Quick Answer

Yes, estonian e-residency freelancers can be workable, but only after a jurisdiction-first screening process. The article’s core position is that e-Residency supports remote company administration in Estonia, while tax residency, employment classification, and social-contribution duties are decided where work is actually performed. It recommends a go/no-go gate using a country matrix, explicit escalation triggers, and payout controls tied to verifiable records.

Estonian e-Residency for freelancers in 2026 and what this guide will help you decide#

Treat this as a screening guide, not a sales pitch for Estonia. If you are assessing an Estonia-linked setup for a freelancer or solopreneur, first decide whether the problem is mainly EU VAT administration or a wider tax, labor, and payout-control issue. Those are not the same thing, and they do not call for the same tools.

Step 1 Set the decision scope#

Start by writing down the operating question in one sentence. A good version is specific: "We need a workable cross-border setup for one operator, EU clients, and controlled payouts," not "We want a simple international structure." That scope matters because some EU tools solve only narrow administrative points.

For example, the One Stop Shop, or OSS, is a VAT scheme where a taxable person can register in one single Member State, the Member State of identification, for relevant VAT declaration and payment flows. The OSS materials also cover registration, VAT declaration and payment, record keeping and audits, and leaving the scheme. If your main pain point is cross-border B2C VAT administration, that is relevant. If your main pain point is tax residency or employment classification, OSS is not enough on its own.

A practical red flag is when the business case quietly shifts from "simpler VAT handling" to "full cross-country legal certainty." That is usually where teams start asking an Estonia-based setup to do more than these VAT tools are designed to do.

Step 2 Separate the real decision checkpoints#

Before launch, split three checkpoints into separate lanes: tax residency, employment classification, and payout controls. Keeping them separate avoids the common mistake of treating a VAT registration choice like a legal answer to everything else.

When the issue is genuinely about VAT treatment of a complex cross-border transaction, VAT Cross-border Rulings, or CBR, may help. The EU describes CBR as a mechanism for advance rulings on complex cross-border VAT transactions, and taxable persons can request such a ruling where two or more participating Member States are involved. The catch matters: the request must follow the national VAT ruling conditions in the participating EU country where the requester is VAT-registered.

Your verification point here is simple. For each open issue, label it either "VAT admin," "tax residency," "worker status," or "payment control." If one issue does not fit cleanly, escalate it instead of forcing it into the VAT bucket.

Step 3 Define the output you need from this guide#

By the end of the article, you should be able to produce three things without hand-waving:

- A go or no-go decision on the proposed Estonia-linked model

- A named escalation path for questions that VAT tools do not answer

- A copy and paste control checklist for onboarding, invoicing, and payouts

The document pack behind that decision should be boring but clear: who the operator is, where work is performed, what kind of supplies or services are being made, whether the activity is B2B or B2C, which country handles VAT registration, and who can release payments. If you cannot assemble that pack early, do not mistake momentum for readiness.

If Italy is one of the countries in scope, compare the same evidence pack against Tax Residency in Italy: A Guide for Freelancers and Nomads.

What Estonian e-Residency solves and what it does not solve#

Use Estonian e-Residency as an access tool, not a legal conclusion. It is a digital identity card issued by the Estonian government for remote access to company administration in Estonia.

| Tool | Main use | Limit / note |

|---|---|---|

| Estonian e-Residency | Digital identity card for remote access to company administration in Estonia | Not tax residency; does not automatically resolve local tax or labor obligations in the country where work is actually performed |

| OSS | VAT scheme to register in one single Member State for relevant VAT declaration and payment flows | Covers certain VAT flows through one Member State of identification; if the main pain point is tax residency or employment classification, OSS is not enough on its own |

| CBR | Mechanism for advance rulings on complex cross-border VAT transactions involving two or more participating Member States | Limited to advance rulings on VAT treatment for complex cross-border transactions; the request must follow national VAT ruling conditions in the participating EU country where the requester is VAT-registered |

- What it solves

If your goal is to run an Estonia-linked company remotely, this can help. It can also support digital operations tied to an EU company and the EU single market.

- What it does not solve

Estonian e-Residency is not tax residency. It does not automatically resolve local tax or labor obligations in the country where work is actually performed.

- How to test fit before launch

If you only need EU company access and digital administration, it may be a good fit. If you need legal certainty across countries, it is not sufficient on its own. OSS and CBR are narrower tools: OSS covers certain VAT flows through one Member State of identification, and CBR is limited to advance rulings on VAT treatment for complex cross-border transactions. Keep separate lines in your file for company access, tax residency, worker status, and payout controls; if they blur, escalate before launch.

For Spain, use Spain Tax Residency for Mobile Freelancers Who Need Defensible Records to stress-test the residency record before you rely on the Estonia setup.

Prerequisites and evidence to gather before you structure anything#

Do the evidence work before contracts or payouts. e-Residency is a digital identity tool, not a shortcut for tax residency or country-level compliance decisions.

Step 1 Build a jurisdiction file for every place people actually work#

Create one file per founder/operator location, including where the person lives, where work is performed, and Estonia if you plan to use an Estonian company. For Germany and Italy, treat Estonia-based assumptions as assumptions until separately reviewed.

Keep each file factual and operational: where work happens, where clients are served, where decisions are made, and which Estonia-linked assumptions you are relying on. Because e-Residency is a government-issued digital identity for non-residents, not physical presence or tax residency, mark those boundaries explicitly.

Use a simple status on each file: clear, escalate, or blocked, plus owner and review date.

Step 2 Capture the role facts that drive employment classification#

Record the real operating facts before anyone drafts a "freelancer" agreement: who sets schedule, who controls pricing, who bears business risk, and whether the person operates as a true freelancer in practice.

If facts look employment-like, escalate early instead of relying on contract labels. Check consistency across agreement terms, onboarding, approvals, and invoicing behavior.

Step 3 Prepare the document set that supports the operating model#

Before first payout, assemble one pack with the service agreement, invoicing flow, bank account ownership evidence, and the named contact person for the Estonian company. If needed, see The Role of a 'Contact Person' for an Estonian e-Resident Company.

| Application element | Stated detail |

|---|---|

| Government-issued ID | Required in one documented process |

| Motivation letter | Required in one documented process |

| Passport-style photo | Required in one documented process |

| Fee | 100€ |

| Estimated review window | Four to five weeks |

Match the core identifiers: contract party, invoice issuer, and receiving account should align with who you intend to pay. If e-Residency is still pending, keep the identity application pack ready. One documented process requires government-issued ID, a motivation letter, a passport-style photo, a 100€ fee, and an estimated four to five week review window.

Step 4 Define escalation ownership before first payout#

Set decision boundaries before exceptions appear. Finance decides only when jurisdiction files are complete, role facts align with contracts, and payout routing matches the document pack. Legal/tax signs off when location conflicts remain unresolved or tax-residency assumptions are doing too much work.

Make pre-payout evidence mandatory: completed country file, signed agreement, bank ownership proof, named approver, and documented exceptions if anything is missing.

With that evidence in place, the next question is whether the facts support an Estonia-linked operating model at all.

For a step-by-step walkthrough, see Deductible Expenses for Freelancers in Spain Under IRPF and VAT.

Step 1: Run a jurisdiction conflict check before opening the operating flow#

Run this before banking, contracts, or payouts. If the operating facts do not match an Estonia-first setup, pause and escalate before onboarding.

Estonian e-Residency supports digital administration, but it is not actual residency and it does not remove tax obligations in the person's real country of residence. Keep this step focused on where obligations can arise in practice, not on company-formation assumptions.

Step 1 Build the matrix from real operating facts#

Create one row per relevant country, then fill each row from actual behavior.

| Jurisdiction row | Record | Flag |

|---|---|---|

| Actual country of residence | Where the person really lives and performs day-to-day work | Local tax, labor, and reporting exposure |

| Client-facing country | Where clients are contracted, sold to, or serviced from | Nexus, invoicing, and reporting friction |

| Estonia | Where the company is incorporated and administered | Estonian tax-law applicability for business conducted in Estonia |

Use operating facts, not marketing language: where work happens, where decisions are made, who manages client relationships, and where records are maintained.

Step 2 Apply explicit pause rules#

Use clear stop conditions when facts conflict with structure.

- If a person lives and works outside Estonia, treat that country's tax and labor analysis as required.

- If local facts in a country (for example, Germany) conflict with the Estonia-first plan, pause implementation and escalate for local advice.

- If contract labels and operating behavior do not match, escalate instead of forcing the paperwork.

Step 3 Review permanent-establishment exposure from behavior#

Assess exposure from real activity: sales behavior, management control, and where day-to-day business direction happens. Do not treat e-Residency as a substitute for this review.

If business is conducted in Estonia, Estonian tax legislation applies to that activity. In practice, check Estonia plus any other country with a credible claim based on operating facts.

Step 4 Gate go-live with status and ownership

Do not go live until every jurisdiction row is marked cleared, cleared with conditions, or blocked, with a named approver. For cleared with conditions, write the condition, owner, and date.

Related: Canada Tax Residency Ties for Freelancers Who Move Often.

Step 2: Design the operating model for pay, contracts, and role clarity#

After a jurisdiction row is cleared, lock one operating model before any invoice or payout starts. The goal is simple: one role model, one payment path, and one named owner for filing-related duties per operator.

Step 1 Lock one role model per operator#

Choose one model per operator and document it: contractor (freelancer) or employment-like arrangement. If the contract label and the real operating setup conflict, pause and escalate instead of papering over it in drafting.

Use Estonian e-Residency for what it supports: online authentication, digital signatures, and remote administration of the Estonian company. It is a digital identity, not physical presence or tax residency, so role design still has to match where the person actually lives and works.

Checkpoint for each operator file:

- signed agreement

- short role summary

- clear ownership of scope, pricing, delivery, and acceptance

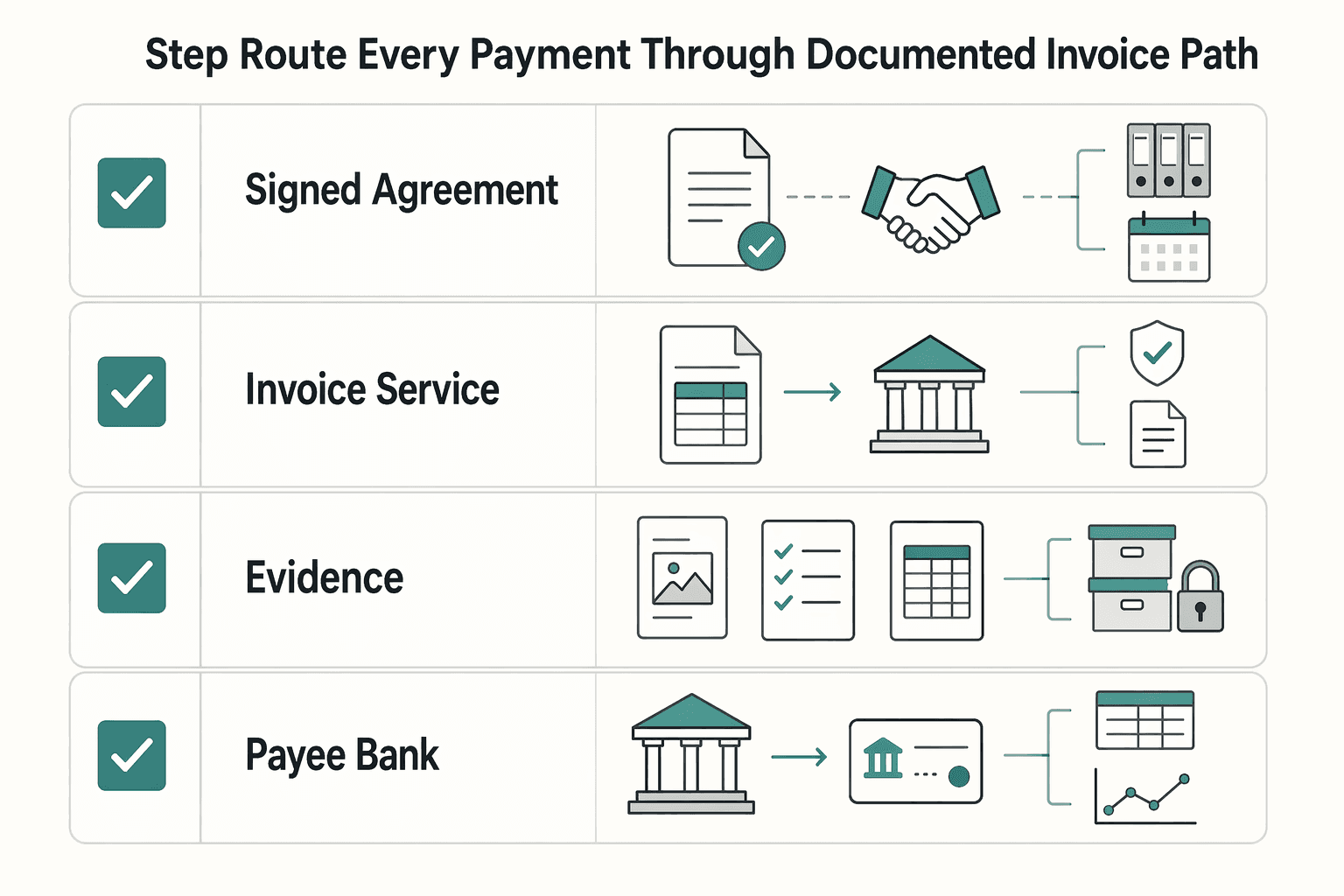

Step 2 Route every payment through a documented invoice path#

Define the compensation flow before the first cycle. In a contractor model, the invoice path should run through the Estonian company based on the documented commercial relationship, then move through named approval routing, then release.

| Payout-pack item | Stated detail |

|---|---|

| Signed agreement | Included in the minimum payout pack |

| Invoice for the service period | Included in the minimum payout pack |

| Approval evidence | For delivered work |

| Payee bank-account ownership details | Match the record |

Minimum payout pack:

- signed agreement

- invoice for the service period

- approval evidence for delivered work

- payee bank-account ownership details that match the record

Set an exception rule in advance: if required documents are incomplete, route to exception handling with an owner and date instead of releasing payment.

Step 3 Assign filing ownership before first payment#

Before first payment, explicitly assign who owns social contributions assessment, filings, and follow-up in the relevant country. Record the jurisdiction and review date in the operator file.

If someone is resident in Germany and the structure raises "self-employment through own structure" concerns, treat that as a legal-review trigger, not standard contractor flow.

Expected outcome: one operator file should show the role model, payment path, exception rule, and filing owner without interpretation.

With the operating model locked, you can build controls around the actual payment and reporting sequence.

Step 3: Implement payment, reporting, and audit controls in order#

Set one enforced payout sequence and require every payment to follow it. The goal is consistent controls and records that can explain who was paid, why, under which contract, and what reporting risks were reviewed.

Step 1 Gate the payout path before release#

Use a fixed internal order: identity and business checks, contract validation, invoice review, payout release, then reconciliation. That sequence does not answer the legal questions, but it reduces undocumented exceptions.

Before release, confirm the agreement, role summary, and invoice describe the same working reality. Proper contractor classification is essential to avoid tax and regulatory issues, so mismatches should stop payout and trigger escalation.

Keep the same discipline even when cross-border payments feel operationally easy. Eurozone rails can make payments easier, while local tax and invoicing compliance still apply.

Verification point: from one file, you should be able to show who is paid, which entity pays, which contract authorizes payment, which invoice period is covered, and who approved delivery.

Step 2 Map each transfer to a reconstructable record chain#

For each payout, keep a linked chain that can be reconstructed end to end:

- payment request or invoice intake

- approval record with named approver

- provider transaction reference

- ledger entry

- saved export/report pack

The control test is linkage, not document volume. Your records should reconcile to the same payee, amount, currency, and service period.

If your provider operates in an environment aligned with PSD2, treat that as support for secure and transparent payments, not a replacement for your own audit trail. Also keep reporting obligations in view: the EMTA handbook references penalties for non-reporting of reportable arrangements, and FATCA declarations are an obligation for Estonian financial institutions that hold relevant US-resident accounts.

Step 3 Tie tax evidence to payment events and run a monthly exception review#

Attach tax-relevant evidence to each payment event so your file shows what you relied on at the time of payment. For cross-border freelancer flows, keep residency or country-of-work statements, invoice, signed agreement, bank ownership details, and any reporting/withholding assessment artifacts together.

Run a monthly internal review to:

- review held, reversed, or manually touched payouts

- clear or escalate unresolved holds, unmatched receipts, and returned transfers

- collect jurisdiction-change attestations that may affect tax residency or reporting analysis

Handle failures through defined escalation, not ad hoc resends. Expected outcome: no orphaned transfers, no unresolved holds without owners, and no silent jurisdiction changes in active payout files.

Common mistakes and how to recover without freezing operations#

Do not freeze the whole program when exceptions appear. Contain the issue, keep clean cases moving, and reopen only the affected lane when the file is defensible.

Step 1 Re-baseline Estonia-first assumptions#

If your team has treated Estonian e-Residency as a legal shortcut, reset the case using current operating facts. Re-run your tax residency and permanent establishment check based on where work is actually done and managed, not only where the company is formed or which payment rail is used.

This reset is necessary because cross-border tax frameworks are fragmented across the EU, and compliance costs can differ by country, industry, and business size. One approved setup does not automatically transfer to another operator.

Verification point: each affected file should show an updated jurisdiction review, a named reviewer, and a current status (cleared, cleared with conditions, or blocked).

Step 2 Rewrite documents to match how the freelancer actually works#

When contract terms and day-to-day practice diverge, classification risk rises. Update service terms, approval logic, and invoice instructions so they match the real working model, and escalate when they do not.

Your release rule should be strict: if role facts and paperwork point in different directions, hold the next payout until the mismatch is resolved.

Verification point: the signed agreement, role summary, invoice pattern, and approver notes should describe the same operating reality.

Step 3 Backfill local-obligation evidence before reopening#

If evidence for local obligations, including social contributions, is incomplete, use a targeted hold instead of a global stop. Pause new payouts for the affected operator or jurisdiction, backfill missing documents, and reopen only after finance and legal or tax sign-off.

Keep one complete evidence pack: country-of-work statement, tax residency statement used in analysis (if applicable), signed agreement, invoices, bank account ownership details, and an internal owner for each unresolved local filing or contribution question.

Step 4 Cap payout volume until governance catches up#

If exceptions are rising, slow volume before scaling. Apply temporary caps, require enhanced approvals for manual touches or new corridors, and run weekly exception reviews until performance stabilizes across a full payment cycle.

Do not anchor recovery on a guaranteed local banking outcome. Reporting from 2025 notes that standard Estonian banks usually require a real connection to the country and applications can be rejected, so plan for contingencies while controls are being repaired.

When Estonia is the right fit and when another route is cleaner#

Estonia is usually a cleaner fit when you need remote administration of an EU company and your cross-border VAT position is stable; if local compliance keeps driving escalations, the cleaner route is the one you can defend locally, even if it is less convenient.

Step 1 Favor Estonia only when the cross-border file is manageable#

Use Estonian e-Residency for administrative access, not as a workaround for country-level obligations. The strongest fit is a freelancer with clear jurisdiction ownership, limited location changes, and transactions that can be handled through standard EU VAT mechanisms.

For B2C e-commerce, EU VAT rules changed on 1 July 2021, and the One Stop Shop (OSS) lets a taxable person register in one Member State (the Member State of identification) for scheme VAT declaration and payment. That can simplify an Estonia-centered setup, including when cross-border distance-sales rules become relevant around the EUR 10 000 EU-wide threshold. It does not remove filing, payment, record-keeping, or audit responsibilities.

Step 2 Compare alternatives on compliance burden, not branding#

If escalations are mostly tied to your country of residence, compare Estonia with a home-country structure or a residence-linked option like the UAE Golden Visa Program using one test: where are obligations clearer to document and maintain? Keep the decision file practical and explicit about ownership for VAT and related reporting.

Step 3 Re-test before relocating#

A setup that works in one country can become harder to defend after a move to Italy or Germany if local obligations overtake the Estonia-first model. Before moving, re-run the jurisdiction review, confirm whether your OSS Member State of identification still fits, and for complex cross-border VAT treatment consider whether a VAT Cross-border Ruling request is appropriate under national ruling conditions. If escalations remain frequent and unresolved, choose the structure with clearer local compliance.

Final takeaway and copy/paste launch checklist#

Use Estonian e-Residency as an operating tool, not a compliance conclusion. Your go/no-go still depends on tax residency, worker classification, social-contribution handling, and the facts in each country where work is performed.

Keep VAT on a separate track. For covered cross-border VAT obligations, OSS allows registration in one single Member State, the Member State of identification, for declaration and payment, and CBR can be used to request an advance ruling on envisaged complex cross-border VAT transactions. These VAT tools do not settle income tax, employment status, or social-contribution obligations.

Copy and paste this launch checklist#

- Confirm the business objective. State why you want an EU company in Estonia and what operational problem it is meant to solve.

- Complete the jurisdiction matrix. Include Estonia and each operator country (including Germany or Italy where relevant), and mark each as cleared, cleared with conditions, or blocked.

- Classify worker models against real operations. If contract terms and day-to-day reality do not match, escalate before first payout.

- Assign owners for filings and escalations. Name who owns social contributions, tax reporting, and escalation decisions.

- Route VAT decisions explicitly. If you have covered cross-border B2C services or distance sales, assess OSS scope; for complex cross-border VAT treatment, assess CBR. Keep in view that EU e-commerce VAT changes applied from 1 July 2021, and confirm whether the EUR 10 000 threshold applies to your transaction scope.

- Set payout and audit controls before scale. Require approval gates, traceable records, and monthly verification checkpoints; if you use OSS, keep scheme-required records because single-state registration does not remove audit or record-keeping duties.

- Handle multi-company CBR requests correctly. Where multiple companies are involved, one company submits on behalf of the others.

- Record unresolved risks and get specialist sign-off before expanding volume.

If you cannot state which country owns the main tax, labor, and VAT obligations for a given operator, pause scaling and escalate.

Frequently Asked Questions

Is Estonian e-Residency the same thing as tax residency?

No. e-Residency is a digital identity from Estonia for access to Estonian e-services, not tax residency. A common rule in many countries looks at 183 days in a tax year, but that is not universal, and other residency tests may also apply.

Can a freelancer legally pay themselves from an Estonian company while living in another country?

Sometimes, but the hard answer sits in the country where you live and work, not in the e-Residency card itself. Remote work in another jurisdiction can create tax nexus and trigger obligations there, so this needs jurisdiction-specific legal and tax review.

What minimum controls should a platform require before supporting e-Residency-based freelancer payouts?

There is no universal minimum checklist here. What is clear is that country of work and residence can change tax obligations, so cross-border cases should be documented clearly and routed for jurisdiction-specific review before payouts.

When does permanent establishment risk become a practical concern?

There is no universal trigger point here. What is clear is that remote work abroad can create tax nexus and obligations outside the worker's home country, so PE questions need country-specific analysis.

How should teams handle social contributions if work is performed outside Estonia?

Do not assume an Estonian company automatically determines the social-contribution outcome. This remains jurisdiction-specific and should be reviewed where the work is actually performed before payouts.

What are the clearest escalation triggers to legal or tax counsel?

Escalate when someone changes countries, spends extended time abroad, or creates potential tax nexus or double-taxation risk. Escalate whenever the relevant filing jurisdiction is not clear.

What is known from official e-Residency messaging and what remains unknown without jurisdiction-specific advice?

Official messaging is clear that Estonian e-Residency is not a travel document, citizenship, visa, or residency permit, and it does not automatically provide a business bank account. What it does not settle is tax residency, permanent establishment exposure, social contributions, or whether two countries may both assert taxing rights. Those answers still depend on the specific countries and facts in your file.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 2 external sources outside the trusted-domain allowlist.

- europarl.europa.eu/cmsdata/296344/Study%20Tax%20barriers%20and%...trusted

- oecd.org/content/dam/oecd/en/publications/reports/201...trusted

- oecd.org/content/dam/oecd/en/publications/reports/202...trusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- vat-one-stop-shop.ec.europa.eu/index_entrusted

- vat-one-stop-shop.ec.europa.eu/one-stop-shop_entrusted

- 1office.co/blog/how-to-form-company-estonia-eresidency-...external

- eddieoz.com/live-q-a-with-the-e-residency-team-ask-us-an...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

UAE Golden Visa for Freelancers and the Green Visa Decision Guide

Choose the route your documents can support now, not the visa label with the most search volume. If you searched for `uae golden visa for freelancers`, use that as a starting query, then choose between Golden Residency and the Green route based on the evidence you can actually file.

The Role of a Contact Person for an Estonian e-Resident Company

In a few minutes, you can check whether your Estonian OÜ needs contact-person action now, then put controls in place so important notices do not get missed. Start by naming one person to monitor forwarded notices and one backup to step in when that person is unavailable.

Tax Residency in Italy for Freelancers and Nomads

You can usually reach a defensible first view in one focused sitting: based on your facts, are you more likely tax resident in Italy right now or not. This draft is for freelancers and consultants who want a practical first pass on whether Italy tax residency is likely, then a low-stress routine to keep records aligned with that position.