Quick Answer

Choose a SPAC only when your team can already operate with public-company discipline; otherwise prefer an IPO path or wait. Since the SEC’s Jan. 24, 2024 rule changes, de-SPAC expectations are closer to IPO disclosure standards, including stronger focus on conflicts and dilution. Use concrete readiness checks before committing: clear drafting ownership, support for Form 10-K and Form 10-Q inputs, and a documented plan for time-sensitive Form 8-K events.

What payment platform founders need to decide before choosing a SPAC#

The core decision is readiness, not structure. Choose the route your team can support under public-company disclosure, governance, and reporting pressure. If your operating claims are not backed by evidence today, a Special Purpose Acquisition Company (SPAC) should not be treated as a shortcut.

- Start with route selection, not definitions

A SPAC is typically a shell company when it becomes public, and the combination with an operating company is the de-SPAC transaction. In an Initial Public Offering (IPO), the operating company sells shares to the public, typically to raise capital. For founders, the practical question is which route fits your current operating reality and reporting readiness.

Since SEC rule changes adopted on Jan. 24, 2024, SPAC and IPO disclosure expectations are more closely aligned. Treat that as a planning signal. Underprepared teams should not assume structure alone reduces scrutiny.

- Be explicit about the tradeoff

A SPAC can provide a path into public markets through a listed shell company, often with sponsor-led deal dynamics. But readiness pressure can compress. One advisory source describes companies needing to operate as public companies within three to five months of signing a letter of intent. For payment operators, that means testing whether leadership, controls, and reporting processes can hold up under a tighter transition window.

- Use reporting obligations as the reality check

After going public, companies face ongoing SEC reporting, including Form 10-K and Form 10-Q. Certain current events may also trigger Form 8-K, often within four business days.

Before committing to a SPAC or an IPO, ask the blunt question: can the team support investor-facing disclosures with clear records, clear ownership, and disciplined review now?

- Fix readiness gaps before picking a path

Prioritize evidence and process discipline that can stand up in diligence and public-company reporting. A practical starter set is:

- current board reporting materials used for decisions

- clear owners for disclosure drafting and review

- documented tracking of open risk and remediation items

- support for material operating assumptions, including complex payment flows

- Decision rule for the rest of this guide

Use this article to place your company in one of three buckets: ready for SPAC discussions now, better suited to an IPO path, or not ready for either yet. The rule is simple: if management cannot defend key assumptions under investor and regulator scrutiny, delay the route choice and close readiness gaps first.

If you want a deeper dive, read Freemium vs. Free Trial vs. Reverse Trial: Which Acquisition Model Works for Payment Platforms.

Who this list is for and the selection criteria that matter#

Use this guide when your team could realistically choose a go-public route in the next planning cycle. If your assumptions, controls, and disclosure process are still shifting, pause the SPAC-versus-IPO debate until you can defend them.

- Best fit: teams actively choosing between routes

This section is for teams comparing a SPAC merger with a traditional IPO path. Both routes lead to ongoing public-company reporting, including Form 10-K and Form 10-Q, plus certain Form 8-K filings often due within four business days.

- Poor fit: teams still proving the operating story

This is a decision filter, not a legal exclusion. A SPAC raises IPO capital to acquire an operating business, and the de-SPAC may occur many months, or more than a year, after the SPAC's own IPO. In practice, unresolved reporting and governance gaps can become more visible, not less.

- Score these criteria before valuation talks

Before you get pulled into deal math, score the basics in order: timeline pressure, reporting maturity, sponsor quality, compliance readiness, and the ability to operate under stock-exchange scrutiny. Under the SEC's Jan. 24, 2024 rules, de-SPAC disclosures include enhanced detail on sponsor compensation, conflicts, and dilution, and the target can be a co-registrant responsible for registration-statement disclosures.

A practical check is to confirm clear owners and support for 10-K, 10-Q, and 8-K inputs. Then test whether sponsor discussions are specific about incentives, conflicts, and public-company disclosure responsibilities.

- Readiness check: can you defend the disclosure package?

Treat the future ticker symbol as one disclosure stress test, not a standalone decision rule. If leadership cannot clearly defend the numbers, assumptions, and risk language that would sit behind that public identity and related reporting obligations, defer route selection and close the readiness gaps first.

We covered this in detail in SOC 2 for Payment Platforms: What Your Enterprise Clients Will Ask For.

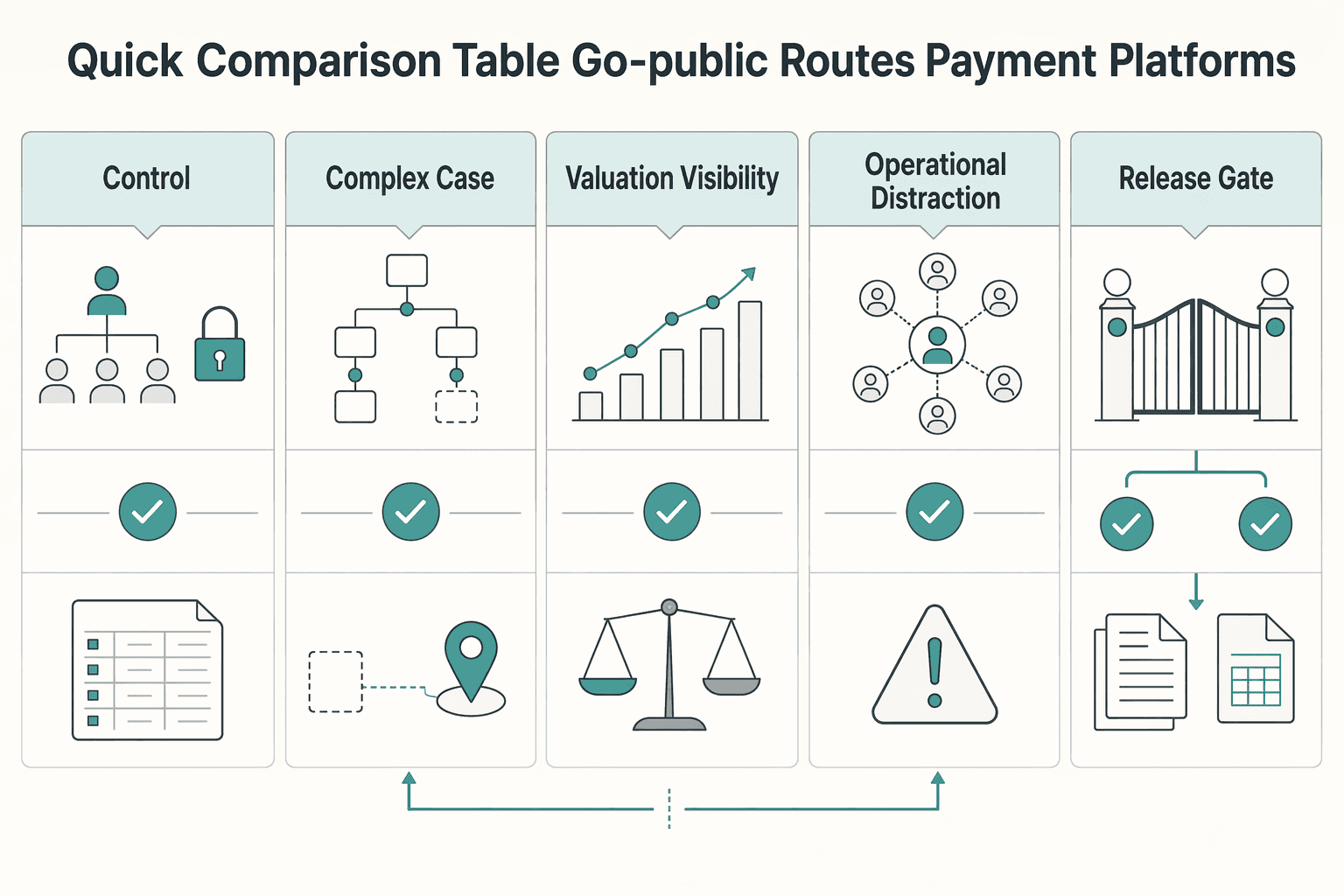

Quick comparison table of go-public routes for payment platforms#

For many payment platforms, the default should be wait and prepare unless you can already operate at public-company reporting quality and absorb listing-period execution pressure.

| Decision factor | SPAC merger | IPO | Wait and prepare |

|---|---|---|---|

| Timeline control | Often shorter than an IPO, but not guaranteed. De-SPAC timing still depends on shareholder approval and redemptions, and SEC materials describe the advantage as only potential. SPACs generally combine with a private company within 2 years. | Generally longer. Underwriter coordination, drafting, review, and offering prep usually extend the timeline. | Highest internal control because you set remediation order and pace, but there is no listing date. |

| Execution complexity | High. SEC final SPAC rules effective July 1, 2024 increased focus on sponsor compensation, conflicts, and dilution disclosures. | High and document-heavy. A private company raises capital by selling newly issued shares to underwriters, and the process typically takes a long time. | Lower securities execution now, but only if delay is used for real remediation. |

| Valuation visibility | Negotiated with the SPAC counterparty, then tested by market reaction and redemptions. | More external price testing through underwriters and investor demand. | No public price signal yet; valuation depends on private-market inputs and internal assumptions. |

| Operational distraction | Compressed. Teams may need to be ready to operate as a public company within three to five months. | Heavy, but spread over a longer prep cycle. | Lowest immediate listing distraction if leadership stops running half-prep for an unready route. |

| Compliance-gated payouts | Risk rises if key controls still depend on manual checks or unresolved AML/CFT and sanctions reviews. | More prep time helps, but scrutiny still exposes weak compliance governance. | Best fit when AML/CFT or sanctions escalation processes are still inconsistent. |

| Cross-border corridor risk | High when corridor documentation is thin. Cross-border payments depend on cross-border data flows and overlapping rules for collecting, storing, and managing data. | Still material, with more runway to map corridor by corridor data, AML/CFT, and sanctions dependencies. | Preferred when expansion is outpacing regulatory evidence or the country data map is incomplete. |

| Reconciliation burden | Can be hard to compress if close and reporting controls are not yet repeatable. | Heavy, but the longer window can be used to harden close, audit support, and exception handling. | Use delay to prove repeatable close quality and evidence retention before listing. |

| Leadership bandwidth during the trading period | Scrutiny can start while the same team is still finishing readiness work. | Still demanding, but leadership is more likely to enter trading after fuller preparation. | No trading-period pressure yet, so leadership can protect service quality and incident response. |

| Failure mode | High redemptions or unresolved sponsor conflict and dilution issues leave you public without enough operating room. | Underprepared public-company controls create repeated delay, rework, and credibility loss. | Delayed expansion from premature listing attempts, or endless prep without owners, dates, and evidence. |

| Route call | Commit with conditions | Commit now | Do not commit yet |

The table makes one point: faster access does not erase readiness work. A SPAC is a shell company that goes public first and then merges with an operating company, so it can improve speed but does not remove disclosure or reporting requirements. The deal still depends on shareholder approval and redemptions, and disclosure demands tightened under the SEC rule changes effective July 1, 2024.

If you are evaluating this route, sponsor diligence is a gating check, not a soft check. You need clear explanations of sponsor compensation, conflicts of interest, and dilution. For NYSE-listed vehicles, verify trust mechanics. Section 102.06 requires a SPAC to keep 90% of gross IPO proceeds in trust until the business combination closes.

An IPO gives you broader market price discovery, but the tradeoff is cost and duration, including high transaction costs such as underwriter fees. For payment operators, that longer timeline can be useful when reporting controls and close processes still need hardening.

Also remember that both SPAC and IPO pathways commonly involve 180-day lock-ups. A listing can change access to public markets, but it does not remove readiness work.

Related: Intercompany Payments: How Multi-Entity Platforms Manage Cross-Border Internal Transfers.

Choose a SPAC merger when speed and sponsor fit beat valuation precision#

Choose a SPAC merger when faster access to public markets matters to your operating plan and sponsor alignment is clear. The route can be quicker than an IPO, but that advantage fades fast if sponsor economics, dilution, and readiness are not clear up front.

- Faster access through a listed shell company

A de-SPAC takes a private company public by merging with a listed shell company. Commonly cited timing is 3-6 months for a SPAC merger versus 12-18 months for an IPO, but those are averages, not guarantees. Use this route when earlier listing timing supports your sequencing. If you need more time before becoming public, the speed tradeoff may not be worth it.

- Execution benefits depend on sponsor alignment

A SPAC path can move quickly, but only if sponsor incentives fit your post-close reality. Sponsor selection is a core challenge, and sponsor economics often include a 20 percent promote that can affect dilution and ownership outcomes. Review those terms directly and pressure-test how they affect decision-making after listing.

- Disclosure pressure is now closer to IPO expectations

The old idea that a SPAC is a lighter disclosure route no longer holds up well. SEC final SPAC rules adopted on Jan. 24, 2024 increased emphasis on disclosures around conflicts of interest, sponsor compensation, and dilution, and the SEC has said SPAC rules are now substantially aligned with IPO expectations. If your team still struggles to explain those points in plain language, sponsor fit is not ready.

- Treat speed as useful only when readiness is real

SPAC timelines can compress execution. Companies may need to operate as public companies within three to five months of signing a letter of intent. That makes the structure strongest for teams already working with disciplined controls and evidence-backed reporting, not teams still trying to fix basic readiness gaps.

This pairs well with our guide on Tipping and Gratuity Features on Gig Platforms: Payment and Tax Implications.

Choose a traditional IPO when governance strength and market signaling matter most#

Choose a traditional IPO when your team is ready to operate as a public company under ongoing SEC and exchange requirements. Do not choose it just because it feels more familiar.

- Best fit: mature controls and reporting discipline

An IPO is strongest when you can sustain Exchange Act reporting after listing. That includes ongoing Form 10-K and Form 10-Q filings, plus CEO/CFO certifications as a recurring operating duty.

- Why teams choose it: established registration and review path

An Initial Public Offering (IPO) requires SEC registration before shares are sold, and SEC staff review commonly leads to comment rounds and disclosure revisions. One practitioner source summarizes a typical first SEC comment cycle at 27 calendar days. For some boards and investors, that process can read as a stronger governance signal, but it is not a universal outcome.

- Main tradeoff: heavier prep and market-timing exposure

Traditional IPO preparation is often a longer build phase. Practitioner guidance describes 12 to 18 months before filing for financial-statement readiness, and in some cases two years or more to build public-company processes. IPOs also remain exposed to late-stage market volatility during roadshow and book-building.

- Concrete use case: operator with documented readiness

This route fits an operating company whose leadership prioritizes a conventional offering path over a potentially faster de-SPAC timeline. For NYSE listings, readiness includes governance transition milestones such as a majority-independent board within one year of listing and a majority-independent audit committee within 90 days of the effective registration statement. Stable revenue alone is not enough. Governance and reporting evidence still need to be in place.

Delay both options when core controls are not ready#

If evidence for core controls is weak, delay both paths. Do not force a SPAC merger or an IPO just to preserve a listing narrative.

Hard stop 1#

Under 17 CFR 229.308, management must provide an annual report on internal control over financial reporting (ICFR), assess whether ICFR is effective at fiscal year end, and disclose any material weakness. Management also cannot conclude ICFR is effective if one or more material weaknesses exist.

That makes control evidence a gating issue, not a polish item. If control ownership is unclear or key controls are still unstable, treat that as a readiness gap and fix it before choosing a listing path.

Hard stop 2#

A SPAC route does not remove disclosure readiness requirements. On Jan. 24, 2024, the SEC said SPAC IPOs and de-SPAC transactions can take private companies public. It described these transactions as complex and adopted rules that increase disclosure on conflicts of interest, sponsor compensation, and dilution. The rules also align de-SPAC disclosure and legal liability more closely with IPO expectations.

If your team expects to defer difficult disclosure work through a de-SPAC route, plan for the opposite. Disclosure and reporting obligations still apply.

What a useful delay should produce#

Delay only helps if it closes the gaps that are blocking readiness. Investor.gov's Aug. 21, 2024 bulletin says a company considering an IPO should have resources and structures for both the IPO process and subsequent SEC reporting requirements. Use the delay to answer, clearly and with evidence:

- Who owns each control that supports financial reporting and disclosure?

- Can management support an ICFR effectiveness assessment with documented evidence?

- Is escalation clear enough that disclosure decisions are not improvised when issues appear?

Done well, a delay preserves the option to pursue either route later with stronger readiness. The tradeoff is a later timeline. If evidence quality is weak, wait and prepare.

Build the evidence pack before committing to any route#

Once controls are no longer the hard stop, evidence quality is the next gate. Do not commit to a SPAC or an IPO until leadership can defend a complete pack under diligence, investor questions, and regulator-style scrutiny.

| Artifact | Includes | Why it matters |

|---|---|---|

| Economics tied to acquisition target assumptions | Scenario analysis showing how outcomes change when volume mix, pricing, or rollout timing shifts | SEC final rules increased de-SPAC projection disclosure, including the material bases and assumptions behind projections |

| Risk register | Issue, why it matters, owner, what closes it, and whether it can affect disclosure, timing, or valuation | For a SPAC path, include sponsor diligence, conflicts of interest, sponsor compensation, and dilution |

| Board decision log | What the board reviewed, what assumptions it challenged, what alternatives it considered, and why it moved toward one path | Final SEC rules require disclosure on whether the transaction is advisable and in the best interests of the SPAC and its shareholders |

| Capital structure clarity | Trust proceeds, dilution sensitivity, and redemption cases before a go decision | SPAC IPO proceeds are held in a trust account, and shareholders must have the opportunity to redeem around business-combination approval |

1. Economics tied to acquisition target assumptions#

Start with the economics that matter most to acquisition target assumptions and public-market projections (for some businesses, this may include corridor-level views). If your scenario analysis cannot show how outcomes change when volume mix, pricing, or rollout timing shifts, the forecast is not ready.

This is now a stricter standard. The SEC's January 24, 2024 final rules increased de-SPAC projection disclosure, including the material bases and assumptions behind projections. If leadership cannot explain forecast movement driver by driver, keep it out of decision materials.

2. A risk register with named owners and remediation actions#

Use a listing-readiness risk register with explicit ownership and closure evidence, not a generic risk list. Each item should state the issue, why it matters, who owns remediation, what closes it, and whether it can affect disclosure, timing, or valuation.

For a SPAC path, include sponsor diligence in the same register. Disclosure now puts direct attention on conflicts of interest, sponsor compensation, and dilution, so document sponsor incentives, decision rights, post-close involvement, and any divergence from your interests.

3. A board decision log that survives hindsight#

Keep a dated internal board decision log before you commit to a route. Record what the board reviewed, what assumptions it challenged, what alternatives it considered, and why it moved toward one path.

That discipline matters because final SEC rules require disclosure on whether the transaction is advisable and in the best interests of the SPAC and its shareholders. In some filings, the target can be a co-registrant responsible for disclosures. If this record is missing, drafting and defense get harder later.

4. Capital structure clarity before discussing proceeds#

Define capital structure mechanics up front. Be explicit that SPAC IPO proceeds are held in a trust account for a future acquisition. Public investors often hold SPAC units that traditionally combine common stock with fractional warrant exposure.

Model use of trust proceeds, dilution sensitivity, and redemption cases before a go decision. PwC describes sponsor founder shares as about 20% of SPAC capitalization and public shareholders as roughly 80% through IPO units. Nasdaq notes shareholders must have the opportunity to redeem around business-combination approval. If the case only works under low redemptions or ignored dilution, treat that as a no-go signal.

Final checkpoint: pressure-test the full pack before committing. If leadership cannot defend each artifact clearly, wait. For a deeper breakdown, read Webhook Payment Automation for Platforms: Production-Safe Vendor Criteria. Before you commit, pressure-test whether payout controls, status visibility, and audit trails are decision-grade by reviewing Gruv Payouts.

Sequence execution so listing work does not break payment operations#

Once you know which route could work, execution order matters. Run the process in phases: protect production reliability, lock governance cadence early, then advance SPAC or IPO workstreams in parallel with explicit stop/go rules.

| Phase | Focus | Checkpoint |

|---|---|---|

| Protect core money movement | Keep payout timeliness, reconciliation, chargeback handling, and support backlogs stable during diligence | Set two or three non-negotiable production KPIs, define weekly thresholds, and pause noncritical listing tasks if incident volume, settlement exceptions, or unresolved ledger breaks cross the agreed line |

| Lock governance cadence early | Operate the board calendar, committee charters, disclosure review cadence, and named owners before merger or filing readiness | Nasdaq paths must meet Rule 5600 qualitative governance requirements; Form 10-Q is due in 40 or 45 days, and Form 10-K is due in 60, 75, or 90 days depending on filer status |

| Map decision gates to disclosure milestones | Set sign-off owners for pre-announcement diligence, merger or filing readiness, and the first two quarters as a public company | SEC rules adopted on January 24, 2024 increased de-SPAC disclosure requirements; certain Form 8-K events carry a four-business-day timeline; NYSE market-hours material news requires telephone notice at least ten minutes before release |

1. Protect core money movement before the transaction calendar takes over#

If payout timeliness, reconciliation, chargeback handling, or support backlogs are already unstable, treat that as a sequencing warning as you plan pre-announcement diligence. A financing event does not remove operating risk, and scrutiny can rise as you approach public markets.

Set two or three non-negotiable production KPIs, define weekly thresholds, and tie breaches to escalation. Document one clear rule: if incident volume, settlement exceptions, or unresolved ledger breaks cross the agreed line, pause noncritical listing tasks and return capacity to operating teams.

Watch for staffing drift while diligence and drafting expand. If you cannot show a stable control log, incident trend, and remediation owner before pre-announcement diligence, treat readiness as incomplete.

2. Lock governance cadence early because the deadlines arrive fast#

A future public company needs governance rhythm before it needs a ticker. For Nasdaq paths, listing applicants must meet the Rule 5600 qualitative governance requirements, including board, audit committee, and executive compensation oversight requirements.

Post-listing reporting windows are tight. Form 10-Q is due in 40 days after quarter-end for large accelerated and accelerated filers, or 45 days for other registrants. Form 10-K is due in 60, 75, or 90 days depending on filer status, and annual reports must include management's report on internal control over financial reporting.

Before merger or filing readiness, the board calendar, committee charters, disclosure review cadence, and named owners should already be operating, not assembled late.

3. Map decision gates to disclosure milestones and early trading pressure#

Set three gates with named sign-off owners: pre-announcement diligence, merger or filing readiness, and the first two quarters as a public company. For SPAC routes, include sponsor incentive review at the diligence gate.

Anchor those gates to current disclosure obligations. SEC rules adopted on January 24, 2024 increased de-SPAC disclosure requirements around sponsor compensation, conflicts, dilution, and whether the transaction is advisable and in security holders' best interests. The rules also require a minimum dissemination period for security-holder communication materials in de-SPAC transactions, so planning should not assume instant turnaround.

Set failure containment before early trading starts. On NYSE, market-hours material news requires exchange notice by telephone at least ten minutes prior to release, and trading may be halted temporarily. Separate from exchange handling, certain Form 8-K triggering events carry a four-business-day filing timeline in SEC guidance, so materiality decisions, drafting, approvals, and incident escalation ownership should be explicit before you list.

For a step-by-step walkthrough, see How Payment Platforms Really Price FX Markup and Exchange Rate Spread.

Red flags that should pause a SPAC path immediately#

If you cannot document and defend these points with named owners, draft disclosures, and a credible downside case, pause the SPAC path.

| Red flag | Verify | Trigger |

|---|---|---|

| Sponsor incentives you cannot defend | Written sponsor economics and conflict/dilution handling | De-SPAC disclosures must cover sponsor compensation, conflicts of interest, and dilution |

| Trust-account assumptions fail document review | Trust or escrow terms and redemption rights in the IPO prospectus and constitutive documents | Under the NYSE framework, a SPAC must keep 90% of gross IPO proceeds in trust, and the business combination must be at least 80% of trust-account value |

| Listed shell company does not fit the operating company | A target rationale that clearly supports the operating strategy | Investor guidance notes a SPAC may identify an industry focus but is not obligated to pursue a target in that industry |

| Story only works in the best case | Why this SPAC merger is better than an IPO now, plus a downside case | The case has to survive projection-assumption disclosure and a 20-calendar-day minimum dissemination period for certain de-SPAC materials |

- Sponsor incentives you cannot defend

Weak sponsor alignment is a disclosure risk, not a minor concern. Since the SEC's January 24, 2024 rule adoption, de-SPAC disclosures must cover sponsor compensation, conflicts of interest, and dilution. If you cannot show written sponsor economics and conflict/dilution handling, stop and fix that first. Also pressure-test incentives: if no acquisition closes and the SPAC liquidates, sponsor promote upside can be forfeited.

- Trust-account assumptions that fail document review

If your cash model depends on trust funds being freely available, pause. Confirm trust or escrow terms and redemption rights in the IPO prospectus and constitutive documents. Under the NYSE framework, a SPAC must keep 90% of gross IPO proceeds in trust, and the business combination must be at least 80% of trust-account value.

- A listed shell company that does not fit your operating company

Do not assume fit based on a broad industry label. Investor guidance notes a SPAC may identify an industry focus but is not obligated to pursue a target in that industry. If the target rationale is vague or does not clearly support your operating strategy, treat that mismatch as a pause signal.

- A story that only works in the best case

If leadership cannot clearly explain why this SPAC merger is better than an IPO for this business now, pause. The case must hold up under board-level scrutiny, including whether the transaction is advisable and in shareholders' best interests. It also has to survive explicit projection-assumption disclosure and a 20-calendar-day minimum dissemination period for certain de-SPAC materials.

What current SPAC search results miss for payment operators#

Most current Special Purpose Acquisition Company (SPAC) search results help with definitions. They usually do not tell you whether a SPAC merger is a better path than an Initial Public Offering (IPO) for your payment business.

- Definition first, operator decision criteria second

Search results usually explain the structure: a SPAC is typically a shell company, often described as a blank check company, and IPO proceeds are generally held in a trust or escrow account. SEC and investor-facing materials also emphasize disclosure and investor protection, including the January 24, 2024 rule adoption. The missing piece is practical. Knowing the structure does not tell you whether your team can handle post-close reporting, dilution scrutiny, and execution pressure.

- Payment risk sits on a separate layer

Generic SPAC explainers often do not map decisions to payment-channel realities. For payment operators, controls need to match the channels, products, and services you actually run, not just the listing mechanics. If you cannot clearly show your channel-level operational risks and controls, structure education alone is not a go-public decision.

- You still need your own evidence pack

Advisory coverage is mixed. Some sources frame SPACs as offering valuation certainty and clearer dilution expectations at the start, while others warn of heavier accounting and reporting demands than an IPO. So you still need operator-owned artifacts before deciding: draft disclosures, sponsor diligence, remediation ownership, and a board-ready downside case. Also confirm timing constraints in the shell company's governing documents, which may be set at examples like 24 months in some structures.

- Benchmarks exist, but mostly at sector level

Public SPAC dashboards provide context, such as one 2026 snapshot reporting 60 IPOs, $12,725.1 million in gross proceeds, and a $212.1 million average IPO size. That is market backdrop, not payment-platform readiness. Single-company payment merger news may show that a listing happened, but it does not validate your controls or operating capacity.

You might also find this useful: Real-Time Payment Use Cases for Gig Platforms: When Instant Actually Matters.

The practical takeaway for founders deciding now#

Choose the path your team can support immediately as a public company, not the path with the best story. Since the SEC's January 24, 2024 SPAC rule changes aligned SPAC disclosures more closely with IPO protections, this is a readiness decision, not a shortcut decision.

Choose a SPAC merger when sponsor fit is strong and disclosure readiness is strong#

A SPAC is most viable when your team can defend the deal economics and disclosure package under investor scrutiny. The practical advantage is earlier negotiation of valuation and expected dilution, while IPO pricing is set later through market-based price discovery and can move with market conditions.

Treat speed claims carefully. Source material notes that teams may need to operate as a public company within three to five months of signing a letter of intent. SEC-focused disclosures also include sponsor compensation, conflicts, and dilution. A sponsor's timeline is not proof of your readiness, even if SPACs typically have 18 to 24 months to complete an acquisition.

Choose a traditional IPO when governance strength is your edge#

A traditional IPO is cleaner when your governance and reporting discipline are already strong. If your board, audit committee, and reporting controls are operating at public-company standard now, late-stage pricing uncertainty may be a manageable tradeoff.

Nasdaq qualitative governance requirements include board and audit-committee rules, and Exchange Act annual reporting includes management reporting on internal control over financial reporting. If those are already embedded in how you run the business, the IPO route can be the better fit.

Delay both routes when core readiness is still unresolved#

If sponsor fit is weak and governance execution is not durable, wait and close the gaps first. Forcing either route before your team can consistently support disclosures, controls, and public-company reporting usually turns timeline pressure into execution risk.

The rule is straightforward: a SPAC can work when sponsor alignment and disclosure readiness are both strong; an IPO can be cleaner when governance depth is your strength; if neither is true, delay. Related reading: Continuous KYC Monitoring for Payment Platforms Beyond One-Time Checks. If you want to map timing decisions to real compliance gates and cross-border money movement constraints, talk with Gruv.

Frequently Asked Questions

What is a SPAC in one sentence for payment platform founders?

A Special Purpose Acquisition Company (SPAC) is a company formed for an acquisition-focused public listing transaction that later combines with a private operating company. For payment founders, the practical point is that the shell is public first, and your business becomes public through that combination rather than through your own IPO at the start.

How does a SPAC take an operating company public in practice?

A SPAC raises money in its own IPO, and substantially all offering proceeds are generally placed in a trust or escrow account while it looks for a target. The de-SPAC transaction is the business combination between that public shell and your private company, which is what moves the operating company into public trading status. Before you sign, verify sponsor diligence, expected dilution, and whether your finance and compliance teams can operate as a public company within three to five months of a letter of intent.

What is the core difference between a SPAC merger and a traditional IPO?

In an IPO, the private company itself issues new shares and lists with underwriters. In a SPAC deal, a listed shell is already public, and your company reaches public markets by combining with it. Since the SEC’s January 24, 2024 rule adoption, the decision is not just route or speed, but also disclosure standards around conflicts, sponsor compensation, and dilution.

What happens if a SPAC does not complete an acquisition in time?

A documented outcome is liquidation, with IPO proceeds held in the trust account returned to public shareholders. Do not assume one universal deadline like 18, 24, or 36 months. Deadline terms can vary, so read the shell’s actual timeline before treating it as execution certainty.

Why would a payment platform choose a SPAC route instead of a traditional IPO?

A SPAC can be an alternative path to public markets, and some sources frame it as offering earlier visibility into valuation and expected ownership dilution at the start. Some sources also describe average timing around 3 to 6 months for a SPAC merger versus 12 to 18 months for an IPO. Review sponsor economics closely, because sources also cite roughly 20% common equity plus 3% to 5% of IPO proceeds for sponsors.

Do current search results provide payment-platform-specific SPAC benchmarks?

No, not in a form you should rely on for a go-public decision. Most surfaced results are broad SPAC explainers and sector-level de-SPAC statistics, which help with structure and market context. Treat them as background, not operator evidence for payment-platform execution.

What information is still missing before a founder can make a high-confidence go-public decision?

You still need an operator-owned evidence pack: draft investor-facing disclosures, sponsor diligence notes, corridor-level economics, a risk register, dilution sensitivities, remediation owners, and a board-ready downside case. For payment businesses, understanding SPAC structure is only part of the decision. You also need supportable claims about markets, compliance gates, and reporting readiness under public-company scrutiny. If those points are not documented with clear owners, wait before choosing either route.

Try a related tool

Ethan covers payment processing, merchant accounts, and dispute-proof workflows that protect revenue without creating compliance risk.

Sources

- ecfr.gov/current/title-17/chapter-II/part-229/subpart...trusted

- federalregister.gov/documents/2024/07/15/2024-15411/self-regulat...trusted

- investor.gov/introduction-investing/general-resources/new...trusted

- investor.gov/introduction-investing/investing-basics/glos...trusted

- sec.gov/spotlight/sbcfac/comparison-chart-for-differ...trusted

- sec.gov/newsroom/speeches-statements/spacs-ipos-liab...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: