Quick Answer

Start by using an employee cost by country calculator as a controlled estimate, not final truth. Lock inputs, record the as-of date, and capture what is included or excluded in the total. Run separate cases for direct hire, Employer of Record, and Agent of Record when model choice is unsettled. Then assign a confidence level based on evidence quality, and escalate when unresolved items could change cost, reporting, or approval.

How to estimate total employee cost across countries#

An employee cost by country calculator is useful only if you can explain what sits inside the number and what happens to that estimate after approval. Finance and ops teams do not need a headline total by itself. They need a planning figure that can survive review and still make sense when payroll, reconciliation, and settlement workflows start moving money.

At its core, these tools estimate the total cost of employment for a given gross salary. That usually means salary plus employer-side costs such as taxes and mandatory pension or insurance payments. Some tools also include local employment costs or the provider fee in the output. That last point matters. If one quote includes a service fee and another does not, your country comparison is already skewed before anyone debates hiring strategy.

That is why transparent assumptions matter as much as the number itself. Labor cost assumptions can materially affect employment outcomes, and the OECD has noted that taxes can have a significant impact on employment. In practice, treat every estimate as a dated planning artifact, not final truth. If you cannot answer which cost components were included and whether fees were bundled into the total, you do not yet have something strong enough for budget approval.

A workable minimum record is simple and strict. For each market, keep the calculator output, the as-of date, the salary basis used, and a short note listing open questions. Add an owner name and approval status. That gives you a clear verification checkpoint before any hiring decision. Can another person retrace the estimate without reopening the whole analysis from scratch?

A common failure mode is copying a single total into a planning sheet without component detail. Later, teams may struggle to tie that estimate back to payroll entries or provider invoices, and reconciliation discussions can reopen what the calculator output actually covered.

The aim of this article is to make those handoffs explicit. You will leave with a practical way to compare countries, flag unknowns, and connect hiring assumptions to operational records rather than isolated budget cells. One scope note before we go further: calculator outputs are planning estimates, not legal or tax advice, and they should be revalidated whenever local rules, provider terms, or program setup changes.

Related reading: Is a No-Tax Country Really Tax-Free for a US Citizen?.

What an employee cost by country calculator actually measures#

An employee cost by country calculator is a model of employer-side burden, not just a salary figure. It usually combines gross pay with statutory and employer contributions, plus required employment costs such as mandatory insurance or pension items. Some tools also include benefits. Depending on the tool, this appears as a single "total cost of employment" output or a more detailed country-level breakdown for hiring decisions.

Treat total employer cost, gross-to-net, and net pay as related but different views. Gross-to-net shows how gross compensation maps to take-home pay, while some calculators show employer costs, statutory contributions, and net pay together. Keep both views in your planning model so budget decisions and offer competitiveness stay aligned.

Assumptions and scope are the control point. OECD's calculator documentation explicitly emphasizes policy scope and underlying assumptions, including regional treatment, and commercial tools can also vary by required input detail (country only vs. region/country/local area and compensation package). Two polished calculators can therefore produce different outputs because they are modeling different things.

Use each output as a dated planning artifact, not a permanent truth. Local tax and employment rules change, so every estimate needs an as-of date, scope note, and assumption record showing what was included and excluded. If that record is missing, treat the result as directional rather than approval-ready.

If your model also needs FX assumptions, see Cross-Currency Payment Cost Calculator: How to Model FX Costs Across 50 Country Pairs.

Inputs you must lock before you trust any output#

If inputs are not locked, the output is not decision-ready. Before anyone runs the calculator, define one required-input standard and use it for every market.

Use one consistent intake for each estimate:

- country

- subnational location when local rules vary

- salary basis

- contract type

- benefit assumptions

The goal is comparability. If one case uses annual gross salary in a capital city and another uses monthly salary with limited location or benefit detail, totals will look precise but will not be comparable.

A quick quality check prevents common errors: confirm whether salary is annual or monthly, and whether the entered figure is gross pay or closer to take-home intent.

Pick the engagement model first#

Choose the engagement model before comparing countries. Direct hire, Employer of Record (EOR), and Agent of Record (AOR) can support similar hiring plans, but they can produce different cost structures and assumption sets.

If you are still deciding between models, run separate labeled cases. If the model changes after approval, rerun the estimate so the budget matches the operating approach.

Build a source packet, not a screenshot habit#

Require a small source packet for each market:

- calculator export or saved output

- relevant Country Guides

- a short note on unresolved assumptions and ownership

Treat that packet as the decision record, not the headline number. A screenshot in chat usually omits version context, date context, hidden fields, or exclusions.

Use the same freshness discipline shown on eCFR pages: keep an explicit "up to date as of" date and a last-amended reference in your notes. Set one hard rule: no decision meeting without documented inputs, owner sign-off, and explicit unknowns tied to local tax legislation. If key points are still unclear, treat the meeting as estimate review, not final approval.

For a step-by-step walkthrough, see How to Create an Employee Recognition Program for Distributed Teams.

Build a country comparison sheet finance can defend#

Build one side-by-side sheet for all candidate country scenarios so finance can approve a cost model, not a set of disconnected screenshots. Each row should be one approved scenario only (for example, one country plus one engagement model), with separate rows when you are testing alternate models.

| Country scenario | Salary | Taxes | Statutory contributions | Benefits | Insurance | Total employer cost | Confidence level | Global payroll complexity | Payout path | Ledger reconciliation effort | Method gap | Source and as-of |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Candidate A | input | input | input | input | input | calculated total | High / Medium / Low | Low / Medium / High | local payroll, EOR invoice, or other | Low / Medium / High | Visible | export, Country Guide, date |

| Candidate B | input | input | input | input | input | calculated total | High / Medium / Low | Low / Medium / High | local payroll, EOR invoice, or other | Low / Medium / High | Partially visible | export, Country Guide, date |

| Candidate C | input | input | input | input | input | calculated total | High / Medium / Low | Low / Medium / High | local payroll, EOR invoice, or other | Low / Medium / High | Opaque | export, Country Guide, date |

Use the sheet to make uncertainty explicit. The total should be traceable to row components, and the confidence level should reflect evidence quality, not intuition.

Make confidence evidence-based#

Confidence should come from the packet behind each row: calculator export, relevant Country Guides, stated assumptions, and clear dates. If a tool shows only a headline total and hides component logic, record that gap directly.

Keep freshness metadata in the table as well. Use the same pattern as regulatory pages that show both a current-as-of and last-amended date (for example, eCFR Title 2 shows "up to date as of 3/27/2026" and "last amended 2/26/2026").

Track method gap, not just totals#

Method visibility is a decision signal. Use one of these labels consistently:

| Label | Definition |

|---|---|

| Visible | Enough component or formula logic to understand how the total was built. |

| Partially visible | Some components are clear, but key assumptions or steps are hidden. |

| Opaque | Output is provided with little or no usable method detail. |

If two tools differ materially and neither shows method detail, treat both outputs as directional and escalate before budget approval.

Add operational burden competitors skip#

Add columns for global payroll complexity, payout path, and ledger reconciliation effort. These fields often determine whether a country that looks cheaper on paper is actually harder and costlier to run.

When total employer costs are close, default to the cleaner payout path and lower reconciliation effort unless there is a stronger hiring constraint. After baseline totals are stable, sanity-check them against broader employer cost benchmarks by country.

Decide when calculator estimates are enough and when to escalate#

Use calculator output as estimate-only when acceptable variance will not change the decision. Escalate when unresolved tax treatment could change cost, reporting, or the hiring path.

That is the step after your comparison sheet: decide whether confidence in the number is enough for the decision in front of you.

Use variance tolerance, not optimism#

For low-risk planning, calculator output with documented assumptions can be enough. Use it for directional planning where reasonable variance will not change the go/no-go decision, and log it as provisional.

Escalate review when any of these are true:

- hiring is high-volume or repeated in the same market

- margin is thin enough that employer-cost drift changes the business case

- the engagement model or local labor/tax interpretation is still unresolved

- tax-document handling is unclear (for example, W-8, W-9, 1099, FEIE, or FBAR workflow)

Treat FEIE assumptions as a specific review trigger#

If FEIE is being assumed in planning, require explicit review. IRS framing is narrow: qualifying individuals must have foreign earned income, have a tax home in a foreign country, and still file a U.S. return reporting the income.

Under the physical presence route, the test is 330 full days in any 12-month period, and those days do not need to be consecutive. If 330 full days are not met, the physical presence test fails regardless of reason. For 2026, the maximum exclusion is $132,900 per person.

A simple evidence pack is enough for escalation: document the tax topic, unresolved point, country, owner, and whether the issue can change employer cost, worker reporting, or payout handling.

Make the decision state explicit#

Do not leave escalation in chat notes. Force one approval state in the log:

| State | Use when |

|---|---|

| Estimate-only | Directional planning with accepted variance |

| Estimate plus review | Budgeting can continue but review is still required |

| Hold decision | Unresolved issues could change structure, cost, or filing treatment |

Before approval, confirm that the state is set, an owner is named, and unresolved items are listed. This avoids approving a number first and discovering later that tax-document handling or local interpretation changes the real path to hire.

Turn calculator results into ledger and payout operations#

An approved estimate is operational only when every modeled cost can be posted, tracked, reconciled, and settled. If it cannot move end to end through that path, it is still a planning number.

Map each modeled cost to a ledger path#

Break each country estimate into the components you will actually close: salaries or wages, employer taxes, and benefits. Payroll is the total workforce cost across those elements, and even direct labor calculations still require careful tracking to account for every dollar.

Treat unpaid payroll-related amounts as accrued payroll until they are paid and cleared. This is where teams usually lose control when one estimate is booked early but invoices, remittances, and benefit charges settle on different dates.

| Modeled component | Operational record path | Reconciliation question |

|---|---|---|

| Salary or direct labor | Expense posting tied to person, country, program, and pay period | Can you trace the booked amount to the payroll register or provider statement? |

| Employer taxes or statutory contributions | Liability or accrual entry that clears on payment | Does the unpaid balance clear from accrued payroll at settlement? |

| Benefits and mandatory employer costs | Separate expense or liability record with country and period tags | Is it visible in the settlement flow, or flagged for a separate close check? |

At minimum, tag each component with country, pay period, program or vendor reference, and estimate version. The control standard is simple: every modeled component has one ledger destination and one reconciliation owner.

Lock the operating sequence before go-live#

Do not design payout operations after activation. Fix and document the sequence first:

| Step | Checkpoint |

|---|---|

| 1. Estimate approved | with assumptions, source date, and decision state |

| 2. Vendor or program selected | so source records are known |

| 3. Payout design defined | with batch structure and settlement references |

| 4. Control checks completed | with sample postings, liability clears, and named exception owners |

| 5. Go live | only after a dry run reconciles cleanly |

If the engagement path changes, update the posting map before launch.

Make payout and status tracking auditable#

Define how payout batches are created, tracked, and retried, and keep retry handling consistent so unclear outcomes do not create duplicate operational records. Route provider updates into internal status changes through your event intake path, and send mismatches to an exception queue instead of forcing close assumptions.

Use one checkpoint before first live payroll in each country: for every modeled cost component, show a record path from estimate to posting to reconciliation to settlement. If that path is missing, month-end close will be manual.

Related: Payout Support Ticket Cost Calculator: What Delayed Disbursements Really Cost Your Platform.

Failure modes that break budgets after hiring starts#

Budgets usually break after hiring starts when teams keep using a static estimate while the cost definition changes. If full employee cost runs 25% to 40% above the offer-letter number, stale assumptions become a material gap, not a rounding issue.

The most common failure pattern is not one large error. It is a stack of small misses in taxes, benefits, and overhead that only becomes clear at close.

Setup drift turns a good estimate into an old one#

A calculator output is only reliable while its inputs are current and explicit. When assumptions go stale, totals drift quickly.

A practical warning sign is heavy reliance on defaults. One cited calculator uses a default 10% payroll-tax assumption for approximate FICA plus FUTA/SUTA, while also listing specific components like Social Security (6.2%) and Medicare (1.45%). Defaults are useful for speed, but they can hide changes in component-level cost.

Use a simple control: keep an up-to-date assumption record for each active country estimate, including the latest export, its "as of" date, and any open assumption owners. If that record is incomplete, treat the total as directional and refresh before hiring or budget decisions.

Blended totals hide what changed#

Another failure mode is carrying one headline number without checking whether all cost components still match current reality. Total employee cost includes salary plus employer-side taxes, benefits, and overhead, so a single rolled-up figure can mask where drift started.

Anchor reviews at component level, not only at the top-line total. If one component changes and the rest are left untouched by default, the budget risk is usually already in motion.

Tooling gaps delay correction#

Teams also miss cost impact when they do not have a practical way to calculate and revisit changes over time. In practice, that shows up as late detection rather than quick correction.

Keep the model operational by revalidating assumptions on a fixed cadence and before commitment points. That is cheaper than discovering at close that the approved budget and actual hire burden diverged.

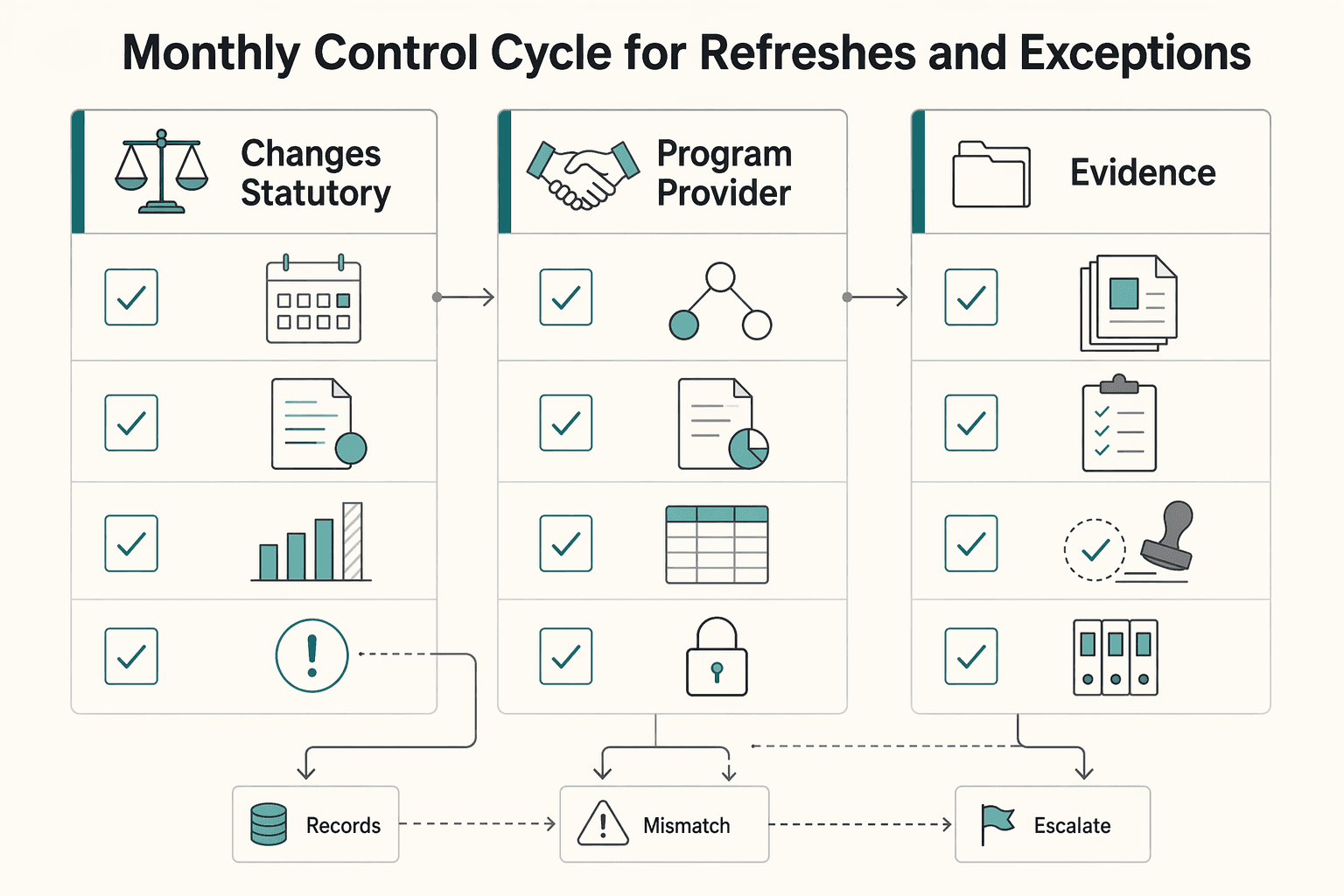

Monthly control cycle for refreshes and exceptions#

Treat this as a standing control: an estimate is only as reliable as the dated assumptions, change log, and named approver behind it.

Set a consistent review cadence (monthly if that fits your operating rhythm): recheck active markets, rerun inputs, and log what changed, when, and who approved it. If a legal, program, or payout-eligibility change affects the model inputs, rerun immediately and replace the prior estimate.

Keep rerun triggers explicit:

- changes to statutory contributions, benefits assumptions, or payout eligibility

- program or provider changes that alter how costs are modeled

- reconciliation or compliance issues that prevent modeled and operational records from matching

Maintain an exception register until each item is resolved. Track country, reference, owner, opened date, and blocking impact so unresolved items stay visible.

Keep one evidence bundle per market: latest estimate, approval notes, and links to tax/compliance artifacts. Also record inclusion and exclusion rules explicitly, because unclear population rules can distort comparisons over time.

Conclusion#

Use this process to keep planning estimates reviewable and traceable, but do not treat it as enough by itself to set country-specific calculator controls, reconciliation design, or hiring-cost governance workflows.

The exact checkpoints, ownership model, and refresh cadence should still be set by your finance and compliance policies and validated against current country-specific requirements.

A practical next step is to treat this as an open validation item:

- define the countries and hiring models you need to evaluate

- document assumptions and owners for each estimate

- confirm legal, tax, payroll, and reconciliation requirements with qualified internal or external advisors before approvals

This keeps planning decisions traceable.

Frequently Asked Questions

What is included in an employee cost by country calculator?

Most calculators are trying to show the employer-side burden, not just salary. In practice, that usually means employer costs plus statutory contributions, and some tools also show net pay so you can compare the company view and worker view together. Treat base salary as the starting point, not the full answer.

Is calculator output final or only an estimate?

It is an estimate for planning, not a final legal or tax determination. The number is only as reliable as the inputs and assumptions behind the tool. If you cannot state the as-of date and assumptions, do not treat the result as approval-ready.

Why can two calculators show different totals for the same country and salary?

Because calculators do not have to use the same method, assumptions, or scope. One tool may include employer costs or statutory contributions that another leaves out or treats differently. A practical red flag is when neither tool shows what is included. In that case, treat both as directional and escalate before you lock budget.

Which inputs matter most before trusting a result?

Country selection is the minimum, and many tools also require role details to estimate total employment cost. You should also confirm your hiring model (for example, direct hire, Employer of Record, or Agent of Record) because cost structure can change with that choice. If contract type or benefit assumptions are still open, your confidence level should stay low.

When should we escalate from calculator estimates to legal or tax review?

Escalate when the decision is high-stakes or the assumptions are unclear. You should also escalate when local treatment is uncertain or key model choices are still in flux. A useful evidence pack is the calculator output, any relevant country guidance, and a short note listing unresolved assumptions.

How often should finance teams rerun country cost estimates?

Rerun when core inputs or assumptions change. That includes changes in statutory contributions, benefits assumptions, country selection, role details, or hiring model. The checkpoint that matters is simple: every live estimate needs an owner, an as-of date, and a visible reason if it changed.

How do we connect hiring cost estimates to payout and reconciliation operations?

Use calculator outputs as planning inputs, then validate payout, ledger, and reconciliation workflows separately. This section’s source material supports cost-estimation scope, not downstream payment or accounting mechanics.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- 2009-2017.state.gov/m/fsi/tc/79700.htmtrusted

- acquisition.gov/far/part-31trusted

- bls.gov/news.release/archives/ichcc_08262010.htmtrusted

- comptroller.war.gov/portals/45/documents/fmr/volume_12.pdftrusted

- congress.gov/bill/119th-congress/senate-bill/1071/text/eahtrusted

- congress.gov/bill/119th-congress/house-bill/3838/texttrusted

- ec.europa.eu/eurostat/documents/64157/4374310/11-STANDARD...trusted

- ecfr.gov/current/title-2/subtitle-A/chapter-II/part-200trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Model FX Payout Costs Across 50 Country Pairs with a Cross-Currency Calculator

---

Employer Cost by Country Benchmark for Finance and Ops Teams

Salary-only comparisons fall apart as soon as you try to tie them to real employer spend. A usable employer cost by country benchmark has to include the full cost stack: wages or salary, benefits, payroll taxes, social security, and any employer-paid health insurance or pension contributions that apply in that jurisdiction.

Payout Support Ticket Cost Calculator for Delayed Disbursements

Delayed disbursement tickets are not always just a queue problem. In many teams, one customer contact triggers additional internal follow-up, so visible ticket counts can understate total operating effort.