Quick Answer

Start by confirming who is Merchant of Record for each flow, then lock owners, deadlines, and evidence standards before adding automation. Effective chargeback management for marketplaces depends on a repeatable path: intake, decision, representment, and reconciliation. Build one default evidence packet, route every case through a fight-or-accept table, and tie outcomes to reserves or offsets so Finance and Ops track the same loss owner.

How to handle chargeback management for marketplaces when you are the Merchant of Record#

If you are the Merchant of Record (MoR) in a marketplace flow, chargebacks are an execution problem. The dispute lands with you. The real question is who reacts, how fast, and with what evidence.

Before you tune fraud rules or add software, confirm a basic fact: which entity acts as MoR for each payment flow you run. In many marketplace sales, the platform receives the dispute first. That matters because the cost does not stop at the order value. You can also lose the sale, pay added fees, and create cleanup work across teams. Slow or messy handling gets expensive fast.

Start with ownership#

Treat disputes as a cross-team operating issue, not a support queue. In practice, a common failure mode is handoff delay. Risk sees the alert, Ops needs seller context, Finance needs the ledger impact, and Engineering owns the event trail. If nobody owns the deadline, the case can expire before you even decide whether to fight it.

Start with three checks:

- Identify who receives the dispute notice first.

- Identify who decides whether to accept or contest it.

- Identify where the supporting records live today.

If you cannot answer those three questions in one meeting, you do not have a disputes process yet. You have scattered knowledge.

Build for messy reality#

Plan for messy reality from the start. Many platforms do not have one clean payments stack, and multiple processors can force teams to manage disputes across different systems and currencies. That creates a familiar trap: the transaction record is in one tool, seller communications are somewhere else, and payout or ledger data sits with Finance. By the time someone pulls it together, the response window is already tight.

Use that reality to set decision rules now: assign owners, deadlines, and minimum evidence requirements before volume forces the issue. Decide what gets automated, what still needs human review, and where judgment calls belong. Descriptor confusion and seller quality problems do not look the same in the data, so your process has to separate them.

Tailor the process to your marketplace#

Tailor the workflow to your marketplace rules. There is no universal dispute process across marketplaces, processors, or dispute programs. Some platforms pass non-fraud chargeback costs and fees to the relevant merchant, while others may allocate them differently, so your contracts and internal policies need to match the actual payment flow.

One early red flag is a confusing billing descriptor. If customers do not recognize the charge, they are more likely to dispute it, which means prevention and recovery are linked from day one. Read the rest of this guide as an operating blueprint you tailor to your processor rules, seller terms, and evidence requirements, not as a generic policy you copy unchanged.

Set liability boundaries before you optimize disputes#

Before you tune rules or buy software, define dispute responsibility by payment flow and document it in writing. If you run card checkout, Virtual Accounts, and other rails, verify each flow separately instead of assuming one pattern across all of them.

Map the real dispute path#

For each flow, record:

- Who receives the dispute notice first

- Who can submit evidence

- Who books provisional loss or fees in Finance

- Who decides to accept or contest

Use one recent disputed payment per flow to confirm the path from processor alert to ledger entry. Track chargeback rate as (disputed transactions / total transactions) x 100, and make sure owners understand that network measurement windows can differ.

Align policy before tooling#

Align contracts and internal policy before adding automation. Platform terms, seller terms, and pass-through language should match how disputes are actually handled. Tools can be added without replacing your full stack, but they will not fix unclear approval rights or conflicting policy.

Write a one-page responsibility split#

Create a one-page operating split for Risk, Marketplace Ops, Finance, and Engineering with owner, deadline, required inputs, and escalation point. This keeps handoffs clear and gives dispute review a traceable path.

Choose your operating model and ownership map#

Once liability is clear, choose the model you can actually run with clear ownership and an audit trail. Then add tooling to reduce handoff delay. A practical default is hybrid when volume is growing but still controllable.

Compare the model you can staff#

Choose the model your team can actually execute, not the one that looks clean on a slide. The test is simple: can you reliably create cases, collect evidence, message the right party, track deadlines, and log decisions with an audit trail?

| Model | Control | Speed | Internal staffing load | Best fit |

|---|---|---|---|---|

| In-house operations | High | Medium | High | You need tight judgment control and already have aligned Risk, Ops, Finance, and Engineering owners |

| Hybrid with chargeback management software | High | High | Medium | Your queue is still manageable, but manual evidence collection and deadline tracking are starting to slip |

| Outsourced-heavy support | Low to medium | Medium | Low | You need coverage quickly, but can tolerate less direct control over case nuance and internal reporting detail |

In-house keeps context closest but can strain teams as dispute categories demand different evidence and time windows. Outsourced-heavy support lowers internal load but can weaken feedback loops into product, finance, and seller operations. Hybrid usually balances both by automating intake and tracking while keeping decision rights in-house.

Assign stage owners and approvals#

Set one owner per stage, with required inputs and approval rights. Without this, cases get touched by multiple teams and owned by none.

| Stage | Owner | Main responsibility |

|---|---|---|

| Prevention | Risk; Engineering; Product | Risk owns rule decisions for payment and fraud controls; Engineering implements and logs changes; Product signs off when checkout friction changes |

| Response | Risk or Marketplace Ops | Owns the evidence workflow, gathers seller or fulfillment inputs, and decides when a case is submission-ready |

| Reconciliation | Finance; Risk | Finance owns ledger journals, loss booking, fee mapping, and close impact; Risk confirms case outcomes when finance treatment depends on representment results |

Use one recent case from each major dispute type as a checkpoint. Treat dispute type as a workflow driver, not just a label, because different categories need different evidence, timelines, and outcomes.

Match the model to your queue#

If your queue is small but growing, start hybrid. If queues are already large and cross-functional delays are common, tighten owner SLAs and escalation paths first, then expand automation.

The key warning sign is reporting nobody trusts because allocation is unclear. If Finance cannot tie outcomes to ledger treatment, or Risk cannot see why cases were accepted versus contested, more tooling will only scale confusion.

Build the dispute evidence packet before first chargeback#

Build your dispute evidence packet before the first notice arrives. In representment, you get one chance to make your case, and an expired case cannot be won.

Define the default packet#

Set one default packet for your marketplace, then adjust by dispute type instead of reinventing intake each time. A practical house standard is:

- Transaction record

- Fulfillment or shipping proof

- Buyer communication history

- The policy or terms version accepted at checkout or order confirmation

Treat this as your internal template, not a universal network checklist. The point is repeatability: teams start from the same structure, then tailor the case file to the dispute reason and narrative.

Tie each artifact to an immutable source#

Every artifact should trace back to an immutable system record. Transaction evidence should reconcile to ledger journals, and operational evidence should map to webhook or other append-only event history.

Under deadline pressure, mismatched timestamps or finance records weaken your case quickly. Require source references in each file, for example: order ID, payment ID, shipment ID, message thread ID, and journal or event record, so reviewers can verify provenance fast.

Also set notice intake now. Processor integrations can deliver notices faster than mail, so one owner should open and route notices as soon as they arrive.

Push seller document rules upstream#

Define seller evidence requirements before disputes happen. State what sellers must submit, in what format, and by when, so representment is not blocked by missing or unusable inputs.

Prioritize records that preserve identifiers and timing context. If a seller file cannot be tied to an order ID and timestamped event, it should not be primary evidence.

For deeper implementation detail, use dispute evidence workflows for marketplaces.

Add failure-mode checks before the first live case#

Run a preflight checklist and assign owners for common gaps:

- Timestamp inconsistencies across systems

- Delivery evidence that is incomplete for the case narrative

- Buyer communication logs that are partial

- Missing or unreadable seller files

Set fix order and accountability before go-live, then run a dry run from source records only. If the team still depends on ad hoc chasing across inboxes or spreadsheets, tighten the workflow before handling real disputes.

If you want a deeper dive, read Document Management for Accounting Firms: Secure Intake, Retrieval, Retention, and Automation.

Set prevention controls where they reduce friendly fraud fastest#

Once your evidence packet is ready, prioritize prevention controls that stop avoidable disputes before they become chargebacks.

Fix purchase clarity before adding friction#

Start with customer clarity after checkout: statement descriptor, order confirmation language, and easy order or service-status visibility. If buyers cannot quickly match the charge to what they purchased, preventable disputes rise.

Use a simple check in your own flow: a reviewer should be able to confirm what was bought, who charged the card, and current status without digging through support threads.

Add fraud controls selectively#

Apply fraud controls where they target suspicious patterns, not as blanket friction for every buyer. Tools such as A Guide to Stripe Radar for Fraud Protection are most useful when tuned to specific risk signals.

If your processor or network stack supports pre-dispute rules or real-time issuer data sharing, test those paths early. They are designed to deflect disputes before chargebacks and can reduce manual handling overhead.

Use existing risk gates and verify impact by team#

Use the risk and compliance checkpoints you already run in onboarding, activation, or payout workflows, but do not rely on them as a substitute for buyer-facing clarity.

| Team | What to verify |

|---|---|

| Product | Validate conversion and support impact from added friction |

| Ops | Track dispute reasons and pending dispute trends |

| Finance | Confirm net recovery impact, including avoidable dispute and fee reduction |

Define fight or accept rules by loss exposure and proof strength#

Do not treat every chargeback the same. Contest when proof is strong and recovery value is meaningful; accept faster when proof is weak or recovery odds are low.

Score exposure and proof strength#

Score each case on two axes before deciding. First, total exposure: not just the disputed amount, but fee pressure, account risk, and whether loss spills into seller negative-balance handling. Second, proof strength from your dispute evidence workflow, not gut feel alone.

A strong packet means core records are ready without cross-team scrambling: transaction details, fulfillment or service proof, buyer communication, and the policy or terms the buyer accepted. If timestamps conflict, delivery proof is partial, or accepted terms are unclear, treat the case as weak even if it looks suspicious.

| Financial exposure | Evidence strength | Default action | What to check next |

|---|---|---|---|

| High | Strong | Contest | Confirm recovery owner, seller-balance impact, and representment timing |

| High | Weak | Accept or escalate for one manual review | Decide whether reserves or offsets need adjustment |

| Low | Strong | Contest selectively | Prioritize repeat patterns or policy-setting cases |

| Low | Weak | Accept and learn | Feed the reason back into prevention and seller controls |

Keep the table simple if you need to. Consistent use matters more than complexity.

Keep exceptions narrow#

Use exceptions, but keep them tight. A strategic seller can justify one extra manual review if missing proof is likely retrievable quickly, but avoid turning seller importance into a blanket reason to fight weak cases.

Create a repeat-abuse path for friendly fraud signals as well. Repeated buyer patterns or dispute reasons can justify contesting even lower-value cases, but do not assume intent too early, since some chargeback fraud is accidental.

Tie decisions to seller recovery#

Link the dispute decision to reserves, offsets, and seller-balance handling the same day. If you contest, Finance and Marketplace Ops should align on who carries exposure during the dispute. If you accept, make the recovery path explicit: absorb, offset future payouts, or move the seller into reserve or negative-balance handling.

Reconciliation is the control point. Your dispute queue, finance export, and seller-balance records should show the same loss owner and next action. If those rules are still loose, build them alongside Negative Balance Management for Marketplaces: Reserves Offsets and Recovery Playbooks.

Wire the system for auditability and fast retries#

Before you add more automation, make the operation auditable. If you cannot reconstruct who changed a case, when, and from which API call or inbound event, retries will keep creating confusion and Finance will keep finding mismatches later.

Log the full event trail#

Before any pilot, confirm clean catalog data and core event readiness. At minimum, ensure view, add, purchase, and search events are instrumented so you have a complete purchase trail for dispute review.

Then log every dispute state change in one recordkeeping flow tied to your reporting/analytics layer. Include the internal case ID, external processor reference, prior state, new state, actor or service, and timestamp. The checkpoint is replayability: an ops lead should be able to open one case and follow its full history without asking Engineering for raw logs.

Make retries measurable#

Set retry behavior before you increase volume, then test it in one 14-day pilot per use case with a single KPI. At the end of the pilot, make one decision: scale, iterate, switch, or park.

Keep the validation simple: resend the same request or inbound event in test and confirm case history stays coherent instead of branching into conflicting updates. If you skip this, duplicate work and late reconciliation usually show up when volume increases.

Connect case records to finance lineage#

Tie dispute records to finance lineage with stable payment references that appear in both the dispute tooling and finance exports. This gives Ops and Finance a shared thread for reconciliation without manual detective work.

For sensitive tax or identity documents, reference the governed system record rather than copying details into case notes. Close the loop with a weekly ops review of stuck states, timeout breaches, and dispute-versus-finance mismatches, with a clear owner for each issue.

Plan recovery for seller balances and payout risk#

Plan recovery paths before payout volume grows so each dispute is handled consistently instead of becoming ad hoc finance cleanup.

Map disputes to seller balance states#

Assign each chargeback to a seller balance state as soon as the case opens. Chargebacks can affect digital goods, physical goods, and services, and the response strategy can differ by what was sold, so use both product context and reason code in your routing.

Keep one view that shows seller account, disputed amount, reason code, and current recovery state. If cases like Visa 13.3, Mastercard 4853, and AmEx C08 all land in one generic bucket, your policy is likely too coarse for payout risk.

Set reserve and payout-hold rules early#

Define reserve, offset, and payout-hold policy before scaling Payouts. Be explicit about when you net funds, when you delay disbursement while a dispute is active, and when no hold applies, so outcomes do not depend on analyst preference.

A practical failure pattern is paying out in full while the dispute is still active, then trying to recover through collections later. For a deeper playbook on reserve and offset design, see Negative Balance Management for Marketplaces: Reserves Offsets and Recovery Playbooks.

Use risk status as a review input#

Use dispute status and reason-code context as the core release signals, and treat compliance or operational risk status as supporting review input in borderline cases. Before release, confirm the seller record and payment/dispute records still match so the recovery path stays clear.

For adjacent workflow design, see A Guide to Dunning Management for Failed Payments.

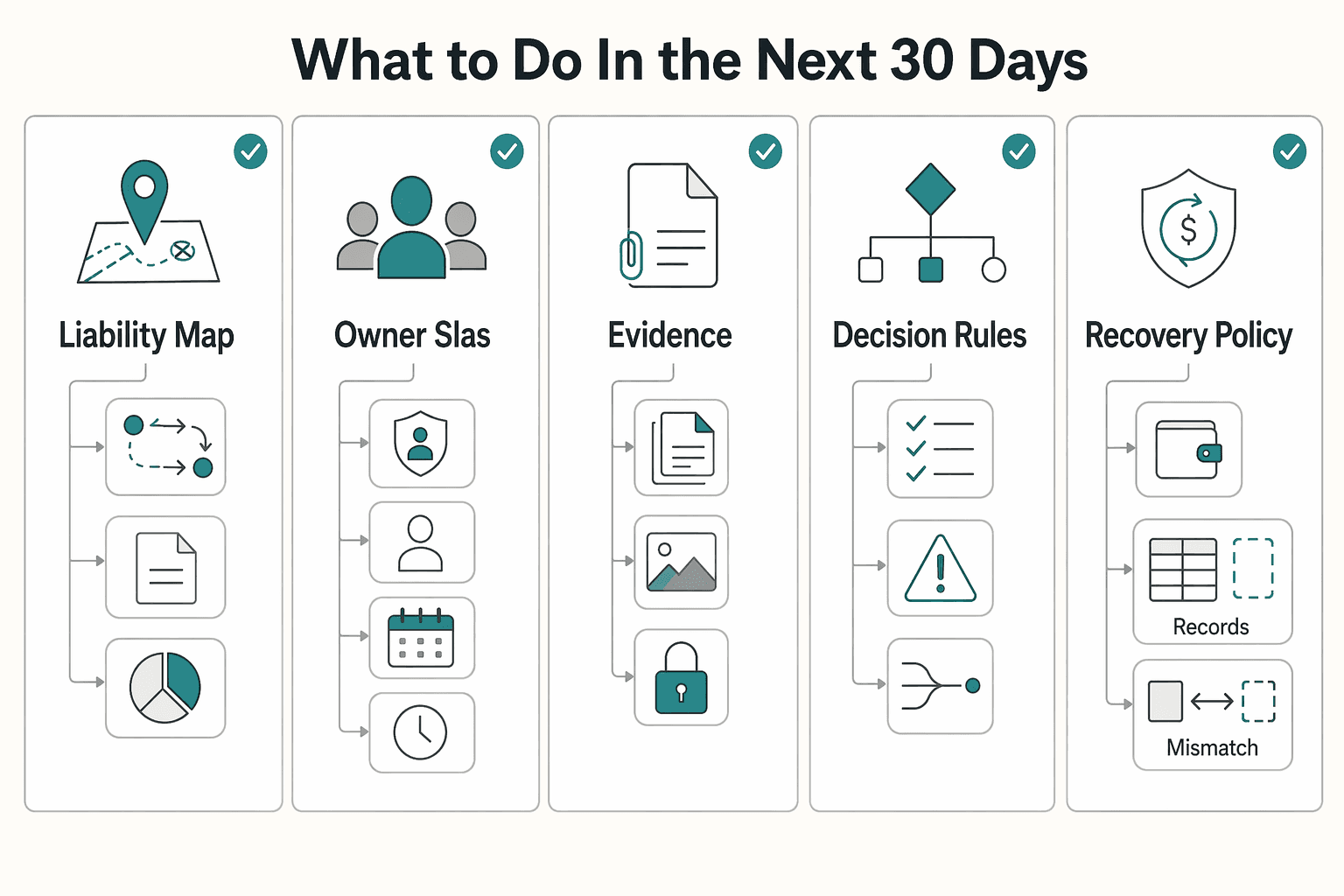

What to do in the next 30 days#

In the next 30 days, focus on ownership, evidence quality, and clean dispute data before adding more tooling. The goal is not a perfect system. It is a minimum system you can run consistently.

| Week | Focus | Main actions |

|---|---|---|

| Week 1 | Confirm liability boundaries and owners | Map where first loss sits by payment flow, what seller pass-through terms allow, and who decides each step across Risk, Ops, Finance, and Engineering; keep it to one page |

| Week 2 | Ship the minimum dispute evidence workflow | Require transaction record, fulfillment or shipping proof, buyer communications, and policy or terms acceptance proof; make each artifact traceable to webhook event history and matching ledger journals; lock a required seller evidence format and handoff path if sellers submit evidence |

| Week 3 | Launch a fight-or-accept decision table | Use evidence strength and recoverable exposure, including reserves and offsets; contest when proof is strong and recovery is realistic; accept early when proof is weak or balances are unrecoverable; log the reason |

| Week 4 | Add auditability checks and review by reason code | Sample recent disputes and confirm each status change appears in webhooks, lands once in the internal case record, and maps to the correct ledger journal; review outcomes by reason code to find operational root causes |

Week 1: Confirm liability boundaries and owners. Map where first loss sits by payment flow, what seller pass-through terms allow, and who decides each step across Risk, Ops, Finance, and Engineering. Keep it to one page. Success check: a live dispute can be assigned immediately, with clear owners for evidence response, seller recovery, ledger reconciliation, and webhook/data issues.

Week 2: Ship the minimum dispute evidence workflow. Require core artifacts on eligible transactions: transaction record, fulfillment or shipping proof, buyer communications, and policy/terms acceptance proof. Make each artifact traceable to webhook event history and matching ledger journals so teams are not reconstructing cases from screenshots. If sellers submit evidence, lock a required format and handoff path. For a deeper build guide, use Dispute Evidence Workflows for Marketplaces: What to Collect Before a Chargeback Happens.

Week 3: Launch a fight-or-accept decision table. Use two inputs: evidence strength and recoverable exposure, including reserves and offsets. Contest when proof is strong and recovery is realistic. Accept early when proof is weak or balances are unrecoverable, and log the reason so downstream teams do not reopen dead-end recovery work.

Week 4: Add auditability checks and review by reason code. Sample recent disputes and confirm each status change appears in webhooks, lands once in your internal case record, and maps to the correct ledger journal. Then review outcomes by reason code to find operational root causes. If "unrecognized transaction" rises, tighten statement-name clarity and post-purchase communication before adding checkout friction.

Copy and paste checklist

- Liability map done

- Owner SLAs set

- Evidence packet live

- Decision rules approved

- Recovery policy active with reserves and offsets named

- Webhooks and ledger journals verified against real cases

Frequently Asked Questions

Who is liable for chargebacks in a marketplace when the platform is the Merchant of Record (MoR)?

Use your processor agreement and seller terms as the deciding documents for liability.

Can marketplaces pass chargeback costs to sellers, and what usually limits that in practice?

Stripe Connect's You handle pricing model is recommended for marketplaces, makes the platform responsible for Stripe processing fees, and allows the platform to charge users; if Stripe bills connected accounts directly, the platform does not incur additional account, payout volume, tax reporting, or per-payout fees.

What evidence should be collected before a chargeback happens to improve representment outcomes?

The grounding sources here do not specify required representment evidence fields or card-network evidence standards. Use your processor’s dispute documentation and program rules to define evidence requirements.

When should a marketplace fight a chargeback versus accept the loss?

Use your own dispute economics, contractual recovery rights, and processor guidance to make that decision.

What does chargeback management software automate, and what still needs human review?

Validate automation scope against your internal workflow and processor requirements.

How do prevention controls like Stripe Radar relate to post-dispute recovery performance?

These sources do not provide quantified Radar-to-recovery performance impact. They do confirm pricing mechanics, including that Managed Payments adds a 3.5% fee per successful transaction (calculated on full transaction amount, including indirect taxes) on top of standard Stripe processing fees.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- academia.edu/145161582/Canonical_Payment_Data_Models_for_...trusted

- oecd.org/content/dam/oecd/en/publications/reports/201...trusted

- one.oecd.org/document/OCDE/GD(96)142/En/pdftrusted

- sec.gov/Archives/edgar/data/1476840/0001628280210209...trusted

- stripe.com/resources/more/ecommerce-chargebacks-101trusted

- stripe.com/connect/pricingtrusted

- uscc.gov/sites/default/files/2025-11/2025_Annual_Repo...trusted

- absoluteweb.com/ai-tools-for-ecommerce-2025-what-to-use-why-...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

A Guide to Stripe Radar for Fraud Protection

**Treat Stripe Radar for fraud as a cashflow protection system, not a vanity fraud score.** Stripe Radar gives you real-time screening with AI and no extra development setup, but outcomes still depend on your rules and operations. Your job is simple: decide when to `Block`, `Review`, or `Allow`, then tie those decisions to fulfillment timing and client communication so fraud protection supports more predictable revenue.

Negative Balance Management for Marketplaces

Marketplace deficits are a payments liability problem, not something you can explain away after launch. They hit finance, ops, and engineering at the same time, because someone still has to absorb the loss, stop more money from leaving, and reconcile the ledger cleanly. This piece treats marketplace negative balance management as an operating discipline: who is liable, how recovery works, and which controls you can actually enforce.

Dispute Evidence Workflows for Marketplaces Before a Chargeback

If you want better dispute outcomes, start before a chargeback exists. Build a dispute evidence workflow that still holds up when the clock is already running. Do not spend another quarter polishing workflows that look helpful but still leave teams scrambling at filing time.