Quick Answer

Set your filing position by ranking ties before counting days: housing access plus spouse or dependants in Canada are primary CRA indicators, then secondary ties, then the 183-day sojourn branch. Record change dates in one timeline and keep status labels consistent across your memo and return. If another treaty country can also claim residence, run tie-breaker analysis and subsection 250(5) before filing. Use Form NR74 only as a CRA opinion request in close deemed non-resident cases.

How Canada Tax Residency Ties Work When You Move Often#

Cross-border freelancers should determine residency status before relying on day count alone. In Canada, income tax liability starts with whether you are a resident or non-resident, and CRA looks at multiple factors rather than a single shortcut.

In practice, residential ties are a key part of determining status, which sets your tax scope. A resident of Canada is taxed on worldwide income, while a non-resident is generally taxed only on Canadian-source income. CRA distinguishes ordinarily resident and deemed resident individuals, and in some situations treaty rules can result in deemed non-resident treatment.

A common risk is treating day count as the whole test. Residency is assessed using ties and other factors, so day count on its own may not resolve status.

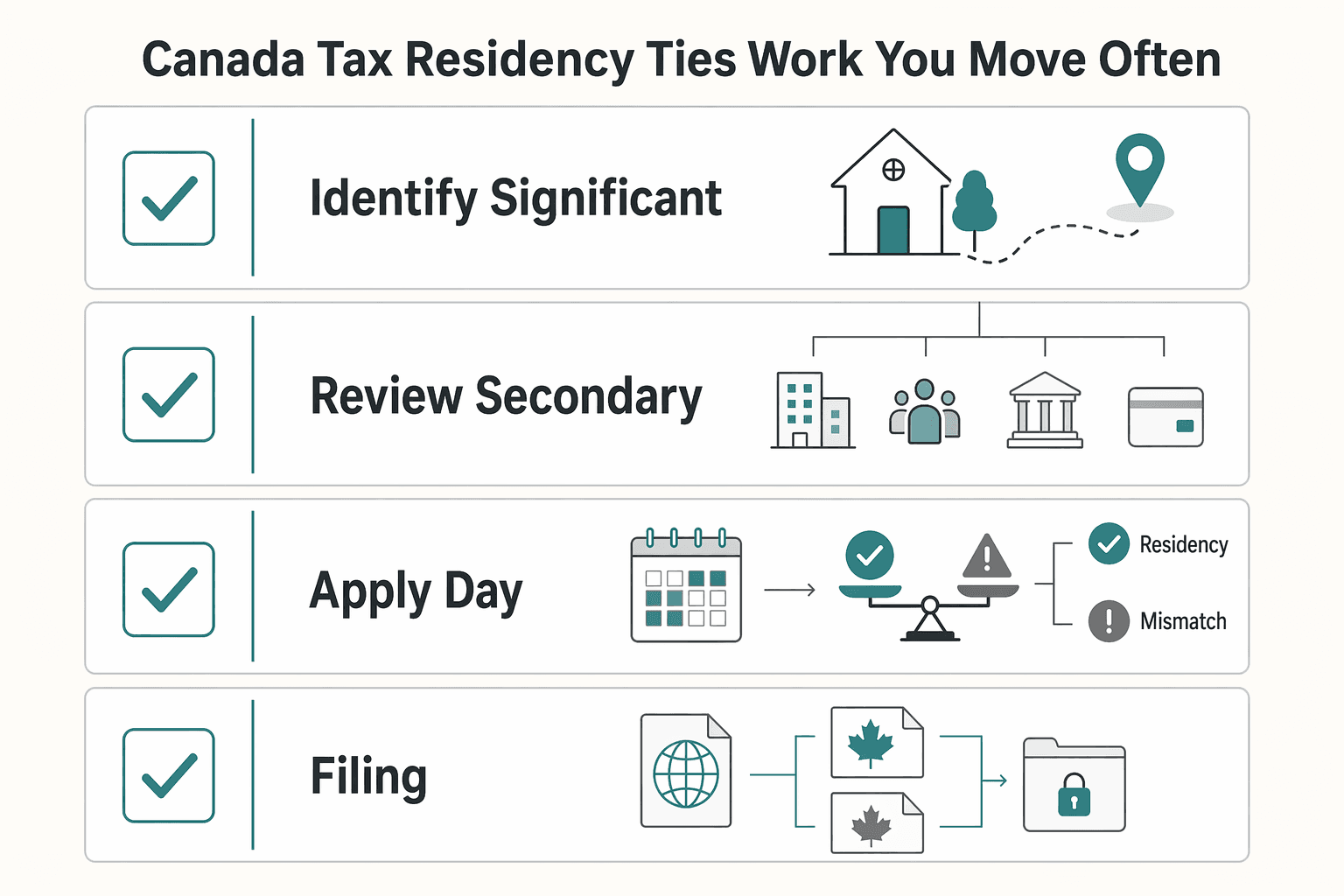

Use this order each year:

- Identify significant residential ties first, especially whether you have a dwelling available in Canada and where your spouse or dependants live.

- Review secondary ties as a group, not as isolated checkboxes.

- Apply day-count rules, including the 183-day sojourn threshold, after tie analysis.

- If two countries can claim residence, apply treaty tie-breaker analysis before locking in your filing position.

This sequence helps organize your analysis from first draft to filing package. If facts conflict, escalate before you prepare forms.

Start with the terms that change your tax outcome#

Your tax obligations to Canada depend on your residency status, so define the terms before you start day-count math.

Use these terms consistently in your filing notes:

- Factual resident of Canada: an individual with significant residential ties to Canada.

- Deemed resident of Canada: treated as resident and taxed in Canada on worldwide income throughout the year.

- Deemed non-resident of Canada: someone who might otherwise be resident, but is treated as not resident under subsection 250(5) and treaty tie-breaker rules.

- Non-resident of Canada: generally taxed in Canada only on income from sources inside Canada.

Keep ties in two buckets. Significant residential ties carry the most weight, including a home in Canada, a spouse or common-law partner in Canada, and dependants in Canada. Secondary residential ties still matter, but CRA reviews them together rather than treating one item as an automatic trigger.

CRA uses a full facts-and-circumstances review. That means ties, length of stay, purpose, intent, and continuity all matter. Day-count branches like more than 182 days or less than 183 days can affect outcomes, but they do not replace tie analysis.

Citizenship and immigration status are separate from tax residency. A passport or visa can describe your legal status in a country, but tax residency is still a factual determination. If your facts are mixed and treaty status may apply, Form NR74 is available to request CRA's opinion on deemed non-resident status.

A practical way to stay organized is to keep a one-page term sheet at the top of your residency file. Use the same status label in your timeline, memo, and return prep notes. Mixing labels across documents creates avoidable friction later, especially if your facts change mid-year and you need to explain when your view changed. If you want a deeper dive, read The Ultimate Digital Nomad Tax Survival Guide for 2025.

How CRA weighs significant and secondary ties in real life#

When facts point in different directions, significant ties usually carry more weight.

Start with the ties CRA treats as most important. Focus on:

- A dwelling place available for you to use in Canada

- A spouse in Canada

- Dependants in Canada

Then assess secondary ties together. One minor tie may not move your result, while several secondary ties can strengthen a residency position when combined with other facts.

Use a conservative working rule. If you keep a home available in Canada and a spouse or dependants remain there, that combination is generally strong evidence of residency unless other relevant facts point the other way. Day count can refine that conclusion, but it does not replace the initial tie review.

Treat this as a sequence of checkpoints, not a debate over one document. First, confirm which significant ties existed at the start and end of the year. Next, mark exactly when any significant tie changed. Then review secondary ties on that same timeline so you can see whether they reinforce or weaken your working result.

Use Form NR74 if you want CRA's opinion on deemed non-resident status. Treat it as an opinion request, not a final binding determination.

The goal is internal consistency. If your timeline says a home remained available in Canada while your filing notes assume a full exit, fix that contradiction before filing. A clean file is one where the tie story, day count, and final status all point in the same direction. If you want a quick next step, try the tax residency day counter.

Use this decision order before you file anything#

Set your filing position in sequence: ties first, day count second, treaty context third if needed, and filing posture last.

| Step | Focus | Key direction |

|---|---|---|

| 1 | Current ties | Build a yes or no inventory of current ties with dated evidence |

| 2 | Factual residence | Test factual residence before any day-count branch |

| 3 | 183-day branch | Apply the 183-day branch after tie analysis |

| 4 | Treaty context | Consider treaty context only if another country may also claim residence |

| 5 | Filing posture | Map final status to returns, disclosures, and supporting records |

- Build a yes or no inventory of current ties with dated evidence.

List significant ties first, then list secondary ties. Record when each tie started, changed, or ended. If a fact is uncertain, mark it clearly so you do not treat assumptions as settled facts.

- Test factual residence before any day-count branch.

Use CRA guidance to evaluate all relevant facts together. If your strongest ties point to Canada, use that as your working result unless contrary facts are stronger and well documented. Keep a short note on why you reached this result so future edits stay anchored to the same reasoning.

- Apply the 183-day branch after tie analysis.

Less than 183 days or more than 182 days can change the outcome, but day count is not a substitute for tie analysis. Use it to confirm or challenge your tie-based conclusion. If the day-count branch points away from your tie result, flag the file for deeper review rather than forcing a quick answer.

- Consider treaty context only if another country may also claim residence.

If another treaty country can also treat you as resident, review treaty context before finalizing returns. If no competing claim exists, keep the file focused on domestic analysis. Avoid adding treaty language to a file that does not need it.

- Map final status to filing posture and exposure.

Once status is set, align returns, disclosures, and supporting records to that status. Resident outcomes can include worldwide income exposure. Make sure every document reflects the same status decision.

Before filing, write a short pre-filing memo that states your conclusion and the key evidence behind it. Keep it practical: what you concluded, why, what could challenge that view, and what documents support it.

Run one last contradiction check:

- Do ties, day count, and treaty notes point to the same result?

- Do the dates in your timeline match the status periods in your filing notes?

- Does the file clearly separate settled facts from assumptions?

If any answer is no, resolve the gap before return prep continues.

Why the 183-day rule is often misunderstood#

The 183-day rule matters, but it is not a complete residency test on its own.

It is often misread as automatic in either direction. Under 183 days is not an automatic non-resident result, and more than 182 days is not a full answer by itself. CRA still evaluates residential ties and the broader pattern of your stays.

Two travel logs that look similar can still lead to different outcomes. For example:

- Frequent visitor with weak ties: days near the threshold, limited residential ties, and lower residency risk than day count alone suggests.

- Similar travel days with stronger ties: comparable travel pattern, but stronger residential ties in Canada increase residency risk.

A common failure mode is counting days from memory and only checking totals at year-end. By then, details about your stays and ties can be hard to reconstruct. Build the record as the year goes so your count and tie analysis evolve together.

If your count is near 183 and your ties changed mid-year, treat the year as higher uncertainty. Keep a month-by-month record of travel days and material tie changes. That timeline can show where your strongest position begins and where it weakens.

The day-count branch can also intersect with treaty analysis when another country treats you as resident. In dual-residency years, reconcile ties, day count, and treaty outcome before filing.

The takeaway is simple: day count is a test you run in context, not a shortcut you run in isolation.

When a tax treaty can override your domestic result#

A treaty can become decisive when both countries treat you as resident under domestic law.

| Order | Factor | Article wording |

|---|---|---|

| 1 | Permanent home | Where a permanent home is available |

| 2 | Centre of vital interests | Where your centre of vital interests is stronger (personal and economic ties) |

| 3 | Habitual living | Where you habitually live |

| 4 | Citizenship | Citizenship, if earlier factors do not resolve the result |

| 5 | Mutual agreement | Mutual agreement, if needed |

At that point, treaty tie-breaker rules can resolve the conflict for treaty-residence purposes. They do not rewrite domestic residency law. In Canada, that analysis can support deemed non-resident treatment.

CRA's decision path asks whether you are resident in another country that has a tax treaty with Canada. If yes, complete tie-breaker analysis before filing. If no, continue with your domestic result.

Build tie-breaker support around dated, verifiable evidence in the commonly cited Canada-US order:

- Where a permanent home is available

- Where your centre of vital interests is stronger (personal and economic ties)

- Where you habitually live

- Citizenship, if earlier factors do not resolve the result

- Mutual agreement, if needed

Do not let treaty analysis float as a separate note. Connect each treaty factor to documents already in your file and to dates in your timeline. If a vital-interests claim depends on a move-out date, that date should appear in your housing records and in your travel ledger notes.

If treaty outcome would materially change what you report, withhold, or pay, get professional review before filing. If you use Form NR74, keep facts consistent across that request, your return position, and your records.

To keep this manageable, draft a short treaty memo with headings that match the factors you rely on. Under each heading, list the facts you rely on and the documents that support those facts. This keeps your treaty conclusion tied to evidence instead of broad statements.

Freelancer scenarios that break generic advice#

Generic advice breaks down when your facts are mixed, because similar travel patterns can produce different outcomes once ties are considered.

| Scenario | Likely risk direction | What to verify before filing |

|---|---|---|

| Remote consultant keeps a usable apartment in Canada and rotates between contracts | Higher risk of resident treatment for Canadian tax purposes | Housing records, whether a spouse or dependants remain in Canada, other ongoing financial ties, and whether your filing position remains consistent if resident treatment applies |

| Consultant fully exits Canadian housing and family ties | Stronger path toward non-resident treatment, or deemed non-resident treatment when treaty facts support it | Dated housing-exit records, family relocation evidence, and consistency between treaty position and domestic filing facts |

| Part-year mover with mixed contracts and mid-year relocation | Mixed-status risk, with one period looking more resident and a later period looking more non-resident | Month-by-month timeline for address, family location, contract location, and entry and exit days, including whether you fall in the more than 182 days or less than 183 days branch |

Use extra caution when a spouse or dependants remain in Canada while you work abroad. Reducing weaker ties does not automatically offset ongoing core ties.

When facts are mixed and status could swing between resident and non-resident outcomes, request CRA's opinion through Form NR74 before finalizing. Keep one consistent fact pattern across return positions, treaty analysis, and records.

To make these scenarios practical, run a quick contrast test on your own file. Ask: which facts pull toward residence, which pull away, and which facts are missing. If your answer depends on undocumented assumptions, pause and collect records before moving to filing decisions.

Scenario planning also helps when your year changes in phases. Early months may look like one status and later months another. Build the timeline first, then assess your residency status using your ties, treaty position, and day-count context.

Build an evidence file before CRA ever asks#

A defensible position depends less on argument than on dated records that tell one coherent story.

| File item | What to include | Article note |

|---|---|---|

| Timeline document | Monthly entries for ties, travel, and major changes | Every status-period change should appear in the timeline |

| Evidence index | Each key fact mapped to at least one document | Every major claim in your memo should trace to at least one dated document |

| Status memo | Your conclusion and why | States your status conclusion clearly |

| Filing checklist | Return treatment matches the status memo | Checks that return treatment follows the same status logic |

Use a single file with three headings: significant residential ties, secondary residential ties, and treaty position. Under each heading, record what existed, what changed, and the exact date of each change. Include length of stay, purpose, intent, and continuity in the timeline so your status logic is easy to follow.

For significant ties, keep documents that show where life was anchored, including housing records, spouse or dependant location, and move-in or move-out dates. For secondary ties, track them consistently and note whether each was canceled, moved, or retained.

Keep a separate travel ledger with entry and exit dates, country, and travel purpose. Total days against the less than 183 days and more than 182 days branches, then add monthly notes where facts changed. This is especially useful in part-year cases.

Add a short filing-position note that references Income Tax Folio S5-F1-C1 and states your status conclusion. Keep the consequence explicit: resident status means worldwide income exposure, while non-resident status is generally limited to Canadian-source income.

If Form NR74 is submitted, store the submission and CRA response in the same file and label it clearly as CRA's opinion. If income comes through multiple channels, archive invoice records, payout records, and relevant ledger exports in month order, including Gruv records where enabled. Before filing, run a final date check so each period's evidence supports the status claimed for that period.

A practical minimum pack looks like this:

- One timeline document with monthly entries for ties, travel, and major changes.

- One evidence index that maps each key fact to at least one document.

- One status memo that states your conclusion and why.

- One filing checklist showing that return treatment matches the status memo.

Keep file naming boring and consistent. Put dates at the front, use clear labels, and avoid duplicates with slightly different names. This is not about style. It is about being able to retrieve proof quickly when you revisit your position months later.

Before submission, do a coherence check across the full pack:

- Every major claim in your memo should trace to at least one dated document.

- Every status-period change should appear in the timeline.

- Every treaty note should match the same dates and facts used elsewhere.

What each status means for tax and filing exposure#

Status controls tax exposure first and filing complexity second. Canadian tax exposure turns on residency, not citizenship.

A factual resident of Canada is taxed on worldwide income. A deemed resident of Canada can apply when time in Canada reaches 183 days or more in the relevant fact pattern. That status can carry resident-level reporting complexity. A non-resident of Canada is generally taxed only on Canadian-source income, while still potentially facing Canadian filing obligations.

| Status | Core tax exposure | Filing pressure point |

|---|---|---|

| factual resident of Canada | Worldwide income in Canada | Consistent reporting across Canadian and foreign income streams |

| deemed resident of Canada | Resident-type exposure can apply, including broad income scope | Day-count support and classification must match records |

| non-resident of Canada | Generally Canadian-source income only | Correct separation of income under Part I tax and Part XIII tax |

For non-residents, income-type classification is critical. Canadian-source employed or self-employed income can fall under Part I tax, while other Canadian-source amounts may fall under Part XIII tax. The cited Part XIII rate is 25% and may operate as final tax in that regime. When income type, withholding, and reporting do not match, post-filing corrections may be required.

Cross-border files still depend on a well-documented status position. If status, withholding, and return treatment are misaligned across countries, extra reconciliation work can follow.

Before return prep is final, test each income stream against your status timeline. If a stream spans more than one status period, mark how you are treating it in each period. This avoids late edits where withholding logic and reporting logic diverge.

Use this checkpoint before filing season and again before submission:

- Reconfirm status logic against dated ties and travel records.

- Match each income stream to the correct status period, especially in part-year patterns.

- Verify withholding treatment by income type, including whether Part I or Part XIII applies.

- Confirm return reporting follows the same logic as withholding, then flag mismatches early.

If the signals conflict, resolve classification before filing. Filing first and reconciling later usually creates more work, not less.

Red flags that mean you should escalate to a professional#

Escalate before filing if your facts do not support one clear residency result.

- You may be considered a resident of another country that has a tax treaty with Canada, creating a potential dual-residency question before filing.

- Your living pattern changed mid-year and you cannot clearly classify your residency status for each period.

- You are relying on day count alone even though CRA also requires review of ties, length of stay, purpose, intent, and continuity.

- Your records conflict across travel history, banking activity, and family connections.

Form NR74 can help in close cases, but it is a request for CRA's opinion on whether you would be considered a deemed non-resident, not a guaranteed final outcome. If any red flag is present, pause and get cross-border advice before submission.

When you escalate, bring an organized package, not loose notes. Share your ties inventory, travel ledger, treaty memo if relevant, and your current status conclusion with supporting dates. That lets a professional focus on decision quality instead of spending time reconstructing your timeline.

A practical trigger is uncertainty that survives your own contradiction check. If you cannot explain your status in plain language with dated evidence, do not push forward to final filing.

Your 30-day checklist to reduce residency risk this year#

Use the next 30 days to build one clear, evidence-backed residency position before you file.

- Week 1: Complete a written ties inventory. List significant ties and other ties, then mark each as active, ended, or changed with dates. Attach supporting records. If you plan to file as non-resident, your file should show that most or all primary residential ties were severed.

- Week 2: Reconcile travel logs and day-count risk. Build one ledger with every entry and exit date, location, and trip purpose. Test both branches: less than 183 days and more than 182 days. Add notes on time spent in and outside Canada because day count is only one input and all relevant facts matter.

- Week 3: Finalize evidence and decision notes. Combine ties and travel records in one folder, then add a short memo explaining your status conclusion. If facts are close, decide whether to submit Form NR74 and keep related records together.

- Week 4: Run a pre-filing review if complexity remains. Escalate when your residency status is still unclear, key changes during the year are unclear, or records conflict. Share your ties inventory, travel ledger, and draft filing position before returns are prepared.

- Ongoing each month: Keep records current. Update the same file with new travel, tie changes, and supporting documents so next year's position is based on evidence, not memory.

For each week, define one deliverable you can verify:

- Week 1 deliverable: inventory complete, with dates filled and missing evidence flagged.

- Week 2 deliverable: travel ledger totals checked against both day-count branches.

- Week 3 deliverable: status memo finalized and aligned with timeline.

- Week 4 deliverable: unresolved items either closed or sent for professional review.

Use a short month-end review to keep momentum. Check whether new travel or tie changes affect your working conclusion, then update the timeline immediately. Small monthly updates are easier than rebuilding a year from scratch.

Two rules keep this checklist useful: determine status before filing obligations, and do not treat citizenship as the deciding factor. If your month-end review shows contradictions, resolve the facts before filing.

Conclusion#

A defensible filing is easier to support when you work through ties, day count, treaty conflict rules, and filing impact in a consistent order.

Begin with the facts that carry the most weight. A dwelling available in Canada and spouse or dependant location are significant indicators, while social or business connections and personal property are secondary factors reviewed in context. Citizenship or another country's domicile label is generally not decisive on its own.

Then apply day count. Time in Canada can change the result, including the 183-day sojourn branch in specific fact patterns, but it is not a universal shortcut. If your pattern changed during the year or your count is close to the threshold, rely on dated travel records instead of memory.

If two countries can treat you as resident, complete treaty tie-breaker analysis before filing. Tie-breaker rules can override domestic tests, so this is a core conflict-resolution step.

Keep one consistent file that supports what you submit: ties inventory, travel log, and brief written reasoning. If deemed non-resident treatment is in play, Form NR74 is a practical way to request CRA's opinion, and the submission and response should stay together.

Before filing, run one final check:

- Confirm your ties conclusion still matches year-end facts.

- Reconcile day count against travel records.

- Complete treaty tie-breaker analysis if dual-residency risk exists.

- Escalate early if facts still conflict or continue changing.

The goal is not a clever interpretation. The goal is a position you can explain, support, and keep consistent across your records and returns.

Frequently Asked Questions

What are significant residential ties in Canada?

Significant residential ties are key connections CRA considers as part of your overall fact pattern. CRA does not use a one-factor test and requires a review of all relevant facts, including residential ties. There is no single checklist that fits every case. Treat these ties as high-priority inputs when building your residency timeline.

Does the 183-day rule automatically make me a Canadian tax resident?

No. CRA includes day-count branches for less than 183 days and more than 182 days, but day count is only one input. Final status still depends on full facts, including ties and continuity of stay. Use day count to test your conclusion, not to replace tie analysis.

What is the difference between factual resident and deemed resident of Canada?

Residents and deemed residents are taxed in Canada on worldwide income, while non-residents are generally taxed only on Canadian-source income. In practice, keep your records clear enough to support whichever status label you apply.

Can I be a resident of Canada and another country at the same time?

Potentially. CRA's decision path asks whether you are considered a resident of another country that has a tax treaty with Canada. In that case, treaty tie-breaker rules, including outcomes under subsection 250(5), can affect whether you are treated as resident in Canada. That is why treaty analysis belongs before final filing when dual-residency risk exists.

What documents best prove my residency position if CRA reviews my file?

There is no universal document set that works in every case. Keep a dated file that matches the position you filed, including ties records, travel history, and written reasoning. If you submitted Form NR74, keep that submission and any CRA response in the same file. The strongest file is one where dates and facts are consistent across every document.

When should a freelancer hire a cross-border tax professional instead of self-filing?

Escalate before filing when facts point in different directions or dual-country residence is in play. Get help if treaty tie-breaker analysis may change your outcome or if you cannot support your position with consistent records. If you cannot explain your conclusion clearly from your own records, escalate.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 4 external sources outside the trusted-domain allowlist.

- finance.senate.gov/download/1995/07/11/tax-treatment-of-expatri...trusted

- canada.ca/en/revenue-agency/services/tax/international...external

- cbfinpc.com/residency-and-the-us-canada-tax-treaty-tie-b...external

- globalwealthprotection.com/why-the-183-day-rule-is-misunderstood-and-ho...external

- turbotax.intuit.ca/tips/how-to-determine-residential-ties-to-ca...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

Digital Nomad Taxes in 2026 With a Defensible Filing Plan

With digital nomad taxes, the first move is not optimization. It is figuring out where you may be taxable, where filings may be required, and what proof supports that position.

Ho Chi Minh City Digital Nomad Guide for a 30-Day Move (2026)

Ho Chi Minh City is a strong base if your priority is keeping work momentum while relocating. You get density, plenty of places to work from, and a social scene that can help you settle quickly. It is a weaker fit if your best days depend on calm streets, easy walking, and long stretches of quiet. In practice, Saigon tends to reward people who want convenience and activity more than retreat pace.

Value-Based Pricing for Creative Services That Protects Cashflow

Higher fees can improve project revenue, but they do not guarantee steady cashflow. You can send a larger bill and still face payment delays.