Quick Answer

Use this dac7 compliance case study as an operating decision guide: define your baseline pain, choose a centralized model where scope supports it, and verify each stage before adding countries. The article’s core pattern is evidence first, then implementation order, then wave launches with hard gates. It also warns that public vendor stories often omit independently validated ROI, so leadership should separate proven metrics from unproven claims.

Why this DAC7 compliance case study matters for growth leaders#

Treat this as a decision memo, not a generic explainer. This case study matters because compliance design can either support expansion or slow it down. If your team is already working through cross-border reporting obligations, the real question is simple: how do you keep expansion moving without letting manual reporting work eat margin?

Step 1. Set the right lens#

Growth leaders often get pulled into DAC7 late, after legal has flagged an obligation or finance has started feeling the reporting burden. By then, the issue is no longer legal interpretation alone. It is whether seller data, payout records, internal ownership, and filing steps are clean enough to support new-country launches without rework.

A useful reference point comes from adjacent EU compliance design. In VAT, the European Union's One Stop Shop lets eligible businesses register in one Member State, the "Member State of identification," for declaration and payment on qualifying cross-border activity. The European Commission says OSS can reduce red tape by up to 95%.

That does not prove any DAC7 outcome by itself. It does show the broader operating lesson: centralized compliance design can materially change the cost of cross-border expansion.

Step 2. Focus on the decisions that change economics#

Read this case study for operating choices, not theory. The value is in the baseline bottleneck, the decisions made to remove it, the order of execution, the likely economics, what broke, and how recovery was handled when reality did not match plan.

Stay close to decision-grade questions: What was manual before tooling changed? Which team owned the reporting sequence? What checkpoint proved the data was ready? A useful verification detail is whether the company can show who owned submission, what evidence pack existed before implementation, and how readiness was confirmed before expansion. If those details are missing, treat any growth claim as incomplete.

A common failure mode is treating compliance as if it lives only inside finance. In practice, margin gets hit when product, ops, and finance do not agree on data ownership early enough, and fixes get pushed into launch windows.

Step 3. Apply evidence discipline from the start#

Public evidence is limited, so this article calls out unknowns instead of smoothing them over. Some vendor-led public examples are useful, but they still leave important gaps. Public material often does not give you audited implementation cost, internal hours saved, rejection rates, or a clean counterfactual for how much faster expansion actually became.

Use public examples to understand the pattern and sequence, not to assume universal ROI. Where cross-border tax questions overlap with broader EU obligations, mechanisms like VAT Cross-border Rulings also matter because they let taxable persons seek advance rulings on complex transactions rather than fixing interpretation problems after launch.

The same discipline applies here. If a case study cannot show baseline pain, named owners, and recovery steps, it is marketing. If it can, it becomes a useful operating reference.

You might also find this useful: A Guide to Writing Case Studies for a B2B SaaS Audience.

Start with the baseline bottleneck and success criteria#

Start by documenting your current filing workflow as evidence, then set success criteria you can verify before you evaluate any tool.

Step 1. Write the starting state as evidence, not opinion#

Build a one-page baseline for each jurisdiction in scope: submission method, named owner, required inputs, and where exceptions are resolved. Keep it auditable so someone outside finance can trace one filing cycle from source data to submission evidence.

Avoid broad statements like "compliance is slowing expansion" unless you can show where time is actually spent. If the constraint is unclear, later tool choices are hard to test.

Step 2. Use public structure as a prompt, not proof#

Use public examples to shape questions, not to assume your bottleneck is identical. In adjacent EU VAT operations, OSS is structured around one Member State of identification, and the guidance explicitly includes record keeping and audits. That does not define DAC7 execution on its own, but it is a useful operating pattern: clear ownership plus clear evidence requirements.

Step 3. Set success criteria before evaluating tools#

Choose measures that change decisions and can be checked quickly:

| Measure | Evidence example |

|---|---|

| Filing timeliness | Submission receipts |

| Time to resolve submission or data exceptions | Issue timestamps |

| Internal hours per filing cycle | Internal records or time tracking |

| Market launch readiness for the next jurisdiction | Launch checklists |

Tie each measure to concrete evidence, for example submission receipts, issue timestamps, and launch checklists. If a vendor process cannot show how your team will verify improvement on those points, you have not reduced execution risk yet.

For a step-by-step walkthrough, see Case Study Framework: How to Document Platform Payment Wins for Marketing.

Prepare the inputs before touching tooling#

Do the prep work before you buy or build anything. Software will not fix disputed scope, weak evidence, or unclear data ownership. Get these inputs stable first. DAC7 sits within the EU Directive on Administrative Cooperation, and the operating trend is more data and more automatic exchange of information.

| Artifact | What it covers | Detail to include |

|---|---|---|

| Legal interpretation note | Scope across DAC7 and adjacent regimes | Real product lines, seller types, countries, and points that still need counsel |

| Reportable activity map | Flows that may create reportable seller income | Owner of each flow and the source tables |

| Seller field dictionary | Seller attributes used for reporting | Origin, whether entered or derived, and what counts as complete |

| Per-jurisdiction filing owner list | Filing ownership by jurisdiction | One named filing owner per jurisdiction |

- Confirm scope in writing across DAC7 and adjacent regimes.

Start with a short legal interpretation note tied to your real product lines, seller types, and countries. Use it to answer: which parts of your platform may fall under DAC7 reporting rules for digital platforms, whether MRDP or the OECD Model Rules also need assessment for your business, and which points still need counsel.

Verification: product and finance should be able to read the same note and reach the same view on in-scope, out-of-scope, and escalation items. Failure mode: broad assumptions get documented without mapping to actual transaction types, and downstream teams build the wrong model.

- Build the minimum evidence pack before integrations start.

Keep four artifacts together in one controlled folder: legal interpretation, reportable activity map, seller field dictionary, and per-jurisdiction filing owner list. The activity map should name each platform flow that may create reportable seller income, the owner of that flow, and the source tables. The field dictionary should define each seller attribute, origin, whether it is entered or derived, and what counts as complete.

Verification: trace one seller from onboarding to payout using only this pack. If you cannot, the tooling project is early.

- Lock the data prerequisites you will rely on for reporting.

Even where a field is not established here as a DAC7 legal requirement, decide explicitly whether your reporting approach depends on VAT identifiers, tax residency fields, W-8 or W-9 collection logic, and seller records that link cleanly to payouts. Treat these as design decisions, not hidden assumptions in forms or exports.

The key checkpoint is payout linkage: if you cannot show which payouts belong to which seller entity, later reporting outputs are difficult to trust.

- Assign control owners across product, finance, and ops.

Product should own field capture and change management, finance should own reporting interpretation and filing readiness, and ops should own exception handling and seller follow-up. For each control, define reviewer, sign-off owner, and incident logging path. This audit trail is an internal control choice, but it becomes more important as data volumes and correction load increase.

If one control has no named owner, stop and fix that before vendor selection.

If you want a deeper dive, read How a Legal Marketplace Modernized Trust Accounting Compliance.

Choose the operating model that protects margin#

If you expect to enter new EU markets quickly, start with the most centralized VAT path your transaction mix allows. Then decide how much of the process you own. For covered cross-border B2C flows, OSS is designed around one-member-state registration and centralized VAT declaration/payment. For complex cross-border VAT treatment questions, CBR can be used to seek an advance ruling.

Use the evidence pack from the last section as your filter. Bring your activity map, seller/data dictionary, and filing ownership model into every build-versus-buy discussion. If you cannot show which flows are covered by OSS, which still require local handling, and how ambiguous VAT treatment will be resolved, the operating model is not ready.

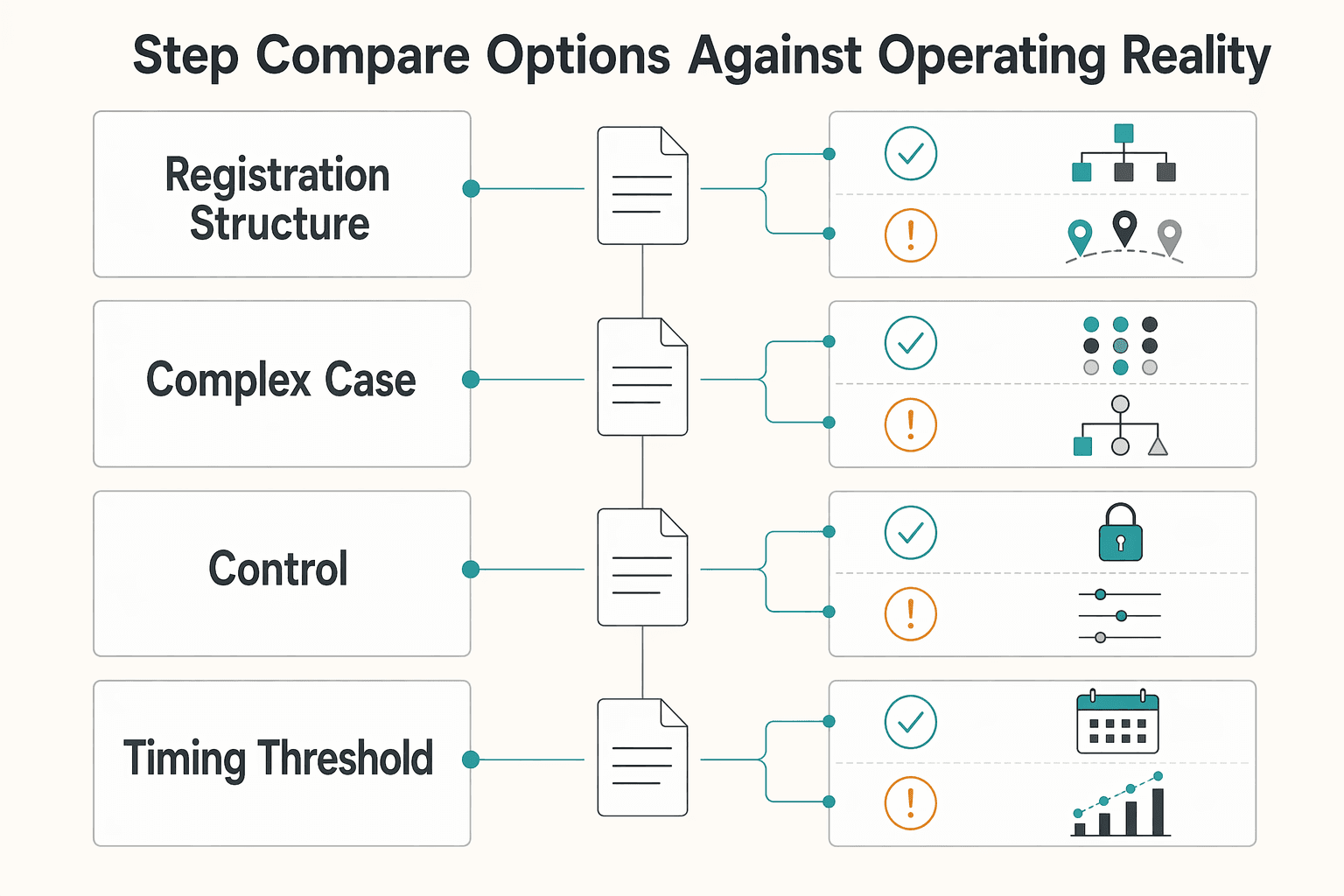

Step 1. Compare your options against EU operating reality#

| Decision area | What the EU mechanism supports | What you still need to decide |

|---|---|---|

| Registration structure | OSS allows eligible taxable persons to register in one single Member State (the Member State of identification) for covered VAT declaration/payment flows | Which transactions are in scope for OSS vs outside scope and handled separately |

| Complex cross-border VAT treatment | CBR allows advance rulings for complex cross-border VAT questions, with requests filed in the participating EU country where you are VAT-registered | When to seek a ruling and who owns that process internally |

| Compliance controls | OSS guidance explicitly covers record keeping and audits | How finance, tax, and engineering share evidence retention and audit-readiness ownership |

| Timing and threshold context | The OSS framework reflects the 1 July 2021 rule changes, including the EU-wide EUR 10,000 threshold; OSS also states potential red-tape reduction of up to 95% | Whether your current and near-term EU sales profile justifies centralizing now |

The choice is less about ideology than about clear scope and ownership: does your model support consistent VAT treatment decisions, repeatable filings, and audit-ready records as you add countries?

We covered this in detail in How Freelancers Choose a Compliance-First Fintech Platform.

Implement the reporting flow in the right order#

Build the flow in the same order the data is created and validated: seller onboarding, transaction classification, reporting extract, file generation, then submission tracking. That order keeps data issues out of filing cycles, where fixes are slower and more expensive.

| Stage | Primary action | Validation focus |

|---|---|---|

| Seller onboarding | Capture known reporting fields, including TIN and VAT-related data where relevant | Add a completeness check before sellers are fully active for reportable activity |

| Transaction classification | Set a clear in-scope versus out-of-scope classification tied back to seller records | Verify traceability from seller record to classified transaction to reporting line |

| Reporting extract | Give finance a stable extract tying seller identity, activity classification, and reportable income values together | Keep correction history auditable |

| File generation | Generate filing files only from validated extracts | Fix incomplete or inconsistent records upstream, not during filing preparation |

| Submission tracking | Separate accepted, pending, and rejected filings clearly | Make corrections traceable before resubmission |

Step 1. Lock seller onboarding controls first#

Under DAC7 (Council Directive 2021/514), reporting starts with seller data quality, not year-end file assembly. If you cannot reliably connect activity to a usable seller identity record, your reporting process is not ready.

Capture the reporting fields you already know you need, including Tax Identification Number (TIN) and VAT-related data where relevant to your activity model. Add a completeness check before sellers are fully active for reportable activity, and route missing fields back for correction early.

Step 2. Classify transactions before you extract for reporting#

DAC7 reporting is about income data submitted to a local tax authority and then shared across EU member states. Your transaction layer therefore needs a clear in-scope versus out-of-scope classification, tied back to seller records collected during onboarding.

Make that classification close to where the event is created, then verify traceability from seller record to classified transaction to reporting line.

Step 3. Produce a dedicated reporting extract#

Give finance a stable reporting extract instead of raw transaction output. The extract should tie seller identity, activity classification, and reportable income values together in one reviewable layer.

Keep correction history auditable so teams can see what changed, when it changed, and whether the extract reflects the latest approved record.

Step 4. Generate filing files only from validated extracts#

Treat file generation as a formatting step, not a data-repair step. Run validation before generation so incomplete or inconsistent records are fixed upstream, not during filing preparation.

Step 5. Track submission outcomes clearly#

After generation, track submission outcomes with explicit status visibility so accepted, pending, and rejected filings are easy to separate and resolve. For rejected cases, make corrections traceable before resubmission so teams can confirm what changed.

Keep PII handling explicit in operations by limiting exposure in day-to-day views and preserving clear audit logs for corrections. For the full breakdown, read How a Creator Platform Streamlined 1099 Filing with Gruv.

Launch countries in waves and govern the filing calendar#

Once your reporting flow works end to end, launch in waves so execution stays controllable. Start with the jurisdictions your team can run cleanly, then add higher-friction markets after the first cycle is stable.

Step 1. Rank launch countries by filing friction, not just revenue potential#

Wave order should reflect operational readiness first. Use a country-by-country sheet to track data completeness, submission-path readiness, and clear ownership before a jurisdiction enters a launch wave. If a country still depends on manual fixes to close core gaps, move it to a later wave.

| Jurisdiction | Filing path readiness | Known data or schema issue | Fallback if submission stalls |

|---|---|---|---|

| Wave 1 candidate | Ready for end-to-end run | None or low | Named owner runs manual review and resubmission plan |

| Wave 2 candidate | Partially ready | Open issue to clear | Hold launch until issue is closed |

| Edge-case candidate | Not ready | Multiple open issues | Keep out of current wave |

Step 2. Put a fixed governance rhythm around the filing calendar#

A fixed review rhythm keeps the calendar from drifting. Run recurring readiness checks, schedule a dry run before the live window, and assign explicit deadline checkpoints to owners. Review the same evidence each time so decisions stay operational rather than anecdotal.

Step 3. Set go or no-go gates before each country launch#

Define go/no-go gates before launch pressure builds. At minimum, confirm your required data-completeness level is met, exceptions are manageable inside the window, and one accountable owner is assigned for submission and confirmation. If any gate is unclear, delay that country and keep the wave intact.

This pairs well with our guide on How to Write a Compelling Case Study.

Measure compliance as a monetization system, not overhead#

Treat DAC7 compliance as a growth system only if you measure business impact, not just filing completion. For DAC7 under Directive (EU) 2021/514, the real decision question is what changed in operating cost, margin pressure, and rollout speed after reporting became cleaner and more repeatable.

Step 1. Baseline economics before you claim improvement#

Start with costs you can defend from internal records for one baseline month or one full filing cycle: seller-data fixes, file prep, submission follow-up, rejected-record repair, and cross-team handoffs. If finance cannot show hours, owners, and external spend without memory-based estimates, any ROI claim is still unproven.

Step 2. Tie compliance outputs to unit economics#

Track compliance outcomes in the same frame leadership uses for expansion decisions: cost-to-serve per seller, margin share consumed by manual compliance work, and incremental cost of adding one more EU jurisdiction. If manual review work rises faster than seller volume, treat it as a scaling and expansion constraint, not just an ops annoyance.

Step 3. Separate proven outcomes from unproven claims#

Use two labels in reporting: proven and unproven. Proven means the metric is traceable to internal records, filing logs, or time tracking. Unproven means it may be plausible, but the baseline, method, or comparison is not defensible yet.

The excerpts available here do not provide independently validated DAC7 ROI, internal-hours-saved, margin-impact outcomes, or like-for-like vendor comparisons.

| Function | KPI | Owner | Frequency |

|---|---|---|---|

| Finance | Cost-to-serve per seller in DAC7 scope | Finance lead | Monthly |

| Finance | Manual compliance hours and external spend per filing cycle | Finance or tax ops | Monthly and post-filing |

| Product | Seller profile completeness for reportable fields | Product manager | Weekly |

| Product | Exception rate from missing or mismatched seller data | Product with data owner | Weekly |

| Ops | Rejected submissions still open by jurisdiction | Compliance ops | Weekly during filing windows |

| Ops | Time from issue detection to corrected resubmission confirmation | Compliance ops | Weekly and post-incident |

Do not approve further jurisdiction expansion until these KPIs exist and at least one filing cycle is measured against them.

Related: Gig Worker Tax Compliance at Scale: How Platforms Handle 1099s W-8s and DAC7 for 50000+ Contractors.

Avoid the failure patterns most teams repeat#

The repeat failure is running compliance reporting as a seasonal filing task instead of an always-on data-quality process. If records are only cleaned up right before submission, errors surface when timelines are tight and expansion decisions are already in motion.

Step 1. Keep reporting data live year round#

Treat reporting data as an operating record, not a year-end export. A practical checkpoint is a mid-cycle sample to confirm seller profile data still matches payout and reporting records. The OSS model reflects this operating reality: registration, VAT declaration/payment, record keeping, and audits are connected, and filing is only the endpoint.

Step 2. Baseline before you compare vendors#

Do not evaluate tools without a baseline. If you cannot show current internal effort, exception volume, and correction cycle time, feature comparisons are not decision-grade. Keep one evidence pack per filing cycle with input counts, correction reasons, file versions, and submission confirmations by jurisdiction.

Step 3. Assign exception owners before you need them#

Set clear ownership for exception handling before issues appear. Each jurisdiction should have a named owner responsible for tracking errors through root cause, corrected version, and confirmation of resubmission. If error volume rises, pause new-market rollout until data quality and the correction cycle are stable.

Related reading: How to Build a Compliance Operations Team for a Scaling Payment Platform.

Turn DAC7 into an expansion asset with a copy-paste checklist#

Use a checklist that proves you can launch jurisdictions with controlled reporting operations, not just DAC7 awareness.

- Define the bottleneck and set 4 to 6 metrics before changing tooling.

Write the current failure in one sentence, then track only metrics you can verify: internal hours per filing cycle, percentage of sellers with complete payout-linked records, exception volume, time from rejection to corrected resubmission, and launch delay caused by reporting readiness gaps. If you cannot reconcile sampled seller identity, tax data, and payouts, your baseline is not reliable.

- Confirm scope across DAC7 and OECD model rules, then assign owners.

Document what is in scope under DAC reporting rules for digital platforms, what is out of scope, and where OECD Model Reporting Rules also apply. Keep a minimum evidence pack: legal interpretation, reportable-activity map, seller field dictionary, and one named filing owner per jurisdiction.

- Choose an operating model with explicit build-versus-buy criteria.

Decide against clear criteria, not vague "flexibility" language: country-output maintenance, integration effort, change-control burden, exception handling, and finance operating load. If you are expanding across multiple EU markets, centralize reporting logic only if exported data is verifiable, correction logs are preserved, and support effort is costed realistically.

- Implement the flow in sequence with checkpoints and owners.

Run onboarding controls, transaction classification, reporting extracts, file generation, then submission and confirmation tracking. At each stage, assign one owner and one check: field completeness, file-schema validity, payout-to-seller reconciliation, and saved submission receipt by jurisdiction. Watch for identity mismatches, missing seller tax fields, and broken payout linkage.

- Launch in waves with hard go/no-go gates.

Sequence jurisdictions by operational readiness, not revenue potential alone. Before each wave, require data completeness above your internal threshold, a successful dry run, and a named owner for the submission window and exception queue. Use simple governance: weekly readiness review, visible issue log, and a pause rule when rejection or correction volume rises.

- Review economics and reliability monthly before the next wave.

Since tax-administration operating environments have changed significantly since 2010, a year-end-only review is too late for digital-platform reporting. Track reliability and cost together: exception volume, correction cycle time, internal support hours, and operating cost per added jurisdiction. If reliability worsens as you add countries, pause expansion, fix data and ownership gaps, then resume.

Frequently Asked Questions

What does a dac7 compliance case study actually prove beyond legal awareness?

A decision-useful case study should show whether a team turned legal scope into repeatable operations. The useful evidence is not just “we understood DAC7,” but whether records were complete, linked to payouts, turned into the required output, and documented through submission confirmation by jurisdiction. If a case study does not show baseline pain, ownership, checkpoints, and corrections, it is mostly an explainer.

What changed operationally in the Munch example that explainers usually skip?

Public vendor-led material does not give enough detail to verify the exact operating changes at Munch. The missing pieces are usually the ones that matter most: who owned exceptions, how seller fields were validated, what happened when records failed checks, and how corrected submissions were tracked. Treat those gaps as a red flag, not a minor omission.

Which metrics should founders and revenue leaders track first in a DAC7 rollout?

The public grounding here does not provide verified DAC7 benchmark metrics. As an internal checklist, track internal hours per filing cycle, exception volume, correction turnaround time, and the percentage of sellers with complete payout-linked records. A practical checkpoint is a sampled record review mid-cycle, not just at year end. If you cannot reconcile seller identity, tax data, and payout data in the sample, your dashboard is too optimistic.

How does stricter Dutch Tax Authority enforcement change operating priorities?

The public grounding here does not support specific claims about Dutch Tax Authority enforcement changes, so do not build your plan on rumored deadlines or penalty stories. What you should change is your evidence standard: keep portal receipts, corrected file versions, resubmission timestamps, and named owner sign-off for the Netherlands before you call that jurisdiction stable. If a country matters commercially, act as if weak documentation will be expensive.

What is the difference between a DAC7 explainer and a decision-useful case study?

An explainer tells you what the rule is. A decision-useful case study shows the starting bottleneck, the chosen operating model, the documents used to control quality, and the before-and-after metrics that management would actually use. It should also state what is still unknown, especially around ROI and vendor comparison.

Can DAC7 readiness accelerate European Union market expansion without hurting margin?

It can, but only when readiness means shared records and centralized control, not just filing capability. The best grounded parallel is VAT One Stop Shop. From 1 July 2021, online sellers and marketplaces can register in one EU Member State for VAT declaration and payment across covered supplies. In the Union-scheme scenario cited by the OSS registration guidance, the Member State of identification choice is tied to the calendar year plus two following calendar years. That centralization gives one registration point for covered OSS supplies, but it still depends on clean source data and clear jurisdiction ownership.

What key information is still unknown in public vendor-led DAC7 case studies?

In the public vendor-led material covered here, key gaps include independently verified outcome metrics, like-for-like vendor comparisons, and the exception-handling burden after launch. Public material may also omit adjacent tax decisions that affect expansion. Examples include whether a business used VAT Cross-border Rulings for complex transactions or how OSS was structured once the EU-wide EUR 10 000 threshold became relevant. If those details are missing, assume more internal work remains than the story suggests.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- blockchain-observatory.ec.europa.eu/european-blockchain-sandbox-announces-select...trusted

- cpuc.ca.gov/-/media/cpuc-website/divisions/energy-divisi...trusted

- sec.gov/Archives/edgar/data/1041061/0001193125230952...trusted

- sec.gov/Archives/edgar/data/1315098/0001315098230000...trusted

- taxation-customs.ec.europa.eu/archives/taxable-persons/vat-cross-border-ru...trusted

- taxation-customs.ec.europa.eu/system/files/2024-01/2023_CRM_Guide.pdftrusted

- tile.loc.gov/storage-services/service/ll/fedreg/fr041/fr0...trusted

- ufdcimages.uflib.ufl.edu/AA/00/01/66/16/01035/03-29-2016_pdf.txttrusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

How a Legal Marketplace Modernized Trust Accounting Compliance

Trust accounting is often treated as a compliance topic, but for a legal marketplace it is also an economic decision. When money movement and control are unclear, operating friction rises and pricing pressure gets harder to manage.

Gig Worker Tax Compliance at Scale: How Platforms Handle 1099s W-8s and DAC7 for 50000+ Contractors

At scale, the hard part is not the acronyms. It is deciding sequence, ownership, and evidence when Form 1099-K, Form 1099-NEC, Form W-8BEN/W-8BEN-E, and DAC7 do not line up cleanly. If you run a high-volume marketplace, put controls in the right order and define clear stop points where legal or tax takes over.

Writing Case Studies for B2B SaaS That Buyers Trust

If you work independently, you do not need another gallery of polished examples. You need a way to produce B2B SaaS case studies that help a buyer trust the result, help a client feel fairly represented, and hold up in review when someone asks, "Where did this number come from?"