Quick Answer

To obtain a Dutch VAT number as a freelancer, register through the correct route for your legal form and wait for the Belastingdienst to confirm your entrepreneur status for tax purposes. For an eenmanszaak, KVK handles the handoff; for a bv, the notary registers with KVK and the Tax Administration. Do not issue VAT-bearing invoices until your status, identifiers, and filing obligations are confirmed.

Start here so you do not create a tax mess later#

If you want the clean, compliant route as a freelancer or zzp'er in the Netherlands, set up first and bill second. VAT problems usually start when people invoice before confirming registration steps, VAT treatment, and filing duties, then have to fix missed deadlines or filing errors later.

Before you start#

This guide is for freelancers in the Netherlands who want a safe, workable setup and may feel overwhelmed by Dutch tax paperwork. It focuses on execution: getting set up, using that setup correctly, and knowing when to stop and get help.

One practical nuance matters up front: a freelancer or zzp'er label is related to, but not the same as, a sole proprietorship. Treat the label as secondary. What matters is the operating path: register with the Chamber of Commerce (KVK), confirm your VAT obligations, and run your admin in a way that supports clean filing.

What this section covers#

This article stays focused on Dutch VAT registration and day-to-day VAT operations for a zzp'er, with cross-border caveats only where they affect invoicing or filing. It is not a full guide to every residency, immigration, or entity-structure scenario.

What you should have by the end#

You should leave with:

- A decision path you can use to assess your next Dutch VAT registration step.

- A document checklist for registration and VAT operations.

- A setup sequence you can run in order.

- A copy/paste pre-billing checklist.

- A clear escalation rule: if VAT treatment, client location, or filing duty is unclear, pause, verify, and document before issuing a live invoice.

Keep this principle in view throughout: VAT compliance does not end at registration. You still need to manage output and input VAT, handle domestic and international filing requirements, track VAT and ICP deadlines, and correct filings when needed.

Decide if you need Dutch VAT registration now#

Start with the safer default: if you plan to invoice from a Dutch business presence, verify VAT treatment first and do not assume an exception applies without confirmation. Do that check before your first live invoice, not after.

Step 1#

Base the decision on how and where you operate, not on the label you use for your business. If your freelance activity has a Dutch operating footprint and you expect to invoice from that setup, run Dutch VAT analysis first. Only treat non-registration as valid when you have actually confirmed it.

Use this checkpoint: if you plan to send client invoices from a Dutch business presence, pause and verify VAT treatment first. Edge cases exist, especially in cross-border setups, but those are review cases, not guess cases.

Step 2#

Break the decision into three branches: Netherlands domestic activity, EU cross-border activity, and EU simplification routes.

| Branch | What it usually means for you | What to verify before invoicing |

|---|---|---|

| Netherlands domestic setup | You need a Dutch VAT determination before invoicing and filing decisions | Whether your activity is taxable in the Netherlands and whether a confirmed exception applies |

| EU cross-border activity | Your Dutch setup may still matter, but EU rules can change how VAT is declared | Whether OSS is relevant, and whether your services fall within the relevant EU rules |

| Cross-border SME route | A possible simplification in specific cases, not an automatic shortcut | Prior notification in your Member State of establishment, threshold checks, and EX number confirmation |

For the EU branch, keep two points straight. OSS schemes are optional, and OSS VAT returns are additional. They do not replace regular VAT returns. Also, the EUR 10,000 EU-wide threshold is tied to specific cross-border B2C e-commerce categories from 1 July 2021, including TBE services and intra-EU distance sales of goods, so do not apply it to every freelance service scenario.

Step 3#

Check your assumptions against the tax authority's rules before you send the first VAT-bearing invoice. Confirm the transaction type, whether the client setup is domestic or cross-border, whether OSS is actually relevant, and what VAT treatment applies.

Document your reasoning at the same time. Keep the rule page you relied on, the date checked, and a short note on why you chose that treatment. If the treatment is unclear, hold the invoice draft and verify first.

Step 4#

Escalate early when the cross-border facts get complicated.

For complex cross-border transactions, the EU VAT Cross Border Rulings (CBR) mechanism can provide advance VAT treatment rulings. Requests are made in a participating EU country where you are registered for VAT, and the Netherlands is a participating country.

If you are exploring the cross-border SME scheme, treat it as a separate eligibility track. You need prior notification in your Member State of establishment, Union turnover in the current and previous calendar year must not exceed EUR 100,000, and a practical completion checkpoint is confirmation that the EX number can be used in the selected Member State or Member States. The process should not take longer than 35 working days, but it can take longer if additional investigations are required.

If you still cannot clearly place your case in one branch, the next move is simple: verify first, then bill.

For a step-by-step walkthrough, see How to Get a SIREN/SIRET Number as a Freelancer in France.

Gather the documents before you register#

Make sure your business story is consistent before you start. At the start, registration runs through the KVK and Belastingdienst route, and the Belastingdienst decides whether you are an entrepreneur for tax purposes.

Step 1#

Start with a minimum prep pack. This is a practical checklist, not an official exhaustive list.

- valid personal identification: passport or ID card

- your planned legal-form route,

eenmanszaakorbv - a short business activity description, what you sell and how you deliver it

- a simple client model note, where you expect clients

- your business address plus where administration and records will be kept

Run one consistency check before you submit anything: your activity, address, and operating model should match across your notes and registration inputs.

Step 2#

Create a basic evidence folder before you file. Keep it simple and searchable, for example:

01_ID02_KVK_submission03_Business_activity_and_client_model04_Address_and_admin_records05_Tax_letters_and_notes

Save PDFs, screenshots, confirmations, and a dated note of what you submitted. If you register as an eenmanszaak, keep proof of what KVK received because KVK handles the Belastingdienst registration handoff. If you use a bv, keep the notary paperwork with your KVK and Tax Administration registration records.

Step 3#

Set one legal-form checkpoint before you file:

eenmanszaak: KVK handles registration with the Belastingdienstbv: your notary registers with KVK and the Tax Administration- entrepreneur status for tax purposes is decided by the Belastingdienst

If you see guidance that suggests a separate VAT application, treat it as case-specific and confirm your route before assuming extra filing steps.

Pick the right setup path for your business form#

Choose the simplest compliant form that matches your facts. If you are a solo freelancer with straightforward operations, an eenmanszaak is often a practical starting point, and you can revisit the structure as your risk or scale changes.

Step 1 Choose a legal form, not a freelancer label#

zzp'er describes how you work, not your legal structure. The common legal forms are an eenmanszaak or a bv, and your registration follows that form, not the freelancer label.

If you offer services or products with a profit goal, KVK registration is generally the starting point. Before you proceed, do a basic independence check. If your setup looks like de facto employment, fix that first.

Step 2 Use the practical default path for simple solo setups#

For many solo freelancers, an eenmanszaak is the common route. After KVK registration, there is typically an automatic handoff to the tax authorities, so your next job is to track the follow-up correspondence.

Treat timing and filing cadence as confirmation items, not assumptions. Correspondence is often cited at around two weeks, and VAT filing can be monthly or quarterly, with quarterly common but not universal. Until your KVK number, VAT number, and obligations are confirmed, do not assume you are ready to issue VAT-bearing invoices.

Step 3 Treat a bv as a structure decision, not a shortcut#

Choose a bv because your business facts call for it, not because it sounds more formal. The practical rule is to verify each registration and tax step for your case instead of assuming the same handoff flow as a simple eenmanszaak.

Keep the records together: KVK confirmations, tax letters, and company setup documents. If you want a deeper sole-trader walkthrough, use A Guide to the Netherlands' 'Eenmanszaak' for Sole Traders.

Step 4 Confirm tax classification and VAT obligations after registration#

Your decision is not complete until tax classification is clear. Freelancers need to handle VAT and income tax, and VAT is a separate return stream from income tax.

Final checkpoint: confirm your VAT obligations, filing cadence, and identifiers before first billing, then keep your records for at least seven years.

Related: Can Digital Nomads Claim the Home Office Deduction?.

Register and confirm your VAT status end to end#

Treat registration as incomplete until you can show the full chain from business registration to tax classification. A common mistake is assuming that a completed KVK step means your VAT position is already live.

Step 1 Register through the correct route#

Start with your legal form, because the route differs by structure. If you register as an eenmanszaak, KVK handles registration with the tax authority. If your structure is a bv, your notary registers you with KVK and the Tax Administration.

After that step, keep a record of what was submitted, when, and through which route. That is your first control point if anything later is delayed or unclear.

Step 2 Wait for tax classification before treating VAT as live#

Do not treat VAT as active until the tax authority has decided whether you are an entrepreneur for tax purposes. That decision matters because, if you are classified as an entrepreneur, you must file VAT and income tax returns.

Use a simple rule: status is still pending until you have tax-side confirmation, not just business-side registration.

Step 3 Use a hard completion test#

You are only done when you can evidence both parts:

- the KVK or notary registration step is completed

- the Belastingdienst has decided your entrepreneur status for tax purposes

If either side is missing, you are still mid-process. Keep the records together so the chain is easy to prove.

Step 4 Handle delays or unclear status without assumptions#

If classification is unclear after registration, verify the original handoff route first, KVK for eenmanszaak, notary for bv, then confirm your status with the Belastingdienst.

Use one timeline and log each step:

- registration date

- key follow-up dates

- what was confirmed versus what is still unclear

If classification is still unresolved, treat your VAT status as unresolved too.

Use the right number in the right place every time#

Use this rule every time: share your VAT identification number (btw-id) externally, and use your omzetbelastingnummer (ob-nummer) when dealing with the Netherlands Tax Administration.

If you are treated as an entrepreneur for VAT purposes, you receive a btw-id and use it with customers and suppliers, including on invoices.

| Number | Use it for | Keep it out of |

|---|---|---|

| btw-id (VAT identification number) | Customer and supplier communication and invoices | Primary tax-administration correspondence |

| omzetbelastingnummer (VAT tax number / ob-nummer) | Contact with the tax authority | Customer-facing documents and invoices |

Set your invoice template so the btw-id is fixed and not retyped each time. Also check invoice numbering. Invoices must be sequentially numbered, and numbering errors must be rectified.

Before sending EU-facing invoices, validate the public VAT number in VIES when relevant. As a practical check, some guides describe Dutch VAT IDs as NL + 12 characters. Use your issued documentation as the source of truth. If your template number, customer-shared number, and VIES result do not match, fix the template before billing.

Before you send your first cross-border invoice, run your btw-id through the VAT Number Validator and store the result with your invoice records.

Set up invoicing and recordkeeping before first client billing#

Before you send the first invoice, lock in a repeatable process. You want one clean line from issuance, to payment tracking, to record storage, to VAT return inputs. If your business is based in the Netherlands, invoices must meet legal requirements, and non-compliant invoices can affect your customer's VAT deduction.

| Control area | Key requirement | Record or action |

|---|---|---|

| Invoice template | Include your VAT identification number, your KVK-nummer if you have one, the applicable VAT rate, the VAT amount, and a sequential invoice number | Build one template and stop hand-editing core fields |

| Invoice sequence | Numbering must stay sequential, and unnumbered invoices must be rectified | Keep a clear trail for any correction so gaps are explainable |

| Payment tracking | Record issue date, status, amount due, amount collected, and payment date once settled | Use auditable invoice and payment status trails so changes are traceable instead of overwritten |

| Invoice records | Keep the issued invoice, payment proof, and any correction or dispute context in one invoice record | For cross-border work, note when a listed special case applies |

| VAT return inputs | Tag invoice VAT handling when you issue it, then reconcile corrections, cancellations, unpaid invoices, or edge cases before filing | If key fields are missing, fix the record before it goes into your return data |

- Lock your template before billing

Build one template and stop hand-editing core fields. Include your VAT identification number, your KVK-nummer if you have one, the applicable VAT rate, the VAT amount, and a sequential invoice number.

- Issue invoices in a clean sequence

Numbering must stay sequential, and unnumbered invoices must be rectified. Set your numbering format once, then keep a clear trail for any correction so gaps are explainable.

- Track payment separately from issuance

Treat "sent" and "paid" as different states. For each invoice, record issue date, status, amount due, amount collected, and payment date once settled. Where possible, use auditable invoice and payment status trails so changes are traceable instead of overwritten.

- Store records with each invoice

Record retention is part of invoicing compliance, so store documents as you go. Keep the issued invoice, payment proof, and any correction or dispute context in one invoice record. For cross-border work, note when a listed special case applies, such as selling a new or nearly new means of transport to a customer in another EU country.

- Prepare VAT return inputs continuously

Tag invoice VAT handling when you issue it, then reconcile exceptions before filing, for example corrections, cancellations, unpaid invoices, or edge cases. If key fields are missing, fix the record before it goes into your return data.

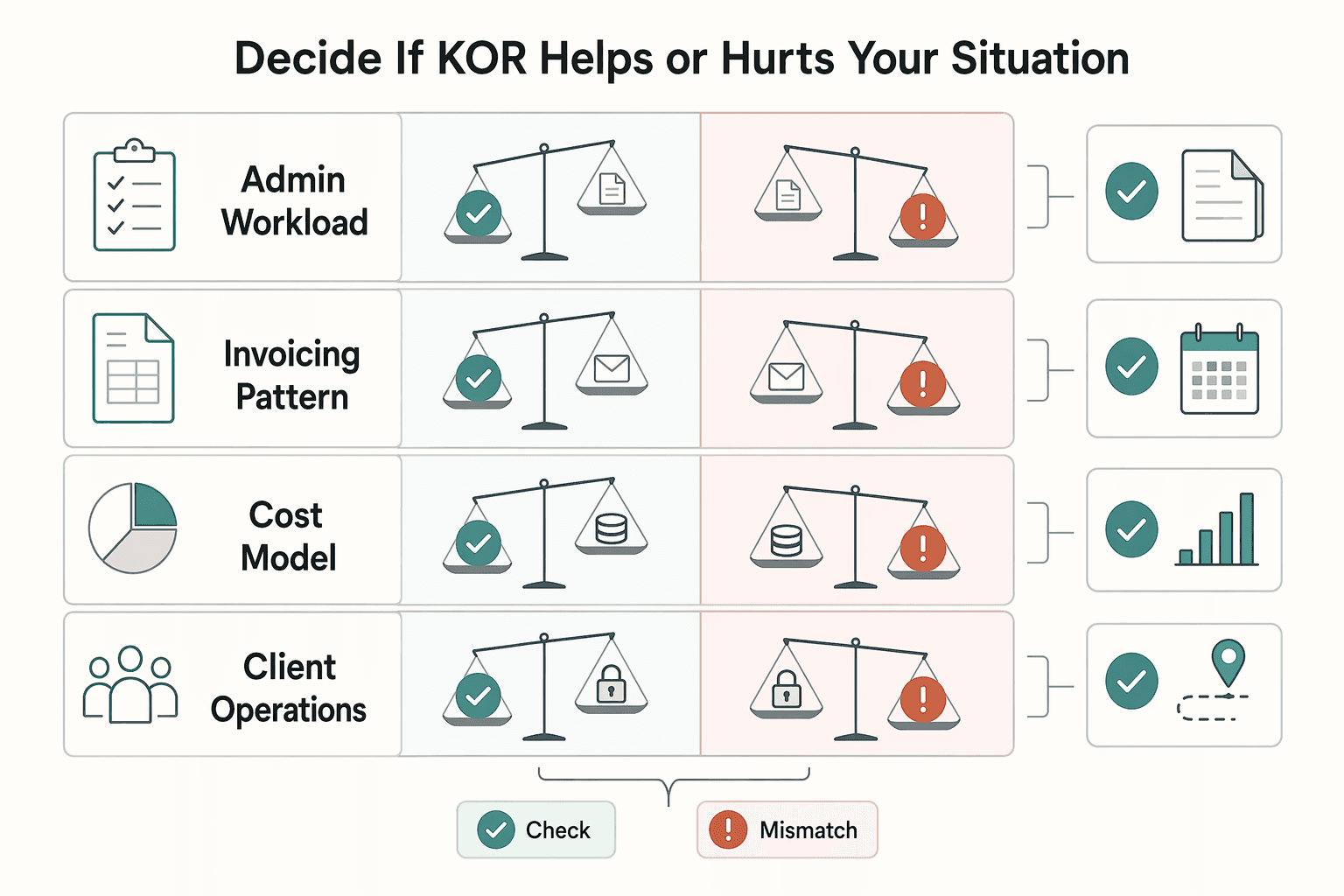

Decide if KOR helps or hurts your situation#

KOR is a business decision, not an automatic under-threshold choice. In the source material for this guide, KOR is described as potentially freeing you from VAT payments if turnover stays under €20,000, but you still need a clean tax process overall, including income tax.

Before you decide, confirm your base setup first. Make sure your KVK registration is in place, then verify current KOR conditions with the tax authority or a qualified adviser before you change invoice treatment.

Use a quick side-by-side check with your real numbers:

| Decision area | KOR path (what to test) | Regular VAT path (what to test) |

|---|---|---|

| Admin workload | Could simplify parts of VAT handling. Confirm what work remains in your case | Keep your current VAT invoicing and tracking flow and measure the actual monthly effort |

| Invoicing pattern | Validate invoice treatment before issuing invoices | Continue with your normal VAT invoicing pattern, with standard VAT commonly 21% unless another treatment applies |

| Cost model | Compare your total admin effort, pricing, and tax workflow before you switch | Keep your current setup and track real cost and effort over the same period |

| Client operations | Check whether your clients can process your invoice format without friction | Keep the format your clients already expect |

Decision rule: if the operational impact is unclear in your numbers, do not move into KOR until you have modeled the impact and confirmed the current rules.

Reassess this choice when your revenue pattern, client geography, or business model changes. This matters even more once cross-border work grows, where compliance can get heavier for small businesses. Keep a dated decision note, and if requirements or deadlines are unclear, confirm them before the next invoice cycle, because missed tax requirements can lead to fines and penalties.

Handle EU and non-EU client scenarios without guessing#

For each cross-border invoice, use the same sequence: classify the client and transaction, validate key details, then choose the filing path. If the client's VAT status or the place-of-supply treatment is unclear, stop and check before you issue anything.

Step 1 classify before you invoice#

Start with two checks: EU versus non-EU, and business customer versus consumer. In EU scenarios, that B2B or B2C split can change VAT handling, so do not work from assumptions.

For EU business clients, request the VAT identification number early. If it is missing or inconsistent, treat that as a validation flag and confirm the VAT treatment before invoicing. Add a short note to the invoice file with client location, status used, and your reasoning.

Step 2 use OSS only when it actually simplifies your setup#

OSS can let you declare and pay VAT due in multiple Member States through one portal, and registration is in one Member State of identification. It is optional, not mandatory.

If you use an OSS scheme, two rules are non-negotiable:

- OSS returns are additional and do not replace your regular VAT return.

- You must declare all supplies that fall under that scheme through the OSS return.

For EU cross-border B2C activity, OSS can reduce separate registrations. Since 1 July 2021, EU cross-border B2C e-commerce rules changed and refer to an EU-wide EUR 10 000 threshold, but do not apply that threshold beyond its scope without checking first.

Step 3 validate EU VAT numbers where relevant and log the result#

When relevant, validate the client VAT number and keep the result with the invoice records. Log the check date, VAT number, result, and linked invoice ID. For process detail, see How to verify a European VAT number using the 'VIES' system.

Step 4 keep an audit-ready evidence pack per cross-border client#

For each client file, store:

- client VAT details, when applicable

- invoice logic notes, why you applied that VAT treatment

- supporting correspondence confirming client status or location

Keep these records with the invoice trail so the VAT decision is defensible without reconstructing it later.

For non-EU work, keep the same discipline. The non-Union OSS scheme exists. If the case is complex, get validation before invoicing. For complex EU cross-border matters, a VAT Cross Border Ruling may be requested in a participating EU country where you are VAT-registered.

Avoid the mistakes that create penalties and cleanup work#

VAT problems often start in day-to-day execution errors such as forgotten invoices, incorrect amounts, or incorrect VAT codes. If invoice data, a VAT code, or a filing period looks wrong, correct it quickly and document the fix, because VAT return errors can lead to extra assessments, fines, and wasted time.

| Issue type | What it means | What to review or do |

|---|---|---|

| Invoice-admin issue | Invoices are missing, incomplete, or not traceable in your records | Correct the invoice trail, then log what changed, which invoices were affected, and when you fixed it |

| VAT-reporting issue | VAT coding or amounts are wrong in bookkeeping or return inputs | Correct bookkeeping entries and VAT codes, then check whether submitted VAT returns used the wrong values |

| Cadence issue | A filing period is missed or unclear | Keep a compliance calendar for your VAT periods and reconcile each period to complete incoming and outgoing invoice lists before filing |

Step 1 separate invoice-admin errors from VAT-reporting errors#

Treat these as different failure types so you fix the right layer:

- invoice-admin issue: invoices are missing, incomplete, or not traceable in your records

- VAT-reporting issue: VAT coding or amounts are wrong in bookkeeping or return inputs

- cadence issue: a filing period is missed or unclear

For each affected invoice set, review:

- whether all sales and purchase invoices are present in your records

- VAT code used in bookkeeping

- return period the invoice was included in

If you find missing or inconsistent invoice records, correct the invoice trail, then log what changed, which invoices were affected, and when you fixed it.

Step 2 correct VAT coding through the reporting chain#

A corrected invoice file is not enough if your return inputs still carry the old value. Common error patterns include forgotten invoices, incorrect amounts, and incorrect VAT codes. Missing invoices may only surface during an audit and can cause double taxation or missed deductions.

Use this recovery path:

- Identify all affected sales and purchase invoices.

- Correct bookkeeping entries and VAT codes.

- Check whether submitted VAT returns used the wrong values.

- If EU sales reporting was involved, review whether ICP declarations or EU sales listings also need correction.

- Record a remediation note linking invoice IDs, corrected entries, and reporting impact.

Step 3 lock your filing cadence and reconcile every period#

If your filing rhythm is unclear, treat that as a red flag. VAT workflows can run monthly, quarterly, or annually, and uncertainty here can create extra cleanup.

Use a simple control:

- keep a compliance calendar for your VAT periods

- reconcile each period to complete incoming and outgoing invoice lists before filing

- keep invoice processing consistent in your admin flow

If bookkeeping is outsourced, you still remain legally responsible as the entrepreneur.

Step 4 escalate repeated uncertainty early#

If you are repeatedly unsure about VAT coding, invoice inclusion, or EU sales reporting, bring in a professional instead of improvising. Repeated corrections can signal that your decision process is unstable.

Keep an audit-ready evidence pack:

- invoices

- booking exports or screenshots

- correction notes

- return calculations and adjusted reporting records

- tax correspondence

Your file should show one clear line from original invoice to corrected VAT outcome, with no reconstruction needed later.

Related reading: A Deep Dive into the US-Netherlands Tax Treaty for Independent Contractors.

Know exactly when to bring in a tax professional#

Bring in a professional as soon as the issue affects VAT treatment logic, not just invoice wording. If you are unsure which EU route applies, or you keep correcting returns, get a review before the risk compounds.

Step 1 escalate on decision-level uncertainty#

Escalate when you are deciding between regular domestic VAT handling, OSS, and the cross-border SME route, and you cannot clearly justify the choice. OSS returns are additional and do not replace your regular VAT return, and if you opt in, you must report all supplies covered by that OSS scheme through OSS.

For the cross-border SME scheme, a small enterprise files one prior notification in its Member State of establishment, MSEST, and exemption starts only after that state grants and confirms the EX number. If that confirmation is not clear, do not treat supplies as exempt.

Step 2 bring a file your advisor can verify quickly#

Bring a compact working file so the advisor can trace your treatment from setup to filing. For example:

- registration and VAT ID details you already have on file

- invoice and return examples for the scenarios you are unsure about

- notes or correspondence tied to prior corrections or disputed treatment

Your quality check is simple: they should be able to follow one clean line from registration, to invoice, to return period, to VAT treatment.

Step 3 use a clear pay-now vs pay-later standard#

Pay for review before notices or repeated corrections force reactive cleanup. Escalate immediately if your cross-border classification is still unresolved, if a cross-border SME registration moves beyond the normal 35 working days, or if corrections keep repeating.

For genuinely complex EU cross-border cases, ask whether a VAT Cross-border Rulings (CBR) request is appropriate. The Netherlands participates in that mechanism for advance treatment on complex cross-border VAT transactions.

Your next steps and copy paste checklist#

Treat your setup as complete only when each identifier, filing route, and cross-border choice is documented from official records.

- Confirm your business form and registration route.

Decide your legal form and complete the required registration steps using official guidance for your jurisdiction. Do not fill gaps from memory. Keep your registration confirmation, submission date, reference numbers, and the exact business activity description you used.

- Verify every tax identifier issued by the tax authority.

Save each letter, email, or portal download in one place. Track four fields: official label, number shown, issue date, and where it is used. Keep identifier usage aligned with the official records.

- Set invoice and recordkeeping controls before invoicing.

For each invoice, keep the invoice, payment status, client country, any client VAT details, and a short VAT logic note for the treatment used. This is what lets you justify why domestic VAT was charged, why another treatment applied, or why a cross-border route was used. If you cannot trace one invoice from document to return values without guessing, tighten the process before you bill again.

- Choose your EU cross-border route deliberately.

If you have EU cross-border supplies, decide between your domestic filing route, OSS, the cross-border SME scheme, or a case that needs advice. Under OSS, you register in one Member State of identification and must declare all supplies covered by that scheme through OSS. OSS returns are additional and do not replace the regular VAT return. Union and non-Union are quarterly, import is monthly.

- If using the cross-border SME route, track the actual trigger points.

The Union turnover cap is EUR 100 000 in the current and previous calendar year. You file one prior notification in your MSEST, and exemption starts only when MSEST grants and confirms the EX number. If registration goes beyond 35 working days, escalate for review.

- Decide on domestic small-business VAT relief only after you document the tradeoff.

Verify the current local rules first, then write down why you chose in or out and when you will reassess.

- Run one compliance calendar and escalate early when signals appear.

Track regular VAT tasks, OSS deadlines where relevant, and any cross-border SME quarterly turnover report in one reminder system. Escalate early if EU treatment is unclear, your structure changes, or invoice and tax corrections keep repeating. For complex cross-border VAT transactions, ask whether a VAT Cross-border Rulings request fits. It can provide advance guidance, but it does not guarantee a favorable outcome.

If any part of your setup is still ambiguous after the checklist, contact Gruv to confirm a compliant, traceable operating path for your workflow.

Frequently Asked Questions

Do freelancers in the Netherlands usually need an NL VAT number, or are there real exceptions?

There is no safe blanket assumption. If you plan to invoice from a Dutch business presence, verify your VAT treatment under current Dutch tax guidance before you invoice. Only treat non-registration as valid when you have actually confirmed it and kept written support.

What is the practical difference between a VAT identification number (btw-id) and an omzetbelastingnummer?

Use the btw-id externally, including on invoices and with customers or suppliers. Use the omzetbelastingnummer when dealing with the Netherlands Tax Administration. Keep the official labels and usage instructions from your Dutch tax correspondence.

How do I obtain a Dutch VAT number step by step through KVK and Belastingdienst?

Follow the route for your legal form. If you register as an eenmanszaak, KVK handles the handoff to the tax authority; if your structure is a bv, your notary registers you with KVK and the Tax Administration. Then wait for the Belastingdienst to decide your entrepreneur status for tax purposes, and keep a dated log of what was submitted and confirmed.

If I use the Small Businesses Scheme (KOR), do I still need to file VAT returns?

Do not assume KOR removes all VAT obligations. The guide describes KOR as potentially freeing you from VAT payments if turnover stays under €20,000, but it says to confirm current conditions before changing invoice treatment. Also verify what remains for VAT charging, VAT recovery on costs, and any ongoing filing or recordkeeping duties.

Do I need to handle both turnover tax (omzetbelasting) and income tax (inkomstenbelasting) as a freelancer?

Yes. Treat VAT and income tax as separate questions and separate return streams. If you are classified as an entrepreneur for tax purposes, you must file VAT and income tax returns.

When does One-Stop Shop (OSS) matter for EU clients, and when is separate Dutch VAT registration still required?

OSS matters when you opt into an optional special scheme for supplies covered by that scheme and register in one Member State of identification. If you opt in, you must declare all supplies covered by that scheme through the OSS return, and OSS returns are additional to your regular VAT return. The cross-border SME route is separate, and this guide does not define Dutch domestic registration triggers.

What are the clear signs that I should stop and hire a tax professional?

Bring in a professional when cross-border VAT treatment is unclear, you cannot justify choosing regular domestic VAT handling, OSS, or the cross-border SME route, or corrections keep repeating. Escalate if you are waiting on EX number confirmation, if cross-border SME registration runs past the normal 35 working days, or if the case is complex enough that a VAT Cross-border Rulings request may fit.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- business.gov.nl/starting-your-business/starting-as-a-self-em...trusted

- business.gov.nl/regulations/invoice-requirementstrusted

- purl.dlib.indiana.edu/iudl/inauthors/encodedtext/VAA2443trusted

- sec.gov/Archives/edgar/data/769218/00011931252007706...trusted

- sme-vat-rules.ec.europa.eu/sme-scheme/cross-border-sme-scheme_entrusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- vat-one-stop-shop.ec.europa.eu/one-stop-shop_entrusted

- vat-one-stop-shop.ec.europa.eu/index_entrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Can Digital Nomads Claim the Home Office Deduction?

Claim the deduction only when your facts and records can carry it. With the home office deduction for digital nomads, the real decision is usually a three-way call: claim it, do not claim it, or pause and get help because your file is not ready.

Choosing an Eenmanszaak in the Netherlands as a Sole Trader

Treat "unlimited liability" as a legal exposure question, not a tax registration question. If you are weighing an **eenmanszaak netherlands** setup, keep the main warning simple: clean VAT or GST registration evidence does not tell you whether a Dutch business claim can reach your personal assets, or how that plays out when some of those assets sit outside the Netherlands.