Quick Answer

Build accounting bookkeeping freelancers operations as one continuous process: invoice record, payment proof, posted entry, and monthly review with evidence attached. Use a documented close sequence, keep unresolved items visible, and require traceability from reported balances back to source records. Pick one primary system of record, then test whether your CPA can access what they need and whether bank feeds support direct transaction imports. This turns year-end work into validation, not reconstruction.

Accounting and bookkeeping for freelancers should run all year#

Treat freelancer finance as a year-round money trail, not a tax-season rescue job. For teams handling accounting and bookkeeping for freelancers at scale, the workable model is a controlled process from invoicing through bookkeeping and review, not a set of isolated tasks.

That matters because bookkeeping is not just a pile of receipts. It is the ongoing record of money coming in and going out, including what others owe you and what you owe them. Once you see it that way, year-end work becomes a check on a process you have already been running, not a last-minute reconstruction. The OECD has pushed the same idea from a compliance angle for years: deal with obligations in real time, upfront, and through end-to-end processes instead of isolated tasks.

This guide is not just for solo freelancers. It is also for finance leads, ops owners, and product teams that need cleaner records, clearer handoffs, and fewer surprises at close. If you are the person who has to explain how an invoice, a payment, and a book entry connect, this is your problem set.

The operating shift is straightforward: stop treating invoicing, bookkeeping, and close as separate jobs owned by separate moments. They are connected handoffs. A healthy chain leaves evidence at each step for the next one. In practice, you should be able to connect invoice records, payment proof, and the related posting in your books. If one link is missing, reporting gets weaker and cleanup grows.

A useful design checkpoint comes early: before you rely on a record, can your team verify both the commercial event and the related payment? If the answer depends on inbox searches, spreadsheet stitching, or platform screenshots, you are already carrying cleanup debt. A common failure mode is letting records drift until unpaid invoices or lost receipts only show up at month-end or tax time.

There is an important boundary here. Compliance and tax rules are not universal. Country, business setup, and reporting context all affect what must be collected, validated, and retained. Use this guide to tighten your operating discipline, then validate tax, document, and reporting decisions for your own setup. If you want a deeper dive, read How to Manage Bookkeeping for Your Freelance Business.

Accounting and bookkeeping are different control layers#

Treat bookkeeping and accounting as related but different control layers. Bookkeeping is the structured recording, organizing, and storage of daily transactions. Accounting is the broader layer that interprets that raw data for reporting, planning, and compliance decisions. Even if one person or team handles both, the distinction still matters.

The outputs are different. Bookkeeping owns daily capture and record hygiene: getting invoices, payments, and expense records into the books in an organized way. That includes the raw records behind AR and AP, since receivables are money customers owe you after invoicing, and payables are money you owe vendors or suppliers. Accounting takes over once that data exists: reviewing balances, producing statements and reports, and deciding whether the underlying classifications support the decisions you need to make.

A practical rule helps keep the line clear: if your team cannot explain a balance from the posted entries and source records, bookkeeping is not done yet, no matter which tool you use. The checkpoint is traceability. You should be able to move from a reported balance to the underlying entries, then to the source evidence that shows what happened.

A common failure mode is calling the books done because the totals look plausible while the support is missing or scattered across inboxes and spreadsheets. When that happens, accounting inherits cleanup instead of review. At minimum, keep the source invoice or bill, payment proof, and related book entry together so accounting review does not turn into reconstruction.

For a step-by-step walkthrough, see Accounting and Bookkeeping Platform Payments: How to Pay CPAs and Bookkeepers at Scale.

Map the money lifecycle before you choose tools#

Before you buy or connect anything, map the money path. If you choose tools first, you usually inherit mismatched statuses, duplicate handoffs, and a close process that depends on manual cleanup.

Start with one canonical sequence for your own operation, even if different products touch different parts of it. A practical draft is: invoice creation, payment collection, posting in the books, and reconciliation or review. This is how you make every team agree on where money is, what proof exists, and who owns the next step.

That sequencing should drive tool choice, not the other way around. Focus on integration reality, compliance support, and scalability, not feature lists. The invoicing side matters as well. If your invoicing flow can connect the initial proposal to payment collection, you reduce manual re-entry before the transaction ever reaches the books.

Build a reference table before any integration work#

Keep the first version plain. One table is enough if it shows the source, the record you expect to confirm, and the owner who clears it.

| Step | Source system | Record to confirm | Why it matters | Owner |

|---|---|---|---|---|

| Invoice creation | Invoicing tool | Final invoice record | Starts the bookkeeping trail | Billing or ops |

| Payment collection | Payment system | Payment confirmation | Shows money was received | Finance or ops |

| Book posting | Accounting or bookkeeping system | Posted entry | Puts the transaction into the books | Accounting |

| Reconciliation or review | Bank feed and accounting workflow | Reviewed report or matched record | Helps catch errors before close | Accounting |

What matters most is evidence quality, not table completeness. For each row, test whether a reviewer can move from the status shown in the tool to the record that supports it. If the answer is "we can probably find it in email or a dashboard," that handoff is still weak.

Plan rollout before you automate more#

Automation can reduce manual data entry and reconciliation work, but rollout quality still depends on planning. A successful rollout needs a clear approach to data migration and team training, not just a new subscription.

That is why implementation KPIs matter. Set measures for speed, accuracy, and cost from the start, then review whether the new workflow is actually improving those outcomes. The map is what keeps your tools honest.

Define status meanings and KPIs in writing#

Do not let "paid" mean three different things in three tools. Define what each status means in your workflow, who owns the next step, and what KPI tells you the handoff is improving.

That gives you a clear reference point when systems disagree. It also keeps rollout conversations grounded in operating reality instead of vendor demos.

This pairs well with our guide on Accounting Cycle for Payment Platforms: How to Structure Month-End and Quarter-End Close.

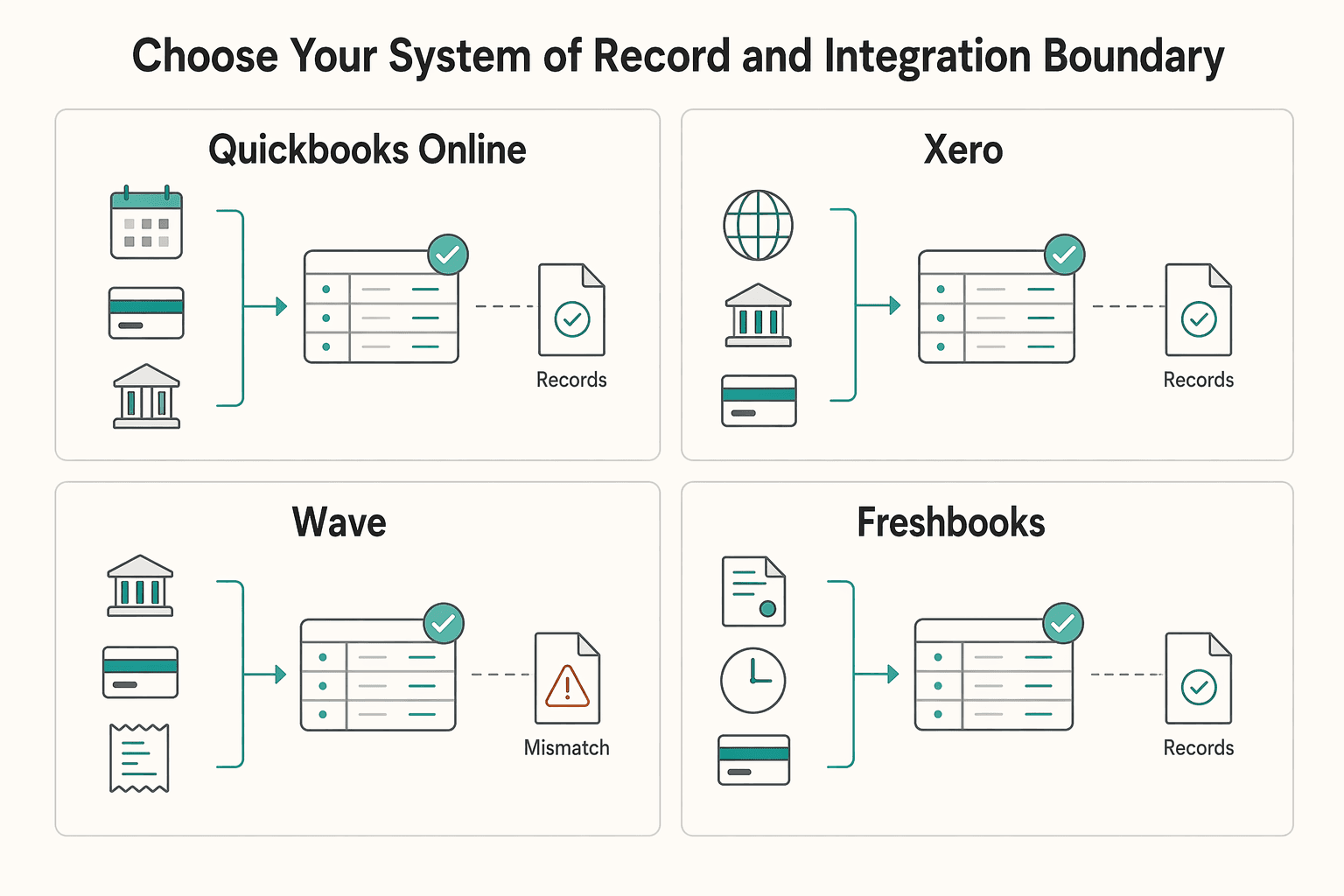

Choose your system of record and integration boundary#

Once the money map is clear, choose one primary bookkeeping system and define what other tools feed into it. If your operation is simple, one accounting tool may be enough for day-to-day bookkeeping and reporting. If you use several tools, be explicit about which one holds the official records and how the others connect to it.

Do not assume QuickBooks is the default answer. In this comparison set, QuickBooks Online is the strongest fit when CPA access matters. Xero stands out when multi-currency is a real operating need. FreshBooks is a strong fit for invoicing-heavy freelancers. Wave can be attractive because it is free, but the same comparison frames it as less scalable.

| Tool | Fit signal from sources | What to verify |

|---|---|---|

| QuickBooks Online | Most CPA-compatible | Confirm your accountant can log in and get what they need |

| Xero | Strong for multi-currency needs | Check that it fits your reporting structure and workflow |

| Wave | Free but less scalable | Make sure it still fits if complexity grows |

| FreshBooks | Strong for invoicing-heavy freelancers | Confirm it covers the review depth you need |

Use a simple control test. Ask the product to prove three things. Can your CPA log in and see what they need? Do bank feed connections import transactions directly? Does the tool fit your business complexity, technical comfort level, and budget? The bank-feed point matters because one CPA-led comparison treats it as non-negotiable.

Migration is where teams often create mismatches. If you switch tools, plan the transition carefully and make sure your accountant can still access the records they need during and after the change. Related: A Guide to QuickBooks Self-Employed for Freelancers.

Run a monthly close that catches payout risk early#

A monthly close is only useful if it runs consistently, with clear evidence and a real review point before you rely on the numbers for decisions. If your team is still discovering basic problems after the period should already be reviewed, you do not have much of a close yet. You have a delayed discovery process.

Month-end close discipline matters here for a simple reason: clear steps and best practices help keep financial data accurate. For freelancer operations, timing matters as well. Delayed invoice payments and work that slips into a later period can distort the picture you are using to judge performance, especially when seasonality changes income timing. If income varies across the year, your close has to separate timing noise from the period view you are relying on.

Set one documented close process and do not improvise it#

Pick a documented month-end process and use it consistently. The exact sequence will vary by business, but the goal stays the same: follow clear steps that keep financial data accurate and make accounting errors easier to spot before they roll into the next period.

Consistency matters because errors are easier to carry forward than to unwind later. A close that changes shape every month makes that problem worse, not better.

Build a minimum evidence pack every cycle#

You do not need a huge binder. You do need the same core records every cycle, stored where accounting and operations can retrieve them without asking around.

That usually means keeping the reports and notes your team actually used to review the month, along with the month-end financial snapshot that reflects the period under review. If you have unresolved items, keep a record of those too so later reviewers are not guessing what was known at the time.

The detail that matters most is cut-off consistency. The records in your close pack should reflect the same period end, not a mix of refreshed files from different days.

Use explicit rules for unresolved items#

Do not leave month-end decisions to "close enough." Write down how unresolved items are tracked, who reviews them, and when they are revisited. That will not eliminate every timing issue, but it makes the close more repeatable and easier to review later.

A good monthly close for freelancer operations is not just about tidy books. It helps keep weakly supported transactions from becoming bigger reporting or payment problems later. Related reading: How to Export Invoice Data to Excel for Accounting and Reporting.

Set compliance and tax gates before money moves#

Before money moves, define the tax and reporting checkpoints that apply to your business. The exact requirements are not universal, so the useful habit is to make the relevant status visible before decisions are finalized.

You do not need to force one global sequence onto every situation. You do need a documented policy for your own program, because requirements vary and scattered records create avoidable confusion.

Treat missing documentation as an open issue, not cleanup later#

If your process depends on tax or reporting documents, track that status clearly. A simple status model can be enough: on file, under review, exception open, or not applicable.

The key is visibility. If documents live in one tool and approvals in another with no shared status field, it becomes much harder to see what is complete and what still needs attention. When the status is unclear, the work stays risky even if the amount itself looks correct.

Keep cross-border reporting artifacts account by account#

Where cross-border reporting obligations apply, keep the reporting artifact with the same discipline you use for monthly matching. For FBAR, the official report is the Report of Foreign Bank and Financial Accounts, filed on FinCEN Form 114. If you may need that filing, preserve the account-level calculation support, not just a final total.

| FBAR point | Detail |

|---|---|

| Official report | Report of Foreign Bank and Financial Accounts filed on FinCEN Form 114 |

| Maximum account value | "A reasonable approximation of the greatest value" during the calendar year |

| Each account | Value each account separately |

| Amounts | Record in U.S. dollars and round up to the next whole dollar |

| Non-U.S. currency accounts | Use the Treasury Financial Management Service rate for the last day of the year |

| Negative determined value | Enter 0 in item 15 |

The practical details matter here. Maximum account value is defined as "a reasonable approximation of the greatest value" during the calendar year. Each account must be valued separately. Amounts should be recorded in U.S. dollars and rounded up to the next whole dollar, so $15,265.25 becomes $15,266. For non-U.S. currency accounts, conversion uses the Treasury Financial Management Service rate for the last day of the year. If the determined value is negative, FinCEN instructs filers to enter 0 in item 15. If you cannot show how those figures were derived, your reporting file is weak even if the final form is submitted correctly.

The broader lesson is the same one from close: incomplete evidence creates downstream cost. The OECD has noted that tax administrations look for approaches that improve compliance while reducing burdens. You get closer to that outcome when required status is visible in the workflow instead of buried in email.

Other tax and reporting obligations vary by jurisdiction and program design. Confirm the exact rule set with qualified local guidance before you operationalize it. You might also find this useful: A Guide to Xero for Freelancers and Small Businesses.

Handle exceptions before they become reconciliation debt#

Exceptions do not stay isolated for long. If you let them sit, they make the accounting cycle harder to follow later. The goal is simple: keep exception work inside the same bookkeeping process that handles the rest of your records, with clear notes and supporting documents attached.

You do not need an elaborate matrix to start. You do need a habit of recording the issue, tying it back to the related transaction, and bringing it back into closure as part of the normal accounting cycle. That is how you stop small discrepancies from becoming larger cleanup work at month-end.

Frequently Asked Questions

What is the difference between bookkeeping and accounting?

The article defines bookkeeping as recording and organizing daily transactions and supporting records. Accounting is the broader layer that reviews those records for reporting, planning, and compliance decisions.

Why map the money lifecycle before choosing tools?

Because tool-first decisions tend to create mismatched statuses, duplicate handoffs, and close processes that depend on manual cleanup. A canonical sequence from invoice to payment, posting, and review keeps ownership and evidence clear.

How do you choose a system of record?

Pick one primary bookkeeping system and define how the other tools feed it. The article suggests testing practical needs such as CPA access, bank-feed imports, multi-currency requirements, and how much business complexity the tool can support.

What makes a monthly close useful?

A useful close runs on a documented schedule with clear evidence, a consistent period cutoff, and explicit treatment of unresolved items. If teams are still discovering basic problems after the review point, the close is functioning as delayed discovery instead.

How should tax and reporting documentation be handled?

Keep the relevant document status visible before decisions are finalized and store account-level support where filings depend on it. For example, the article calls out retaining the calculation support behind FBAR reporting instead of relying only on the final filed form.

Why do exceptions become reconciliation debt?

Because unresolved discrepancies do not stay isolated; they make later matching and review harder. The article recommends recording each issue, tying it to the related transaction, and resolving it inside the normal accounting cycle.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- fincen.gov/system/files/shared/FBAR%20Line%20Item%20Fil...trusted

- fincen.gov/report-foreign-bank-and-financial-accountstrusted

- guides.gaoinnovations.gov/greenbook/2025/principle-12-implement-contro...trusted

- inside.seattlecolleges.edu/public/getdocument.aspxtrusted

- irs.gov/payments/pay-as-you-go-so-you-wont-owe-a-gui...trusted

- irs.gov/businesses/small-businesses-self-employed/wh...trusted

- ncbi.nlm.nih.gov/books/NBK22946trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Freelance Bookkeeping for Faster, Safer Client Payments

Control over cash starts with records you trust. When entries are current, categorized, and easy to trace, you spot risk earlier and make calmer decisions about follow-up, spending, and month close.

A Guide to QuickBooks Self-Employed for Freelancers

**QuickBooks Self-Employed can support basic bookkeeping, but predictable cashflow comes from your payment controls, not invoicing alone.**

A Guide to Xero for Freelancers and Small Businesses

---