Quick Answer

QuickBooks Self-Employed can work for freelancers with simple, stable operations, but it is not enough on its own to guarantee predictable cashflow. The article recommends a risk-first operating system: pair bookkeeping with clear contract terms, structured follow-up, and a pass-or-fail scorecard. Keep it when process fixes close gaps quickly, and upgrade or replace when the same workflow failures repeat.

QuickBooks Self-Employed Review for Freelancers Who Need Predictable Cashflow#

QuickBooks Self-Employed can support basic bookkeeping, but predictable cashflow comes from your payment controls, not invoicing alone.

Invoicing is easy. Getting paid on time, with low dispute risk, is the hard part. In a business-of-one, cashflow reliability is your job, not your software's.

This QuickBooks Self-Employed review is for operators who want a fast, defensible decision instead of a long feature tour. Intuit markets QuickBooks Self-Employed to solo operators, and reviews often focus on basics like expense tracking, invoicing, and mileage logs. That can work when client terms are simple and approvals move fast.

The cracks show up when scope is fuzzy, signoff drags, or follow-up is inconsistent. Software cannot enforce scope, acceptance, or dispute posture for you.

This guide uses one decision framework from start to finish: the Get Paid Reliability Scorecard. Use it to decide whether QuickBooks Self-Employed fits your current stage or whether you need a stronger stack now. The goal is speed and clarity, before a missed payment forces the decision.

One more thing before we get tactical. Public review signals are mixed and not always current. TraderScooter publishes a strong endorsement, while Jamie Trull explicitly argues against recommending it. Some Small Business Computing coverage is materially old, including legacy pricing references, so treat it as historical context, not current buying guidance. Anecdotal creator takes are useful context, but they are not decision-grade coverage on their own.

| Signal source | Useful for | Not enough for |

|---|---|---|

| TraderScooter and Jamie Trull | Spotting practical pros and objections | Making a final tool decision alone |

| Small Business Computing | Historical context | Current pricing or plan assumptions |

| Any single creator review | Real-world context | Complete, current product detail by itself |

Here is the failure mode to watch for: you deliver on time, send the invoice, and still wait because acceptance proof and follow-up steps were never standardized. The tool did not fail. The process did.

By the end, you will have a reusable system for safer terms, cleaner workflows, and fewer payment surprises. If you want a deeper dive, read Value-Based Pricing: A Freelancer's Guide.

Build the Mental Model Before You Pick a Tool#

Treat QuickBooks Self-Employed as a bookkeeping layer, then add contract and payment controls to protect cash flow.

| Control | Defines | Article note |

|---|---|---|

| Statement of Work (SOW) | Scope, timeline, and cost | Set before kickoff |

| NDA | Confidential information for both sides | Confirm signed before work starts |

| Termination | Exit rights when milestones stall | Tie triggers to missed approvals or payment delays |

| Governing Law | Which legal rules apply | Can affect how damages and limitation are analyzed if a dispute escalates |

| Jurisdiction | Where disputes get heard | Reduces forum uncertainty |

Keep this review anchored on payment reliability, not feature hype. QuickBooks Self-Employed covers core solo-operator bookkeeping needs like recording income and expenses, tracking mileage, and preparing Schedule C. It is a lightweight workflow, not an advanced accounting system.

That distinction matters. The tool can organize records and support tax prep, but it does not replace contract terms for scope, acceptance, and dispute handling.

Use the Get Paid Reliability Scorecard to evaluate fit across four pillars, then pick the simplest tool that supports your operating controls.

| Pillar | What to score first | Pass signal |

|---|---|---|

| Invoice execution | Invoice speed, follow-up cadence, payment status visibility | You can track every invoice from send to paid without manual guesswork |

| Risk controls | SOW, NDA, and termination triggers in every client packet | You never start work without signed terms |

| Operational visibility | One place for obligations, due dates, and proof of acceptance | You can explain current risk in minutes |

| Upgrade readiness | Friction points that bookkeeping alone cannot solve | You know exactly when to upgrade or add controls |

Set your legal controls before kickoff. A Statement of Work (SOW) sets scope, timeline, and cost. An NDA protects confidential information for both sides. Termination defines exit rights when milestones stall. Governing Law chooses the legal rules, and Jurisdiction sets where disputes get heard, which reduces forum uncertainty.

Governing law is not cosmetic boilerplate. It can affect how damages and limitation are analyzed if a dispute escalates.

A common scenario: a client approves early drafts in chat, then challenges the final invoice. If your SOW acceptance terms, termination trigger, and governing law language stay clear, you can escalate with structure instead of improvising under stress.

Use this default checklist before any new client, and log it in your workflow notes so follow-ups stay consistent.

- Confirm signed SOW and NDA before work starts.

- Set termination triggers tied to missed approvals or payment delays.

- Align governing law and jurisdiction with your enforcement strategy.

- Record these controls in your workflow notes so follow-ups stay consistent.

For more tooling context, see The Best Expense Tracking Apps for Freelancers.

Is QuickBooks Self-Employed Enough for Your Stage Right Now?#

QuickBooks Self-Employed can fit simple solo operations, but it often stops fitting cleanly as business complexity grows.

Decide by stage fit, not brand familiarity. QuickBooks Self-Employed is positioned for freelancers, independent contractors, and sole proprietors. Reviews commonly frame it as a strong entry point, but one that may not scale as your business grows.

Intuit positions QuickBooks Solopreneur as the successor, and support forum responses indicate QuickBooks Self-Employed is no longer offered to new users. If mobile workflows matter, verify current app access. The QBSE iOS app stopped being available for download starting March 24, 2024.

| Stage | Operational reality | Best-fit direction |

|---|---|---|

| Solo freelancer, simple workload | Low complexity, one-person operation | QuickBooks Self-Employed or Solopreneur can fit |

| Solo but process strain appears | More moving parts and less room for manual workarounds | Stay only if your process remains reliable |

| Growth stage | Your setup is outgrowing an entry-point tool | Move to broader workflows |

Use public opinions as inputs, not verdicts. TraderScooter offers a strong solo-operator perspective. Jamie Trull explicitly warns it is not the best choice for everyone. Both viewpoints help, but neither replaces your own risk profile.

Before you subscribe, run this confidence gate so you validate your real workflow, not a marketing checklist.

- Verify live pricing and plan details directly, since third-party pages can lag.

- Treat older excerpts, including Small Business Computing, as historical context only.

- Run a short live trial with your real invoice flow, follow-up routine, and month-end bookkeeping tasks.

- Check whether your process still works when one client pays late.

If you manage a small roster with simple deliverables, this setup can stay stable. If approvals and payment handoffs keep multiplying, upgrade before cashflow breaks.

Score QuickBooks Self-Employed with the Get Paid Reliability Scorecard#

Use a pass-or-fail scorecard to test payment reliability in your workflow, then decide whether QuickBooks Self-Employed or another QuickBooks setup is the safer fit.

Move from opinion to execution checks. QuickBooks Self-Employed supports invoice, income, and expense tracking, but your contracts and operating discipline still carry the risk. Score the workflow, not the marketing.

| Score area | Pass rule | Fail signal |

|---|---|---|

| Invoice-to-cash reliability | You can track every invoice from sent to paid, with acceptance proof and follow-up steps | You rely on memory, inbox search, or ad hoc reminders |

| Legal defensibility | Every job starts with a signed Statement of Work (SOW) and clear Work for Hire language when ownership matters | Scope or ownership terms appear late, or not at all |

| Dispute posture | Limitation of Liability and Indemnification language match the services you actually deliver | Contract language stays generic and misaligned with delivery risk |

| Edge-case resilience | Your process documents Force Majeure and Assignment of Rights scenarios before conflict starts | You negotiate these terms only after a problem appears |

Use consistent definitions while you score. Statement of Work (SOW) defines scope and project execution details. Work for Hire can determine authorship and ownership under specific conditions. Limitation of Liability caps damages. Indemnification allocates specified loss risk. Force Majeure can excuse obligations after extraordinary events. Assignment of Rights transfers rights and delegates duties.

Example: a client asks to transfer the contract to a partner entity right as a disruption delays delivery. If your assignment and force majeure steps already sit in your client packet, you can keep decisions clear and move faster.

Run the same pass-or-fail test for QuickBooks Self-Employed and your broader QuickBooks option. Keep the tool that supports your process with the fewest manual gaps, then rescore each quarter.

Can It Reduce Late Payments and Risky Clients in Practice?#

It can help reduce late payments and risky client exposure when you run QuickBooks Self-Employed inside a contract-first control flow.

Turn the scorecard into daily execution. QuickBooks Self-Employed can support structured invoice follow-up, including reminders before, on, and after due dates, which reduces manual chasing. That supports steadier cash flow habits. It still will not replace contract controls.

Build a payment control flow#

Tie each invoice to contract proof, not just a due date.

| Step | Action | When it applies |

|---|---|---|

| Invoice milestones | Send invoices against defined milestones in the Statement of Work (SOW) | For defined milestones |

| Acceptance proof | Capture acceptance proof for each milestone before final billing | Before final billing |

| Follow-up sequence | Run a fixed follow-up sequence for overdue invoices | For overdue invoices |

| Termination path | Follow the Termination path already defined in your agreement, where applicable | If milestones or payment obligations fail |

In practice, that means invoicing against defined Statement of Work (SOW) milestones, capturing acceptance proof before final billing, running a fixed overdue follow-up sequence, and using the Termination path only when the agreement already supports it.

Scenario: a client accepts a deliverable, requests extra scope, then pauses payment. If your workflow links invoice, acceptance proof, and termination triggers, you respond with a clear next step instead of a reactive negotiation.

Lock dispute and liability terms before stress hits#

Include both NDA and SOW in each client packet. The NDA protects confidential information, while the SOW defines the actual work requirements and helps reduce scope ambiguity during payment discussions.

Predefine escalation paths inside the contract packet so you are not improvising when payment stalls.

| Contract control | Practical purpose |

|---|---|

| Arbitration or Jurisdiction | Routes disputes to a defined forum instead of improvised escalation |

| Governing Law | Sets which legal rules apply during disputes |

| Limitation of Liability | Sets boundaries on recoverable damages |

| Indemnification | Assigns who covers specific losses tied to service delivery |

Align these terms with the services you actually deliver, not generic template language. Rules vary by market and legal venue, so confirm your standard template with qualified local counsel before you roll it out across all clients.

Set Up a Safe Default Client Onboarding and Payment Checklist#

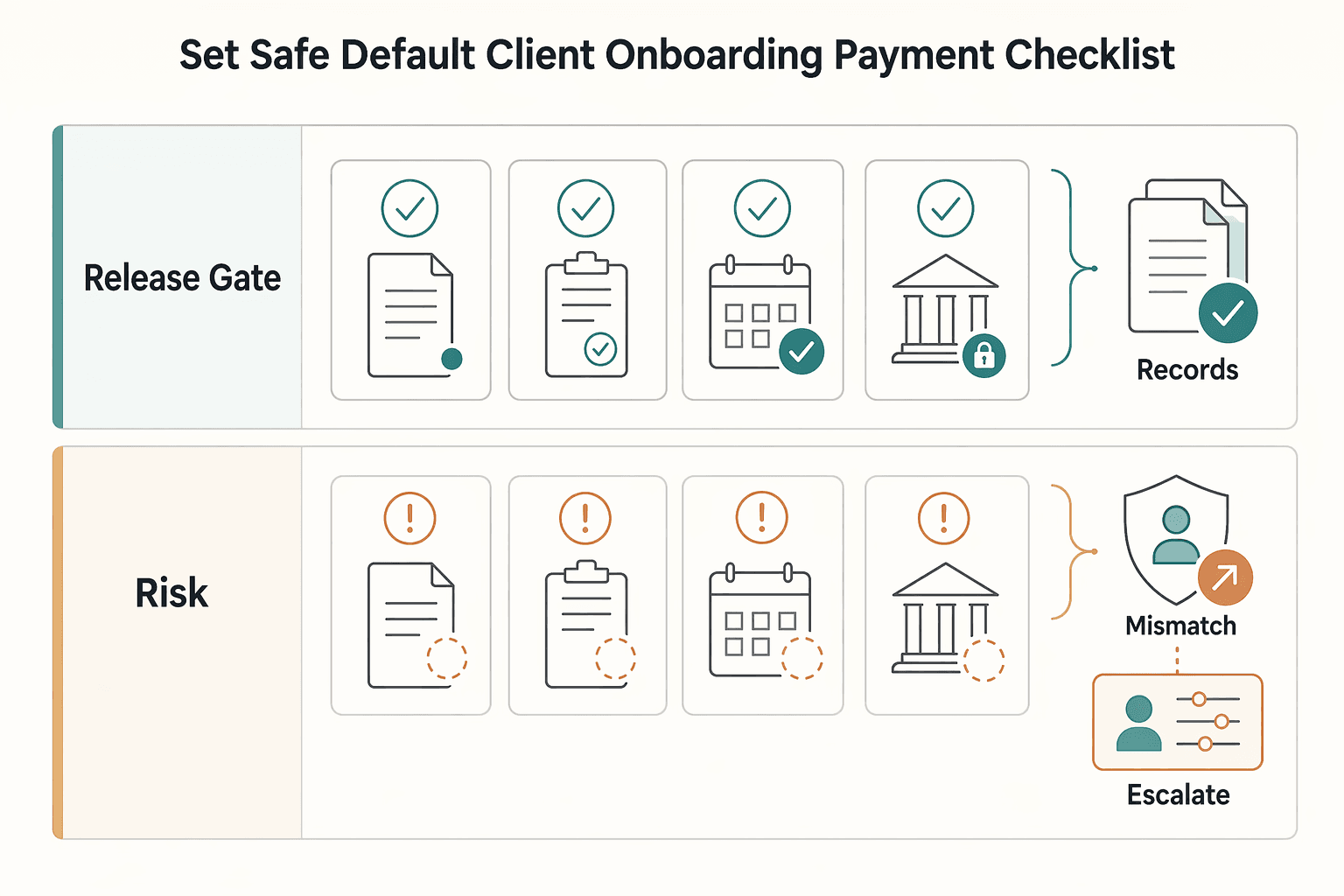

Use a four-gate onboarding checklist before kickoff so every client starts with clear scope, clear contract terms, and a predictable payment path.

You turned invoicing into a control flow. Now hard-code that flow into onboarding so you stop negotiating process details under pressure.

Treat onboarding like a system, not admin work. QuickBooks provides a new-client intake checklist, and QuickBooks Self-Employed profiles help you collect setup details early. Use that structure to keep records cleaner and reduce surprises later.

| Gate | What you verify | Pass condition | If it fails |

|---|---|---|---|

| Pre-work gate | Signed Statement of Work (SOW), signed NDA, agreed Termination triggers | No work starts without all three | Pause kickoff and return redlines |

| Contract consistency gate | Governing Law, Jurisdiction, and Arbitration align with your plan and client location | Dispute route stays clear before conflict starts | Escalate to counsel review |

| Scope and IP gate | Work for Hire and Assignment of Rights match deliverables and payment milestones | Ownership and transfer terms match what you actually sell | Revise scope and milestone language |

| Risk gate | Indemnification and Force Majeure appear and fit project risk | Liability and disruption terms reflect delivery conditions | Replace template clauses with project-specific terms |

Use crisp definitions if you train a team or contractors. Termination ends remaining executory duties while preserving rights tied to prior breach or performance. Assignment of Rights can transfer rights and delegate duties, so you must check both sides of the clause. Work for Hire can shift ownership from the creator to a third party, so match it to what you are delivering.

Scenario: a client changes internal ownership mid-project and asks a new entity to take over approvals. If your onboarding packet already aligns assignment, jurisdiction, and arbitration terms, you can keep momentum and reduce approval-related payment delays.

Close every onboarding with a one-page checklist in your internal record for each client profile. Include milestone owners, follow-up cadence, and clause status. Repeat it on every client. Consistency helps you catch gaps before they turn into billing friction.

If you want a quick next step, try the free invoice generator.

When Should You Keep It, Upgrade It, or Replace It?#

Keep your current setup while it works for a one-person workflow, then upgrade or replace when repeated internal scorecard failures show the tooling is the bottleneck.

Use the same control mindset for platform decisions, and prioritize predictable cashflow over feature collecting.

| Decision path | Trigger you can observe | Action |

|---|---|---|

| Keep your current QuickBooks setup | You run a one-person business, your flow stays stable, and your internal reliability scorecard stays above your own cutoff. | Keep your stack simple and protect bookkeeping quality with weekly expense tracking, invoice follow-up, and contract checks. |

| Upgrade within QuickBooks | Team handoffs grow, approvals slow down, or reconciliation work creates payment lag. QuickBooks Online Essentials supports up to 3 users, and Plus supports up to 5. | Upgrade when collaboration limits create operational drag. If you bill across currencies, confirm you choose a QuickBooks Online tier that supports multicurrency. |

| Replace or augment | Your operating model needs capabilities beyond a lightweight setup. | Evaluate Gruv and peer options against the same scorecard. Approve migration only after you confirm coverage and compliance requirements for your target markets. |

Intuit allows current QuickBooks Self-Employed subscribers to keep their subscription or upgrade to QuickBooks Solopreneur, and it positions Solopreneur for one-person businesses. Use that as a stage check. If quarterly taxes and month-end work now demand tighter controls, you likely outgrew a lightweight setup.

Run a quarterly checkpoint#

- List your last quarter failures by type: late payment, reconciliation miss, scope dispute, or tax-prep friction.

- Mark each failure as a process gap or tooling gap.

- Keep your current setup if process fixes close the gap within one cycle.

- Upgrade or replace if the same tooling gap repeats after you enforce the process fix.

Protect migration execution#

If you add a coordinator and an external bookkeeper in the same quarter, handoffs multiply quickly. Before you switch, run a small migration test, verify reporting continuity, and confirm data history access.

| Migration check | Article note |

|---|---|

| Small migration test | Run a small migration test before you switch |

| Reporting continuity | Verify reporting continuity before you switch |

| Data history access | Confirm data history access before you switch |

| One-way move | If you copy data from Self-Employed to QuickBooks Online, you cannot return to QuickBooks Self-Employed |

Because copying data from Self-Employed to QuickBooks Online is a one-way move, treat it as a one-way decision.

Run the Playbook and Decide with Confidence#

Use one operating playbook every quarter: score risk, lock legal controls, then pick the simplest platform that keeps cashflow reliable.

Turn everything above into a repeatable operating decision. The goal is not to chase features. The goal is to protect payment timing, bookkeeping quality, and decision clarity as your business changes.

| Playbook step | What to check | Decision rule |

|---|---|---|

| Score the current setup | Review your Get Paid Reliability Scorecard across invoice execution, risk controls, visibility, and upgrade readiness. | Keep your current stack if process fixes close gaps within one cycle. |

| Lock contract controls | Confirm every client packet includes a clear Statement of Work (SOW), signed NDA, and explicit dispute terms. | Do not optimize tooling until these controls run consistently. |

| Verify product fit now | Confirm whether you are a current QuickBooks Self-Employed subscriber or a new buyer evaluating available QuickBooks paths, including Solopreneur. | Choose the path that matches your current operating shape, not your hoped-for future shape. |

| Validate market execution | Check payout program coverage, country-specific payment regulation requirements, and current product terms before rollout. | Migrate only after you confirm support for your target market and program. |

Use crisp definitions so your process stays teachable. SOW is the work statement that clarifies the work and objectives. NDA protects defined confidential information. Governing law selects which law applies in a dispute, while jurisdiction defines which court can hear it. Arbitration can be binding or nonbinding, depending on your agreement.

Example: you add an international client while your bookkeeping load increases. If you are already on QuickBooks Self-Employed, keep it for now, tighten your SOW and NDA workflow, and run a market support check before any migration. That sequence helps keep risk low and momentum high.

Take the low-friction next step. Run your scorecard this week, confirm current QuickBooks terms and availability at decision time, and document one keep, one upgrade, and one replace trigger. If cross-border control and audit-ready process discipline now drive your roadmap, evaluate Gruv with the same checklist and confirm market and program coverage where supported before rollout.

Frequently Asked Questions

Is QuickBooks Self-Employed worth it for freelancers focused on cashflow reliability?

For many solo operators, yes. QuickBooks Self-Employed is commonly framed for freelancers and sole proprietors, with income, expense, and tax tracking in one workflow. Cashflow reliability can improve when you pair the software with strict follow-up and clear contract gates.

Who should use QuickBooks Self-Employed and who should move to a different setup?

Use it when you run a one-person business with straightforward client work and stable processes. Move when growth creates recurring friction, because this setup may not scale for growing ventures. If your scorecard keeps flagging misses after process fixes, upgrade your stack instead of forcing more manual work.

What are the biggest pros and cons of QuickBooks Self-Employed?

Review summaries highlight ease of use, automatic mileage tracking, and personalized bookkeeping support as key strengths. They also flag core downsides for growing businesses, including limited scalability and migration constraints. Coverage can conflict, so treat sentiment as directional and validate fit in your own workflow.

Can QuickBooks Self-Employed prevent late payments and risky client terms on its own?

No. Software can support payment follow-up, but it cannot replace your SOW, NDA, and dispute terms. QuickBooks reminder workflows let you schedule nudges up to 90 days before or after a due date, which helps execution, but your operating discipline still controls risk.

What should I verify before subscribing if competitor reviews are incomplete or conflicting?

First, confirm the exact product you can buy today, because some coverage notes a shift from QuickBooks Self-Employed to QuickBooks Solopreneur for new users. Next, run a hands-on validation in the 30-day QuickBooks Online trial and test your real workflow, not sample data. Check invoice reminders, expense tracking quality, tax readiness, and month-end bookkeeping handoff before you commit.

What are the signs my workflow has outgrown QuickBooks Self-Employed?

The clearest sign is growth pressure: your solo workflow no longer keeps up without recurring friction. You should move when your process still depends on expanding manual work after reasonable fixes. In practice, repeated scorecard misses after process cleanup usually signal a tooling gap.

How do I compare QuickBooks Self-Employed alternatives without relying on hype?

Run a structured review with pass-or-fail criteria for invoice execution, risk controls, visibility, and upgrade readiness. Give more weight to review outlets with transparent editorial standards than to star ratings alone. Use one live-trial checklist across options, then compare results side by side.

Watch

Is QuickBooks Self-Employed Enough for Freelancers?

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- irs.gov/businesses/small-businesses-self-employed/es...trusted

- capterra.com/p/212141/QuickBooks-Self-Employed/reviewsexternal

- forbes.com/advisor/business/software/quickbooks-self-em...external

- merchantmaverick.com/reviews/quickbooks-self-employed-reviewexternal

- traderscooter.com/quickbooks-self-employed-reviewexternal

Educational content only. Not legal, tax, or financial advice.

Related Posts

Value-Based Pricing for Freelancers Under Real Payment Risk

Value-based pricing works when you and the client can name the business result before kickoff and agree on how progress will be judged. If that link is weak, use a tighter model first. This is not about defending one pricing philosophy over another. It is about avoiding surprises by keeping pricing, scope, delivery, and payment aligned from day one.

The Best Expense Tracking Apps for Freelancers

Admin drag usually starts small, then eats margin at month-end. Use this as a decision guide, not a popularity roundup: pick one tool quickly, then stick to a weekly routine that keeps records clean.

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.