Quick Answer

Split the work into separate Canada lanes first: contractor payouts, CRA remittances, and FINTRAC reporting analysis. Then assign one accountable legal owner per lane before engineering starts. The article’s decision rule is to choose Interac e-Transfer or EFT only after provider evidence covers failed payments, returns, and reconciliation outputs. It also keeps a hard boundary in scope: CRA says it does not accept direct Interac e-Transfer, so CRA payment handling must be designed independently from contractor disbursements.

Why this Canada contractor payout guide exists#

Step 1. Treat the payout choice as a market-entry choice. If you want to pay contractors in Canada, you are not just picking a payment rail. You are deciding who owns compliance interpretation, who absorbs support exceptions, and how much product work you need before launch. That matters because Canadian payout design can pull in separate obligations for payment operations and anti-money laundering compliance. Those responsibilities do not always sit with the same team or role.

A useful checkpoint is simple. Ask whether your team can name the accountable party for each lane before engineering starts. If the answer is still "the platform, probably," you are not ready to scope this as a button-level feature. That is the first failure mode this guide is meant to prevent.

Step 2. Separate search noise from the decision you actually need to make. Most public material here sends founders down the wrong path. You either land on FINTRAC pages, which are authoritative but narrow, or you find generic contractor-payment advice that skips role ownership and reporting scope. Neither gives you the sequence an operator needs: what flow am I building, what role am I playing in that flow, and what obligations attach to that role?

That gap gets worse around EFT language. FINTRAC's own guidance says it "explains the requirement to report electronic funds transfers to FINTRAC." Its travel-rule guidance is explicit that it applies to financial entities, money services businesses, foreign MSBs, and casinos under the PCMLTFA. It also defines EFT narrowly for that guidance: international EFTs and certain EFTs within Canada sent via SWIFT MT-103 or its equivalent.

Verification point: if you see EFT reporting language, "travel rule," or PCMLTFA in the requirement set, route that question to your AML or compliance owner, not only to product or payments.

Step 3. Scope payout and compliance paths as different lanes before you build. Do not flatten this into "Canada payments." Separate customer-facing payout flows from FINTRAC reporting and travel-rule analysis so you can design the right launch shape with fewer reversals. In practice, that usually means different documents, different owners, and different exception handling, even when the user-facing story sounds similar.

One red flag to catch early is the assumption that "EFT" means one thing everywhere. FINTRAC guidance does not support that shortcut. For compliance analysis, EFT has a specific meaning. The travel rule became effective in this guidance on June 1, 2021. The real job is to map each Canadian flow to its governing obligation set, then decide what role your organization is playing in that flow. That is why this guide exists: to turn fragmented Canadian guidance into one operator-level decision sequence.

For a Turkey payout playbook with similar ownership questions, see How to Pay Contractors in Turkey: FAST EFT and MASAK Compliance for Platform Operators.

What to prepare before you commit engineering resources#

Treat this as two scopes, not one: define contractor payouts and CRA remittances separately before engineering starts.

Step 1. Define the target flow in writing. State whether you are building a contractor payout flow, a CRA remittance flow, or both. Do not assume contractor payout choices answer CRA remittance design. CRA says it does not accept payments directly by credit card, PayPal, or Interac e-Transfer, so the CRA lane needs its own payment method and ownership model.

Verification point: your scope memo should name the destination, method under evaluation, and whether the flow is contractor payout or CRA remittance.

Step 2. Confirm your operating role for each flow. Name who operates each lane: your platform, a third-party service provider, or another regulated role where applicable. For CRA remittances, confirm who sends payment and remittance details online to CRA. CRA states third-party service providers can do this on the payer's behalf, and only providers established as Electronic Data Interchange (EDI) remitters can offer payments to CRA and request listing on CRA's website.

Practical constraint: provider capabilities are not interchangeable. CRA also notes that different providers support different payment methods, and credit card payments can currently only be made through PaySimply or Plastiq.

Step 3. Assemble a lean evidence pack for sign-off. Include:

- a responsibility matrix by flow and entity

- Electronic Funds Transfer Report steps marked as open compliance questions

- Canada-specific legal unknowns for review

- provider constraints, service-fee notes, and required contracts or onboarding documents

If ownership is still TBD for a required remittance or reporting artifact, hold build scope for that lane.

For another market-specific contractor payout lane, see How to Pay Contractors in UAE: UAEFTS AMLSCU Compliance and WPS Rules for Platforms.

Map the three Canadian layers before you design payouts#

Treat these as three separate lanes from day one: contractor payout rail, CRA remittance interaction, and FINTRAC AML reporting. If you combine them into one "payments" track, ownership and controls drift.

| Lane | What it covers | Grounded cue |

|---|---|---|

| payout rail | Moving funds to the contractor | Interac e-Transfer or EFT to move funds to the contractor |

| CRA remittance | Tax and remittance interaction with CRA | References CRA remittance methods or submission mechanics |

| FINTRAC/AML | AML reporting through FINTRAC | References FINTRAC, Electronic Funds Transfer Report, reporting entity status, or ML/TF risk assessment |

Step 1. Label each requirement to one lane only. Layer 1 is the contractor payout rail, for example Interac e-Transfer or EFT to move funds to the contractor. Layer 2 is tax and remittance interaction with CRA. Layer 3 is AML reporting through FINTRAC.

Use one label per requirement: payout rail, CRA remittance, or FINTRAC/AML. If a ticket mixes "send contractor funds" with "file/report/remit," split it before build.

Step 2. Anchor AML interpretation to the named instruments and FINTRAC entity context. For AML interpretation, anchor to the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA) and the Proceeds of Crime (Money Laundering) and Terrorist Financing Regulations. FINTRAC states its guidance is "applicable to all REs subject to the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA) and associated Regulations," and its EFT guidance explains "the requirement to report electronic funds transfers to FINTRAC."

Keep sector context explicit. FINTRAC also notes some obligations may apply only to certain sectors, and EFT guidance is organized by entity type, including separate MSB/FMSB reporting requirements. Do not infer a trigger threshold from the $10,000 example note alone.

Step 3. Route ownership by regulator language, not feature surface. Apply a strict routing rule. If the requirement references FINTRAC, Electronic Funds Transfer Report, reporting entity status, or ML/TF risk assessment, assign it to AML/compliance owners. If it references CRA remittance methods or submission mechanics, assign it to tax/remittance owners.

This adds upfront coordination, but it prevents legal interpretation from being embedded in product assumptions.

Related: How to Pay Contractors in South Africa: RTGS EFT and SARB Compliance for Platforms.

Compare Interac and EFT using decision criteria founders actually need#

Start with evidence, not brand preference. From the current excerpts, you can scope decision lanes and unknowns, but you cannot treat public summaries as proof of rail-level compliance or operating behavior.

Step 1. Compare rails and caveats using only verified signals#

| Option or caveat | Use case fit | Operational dependency on a third-party service provider | Reconciliation burden | Exception handling complexity | Reporting implications |

|---|---|---|---|---|---|

| Interac e-Transfer for contractor payouts | Candidate for the contractor payout lane only. | May depend on bank/provider setup; exact model is provider-specific. Confirm with your provider. | Not established by current public summaries. | Not established by current public summaries. | Do not infer FINTRAC duties from the rail name alone. |

| Electronic Funds Transfer (EFT) for contractor payouts | Candidate for the contractor payout lane; evaluate when you want bank-transfer style operational control. | May involve a bank and/or third-party service provider; confirm in implementation and contract docs. | Not established by current public summaries. | Not established by current public summaries. | Do not equate operational EFT with an automatic EFT report obligation. |

| CRA payment or remittance lane | Hard boundary: model separately from contractor payouts. Confirm direct Interac acceptance by CRA with official CRA guidance. | May require a separate remittance arrangement or path. | Keep remittance evidence separate from payout evidence. | Route to tax/remittance ownership, not contractor-support ownership. | Separate lane from FINTRAC reporting and payout execution. |

| FINTRAC reporting analysis | Not a payout rail. | Ownership may vary by legal role/entity type. | Keep records showing who assessed responsibility. | Unclear ownership increases rework risk. | Confirm exact trigger mechanics with your provider. |

| Public-summary and provider caveat | Useful for scoping questions, not final compliance conclusions. | Sales decks and commentary are not substitutes for product terms or regulator guidance. | Low until relied on as final evidence; high during audit or incident review if wrong. | Assumed edge-case support is a common failure mode. | The July 2024 McGill policy-lab report states findings are student-authored and may not reflect Interac Corp.; do not treat it as a compliance rulebook. |

Step 2. Pick the first rail by near-term objective, then verify before build#

If your near-term goal is a faster contractor disbursement experience, start with the rail that produces fewer support exceptions after provider validation. If your near-term goal is more structured bank-transfer style operations, evaluate EFT first as a working hypothesis, then confirm with provider artifacts.

Before you approve build tickets, require four artifacts: a sample reconciliation export, a complete payout outcome-state list, a written statement on who analyzes FINTRAC reporting responsibility, and a clear answer on whether CRA-facing payments run on a separate remittance path. The TD legal notices reference to designated locations for CRA-related requirements reinforces this lane split, but it does not select a payout rail for you.

The expensive mistake is not choosing Interac or EFT. It is choosing either without evidence for ownership, exceptions, and reporting boundaries.

For a step-by-step walkthrough, see How to Pay Contractors in Malaysia: DuitNow and Bank Negara FX Compliance for Platforms.

Assign ownership for every reporting and remittance step#

Pause any lane where the accountable legal entity is still unnamed. Rail choice is only practical after you assign ownership for FINTRAC reporting tasks, CRA remittance transmission, and evidence retention.

Step 1. Name the accountable entity before you map product behavior#

Do not presume the platform operator files the Electronic Funds Transfer Report just because the product initiates or displays a payout. Start with FINTRAC's "1. Who must comply" section, then assign ownership.

Use a compact RACI (A, R, C, I) that names the legal entity for each task and points to the contract or policy that supports it.

| Task | Platform operator | Financial entity / MSB / FMSB | EDI remitter | Verification artifact |

|---|---|---|---|---|

| Determine who must comply for FINTRAC EFT reporting | A for internal decision record, C to legal/compliance | Candidate A/R if role analysis lands here | I | Written role memo tied to FINTRAC "Who must comply" |

| Submit any required Electronic Funds Transfer Report | I or C unless contract says otherwise | Candidate A/R where reporting duty sits | I | Filing procedure, named submission owner, escalation path |

| Transmit CRA remittance | C or I unless you are the remitter | C or I | Candidate A/R where an EDI remitter is used | Named remittance channel and proof of sender |

| Retain audit evidence | A/R for internal records | A/R for filing records they own | A/R for remittance confirmations they own | Retention location, access owner, retrieval SLA |

If a row stays "shared," teams usually make conflicting assumptions. Keep each row explicit.

Step 2. Define who submits what and which document proves it#

Use the guidance labels directly. For FINTRAC ownership, reference "How to submit a report to FINTRAC" and "Annex A: Field instructions to complete an Electronic Funds Transfer Report."

Your evidence pack should include:

- signed responsibility matrix

- contract or addendum naming filing/remittance owner

- internal memo recording the FINTRAC "Who must comply" outcome

- sample submission or confirmation artifacts per lane

- retention map for confirmations, exceptions, and reconciliations

Ask for the artifact before launch, not a verbal assurance. If no document owner is named, treat ownership as unresolved.

Do not code threshold logic from summary text alone. FINTRAC notes that dollar references such as $10,000 are in Canadian dollars unless otherwise specified, but this section does not establish exact trigger mechanics or exceptions.

Step 3. Treat third-party remittance options as constraints, not defaults#

Treat third-party CRA remittance options as provider-specific constraints, not universal defaults. Validate availability, contract coverage, fees, operational ownership, and support handling before you build around any single option.

Use one strict decision rule: if ownership of any compliance artifact is ambiguous, pause launch scope for that lane until the accountable legal entity is named.

Build the contractor tax documentation lane early#

Treat contractor tax documentation as a launch gate. If the contractor record does not clearly show payout eligibility, tax-review path, and where period-level remittance evidence is stored, that contractor is not launch-ready.

Step 1. Make tax profile completion a payout prerequisite#

Set tax profile completion as a hard prerequisite before any payout. Your onboarding record should require a status such as pending review, approved for payout, or blocked pending documents, so T4A or NR4 handling is managed in-process instead of reconstructed later.

At this stage, do not encode filing thresholds or withholding formulas from summary material. Build fields and review checkpoints so tax or finance can determine whether a T4A path may apply, whether an NR4 path may apply, and whether non-resident treatment needs separate review. A practical test is simple: if residency or entity details are missing, payout approval must stay blocked.

The failure mode is consistent: payouts launch first, then teams cannot prove who was treated as resident or non-resident at approval time, what documents supported that decision, or why one contractor was paid while another was held.

Step 2. Put GST/HST and non-resident checks into onboarding and approval#

Make GST/HST and Part XIII non-resident withholding checkpoints explicit in onboarding and payout approval, not buried in notes. For GST/HST context, keep the legal basis clear: CRA guidance states that legislative references are to the Excise Tax Act or, where appropriate, the GST/HST Regulations. Product should collect facts for review, not infer tax treatment from UI labels.

Use a two-step control: onboarding captures facts and documents, then payout approval confirms the profile is still current. Without that second check, stale profiles continue to clear payouts.

Keep CRA remittance handling separate from contractor payout rails. CRA says it does not accept payments directly by credit card, PayPal, or Interac e-Transfer, and that only third-party providers established as EDI remitters can offer CRA payments. If a payout period requires a CRA-facing remittance action, record the provider and evidence path explicitly instead of assuming the payout method covers it.

Step 3. Give operations a period-by-period evidence checklist#

Use one checklist row per contractor per payout period:

| Required record | What ops should see | Verification point |

|---|---|---|

| Contractor tax profile status | Pending, approved, or blocked, plus review owner and review date | Payout cannot move to approved if status is pending or blocked |

| Payout eligibility status | Cleared, held for tax review, or held for missing documents | Hold reason is visible in the payout queue, not hidden in notes |

| Remittance evidence reference | Link or ID for any CRA remittance confirmation, provider record, or internal memo for that period | Evidence is retrievable without asking another team where it lives |

Tie evidence references to each payout period, not only to the contractor profile. Profiles change, but audit questions usually ask what was known, approved, and retained when that specific payout was released.

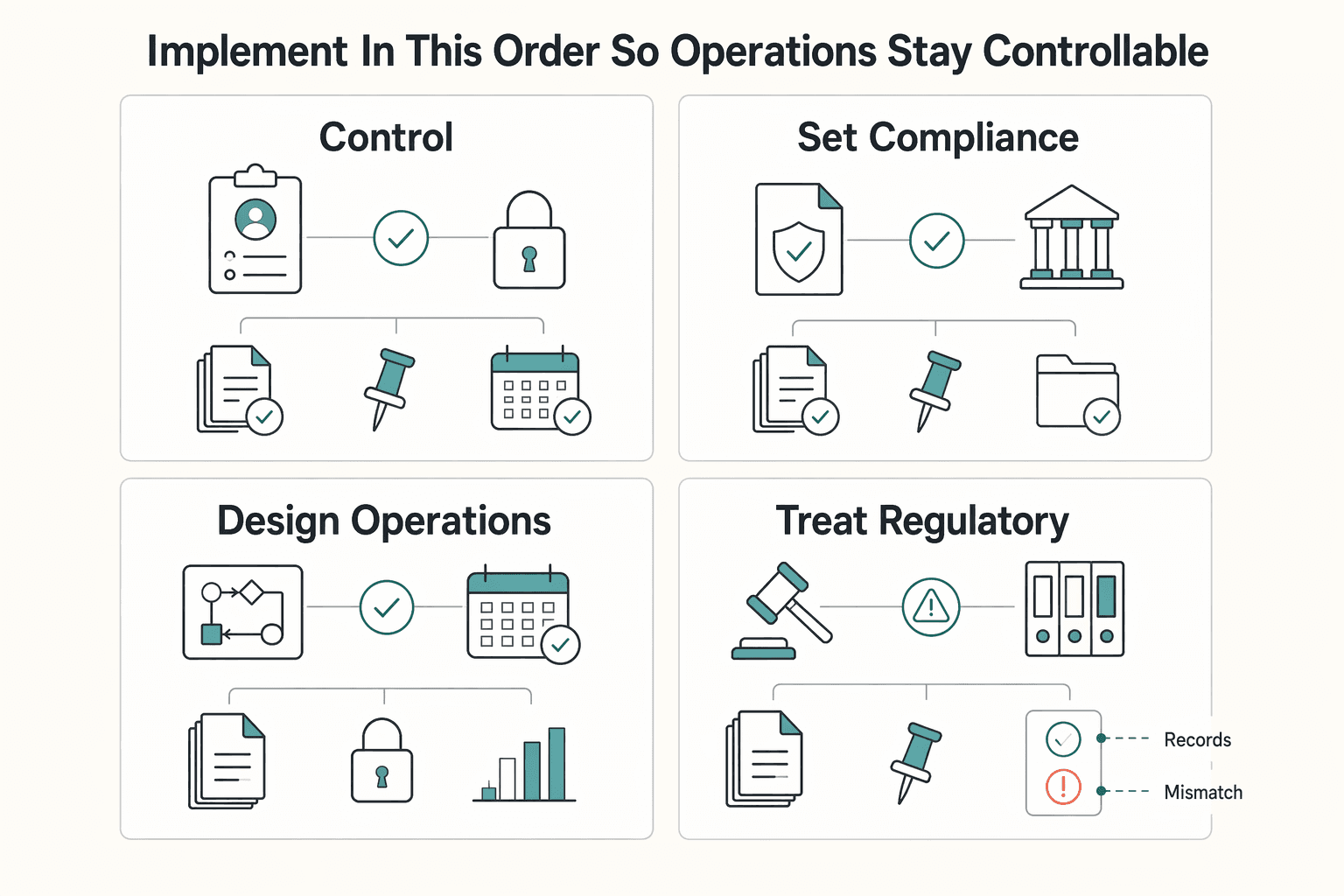

Implement in this order so operations stay controllable#

Build in this order so ownership and evidence are clear before you scale payouts.

- Lock onboarding and payout eligibility controls first.

Require a contractor record state and evidence path before payout initiation. If a record is incomplete or under review, keep payout blocked so operations can explain each approval decision later.

- Set compliance ownership before encoding reporting logic.

If a requirement touches FINTRAC or an Electronic Funds Transfer Report, assign ownership first and document the decision path. FINTRAC's framework puts risk-assessment responsibility on the reporting entity, and the method is risk-based rather than one fixed template across every sector.

- Design operations for outcomes, not just successful sends.

Before broader rollout, confirm your team can handle success, return or failure, and manual investigation paths with retrievable evidence and reconciliation records.

- Treat regulatory change as pending until it is in force.

Where proposed AML updates are involved, keep implementation assumptions conservative and document interim controls; a closed consultation is not the same thing as finalized rules.

Common mistakes that cause rework in Canada launches#

Rework usually starts when teams collapse different obligation lanes into one implementation stream. Keep each lane explicit: name the flow, the accountable legal role, and the evidence owner before you lock requirements.

| Mistake | Why it causes rework | Stated control |

|---|---|---|

| Mixing CRA-facing requirements with contractor payout requirements | Different obligation lanes get treated as one implementation stream | Require each ticket to declare its lane up front before it can move to build |

| Encoding reporting assumptions before legal-role mapping is documented | Product fills in legal accountability by default | Document the legal entity and record/evidence ownership for each lane first |

| Deferring tax-document and GST/HST decision points until after scale | Eligibility gates and evidence tracking arrive late even when final treatment still needs review | Add eligibility gates and evidence tracking early |

| Choosing providers before exception operations are defined | Returned/failure artifacts, reconciliation outputs, stable transaction identifiers, and clear rejected-payment records may be missing | Make provider selection require those artifacts and records |

- Mixing CRA-facing requirements with contractor payout requirements.

Treat these as separate tracks with separate owners from day one. A practical control is to require each ticket to declare its lane up front - payout operations, tax/remittance, or compliance - before it can move to build.

- Encoding reporting assumptions before legal-role mapping is documented.

Do not let product fill in legal accountability by default. Document the legal entity and record or evidence ownership for each lane first, then build integrations that match that assignment.

- Deferring tax-document and GST/HST decision points until after scale.

Add eligibility gates and evidence tracking early, even when final treatment still needs review. For GST/HST context, use CRA RC4022(E) Rev. 25 (registrants) and RC4027(E) Rev.23 (non-residents) as guidance only: CRA states these are plain-language resources that do not replace law, and legislative references point to the Excise Tax Act and GST/HST Regulations.

- Choosing providers before exception operations are defined.

Provider selection should require returned or failure artifacts, reconciliation outputs, stable transaction identifiers, and clear rejected-payment records. If a provider can only demo successful sends, you are missing the operational path that creates most finance and support rework.

The practical next step for founders#

Use a strict go or no-go rule: do not scale any Canada payout or remittance lane until each step has a named legal owner, an operating owner, and a retained proof artifact. If any row in your ownership matrix is blank, pause rollout and close that row first.

- Define each flow boundary in writing.

Write one sentence per lane: contractor payout by Interac e-Transfer, contractor payout by EFT, CRA remittance, or a specific combination. Keep those lanes separate in your specs and tickets. If one ticket changes contractor disbursement, CRA payment behavior, and FINTRAC reporting at the same time, scope is already mixed.

Keep the CRA acceptance boundary explicit: CRA does not accept direct Interac e-Transfer, and Interac/PayPal CRA payments are provider-mediated. If your note says "use Interac for CRA payments" without naming the provider path, the lane is not defined.

- Name the accountable entity for each compliance action.

For every lane, list the platform operator, any third-party provider, and any regulated entity involved. If CRA remittance is in scope, confirm whether an Electronic Data Interchange (EDI) remitter is part of the path, since only providers established as EDI remitters can offer payments to the CRA.

Your verification check is simple: every reporting or remittance artifact has one explicitly named legal owner. A common failure is listing only a provider brand and never naming the actual reporting entity.

- Map FINTRAC duties separately from CRA duties.

FINTRAC duties attach to reporting entities, not to whoever built the payout flow. Track Electronic Funds Transfer Report ownership separately, including how threshold handling is assigned for international EFT reporting ($10,000 or more). In the CRA lane, track method, provider, fees, and deadline-sensitive obligations.

- Choose rails by operational fit, then prove exception handling.

Pick the rail your team can operate under failure, not just on the happy path. Interac e-Transfer can work when your provider can show reject, return, and investigation artifacts. If you need bank-account-based operations and structured reconciliation, evaluate EFT first.

Before signing, request sample status exports, stable transaction IDs, and returned-payment records. Do not assume parity across providers; methods and fees vary.

- Validate tax-document gates before build commitment.

Gate payout eligibility on tax profile status, contractor classification status, residency/non-residency review status, and document-received evidence links. Keep room for T4A and NR4 handling, and for other document paths when the case requires them.

Final test: can your team show why a contractor was eligible on a specific date, who approved it, what rail was used, and the tax-document state at that point? If not, launch fewer lanes and make those lanes audit-ready first.

For another contractor-payout country playbook, see How Platform Operators Pay Contractors in Indonesia With GoPay, OVO, DANA, or BI Fast.

Frequently Asked Questions

Is CRA Interac guidance the same as contractor payout compliance in Canada?

FINTRAC guidance covers EFT reporting, but CRA remittance questions fall in a separate lane. Treat CRA-facing method questions as distinct and confirm them with CRA-specific guidance and counsel.

Who is responsible for filing an Electronic Funds Transfer Report to FINTRAC in a platform-led model?

Do not assume the platform files it just because it initiates or orchestrates payment. FINTRAC’s guidance confirms the EFT reporting requirement, includes “1. Who must comply”, and lists exceptions, but the excerpt here does not provide enough detail to assign responsibility between a platform, financial entity, or MSB/FMSB.

Do we need to become an Electronic Data Interchange (EDI) remitter to handle CRA-facing payment methods?

Confirm the remittance method, transmitting entity, and any third-party role with CRA-specific guidance and counsel before scoping product work.

When should we choose Interac e-Transfer versus EFT for contractor payouts?

FINTRAC has EFT reporting requirements, a “Who must comply” section, and exceptions, but rail selection between Interac e-Transfer and EFT should be finalized with provider documentation and compliance review.

What records should we retain to satisfy audit and reconciliation expectations?

This section does not include a confirmed FINTRAC or CRA record-retention checklist for your model. Define required records with legal/compliance owners before implementation, and avoid treating this FAQ as the source of final retention obligations.

Which tax-document checkpoints should be in MVP for Canadian contractor payouts?

T4A, NR4, GST/HST, withholding, and related threshold obligations should be treated as open items. Finalize them with CRA-specific guidance and counsel.

What key items are still unknown from public summaries and must be confirmed with legal or compliance counsel?

The main unknowns are the exact FINTRAC filing entity in your model, which EFT scenarios qualify for exceptions, whether any CRA-facing method requires an EDI remitter arrangement, and the final tax-document/withholding treatment for your contractor population. FINTRAC’s EFT guidance references Canadian-dollar amounts such as $10,000, but threshold logic should not be implemented from a snippet alone.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- eda.gov/sites/default/files/2024-09/Enhancing-Rural-...trusted

- govinfo.gov/content/pkg/CRPT-116hrpt40/html/CRPT-116hrpt...trusted

- occ.gov/static/cra/craeval/apr19/24096.pdftrusted

- oecd.org/en/publications/tax-administration-2025_cc01...trusted

- sec.gov/Archives/edgar/data/1584207/0001584207180000...trusted

- sec.gov/Archives/edgar/data/1488813/0001488813250000...trusted

- utah.gov/pmn/files/1312591.pdftrusted

- wipp.energy.gov/library/CRA/CRA-2014/References/Others/US_EP...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Pay Contractors in Turkey on FAST and EFT With MASAK Controls

Start with a narrow decision, not a country-level yes or no. If you can support Turkish lira payouts, treat FAST as a likely primary rail, and accept that MASAK and EFT details still need local confirmation, a controlled pilot in Turkey is reasonable. If those unknowns affect whether you can legally monitor, release, or reconcile contractor payouts, delay direct launch or use an Employer of Record as an interim model.

Pay Contractors in South Africa with RTGS and EFT Decisions That Hold Up

If you are evaluating contractor payouts in South Africa, do not start with rail selection. Start by separating what the South African Reserve Bank has clearly published from what still needs direct validation for a private platform.

Pay Contractors in UAE with Clear WPS Boundaries and UAEFTS Checks

Write down the exact flow you want to launch in the United Arab Emirates: who contracts with the worker, who holds funds, who instructs the payout, and where the money actually moves. If you cannot explain it on one page, you are not choosing a payout feature yet. You are still defining a regulated operating model.