Quick Answer

Start with a country register and an "unknown" block state, then enable only where Legal and Finance approvals are documented. Late fee automation marketplace invoices country execution works when due-date breach, grace period, and start-date logic are tied to fee basis rules and ledger postings, with tests that prove both charge and suppression behavior. Use weekly control checks on DSO, waiver rate, and dispute rate to decide whether to expand or pause each market.

Set Country Rules Before Automating Late Fees#

Late fee automation in marketplace operations is first a legal and accounting control decision, not a convenience feature. When a fee is triggered automatically, you are deciding whether the charge is allowed and how it will be posted, reconciled, and explained later.

A late fee changes more than invoicing UX. Accounts Receivable (A/R) is money customers owe for delivered goods or services, so automated fees change expected collections. Reconciliation depends on fee events lining up across the invoice, ledger, and settlement records. If they do not, reporting gets less reliable and it becomes harder to reconstruct what happened in the audit trail.

The legal side is country-specific in practice. In the EU commercial context, late payment means payment not made within the contractual or statutory period, and it is tied to liquidity and financial management risk. Businesses can be entitled to interest and compensation when payment is late. Directive 2011/7/EU is implemented through Member State transposition measures, so treating Europe as a single rule toggle can be a risk signal. A practical country-by-country setup should make these control points explicit:

- what rule is allowed in each jurisdiction

- when the fee starts, including grace period and start date

- how the fee is represented, typically as a separate invoice line item

- how exceptions are handled and recorded without breaking reconciliation

You should tie implementation to a measurable collections outcome. Days Sales Outstanding (DSO) measures average collection time on credit sales, commonly over a 365-day period. If fees are being applied and DSO does not improve, review policy design, exception handling, and automation configuration before assuming the process is working.

A defensible rollout starts with one rule: do not launch a country until policy, posting logic, and evidence are documented together. At minimum, keep a country record with the rule basis, owner, effective date, and a test result showing both fee creation and fee suppression work as intended. That is the standard this guide targets: country-aware enforcement that is consistent, reconcilable, and audit-ready.

For a step-by-step walkthrough, see Accounts Receivable Automation for Platforms to Collect from Enterprise Buyers at Scale.

Define late fee automation in marketplace operations#

Late fee automation is preconfigured rule enforcement. The system applies a late fee to eligible overdue invoices instead of relying on someone to add charges case by case.

A late fee is an extra charge on an invoice paid after its due date, and "late payment" means payment outside the contractual or statutory payment period. The trigger should map to the invoice payment terms and the rule configured for that jurisdiction. In practice, the core setup is:

- Grace period: how many days after past due before assessment starts

- Start date: only invoices dated on or after this date are eligible

- Fee basis: flat fee or percentage fee

- Posting behavior: add the fee as a separate invoice line item so the charge is explicit

For marketplace finance teams, the key artifact is the rule record behind that line item: what qualifies, what does not, and why a fee was suppressed when criteria were not met. Auditability depends on system logging for rule changes and fee events, not just final invoice totals.

Country limits can also change what is allowed, including fee type and amount. That variation is material. The EU framework includes interest of at least 8 percentage points above the ECB reference rate plus a €40 minimum fixed sum, while UK B2B statutory interest is framed as 8% plus the Bank of England base rate.

For broader AP workflow tradeoffs in marketplace finance, see AP Automation vs. Manual AP Processing: A Cost-Benefit Analysis for Marketplace Operators.

Assign legal and financial ownership before any rule goes live#

Once trigger logic is clear, ownership is the next control. Do not enable automated late fees in a market until Legal signs off on interpretation and Finance signs off on posting, reversal, and settlement treatment.

Marketplace liability can split across parties, so ownership needs to be explicit before go-live. EU VAT guidance shows platforms can be treated as deemed suppliers in some cases, and can still carry recordkeeping duties even when not deemed suppliers. Washington marketplace-facilitator rules show mixed allocation too. Facilitators are treated as agents for covered retail sales, must collect and remit tax on taxable facilitated sales, and in some relief cases the seller is solely liable for uncollected tax. For late fees, the lesson is simple: unclear ownership can create hidden liability risk and value shifts during exception handling and settlement.

Split the decision, not just the task list#

Use three named owners because these are three different decisions.

| Function | What they own | What must be explicit before go live |

|---|---|---|

| Product | Rule implementation and country enablement | Eligibility logic, suppression logic, start date, and the gate that blocks launch without required approvals |

| Legal | Late fee policy and country exceptions | Terms text, whether automation is allowed for that market and party structure, and who can approve exceptions |

| Finance | Posting, reversal, and settlement treatment | Which legal entity books the fee, which ledger receives it, how waivers are recorded, and settlement impact |

Keep waiver outcomes under Finance ownership, or a finance-led committee, not front-line support, so revenue-impacting exceptions stay controlled and auditable. PCAOB language assigns management responsibility for effective internal control over financial reporting, and GAO guidance emphasizes control responsibilities across organizational levels.

Define the balance-sheet boundary before exceptions happen#

Exception handling is often where risk shows up, not fee math. If a fee is assessed, then waived, disputed, or paused after settlement timing has moved, unclear ownership can leave unintended receivables or unreconciled adjustments.

Set one hard checkpoint: for each country and model, Finance should confirm the posting path by legal entity tied to the active ledger. Oracle's late-charge guidance reflects this control by applying separate late-charge invoices per legal entity associated with the active ledger. The same principle applies even if your tooling is different.

Require a country evidence pack#

Do not enable a country without an evidence pack linked to the audit trail. NIST's audit-trail definition is a practical baseline: record system and application activity, including user activity. Minimum pack contents are below. If any item is missing, keep the country disabled. No legal interpretation, no posting design, no automation.

| Evidence item | What to include |

|---|---|

| Terms text | Current terms text for that country and counterparty type |

| Approvers | Named Legal approver and Finance approver, with approval date |

| Posting memo | Legal entity, ledger, settlement treatment, and reversal method |

| Exception notes | Country exception notes, including unresolved points |

| Audit notes | Where rule changes, fee events, and waivers are logged |

Those are the minimum contents. If one is missing, keep the country disabled.

Related: How to Calculate LTV for a Two-Sided Marketplace: Buyer LTV Seller LTV and Platform LTV.

Build a country rule register your system can enforce#

Treat your country rule register as a production control, not a reference sheet. Once Legal and Finance approvals are assigned, this is the system layer that keeps fee behavior consistent at runtime and auditable later.

Store legal differences as enforceable fields#

Use fields your engine can execute directly: jurisdiction, allowed fee basis, notice requirement, grace period, start date logic, and escalation constraints. If a legal point cannot be mapped to an enforceable field, it is not ready for automation.

| Register field | Runtime behavior | Why it matters |

|---|---|---|

| Jurisdiction | Select the correct rule set before fee logic runs | Late-fee limits are jurisdiction-specific; avoid one global rule. |

| Allowed fee basis | Allow only the approved charge structure | US guidance allows flat or percentage structures only within state limits. |

| Notice requirement | Block fee creation until notice conditions are met, if required | In covered EU commercial transactions, interest can be due without a reminder. |

| Grace period | Delay fee assessment until the configured wait period passes | Grace period is a core automation input. |

| Start date | Control when automation becomes active | Prevents accidental backdating and clarifies activation behavior. |

| Escalation constraints | Restrict reminders, collections, or handoff by jurisdiction | Keeps follow-up behavior aligned with the approved country rule set. |

Germany and the United States show why this has to be specific. Germany late-payment interest is tied to Section 288 BGB, and the Bundesbank basic rate framework updates on 1 January and 1 July each year. In the US, limits can vary by state, so a single national row is often too coarse.

Make unknown a hard state#

Keep an explicit unknown status for incomplete rules. As an internal control policy, unknown should block automatic late-fee creation and prevent enablement until Legal confirms the missing point.

Track the blocker in a short unresolved field, such as notice requirement pending, state cap not confirmed, or scope unclear. That turns legal uncertainty into an implementation gate instead of a vague note.

Add implementation columns to prevent drift#

Add operational columns to every row: enabled status, effective start date, owner, and last review date. Without them, stale policy can stay active after legal interpretation or operating model changes.

Activation timing also needs to be explicit. QuickBooks, for example, applies automatic late fees to overdue invoices starting the day after activation, while older invoices may need manual line-item handling. Your register should state how pre-activation overdue invoices are handled so treatment stays consistent.

Require tests for creation and suppression#

Do not mark a country enabled unless it maps to tests that prove both fee creation and fee suppression behavior. Minimum checkpoints are:

- creation only after due date, after grace period, and on or after start date

- suppression when jurisdiction is

unknown, when required notice conditions are unmet, or when invoices are outside active scope - defined suppression or manual path for invoices predating activation, where retroactive automation is not supported

This is what makes audits and disputes defensible: documented rules, explicit approvals, and test evidence for both when a fee is charged and when it is not.

Choose flat fee or percentage fee with explicit decision rules#

After legal review confirms what a country allows, choose the clause shape with a policy rule and test it on your own overdue data. Do not rely on a single default heuristic. Evaluate both flat fee and percentage fee clauses against your invoice mix, dispute patterns, and approved legal limits. In some jurisdictions, the law already narrows the structure you can apply.

| Clause type | Invoice size variance | Dispute risk | Fairness perception | Operational simplicity |

|---|---|---|---|---|

| Flat fee clause | One fixed charge applies per overdue invoice; policy may need limits for very small or very large balances | Can still be disputed depending on contract terms and amount | Easy to understand; acceptance can vary by customer | Usually straightforward to configure and audit per overdue invoice |

| Percentage fee clause | Fee amount scales with overdue balance based on an approved rate | Can still be disputed, including rate, timing, or rounding | Often presented as proportional, but acceptance can vary | Needs clear settings for rate, timing, rounding, and approved limits |

| Statutory or fixed-compensation model where law prescribes structure | Structure is defined by law where applicable | Lower policy ambiguity if you mirror the legal basis | Usually easier to defend because it follows defined legal rules | Clear to operate when legal formula or amount is bound directly in the fee engine |

Let jurisdiction narrow choice first#

Do not treat flat versus percentage as only a product preference. In UK B2B late payment, statutory interest is 8% plus the Bank of England base rate, and fixed recovery charges are £40 / £70 / £100 by debt band. The UK framework also states enterprises should pay within 60 days, unless they expressly agree otherwise and the term is not grossly unfair. Under Directive 2011/7/EU Article 6, when late-payment interest is payable, the creditor is entitled to a minimum fixed EUR 40.

In practice, some countries leave room for product choice and others do not. EU countries may also keep or introduce rules more favorable to creditors than the directive baseline, so country-level rules should drive configuration.

Bind approved limits directly to automation#

Where legal review allows caps, floors, or fixed statutory amounts, encode them in the fee engine. Keep manual overrides as exceptions with controlled approval.

QuickBooks supports Amount and/or Percent (%) and optional grace period days, and also warns that legal limits can apply to fee amount and type. Your country rule should map directly to executable settings for allowed basis, approved limits, and override controls.

Simulate before launch on historical overdue invoices#

Before launch, run a simulation on historical overdue invoice data to surface operational edge cases and likely waiver points. Treat the simulation as a risk check, not a certainty forecast.

At minimum, compare outcomes by country, invoice band, and customer cohort under each clause design. Review outliers that teams would likely waive, then adjust the clause logic before launch.

Design invoice lifecycle and posting logic end to end#

Once your fee basis is approved, lock one explicit lifecycle before launch. Ambiguous sequencing creates duplicate fee postings, false settlement signals, and reversals that are hard to defend.

Make the trigger order explicit#

Use one ordered path for every invoice: issuance, due-date breach, grace-period check, fee trigger at the approved start date, invoice line-item posting, then reminder or escalation. Each step should depend on the prior state being true in the ledger, not just in a notification service or background job.

| Stage | Article detail |

|---|---|

| Issuance | Start of the ordered path for every invoice |

| Due-date breach | Comes after issuance in the ordered path |

| Grace-period check | Comes after the due-date breach |

| Fee trigger | At the approved start date, after finalization, due-date breach, and a passed grace-period rule |

| Invoice line-item posting | Comes after the fee trigger in the ordered path |

| Reminder or escalation | Comes after invoice line-item posting |

If you use Stripe-style states, enforce status gates. A new invoice starts as draft, and finalization moves it to open. Fee logic should not attach to a draft invoice. It should run only after finalization, due-date breach, and a passed grace-period rule.

Do not treat failed collection as settlement. If payment fails or is incomplete, the invoice remains open, so reminders and escalation can continue while settlement logic waits for actual payment or an approved adjustment.

Before go-live, run a simple control test for each enabled policy rule: one invoice that should create a fee and one that should suppress it. Verify event time, start date, posted line item, and resulting invoice status.

Let the ledger decide what happened#

Make the ledger the source of truth for every fee event. Every late-fee posting should create traceable journals tied to the triggering invoice, because reconciliation depends on matching recorded transactions to external statements.

Reconciliation alone does not prove settlement finality, but deterministic settlement still requires complete posting records for fee creation, payment application, waiver, and reversal. If an invoice moves to void or uncollectible, reporting and accounting treatment should reflect that state change. If a fee is real enough to collect, it is real enough to journal and reconcile.

Build duplicate protection into every retry#

Treat duplicate defense as mandatory. Webhook endpoints can receive the same event more than once, retries can continue for up to 3 days, and finalization or send can still be attempted within 72 hours when acknowledgment is not received. Use both controls together. Event dedupe protects inbound processing, and idempotency protects outbound create and update calls:

- Store processed event IDs and skip repeats.

- Send an idempotency key with fee-creation requests so retries return the original result instead of creating duplicates.

Define reversal paths before the first dispute#

Define reversal as a controlled accounting path. If you need to reduce amount due without recording payment, use a credit note so receivables are adjusted correctly.

Limit reversal authority to named roles and keep every action in the audit trail. Xero, for example, restricts delete and void actions on customer credit notes to specific roles.

Keep evidence complete and durable: who posted the fee, who reversed it, what changed, and when. QuickBooks audit-log events are available for two years, which can serve as a practical baseline for dispute handling. Before rollout, map each trigger, retry path, and ledger posting to an implementation checklist: Review the Gruv docs.

Set reminders, escalation, and waiver controls that actually get paid#

Once fee posting is stable, collections behavior needs the same discipline. Put the late fee policy in your terms, then enforce it with scheduled reminders, clear escalation stages, and stop rules tied to status changes, including dunning pauses or approved waivers.

Tie outreach to overdue age#

Use overdue age to drive outreach. A dunning-level model keeps each overdue invoice on defined stages based on days in arrears, regardless of what your system calls those stages.

Focus on fixed cadence by invoice age, not a universal day pattern. Map each stage to a specific action type, such as email reminder, phone call task, or collection letter. Dynamics 365 supports this broader ladder, and QuickBooks supports reminder timing up to 90 days before or after due date, including second and third reminders.

Before launch, age a test invoice through every stage and confirm each reminder triggers once, in order, and stops when status changes.

Pause and stop on real state changes#

Escalation should stop on real ledger states: payment posted, approved waiver posted, or intentional pause. NetSuite's pause and resume dunning model at customer, invoice, or invoice-group level, with reason and reason detail fields, is a practical control for disputes, billing queries, or temporary holds.

If pause and resume is not explicit, teams can work around the system and auditability can drop. Keep the pause reason visible on the invoice record and require a resume event so items do not stay paused indefinitely.

Also enforce legal-rule checks in escalation content. In the United States, late-fee limits can vary by state, so templates should be rule-checked before stating amounts. In the UK, businesses may add fixed recovery sums on top of interest for late commercial payments. Under Directive 2011/7/EU, statutory interest in commercial transactions can apply without a reminder first.

Lock down waivers before they leak revenue#

Treat waivers as controlled financial adjustments, not informal customer-service actions. Oracle Receivables' adjustment approval limits model is the right pattern: per-user approval thresholds and pending status until an authorized approver approves or rejects.

Require a reason code for each waiver or write-off. JD Edwards requires write-off reason code 03B/RC when part of an invoice is written off; your process should be just as explicit about approver, reason code, detail, and linked case evidence.

If you allow commercial flexibility, define limits and approval routing in advance. Any waiver path without pending status, reason coding, and approver trail can create quiet revenue leakage. Related reading: Platform Revenue Split Calculator for Modeling Marketplace Take Rates.

Handle disputes and misapplied fees without breaking your books#

Use a dispute workflow that can pause collection actions on the disputed item where your system supports it, while preserving history, then correct through controlled entries instead of rewriting posted records. Keep dispute codes separate from waiver or exception codes in your own process so root-cause tracking stays usable.

Freeze actions without deleting evidence#

When a dispute is open, apply an item-level dunning block where your system and policy support it. SAP supports rules-based dunning blocks for disputed items, and the 3,000 EUR threshold shown in SAP documentation is an implementation example, not a universal rule.

Keep records traceable during correction. Stripe's invoice-void behavior is a useful model for preserving a paper trail, and Xero's History and notes view shows date-stamped, user-level change history. As an operational check, confirm the original line item remains visible, the dunning stop is visible, and dispute comments and history stay attached to the same transaction.

Also set and test your finance-charge behavior explicitly. Oracle documents finance-charge handling on disputed items as configurable, so define whether disputed items continue accruing finance charges during review.

Separate error types so you can measure them#

At minimum, code disputes so you can distinguish operational errors from policy exceptions in your own process. Operational errors can include calculation logic, duplicate triggers, or mapping issues. Policy exceptions can include approved waivers or commercial concessions.

Oracle Receivables supports this structure with Manage Disputes for all or part of a transaction amount, dispute reason and type fields, approval comments, and notes attached to the transaction. It also supports custom dispute-type coding via ORA_IEX_DISPUTE_TYPE_CODE, which helps separate internal error classes from approved exceptions for reporting and remediation.

Correct misapplied fees with standard entries#

Standardize one correction path per error class and use it consistently. In QuickBooks, a credit memo reduces an open balance immediately, and in Oracle, Credit Memo Rebill reverses prior receipts and adjustments and creates a credit memo for the invoice amount.

Avoid direct edits to posted charges without a reversal pattern. As an internal control, verify that the original charge remains traceable, the correcting entry nets as intended, and the customer balance matches the intended outcome.

After incidents, run a short internal review so recurring fee errors do not turn into month-end cleanup work.

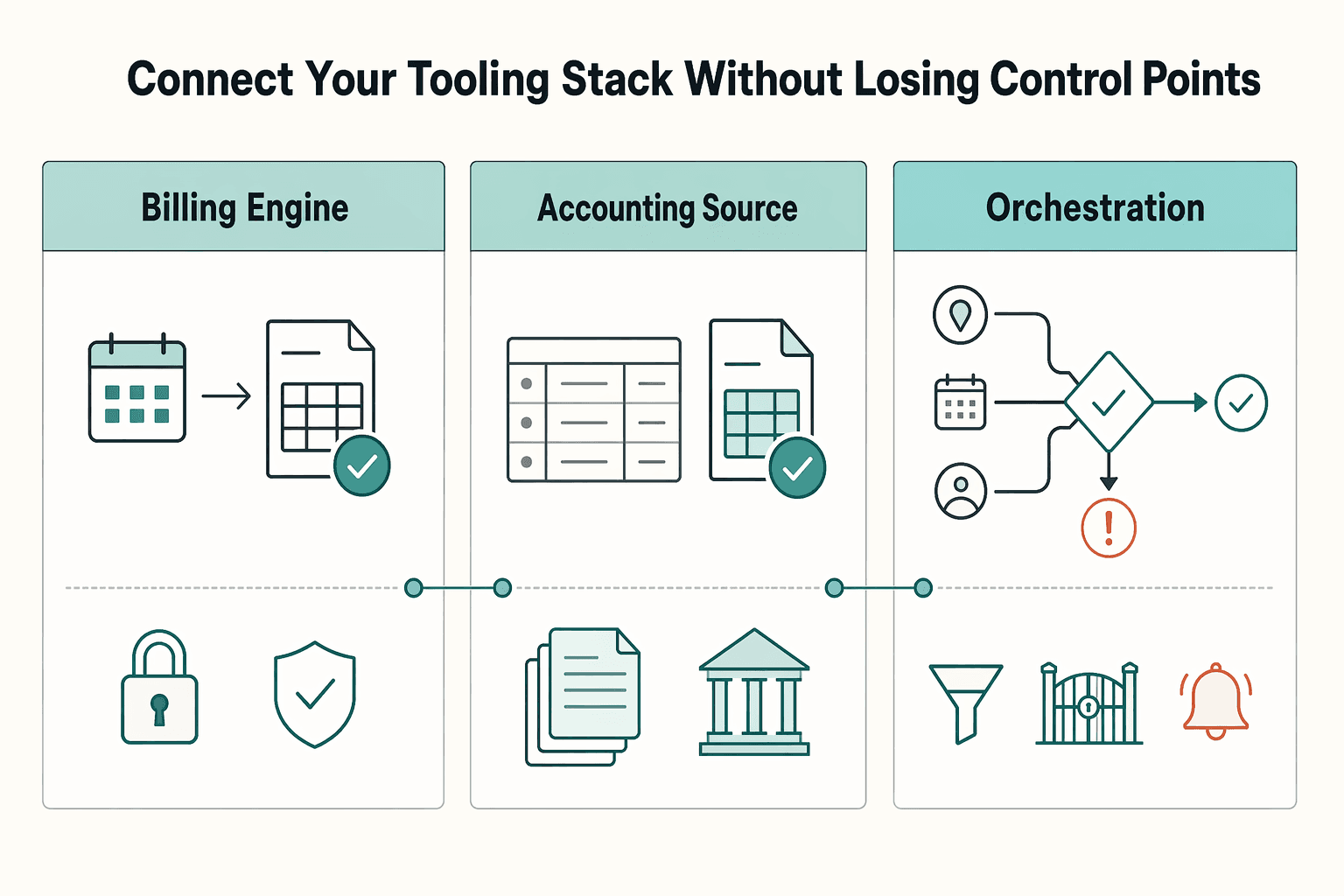

Connect your tooling stack without losing control points#

Assign one owner per layer so controls do not get bypassed. Let the billing engine decide whether a fee is calculated and created, keep accounting as the system of record for the posted invoice, and use Zapier or Make to route data and enforce gates. If orchestration can create a fee before country eligibility and approval status are checked, the control has already failed.

| Layer | Tool examples | Use it for | Do not let it do on its own |

|---|---|---|---|

| Billing engine | Invoiced, Stripe Billing | Trigger overdue logic, apply conditions, and initiate fee handling | Skip policy approval checks just because an invoice is overdue |

| Accounting source | QuickBooks, Xero | Read or write invoice records for posting and reconciliation | Become the place where fee policy is decided ad hoc |

| Orchestration | Zapier, Make | Route events, apply filters, stop non-eligible items, log outcomes | Bypass billing rules with a direct create action |

The pre-create gate is the key control point. Stripe Billing automations use triggers, filter conditions, and actions, and Invoice is overdue is a supported trigger. Zapier Filters and Make filters can stop downstream steps, so use that checkpoint to require approved country, approved fee policy version, and the correct account or connected-account eligibility. Do not assume one Stripe account's eligibility applies everywhere, because eligibility can vary by country, currency, product setup, and connected account.

Expect timing drift across tools and design checks for it. Invoiced supports automated late-fee policies with fee type, grace period, and start date controls, and adds late fees as a separate invoice line item. Invoiced integrations with QuickBooks Online and Xero sync new data once per hour, so checks that expect immediate reflection in accounting can create false exceptions. Test one happy path and one blocked path each release: an approved overdue invoice creates a fee line item, and a non-approved overdue invoice is stopped and logged.

Require step-level observability, not just "it ran." Track checkpoints such as triggered, filter passed, fee created, posted to accounting, or blocked with reason. Zap history in Zapier and scenario history in Make can help catch silent drops, but only if someone reviews them. If you are tightening the collections side at the same time, The Best Ways to Handle Late-Paying Clients is a useful companion.

Monitor weekly control metrics and intervene early#

Weekly KPI review is where automation turns into an operating control. Track a compact set: Days Sales Outstanding (DSO) trend, an internal fee-assessment check rate, waiver rate, dispute rate, and Accounts Receivable (A/R) aging buckets. Because DSO is the average number of days needed to collect after a credit sale, judge direction over time rather than a single week. For internal fee-assessment checks, sample new late payment fee items and verify that the due-date breach, grace period, country eligibility, approved policy version, and posted amount match the record.

| Metric | How to review it |

|---|---|

| DSO trend | Judge direction over time rather than a single week |

| Internal fee-assessment check rate | Sample new late payment fee items and verify due-date breach, grace period, country eligibility, approved policy version, and posted amount match the record |

| Waiver rate | If it jumps in a segment, treat that as an intervention signal |

| Dispute rate | If it jumps in a segment, treat that as an intervention signal |

| A/R aging buckets | Use due within 30 days, past due 31 to 60 days, and past due 61 to 90 days |

Use aging buckets that force action, such as due within 30 days, past due 31 to 60 days, and past due 61 to 90 days. If waiver or dispute rates jump in a segment, treat that as an intervention signal and consider pausing further automation expansion there until policy wording and execution logs are reviewed. This can help separate real customer pushback from execution defects like wrong start dates, bad cohort mapping, or outdated policy logic.

Review outcomes by country and payer cohort, not only global averages. Keep each country, including Germany and the United States, as a separate operating view. Evaluate each against its own legal context: the EU late-payment framework for commercial transactions includes a fixed €40 per invoice compensation amount, while the U.S. federal prompt-payment source in this research is limited to Executive branch procurement contracts.

Assign explicit ownership for remediation. Finance should own the KPI pack and accounting impact. Ops should own execution checks and follow-through. Every major policy change should be logged with date, segment, trigger metric, evidence reviewed, owner, decision, and next review date.

Conclusion#

Treat late-fee automation as a compliance and accounting control. A setup is reliable when you can show which jurisdiction rule applied, whether an invoice qualified as a late payment under the applicable terms, who approved exceptions, and what was posted, reversed, or suppressed in the audit trail.

Late-payment rights are jurisdiction-specific, not global. Under Directive 2011/7/EU (16 February 2011), in commercial transactions where late-payment interest is payable, the creditor is entitled to a minimum fixed sum of EUR 40. Statutory interest is set at the reference rate plus at least 8 percentage points. UK guidance is also explicit: businesses can claim interest and debt-recovery costs on late commercial payments, and agreed payment windows must usually be within 30 days for public authorities or 60 days for business transactions.

The practical standard before rollout is straightforward: prove policy logic, exception handling, and record integrity in the same operating model. In NIST terms, an audit trail records who accessed a system and what operations they performed over time. Your fee engine should let you trace rule creation and edits, effective dates, postings, reversals, waivers, and manual interventions.

Before enabling a market, test the rules across eligible and non-eligible scenarios to confirm charge and suppression behavior and verify traceable records. Failure modes to check for include stale jurisdiction logic after terms changes, duplicate fee events after retries, waivers approved outside named authority, and emergency production changes without re-testing. In financial-sector contexts, FFIEC guidance is a useful operating reference: designate a group to approve emergency changes and still test, model, or simulate before release.

If you want a clean next move, do it in this order:

- Maintain a jurisdiction register (for example: legal basis, fee basis, effective date, named owner, and approval status) per market.

- Test fee creation and suppression on sample invoices, then verify postings and reversals in both system records and the audit trail.

- Launch market by market with explicit approval gates, not a global switch.

This will not remove legal judgment or collection friction, but it gives you a controlled way to expand while keeping compliance objectives and exceptions visible.

Frequently Asked Questions

How do we automate late fees on marketplace invoices without creating legal risk by country?

Start with a country rule register, not a global toggle. Track country status, fee basis, grace period, effective date, approval owner, and an explicit unknown state that blocks automation until legal review is complete. Keep that guardrail because fee type and fee amount can be jurisdiction-limited.

When should we use a flat fee instead of a percentage fee?

Do not pick one model globally across countries. Choose the fee structure only after country-level legal review and contract-language review. For U.S. setups, test reasonableness carefully because preset charges that are unreasonably large can be treated as penalties.

What exactly must change in our setup between Germany and the United States?

Use separate legal configurations for Germany and the United States. In Germany, qualifying commercial transactions fall within the Directive 2011/7/EU framework, including Article 6’s minimum fixed compensation of EUR 40 when late-payment interest is payable, and BGB §288 is commonly cited for nine percentage points above the base rate plus a 40 Euro lump-sum claim in non-consumer remuneration cases. In the United States, enforceability analysis is shaped by state law, so keep separate contract review, reasonableness review, and approval records.

Why are late fees listed on invoices but still not getting paid?

A fee line item alone does not remove collection friction. U.S. B2B data highlights administrative inefficiencies, invoice disputes, and customer cashflow issues as common late-payment drivers. Tool behavior can also block expected outcomes: for example, automatic late fees may apply only up to six months, and older invoices may require a manual late-fee line item.

Which controls should Finance review every week to catch policy failure early?

Use a compact weekly control pack: DSO, fee-assessment accuracy, waiver rate, dispute rate, and A/R aging buckets. Read DSO as a trend, since it measures how long collection takes after a sale. Validate a sample of newly charged invoices against due-date breach, grace period, country eligibility, approved policy version, and posted amount, then pause expansion where waiver or dispute rates spike.

What should we do when country rules are unclear or legal guidance is incomplete?

Treat unclear jurisdictions as ineligible for automated fees. Keep fee logic disabled until you have documented legal interpretation, approved terms language, owner signoff, and a dated test proving both charge and suppression behavior. Continue principal-collection reminders while fees remain off, and log why the country is still marked unknown.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 1 external source outside the trusted-domain allowlist.

- eur-lex.europa.eu/EN/legal-content/summary/combating-late-paym...trusted

- eur-lex.europa.eu/legal-content/EN/NIMtrusted

- europa.eu/youreurope/business/finance-funding/making-r...trusted

- guides.gaoinnovations.gov/greenbook/2025/principle-10-design-control-a...trusted

- gov.uk/late-commercial-payments-interest-debt-recov...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Best Ways to Handle Late-Paying Clients

If you run a business of one, you need a repeatable system you can actually use.

AP Automation vs Manual AP Processing for Marketplace Operators

For marketplace operators, this is not a generic AP explainer. The real choice is whether you should stay with manual AP, move to rules-based automation, adopt AI-powered automation, or run a staged hybrid while volume, controls, and integrations catch up.

How to Calculate LTV in a Two-Sided Marketplace for Buyer, Seller, and Platform Decisions

In a two-sided marketplace, many teams look at buyer-side and seller-side value separately, then compare each view to the relevant Customer Acquisition Cost instead of forcing everything into one blended ratio. Treat Lifetime Value as an operating number, not a spreadsheet guess.