Quick Answer

Start by treating INFORM compliance as an execution problem, not a notice problem: determine scope, run seller verification, publish accurate seller disclosure, and maintain a clear suspicious-activity path. The article ties this to 15 U.S.C. §45f and FTC enforcement context, including June 27, 2023 effectiveness and stated civil-penalty risk, while warning that unresolved threshold and carve-out details should be flagged as legal checkpoints instead of coded assumptions.

What the INFORM Consumers Act requires#

If you own marketplace compliance or product operations in the United States, start narrower than many teams do. The INFORM Consumers Act creates real seller controls for covered marketplaces. The practical job is to build to the legal floor the statute sets, document what the public excerpts do not resolve, and avoid turning open questions into hard-coded product requirements.

At a high level, the law requires online marketplaces to obtain information from certain high-volume third-party sellers, and to collect, verify, and disclose certain information about those sellers. It also requires marketplaces to offer a clear way for people to report suspicious activity. The policy aim is not transparency for its own sake. It is to make online transactions more transparent and deter the online sale of stolen, counterfeit, or unsafe merchandise.

That matters because the work does not sit with one team. Compliance needs a defensible reading of what is required. Risk needs escalation rules for bad or changing seller data. Product has to decide where disclosures appear and how they stay current. Finance and payments may need to tie verification outcomes to payout permissions or other account controls. If you treat this as only a legal notice issue, you will miss the operational dependencies that create real exposure.

The exposure is not theoretical. FTC guidance notes that the statute became effective on June 27, 2023, and that the Federal Trade Commission and the states have authority to enforce it. The same FTC page notes civil penalties of $53,088 per violation for online marketplace violations. That is why the sensible approach is to be exact about scope and evidence, not broad and improvisational.

This article focuses on that execution layer. You should leave with a concrete set of decision checkpoints for:

- when a seller or transaction is actually in scope for these duties

- what to collect and how to structure seller verification

- where seller disclosure belongs in the product experience

- how to route suspicious activity reports and document outcomes

- what evidence to retain so you can explain a decision later

One caution up front: the public excerpts do not resolve every detail you may need. They support the core duties to collect, verify, disclose, and support suspicious activity reporting. They do not settle every threshold, exception, or edge case. For the inform consumers act us online marketplaces seller verification problem, the safest move is to separate confirmed obligations from legal interpretation points, then build controls you can tighten later without rewriting your onboarding and review process.

Start with the legal floor and the known unknowns#

Start from the legal floor, then separate what is confirmed from what still needs statute-level review. Here, that means anchoring implementation to 15 U.S.C. §45f (Title 15) and using FTC guidance for the core duties it clearly describes.

| Implementation point | Status | Handling |

|---|---|---|

| Obtain information from certain high-volume third-party sellers | Confirmed duty | Operationalize |

| Collect, verify, and disclose certain seller information | Confirmed duty | Operationalize |

| Offer a clear way for people to report suspicious activity | Confirmed duty | Operationalize |

| Keep controls aligned with more transparent transactions and deterrence of stolen, counterfeit, or unsafe merchandise sales | Confirmed duty | Operationalize |

| The exact high-volume third-party seller thresholds | Open question | Escalate before hard-coding |

| The full set of disclosure exceptions or carve-outs | Open question | Escalate before hard-coding |

Confirmed duties to operationalize:

- Obtain information from certain high-volume third-party sellers.

- Collect, verify, and disclose certain seller information.

- Offer a clear way for people to report suspicious activity.

- Keep controls aligned with the stated policy aim: more transparent transactions and deterrence of stolen, counterfeit, or unsafe merchandise sales.

Known unknowns to escalate before hard-coding:

- The exact high-volume third-party seller thresholds.

- The full set of disclosure exceptions or carve-outs.

Use a simple implementation checkpoint: for each control, record source, exact text relied on, and open question status. If the requirement cannot be tied to FTC guidance or the statutory text, treat it as interpretation, not a confirmed duty.

Do not assume#

- Do not assume FTC guidance resolves every threshold or carve-out.

- Do not assume secondary summaries can replace the statutory text.

- Do not assume FederalRegister.gov prototype pages are official legal notice; the site states they are not the official legal edition and do not provide legal notice to the public or judicial notice to the courts.

The common failure mode is overbuilding: turning unresolved points into hard product rules creates seller friction and escalation debt without clear legal grounding. If you want a related workflow piece, see The Best Accounting Software for a Freelance Bookkeeper.

Decide if a seller and a transaction are in scope before you verify anything#

Scope first, verification second. If you treat every seller and listing as covered, you create unnecessary holds and friction, especially where thresholds or exceptions are still interpretation-dependent.

Translate key terms into internal eligibility tests so Product, Risk, and Legal classify the same case the same way.

| Term | Working internal test | What to record |

|---|---|---|

| online marketplace | Is this a consumer-directed platform that facilitates or enables third-party seller activity involving a consumer product? | Product surface, transaction model, and whether the platform enables sale, payment, storage, shipping, or delivery |

| third-party seller | Is the seller distinct from your first-party business, with the platform facilitating that seller's activity? | Seller entity ID and whether inventory is marketplace-owned or seller-owned |

| high-volume third-party seller | Does the seller appear to exceed the applicable transaction and revenue threshold over a 12 month period? | Rolling metrics snapshot, calculation date, source text relied on |

| consumer product | Is the item offered as a new or unused consumer product, rather than assuming every listing is covered? | Listing category, condition field, and any manual override note |

Use a strict gate order#

- Confirm marketplace scope.

- Confirm the seller is third-party, not first-party.

- Confirm the item is a covered product type.

- Then decide whether verification and disclosure duties attach.

One secondary legal summary describes a high-volume third-party seller as more than 200 transactions and $5,000 in revenues in a 12 month period, and ties action timing to within ten days of qualifying. Use that as a monitoring trigger until counsel confirms your final statutory interpretation.

Use a seller-level scope memo with five fields: scope result, exact text relied on, metrics snapshot date, decision owner, and next review date.

Create an edge-case queue instead of improvising#

For sellers near threshold boundaries, mixed catalogs, or unclear product categories, route to a dedicated "pending legal interpretation" queue with one Legal owner and one risk owner. Make one documented decision you can reuse.

If scope is uncertain, pause expanded INFORM controls rather than blocking the seller's entire activity by default. For a step-by-step walkthrough, see Defend Trade Secrets Act (DTSA) for Freelancers and Consultants.

Build the seller verification control sequence teams can actually run#

Treat verification as a permission gate, not a document chase: once a seller is in scope, decide what you collect, who verifies it, who can approve exceptions, and who can release payouts.

The FTC's September 5, 2025 enforcement post describes INFORM duties as requiring marketplaces to "collect, verify, and disclose certain information" and provide shoppers with "required information and tools." That means intake alone is not enough; each case needs a clear verified or restricted outcome with named owners.

Start with a tight intake packet#

The FTC excerpt does not enumerate exact field requirements or timing, so keep your legal standard in your own approved policy. Operationally, many teams use a minimum intake set: tax identification number, government-issued identification, bank account information, and core contact or business identity fields.

Build one canonical seller profile before review starts. Verification should not move to complete unless the profile snapshot, submitted records, and reviewer notes all match the same seller identity version.

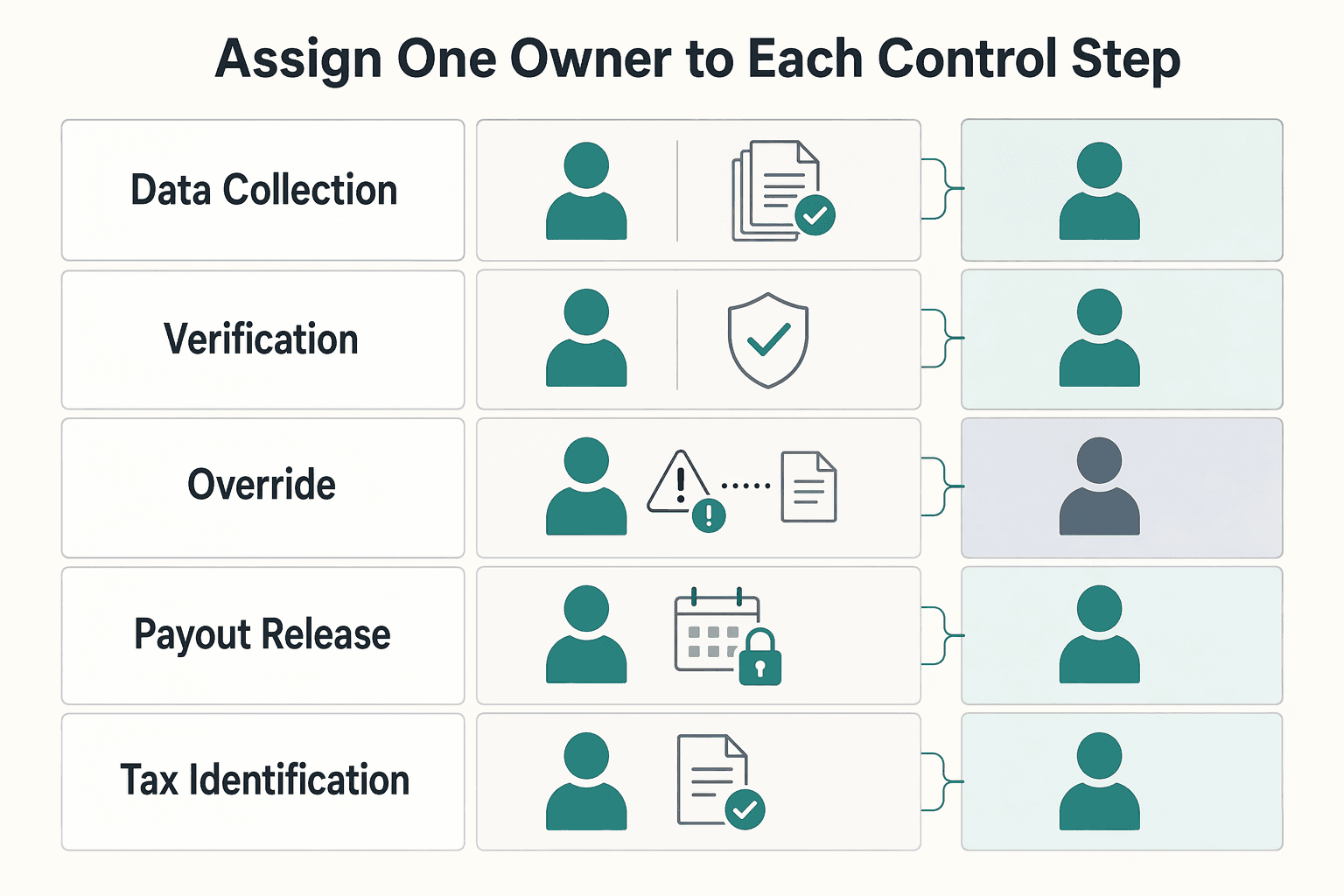

Assign one owner to each control step#

| Control step | Owner | Responsibility |

|---|---|---|

| Data collection | Data collection owner | Collects the intake packet and blocks incomplete submissions |

| Verification | Verification owner | Runs verification checks and records pass, fail, or manual review |

| Override | Override owner | Approves documented exceptions |

| Payout release | Payout release owner | Enables payouts only after approved verification status |

Keep override and payout-release authority separate so one person cannot both waive issues and release funds.

| data element | verification method | evidence artifact | recheck trigger | escalation owner |

|---|---|---|---|---|

| tax identification number | match against the approved seller identity process | match result, timestamp, reviewer note, approved profile snapshot | legal-name or tax-ID change, identity-related payout hold | Compliance or Tax Operations |

| government-issued identification | validate identity document and profile match | document review result, reviewer decision, mismatch notes | expired or unreadable document, resubmission, identity mismatch | Compliance or Risk |

| bank account information | confirm payout account linkage under payments controls | bank verification result, masked account record, approval date | payout-method change, failed payout, fraud signal | Payments Risk or Finance |

| core contact and business identity fields | compare profile fields against approved records | approved profile version, change log, review notes | material profile edit, dormant-account reactivation, complaint trend | Onboarding Ops, then Compliance |

Define failure handling before cases arrive#

A document mismatch should pause verification completion and payout release until corrected or resolved through review. An unverifiable identity should stay in restricted status and move to escalated review.

Stale records and repeated identity or payout-data changes should trigger enhanced review and named risk sign-off before permissions are restored.

You might also find this useful: IRS Form 8233: When Foreign Contractors Claim Treaty Exemptions and What Platforms Must Verify.

Design seller disclosure and suspicious-activity intake without exposing excess data#

Use one controlled disclosure record and one clear reporting path. FTC consumer guidance says online marketplaces must disclose contact information for many third-party sellers of new or unused products, and that shoppers should get seller information plus a way to report questionable activity.

Use one approved disclosure record across the buyer journey#

The FTC excerpt does not prescribe exact placement, so treat listing, checkout, and post-purchase views as operational choices, not mandated surfaces. The key control is consistency: wherever seller details appear, pull them from the same latest approved seller profile version.

If teams can hand-edit seller details in separate tools, conflicting disclosures are likely. Keep one source of truth, and block publishing when public-facing fields do not match the current approved profile.

Make suspicious-activity reporting visible and routable#

When you show seller information, show a clearly labeled way to report questionable activity. A generic support path can bury risk signals in routine service tickets.

| Report field | Qualifier | Purpose |

|---|---|---|

| seller or listing reference | Structured intake example | Triage and disposition reports |

| order reference | If available | Triage and disposition reports |

| issue type | Structured intake example | Triage and disposition reports |

| shopper narrative | Structured intake example | Triage and disposition reports |

| optional proof | Such as screenshots or messages | Triage and disposition reports |

Keep intake structured enough to triage and disposition reports, for example:

- seller or listing reference

- order reference (if available)

- issue type

- shopper narrative

- optional proof (such as screenshots or messages)

Route these reports to a team that can investigate seller risk patterns, not only close customer service requests.

Minimize what you expose and what you log#

Separate disclosure data from verification evidence. Show only the seller information you decide is required to disclose, and keep sensitive verification artifacts out of buyer-facing views and broad internal logs.

Before publishing any disclosure change, run a match check against the latest approved seller profile. That checkpoint helps prevent stale or conflicting disclosures while limiting unnecessary data spread.

Set hard decision rules for failed verification and enforcement actions#

Use two explicit paths: apply a hard stop when seller identity cannot be verified or risk signals are credible, and use manual review for limited administrative mismatches. FTC guidance sets the floor for covered marketplaces to collect, verify, and clearly disclose certain seller information, and to provide a clear way to report suspicious activity. Your policy should then state, in plain terms, what happens when verification fails or reports suggest counterfeit or stolen goods.

Separate hard stops from review cases#

Not every mismatch should trigger the same consequence, but every team should apply the same rule set.

- Critical verification failure: you cannot verify seller identity, the seller profile conflicts with the approved disclosure record, or a suspicious activity report indicates immediate buyer risk.

Action: restrict normal seller activity pending review.

- Non-material inconsistency: the issue appears administrative and does not undermine who the seller is.

Action: route to manual review with a named owner and a target decision date, then require documented clearance or escalation.

Traceability is the core control. Each case should record the seller profile version, the failed or disputed control, affected listings or orders, and the trigger evidence.

Use an internal action ladder, and label it as policy#

The FTC excerpt does not prescribe a mandatory enforcement ladder. You should still define one so outcomes are consistent and reviewable.

- Temporary hold while identity or report facts are checked.

- Listing suppression when risk is tied to specific products or disclosures.

- Payout restriction when releasing funds would outpace review.

- Reinstatement only after conflicting or missing facts are resolved and logged.

- Final account action when critical failures remain unresolved or serious misconduct is credibly supported.

For higher-impact cases, especially suspected counterfeit or stolen goods, require cross-functional approval. Risk assesses immediate harm, Compliance checks policy alignment, and Legal reviews cases with higher exposure or sensitive termination rationale.

| Severity level | Typical trigger | Customer impact | Legal exposure | Recommended approver |

|---|---|---|---|---|

| Low | Minor inconsistency that does not change seller identity | Limited confusion | Low | Operations or Risk reviewer |

| Medium | Unresolved mismatch affecting verified seller information or public disclosure | Buyers may see inaccurate seller details | Medium | Risk lead plus Compliance |

| High | Credible suspicious activity report with supporting signals tied to listings | Possible consumer harm | High | Compliance plus Risk manager |

| Critical | Strong indicators of counterfeit/stolen goods, or unverified seller identity with ongoing sales | Immediate buyer and platform risk | Highest | Risk, Compliance, and Legal |

Set one non-negotiable: no reinstatement after a critical failure without a documented rationale and evidence pack.

Keep an audit-ready evidence pack from intake to escalation#

Build the evidence pack into the workflow from intake through escalation, and treat it as internal policy rather than an INFORM-specific rule from the sources provided. The IRS excerpts on Form 1116, Form 1118, and Topic 856 do not set marketplace seller-verification evidence standards or FTC retention timelines.

Keep one traceable case record for each outcome tied to seller verification, seller disclosure, and suspicious activity reporting. At minimum, include timestamp, reviewer identity, artifact reviewed, result, and any escalation or override so another reviewer can reconstruct what happened.

Restrict sensitive artifacts early#

For tax identification number and government-issued identification records, limit raw-document access and keep broader access to case status and rationale. A practical pattern is to store sensitive files in a restricted repository and reference them in the case log by stable document ID instead of duplicating full records across tickets.

Set retrieval and attestation rules you can sustain#

Set those standards explicitly with Legal, Risk, and Finance. Keep a short monthly attestation that covers:

- sampled cases reviewed against policy

- exception trends (for example, missing artifacts or late escalations)

- unresolved escalations and aging

- remediation owners and target completion dates

Do not close a case until the record is complete enough for a different reviewer to understand and defend the outcome without asking the original analyst.

Handle US law in a multi-market stack without mixing tax and marketplace duties#

Keep US marketplace seller controls separate from tax reporting workflows. The INFORM Consumers Act is a different compliance lane from FATCA, Form 8938, and FBAR, so avoid collapsing everything into one generic "US compliance" intake.

Form 8938 is used to report specified foreign financial assets and is attached to the taxpayer's annual tax return. IRS guidance also directs filers to determine whether Form 8938, FBAR, or both apply, and to review Form 8938 instructions for exceptions. Those tax-reporting rules are not a default basis for marketplace seller-verification data collection.

| Obligation family | What it is tied to | Practical handling rule |

|---|---|---|

| US marketplace seller controls | Marketplace compliance duties | Keep in the seller compliance flow |

| Form 8938 / FATCA | Foreign financial asset reporting with an annual tax return | Keep in tax workflow, not seller verification |

| FBAR / FinCEN Form 114 | Separate foreign account reporting | Route through tax or finance review, not marketplace intake |

If one onboarding flow serves multiple jurisdictions, maintain a required-field map with a "legal basis" column for every question. Each field should tie to one obligation, one trigger, and one evidence artifact. If you cannot tie a field to a specific duty, remove it from the default path.

A common failure mode is collecting extra foreign-asset or account data "just in case," then being unable to explain why it was requested. That adds user friction, expands sensitive-data exposure, and makes evidence harder to defend. A simple jurisdiction matrix that separates "US marketplace seller controls" from "cross-border tax document workflows" helps prevent that drift.

Related reading: How to Use QuickBooks Online to Manage Multiple Currencies as a Freelancer.

Conclusion#

The right end state is narrower than many teams expect. Under FTC guidance on the INFORM Consumers Act, your job is not to collect every possible seller document or turn onboarding into a general fraud dragnet. It is to identify where the law applies, collect, verify, and disclose the required seller information for the covered seller group, and give people a clear way to report suspicious activity.

That discipline matters because overbuilding creates its own risk. If you treat every seller, product, or market the same, you add review burden and delay legitimate sellers. You still may miss the real legal question: is this an online marketplace case involving the covered seller and product category the FTC guidance points to? A simple checkpoint helps. Every approval, hold, or disclosure decision should be traceable to a recorded scope call, not just a generic risk score or a tax intake branch.

The practical win is disciplined documentation. You want written decision rules for when a seller is in scope, what evidence is acceptable for verification, who can clear an exception, and when suspicious activity reports move from intake to investigation. Even if your tools are basic, keep a clean evidence trail with the reason code, reviewer, and timestamp for each material decision. That is what reduces surprises when Legal, Risk, or a regulator asks why a seller was approved, restricted, or disclosed in a certain way.

A useful red flag is product logic that embeds assumptions the source materials do not actually settle. The excerpts here do not give you the exact threshold mechanics for a high-volume third-party seller, the full list of seller data elements, or detailed timing rules for disclosures. If one of those points is still unresolved, do not bury your guess in code or operations policy. Mark it as a legal checkpoint, route edge cases to a named owner, and document that the issue is pending interpretation.

That approach also keeps the law tied to its actual purpose. FTC guidance frames the Act as a transparency and deterrence measure aimed at stolen, counterfeit, or unsafe merchandise. Those points support focused controls, not unlimited data collection. If a control does not improve seller transparency, verification quality, disclosure accuracy, or suspicious activity intake, question why it is in the flow.

So the practical recommendation is straightforward: keep your controls anchored to the Act and FTC guidance, keep ownership explicit, and keep uncertain statutory details out of default product behavior until they are legally resolved. That is the best way to stay credible, reduce operational drag, and make the compliance program something your team can actually run.

Frequently Asked Questions

What does the INFORM Consumers Act require online marketplaces to do first?

These IRS materials do not state what the INFORM Consumers Act requires online marketplaces to do first. They do show that FATCA, FBAR, and Form 8938 are tax-reporting topics, so those requirements should be kept separate from marketplace-law compliance design.

Who qualifies as a high-volume third-party seller for compliance purposes?

These sources do not define “high-volume third-party seller,” and you should not borrow a tax threshold to fill the gap. In particular, the IRS says Form 8938 becomes reportable at $50,000 “in general,” with higher thresholds in some cases, but that number relates to specified foreign financial assets, not marketplace seller volume. Treat any attempt to reuse that threshold as a red flag.

What seller information must be collected, verified, and disclosed?

The IRS excerpts here only tell you about tax reporting for foreign financial assets. They say, “Use Form 8938 to report your specified foreign financial assets,” and that the form is attached to the taxpayer’s annual tax return. They do not tell you what seller identity, banking, or disclosure fields a marketplace must collect under marketplace law, so do not use Form 8938 as your intake checklist.

What should a marketplace do when seller verification fails or is inconclusive?

Do not try to patch a failed seller check by asking for FATCA, FBAR, or Form 8938 materials unless you have a separate tax reason to request them. Those filings do not substitute for marketplace verification. These sources do not provide a marketplace seller-verification failure workflow, so hold/restriction/manual-review rules should come from your marketplace legal and compliance process.

How should suspicious activity reporting be exposed to consumers and triaged internally?

Keep consumer reporting separate from tax reporting. FBAR is FinCEN Form 114, a foreign bank account filing, and these IRS materials do not describe a marketplace consumer complaint channel. Internal triage for suspicious marketplace activity should be defined in your marketplace compliance process, with tax teams involved when there is an actual tax issue.

What details are still unclear without a full statutory and legal review?

Several core marketplace points remain unresolved by these IRS sources: the exact high-volume threshold, the exact seller data elements, disclosure exceptions, and what timing or retry rules apply when verification is incomplete. That uncertainty matters because teams often hard-code assumptions too early. If the answer is not in the statute or your legal memo, mark it as pending interpretation rather than treating it as settled.

How is INFORM compliance different from FATCA, FBAR, FinCEN, or Form 8938 obligations?

FATCA and Form 8938 are about certain U.S. taxpayers reporting specified foreign financial assets to the IRS, generally on Form 8938 attached to the annual tax return. The IRS also says some taxpayers may need to file both Form 8938 and FBAR. Form 8938 can carry penalties of $10,000, with continued-failure penalties up to $50,000 and a 40 percent substantial understatement penalty in some cases. None of that establishes marketplace seller-verification compliance, so you should map those duties to tax workflows, not to your marketplace onboarding logic.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- congress.gov/crs-product/R46751trusted

- consumer.ftc.gov/consumer-alerts/2023/06/inform-consumers-act...trusted

- cppa.ca.gov/regulations/pdf/data_broker_reg_comments.pdftrusted

- federalregister.gov/documents/2023/11/09/2023-24234/trade-regula...trusted

- federalregister.gov/documents/2024/11/15/2024-25534/negative-opt...trusted

- ftc.gov/business-guidance/resources/what-third-party...trusted

- ftc.gov/business-guidance/blog/2025/09/first-inform-...trusted

- govinfo.gov/content/pkg/CHRG-115shrg35965/html/CHRG-115s...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Supply Chain Finance for Marketplaces: How Early Payment Programs Can Attract and Retain Sellers

Treat an Early Payment Program as both a funding decision and a payout-control decision. In a marketplace, it can shape seller experience, payout reliability, exception volume, and who carries cash and credit exposure when payment happens before standard terms.

The Best Accounting Software Stack for Bookkeepers Serving Global Clients

---

IRS Form 8233: When Foreign Contractors Claim Treaty Exemptions and What Platforms Must Verify

Form 8233 is used by nonresident alien individuals to claim exemption from withholding on compensation for personal services, but for platform operators the key exposure is often operational: scope decisions, review quality, recordkeeping, and escalation. When you pay nonresident individuals for U.S.-source personal services income, the real risk is often not whether a form exists, but whether your team can show why a claim was accepted.