Quick Answer

Verify the bank path first, then select the M-Pesa lane with written operating evidence. Here, BoT and IFEM materials are treated as boundary context, not a contractor payout procedure, so teams should not scope builds from policy text alone. Use current M-Pesa Limited lane terms, document who owns USD/TZS conversion and settlement exceptions, and require a pilot batch where payout IDs, provider references, and ledger outcomes reconcile cleanly before broader release.

Where M-Pesa Fits in Tanzania Contractor Payouts#

Tanzania is worth evaluating for contractor payouts, but the decision is not about market interest alone. It comes down to whether your model can operate inside Bank of Tanzania boundaries and still deliver a payout experience that finance, compliance, and contractor support can defend.

Step 1 Start from what is confirmed#

Start narrower than many teams expect. Bank of Tanzania reporting covers mobile payments and cross-border payment and remittance, and M-Pesa documentation includes business account definitions. In the M-Pesa terms issued by M-Pesa Limited, a Business Collection or Disbursement Account is defined as an M-Pesa account held by a third party for collecting or disbursing e-money. That is useful context, but it is not a complete operating guide for contractor payouts.

The same caution applies to policy material. A UNCDF diagnostic on Tanzania is explicitly focused on remittance policy and regulation, not contractor payouts, and it states that its evidence was collected between March 2024 and June 2024. So you have recent signals about the payment environment, but not a basis for skipping product, legal, and partner validation.

Step 2 Separate decision inputs from assumptions#

FX and policy documents can create false confidence if you treat them as ready-made payout procedures. Use them as evidence about market mechanics and controls, not as a complete procedure for paying freelance talent into a wallet. If your team jumps from "there is an FX process" to "we can fund and settle contractor payouts cleanly," that assumption is what usually breaks timelines later.

Keep the working method simple. Split every important point into three buckets. Confirmed means you have a source or written partner statement. Unknown means nobody has shown you the current rule, term, or operating constraint. Must verify means the item blocks design or launch, such as disbursement eligibility, settlement behavior, return handling, and who owns exceptions when a payout does not land as expected.

Step 3 Block budget until the critical unknowns are named#

Before you spend engineering or market-entry budget, ask for the current M-Pesa Limited terms relevant to the lane you think you need. Ask your banking and mobile money counterparties for written answers on the funding path, payout eligibility, and failure handling. The checkpoint is not a glossy product page. It is a document set your legal, compliance, and finance owners can point to later.

The main red flag is false precision. If a partner cannot confirm limits, settlement windows, or reversal behavior in writing, mark that item unknown and keep it out of your launch estimate. That discipline is what makes the rest of this guide useful. Work from what is confirmed, call out what is still open, and verify the blockers before you commit.

For a regional operating comparison, see How Platform Teams Pay Contractors Across UAE, Saudi Arabia, and Egypt.

What BoT FX rules confirm and what they leave open#

Treat the current record as a boundary, not a permission slip. The Bank of Tanzania material in scope confirms that FX and payment infrastructure are part of the national financial architecture, and the December 2024 Financial Stability Report separately references foreign exchange reserves and payment systems infrastructure. It does not provide a contractor payout procedure or a confirmed answer on who may execute FX for a non-bank platform.

| FX point | Status | Grounded note |

|---|---|---|

| Foreign exchange reserves | Confirmed topic | The December 2024 Financial Stability Report references foreign exchange reserves |

| Payment systems infrastructure | Confirmed topic | The December 2024 Financial Stability Report references payment systems infrastructure |

| Contractor payout procedure | Not provided | The BoT material does not provide a contractor payout procedure |

| Who may execute FX for a non-bank platform | Not confirmed | The BoT material does not provide a confirmed answer on who may execute FX for a non-bank platform |

| Direct non-bank participation in IFEM | Unconfirmed for the operating model | Treat as unconfirmed until legal and compliance review the current FX-auction rule set and related BoT materials |

| Any Refinitiv FX Auction platform flow you can rely on | Unconfirmed for the operating model | Treat as unconfirmed until legal and compliance review the current FX-auction rule set and related BoT materials |

| A defined USD/TZS auction path for contractor funding | Unconfirmed for the operating model | Treat as unconfirmed until legal and compliance review the current FX-auction rule set and related BoT materials |

In practice, plan for partner-bank dependency unless your team can disprove it in writing. Ask the proposed bank partner to confirm who executes conversion, which account funds the payout leg, which reference IDs survive into reconciliation, and who owns failed or delayed settlement.

Keep payment-lane facts separate from FX assumptions. M-Pesa Limited terms support business-oriented lanes, including M-Pesa International Money Transfers (IMT) and a Business Collection or Disbursement Account. They do not, by themselves, confirm direct IFEM access or auction-based contractor disbursement.

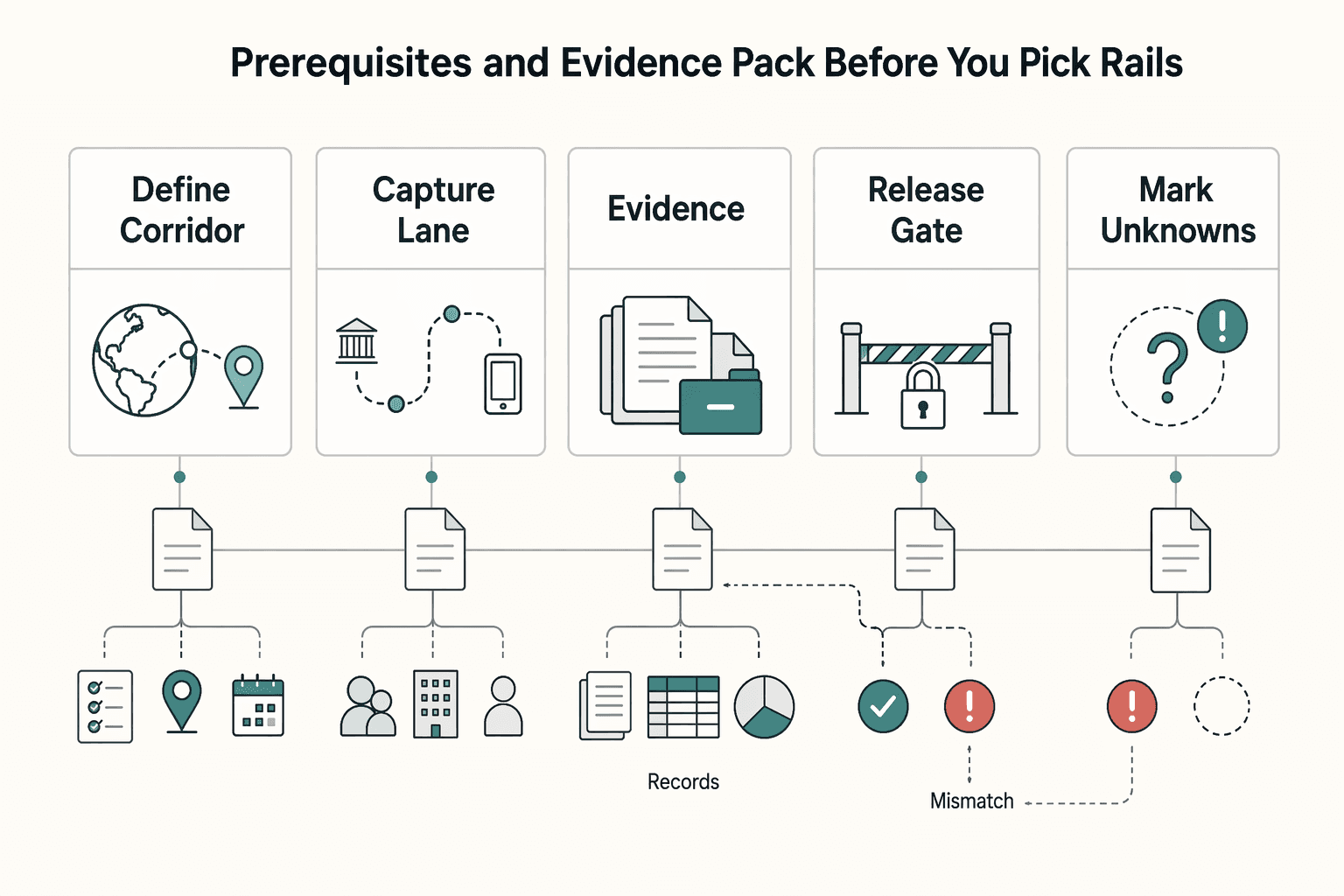

Prerequisites and evidence pack before you pick rails#

Do not choose a Tanzania payout rail until your evidence pack is complete and counterparties have confirmed the operating details in writing.

| Step | Focus | What to capture |

|---|---|---|

| Define corridor and contractor assumptions | Tie the lane decision to real operating conditions | Source currency, destination rail, recipient type, payout endpoint, payout size bands, batch pattern, KYC posture, and individual vs business-account payout structure |

| Capture lane-specific governing terms | Treat M-Pesa as multiple product lanes | The exact current terms page, retrieval date, and whether the needed language appears there, including the Business Collection or Disbursement Account definition |

| Require operating documents before design sign-off | Assemble the minimum set | Current terms for the chosen lane, Conditions of Use for M-Pesa Services, partner-bank documentation, an internal ownership map for compliance, funding/treasury, payout ops, and reconciliation, plus escalation paths on the Vodacom Tanzania and banking sides |

| Set a hard verification gate | Use operational documentation rather than marketing pages | Written confirmation of fees, settlement behavior, and return/reject/delay handling from bank and wallet counterparties |

| Mark unknowns and block launch estimates | Pause until the rail is decision-ready | Label limits, settlement windows, disbursement eligibility, or exception handling as unknown if they are still unclear |

Step 1: Define corridor and contractor assumptions. Document the payout corridor first: source currency, destination rail, recipient type, and payout endpoint. Then record your contractor assumptions: payout size bands, batch pattern, KYC posture, and individual vs business-account payout structure. That keeps the lane decision tied to real operating conditions.

Step 2: Capture lane-specific governing terms. Treat "M-Pesa" as multiple product lanes, not one rail. The Vodacom terms hub shows separate entries for Merchant, IMT, and Business lanes, and the terms are issued by M-Pesa Limited. If you plan to use a business payout path, save the exact current terms page and retrieval date, and confirm whether the needed language appears there, including the Business Collection or Disbursement Account definition.

Step 3: Require operating documents before design sign-off. Your minimum set should include current terms for the chosen lane, Conditions of Use for M-Pesa Services, partner-bank documentation, and an internal ownership map for compliance, funding/treasury, payout ops, and reconciliation. Also record escalation paths on both the Vodacom Tanzania and banking sides.

Step 4: Set a hard verification gate. Do not commit engineering until bank and wallet counterparties confirm fees, settlement behavior, and return/reject/delay handling from their operational documentation, not marketing pages. This is a practical risk control, especially where cost and reliability can affect real account usage and payout quality.

Step 5: Mark unknowns and block launch estimates. If limits, settlement windows, disbursement eligibility, or exception handling are still unclear, label them unknown and pause launch estimates. A rail is only decision-ready when terms, ownership, and failure behavior are documented.

Choose your Tanzania operating model before building integrations#

Start partner-led if you do not already have named owners for local compliance operations and payout exceptions. Evaluate a local-entity path only when tighter margin control and deeper operational control justify longer onboarding.

That recommendation follows from the evidence pack. In-scope Bank of Tanzania material points to regulatory frameworks, payment system licensing procedures, and cross-border payment and remittance oversight, so this is an operating-model decision, not just an integration decision.

Step 1 Pick the model that matches your operating capacity#

Use this comparison to assign responsibility before integration work starts.

| Model | Control | Speed to launch | Compliance burden | Reconciliation overhead | What you must verify |

|---|---|---|---|---|---|

| Local entity plus direct local partnerships | Higher direct control over contracts, funding path, and exception ownership | More onboarding dependencies because entity, bank, and rail relationships must align | Heavier internal burden across compliance, operations, and escalation ownership | Higher internal workload because your team reconciles each leg directly | Exact bank path, current M-Pesa Limited terms for the chosen lane, return handling, settlement artifacts, and who owns FX records |

| Partner-led or aggregator-led setup | Less direct control because a partner runs part of the operating chain | Can be faster to start if partner relationships are already in place, but timing is unconfirmed until documented | Lighter internal burden only if responsibilities are explicit in contract and runbooks | Can be lighter if the partner provides payout-level references and usable reports | Named bank dependency, fee model, payout status evidence, reversals process, and auditable FX references |

Practical rule: if your team cannot staff local compliance review, handle exceptions, and reconcile partner files without manual guesswork, start partner-led.

Step 2 Assign FX responsibility in writing, especially around USD/TZS#

Treat FX ownership as a contract and operations requirement, not a verbal assumption. The in-scope sources do not establish who owns USD/TZS conversion execution, rate timing risk, or transaction references, so your design pack must assign each point explicitly.

- Who executes conversion tied to USD/TZS, and at what point in the payout flow?

- Who absorbs rate timing risk if funding and disbursement are not simultaneous?

- Which immutable references are retained for audit and reconciliation?

Verification checkpoint: finance should be able to trace one payout from source funding to local disbursement using references that survive retries, reversals, and delayed confirmations.

Step 3 Gate go-live on a credible bank path#

If you cannot document a credible bank partner path for conversion and settlement, pause rollout rather than shipping partial payout capability.

Here, credible means a named bank relationship, written confirmation of the payout path, documented settlement behavior, and sample transaction evidence your team can reconcile. If your design uses an M-Pesa Business lane or a Business Collection or Disbursement Account, keep the current M-Pesa Limited terms in the same operating pack so wallet and funding legs are governed together.

No-go trigger: no credible bank path, no usable FX artifact trail, or no exception evidence means no launch estimate.

Map the right M-Pesa product lane to your contractor payout use case#

After you confirm a bank path, choose the wallet lane based on payout evidence and reconciliation quality, not brand familiarity.

Step 1 Compare lanes by contractor payout suitability#

Use current provider terms and written partner confirmation to classify each lane. Treat this as a screening tool, not a claim about eligibility, limits, or fees.

| Lane | Contractor payout fit | Verify in writing before build | Reject if |

|---|---|---|---|

| M-Pesa Business | Possible fit when positioned for business outbound wallet operations | Explicit support for contractor disbursements, instruction flow, payout-level references, and reconciliation export format | You only get summary confirmation with no stable payout or return identifiers |

| M-Pesa Merchant | Consider only if outbound disbursement support is explicitly documented | Proof it supports disbursement, not just acceptance or collection, plus status and reversal handling evidence | Materials describe checkout or acceptance, but no outbound payout artifact or exception flow is available |

| M-Pesa International Money Transfers (IMT) | Consider when cross-border funding and local wallet delivery are both documented for your corridor | Ownership of USD/TZS conversion, and references that connect FX, funding, and wallet delivery end to end | FX or wallet delivery cannot be traced with durable references across failures and returns |

Before you sign off, ask for one sample artifact pack: payout reference, batch identifier, status output, and any reversal or return ID that survives retries.

Step 2 Do not treat virtual card utility as payout proof#

M-Pesa Virtual Card utility does not prove contractor disbursement capability. Card-presentment utility and wallet payout utility are different product intents, so keep disbursement terms, settlement evidence, and exception handling requirements separate.

Step 3 Set rail priority from current market evidence and reconciliation strength#

If your diligence pack includes current Tanzania market evidence, including TCRA-referenced context, use it to decide whether phase one starts with M-Pesa only or also includes Tigo Pesa and Airtel Money. Do not rely on copied or stale market claims.

Selection rule: when one lane has weaker traceability or poorer reconciliation exports, pick the lane with stronger operational evidence even if onboarding is slower.

For another FX-and-rail example, see How to Pay Contractors in Sri Lanka: LankaPay and CBSL FX Rules for Platform Operators.

Build the payout sequence with verification checkpoints#

Build this sequence so one payout can be traced end to end before you scale contractor volume.

Step 1 Approve the contractor and payout policy. Start with onboarding and policy checks before payment execution. Keep an approval record for each contractor that shows approver, allowed payout route, and any corridor or compliance restrictions.

The Bank of Tanzania annual report places payment systems under oversight activities and lists payment system licensing procedures and procedures for approval of payment system instruments. That does not prescribe your contractor workflow, but it supports keeping a dated internal approval trail when you change a bank partner, payout instrument, or M-Pesa Limited lane.

Step 2 Confirm funding path and conversion timing. Before you create a payout instruction, confirm which account funds the batch, who performs conversion when needed, and which reference links that conversion to payout delivery. Your checkpoint artifact is one approval record plus one funding or conversion reference finance can match later.

Step 3 Initiate disbursement with retry controls. Use a stable internal payout ID across retries, and preserve the first provider reference you receive as a permanent record. Record payout intent in your ledger before you treat provider success as final settlement evidence.

Step 4 Track status events and close exceptions with evidence. Do not rely only on a batch-level success signal. Store the payout-level status timeline your provider returns, and keep a finance-ready output with internal payout ID, provider reference, batch identifier, amount fields, and final disposition.

Step 5 Release with a controlled pilot batch. Run a small pilot cohort first, then verify that operations, finance, and compliance can all trace the same payout from approval through reconciliation output before opening broader contractor groups.

For another wallet payout example, see How to Pay Contractors in Egypt: Meeza Instapay and FX Rules for Platform Operators.

Plan failure handling and reconciliation before go-live#

Do not go live until each payout exception has a clear owner, a state-change rule, and a complete evidence bundle. If your team cannot explain what happens when confirmation is delayed, status is disputed, or your ledger does not match the provider view, launch risk is still high.

Step 1 Enumerate the failure modes you will actually operate#

Define separate paths for rejected recipient details, held transactions, delayed confirmations, return flows, and provider-versus-ledger status mismatches. Treat these as different exception classes, not one generic "failed payout" bucket, because each class needs different handling and closure evidence.

Before go-live, run a tabletop walkthrough for each class and confirm the expected ledger outcome at each state.

Step 2 Assign ownership by lane and escalation path#

Set named ownership across your platform operations, your partner bank, and the support channel for the relevant M-Pesa lane. The terms hub includes lane-specific terms, including M-Pesa International Money Transfers (IMT), so do not assume exception handling is identical across lanes.

For each exception class, document:

- Who investigates first

- Who confirms final disposition

- Who can trigger reversal, reissue, or closure

Step 3 Write hard if-X-do-Y rules#

Use explicit rules an ops analyst can execute without interpretation:

- If provider confirmation is delayed beyond your internal SLA, move the payout to investigation and block automatic retry.

- If a return is confirmed, create the reversal workflow, post the reconciliation entry, and notify AP.

- If provider status shows success but your ledger has no matching payout intent or immutable provider reference, hold closure and escalate.

Step 4 Require an audit bundle for every exception#

For every exception, keep one complete bundle: original payout request, status timeline, provider reference, final disposition, and the reconciliation entry used to close the case. Where the lane uses a Business Collection or Disbursement Account, include that account context in the bundle.

The close standard is straightforward: finance or audit should be able to reconstruct the full exception path without engineering log dives.

For a Pix-based reconciliation comparison, see How Platform Teams Pay Brazil Contractors with Pix.

Common mistakes that delay Tanzania rollout and how to recover#

Rollouts usually stall when teams treat high-level Tanzania materials and the M-Pesa brand as operating proof instead of lane-specific payout evidence.

| Mistake | Recovery | Article note |

|---|---|---|

| Using FX/BoT materials as contractor payout instructions | Re-scope those sources to market context only and keep a short list of open payout questions for your bank partner | The BoT Financial Stability Report covers system-level topics like payment systems infrastructure and digital payment systems, not contractor disbursement procedures |

| Picking an M-Pesa lane by familiarity | Re-run lane selection from the actual terms-page entries you reviewed and treat Business, Merchant, and IMT as distinct | Vodacom separates entries such as Business, Merchant, and M-Pesa International Money Transfers (IMT) |

| Estimating timelines with critical payout unknowns | Freeze engineering commitment until unknowns that affect execution are written down and owned | If a payout or reconciliation unknown is still open, it remains on the critical path |

| Launching without exception ownership | Assign named owners and escalation paths across your ops team, bank partner, and chosen M-Pesa lane before the first live batch | If ownership for delayed confirmations or returned payouts is unclear, you are still in pre-launch |

Related: How to Pay Contractors in Ethiopia: Telebirr and NBE FX Rules for Platform Operators.

Conclusion and next action for platform operators#

If you cannot map Bank of Tanzania context, the exact M-Pesa lane you plan to use, and who owns payout exceptions, you are not ready to launch. That is the practical standard for platform operators here, and it is stricter than brand familiarity or a promising partner demo.

Step 1 Freeze the launch decision until the route is written down. Your minimum decision record should answer four things in plain language: which bank partner handles the regulated money movement, where FX conversion responsibility sits, which M-Pesa lane you are pursuing, and who resolves rejects, delays, and returns. If any of those answers still depend on inference from marketing pages, treat the item as unknown and block go-live.

A useful checkpoint here is document freshness. The grounded source set supports using the current Vodacom Tanzania terms page for named lanes such as M-Pesa Business, M-PESA MERCHANT, and M-Pesa International Money Transfers (IMT). It also supports treating broader market reports carefully: the cited EU investment report is from 2022 and explicitly says it does not reflect the European Commission's official opinion, so it is not launch approval evidence.

Step 2 Choose the lane only after you capture the tradeoff in writing. Do not pick a rail just because M-Pesa is the most familiar name on the shortlist. One candidate to verify is M-Pesa Business, because the terms define a Business Collection or Disbursement Account as an account held by a third party for collecting or disbursing E-Money to customers. That is useful evidence, but it is still not proof that your contractor payout case is accepted, priced, or operationally supported.

A typical failure mode is treating lane naming as product fit, building the integration, then discovering later that reconciliation output, exception handling, or onboarding assumptions do not match the contractor model. Ask for written confirmation on fees, limits, settlement behavior, and return handling before engineering locks scope.

Step 3 Prove your controls in a pilot before broad release. For your first pilot batch, define the evidence you will retain for every payment, such as an internal payout ID, the provider reference, and a stored status timeline. Your verification point is simple: finance should be able to tie the original instruction, partner output, and final ledger result together without manual guesswork. If a delayed confirmation or return breaks that trace, stop after the pilot and fix the evidence trail before volume increases.

Copy this into your launch tracker, then use it as the go-live check:

- Confirm bank-partner path aligned to applicable Bank of Tanzania requirements.

- Select payout lane among M-Pesa Business / Merchant / IMT with documented tradeoffs.

- Lock fee, limit, and settlement assumptions as written partner confirmations.

- Validate pilot evidence trails for status history and reconciliation.

- Approve go-live only after unknowns are reduced to non-critical items.

That is the bar. If you can defend those five checks with documents, you are close. If not, pause rather than improvise.

For a step-by-step walkthrough, see How Platform Operators Pay Creators Globally Across YouTube, Twitch, and Substack.

Frequently Asked Questions

Can a non-bank platform directly access BoT FX auctions to fund contractor payouts in Tanzania?

Do not assume that. Your checkpoint is written confirmation from the partner bank on who executes the FX step and what auditable reference you receive back.

Is M-Pesa enough on its own, or should we design for Tigo Pesa and Airtel Money coverage from day one?

Start from your contractor mix, not from brand recognition. The source set here does not support claiming a guaranteed coverage strategy across M-Pesa, Tigo Pesa, and Airtel Money, so do not lock a multi-rail build just to feel complete. If your onboarding data already shows heavy M-Pesa usage, launch narrow and capture actual wallet distribution before adding more rails.

Which M-Pesa lane is typically relevant for business contractor payouts: M-Pesa Business, Merchant, or IMT?

A reasonable first lane to verify is M-Pesa Business. The terms define a Business Collection or Disbursement Account as an account held by a third party for collecting or disbursing E-Money to customers. That said, the terms page also has separate entries for M-Pesa Merchant and M-Pesa International Money Transfers (IMT), and that separation matters. Presence on the terms page is not proof that a lane fits your contractor payout case, so require written confirmation of disbursement suitability and reconciliation output.

What must be confirmed before we commit engineering resources to Tanzania payouts?

You need the exact funding path, the responsible party for USD/TZS conversion, the chosen payout lane, and the provider fields you will receive for status and reconciliation. You also need written answers on fees, limits, settlement behavior, and returns, because those are not confirmed by the source set. If any of that is still inferred from marketing pages, freeze build.

What are the most important unknowns to resolve with partners before go-live?

Focus on recipient eligibility, required wallet data, exception ownership, return behavior, and what evidence comes back when a payout is delayed or rejected. Also confirm whether your contractor model fits the partner's onboarding and KYC expectations rather than borrowing assumptions from another wallet's terms. A small unknowns register with owner and request date is enough, but it needs to exist.

How should we handle payout failures and returns without breaking reconciliation?

Keep one immutable internal payout ID and store the provider reference and full status timeline against it. If confirmation is delayed, move the payment into investigation instead of retrying blindly. Duplicate retries can create ledger drift. If a return is confirmed, post a linked reversal entry rather than editing the original payout away.

What proof should finance and compliance require before approving launch?

Ask for the exact M-Pesa Limited terms-page entry reviewed. Also ask for partner-bank confirmation of the funding and FX responsibilities, named escalation contacts, and a sample of the status or reconciliation data you will actually receive. If a wallet or partner claims regulated payment activity, capture the contracting entity and the governing terms, not just the brand name. Approval should wait until the evidence pack cleanly separates confirmed facts from open questions.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- bis.org/publ/qtrpdf/r_qt2003.pdftrusted

- documents1.worldbank.org/curated/en/784831625137368238/txt/Building-F...trusted

- documents1.worldbank.org/curated/en/784831625137368238/pdf/Building-F...trusted

- elibrary.imf.org/downloadpdf/view/journals/002/2016/255/002.2...trusted

- imf.org/-/media/files/publications/ftn063/2024/engli...trusted

- oecd.org/content/dam/oecd/en/publications/reports/201...trusted

- openknowledge.worldbank.org/bitstreams/d94a4468-26cc-5c49-8f09-260503ae4...trusted

- openknowledge.worldbank.org/server/api/core/bitstreams/b1b3d215-a564-59b...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Paying Contractors in Sri Lanka with CBSL and LankaPay Decision Checks

Start with regulatory certainty. For a platform operator, Sri Lanka should not be screened from a payout product page or a rail feature list first. The evidence set shows real institutional signals, but it still does not prove that your exact contractor payout flow is permitted, eligible, and operationally supportable.

Pay Contractors in Ethiopia with Telebirr and NBE FX Checks

This brief is for platform founders and operators who need a go/no-go answer on Ethiopia before they spend engineering, compliance, or go-to-market budget. The real question is not whether contractors exist in Ethiopia or whether digital payments exist. It is whether your exact payout model looks feasible enough, based on actual evidence, to justify real work now.

Pay Contractors in Egypt With Clear Rail and FX Decision Gates

Treat Egypt as two launch decisions, not one. A domestic Egyptian disbursement flow and a cross-border contractor payout flow can end with the same beneficiary, but they are not automatically the same operational or compliance problem. If you blur them together, local payment momentum can look like proof of payout readiness when it is not.