exceptions; capture VAT status before close if relevant |

| Freeze the cutoff evidence | Lock the close pack to finalized payout batch files, provider statements by settlement rail, and webhook event exports | Confirm period coverage and keep version control on exports |

| Assign named owners | Use a RACI matrix for approvals, reconciliation review, exception triage, and final sign-off | Keep a clear owner for disposition decisions |

Step 1. Define record boundaries. Set the general ledger as the accountable financial record, the ERP as the reporting surface, and provider statuses as external evidence. Write this down so teams are not debating the source of truth during close. Before you run reconciliation reports, confirm subledger transactions are imported and period journal entries are posted.

Step 2. Confirm payout eligibility inputs. Treat missing compliance or tax documentation as eligibility exceptions, not reconciliation mismatches. Verify required KYC and AML checks are complete for your program. Confirm tax forms are present where needed: Form W-9 for payees providing a TIN for information returns, and Form W-8BEN for foreign beneficial owners providing the form to the payer or withholding agent. If VAT treatment is relevant in your supported jurisdictions, capture that status before close.

Step 3. Freeze the cutoff evidence. Lock the close pack to finalized payout batch files, provider statements by settlement rail, and webhook event exports showing asynchronous status changes. Confirm period coverage and keep version control on exports. Mid-close file refreshes without controls quickly break the audit trail.

Step 4. Assign named owners. Use a RACI matrix so approvals, reconciliation review, exception triage, and final sign-off each have a clear owner. This matters most when ops evidence and finance postings disagree. If no one owns disposition decisions, unresolved breaks carry into reporting deadlines and force bad overrides.

Map every record that must tie out each month#

Start by making each payout traceable end to end before you match amounts. If a payment cannot be followed across the payout request, provider evidence, webhook history, general ledger journal, and ERP posting, fix mapping first.

Step 1. Build a reconciliation matrix before amount matching. Define, for each object, the join key, owner, and month-end evidence.

| Object | Must tie to | Key to store | Month-end check |

|---|---|---|---|

| Payout request | Provider transaction or payout reference | Internal payout ID | Request exists and amount/currency match approved instruction |

| Provider record | Webhook event logs | Provider reference (for example PSP reference, resource ID, or order reference) | Reference is findable in provider logs and statements |

| Webhook status | Provider record and internal payment state | Event timestamp plus provider reference | Events process in timestamp order with no unexplained status gaps |

| General ledger journal | Settled or returned payment activity | Internal payout ID or mapped provider reference | Journal reflects validated money movement |

| ERP posting | General ledger journal | Journal identifier | ERP agrees with posted ledger entries for the close period |

Quick control: sample one payment and prove you can trace both directions, from payout evidence to the underlying transaction batch and from original request to ERP posting.

Step 2. Require a retry-safe key chain. For each payment, retain your internal payout ID, provider reference, and the idempotency key used on create/update flows. This gives you a defensible retry trail and helps separate duplicate attempts from real payment changes.

Step 3. Separate event classes by settlement rail. Use your close taxonomy (for example initiated, submitted, settled, returned, held, reversed) and map provider labels into it by rail. Do not assume the same label means the same accounting state across rails.

Step 4. Document expected timing drift. Treat asynchronous webhook timing and FX quote validity as normal reconciliation factors. Reconcile webhook events by timestamp, and account for provider retry behavior when acknowledgments are delayed (some providers retry after a failed acknowledgment window, such as 10 seconds). For FX, store quote ID, quoted rate, creation time, and validity window (for example 5 minute, 1 hour, or 24 hour options where supported) so expired quotes are reviewed as timing drift, not unexplained breaks.

Set a close calendar and ownership model your team can actually run#

Once every record is traceable, close performance depends on execution discipline: a dated calendar, one accountable decision owner per deliverable, and a hard gate before sign-off.

Put the close on dated phases#

Use dated phases, not a vague "finance week." A practical baseline is Workdays 1 to 5 for closing monthly results, then Workdays 6 to 10 for reconciliations, review, lessons learned, and any post-close adjustments. Your exact dates can vary, but handoffs should be fixed and published before the month starts.

| Phase | What must happen | Primary output |

|---|---|---|

| Cutoff | Freeze payout inputs for the period | Approved cutoff list and frozen source extracts |

| Ingestion | Load provider files, webhook exports, and ledger activity | Timestamped import confirmation |

| Matching | Run joins across payout IDs, provider refs, and journals | Match report with open breaks |

| Exception triage | Assign and investigate unmatched or high-risk items | Exception log with owner and status |

| Approval | Named approver reviews the close package | Signed approval record |

| Final lock | Prevent further GL-impacting postings for the closed period | Period lock confirmation |

Treat each phase as incomplete until its artifact exists and is retained.

Make one person accountable for each deliverable#

Use a RACI matrix and keep accountability singular. Each task can have multiple contributors, but only one person should be accountable for the deliverable or decision. When unresolved breaks appear, unclear decision rights are a common reason close work drifts.

Make the exception owner explicit in the exception log. For each open item, capture the exception type, date opened, first acknowledgment time, accountable decision owner, current disposition path, and whether it blocks close. Keep exception SLA language clear: response time is the time from issue submission to formal acknowledgment, not final resolution.

Set a gating rule for sign-off and lock#

Do not sign off just because the calendar reaches a target day. Sign off only when unresolved exceptions are below your approved threshold and all high-risk items are formally dispositioned (for example, cleared, held, or tracked with an approved journal entry and root cause).

A closed period should not still accept cleanup GL-impacting postings. Final lock is part of close control and should stop additional GL-impacting entries after sign-off. Your close evidence pack should include the calendar, RACI matrix, exception log, approval record, and lock confirmation.

Reconcile in order so upstream errors do not contaminate downstream reports#

Use this operating order for close: instruction integrity, status progression, money movement, then finance outputs. Starting with bank or ERP totals can make bad upstream data look valid and create false breaks later.

| Order | Check | Verification artifact |

|---|---|---|

| 1. Instruction integrity | Compare the frozen payout batch at cutoff against payout API acknowledgments; confirm payout ID, amount, currency, and provider reference where available | Instruction match report with approved batch count, acknowledged count, matched amount total, and explicit rejects or missing acknowledgments |

| 2. Status progression | Match webhook lifecycle events to provider dashboard data or the latest provider resource state; quarantine contradictions or regressions | Duplicate-safe event reconciliation, with retry handling because undelivered webhook events can be retried for up to three days |

| 3. Money movement | Tie settlement rail confirmations to accounting entries, and in provider-led flows reconcile by settlement batch | Settlement confirmation plus transaction set tied to the corresponding general ledger posting |

| 4. Finance outputs | Reconcile general ledger to ERP only after operational states and money movement are validated | Closed-period GL and ERP balances in agreement, with any variance linked to an approved, documented adjustment |

- Reconcile instruction integrity first.

Compare the frozen payout batch at cutoff against payout API acknowledgments before checking bank deposits, general ledger, or ERP totals. Confirm at record level that each payout ID was acknowledged with the expected amount, currency, and provider reference where available. Verification artifact: instruction match report showing approved batch count, acknowledged count, matched amount total, and explicit rejects or missing acknowledgments.

- Reconcile status progression next.

Match webhook lifecycle events to provider dashboard data or the latest provider resource state. This matters because payment updates are asynchronous, and event payloads can be stale by processing time. Quarantine records with status contradictions or regressions. Keep reconciliation duplicate-safe, since undelivered webhook events can be retried for up to three days, and replays should not reopen or double-advance resolved payouts.

- Reconcile money movement third.

After instruction and status checks pass, tie settlement rail confirmations to accounting entries. In provider-led flows, reconcile by settlement batch: the transaction group that ties to what reached the bank. Verification artifact: settlement confirmation plus transaction set tied to the corresponding general ledger posting, with only approved adjustments posted after the tie-out.

- Reconcile finance outputs last.

Reconcile general ledger to ERP only after operational states and money movement are validated. In ERP-led flows, this follows subledger accounting and GL posting, and the subledger-to-GL check should be completed before period close. Verification artifact: closed-period GL and ERP balances in agreement, with any variance linked to an approved, documented adjustment.

If source systems disagree on terminal status, hold the reporting export and route the item to the exception queue instead of forcing manual overrides.

Build explicit decision rules for exceptions, holds, and escalations#

Treat exception handling as a rules engine, not a cleanup task, so each break gets the right owner and action path immediately.

- Classify first, then act.

Put every case into one mismatch family before anyone retries or closes it: amount mismatch, duplicate execution risk, missing settlement, stale FX quote, compliance hold, or tax-document eligibility blocker. Require a minimum case file for every family (internal payout ID, provider reference, amount/currency, latest status timestamp, and the artifact that supports the classification). Do not park unresolved items in a generic "timing" bucket.

- Use idempotency lineage as the duplicate-risk gate.

If duplicate risk is detected, do not cancel or retry until you trace the original request, its idempotency key, the provider response, and any later retries. The decision rule is simple: if lineage is clean, execute the documented recovery step; if lineage is unclear or conflicting, quarantine and escalate.

- Route compliance and tax blockers outside payment-ops closure.

KYC/KYB/AML holds are compliance exceptions and should be handled in that lane, including beneficial-owner checks for legal-entity onboarding where applicable. Treat missing W-8BEN/W-9 and Form 1099-NEC mapping gaps as tax-eligibility exceptions, not reconciliation noise. Keep FBAR/FEIE dependencies in tax/compliance workflows where enabled; they are conditional, not universal, and FBAR depends on facts such as the $10,000 aggregate foreign-account trigger.

- Define SLA, aging, and escalation in writing.

Set your own exception SLA and aging buckets against your close calendar, with owner and next-action date required at intake. There is no universal payout-platform SLA to copy. If a high-value item passes deadline, escalate to finance leadership even when the root cause sits in ops, tax, or compliance.

Keep one live exception register with family, owner, age, value, next action, and status so overdue high-value items are visible in one view. Related: Payment Transparency for Contractors: How to Build a Payout Tracker Your Recipients Trust. If you're building this process now, browse Gruv tools.

Decide what to automate now versus later#

Automate what is deterministic first, and keep interpretation-heavy exceptions in human review until your outcomes are consistent and well evidenced.

Step 1. Automate deterministic matches first. Start with matches you can prove from source records: internal payout ID to provider ID, amount and currency checks, and status alignment between webhook events and provider files. Matching rules are built for this kind of work, with exact-match and tolerance-based conditions that reduce manual intervention.

Set a hard checkpoint: every auto-cleared item must have an exportable trail of matched attributes, the rule that fired, and the source artifacts used. If you cannot explain why an item matched, automation is creating a black box instead of reducing close risk.

Step 2. Keep judgment-heavy exceptions manual at the start. Cases like ambiguous returns, multi-cause failures, or escalations involving AML or KYC are usually safer in manual review first. These often depend on context outside payment-event data, so early automation can misclassify the true cause.

Treat this as a sequencing decision, not a permanent rule: automate these paths only after your team shows stable disposition logic and evidence standards for edge cases.

Step 3. Compare tools on operating detail, not product claims. Choose tooling based on how it supports close operations, especially ERP sync, audit evidence, and replay safety.

| Criterion | What to verify | Why it matters |

|---|---|---|

| ERP integration depth | Whether data syncs automatically into your ERP or accounting layer, and which objects sync | Reduces rekeying and posting drift |

| Audit export quality | Whether approval history, source references, and audit trails are preserved and exportable | Supports defensible close decisions |

| Replay safety | Whether retries reuse the same idempotency key and request history is exportable | Reduces duplicate effects on retries |

For replay controls, validate operating specifics. Stripe documents safe retries with the same idempotency key within a 24-hour window, so confirm any vendor's retry window and whether first-request results are preserved for review.

Step 4. Use market examples as patterns, then decide from your own process. Use Tipalti and Lightspark as pattern references, not defaults. Tipalti examples can inform ERP-sync and audit-trail expectations, and Lightspark's framing reinforces idempotency keys as client-generated unique request identifiers.

Then apply your own decision rule: if exception volume is low, aging is controlled, and reviewer outcomes are consistent, tighten process discipline before expanding automation scope. Add broader automation when repetitive, evidence-based work is clearly crowding out human exception handling.

For a step-by-step walkthrough, see How Independent Contractors Should Use Deel for International Payments, Records, and Compliance.

Common failure modes and how to recover without losing audit trust#

When recovery starts from reports instead of source events, audit trust drops even if totals look right. Rebuild traceability first, then refresh reporting outputs.

| Failure mode | Recovery action | Evidence to keep |

|---|---|---|

| Reporting reconciled before the event trail settled | Rerun from source payment records and provider evidence before updating downstream reports | Internal payout record, provider transfer identifier, and event timestamps that explain the final status |

| Retries during latency or endpoint issues | Treat retries as duplicate-risk by default and use recovery checks that show which events were already processed | Recovery checks; if needed, list undelivered events from the last 30 days; branch handling if a payout.failed event appears |

| Compliance-related holds in a generic exception bucket | Track them as compliance dispositions with their own evidence | Requirement status and the operational outcome for each affected payout |

Reconcile from source events before reporting outputs#

If reporting was reconciled before the event trail settled, rerun from source payment records and provider evidence before updating downstream reports. Payout outcomes are asynchronous, and undelivered webhook events can be retried automatically for up to three days, so reporting can get ahead of the real lifecycle. For each corrected item, keep a clear chain: internal payout record, provider transfer identifier, and event timestamps that explain the final status.

Treat retries as duplicate-risk until processing state is proven#

Retries during latency or endpoint issues should be handled as duplicate-risk events by default. Use recovery checks that show which events were already processed, so replay does not apply the same event multiple times. If you need to recover missed delivery, Stripe supports listing undelivered events from the last 30 days; if a payout.failed event appears, branch handling because the failed payout can also disable the external account involved.

Keep compliance holds separate from ordinary payout exceptions#

Do not close compliance-related holds inside a generic exception bucket. Track them as compliance dispositions with their own evidence, because outstanding requirements can restrict payout capabilities until resolved. Your close evidence should clearly show the requirement status and the operational outcome for each affected payout.

Conclusion and copy-paste monthly checklist#

Do not lock close just because the batch total looks right. A reliable month-end for contractor payouts depends on sequence, cutoff discipline, and retained evidence that shows reported amounts are accurate, supported, and complete.

- Confirm prerequisites before you match anything.

Verify eligibility, compliance, and tax documentation inputs are complete where applicable, along with frozen data cutoffs and named owners for review and sign-off. Your checkpoint is simple: the period's payout population is final, the source extracts are timestamped, and each exception queue has an assigned reconciliation owner. If you skip this, ineligible or held payouts can get mixed into normal payment breaks and distort the month.

- Reconcile in a sequence that keeps downstream reports clean.

Start by tying payout batches to the payout date and the transactions included in each batch. Then check how amounts populate as they become available throughout processing, rather than assuming everything is final at once. This order matters because payment processing can be a three-step process over multiple days.

- Review variances explicitly, not by feel.

Use a payout reconciliation report or equivalent extract tied to the payout date and the transactions included in that batch. Compare payout amounts, payment totals, and variances item by item before accepting summary totals. One easy miss is assuming a single payout maps to one business date. In practice, a payout can include transactions from multiple business dates, so date-only matching can create false breaks or hide real ones.

- Resolve or formally disposition exceptions on a documented timeline.

For each unmatched or disputed item, record the root cause, current owner, next action, and whether an adjustment is recommended. Escalate aged, high-risk items based on your internal policy. The failure mode to avoid is silent carry-forward: an old break stays open, nobody owns it, and it reappears after reporting has moved on.

- Lock close only after the evidence pack is complete, then note what to improve next cycle.

Before sign-off, confirm the audit file contains the key mappings for each payout, the decision log for exceptions, and the approval record for close. That documentation is your evidential matter if someone later asks how management concluded the numbers were supported. After lock, capture the top exception causes, the deterministic checks you can automate next, and the controls to tighten. At scale, that review is what keeps next month from turning into manual archaeology.

Related reading: A Guide to Using Wise for Payroll for International Contractors.

Frequently Asked Questions

What should be reconciled every month for a 1,000-contractor payout operation?

Reconcile the full chain, not just the money total: instruction creation, processing, and final booking, with item-level links across your internal records and provider records, including webhook status history. If you can submit up to 1,000 payouts in one batch, keep item-level visibility anyway, because month-end breaks usually hide inside a small number of records, not in the batch total. Your verification point is a complete key chain for each item: internal payout ID, provider reference, and (for retries) the idempotency key.

Which mismatch types should be triaged first to protect month-end close timelines?

Start with anything that can create a false financial position or a duplicate payment risk: duplicate events, missing final booking, and terminal-status disagreements between provider records and your ledger. A status mismatch matters more than it looks because processing and booking can be independent events, and "Processed" and "Booked" may occur in any order. Leave cosmetic reporting mismatches until after you confirm whether money actually moved.

What KPIs prove a monthly payment reconciliation process is healthy?

Do not look for a universal benchmark, because none is reliable across payout stacks. Track whether your matched count and matched value improve, whether exception aging stays within your own close calendar, whether close needs to be reopened, and how many records reach sign-off with full evidence attached. A strong practical KPI is coverage: what share of payouts can be traced from instruction creation through final booking without manual reconstruction.

When should a payout be held instead of retried?

Hold when the blocker is eligibility or uncertainty, not transport failure. That can include unresolved identity/compliance checks, missing tax documents such as Form W-9 or Form W-8 BEN, stale FX quote conditions, or any case where source systems disagree on final status. Retry only after you confirm the prior attempt through the idempotency key, because the same key should return the original result rather than create a new outcome.

How do FX quote timing and asynchronous webhook events affect reconciliation accuracy?

FX adds a timing dependency that many teams miss. If you use an extended quote with a 5 minute, 1 hour, or 24 hour validity window, record which quote applied and whether the payout was submitted before expiry. Otherwise, your amount and rate checks can drift. Webhook events add a second timing issue because they are asynchronous and should not be your sole reconciliation method.

What should be automated first in a contractor payment API stack?

Automate deterministic checks first: ID joins, amount and currency matching, event ingestion, duplicate detection, and status progression checks from provider records plus webhook events. Keep ambiguous returns, compliance escalations, and manual dispositions in human review until the data quality is stable. If automation cannot show the evidence behind a match, it is not ready for close.

How do you keep reconciliation audit-ready when compliance checks like KYC and AML are in the flow?

Separate compliance-held payouts from normal payment exceptions so they do not disappear into a generic break queue. Keep the requirement snapshot, reviewer name, decision date, related payout IDs, and whether the item was held, failed, or later reissued. Where your recordkeeping obligations apply, design retention to support five years of evidence rather than rebuilding the trail after an audit request.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

Invisible Payouts: How to Remove Payment Friction for Contractors Without Sacrificing Compliance

Invisible payouts should make life easier for contractors without hiding the controls your team needs. Contractors should get a predictable, low-friction flow, while internal teams can still enforce and document payout decisions when needed. If you run contractor payouts at scale, you need both outcomes at once. We recommend treating every easy payout as a controlled release path your team can replay later.

Building a Contractor Payout Tracker Recipients Trust

A payout tracker can help build trust when recipients can see what is happening, what happens next, and whether they need to act, without opening a support ticket. When payout status is vague, routine questions can turn into tickets, calls, and escalations. When status is clear, timestamped, and action-oriented, recipients can self-serve and support teams may spend less time chasing updates.

Scaling a Global Payout Platform from 100 to 10000 Monthly Payments

Scaling a global payout platform is rarely just a vendor problem. More often, it is an infrastructure and operating-discipline problem, because cross-border payments still carry persistent issues around cost, speed, access, and transparency. If growth is framed as "one more provider" or "higher API throughput," breakpoints can show up in finance, support, compliance, and reconciliation.