Quick Answer

Start by treating hiring contractors UK IR35 as an ownership and controls problem: name the decision owner, collect a repeatable evidence pack, and block payout setup when core facts are missing. The article’s practical checkpoints are business structure, chain role, Self Assessment readiness, and account reactivation status for existing filers. It also anchors operations to HMRC dates, including notification by 5 October where required and payment due by 31 January, so teams can escalate before reconciliation fails.

Set up IR35 ownership and payout controls before you hire#

If you are hiring contractors in the UK, compliance issues can come down to unclear ownership, thin records, and money moving before basic checks are done. The practical question is not just "do we know the acronym?" It is "what do we need on file, who signs off, and what makes us stop?"

That matters because HM Revenue and Customs (HMRC) sets clear process expectations. Where a return is needed under the listed conditions, HMRC must be told by 5 October 2025 for the prior tax year running from 6 April 2024 to 5 April 2025. Late notification can lead to a penalty. HMRC guidance also says taxpayers should keep records, such as bank statements or receipts. That is the standard to design for: dated obligations, named records, and evidence that still makes sense when someone reviews it later.

This article uses three practical tests for every control option:

- Ownership

Name the person or team that can approve, block, or escalate a UK contractor payout path. A good checkpoint is whether they can explain what evidence is required before activation, not just after a problem appears. A named owner can hold the line when facts are missing. A shared inbox usually cannot.

- Evidence

Verbal reassurance is not enough when registration or filing status is part of the picture. HMRC guidance is explicit that taxpayers need to keep records such as bank statements or receipts. If someone is waiting on a Unique Taxpayer Reference (UTR), or needs to reactivate an existing Self Assessment account before filing, that status should be clear in the file. What matters here is traceability: you want a record set that shows what was known, when it was known, and what the team did next.

- Escalation before payout

The cheapest control is often a pause at the right moment. A practical risk is onboarding on the assumption that tax admin is "in hand," only to find the payee is still waiting for a UTR or has not reactivated an existing Self Assessment account. GOV.UK says filing without reactivating an existing account may delay the return. Timing matters: escalate before payout setup, not after reconciliation breaks.

So this is a practical guide for operators, not a theory piece. The aim is to help you choose the lightest controls that still stand up to HMRC-facing compliance checks, without burying the team in forms, approvals, and duplicate reviews. Related reading: How to Pay Contractors in Malaysia: DuitNow and Bank Negara FX Compliance for Platforms.

How to choose an IR35 control setup for your platform#

For hiring contractors UK IR35 controls, start with ownership, not theory: for each worker, name who gathers facts, who reviews them, and who can block payout setup when the file is incomplete. If ownership is unclear, do not scale onboarding.

Use three filters before picking a setup. First, map your role in the chain (client, end client, agency, supplier, or payment layer). Second, size for engagement volume so your review model still works as volume grows. Third, record whether the UK counterparty is in a small-business or medium/large-client context, and route the legal effect to specialist review instead of guessing.

Quick comparison#

| Control option | Owner team | Required inputs | PAYE and NICs impact surface | Escalation threshold |

|---|---|---|---|---|

| Manual case review | Legal or compliance | Role in chain, business structure, contract set, named reviewer, filing-readiness facts | Potentially material if status decisions affect payment treatment | Missing owner, unclear intermediary, conflicting file facts |

| Ops intake plus compliance checkpoint | Operations intake; compliance exceptions | Structured intake, entity type, filing/registration readiness, client-size flag, approver | Potentially material if intake errors reach payout setup | Missing business structure, unclear chain role, unresolved filing status |

| Gated self-serve with hard stops | Product/ops rules with compliance oversight | Required fields, document upload, named decision owner, timestamped approval | Broad operational exposure if gates or overrides fail at scale | Unknown owner, override request, incomplete evidence pack |

Three workable setups#

- Manual case review

Best for lower-volume or messy chains. The pro is judgment on full context; the con is slower throughput and reviewer inconsistency. Minimum evidence should be explicit: business structure, chain role, and filing-readiness facts. GOV.UK states business structure can affect tax and legal responsibilities, and if someone is a sole trader, registration is through Self Assessment with a National Insurance number required to register. A common failure mode is approving while the file still shows registration as incomplete.

- Ops intake plus compliance checkpoint

Best for medium volume when you want speed with a real review gate. The pro is higher throughput; the con is risk from weak intake quality. Minimum evidence should be verifiable, not only self-certification: declared structure, contracting chain, first-time filing status, and whether an existing account must be reactivated. GOV.UK says first-time filers must register for Self Assessment before using online filing, and returns may be delayed if an existing account is not reactivated first. Failure mode: payout pressure before filing readiness is clear.

- Gated self-serve with hard stops

Best for higher volume when controls must be systematic. The pro is consistency; the con is concentrated risk if rules or overrides are weak. Hard stops should include missing chain role, no named decision owner, conflicting structure data, or incomplete filing-readiness evidence. Keep dated obligations visible in the workflow where relevant, including HMRC notification by 5 October 2025 when required and payment by 31 January. Failure mode: manual overrides becoming the default path.

Related: Hiring Contractors in the Philippines: Compliance Payouts and Tax Obligations.

Best for low-volume UK engagements with high legal sensitivity#

Use manual review when UK engagement volume is low and you need defensible case-by-case judgment more than speed. This is a practical fit for early-stage teams handling a small number of intermediary arrangements where each file needs careful review.

What this model is good at#

- Best for: low-volume onboarding where one reviewer can be accountable for each decision.

- Pros: stronger judgment on complex files and clearer records using HMRC/GOV.UK language.

- Cons: slower cycle times and inconsistent outcomes if reviewers apply different standards.

- Concrete use case: a platform onboarding a small UK cohort where legal interpretation risk is higher than throughput risk.

Minimum file for this model#

For each engagement, collect the same core pack every time:

| File item | What to collect | Section note |

|---|---|---|

| Contract chain | The contract chain and named intermediary relationship, with one reviewer accountable | Collect the same core pack for each engagement |

| Business structure and filing-readiness facts | The declared business structure and whether the contractor is registering for Self Assessment for the first time or reactivating an existing account | These are valid readiness checkpoints |

| Verification point | A Unique Taxpayer Reference (UTR), registration confirmation, or a clear note on why that evidence is not applicable | If payout readiness depends on unresolved HMRC administration, pause activation |

- the contract chain and named intermediary relationship, with one reviewer accountable

- the declared business structure and filing-readiness facts, including whether the contractor is registering for Self Assessment for the first time or reactivating an existing account

- a verification point where relevant, such as a Unique Taxpayer Reference (UTR), registration confirmation, or a clear note on why that evidence is not applicable

Set one hard rule for consistency: if payout readiness depends on unresolved HMRC administration, pause activation. GOV.UK says you must tell HMRC by 5 October 2025 in the listed Self Assessment scenario, late notification can lead to a penalty, and filing without reactivating an existing account may delay the return. Those are not IR35 determination tests, but they are valid readiness checkpoints.

Best for mixed client sizes across one platform#

For mixed client portfolios, use a gated intake route before activation so each file is classified by evidence, not assumptions. The core control is simple: confirm the business structure first, then send the file to the right owner.

Do not let teams infer off-payroll client-size rules from sales notes, logos, or a counterparty saying they are "small." The sources for this section do not define that test. If your internal policy uses client size to split responsibility, require the exact evidence that policy names and escalate when evidence is missing or contradictory.

The routing split to use#

| Route | When it applies | What to capture or do |

|---|---|---|

| Limited company or PSC route | The intermediary is presented as a company | Capture company identity, contract chain, and named payee entity, then route to the team handling company-based determinations |

| Sole trader route | The worker says they are a sole trader and expects to earn more than £1,000 in a tax year (6 April to 5 April) | Record registration status, plus UTR where available or a dated explanation of what is still pending |

| Contradictory or missing route | The declared structure, payee details, and HMRC admin status do not line up | Stop setup and escalate to compliance review before first payout |

- Limited company or PSC route

GOV.UK says a limited company is legally separate from the people who own it and is run by one or more directors. If the intermediary is presented as a company, capture company identity, contract chain, and named payee entity, then route to the team handling company-based determinations.

- Sole trader route

GOV.UK says most businesses register as either a sole trader or a limited company, and that someone registers as a sole trader by registering for Self Assessment. If the worker says they are a sole trader and expects to earn more than £1,000 in a tax year (6 April to 5 April), record registration status, plus UTR where available or a dated explanation of what is still pending.

- Contradictory or missing route

If the declared structure, payee details, and HMRC admin status do not line up, stop setup and escalate to compliance review before first payout.

This approach adds onboarding friction, but it prevents policy drift and reduces rework. It also aligns with the grounded point that business structure affects tax and legal responsibilities.

One checkpoint is critical: do declared structure, Self Assessment status, and payout recipient match the file record? Keep that evidence in the file. GOV.UK also notes that someone already registered for Self Assessment may need to register again as a sole trader for Class 2 National Insurance contributions, and that filing without reactivating an existing account may delay the return. If evidence is absent, unclear, or conflicting, block payout setup and escalate.

Best for agency and supplier-heavy contracting chains#

Where your marketplace sits in the middle of agency and supplier relationships, the key control is straightforward: require a contract-chain evidence pack before activation, and hold the file if any party role or entity identity is unclear. In multi-entity UK contractor setups, the first failure is often not the status call itself, but losing track of who the parties are, what each party does, and which engagement terms were handed off.

Treat the chain as evidence, not narrative. Notes like "supplier engaged" or "agency model" are not enough on their own. Capture named entities, documented roles, and recorded handoffs so that if ownership is challenged later, you can trace the file without rebuilding it from email threads.

| Evidence pack item | What to capture | Verification checkpoint | Common failure mode |

|---|---|---|---|

| Intermediary entity details | Legal name, business structure, payee name, and where that entity sits in the chain | Check that the declared structure matches the payout recipient and contract record | Agency named in the contract, but payment is requested to a different entity |

| Role definitions | Plain-language role for client, end client, agency, supplier, and worker (contractor) | Confirm the same labels appear across onboarding, contract metadata, and approval notes | Teams use "client" to mean different parties, so escalations go to the wrong owner |

| Determination output | The status or review result your policy requires, plus timestamp and responsible reviewer | Make sure the output is attached to the correct engagement and not a reused prior file | Old decision copied forward after the chain changed |

| Handoff confirmations | Written confirmation of what was sent from client to agency to supplier, and when | Check dates, version names, and recipient names line up | A later contract amendment never reaches the downstream party handling setup |

One grounded detail is worth enforcing. GOV.UK says most businesses register as either a sole trader or a limited company, and that business structure affects tax and legal responsibilities. If an agency or supplier is presented as a company, the file should show the company identity. If a party is presented as a sole trader, ask for Self Assessment status. Where relevant, ask whether they expect to earn more than £1,000 in a tax year running from 6 April to 5 April.

The upside of this heavier pack is clearer accountability and faster root-cause analysis when ownership is challenged. The tradeoff is onboarding overhead: more collection steps, more exceptions, and more pressure on ops to move files through quickly.

Do not let that pressure weaken the gate. If the declared entity type, contract party, and payout recipient do not align, stop setup and escalate. That is especially important when someone says Self Assessment is already handled, because GOV.UK notes a tax return may be delayed if an existing account is not reactivated first.

Best for payout-at-scale operations that need fewer tax surprises#

For high-volume payments teams, the practical control is sequence: record the required status first, configure payment treatment second, and release payout last. In hiring contractors UK IR35 operations, this reduces mismatches between compliance records and live payment events.

Put a hard gate between status and payout release#

Make the status record a required input to payment setup, not a separate note in another system. If teams can release payouts without that linked record, exceptions will surface later in reconciliation.

| Stage | What should exist before moving on | Verification checkpoint | Common break |

|---|---|---|---|

| Status recorded | Status result, decision timestamp, responsible reviewer, engagement ID | Confirm the status is attached to the live engagement | Older record reused after engagement details changed |

| Payment treatment configured | Payment treatment linked to the same engagement ID and status record | Check compliance and finance are viewing the same record | Status lives in notes while payout setup uses a manual field |

| Payout released | Release only after the records match and required holds are cleared | Reconcile the first production payout to the linked engagement record | Payment released before status-linked setup is complete |

Where your model relies on the payee handling their own filing, keep your checks specific. GOV.UK states first-time filers must register for Self Assessment before using the online service. It also states they may need to reactivate an existing account, and filing without reactivation may delay the return.

Keep basic filing-operability checks in the evidence pack: whether this is a first filing, whether reactivation is needed, and whether the payee can keep records such as bank statements or receipts. Date checks also matter: GOV.UK states returns can be filed on or after 6 April following the end of the tax year, and the tax bill is due by 31 January.

Validate entity type before assuming online filing is available. GOV.UK states the online Self Assessment service cannot be used for a partnership return.

The upside is fewer downstream remediation cases and cleaner reconciliation. The tradeoff is integration effort, especially if compliance and payout systems do not share a durable engagement identifier.

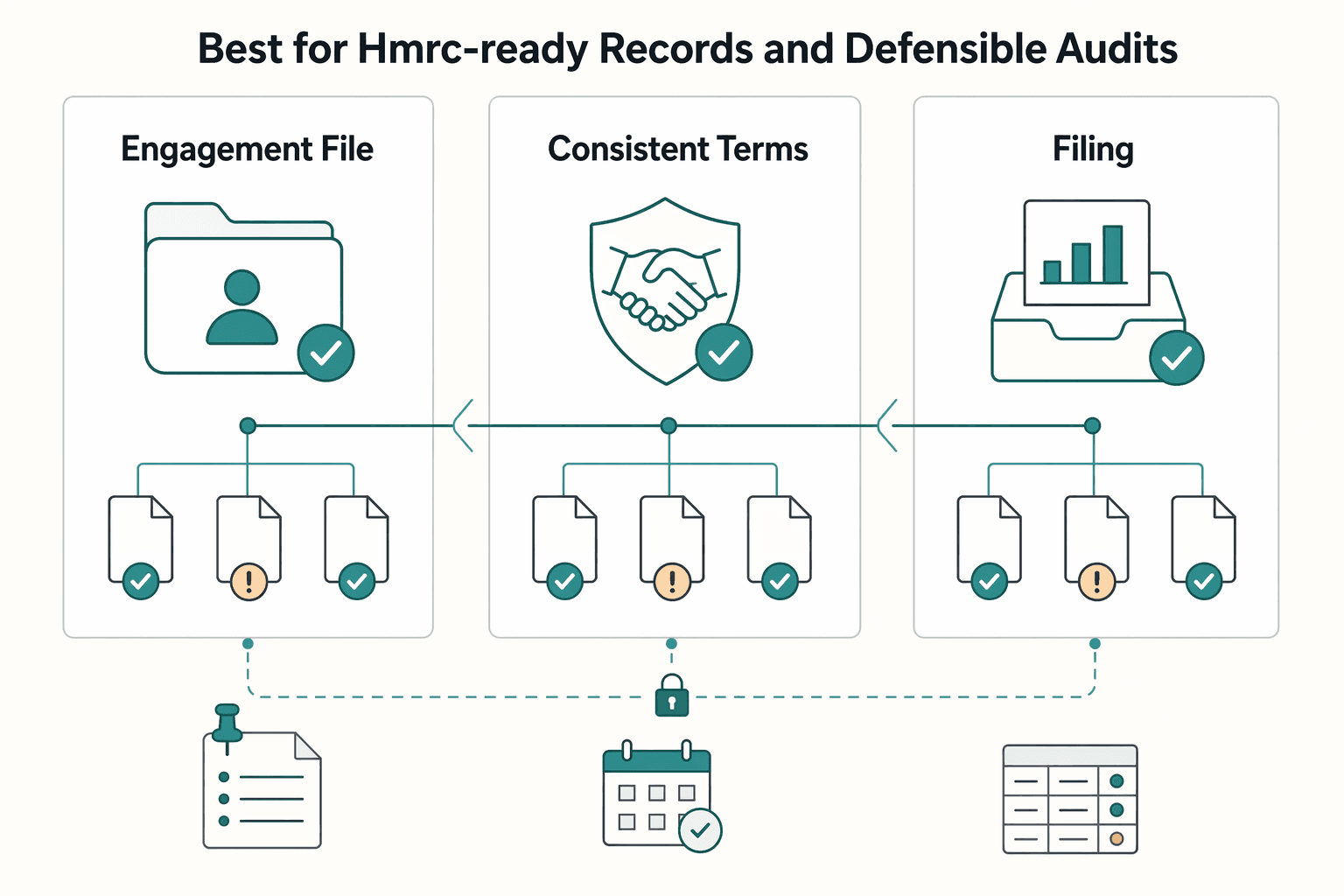

Best for HMRC-ready records and defensible audits#

If you expect formal scrutiny, make one team own a single engagement audit bundle so the decision can be reconstructed later without relying on memory.

| Audit item | What to keep | Why it matters |

|---|---|---|

| Engagement file | Determination rationale, responsible owner, intermediary details relied on, decision timestamp, and change history | Keep it tied to one live engagement record, not split across email threads, contract folders, and finance notes |

| Consistent terms | Use the same wording for Self Assessment, tax return, reactivate your Self Assessment account, and keep records | This reduces interpretation drift between legal, compliance, and finance |

| Filing-readiness evidence | Whether the contractor needs to complete a tax return for the previous year, the 5 October notification date, the 31 January tax bill date, whether account reactivation is needed, and records such as bank statements or receipts | Record what the contractor is actually relying on, not only a generic "tax sorted" assurance |

- Keep one engagement file with a minimum internal bundle.

The GOV.UK pages cited here do not provide a ready-made IR35 audit checklist, so set a repeatable internal standard: determination rationale, responsible owner, intermediary details relied on, decision timestamp, and change history. Keep it tied to one live engagement record, not split across email threads, contract folders, and finance notes.

- Use GOV.UK and HMRC terms consistently across records.

Use the same wording everywhere your teams will rely on later, including Self Assessment, tax return, reactivate your Self Assessment account, and keep records. This reduces interpretation drift between legal, compliance, and finance when they review the same case.

- If your model depends on payees filing themselves, capture filing-readiness evidence.

GOV.UK says someone who needs to complete a tax return for the previous year must tell HMRC by 5 October, and that the tax bill is due by 31 January. It also says filing without reactivating an existing account may delay the return, and that records such as bank statements or receipts are needed to complete returns correctly. In your file, record what the contractor is actually relying on, not only a generic "tax sorted" assurance.

For a step-by-step walkthrough, see Vendor Approval Process for Platforms That Screen and Onboard Contractors.

Best for uncertainty and edge cases you should escalate early#

When key facts are missing, use one default: hold and escalate, not "assume outside IR35."

These GOV.UK pages do not define IR35 escalation criteria, client-size routing, end-client identity tests, or intermediary-control tests. If you need those triggers, set them in your internal policy and route each case to a named owner. What GOV.UK does provide is clear filing-readiness checkpoints you can use as objective pause points.

| Trigger | Owner | Stop/go action | Required artifact | Resolution SLA |

|---|---|---|---|---|

| First-time filer plans to file online but has not registered for Self Assessment | Named tax or compliance owner | Hold any process that depends on online filing readiness | Registration confirmation or equivalent case evidence | Set internally |

| Existing filer cannot confirm an active account | Named tax or compliance owner | Hold and escalate | Proof the account was reactivated, since filing without reactivation may delay the return | Set internally |

| Payee says they are filing online as a partnership | Named tax or compliance owner | Stop and reroute | Entity-type confirmation and alternative filing approach, since the online service cannot be used for a partnership | Set internally |

| Team cannot confirm whether a tax return is required | Named tax or compliance owner | Escalate; do not register by reflex | Review note showing the "check if you need to send a tax return before registering" step was completed | Set internally |

Use the engagement file as a quick decision check: does it show whether the person needs to file, whether they can use the online service, and whether the account step is complete? If any answer is unclear, pause and escalate rather than relying on assurance alone.

Conclusion#

If you are handling hiring contractors in the UK, the practical win is not a longer explainer. It is a short control list people actually follow: one named owner, a minimum evidence pack, and a clear hold point when core facts are missing.

- Start with entity type and filing route.

Before anyone moves ahead, confirm the worker's business structure. GOV.UK is explicit that the structure you choose can affect how you pay tax and your legal responsibilities, so this is not admin trivia. The first checkpoint is simple: are you dealing with a sole trader, a limited company, or a setup such as a partnership, trust, or estate? This early check keeps you from sending people down the wrong HMRC path, and it catches a real edge case because the standard online Self Assessment service cannot be used for partnerships, trusts, or estates.

- Tie your evidence pack to HMRC's actual dates.

If a worker says they need to complete Self Assessment, verify where they are in that process instead of accepting a verbal "sorted." HMRC says you must tell it by 5 October if you need to complete a return for the previous year, online filing is available on or after 6 April following the end of the tax year, and the tax bill is due by 31 January. Ask one more practical question when someone has filed before: does the account need reactivation? HMRC says that may be required, and missing it can delay the return. Dates make your controls testable, not subjective.

- Keep the record set lean, but keep it defensible.

You do not need a giant file for every engagement. You do need a small set that helps your team reconstruct what happened later: entity details, filing path, and supporting tax admin evidence such as registration or reactivation confirmation. Where HMRC guidance points to retained records, make that explicit too: workers should keep records such as bank statements or receipts so the tax return can be completed correctly. A smaller bundle is more likely to stay current, auditable, and usable when guidance on GOV.UK changes.

The operating test is straightforward. If your team can verify entity type, filing path, key deadlines, and underlying records, you reduce surprises without building process for its own sake. If you cannot verify the entity type, the filing path, or the underlying records, pause and escalate before money moves.

Frequently Asked Questions

Who determines IR35 status when hiring contractors in the UK?

These GOV.UK pages do not say who determines IR35 status, so do not treat Self Assessment guidance as authority for that point. A practical internal step is to assign a named owner and document that ownership before onboarding scales. If you need the legal allocation rules themselves, use IR35-specific material such as A Deep Dive into IR35 for Freelance Contractors in the UK.

Does IR35 apply when the worker provides services through a PSC or other intermediary?

The cited sources do not answer IR35 scope for a PSC or other intermediary. What they do confirm is that a limited company is legally separate from its owners, and that business structure affects tax treatment and legal responsibilities. So your first verification step is basic but important: confirm whether you are dealing with a sole trader, limited company, or another setup before you infer anything else.

How do obligations differ between small business clients and medium and large clients?

That split is not covered by the excerpts here, so you should not infer it from these pages. If client size changes responsibility in your process, treat missing or contradictory size evidence as a stop point and escalate.

What operationally changes when an engagement is inside IR35?

These sources do not set out the operational consequences of an inside IR35 decision. The concrete dates they do give are tax admin dates: tell HMRC by 5 October 2025 if you need to complete a tax return for the previous tax year, file online on or after 6 April after the year ends, and pay the tax bill by 31 January. Useful dates, yes, but they are not a substitute for an actual status decision.

What should a platform collect before first payout to reduce off-payroll risk?

From these sources alone, focus on confirming the contractor’s business structure, whether they need to complete Self Assessment, and whether an existing account needs reactivation before filing where relevant. HMRC also says records such as bank statements or receipts should be kept so the return can be completed correctly, so make recordkeeping expectations explicit early. One red flag worth checking before money moves is an existing filer using an old account, because HMRC says filing without reactivating it may delay the return.

How should agencies and suppliers share responsibility with the end client in practice?

The cited pages do not allocate responsibility across agencies, suppliers, and end clients under off-payroll working rules. What you can do now is require each party to confirm its entity type and any HMRC-facing tax admin steps it is actually handling. If nobody can point to who owns registration, reactivation, or record retention, you do not have enough clarity to rely on verbal assurances.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

Educational content only. Not legal, tax, or financial advice.

Related Posts

IR35 for UK Freelancers: Records, Self Assessment, and Pre-Signing Checks

For UK freelancers dealing with IR35, start with one practical rule: keep each engagement and its tax admin documented in one place from day one. That habit can save you from rebuilding files later under pressure.

Agency Scaling Blueprint for Hiring Your First Global Contractors

Scale after you harden what already works. Before you write a job description, lock down the parts of the business that usually break first under growth: contracts, cash, worker status, delivery documentation, and how work gets reviewed. This blueprint is about adding capacity without adding avoidable risk.

Hiring Contractors in the Philippines with Compliance-First Payout Controls

If you are hiring contractors in the Philippines, set your compliance controls before onboarding starts. One common breakdown is not finding talent, but proving during an audit, dispute, or internal review that the working relationship, contract terms, payout trail, and tax handling still line up.