Quick Answer

Yes. Moving to a no-tax jurisdiction does not end U.S. obligations: you may still need Form 1040, and separate foreign-account reporting can apply through FinCEN Form 114. A workable plan sets the filing baseline first, then decides FEIE, FTC, and housing treatment before relocation. Keep day counts, legal-stay evidence, and currency-conversion support current during the year so your position is defensible when deadlines arrive.

Living in a No-Tax Country as a US Citizen#

A no-tax destination can lower local income tax, but it does not end U.S. filing and reporting duties. U.S. citizens abroad are still taxed on worldwide income, and tools like the FEIE or Foreign Tax Credit are tied to filing a U.S. return.

Use this as an execution guide, not a country ranking. The goal is to help you decide what to verify, what records to keep, and when your facts are complex enough to escalate to a tax professional.

Start with these checkpoints:

- Set your baseline first. Filing and reporting duties generally still apply abroad, including reporting taxable income under the Internal Revenue Code.

- Lock your calendar early. The regular due date is April 15, with an automatic overseas extension to June 15 for eligible filers.

- Keep account reporting separate. Some foreign account reporting can apply even when accounts produce no taxable income, and FBAR is filed electronically through the BSA e-filing system.

- Keep records current all year. Amounts on a U.S. return must be in U.S. dollars, so keep your conversion records and dates with your tax files.

The goal is lower tax friction with records you can defend. If your plan assumes moving abroad ends U.S. obligations, reset that assumption first. For a deeper legal baseline, read Tax Residency vs. Citizenship-Based Taxation: The US Anomaly and return with your facts.

Start With the Right Tax Mental Model#

Start with a two-layer model before you compare countries. U.S. tax treatment and local tax residency are different questions. On the U.S. side, IRS noncitizen status rules determine whether someone is treated as a nonresident or a resident for federal tax purposes. On the local side, residency rules determine where else you may owe tax. Mixing those two lenses is where expensive errors start.

| Check | What to verify | Key detail |

|---|---|---|

| Scope check | If guidance starts with "if you are not a U.S. citizen," treat it as noncitizen-specific until confirmed otherwise | The green card test and substantial presence test apply to people who are not U.S. citizens |

| Calendar check | Map travel and status changes across January 1 through December 31 and test for a 183-day trigger | Someone can be nonresident for part of the year and resident for the rest, with a dual-status income tax return required |

| Authority check | Keep source titles straight in your notes | Example source title: Publication 519 (2025), U.S. Tax Guide for Aliens |

When you review IRS residency-status material, check scope first. In that IRS approach, the green card test and substantial presence test apply to people who are not U.S. citizens, and IRS notes that some elections can override those tests.

Timing matters too. IRS frames this determination on a calendar-year basis, January 1 through December 31, and examples use a 183-day substantial presence threshold. In that pattern, someone can be nonresident for part of the year and resident for the rest, with a dual-status income tax return required.

Before choosing a destination, run this check against your facts:

- Scope check: if guidance starts with "if you are not a U.S. citizen," treat it as noncitizen-specific until confirmed otherwise.

- Calendar check: map travel and status changes across January 1 through December 31 and test for a 183-day trigger.

- Authority check: keep source titles straight in your notes, such as Publication 519 (2025), U.S. Tax Guide for Aliens, so you do not apply the wrong rule set.

If your plan assumes moving abroad automatically resolves U.S.-side filing outcomes, pause and confirm scope before you commit. If you want a deeper dive, read Dubai, UAE: The Ultimate Digital Nomad Guide (2025).

No Income Tax Is Not No Tax#

Zero local income tax is not the same as being tax-free for a U.S. citizen. The U.S. still taxes worldwide income, so the headline local rate is only one input.

Treat "tax-free" marketing as a claim to verify, not a complete plan. A zero local income-tax headline does not remove U.S. tax and reporting duties.

The Foreign Tax Credit is where many optimistic plans break. FTC is designed to reduce double taxation, but it depends on foreign taxes paid or accrued on income also subject to U.S. tax, and it generally applies only to qualifying income-type foreign taxes. In low- or zero-income-tax setups, that often means less credit to use.

FTC prep also carries execution risk. Claiming FTC usually requires Form 1116, and separate Form 1116 filings may be required by income category. If your outcome depends on perfect categorization, treat that as a red flag.

| Compare lens | Why it matters | Practical checkpoint |

|---|---|---|

| Local personal income tax | Sets the headline number | Treat it as one input, not the full tax picture |

| FTC eligibility | Depends on foreign taxes paid or accrued that are also subject to U.S. tax | Confirm whether you have qualifying foreign income-type taxes to credit |

| FTC filing categories | Can require separate Form 1116 filings by income category | Map your income categories before filing |

| U.S. compliance timeline | Filing and account-reporting duties can still apply abroad | Build around the April 15 to June 15 automatic extension and required account reporting |

Keep one rule explicit: if you exclude foreign earned income or housing costs, you generally cannot also claim FTC on that excluded income. IRS guidance also warns that taking FTC in that context can put one or both exclusion elections at risk.

U.S. account reporting can still apply even if foreign accounts produce no taxable income. Calendar-year filers abroad generally get an automatic extension from April 15 to June 15. Build your calendar early and stress-test your plan under conservative credit assumptions.

Use a Five-Step Move or No-Move Decision Sequence#

Use this as a hard gate: if any step fails, pause the move. This keeps legal stay, tax treatment, and filing load aligned before relocation.

| Step | Focus | Key requirement |

|---|---|---|

| 1 | U.S. baseline | Start with whether you will file a U.S. return based on your facts, then flag any parallel reporting tracks |

| 2 | Residency practicality | Choose a status you can maintain legally and document all year |

| 3 | Relief logic | Choose FEIE or FTC logic before you move; Form 1116 is category-specific |

| 4 | Admin load | Reject the setup if records cannot tie work dates and income categories cleanly |

| 5 | Compliance cadence | Set recurring checkpoints for document capture, categorization, and return prep |

- Confirm your U.S. baseline before comparing countries. Start with whether you will file a U.S. return based on your facts, then flag any parallel reporting tracks. Build your account and income inventory now, not after opening foreign accounts.

- Test residency practicality first, tax second. Choose a status you can maintain legally and document all year. For FEIE-related residence or presence positions, legal stay is a gate: IRS guidance says you may not be treated as a bona fide resident or physically present if you are in a country in violation of U.S. law. Keep dated travel, permit, and address records.

- Choose relief logic before you move. FEIE can reduce taxable income, but you still file a U.S. return reporting that income. For 2025, the FEIE maximum is $130,000 per qualifying person; for 2026, $132,900, with day-based adjustment for partial-year qualification. If both spouses qualify in 2025, the combined exclusion can reach $260,000. Housing relief is figured first and is generally capped at 30% of the FEIE maximum, with general housing limits of $39,000 (2025) and $39,870 (2026). If you rely on FTC, Form 1116 is category-specific: one category checkbox per form, with separate country lines when taxes were paid to more than one country.

- Price admin load for your real setup. A setup with one income category and one foreign country is usually simpler than one with mixed income categories and taxes paid to multiple countries. FEIE timing also tracks when work is performed, not only when cash is received. If your records cannot tie work dates and income categories cleanly, reject that setup.

- Build your yearly compliance cadence before relocation. Set recurring checkpoints for document capture, categorization, and return prep so filing is not a year-end rebuild. If you may rely on a waiver of time requirements due to war or civil unrest, verify the country and dates in that year's IRS Internal Revenue Bulletin list.

Decision rule: move only when all five steps work under normal operations, not perfect behavior. If step 3 is still unclear, review FEIE vs. FTC: A Strategic Choice for High-Earning US Expats before you commit.

Before you choose a country, run your facts through a simple residency log so your filing position is defensible later: Tax Residency Tracker.

Choose FEIE, FTC, and Housing Relief With Clear Rules#

Start with this planning sequence: if local income tax is near zero, test FEIE plus housing relief first; if local income tax is meaningful, test FTC in parallel. That order can reduce late surprises, but it does not remove U.S. filing. Even when income is excluded, it still must be reported on a U.S. tax return, and U.S. citizens and resident aliens are taxed on worldwide income.

| Local tax picture | First lane to test | Why this lane may lead |

|---|---|---|

| Local income tax is near zero | Foreign Earned Income Exclusion (FEIE) + foreign housing relief | If little tax is paid abroad, FTC value may be limited |

| Local income tax is material | Foreign Tax Credit (FTC), with FEIE and housing tested in parallel | Paid foreign tax may create credit value when records are clean by category |

Build FEIE eligibility before filing season. FEIE applies to earned service income, including wages or self-employment income for services performed in a foreign country, and is claimed on Form 2555. If you qualify for only part of the year, adjust the maximum by qualifying days. The published cap is $130,000 for 2025 and $132,900 for 2026 per qualifying person.

Compute housing before FEIE. Housing is figured first because it limits how much FEIE room remains. The general housing expense limit is 30% of the FEIE maximum, with general limits of $39,000 (2025) and $39,870 (2026).

Set up FTC mechanics early. Form 1116 is category-based, and each form allows only one checked category box, so mixed income types can require multiple forms. Waiting to sort categories until return assembly can create avoidable rework and force late position changes on your U.S. return.

Use this checkpoint list before year-end:

- Income type: separate earned service income from other streams before drafting Form 2555 or Form 1116.

- Employment structure: confirm employee versus self-employed status so classification stays consistent across the return.

- Local tax paid: retain proof of foreign taxes paid if you may claim FTC.

- Housing profile: keep monthly housing records tied to leases, invoices, and statements.

- Documentation quality: maintain day-count support, legal-stay records, and location history; income earned during periods that violate U.S. travel-restriction law does not qualify as foreign earned income, and related housing expenses cannot be counted for housing relief.

If your facts are high-income, mixed-category, or split-year, run a side-by-side decision before filing: FEIE vs. FTC: A Strategic Choice for High-Earning US Expats.

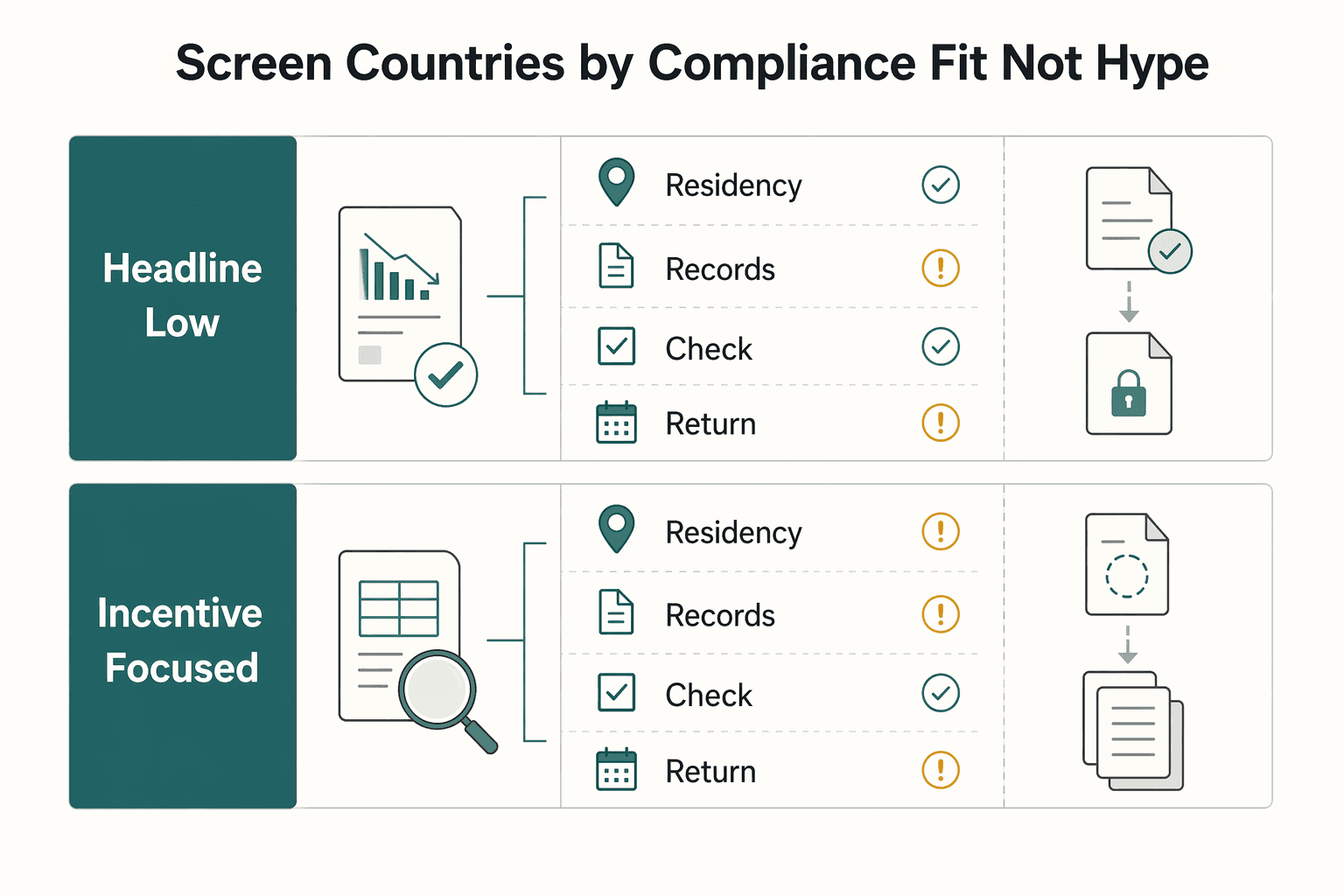

Screen Countries by Compliance Fit, Not Hype#

Pick the country where you can comply consistently, not the one with the strongest low-tax headline. Headline rates are a starting signal, not a final decision rule.

| Country set | Headline appeal | What that headline misses | What to verify before committing |

|---|---|---|---|

| Headline low-tax options | Lower marginal personal income tax figures | Headline rates do not prove your setup is administratively workable | Exact residency path, renewal cycle, evidence requirements, and whether your facts stay consistent year-round |

| Incentive-focused options | Preferential rates in one tax category | Lower stated rates do not guarantee lower ongoing compliance effort | Program terms, reporting obligations, and whether administration is predictable for your income pattern |

A common comparison error is treating marginal rates as real cost. Marginal figures do not account for deductions, exemptions, or rebates, and effective rates are often lower. Broad country tables are also not exhaustive measures of true burden, so one-line comparisons can misread both tax burden and compliance effort.

Country-level numbers can hide local variation. In federations, published national values may be averages that differ by state or province. If a source is older context, like a VAT map labeled October 2019, treat it as directional and re-check current rules before committing.

Use this checkpoint before a final move decision:

- Confirm the exact residency program and its current eligibility and renewal timing.

- Compare multiple tax categories, not only personal income tax, including corporate, capital gains, wealth, property, inheritance, and sales or VAT where relevant.

- Verify whether country-level figures are averages and whether subnational variation changes your expected outcome.

- Date-stamp each rule you rely on and re-verify near commitment.

- Stress-test documentation needs for both local compliance and home-country filing so your reporting position stays defensible.

Decision rule: choose the place where your compliance loop remains stable across multiple years, even if the headline rate sounds less dramatic. If you want to reset the U.S. lens behind that choice, review Tax Residency vs. Citizenship-Based Taxation: The US Anomaly.

Build a Pre-Move Evidence Pack Before You Relocate#

Build your evidence pack before you move so Form 8938 and FBAR decisions stay clear, separate, and defensible. The avoidable mistake is treating them as one filing track and rebuilding records at year-end.

| Reporting item | Where it is filed | Trigger to check | Practical filing note |

|---|---|---|---|

| Form 8938 | Attached to your income tax return with the Internal Revenue Service (IRS) | Total specified foreign financial assets exceed the applicable threshold for your status and location | File by your annual return due date, including extensions |

| FBAR (FinCEN Form 114) | FinCEN through the BSA E-Filing System | Aggregate foreign account value exceeds $10,000 at any time in the calendar year | Separate from the tax return and not filed with the IRS |

Treat this as an internal control set and keep your account and tax-support records in one organized archive.

Use this pre-move checkpoint:

- Track foreign account balances through the year so you can test the FBAR $10,000 aggregate threshold.

- Mark your likely Form 8938 threshold lane by filing status and residence: $50,000/$75,000, $100,000/$150,000, $200,000/$300,000, or $400,000/$600,000.

- Tag which holdings may be specified foreign financial assets and which may be excluded, including some accounts maintained by a U.S. payer.

- Keep current-year records organized so your income tax return, Form 8938, and FBAR review use consistent information.

- Maintain a dated index so each document can be found quickly.

Two common misses are assuming Form 8938 and FBAR are duplicates, and waiting until year-end to reconstruct balances. One boundary matters: if no income tax return is required for the year, Form 8938 is not required even if asset values are high.

If a key document is missing, run a fallback immediately:

- Log the gap with an owner and target date.

- Pull substitute evidence from available records.

- Add a short memo describing the gap and replacement record.

- Re-test both Form 8938 and FBAR thresholds after the file set is updated.

After updating the file set, apply this decision rule: before relocating, confirm your records still let you evaluate both filing thresholds even if one document is missing.

Run a First-Year Compliance Calendar You Can Actually Maintain#

Treat year one as an execution discipline. Keep your annual-return file, Form 8938 support, and FinCEN Form 114 support (if applicable) current so filing is assembly, not reconstruction.

| Cadence | What to do | Why it matters |

|---|---|---|

| Monthly | Capture income, account activity, and supporting statements as they occur | Helps reduce missed items and year-end rework |

| Quarterly | Re-check specified foreign financial asset levels and review Form 8938 data quality | Can help catch threshold-lane or classification issues early |

| Annual filing lane | Complete your annual return (for many individuals, Form 1040), then attach Form 8938 if required | Form 8938 is filed with the annual return and follows that return's due date, including extensions |

| Separate reporting check | Confirm whether FinCEN Form 114 is also required | Filing Form 8938 does not replace a separate FBAR obligation when FBAR is otherwise required |

| Pre-submission | Reconcile disclosures against account statements and payment records | Helps lower mismatch risk before filing |

Use one monthly closeout routine: lock income totals, save statements, and tag records to the correct tax year or calendar year. Keep a simple index that maps each disclosure field to supporting records so you can trace amounts quickly.

At quarterly checkpoints, validate your Form 8938 lane without guessing exact thresholds. Certain U.S. taxpayers report when aggregate specified foreign financial assets exceed applicable thresholds, and higher thresholds can apply for joint filers and taxpayers residing abroad. Confirm the form year designation is correct. If you are not required to file an income tax return for the year, you do not need to file Form 8938 for that year.

Use this minimum monthly capture checklist:

- Income ledger: date, payer, amount, currency

- Foreign account activity log tied to statements

- Asset register for items that may be specified foreign financial assets

- Draft mapping from disclosure fields to evidence

- Exceptions log for missing files, owner, and target resolution date

Before filing, do one reconciliation pass across return disclosures, payment records, and account statements. If totals do not tie, stop and resolve first. If your process still depends on heroic spring cleanup, redesign your calendar now.

Avoid the Expensive Mistakes Competitor Guides Skip#

The biggest costs usually come from wrong assumptions, not hard math. Local zero-tax treatment does not remove U.S. filing duties.

- Assuming "no local tax" means "no U.S. return"

FEIE is not automatic. It applies only if you are a qualifying individual, and the income is still reported on your U.S. return. If you qualify for only part of the year, the FEIE maximum is adjusted by qualifying days.

- Using country lists instead of your actual facts

Eligibility can fail based on your timeline and exception rules, not just a country headline. IRS describes two exceptions to minimum time requirements, and waiver-country treatment is published annually. Travel-restriction rules are also country-specific. In this context, Cuba is currently called out, and income earned during a period of violation does not qualify as foreign earned income.

- Treating FEIE limits as static

FEIE limits change by tax year, and partial-year qualification can reduce what you can exclude. For tax year 2025, the maximum exclusion is $130,000 per qualifying person (or foreign earned income, if lower); for 2026, it is $132,900. Housing limits are also year-specific.

- Waiting until filing season to decide FEIE vs. FTC

FTC prep is form-driven. Form 1116 is prepared separately by income category, one category box per form, and amounts are reported in U.S. dollars except where specified. FEIE also has sequencing rules, including calculating any foreign housing exclusion first because it limits FEIE.

Before year-end, run this checkpoint:

- Confirm your FEIE qualification timeline and partial-year risk.

- Confirm current-year FEIE and housing limits before you file.

- Lock FTC category mapping early for Form 1116.

- Escalate quickly if travel patterns or country status changed mid-year.

For a deeper decision method, see FEIE vs. FTC: A Strategic Choice for High-Earning US Expats.

Know When to Bring in a Professional#

If your core facts are still unclear when you prepare your U.S. return, bring in a professional before filing. The goal is to lock a defensible position on residency, FEIE or FTC treatment, and reporting before those choices harden on paper.

| Trigger | What is unclear | Article detail |

|---|---|---|

| Residency or day-count records | You cannot clearly document tax residency facts or foreign presence days | This includes whether you meet the 330-day path |

| Complex year and weak records | Your year includes mixed income types, multiple foreign accounts, or frequent country moves | Your records do not cleanly support your planned treatment |

| FEIE position | You are unsure how to report it on Form 2555 or Form 2555-EZ | Income is still reported on your U.S. return |

| FTC setup | Your Form 1116 setup is unsettled | This includes separate forms by income category and separate country lines or columns when multiple countries or territories are involved |

| Other information reporting | You are unsure whether additional international information reporting may apply to your facts | Bring in a professional before filing |

Escalate early if any of these are true:

- You cannot clearly document tax residency facts, foreign presence days, or whether you meet the 330-day path.

- Your year includes mixed income types, multiple foreign accounts, or frequent country moves, and your records do not cleanly support your planned treatment.

- Your FEIE position is unclear. You are unsure how to report it on Form 2555 or Form 2555-EZ while still reporting income on your U.S. return.

- You are choosing FTC treatment and your Form 1116 setup is unsettled. This includes separate forms by income category and separate country lines or columns when multiple countries or territories are involved.

- You are unsure whether additional international information reporting may apply to your facts.

Edge-case years need extra caution. There are two exceptions to minimum time requirements, but they are country- and date-specific and tied to IRS bulletin listings. Travel-restriction rules can also block FEIE treatment for a period. Cuba is currently the named restricted country, and income earned during a violation period does not qualify as foreign earned income.

If any trigger applies, ask for a written position and keep it in your tax file. It is not legally required, but it gives you a clear rationale if the IRS questions your treatment later. If your main uncertainty is FEIE versus credit strategy, review FEIE vs. FTC: A Strategic Choice for High-Earning US Expats before your advisor meeting.

Use Gruv Records to Make Compliance Less Fragile#

Gruv records help when they create a complete, reconciled evidence trail before filing. If the records do not tie cleanly to what you plan to report on Form 1040, reconcile them first.

Use only features enabled in your setup, and mark gaps early. Where supported, keep invoice history, payment records, payout status changes, and exportable transaction history together. If coverage differs by market or program, keep an external fallback log so missing data is explained instead of guessed at year-end.

Map each record to a filing purpose well before deadlines.

U.S. citizens and resident aliens abroad are taxed on worldwide income, and FEIE or FTC benefits require filing a U.S. return. When deciding whether a return is required, excluded foreign earned income and foreign housing amounts are still considered in gross income. For self-employed filers, gross income includes the Gross Income line on Schedule C (Form 1040).

Keep currency handling in the same record set. Amounts on a U.S. return must be in U.S. dollars, so store source-currency totals and USD translations in one reconciliation packet.

A lean monthly packet should include:

- Invoice register with date, payer, currency, and amount

- Payment and payout log with status history

- Gruv export snapshot where enabled, plus fallback log where not

- USD conversion record tied to the same transaction IDs

- Foreign account inventory for FBAR and Form 8938 checks when applicable

Use one evidence base, but keep filing tracks distinct. Your IRS return and Treasury account reporting can overlap in facts, but they are separate filing obligations.

If your setup includes policy gates, approvals, or trace views, use them to keep records disciplined. Confirm what is active in your environment, and treat Gruv records as compliance support, not tax or legal advice.

Pick Compliance You Can Repeat#

The decision is straightforward: choose a filing cadence you can repeat each year without chaos. For a U.S. citizen living abroad, the durable advantage is clean records, predictable Form 1040 prep, and clearly separated account-reporting obligations.

A strong plan keeps three things true all year:

- Your tax residency facts are documented consistently.

- Your Form 1040 can be prepared from records you already maintain.

- Your foreign-account reporting path is defined in advance, including when Form 8938 applies and when separate FBAR filing may still apply.

Use this five-step sequence before you commit to relocation:

- Confirm your U.S. baseline filing path, including exactly how Form 1040 will be prepared from your records.

- Confirm you can maintain legal presence and records that support your residency facts each year.

- Define your tax position early so it is supportable and repeatable.

- Stress-test admin load for normal and messy years, and reject options that work only with perfect execution.

- Build your evidence pack before relocation and set recurring data-quality checks.

Keep one checkpoint non-negotiable. If Form 8938 is in scope, attach it to your annual return and file by that return's due date, including extensions, with the correct calendar year or tax year shown. U.S. citizens are in the specified-individual category for Form 8938. Thresholds vary by filer profile. IRS notes a $50,000 aggregate value trigger for certain taxpayers, with higher thresholds for some groups, including joint filers and taxpayers residing abroad. Re-check your filer profile each year instead of relying on an old assumption.

Do not merge separate obligations: filing Form 8938 does not replace FBAR, which is FinCEN Form 114. Also, if you are not required to file an income tax return for the year, Form 8938 is not required.

Final rule before relocation: if you cannot map each account, asset, and income record to a clear filing lane today, pause. Run the five steps, finish the evidence pack, then commit.

If you want a cleaner, repeatable way to keep invoice, payout, and transaction records together for year-end prep, review Gruv for Freelancers.

Frequently Asked Questions

Can a U.S. citizen live in a no-tax country and still owe U.S. tax?

Potentially, yes. In no-tax jurisdictions, the Foreign Tax Credit is often limited because you can claim it only for qualifying foreign taxes imposed on you. Your U.S. tax result still depends on your specific facts and elections.

Do I still need to file `Form 1040` if my country has zero personal income tax?

The IRS excerpts here do not provide Form 1040 filing thresholds or exceptions, so treat this as fact-specific. What is clear from these materials: if you claim the Foreign Tax Credit, you do that on your U.S. return using Form 1116.

Why is the `Foreign Tax Credit (FTC)` often less useful in no-tax jurisdictions?

Because the credit applies only to qualifying foreign taxes imposed on you. Those taxes must pass four tests, and some taxes can still be noncreditable even when the tests appear satisfied. You also cannot claim FTC for taxes on income you exclude; for a deeper comparison, see FEIE vs. FTC: A Strategic Choice for High-Earning US Expats.

What is the difference between `FBAR` and `FATCA` `Form 8938`?

Treat them as separate reporting tracks. The IRS material here does not provide a full legal side-by-side, so verify current requirements for each based on your facts. Do not assume filing one automatically satisfies the other.

What should a freelancer track every month to stay compliant abroad?

The IRS excerpts here do not set a required monthly freelancer checklist. A practical starting point is to maintain records that support what you report on Form 1040 and any FTC claim on Form 1116, including income categories and foreign taxes imposed on you. Keep that file current so filing is a reconciliation step, not a rebuild.

When should I hire an expat tax professional instead of handling this myself?

There is no single rule for when professional help is required. Consider getting support when your facts are unclear or when FTC and exclusion choices could affect election outcomes later. If you self-file, hold yourself to the same standard: each position should be clear and supportable.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Educational content only. Not legal, tax, or financial advice.

Related Posts

FEIE vs Foreign Tax Credit for High-Earning US Expats

Start with compliance, then optimize tax. If you are a globally mobile freelancer or consultant filing `Form 1040`, first confirm what you can actually claim and support, then compare the tax result.

Tax Residency vs. Citizenship-Based Taxation: The US Anomaly

You're not choosing one tax identity and discarding the other. In cross-border life, you're usually operating two systems at the same time: a status-driven filing layer and a place-driven residency layer. Stop asking which one wins and start running one operating flow that covers exposure, obligations, paperwork, and proof.

Dubai Digital Nomad Guide 2026 for a Practical Move Plan

If this move works for you, it will work because you sequence decisions well and keep risk reversible until your status is clear. Treat this route as a chain of checkpoints, not one giant yes or no decision made under time pressure.