Quick Answer

Start by classifying the event before rerouting: gateway failure, acquiring degradation, ransomware, or confirmed breach. For incident response payment platforms outages, run the first hour in a fixed sequence, freeze risky manual overrides, and permit retries only where idempotency is proven end to end. Widen continuity changes only after provider references map cleanly to one internal transaction and ledger posting. Then close in phases by resolving unknown outcomes, validating settlement against bank activity, and assigning owners for unresolved exceptions.

How to Run the First Hour of an Incident#

One of the fastest ways to turn a processor outage or breach into a longer finance problem is to restore traffic before you can prove what happened in your internal record.

This guide takes a record-first approach: make continuity decisions that protect posting integrity, settlement verification, and customer fund accuracy, so you do not trade short-term uptime for long-term cleanup work.

Start from the ledger. In payments, continuity decisions only hold up if you can verify them later. A processor timeout, gateway error, stalled ACH file, or suspected cyberattack can push teams toward manual retries and quick routing changes. Those moves are safest when your internal book remains the source of truth for authorizations, captures, payouts, reversals, and balances.

Use this checkpoint before you approve retries, replays, or failover routing: confirm that each provider event still maps to a unique internal transaction or journal entry. If it does not, you are in higher-risk territory for duplicate debits, duplicate payouts, or orphaned references.

NIST SP 800-61 Rev. 3 (April 2025) frames incident response as part of broader cybersecurity risk management, not a standalone exercise. That fits payment operations, where incident decisions directly affect customer funds, finance close, partner reporting, and the quality of your post-incident evidence.

Put the right owners in the room. This guide is for the people who have to decide, under pressure, whether to pause, retry, reroute, or communicate. That includes finance leads, operations owners, and product owners responsible for payouts, settlement verification, reporting, and incident decisions.

Breach response is cross-functional by design. The FTC describes breach response teams as including legal, security, IT, communications, management, and operations. Payment operations often sits in the middle of that group. Even when you are not leading forensics, you may still be deciding whether funds keep moving, whether reporting stays trustworthy, and whether customer messaging matches what your internal record can support.

Set scope before you act. This is an operations guide, not a deep forensic manual. It focuses on payment decisions during outages, cyberattacks, and breach scenarios: classify the event, contain risk, keep critical flows running where justified, and close without unresolved settlement variance.

Legal and investigative paths vary by incident type, business structure, and jurisdiction. In the United States, breach notification obligations differ across states, the District of Columbia, Puerto Rico, and the Virgin Islands. Under GDPR Article 33, personal-data-breach notification is required without undue delay and, where feasible, within 72 hours of awareness.

For payment-card incidents, PCI guidance expects response plans to identify payment card brands, acquirers, and other parties that require notice by contract or law. Cardholder-data breach forensics may require a PCI SSC-approved Payment Card Industry Forensic Investigator.

Use this guide as a decision aid for payment operations, not a universal legal script. The next move is to classify the incident correctly before anyone touches routing, retries, or customer balances.

Classify the incident before you touch routing#

Your first decision is incident type, not rerouting. Get that wrong, and you can make both containment and later verification harder than the original event.

Separate failure types#

Use a simple matrix before you retry, replay, or fail over. A payment gateway is the front-end checkout layer, while an acquirer processes card transactions for merchants, so treat them as different failure domains.

| Incident type | Likely signs | First containment goal | Verification checkpoint |

|---|---|---|---|

| Payment gateway failure | Checkout errors, degraded transaction processing, payment processing error messages | Prevent duplicate customer submissions and confirm internal transaction creation still matches attempts | Confirm failed attempts still map to unique internal transaction records and check provider status for front-end processing issues |

| Acquiring connection degradation | Card-processing failures after checkout submission while the app remains up | Isolate card-rail impact before changing broader routing | Compare gateway request receipt with acquirer processing acknowledgments |

| Ransomware | Access disruption or other signs impacted systems | Immediately isolate impacted systems, then triage for restoration and recovery | Confirm which systems are impacted and isolated before wider recovery actions |

| Confirmed data breach | Unauthorized access, disclosure, loss, or alteration of personal data | Preserve evidence and restrict access, not just restore service | Validate affected data scope and isolate systems in an evidence-preserving way |

Your evidence pack should change with the failure type. For gateway or acquiring incidents, prioritize provider status updates, failed-payment states, event traces, and posting snapshots. For ransomware or breach incidents, prioritize access logs, host evidence, and isolation records.

Set severity by operational impact#

Set severity bands based on payment and posting impact, not on escalation volume. You do not need a formal 0 to 100 model, but you do need criteria your team will apply the same way every time.

In practice, avoid treating one pattern as a universal severity mapping across failed card payments, delayed ACH settlement, channel disruption, payout backlog, and transaction-state uncertainty. Delayed ACH settlement can increase settlement, credit, and liquidity risk. If transaction state cannot be proven, raise severity.

Default to stricter controls when triage is unclear#

If type is still unclear after initial triage, default to stricter controls that protect posting integrity and customer funds. Pause high-risk manual overrides, hold broad retry jobs, and delay failover routing until provider events can be mapped to internal transactions.

Ambiguity is not a green light. Treat unclear incidents as containment-first until the evidence is strong enough to narrow the path.

Use BridgePay as a concentration-risk warning#

BridgePay Network Solutions is a useful reminder that third-party incidents can stay opaque longer than operators want. Public history shows a major gateway outage labeled "Under Investigation" from Feb 6, 03:29 to Feb 25, 16:20 EST. BridgePay later confirmed ransomware while stating it could not yet provide a specific timeline.

The operational lesson is concentration risk, not assumed root cause. Third-party payment-processing relationships can increase operational risk, and DORA Article 29 highlights dependencies on providers that are not easily substitutable or are clustered in one connected provider group. Classify those dependencies early, because an apparent failover path may share the same underlying provider risk. Related: Airline Delay Compensation Payments: How Aviation Platforms Disburse Refunds at Scale.

Prepare the prerequisites before any incident occurs#

For payment platform outage response, the biggest time saver is deciding in advance who can act, what they can access, and what evidence must be captured while the incident is unfolding.

Name the incident lead and backups. Set a clear command structure before you need it: an Incident Commander to make decisions, a backup to take over if needed, and a Scribe to maintain the live timeline. Keep role ownership explicit so responders are not guessing authority during active impact.

Do not stop at names. Document decision rights for your environment, including who can authorize key response actions and customer updates. If your on-call responder cannot quickly identify the active decision owner, you still have an ownership gap.

Pre-approve access and escalation paths. Do this before an outage starts. Your on-call team should be able to reach response tools, real-time alerts, and provider status pages without waiting on emergency permissions.

Keep the on-call schedule current and the escalation path explicit for cases where the primary responder does not acknowledge. Subscribe the response group, not just one person, to provider incident notifications. Status pages help, but they are not your only source of truth.

Keep an evidence pack template ready. Capture evidence during the incident, not after it. Keep a template ready with the log sources and webhook traces your team relies on. Include internal transaction and reconciliation artifacts where those exist in your stack.

Provider-side webhook logs can speed troubleshooting because they can include timestamps, endpoint URLs, reference IDs, and request and response details. If your team handles cardholder data, include this workflow in your documented incident response plan and test it at least annually.

Execute the first 60 minutes in fixed order#

The first hour is where teams either contain damage or create more of it. Run it in a consistent sequence: centralize command, validate blast radius, contain with retry-safe controls, communicate clearly, then verify posting integrity before you expand continuity measures. Treat these minute buckets as internal operating targets, not a universal standard. The value is consistency under pressure.

| Step | Action | Checkpoint |

|---|---|---|

| Acknowledge the incident and centralize control | Activate incident command structure immediately and use one real-time command channel | Pin incident name, severity, affected services, current owner, and next internal update time |

| Validate the blast radius before you call it a processor outage | Map impact across processor, gateway, acquiring connection, and payout rails separately | Start with internal alerts, provider status pages, webhook failures, API error trends, request IDs, and transaction logs |

| Contain carefully and route only what you can retry safely | Start failover with the smallest meaningful traffic slice and queue uncertain transactions | Retry only where idempotency behavior is confirmed end to end |

| Publish a tight status update without guessing root cause | Send updates on what is confirmed, affected, underway, unknown, and when the next checkpoint will be posted | Do not promise root cause in the first hour unless you have the evidence |

| Gate continuity changes on ledger integrity | Sample transactions from before and during the incident | Match provider references, internal payment IDs, amounts, currencies, and final states |

Acknowledge the incident and centralize control#

Activate your incident command structure immediately. Keep decision authority explicit with an Incident Commander, supporting command staff, and a timeline Scribe.

Use one real-time command channel for operational decisions and treat it as the team's working source of truth. Pin the incident name, severity, affected services, current owner, and next internal update time so responders can join without re-triaging context. As an internal control, consider pausing ad hoc manual retries, spreadsheet fixes, and dashboard edits unless the Incident Commander approves them.

Validate the blast radius before you call it a processor outage#

Map impact across processor, gateway, acquiring connection, and payout rails separately. Similar customer symptoms can come from different failure points.

Start with evidence: internal alerts, provider status pages, webhook failures, API error trends, request IDs, and transaction logs. Then classify the failure before you change routing:

- Hard declines: issuer refuses authorization.

- Soft declines: can trigger authentication flow.

- Timeouts or connection errors: retry only with idempotency controls.

Contain carefully and route only what you can retry safely#

Containment should reduce risk, not spread it. Start failover with the smallest meaningful traffic slice and queue uncertain transactions instead of launching broad retries.

Retry only where idempotency behavior is confirmed end to end. If request keys are missing, inconsistent, or lost between services, do not widen traffic shifts.

Before you expand, run a small replay sample with known request IDs and confirm one intended business event in your internal record for each customer action.

Publish a tight status update without guessing root cause#

Send timely updates in a defined sequence to internal and external stakeholders as impact is confirmed.

A practical format is: what is confirmed, what is affected, what actions are underway, what remains unknown, and when the next checkpoint will be posted. Do not promise root cause in the first hour unless you have the evidence.

Gate continuity changes on ledger integrity#

Before you widen reroutes, resume queued payouts, or declare continuity restored, use posting integrity as a hard internal checkpoint.

Sample transactions from before and during the incident and match provider references, internal payment IDs, amounts, currencies, and final states. If provider success lacks an internal entry, or one customer action maps to multiple entries, stop expansion and route the item to exception handling.

Keep money moving with controlled degradation#

Once immediate containment is in place, shift to controlled continuity. Keep the highest-impact money movement running first, and use only backup routes you already know are compatible for method, currency, and compliance.

Rank flows by business impact#

Set an explicit incident-time priority order for critical flows in your command channel, based on actual business impact. Protect flows tied to stricter SLA expectations before lower-priority traffic.

Use your own business-impact signals to decide what is truly critical. If a flow can wait without immediate harm, queue it while you protect higher-impact movement. Write the ranked order into the incident record and confirm that ops, finance, and product are using the same list.

Shift only eligible traffic to alternative rails#

If primary card rails are unstable, reroute only traffic that is already supported on alternative rails and still passes your existing compliance gates. If the backup path cannot support the required method, currency, or compliance coverage, treat it as an exception path, not normal failover.

Start with a narrow slice, then verify that rerouted transactions are processing as expected before you expand.

Do not assume "offline" means independent from later internet-dependent clearing and settlement. An alternative rail can help continuity now while still depending on downstream clearing and settlement.

Apply payment orchestration with explicit failback criteria#

Use orchestration rules with predefined trigger conditions, not ad hoc switching. Automated failover helps continuity, but it gets riskier if you do not define how and when traffic returns to the primary path.

Write failback criteria before widening traffic: required recovery evidence, approver, and validation on the primary route. Keep the return decision observable and reversible. Treat partial issuer-side fallback behavior as degraded service, not proof that normal routing health has returned.

Record every degraded-mode decision for the postmortem#

Log every route change in a format that will still be usable in after-action review. Capture the owner, timestamp, affected flow, decision, evidence, reversal condition, and next review time.

This is a control, not overhead. If a degraded-mode change has no owner or reversal condition, it is drift, not controlled degradation.

Protect ledger integrity during retries and replays#

Recovery traffic can easily create a second financial truth. The safe order is simple: protect the internal book first, then restore customer-visible state.

| Control | Verify | Detail |

|---|---|---|

| Enforce idempotency keys on every retry path | The same business action keeps the same key across attempts and produces one write to the internal record | Keep keys within the strictest provider limit you support: Adyen 64 characters and Stripe up to 255; PayPal warns that omitting PayPal-Request-Id can duplicate a request |

| Rebuild balances from the ledger, not from provider status | Expected debit or credit entry exists, maps to the internal transaction record, and the rollup matches the balance | If the provider shows success but posting is missing or incomplete, keep the balance pending until it is confirmed |

| Define a discrepancy policy before automatic release | When provider state and internal state disagree, investigate the discrepancy before advancing the item | Make records review-ready with provider reference, internal transaction ID, idempotency key, event ID if available, state-change timestamps, and current posting status |

| Reprocess webhooks in controlled order and ignore duplicates | Track processing state per event and ignore already processed events with a success response | For Stripe, use ending_before with auto-pagination; list results are limited to the last 30 days, and undelivered events can retry for up to three days |

Enforce idempotency keys on every retry path#

Make idempotency keys mandatory on any retry path where the same payment action could be submitted twice. Stripe and Adyen document safe retries with the same idempotency value after timeout or connection issues, and PayPal warns that omitting PayPal-Request-Id can duplicate a request. Also treat support as endpoint-specific, not universal.

For retries on payment actions, confirm that the same business action keeps the same key across attempts and produces one write to your internal record. Keep keys within the strictest provider limit you support: Adyen 64 characters and Stripe up to 255. Generating a new key for each app-layer retry can cause the provider to treat each attempt as a new request.

Rebuild balances from the ledger, not from provider status#

Treat wallet and stored balances as derived state from immutable journal entries, not as the source of truth. Before you show a recovered balance, release funds, or resume payout eligibility checks, verify that the expected posting exists and maps to the internal transaction record.

Use this checkpoint:

- Expected debit or credit entry exists in the internal record.

- Entry maps to the internal transaction record.

- The rollup matches the balance you are about to expose.

If the provider shows success but posting is missing or incomplete, keep the balance pending until it is confirmed.

Define a discrepancy policy before automatic release#

Set a clear incident-time policy for state conflicts: when provider state and internal state disagree, investigate the discrepancy before advancing the item. One control option is routing the item to an exception queue and pausing automatic release pending review.

Make discrepancy records review-ready on first touch:

- Provider reference

- Internal transaction ID

- Idempotency key

- Event ID, if available

- State-change timestamps

- Current posting status

If you cannot explain why provider success conflicts with internal pending, keep the item in review instead of advancing it automatically.

Reprocess webhooks in controlled order and ignore duplicates#

Assume webhooks can be duplicated and arrive out of order. Stripe also automatically retries undelivered events for up to three days, so replay-safe handlers are required.

When reprocessing Stripe events, use the documented chronological path, ending_before with auto-pagination, and remember list results are limited to the last 30 days. Then enforce two checks:

- Track processing state per event.

- Ignore already processed events with a success response to prevent new side effects.

Without ordering and duplicate controls, replay can apply transitions in the wrong sequence and create drift even if provider data is complete. For a step-by-step walkthrough, see How Payment Platforms Really Price FX Markup and Exchange Rate Spread.

Reconcile and settle in phases after stability returns#

Once retries, replays, and routing are under control, do not close the incident yet. Service can look healthy while money movement is still unclear, so use a practical recovery order: transaction outcome first, settlement second, customer correction last.

| Phase | Focus | Pass condition |

|---|---|---|

| Match unknown outcomes to the ledger | Resolve discrepancies, errors, missing transactions, and exception cases to a single defensible status | Require one clear chain: provider reference -> internal transaction record -> expected posting |

| Verify settlement across processor, acquirer, and bank evidence | Treat settlement as complete only when processor reports, internal matching output, and bank movement line up | Pass only when credits, debits, and counts align with internal outputs and any variance has a documented cause |

| Clear the exception queue by reason code, then fix customer impact | Work by exception type such as missing transaction or failed capture, duplicate debit candidate, and delayed payout | Make each case review-ready with provider reference, internal transaction ID, merchant reference if used, payout or settlement batch ID, posting status, and bank-match status where relevant |

| Close only when the done criteria are evidenced | Hold closure until the incident window is fully accounted for with evidence | Unknown outcomes are resolved or explicitly documented, settlement variance is explained, payout SLA is back within your own defined and measured target, and no unresolved high-risk exceptions remain without owner, cause, and next action |

Match unknown outcomes to the ledger#

Start by identifying every payment in the incident window with an ambiguous outcome and force it to a single defensible status. Build a review set from discrepancies, errors, missing transactions, and exception cases, then resolve it by matching transaction records to your accounting records.

Anchor the match with provider references plus your internal canonical identifiers. For each item, require one clear chain: provider reference -> internal transaction record -> expected posting.

Flag three buckets early:

- Matched once and complete.

- Missing candidate: provider record exists without posting, or posting exists without provider record.

- Duplicate candidate: one business action maps to multiple provider transactions or multiple internal writes.

If mappings become many-to-one, stop bulk resolution and investigate. If you cannot explain the identifier chain end to end, keep the item in exceptions instead of forcing success or failure.

Verify settlement across processor, acquirer, and bank evidence#

After transaction outcomes are mostly known, verify cash movement, not just event status. Treat settlement as complete only when processor reports, internal matching output, and bank movement line up.

Use provider-native matching artifacts in your review. For Adyen, use transaction-level Settlement Details plus batch-level aggregate settlement details, including credits, debits, and counts. For Stripe, reconcile each payout as a settlement batch, and handle instant or manual payouts explicitly against transaction history rather than assuming automatic payout behavior covers them.

If external acquirers are involved, include those files or feeds in the same review path. Then match payout batches to bank statements. Pass only when credits, debits, and counts align with internal outputs and any variance has a documented cause.

Clear the exception queue by reason code, then fix customer impact#

Work your exceptions by type, not as one mixed backlog. Queue names and reason-code semantics vary by system, but the core pattern is to route by exception type for investigation and processing.

Use reason families tied to concrete actions:

- Missing transaction or failed capture: determine whether the gap is provider-side, posting-side, or both. Reattempt only when the original action is still valid and traceable to the same internal record.

- Duplicate debit candidate: require two-sided evidence before correction, for example duplicate provider references or duplicate internal postings for one customer action. Then route to refund or reversal with affected references recorded.

- Delayed payout: verify whether payout creation, settlement, and send each occurred. Do not apply manual correction until posting and settlement evidence agree.

Make each case review-ready on first touch with provider reference, internal transaction ID, merchant reference (if used), payout or settlement batch ID, posting status, and bank-match status where relevant. Closure quality depends on outputs being consistent and traceable.

Close only when the done criteria are evidenced#

Close the incident only when the incident window is fully accounted for with evidence, not when traffic looks normal. Use explicit completion criteria and hold closure until each one is met.

Use a closure check like this:

- Matching is complete for the incident window, with unknown outcomes resolved or explicitly documented.

- Any settlement variance is explained across processor reports, any external-acquirer inputs, internal matching outputs, and bank matching.

- Payout SLA is back within your own defined and measured target for the relevant payout flows.

- No unresolved high-risk exceptions remain open without owner, cause, and next action.

If any criterion is missing, the incident is still in recovery.

If you are turning these phases into an internal runbook, map each checkpoint to your webhook events, payout statuses, and reconciliation controls in Gruv Docs.

Handle outage and data breach paths differently#

Outage recovery and breach response should branch early. If breach indicators appear, prioritize containment, evidence preservation, and legal or notification review before resuming normal operations.

Separate restoration from breach containment#

An outage and a breach can overlap, but they should not share the same primary objective. Recovery work focuses on restoring normal operations. Breach response focuses first on securing systems, fixing vulnerabilities, and preserving investigative evidence.

| Decision area | Service outage path | Data breach path |

|---|---|---|

| Primary objective | Restore continuity and reduce business impact | Contain exposure, preserve evidence, and assess notification duties |

| First major action | Re-route, retry carefully, recover impaired service | Secure affected systems and stop further compromise |

| Restoration authority | Ops-led restoration decisions | Security and legal review, with forensic input, before resuming regular operations |

If you cannot yet distinguish provider failure from cyber compromise, take the stricter path and avoid broad changes that could destroy evidence.

Isolate suspected compromise before broad remediation#

If ransomware or cyberattack indicators are present, isolate affected systems first. CISA guidance supports immediate isolation plus system image and memory capture from affected-device samples.

For payment operations, that means taking affected equipment offline and avoiding early power-downs that can hinder investigation or lose evidence. Before broad cleanup, verify that affected hosts are identified, isolated, and forensic artifacts are captured, or that capture is directed, from representative devices. For cardholder-data incidents, document whether PCI forensic investigation must be handled by a listed PFI.

Tighten communications while facts are still forming#

Use stricter communication controls for breach events than for routine outages. Breach response may require notifications to law enforcement, affected businesses or individuals, and potentially regulators, card brands, media, or consumer reporting agencies, depending on obligations.

Send reviewed updates that clearly separate:

- Confirmed facts

- Unconfirmed findings

- Next update time and investigation owner

Gate full restoration on security and legal review#

Set a practical branch rule: when breach indicators are present, the incident lead should not approve return to regular operations alone. Require security and legal sign-off, with forensics or law-enforcement input as appropriate, before resuming regular operations.

This is an internal operating rule, not a universal legal mandate. It aligns with guidance to involve forensics and law enforcement in deciding when normal operations can safely resume. Related reading: Continuous KYC Monitoring for Payment Platforms Beyond One-Time Checks.

Build communication and evidence artifacts that stand up later#

Once you split outage recovery from breach containment, the next job is to make the record defensible from the start. A practical default is three linked artifacts: an executive timeline, a customer update log, and a technical decision log tied to operational evidence.

Create the three linked records early. Start the executive timeline as a chronological record: detection time, who declared the incident, routing changes, customer-impact checkpoints, and restoration decisions. Keep it live during the incident so post-incident analysis can use a complete record and action items, instead of rebuilding events later.

Keep the customer update log separate from the internal timeline. Record what was published, to whom, when, who approved it, and the next promised update time. For each outward statement, map it to a timestamped fact in the timeline.

Build the status pack leaders actually need. Use a consistent status pack each update cycle so leaders can make tradeoff decisions quickly. Include MTTD and MTTR, and, when relevant to your commitments, include SLA impact windows. If you are actively managing exceptions, consider showing open exceptions in the same pack with a clear internal definition so operational risk sits next to timing metrics.

Define terms upfront so interpretation stays consistent: MTTD is time to detect, MTTR is time to recover or resolve, and SLA impact reflects risk to measurable client commitments.

Link each technical decision to evidence. For every major action, log the decision and the evidence available at that moment. Link retries, failover routing, replay, or payout holds to the exact system snapshot, trace, provider report, or queue/export artifact reviewed.

This matters even more when breach indicators are present. Evidence preservation should stay explicit in the log, and cleanup steps should not overwrite artifacts needed for investigation or later review.

Avoid the mistakes that create second incidents#

Second incidents are often caused by avoidable response mistakes. Four failures show up repeatedly: duplicate replays, false recovery signals, misclassified payment errors, and vague ownership.

- Switching providers without idempotency checks: When widening failover routing, verify that retries are recognized as the same operation. Also verify key-retention behavior, because reusing a pruned key, for example after 24 hours in some systems, can be treated as a new request.

- Restoring traffic before settlement verification: Do not treat API success alone, including

200/OK, as proof of payment success. Gate restoration on settlement matching evidence, including transaction-level checks and batch-level matching to payout and bank-statement records. - Treating all payment failures as processor issues: Triage by failure class first. Separate issuer or acquirer response conditions from customer-, business-, and processor-related causes so your fix targets the actual fault path.

- Running escalations with vague ownership: Use a single incident command structure with explicit role ownership, for example incident command, communications, and operations, so decisions, communications, and operations stay coordinated under pressure.

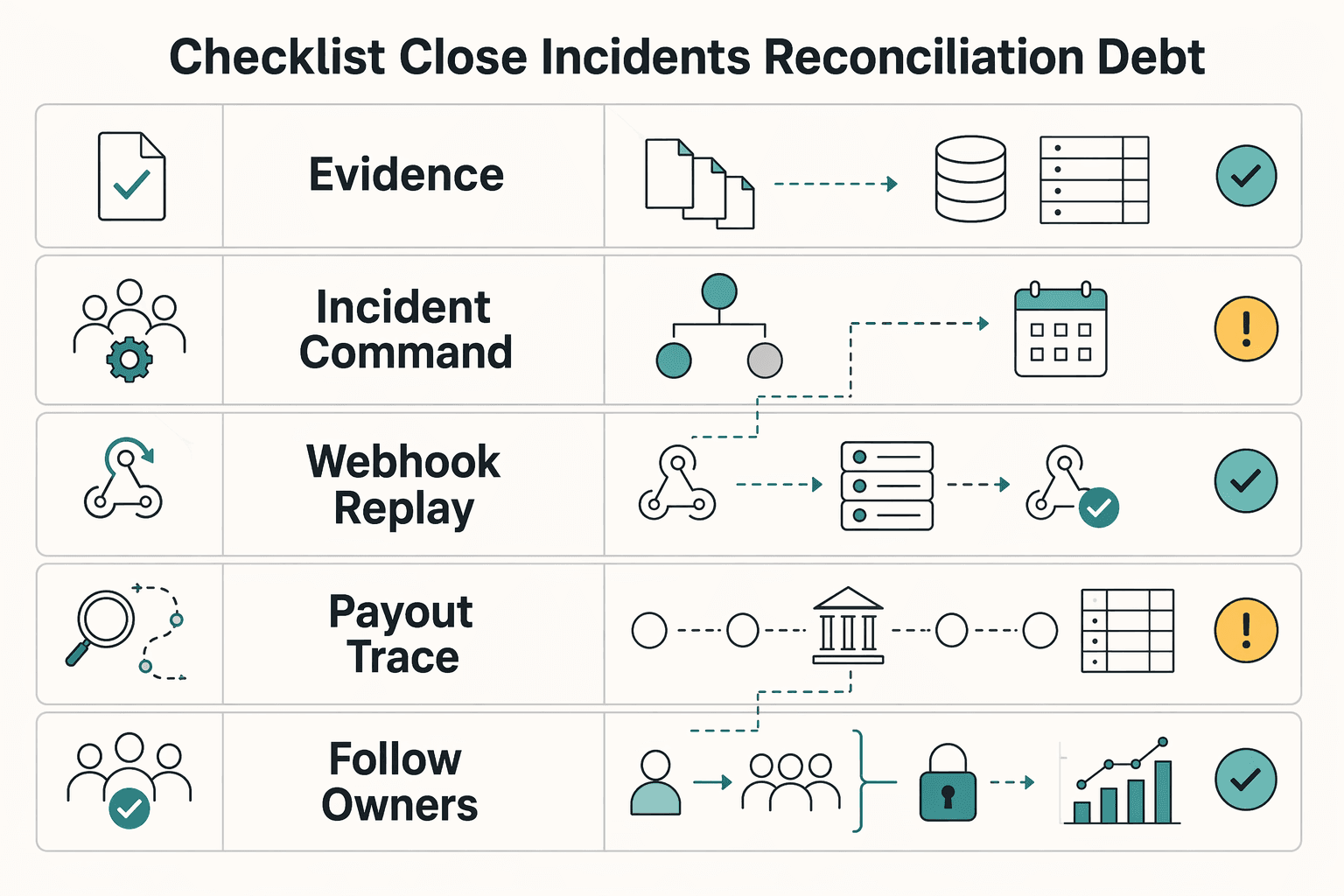

Use this checklist to close incidents without reconciliation debt#

Close the incident only when money state is verified, not just when traffic recovers.

- Incident type confirmed and severity documented across gateway, processor, and acquiring connection.

Record where failure occurred, one link or multiple, affected rails or products, and final severity based on business impact and SLA impact. If triage is uncertain, treat it as higher severity until narrowed.

- Incident command structure active through closeout, with a named owner and decision log.

Keep a clear incident lead through closure and preserve a single timeline of key decisions, timestamps, and money-movement changes.

- Controlled degradation enabled with documented failover routing and failback criteria.

Document what triggered failover and what confirmed failback. Verify temporary routing or manual overrides were removed.

- Idempotency controls validated for retries, replays, and webhook reprocessing.

Confirm retry paths used idempotency keys and webhook processing deduped by event ID, with out-of-order handling considered. Where keys may be pruned after at least 24 hours, validate late replays against your internal record before release.

- Reconciliation and settlement verification completed, with exception handling documented.

Resolve unknown outcomes first, then verify settlement with the relevant provider outputs, for example, payout reconciliation and payment accounting reports. Reconcile any manual payouts against transaction history and document owners for remaining variances.

- Postmortem evidence captured with metrics and corrective actions.

Capture the timeline, impact, investigation, solutions used, detection and recovery timings, and payout SLA impact in one package, with explicit action items. Schedule review within 1 week while evidence is fresh.

- Follow-up owners assigned for resilience gaps in orchestration, alerts, and third-party dependencies.

Assign named owners and due dates, including contract or notification-path gaps involving acquirers or other third parties.

If finance, ops, and product cannot all explain the same money-movement story from the decision log and matching evidence, keep the incident open.

If you want to pressure-test your outage and breach workflow against your payout and ledger operations, talk to Gruv.

Frequently Asked Questions

What should a payment platform do in the first 60 minutes of an outage?

Use a structured incident process first: identify what is failing, coordinate response ownership, apply containment and retry-safe controls, and track mitigations as recovery proceeds. The priority is to protect payment integrity while restoring service, with updates that stay clear about what is known, what is unknown, and when the next checkpoint will be.

How is outage response different from data breach response in payments?

Outage response is mainly about restoring service continuity. Breach response adds containment, evidence preservation, and notification planning before broad restoration. For suspected payment card breaches, PCI guidance emphasizes immediate response and warns that actions like shutting systems down can make investigations harder. Your breach plan should account for payment brands, acquirers, and other required parties, and may require a PCI SSC-approved PFI.

How do idempotency keys prevent duplicate payments during incident recovery?

Idempotency keys make retries safer for non-idempotent requests by tying repeat attempts to the same operation. If the same request is retried with the same key, the platform should return the same result instead of creating a second charge or payout. Duplicate-payment risk can increase when idempotency handling is inconsistent across retry paths.

What minimum controls are needed for multi-gateway resilience?

There is no universal minimum gateway count that guarantees resilience. The practical baseline is redundancy, assessment of critical providers, alternative arrangements, and capacity that remains reliable under stress. Those controls only matter if they are usable during an incident, not just written down.

Which metrics best show incident response is improving over time?

Use a consistent incident metric set that covers both speed and operational impact. Track detection and recovery timing alongside service disruption impact, then compare trends over time. Availability is useful context, but it should be read alongside impact metrics, not by itself.

Why are public outage reports often insufficient for operational decision-making?

Public outage reporting is useful for situational awareness, but it is not complete operational truth. Outage datasets can have measurement uncertainty and transparency gaps, so they may not provide enough detail for operational decision-making on their own. Use them as signals, then rely on your own incident and payment-operations data for decisions.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- cisa.gov/sites/default/files/2024-08/Federal_Governme...trusted

- cisa.gov/resources-tools/resources/federal-government...trusted

- csrc.nist.gov/pubs/sp/800/61/r3/finaltrusted

- eba.europa.eu/activities/single-rulebook/regulatory-activi...trusted

- federalreserve.gov/frrs/guidance/interagency-guidance-on-third-...trusted

- federalreserve.gov/supervisionreg/topics/operational-resilience...trusted

- fedramp.gov/docs/rev5/playbook/csp/continuous-monitoring...trusted

- ftc.gov/business-guidance/resources/data-breach-resp...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: