Quick Answer

Freelancer marketplaces should handle W-8/W-9 migration by routing each payee to the correct form before moving records and tying that form to payout and reporting controls. Use Form W-9 for U.S. persons and resident aliens, Form W-8BEN for foreign individuals, and send conflicting or incomplete records to manual review, payout hold, and escalation before year-end reporting is affected.

What Triggers a W-8/W-9 Migration Review#

This guide walks you through moving tax profiles cleanly. Keep the right form on file, protect payouts, and avoid year-end reporting errors that only show up later. It is written for the compliance, legal, finance, and risk owners at a freelancer marketplace who have to decide what gets validated, who approves exceptions, when a payout hold is justified, and when a case needs escalation instead of a quick fix.

Before you start#

Step 1. Identify which IRS form family each payee should sit in. For U.S. persons, Form W-9 is the IRS form used to request taxpayer identification details, including a TIN, and the IRS instructions say it applies to a U.S. person, including a resident alien. For foreign individuals, Form W-8BEN is used to establish foreign status in the U.S. withholding and reporting context. Before you touch production data, you should be able to sort records into at least a current Form W-9 queue, a current Form W-8BEN queue, and an exception queue for anything that does not fit cleanly.

Step 2. Tie the stored form to the reporting output you may need later. W-8 and W-9 data usually feeds year-end forms such as Form 1099-NEC and Form 1042-S. Form 1099-NEC is the IRS information return used for nonemployee compensation, and the IRS says businesses that pay $600 or more of nonemployee compensation report it on Form 1099-NEC. Form 1042-S is used to report income and amounts withheld for covered foreign-person payments. Before you migrate any cohort, confirm that the form type on file still matches the reporting tag or review status you expect instead of assuming legacy data was classified correctly.

Step 3. Set the operating boundary before you move money. This guide focuses on U.S. tax form handling inside marketplace operations, not every tax classification edge case. The practical question is not just whether a payee submitted a document. It is whether the tax profile now has the right form, the right status, and enough supporting data to let you release payouts without creating downstream reporting trouble.

One early failure mode is treating the Form W-9 versus Form W-8BEN decision as only a migration-mapping issue. In practice, that choice can affect TIN collection for U.S. persons, foreign-status evidence for non-U.S. individuals, and readiness for Form 1099-NEC or Form 1042-S later. If residency signals, identity details, or the existing form record conflict, treat the case as a candidate for a payout hold and an escalation checkpoint rather than a same-day override.

That is the point of the rest of this guide: give you clear control points, named owners, and decision rules to use during migration instead of after reporting season exposes the mistake. Related: How to Get a Residence Permit in Germany as a Freelancer.

Set scope and prerequisites before touching production data#

Do not migrate any tax profile set until scope, source records, and approvals are explicit. If you cannot name the legal entity, jurisdiction, payee cohort, source record, and approver, pause the migration.

Step 1 Map the scope by entity, jurisdiction, and payee cohort#

Start with a record inventory before you run any technical export. Split scope by marketplace entity, operating jurisdiction, and payee cohort (U.S. tax resident vs non-U.S. tax resident): for U.S. persons, Form W-9 is the starting form; for foreign individuals, Form W-8BEN is used to establish foreign status.

Use a control sheet that shows, for each cohort, where the current Form W-9 or Form W-8 record lives, who owns that source, and whether the target profile should preserve or replace it. This helps catch tax-status data stored outside the main profile, such as in a country site, legacy vendor table, or onboarding tool.

Step 2 Confirm the minimum production controls#

Before production migration, confirm encrypted storage, least-privilege access, and an audit trail. Least privilege means granting only the minimum authorizations needed, and an audit log is a chronological record of accesses and operations.

In practice, every tax-profile create/update event should be time-ordered and reviewable. If you cannot produce usable logs, stop the migration. Publication 1075 can serve as an encryption-control benchmark where it is relevant, but the core requirement is the same: do not move sensitive tax data into an environment with weak access controls or unverifiable changes.

Step 3 Lock owners and approval gates#

Set sign-off gates across compliance, legal, finance, and marketplace ops before production changes begin. Use a RACI matrix to define who approves cohort scope, who can place or release payout holds, who accepts exceptions, and who can halt cutover.

Approval gates should pause and review work before go-live, not approve changes after tax data is already in production.

Decide form routing rules before moving any records#

Lock form-routing rules in writing before migration starts: route each onboarding or backfill record to Form W-9, Form W-8BEN, or mandatory manual review before payout release. Do not let code or ops infer form type from a single field.

Step 1 Build the routing table#

Keep the table simple enough for ops to execute and engineering to enforce.

| Record pattern | Request or preserve | Mandatory manual review trigger | Year-end reporting readiness |

|---|---|---|---|

| Payee is treated as a U.S. independent contractor for payment reporting | Form W-9 | Existing profile shows foreign status, or identity and Taxpayer Identification Number (TIN) data are incomplete or inconsistent | Form 1099-NEC readiness path |

| Payee is a nonresident alien beneficial owner providing documentation to the payer | Form W-8BEN | Existing profile shows Form W-9 or other U.S. status signals, or status is ambiguous | Form 1042-S readiness review |

| Source records conflict or core tax data are missing | Do not auto-route to a final state | Manual review before payout release | Hold reporting-tag assignment until resolved |

Do not route from country or state alone. Compare the scoped tax profile, current onboarding inputs, and migrated values before assigning a route.

Step 2 Add conflict gates before payouts move#

Treat conflict rules as hard gates. If current residency signals conflict with the existing tax profile, escalate before payout release, in both directions: a foreign-looking record with an existing Form W-9, or a U.S.-looking record with a prior Form W-8BEN.

For each routed case, retain a clear trail of the source signal, the requested or preserved form, and any exception approval.

Step 3 Tie each route to reporting outputs#

Each route must map to downstream reporting. The Form W-9 lane should support Form 1099-NEC readiness for qualifying independent-contractor payments. The Form W-8BEN lane should support Form 1042-S readiness for foreign-person income and withholding reporting. If Form 1042-S is required, Form 1042 filing is also required.

State caveats explicitly: ambiguous status classification, conflicting records, or a missing TIN should go to compliance or tax/legal review, not frontline closure. Include an evidence pack with the current form, prior tax profile, identity fields, TIN status, and payout status. For a step-by-step walkthrough, see How to Find Your Blue Ocean as a Freelancer Through Operational Clarity.

Assign control owners and escalation checkpoints#

Name control owners before cutover so payout holds, exception decisions, and audit-trail evidence do not depend on ad hoc judgment under deadline pressure.

Step 1 Assign decision rights by control type#

Use a simple RACI-style map with clear decision boundaries: compliance owns form-classification disputes and evidence sufficiency, finance or payments risk owns payout hold placement and release, operations runs data-integrity checks, and product/engineering owns audit-trail field and event completeness.

| Control area | Owner | Stated responsibility |

|---|---|---|

| Form-classification disputes | Compliance | Owns form-classification disputes and evidence sufficiency |

| Payout holds | Finance or payments risk | Owns payout hold placement and release |

| Data-integrity checks | Operations | Runs data-integrity checks |

| Audit-trail completeness | Product/engineering | Owns audit-trail field and event completeness |

Operations should not clear conflicting Form W-9 versus Form W-8BEN status for speed alone. For every held record, you should be able to identify who detected the issue, who applied the hold, who owned the exception SLA, and who made the final form decision.

Step 2 Set severity triggers before cutover#

Treat invalid or missing TIN conditions as highest severity. IRS backup withholding can apply at 24 percent when a TIN is missing or obviously incorrect, and CP2100/CP2100A notice handling should have a named owner and escalation path.

| Trigger | Severity | Handling note |

|---|---|---|

| Missing or obviously incorrect TIN | Highest severity | Backup withholding can apply at 24 percent; CP2100/CP2100A handling should have a named owner and escalation path |

| U.S.-versus-foreign status conflict | Hard stop | If the profile indicates nonresident or foreign status, Form W-9 instructions point the requester to Form W-8 or Form 8233 instead of standard W-9 handling |

| Missing consent artifacts | Escalate internally | Not an IRS-defined trigger, but it weakens evidence quality |

| Repeated profile edits near cutover | Escalate internally | Not an IRS-defined trigger, but it weakens evidence quality |

Treat U.S.-versus-foreign status conflicts as a hard stop. If the profile indicates nonresident or foreign status, Form W-9 instructions point the requester to the appropriate Form W-8 or Form 8233 instead of standard W-9 handling. Missing consent artifacts or repeated profile edits near cutover are not IRS-defined triggers, but they should still escalate internally because they weaken evidence quality.

Step 3 Require dual release approval and complete logging#

If evidence is incomplete but business pressure is high, require dual approval for payout-hold release, typically compliance plus finance. This is an internal control choice, not an IRS-prescribed rule.

Engineering should log each tax-profile create, update, hold, release, and exception decision with timestamp, actor, prior value, new value, source signal, and linked document status. Records should remain inspectable and retained for as long as they may be material to tax reporting, audits, or internal review.

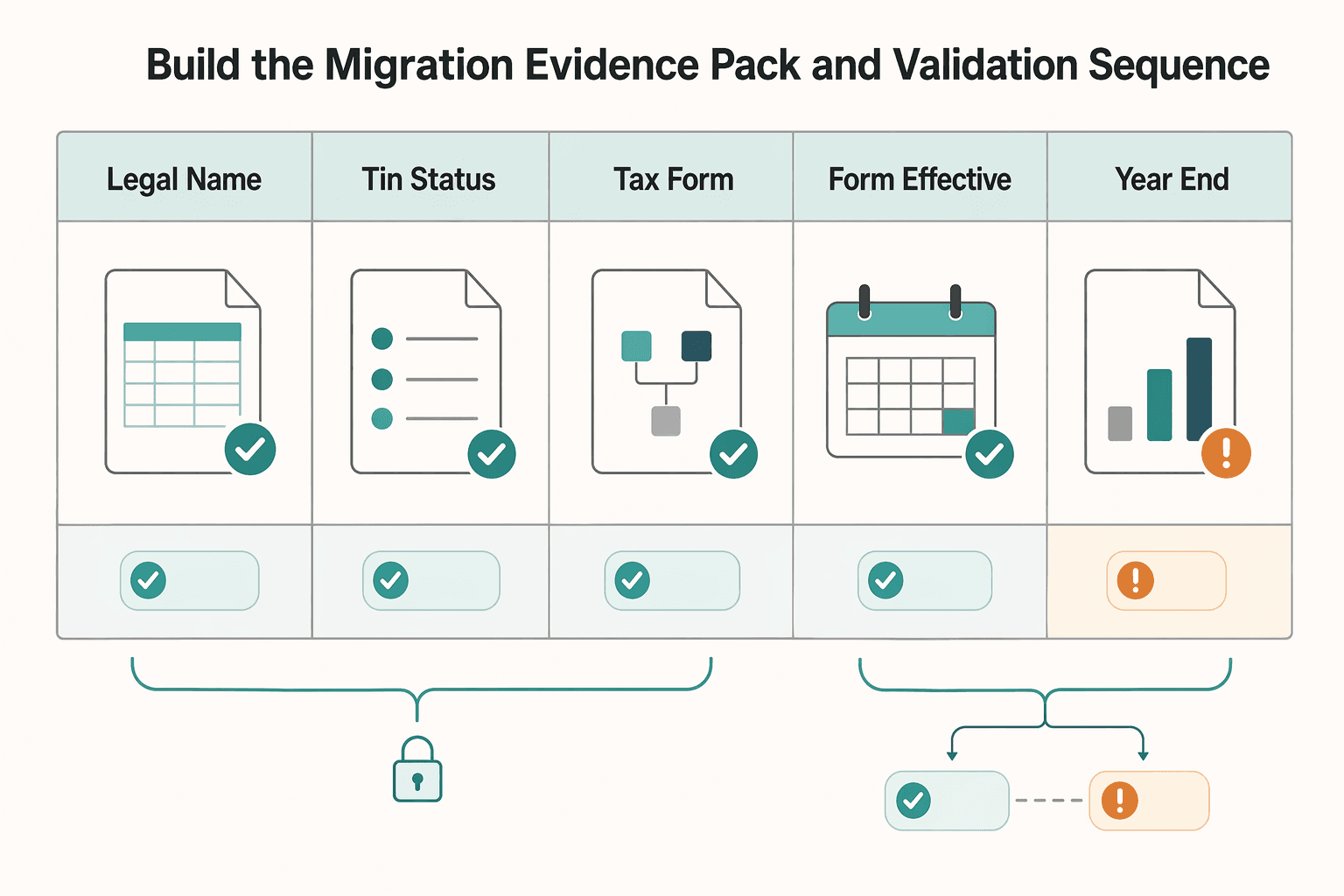

Build the migration evidence pack and validation sequence#

Before cutover, your approvers need evidence that each migrated tax profile still supports the correct payout treatment and year-end reporting path. If that evidence is incomplete or conflicting, call no-go.

Step 1 Assemble a pre-cutover evidence pack that is reviewable. Include source exports for the in-scope population, a field-mapping dictionary, migration transformation rules, and expected record counts by form type for the wave. Version these artifacts by date and wave so reviewers can tie each dry run to the exact inputs. Keep updating migration metadata and wave inputs as scope changes rather than validating against stale discovery data.

Start with count reconciliation. Source and target counts for Form W-9, Form W-8, and any separately tracked Form W-8BEN records should align after documented exclusions. If records were intentionally excluded, merged, or deferred, record that reason in your migration log before review.

Step 2 Reconcile the fields that drive classification and reporting. Prioritize fields tied to identity, withholding risk, and whether records feed Form 1099-NEC or Form 1042-S.

| Field | What to verify | Why it matters |

|---|---|---|

| Legal name | Exact match or documented normalization | For Form W-9, name and TIN alignment is required to avoid backup withholding errors |

| TIN status | Same status in source and target (for example present, missing, unverifiable) | Form W-9 is used to provide a correct TIN |

| Tax form type | Form W-9 vs Form W-8/W-8BEN stays consistent unless approved exception exists | This determines U.S. vs non-U.S. tax handling path |

| Form-effective status | Active/inactive/superseded/expired state carries over correctly | Prevents inactive or superseded forms from driving decisions |

| Year-end reporting tag | Downstream tag remains correct (for example Form 1099-NEC vs Form 1042-S) | W-8/W-9 data drives these reporting outputs |

If address is part of your tax identity controls, reconcile it too.

Step 3 Run dry-run comparisons and define stop conditions in advance. Compare source and target record-by-record, not only totals. Treat cosmetic changes, such as casing or whitespace normalization, as acceptable only when they do not change tax treatment. Treat changes to identity fields, tax form type, form-effective status, or reporting tags as blocking until resolved.

Keep a mismatch log that labels each difference as acceptable, remediated, or blocking. If reviewers cannot reconstruct why a mismatch was accepted, treat it as unresolved.

Step 4 Include security and audit evidence, then issue a go/no-go packet. Include the evidence your reviewers need to reconstruct what happened across systems: access logs, audit log samples, and the controls applied to tax-data review surfaces for that wave. The packet should name signers, open risks, and rollback criteria tied to specific failure modes.

Use specific rollback triggers, such as unexplained count variance, blocking mismatches in form type or reporting tags, missing audit evidence, or access-control defects on tax data. If triggered, stop, fix, and rerun with a fresh evidence pack.

For a related breakdown, read How to Handle a Cease-and-Desist Letter as a Freelancer.

Execute cutover with go/no-go and rollback decisions#

Cutover should stay controlled: freeze risky changes, run formal gates, migrate, validate, and only then reopen writes. If a gate fails, use the preplanned no-go or rollback path instead of patching live tax records under payout pressure.

Step 1 Freeze risky changes and create the recovery point. Apply a change freeze to in-scope tax-profile edits, including source-side intake for the migration cohort, so the pre-flight baseline does not move during execution. Then create and preserve a backup for emergency rollback use. If post-freeze counts change outside approved exceptions, treat the baseline as invalid and stop.

Step 2 Run formal go/no-go gates at T-1 and T-0. Use T-1 to confirm ownership, escalation paths with response-time expectations, and rollback readiness. Use T-0 to reconcile the frozen source against the approved migration package immediately before start.

| Checkpoint | Pass only if | Action if it fails |

|---|---|---|

| T-1 go/no-go | Sign-offs are current, backup is confirmed, escalation coverage is active, open risks are accepted or remediated | No-go |

| T-0 pre-flight | Frozen counts still match expected counts, no unapproved post-freeze edits, migration package matches approved version | No-go and reconcile |

| Post-migration validation | Sample checks preserve form type, effective status, and reporting path | Roll back the wave for systemic defects; isolate affected records if defects are limited |

Step 3 Migrate, validate spot samples, and place temporary payout holds on failed records. Validate spot samples across Form W-9, Form W-8, and Form W-8BEN populations, including records tied to different year-end reporting paths. Confirm each sampled target record maps back to source and keeps intended payout treatment unless an approved exception exists. For failed records, apply temporary payout holds with explicit release conditions, for example corrected form received and revalidation passed, an assigned owner, and escalation if unresolved within your policy window.

Step 4 Reopen controlled writes only after traceability is complete. Reopen edits in a controlled sequence after validation passes and exception records are contained. Execution logs should support end-to-end reconstruction with owner, planned and actual timing, status, and notes. Capture exception decisions in the audit trail so reviewers can trace what was approved, when, and for which records.

Related reading: How to Obtain a 'VAT Number' as a Freelancer in the Netherlands. If you want a practical next step, try the W-8 form generator.

Stabilize the first 30 days after migration#

A clean cutover is not the finish line. For the next 30 days, run tight operating controls so tax-profile changes do not quietly break payout behavior or year-end reporting.

Watch for drift every day#

Use daily reconciliation as a control, not a legal requirement. Review every tax profile changed since the last check, including form type, effective status, payout treatment, and the reporting path for Form 1099-NEC or Form 1042-S.

This matters because W-8/W-9 data feeds year-end reporting outputs, and nonemployee compensation paid to nonresident aliens is reported on Form 1042-S rather than Form 1099-NEC. For each changed record, confirm the current state is traceable in the post-cutover audit trail and still aligned with the form on file. If you track W-8/W-9 request status, review completed vs pending daily so "fixed" profiles are not left in pending-documentation states.

Treat queue age as a reporting-risk signal#

Queue age should drive risk decisions, not just ops reporting. Track manual-review aging against your exception SLA targets and prioritize items that could block complete Form 1099-NEC or Form 1042-S outcomes.

Do not rely on overdue-only views. Use queue controls that flag records likely to miss SLA, then prioritize by reporting impact first, payout impact second, and age third.

Treat repeat edits and reopened cases as defect signals#

Repeat edits and reopened cases are usually a process signal, not just operator noise. If the same record is edited multiple times or reopens under the same reason code, treat it as a likely routing-rule or status-mapping defect until proven otherwise.

Run a weekly trend check across reopened cases, repeated payout holds, and duplicate manual-review reasons. If patterns repeat across operators, fix the rule, prompt, or mapping before scaling reviewer capacity.

Publish a weekly risk log#

Publish one weekly risk log with unresolved escalations, payout hold counts, queue-aging risk, and a named remediation owner for each issue. Keep it short, but specific enough for compliance, finance, and ops to act.

Do not carry open escalations without a clear owner and next action date. In this first month, unclear ownership is itself a control failure.

Handle common failure modes without overbuilding process#

Do not default to full rollback after every post-cutover issue. Use phased remediation for isolated defects, and switch to rollback when routing logic, reporting tags, or other shared controls are affected across a cohort.

| Failure mode | Immediate response | Follow-up |

|---|---|---|

| Wrong form type is captured | Place a payout hold first | Request the corrected form, revalidate the tax profile, and confirm the reporting tag still routes correctly between Form 1099-NEC and Form 1042-S |

| Incomplete TIN evidence or identity conflicts | Keep payout on hold | Include the submitted form, onboarding identity data, conflicting fields, and clear case notes |

| Repeated wrong-form routing, missing reporting tags, or broken audit links across the same slice | Roll back the affected cohort | Replay only validated records and rerun audit-trail checks before release |

| Defect is isolated to a narrow intake path | Use phased remediation | Use rollback when the same error appears across shared routing, status mapping, or reporting tags |

Step 1. Freeze payouts when the wrong form type is captured, then correct the record end to end. If a contractor is routed to Form W-9 when Form W-8 is required, or the reverse, place a payout hold first. Then request the corrected form, revalidate the tax profile, and confirm the downstream reporting tag still routes correctly between Form 1099-NEC and Form 1042-S.

The corrected record should show the right form, effective status, and reporting path in the audit trail. Wrong person-status routing can change reporting outcomes, and nonresident compensation cases may require withholding at 30% unless reduced by treaty. Document approver, evidence reviewed, and release rationale before lifting the hold.

Step 2. Escalate incomplete TIN evidence or identity conflicts instead of guessing. Keep payout on hold when Form W-9 TIN and legal name do not match or when identity data conflicts across onboarding, profile, and submitted form. Form W-9 is used to collect the payee's correct TIN, and mismatches create backup-withholding exposure.

Your evidence pack should include the submitted form, onboarding identity data, conflicting fields, and clear case notes. Do not release funds based on a promise of later cleanup.

Step 3. Roll back the affected cohort when reconciliation points to a migration defect. If reconciliation shows repeated wrong-form routing, missing reporting tags, or broken audit links across the same slice, roll that cohort back to the last known-good state. Rollback should follow a pre-planned path, not an improvised incident response.

After rollback, replay only validated records and rerun audit-trail checks before release. Confirm cohort-level reconciliation by form type, traceability of changed records, and reporting alignment with 1099-NEC versus 1042-S logic.

Step 4. Apply one decision rule to limit remediation risk. Use phased remediation when the defect is isolated and contained to a narrow intake path. Use rollback when the same error appears across shared routing, status mapping, or reporting tags. Planned rollback is disruptive, but emergency rollback is usually worse.

Final checklist to reduce regulatory surprises#

Migration is only complete when you can prove routing is correct, unresolved records are controlled, and year-end reporting outputs are ready.

- Freeze routing rules with record-level evidence.

Document how U.S. person or resident-alien records route to Form W-9 and how non-U.S. records route to the appropriate W-8 path. For sampled records, show why the route was chosen from evidence on file. If identity or tax-residency signals conflict, keep the case in manual review with a payout hold until corrected.

- Lock go/no-go, rollback, and payout-hold triggers as an internal control.

IRS guidance does not prescribe your meeting format, so treat this as your governance checkpoint before release. Confirm owners agree on the same failure triggers, including missing or incorrect TIN, wrong form type, reconciliation mismatch, or unclear reporting path.

- Close the evidence pack before declaring success.

Include migration mapping, reconciliation outputs by form type, exception tracking, and audit-trail exports so reviewers can trace source to target. Make retention operational, not theoretical: W-9 records should be kept for four years.

- Verify reporting readiness, not just profile quality.

Confirm migrated data supports the correct downstream path for Form 1099-NEC and Form 1042-S where applicable. Check filing mechanics early: if you expect 10 or more combined information returns across Form 1099 series, Form 1042-S, and Form W-2, electronic filing is required.

- Publish unresolved risk before closeout.

Keep a visible log of open exceptions with owner, payout status, next escalation step, and target decision time. If you cannot quickly identify cases that still threaten TIN correctness, 1099-NEC completeness, or 1042-S coverage, the migration is not ready to close.

Frequently Asked Questions

What is the first step in a W-8/W-9 migration for a freelancer marketplace?

Start by separating records into the correct tax-status path before moving anything. Decide whether each worker belongs in a U.S. person or non-U.S. person route, then request the matching form instead of bulk-migrating old labels.

When should a platform collect Form W-9 instead of Form W-8BEN during contractor onboarding?

Collect Form W-9 when the payee is a U.S. person or resident alien. Route a non-U.S. individual to Form W-8BEN, and if onboarding signals conflict, send the record to exception review before payout release.

Which controls are mandatory before tax-data cutover in production?

Before cutover, confirm routing and withholding controls, encrypted storage, least-privilege access, and a reviewable audit trail. Also make sure missing or obviously incorrect TINs have a defined escalation path and that each record is mapped to the correct year-end reporting output.

What events should trigger a payout hold during migration?

Place a payout hold on records with a missing or obviously incorrect TIN, a U.S.-versus-foreign status conflict, or an unresolved form and reporting path. The guide also treats incomplete or conflicting identity evidence as a reason to hold and escalate before funds are released.

How should teams validate migrated records before year-end tax reporting starts?

Validate both sampled records and cohort totals before reporting starts. Confirm the form on file, TIN status, form-effective status, and the downstream reporting tag on each record, then reconcile counts by form type and review exceptions across the population.

When should compliance escalate to external tax counsel instead of resolving internally?

Escalate to external tax counsel when the form choice is genuinely ambiguous or the withholding and reporting consequences are material. If the record does not clearly support W-9 versus W-8BEN selection, may point to a different W-8 path, or business pressure is pushing release without support, do not force an internal answer.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

How Platforms Reduce Chargeback Risk With Daily Decision Rules

If you run a marketplace platform or an embedded payments product, generic merchant advice leaves gaps. This playbook is for the team making decisions across product, ops, finance, and engineering, not a single merchant storefront.

How to Get a Residence Permit in Germany as a Freelancer

**Treat your German freelance residence permit like an operations project, and you will cut avoidable delays before they start.** The hardest part is often not the forms but the uncertainty around procedure, especially if you are working from Berlin-based experience while local office workflows shift as you prepare paperwork. Confusion costs time, money, and momentum.

Negative Balance Management for Marketplaces

Marketplace deficits are a payments liability problem, not something you can explain away after launch. They hit finance, ops, and engineering at the same time, because someone still has to absorb the loss, stop more money from leaving, and reconcile the ledger cleanly. This piece treats marketplace negative balance management as an operating discipline: who is liable, how recovery works, and which controls you can actually enforce.