Quick Answer

Start with one country, one checkout setup, and one named reconciliation owner, then stress-test costs before scaling. In a dropshipping business guide payments plan, model Stripe base card fees (2.9% + 30¢) separately from international (+1.5%) and conversion (+1%) adders, and keep supplier payout and FX policy outside the checkout choice. Move forward only when weekly evidence can tie orders, settlements, and supplier disbursements without manual patching.

Dropshipping Payment Setup by Market: Checkout, Supplier Payouts, FX, Reconciliation, and Compliance

Tie checkout, supplier payment, and refund controls together#

Dropshipping keeps inventory light, but it does not remove the need for operating discipline. When payment setup, supplier fulfillment, and refund handling are loosely connected, the problems usually show up after launch.

At its core, dropshipping is a retail fulfillment method where the seller does not keep products in stock. After a customer places an order, the seller buys from a third-party supplier, and that supplier ships directly to the customer. That is why it is often treated as a low-barrier way to start. You can begin without holding large inventory, and you do not handle the product directly.

This article is not a ranked provider list. It gives you an operating model with practical checkpoints for setting up and validating your flow before launch.

Treat payments and shipping as one launch track. Stripe includes both:

- Set up payment and shipping details.

- Test your store and refine before launch.

Two risks are worth planning for early:

- Unreliable suppliers.

- Returns and refunds.

The practical question is which setup you can verify, reconcile, and support cleanly from launch onward.

Related: A Canadian Freelancer's Guide to Setting Up a US Stripe Account.

Build the payment mental model before picking tools#

Choose tools after you map the money movements, not before. In many dropshipping setups, checkout is only one part of the payment operating model.

Separate checkout from the rest of the money#

PayPal's merchant docs make one point explicit. Payflow Pro is labeled a payment gateway. Use that as a practical boundary: checkout collection on one side, and downstream money operations on the other.

For planning, map buckets separately, for example:

- Customer pay-in

- Supplier payout

- Treasury transfer to your main bank

- Operating expense payments

If you blend those together, you can choose a checkout option on pricing alone and still have no clear payout or reconciliation path.

Use product- and market-specific assumptions#

Do not plan from a single headline fee. PayPal separates areas such as Expanded Checkout, Payouts, Chargeback Fees, and Dispute Fees. Model those separately.

Stripe's pricing shows the same issue. One number is not enough:

2.9% + 30¢for domestic cards+ 1.5%for international cards+ 1%if currency conversion is required

Keep a record of the exact fee pages you used, their last-updated dates, and the printable PDF where available. That makes your launch assumptions auditable.

Keep the first decision unit small#

Start with one market, one checkout stack, and clear owners for payout policy and reconciliation. That keeps the rules clear before you scale.

PayPal's definitions show why this matters. "Domestic" and "international" depend on where sender and receiver are registered, and some cross-border EEA transactions are fee-treated as domestic. If reconciliation ownership is still unclear for that first market, pause tool selection until it is assigned.

Compare checkout options by market and platform fit#

Choose checkout by verified market fit first, then by price. A low published rate is not useful if the page is scoped to a different resident market or region, or if your platform setup is still unverified.

| Provider | Platform support | Payout timing | Dispute handling | Country availability |

|---|---|---|---|---|

| Stripe | Not established for Shopify, WooCommerce, or BigCommerce | Not established | Not established in provided excerpts | Breadth signal only: Stripe pricing highlights "100+ payment methods"; exact country availability is not established here |

| PayPal | Not established for specific platform plugins/apps | Not established | Clear signal to model incident costs: dedicated Chargeback Fees and Dispute Fees areas | Strong market-scoping signal: fee pages apply to specific resident markets/regions; US pages are explicitly scoped to United States (US) residents |

| Shopify Payments | Not established in provided excerpts | Not established | Not established | Not established |

| Skrill | Not established in provided excerpts | Not established | Not established | Not established |

| 2Checkout (Verifone) | Not established in provided excerpts | Not established | Not established | Not established |

This comparison is intentionally strict. It shows what you can model now and what still needs direct verification before you make build decisions.

Pick for the real blocker#

Start with the constraint that is actually slowing you down.

If speed to launch is your blocker, keep the first stack small. Prioritize the option you can verify fastest for your exact merchant country and checkout setup.

If geographic method coverage is your blocker, prioritize reach over a slightly lower headline fee. Stripe's pricing position on "100+ payment methods" matters for that decision. PayPal fee pages, by contrast, emphasize that rates are market-scoped and that "domestic" versus "international" depends on where sender and receiver are registered.

Treat cross-border assumptions carefully. PayPal's Iceland consumer fees note that some cross-border EEA EUR and SEK transactions are treated as domestic for fee application, so a blanket "cross-border costs more" model can be wrong.

Decide method coverage with evidence#

Keep method choices tied to what is explicitly supported in your selected provider and market. PayPal's Expanded Checkout states that customers can pay with cards, Apple Pay, Google Pay, and more. That is a concrete coverage signal you can validate against your own flow.

For cards, Apple Pay, and Google Pay, confirm live support in your exact merchant setup before you commit to UX or conversion assumptions.

Verify late-stage constraints before launch#

Before you lock a provider, document the exact fee pages you used and their update checkpoints. For example, the PayPal US business-fee page shows Last Updated: February 9, 2026 and provides a Download printable PDF.

Record merchant country, applicable fee region, and margin-sensitive adders such as Stripe's +1.5% for international cards and +1% for currency conversion required. Keep those alongside the base 2.9% + 30¢ domestic card rate.

When data is incomplete, choose the option you can verify fastest for country, platform, and method mix instead of optimizing around an unverified fee table.

You might also find this useful: Payments Infrastructure for Creator Platforms: A Complete Build vs. Buy Guide.

Choose supplier payout rails and FX rules that protect margin#

Margin can slip in payout and FX decisions, not just at checkout. Lock payout rails and FX policy only where pricing mechanics are verified for your exact flow.

| Payout flow | Verified details | Margin planning implication |

|---|---|---|

| Wise send/convert | Wise says it uses the live mid-market rate with a separate upfront fee, with pricing varying by currency (from 0.57%). | Model total FX and transfer cost explicitly, not just a headline transfer fee. |

| Wise high-volume transfers | Wise says discounts apply after 25,000 USD (or equivalent) and reset on the first of each month. | Payout cadence can change realized cost within a month. |

| Wise USD wire/Swift receiving | Wise lists a fixed fee per payment of 6.11 USD for receiving USD wire/Swift payments. | Include fixed receiving fees in supplier-level margin math. |

| Wise multi-currency receiving setup | Wise lists receiving account details in 24 currencies. | Validate destination method and currency setup during onboarding, not after launch. |

| Card, bank transfer, Revolut, WorldFirst, World Account comparisons | Confirm with the relevant authority | Treat cross-provider speed and cost claims as unverified until you confirm them directly. |

If suppliers invoice in one dominant currency, use a structured conversion policy and keep the same pricing checkpoint each cycle. If supplier currencies shift week to week, set a pre-agreed conversion cadence so FX exposure is managed instead of ad hoc.

Treat "same-day" payout claims as a risk decision, not a default requirement. Prioritize speed only when your operating risk is time-sensitive. Prioritize predictable total cost when it is not.

Use this onboarding checklist before you scale payouts:

- Validate payout destination details and supported currency path.

- Confirm expected settlement windows and operational cutoffs directly with each provider before launch.

- Define exception routing for failed, returned, or mismatched payouts.

- Save fee-validation artifacts from the current pricing view and the regulator-standardized fee format.

Model margins with payment friction included#

If your model uses one blended payment-rate assumption, it will misstate margin. Keep processing, market classification, FX, refunds, and disputes as distinct lines.

- Revenue per order

- Product cost and fulfillment

- Base checkout processing

- Cross-border and currency-conversion costs

- Other payout/conversion costs (if applicable)

- Refund leakage

- Dispute or chargeback loss

For a first pass, use provider-specific inputs and keep them separate:

| Provider | Grounded inputs to model now | What to keep as contract-specific placeholders |

|---|---|---|

| Stripe | 2.9% + 30¢ domestic cards, +1.5% international cards, +1% if currency conversion is required; standard pricing says no setup/monthly/hidden fees; custom pricing can apply at larger volume | Refund leakage assumptions, dispute or chargeback amounts, and any non-public terms |

| PayPal | Product and method rates vary (for example: Starting at 2.89% + $0.29, 2.99% + $0.49, 3.49% + $0.49, 4.99% + $0.49); domestic versus international is defined by same-market versus different-market account classification; some markets are grouped for international pricing; fee tables are scoped to the listed market/region | Dispute or chargeback amounts and refund-loss assumptions from your actual account terms |

Use channel-specific lanes before launch. Model checkout method mix, domestic versus international share, and conversion-required share directly, rather than forcing one blended assumption across all orders.

For scenario contrast, run the same bridge under at least two assumption sets, for example higher refund or dispute pressure versus lower exception pressure, and compare which components drive the variance.

Run two sensitivity checks before go-live:

- Disputes: stress dispute rate and per-case loss separately from base processing. PayPal publishes dedicated Dispute Fees and Chargeback Fees sections.

- FX and market classification: shock conversion-required share and domestic-versus-international mix independently from base processing so you can see when cross-border or FX add-ons become the main driver.

Finally, save versioned pricing artifacts used in your model. For PayPal, keep the page date and market scope used, for example the US merchant fees page Last Updated: February 9, 2026, and monitor Policy Updates. For Stripe, capture whether you are still on public standard pricing or have moved to custom terms.

Sequence rollout in phases to avoid expensive rewrites#

Use a phased rollout. Prove your core order-to-cash flow first, then add cross-border payout and FX controls after weekly reconciliation is consistently clean.

Phase 1 on your storefront#

Keep Phase 1 minimal so failures are easy to spot and fix. Limit it to the storefront, the primary checkout provider, core payment methods, and one payout path you can trace end to end.

Move to Phase 2 only when these are true for a sustained period:

- checkout outcomes are stable enough that failed payments are exceptions

- payout timing is predictable enough for fulfillment planning

- weekly reconciliation is clean enough to match orders, settlements, and payouts without manual patching

Phase 2 with payout and FX controls#

Add payout and FX optimization only after the base lane is steady. For Wise, pricing is usage-based, Wise Business shows a one-time set-up fee of 31 USD, and Wise states it uses the live mid-market rate with an upfront fee. The key operating detail is that fees vary by currency, so corridor-level pricing should drive your expansion math rather than a generic "from 0.57%" assumption.

Use a clear checkpoint before redesigning payout flows. Verify whether monthly transfer volume actually crosses Wise's 25,000 USD discount threshold, and remember that this window resets on the first of each month.

If you are evaluating another provider, validate corridor pricing, setup requirements, and payout timing separately before changing payout rails.

Delay expansion when operations are noisy#

If dispute and refund operations are unstable, delay new market launches until operations are steady.

If you use a Wise card operationally, separate that from supplier payout design. Card cash withdrawals include 2 free withdrawals each month as long as you stay within 100 USD; after that, fees can include 1.5 USD per withdrawal plus 2% of the amount over 100 USD.

Launch artifacts to keep before each phase change#

Keep a small but complete launch file before each phase change:

- Provider accounts: named owners, admin access records, and saved pricing artifacts; for Wise, include the pricing page snapshot and the regulator-standardized fee-format view.

- Platform integrations: payment settings, test-order evidence, settlement destination details, and failed-payment alert routing.

- Payout SOP: approved payout method, destination verification, conversion rule, approval owner, and failed-payout escalation path.

- Incident playbook: clear owner for checkout issues, refunds or disputes, payout failures, and reconciliation breaks.

For a step-by-step walkthrough, see Non-Resident Withholding on Contractor Payments: Platform Guide to the 30% Rule and Treaty Reductions.

Set compliance and policy gates before scaling markets#

A clean weekly close is not a green light to add countries automatically. Before each market launch, set a written compliance gate for the exact market, product set, and payout flow so you can defend the setup during provider or partner review.

Map the real compliance surface#

Dropshipping can feel simple because you are not holding inventory, but your payment operations still sit inside core e-commerce compliance. At minimum, map data protection, taxes, payment information, and import or export obligations. Then add any industry- or product-specific requirements.

Start each new market with one question: which laws and regulations apply to this exact operation? If customer data from multiple regions is in scope, include the applicable data-protection rules in that review at a practical, high level. A short pre-launch note is enough if it clearly states what data you collect, where it is stored, who handles payments, and who owns cross-border product movement.

Treat payout setup as a launch blocker when unclear#

Payout setup is a compliance and policy gate, not just a treasury decision. If ownership, flow design, or provider requirements are unclear, treat that as a launch blocker.

Before launch, confirm with each provider in writing:

- your business model and product set fit the account and policy scope

- your planned sell-to and payout flows are supported for your use case

- any restrictions or exceptions are documented before launch

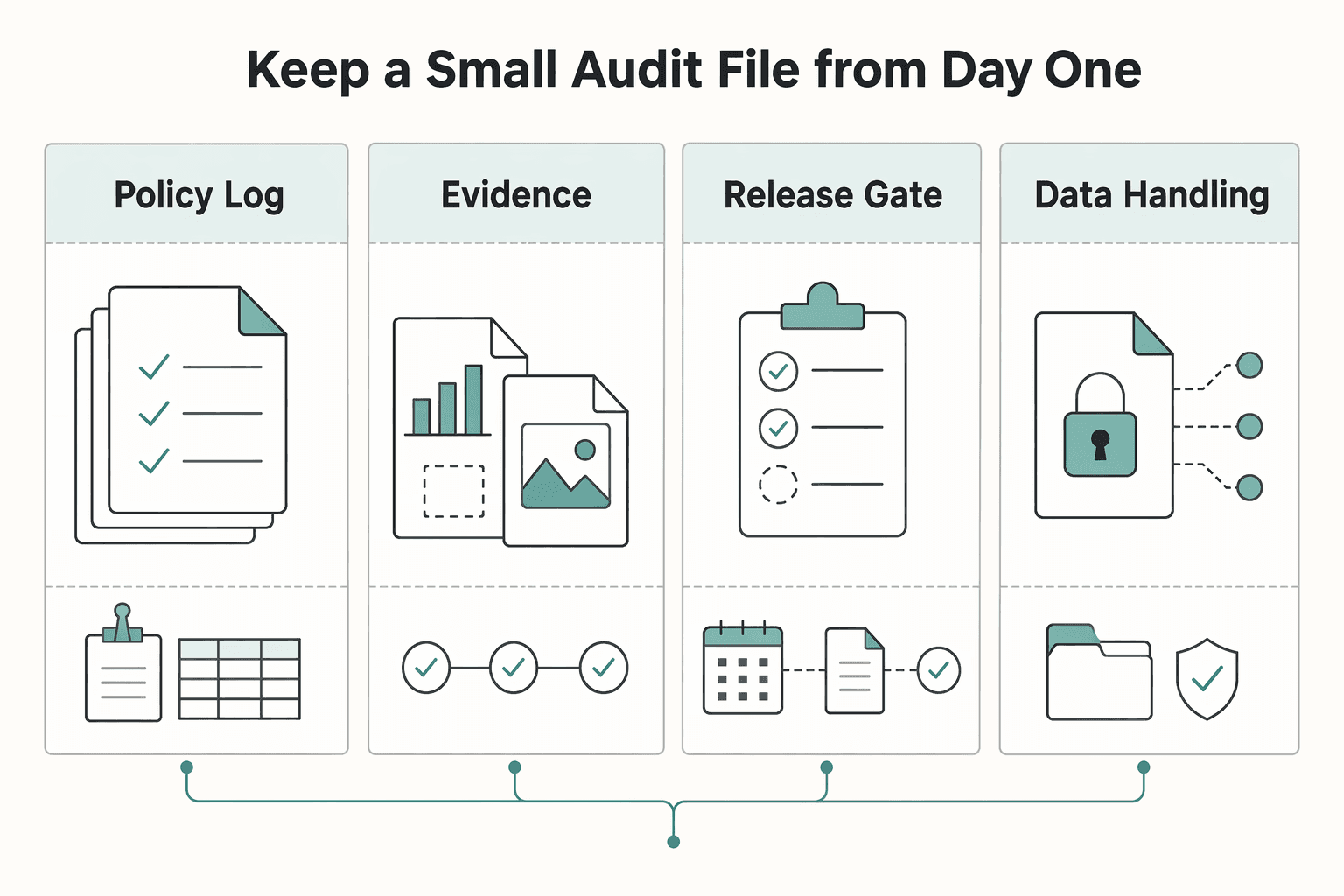

Keep a small audit file from day one#

Compliance work is ongoing, so keep focused evidence instead of broad documentation. For each market, maintain:

| Record | Keep |

|---|---|

| Policy log | market, products, providers, launch decision, approver |

| Account ownership record | entity, owners, admins, access changes |

| Approval history | onboarding decisions, payout destination changes, exceptions |

| Data-handling note | what customer and payment-related data you store, where it lives, and who can access it |

If partners or marketplaces are involved, keep their requirement documents together as a single operating reference. Vendor-guide style documentation is useful here because it centralizes purchase, data security, pricing, and support rules.

Also flag product-level regulation early. PFAS-related products are a concrete example where obligations can extend across the product lifecycle. That is why product compliance should be checked before scaling a market.

If you want a deeper dive, read A Guide to GDPR Compliance for SaaS Businesses.

Build reconciliation and evidence packs from day one#

Use a weekly evidence pack from the start so your margin view stays defensible when refunds, chargebacks, and payout questions appear. In dropshipping, customers pay you and you forward orders to suppliers, so you need a clear record of customer pay-in, supplier pay-out, and any breaks between them.

What goes in the weekly pack#

Keep it narrow and repeatable for each close period:

| Weekly pack item | Keep |

|---|---|

| Order ledger | your order ledger for the period |

| Processor settlements | processor settlement records |

| Supplier payouts | supplier payout records |

| Variance notes | a short variance note file for anything that does not tie cleanly |

This is not about building a large archive. It is about keeping one traceable view when settled cash, shipped orders, and reported revenue do not line up.

Make variance notes brief but specific. Note what broke, which order or batch is affected, whether it looks like timing or loss, who owns the fix, and what evidence supports the treatment. If a break involves a return, include supplier communication and the policy basis, including who pays return shipping and where that policy is shown to buyers. If delay drove the complaint, keep the delivery expectation you gave the buyer, such as 10 to 15 days.

Use one close order every week#

Pick one internal close routine and run it the same way each week so exceptions surface early.

Do not publish margin first and clean up later. Returns can be messy in this model because you do not physically handle the item, and unresolved payment breaks can hide fulfillment or policy issues.

Set escalation rules before the first messy week#

Define one hard rule early: if an unmatched settlement or payout exception stays unresolved past your internal limit, escalate it to payments ops instead of patching spreadsheets to force a close.

Require every unresolved item to have an owner, timestamp, and supporting evidence. If any element is missing, keep it open. Structured supplier workflows help here because unclear financial responsibility between seller and supplier can quickly compound delays.

Over time, the same evidence packs should feed failure handling.

If your weekly close still depends on manual handoffs, use this section as an implementation checklist and map each control to the Gruv docs.

Prepare failure handling for the payment problems that actually happen#

Handle payment failures as repeatable incident types with predefined owners and evidence, not as one-off cleanup work. In dropshipping, one risk is compounding failure across retries, payouts, refunds, and card disputes before margin impact is visible.

Triage by incident type, not by channel#

Route by failure pattern first, because a "cash mismatch" can come from different causes and each one needs a different escalation path.

| Incident | First checkpoint | Escalation path | Evidence to attach |

|---|---|---|---|

| Failed customer payment | Confirm whether this is isolated or patterned, and pause duplicate-money risk before continuing retries | If the pattern appears in checkout or settlement behavior, open a Stripe or PayPal ticket with transaction IDs and timestamps | Order ID, payment ID, attempt timestamps, status history |

| Delayed supplier payout | Verify payout instruction, reference, amount, and linked order batch | Contact the supplier and hold affected shipment decisions until payout state is clear | Payout reference, supplier thread, affected SKUs or batch |

| Refund spike | Group by SKU, supplier, market, and campaign to isolate likely cause | Escalate margin-at-risk SKUs to internal finance review before continuing normal sales cadence | Refund log, complaint pattern, return-policy basis, supplier correspondence |

| Chargeback cluster on card networks | Check concentration by market, SKU, and payment method | Open processor dispute handling and run internal finance or risk review in parallel | Dispute notices, shipment proof, buyer-facing delivery expectation, order timeline |

Use processor classification and fee structure during escalation#

For PayPal incidents, confirm transaction classification early because domestic versus international treatment can change fee handling. It defines domestic as sender and receiver in the same market, international as different markets, and notes that some markets are grouped for international rate calculations. On the Iceland fee page, some EEA EUR and SEK international transactions are treated as domestic for fee purposes.

Keep the current merchant-fee artifact for that account in the incident folder, and record the page's last-updated checkpoint, for example February 9, 2026 on the US merchant-fee page. Reference the dedicated dispute-fee and chargeback-fee sections plus the Policy Updates Page when reviewing case economics. If Seller Protection may apply, check eligibility early and attach supporting shipment evidence.

For Stripe, include fee add-ons in incident impact review, not just base processing. Stripe lists 2.9% + 30¢ for successful domestic-card transactions, plus 0.5% for manually entered cards, 1.5% for international cards, and 1% when currency conversion is required. Stripe also describes 3D Secure as pre-purchase customer identity verification. For custom pricing accounts, it lists $0.03 per 3D Secure attempt.

Assign one owner to each retry loop#

Each retry loop should have one owner, one status view, and one clear handoff point from automation to human review. Split ownership across checkout retries, supplier payout retries, and refund handling so failures do not compound silently across teams.

Related reading: A Freelancer's Guide to Business Process Automation (BPA).

Decide when to add or replace providers#

Add or replace a provider when recurring failures are forcing operational workarounds, not when a headline fee looks better. Common replacement triggers can include repeated payout delays, weak coverage in target markets, dispute handling that keeps escalating, and reconciliation overhead that slows monthly close.

Start with market scope before you compare economics. PayPal's US fee tables are scoped to US-resident accounts, and fee treatment depends on domestic versus international transaction classification, with locale-specific exceptions. For example, the Iceland schedule notes some EEA international transactions treated as domestic for fee purposes.

Before you model costs, archive the current fee PDF for that account. Record the last-updated checkpoints of February 9, 2026 for US merchant fees and February 19, 2026 for US consumer fees. Review the Policy Updates Page so your baseline is stable.

If you currently run a single provider, operations are usually simpler. Adding PayPal can broaden payment-method coverage through Expanded Checkout, including cards, Apple Pay, Google Pay, and more. PayPal also frames a tradeoff between risk management and checkout experience, and its dispute protection is eligibility-based rather than universal. Its pricing is product-specific, with different starting percentages such as 2.89% for card processing, 3.49% for PayPal and Venmo, and 4.99% for Pay Later.

Before migration, run this checklist:

- Export historical settlements, refunds, disputes, and order-to-payment mappings.

- Set a cutoff date and define how long legacy orders stay on the old provider for refunds and chargebacks.

- Verify payment-method continuity explicitly rather than assuming saved methods transfer.

- Validate the first post-cutover settlement batch, refund flow, dispute intake, and close mapping.

If your main issue is supplier payout timing, solve that rail directly before redesigning checkout. For example, WorldFirst markets same-day payments for Chinese suppliers and a 40% FX savings claim for new customers. Validate supplier-country fit and eligibility before treating those claims as migration assumptions.

We covered this in detail in IndieHacker Platform Guide: How to Add Revenue Share Payments Without a Finance Team.

Map the operating model to Gruv modules where supported#

Map Gruv to your operating model only where each flow is confirmed in your program. The practical check is whether each money movement ties to a named module, a traceable record, and an export your finance team can reconcile.

Start with the flow map#

Use your core flow map and assign each leg only where enabled:

| Module | Flow leg | Qualifier |

|---|---|---|

| Collection and invoicing | customer pay-ins or invoice-based collection | only where enabled |

| FX conversion | when collection and payout currencies differ | confirm each required leg explicitly |

| Virtual Accounts | inbound receiving details | where supported |

| Payouts | outbound disbursements | with compliance gates where required |

Do not assume all modules, rails, recipient types, or country coverage are available by default. Confirm each required leg explicitly.

The operator benefit to validate#

The key benefit to validate is traceability, not module count. You want a clear chain from request to provider references to ledger postings to exports, so reconciliation does not depend on manual reconstruction.

Run one live-like sample before rollout. Process a single business event end to end, then verify that the exported records preserve the identifiers your team needs for close.

Where implementations usually break#

A practical risk is partial fit: one leg is live while another is still conditional or unavailable in your setup. Another possible gap is reference continuity, where identifiers appear in one step but do not carry through to exports.

Ask for an evidence pack, not only a demo: originating request, funds received, any conversion event, payout state if used, and final export output.

Use the right next step#

Use Read the docs when you need integration depth, including API and webhook behavior, export fields, and idempotent retries. Use Talk to sales when your decision depends on country coverage, recipient type, rail availability, or conditionally enabled flows.

If one leg remains uncertain, keep that leg on your current provider and test Gruv on a narrower path first.

Need the full breakdown? Read A freelance IT consultant's guide to business interruption insurance.

Conclusion#

The core decision is straightforward: do not run payments from a generic provider list. Run a market-specific operating model instead.

Build one country flow end to end, tied to one store platform, one supplier setup, and one traceable money path from customer payment to supplier payout. That discipline matters in dropshipping, where a third-party supplier fulfills orders and you still own customer service, returns, and margin pressure. A fast launch at checkout is not enough if payment handling and return or refund records are not clear in daily operations.

Keep the execution order strict:

- Pick the checkout stack for the target market and store platform, for example Shopify, WooCommerce, or BigCommerce.

- Lock supplier setup and payment routing before order volume grows.

- Enforce reconciliation and policy gates once the payment paths are fully defined.

Use one country as the minimum decision unit before broader expansion. Run that country's assumptions through your comparison tables and launch checklist, then verify them with operating evidence from real orders, payouts, and return or refund records. If one link is still vague, fix it before adding the next market.

Before launching the next market, confirm payout coverage, policy gates, and operating ownership for your exact flow by talking with Gruv.

Frequently Asked Questions

What payments do you actually need to run a dropshipping business beyond checkout?

Beyond checkout, you need a supplier payment path, and bank transfer is a recognized supplier-payment category. If you buy internationally, a multi-currency account plus planned FX and transfer steps can keep collection, conversion, and payout from blending into one opaque flow. Some provider stacks also offer API and accounting software integrations to help keep records aligned.

What is the difference between a payment gateway and a payment processor in practical operations?

Treat them as separate payment components in your stack. In practice, confirm which provider handles each component before you troubleshoot. Separating ownership early can make triage clearer.

Which customer payment methods should you enable first on Shopify, WooCommerce, or BigCommerce?

There is no single grounded "best first mix" across Shopify, WooCommerce, and BigCommerce. Mobile payments such as Apple Pay and Google Pay are established options, but your first set should be limited to methods your team can reconcile and support reliably. Add methods in stages instead of enabling every available option at launch.

How should you pay overseas suppliers without letting FX costs erode margin?

Use a defined process for multi-currency balances, FX conversion, and global transfers rather than converting ad hoc invoice by invoice. WorldFirst positions these as core tools for international pay-and-get-paid flows and also advertises same-day payments for China, which should be treated as provider- and corridor-specific. Treat promotional claims like "save 40%" for new customers and referral offers up to £355 as conditional, not baseline economics.

What are the most common dropshipping payment failures, and what should the first escalation step be?

A single universal escalation workflow is not verified here. Start by identifying the exact payment leg that failed, then route escalation through the provider responsible for that leg.

How do payment choices change net margin once refunds and disputes are included?

No universal quantified margin model is verified here. Evaluate payment setups with your own order-level outcomes, including refunds, disputes, supplier-payment costs, and FX, instead of relying on checkout metrics alone.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- clame.nyu.edu/Download_PDFS/E0A846/312658/DropshippingTheU...trusted

- dhr.alabama.gov/wp-content/uploads/2019/08/EBT-EFTrfp.pdftrusted

- digitalcommons.pepperdine.edu/context/etd/article/2464/viewcontent/Llamas_...trusted

- govinfo.gov/content/pkg/FR-2014-09-30/pdf/FR-2014-09-30.pdftrusted

- legacy.trade.gov/guide_to_exporting.pdftrusted

- oecd.org/content/dam/oecd/en/publications/reports/201...trusted

- paypal.com/us/business/paypal-business-feestrusted

- paypal.com/us/business/feestrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: