Quick Answer

Choose BaaS when your team can run approvals, monitoring, reconciliation, and change control after go-live; otherwise keep scope narrower until those owners are staffed. The article treats MoR as contract-defined, not a default liability transfer, so require explicit terms for disputes, refunds, and reporting boundaries. Before signing, ask for a written responsibility matrix and at least one real artifact, such as a reconciliation export or escalation workflow.

What Changes Operationally Between BaaS and MoR#

In banking partnerships, the BaaS vs. MoR decision is about operating ownership after go-live, not whose demo looks better. Before you compare vendors, you need clear owners for approvals, monitoring, reconciliation, exception handling, and change control.

Map roles first. In a BaaS setup, fintechs work with banks and other financial institutions to deliver regulated products, often through API integrations at scale. If additional operating parties are involved, make their contract scope explicit. That still does not define who approves changes, who reviews alerts, or who can produce evidence when incidents happen.

For broader policy background, review the interagency guidance on third-party relationship risk management and the request for input on bank-fintech arrangements involving banking products and services. In a dense regulatory environment, BaaS can support scale through APIs, but scale does not replace oversight.

Evidence is the control most teams underweight. Even when operations are outsourced, sponsor-bank accountability for accurate deposit balances remains. Where deposits, custodial balances, or reconciliation depend on third parties, careful records and clear beneficial-owner data matter. If a platform fails or records drift, those records can be the difference between a controlled incident and operational chaos. In the sponsor-bank context, daily reconciliation has been described as required when banks depend on third parties.

Start with three questions early:

- What must be approved before a new flow or product change goes live?

- Who produces monitoring evidence, reconciliation outputs, and exception logs?

- Who owns change control when onboarding, ledger logic, or funds movement changes?

If those answers are still vague, stop. Choose the model whose parties can show named owners, real approval paths, and operating artifacts, not just APIs. If you are still sorting adjacent transaction models, the MoR vs. PayFac vs. Marketplace model comparison for platform teams is a useful companion.

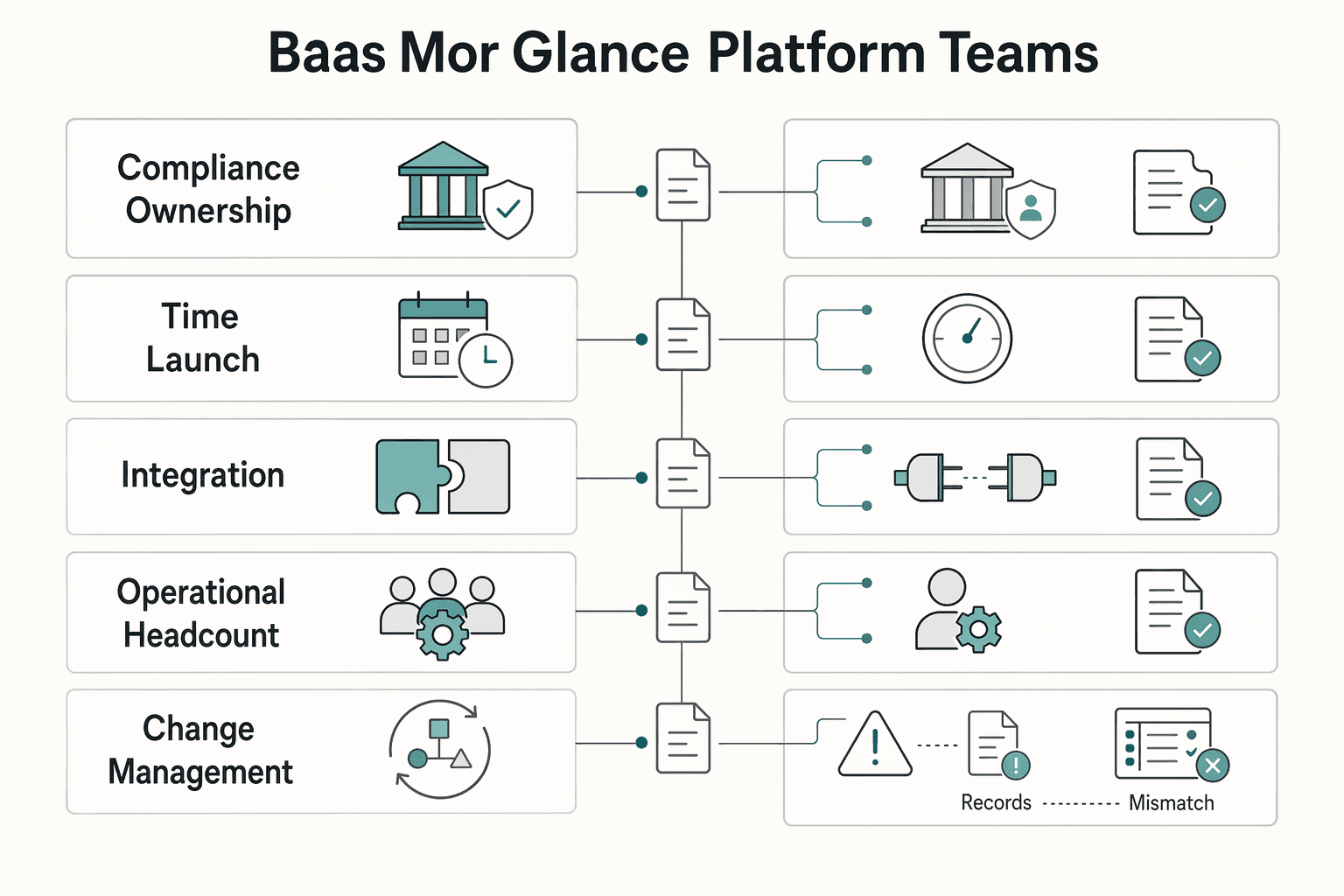

BaaS vs MoR at a glance for platform teams#

For platform teams, this is usually a risk-first decision, not a speed-first one. In current BaaS discussions, partner selection is treated primarily as a safety, compliance, and risk-management decision, and the wrong bank partner is framed as a business-threatening risk. As a market snapshot, U.S. sponsor-bank count was cited at 156 in Q3 2025, alongside tighter oversight. Treat MoR scope as contract-specific.

| Decision area | BaaS | MoR | What to verify before you sign | Common risk in practice |

|---|---|---|---|---|

| Compliance ownership | Program growth and tighter oversight can happen at the same time, so expect compliance scrutiny to remain central as programs scale. | Not established here. Define legal and compliance responsibility explicitly in contract language. | Require a written responsibility matrix for policy decisions, reviews, disputes, support handoffs, and evidence retention. | BaaS: partner controls can be weaker than your risk tolerance. MoR: assumed responsibilities are not explicitly assigned. |

| Time to launch | Speed and developer experience can matter, but current framing treats them as tie-breakers rather than primary selection criteria. | No grounded claim here that MoR is always faster. | Confirm what approvals are required before adding new clients or new product changes, and whether similar checkpoints apply at launch. | A technically ready flow stalls in review or approval queues. |

| Integration scope | Partnerships may involve sponsor-bank and provider layers, so handoffs and decision rights should be explicit. | Not established here. Integration scope depends on provider model and contract. | Review error states, retries, and lifecycle behavior, not only happy-path APIs. | Reconciliation and support issues surface at boundary handoffs. |

| Operational headcount | Risk and compliance operations should be sized for ongoing oversight, not just launch velocity. | Not established here. Required operating load depends on contract scope. | Identify day-to-day exception owners and expected response times. | Exception queues outgrow staffing or ownership coverage. |

| Change-management burden | In at least one enforcement example, adding new clients or new products required prior regulatory non-objection. | Not established here. Do not assume a standard approval path across providers. | Get a written change-approval path for new features, exceptions, and production changes. | Small changes trigger long review cycles or blocked launches. |

| Account management boundary | Boundaries across sponsor bank, platform, and providers must be explicit. | Not established here. Account and customer boundary depends on the specific operating model. | Confirm system-of-record ownership and conflict handling between provider records and your UI. | Stale or inconsistent status creates customer and support friction. |

| Payments capabilities boundary | Where flows rely on correspondent banking networks, costs can be higher and less predictable, and settlement can take up to 5 business days. | Not established here. Capability scope should be treated as contract-specific. | Separate native capabilities from exceptions and items needing extra approval. | A promised flow is treated as out of scope at implementation time. |

| Onboarding rules boundary | In some contexts, new-client onboarding can be constrained by partner controls and approval checkpoints. | Not established here. Acceptance and onboarding rules must be explicitly documented. | Ask for rejection reasons, review paths, and document requirements upfront. | Target segments are blocked by undocumented acceptance criteria. |

| Ongoing monitoring boundary | Oversight emphasis on safety, soundness, and compliance means monitoring and escalation boundaries must be clear. | Not established here. Monitoring visibility should be confirmed in writing. | Ask for sample monitoring outputs and reconciliation exports. | Alerts or payout issues surface without clear escalation context. |

| Direct fit rule | Choose BaaS only if your team can operate within a risk-first partner model where safety and compliance are primary and speed is secondary. | Treat MoR fit as a contract-by-contract decision. | Decide with product, finance, ops, and engineering together. | If ownership is vague on either side, pause and clarify before implementation. |

Do not accept abstract claims like "we handle compliance" or "we move fast." Require a written ownership map for account management, onboarding, monitoring, and payment exceptions. Make MoR liability and compliance scope explicit in the contract before launch. Ask for at least one operating artifact, such as a reconciliation export, escalation path, or change-approval checklist. For adjacent revenue-split questions, see How MoR Platforms Split Payments Between Platform and Contractor.

The three models readers confuse and why that causes bad decisions#

These three models are not interchangeable. Treating them as synonyms can create ownership failures at launch, especially when teams assume an API defines legal responsibility.

| Model | What it is in plain terms | Where the licensed bank and fintech firm sit | What an API actually gives you |

|---|---|---|---|

| bank-fintech partnership | A bank or credit union runs a fintech partnership program, either through its own channel or with an intermediary | The partner bank is the licensed institution; the fintech operator and/or intermediary may run customer-facing and operational layers, depending on structure | Software access to offered functions, not the bank role itself |

| Banking-as-a-Service (BaaS) | An API-driven delivery model within bank-fintech partnerships | The bank remains the licensed institution; a fintech provider or intermediary can provide much of the technical layer | A defined technical interface for actions and data, not by itself a transfer of regulatory responsibility |

| Merchant of Record (MoR) | A separate payments construct often discussed alongside these models | This material does not establish a definitive legal or compliance split for MoR versus bank-partnership roles | Technical tooling may be exposed, but accountability still needs to be explicitly assigned |

The distinction is straightforward. A bank-fintech partnership is the broad arrangement. BaaS is an API-driven delivery model within that market. MoR is a separate construct; treat its risk ownership boundaries as contract-specific.

So "we have APIs" is not a strategy. An API is a technical access point. It can support integration, but it does not by itself resolve compliance ownership or accountability when controls fail.

Before you sign, confirm roles in writing. Confirm whether the model is direct or intermediary-led, which licensed bank is behind the program, who is responsible for regulatory risk and controls, and where approval responsibilities sit. In enforcement context, one concrete gating checkpoint is regulator non-objection before onboarding new fintech partners. A common failure mode is weak sponsor selection, which is associated with transaction failures, regulatory issues, and customer fund-access risk.

Compliance ownership is the real decision point#

Choose the model your team can operate after go-live, not the one that looks easiest in a demo. If ownership of funds, ledger control, and recordkeeping is unclear on day one, risk can show up later under stress.

Ownership map that matters in practice#

| Decision point | Licensed bank role | Partner program or your platform role | MoR setup role |

|---|---|---|---|

| Service origination vs. distribution | Underlying banking services must originate from a licensed entity | Aggregators or partners may package and distribute assembled services | The label alone does not answer who owns accountability in practice |

| Legal fund-holding responsibility | Must be explicitly assigned | Must operate in line with the legal assignment | Must be explicitly assigned in contract. Do not assume. |

| System of record (ledger ownership) | Needs independent control and real-time or near-real-time visibility into balances, fund location, and proof of ownership | May run parts of operations, but ownership and access must be explicit | Verify who maintains the ledger and what visibility exists in practice |

| Governance, controls, and recordkeeping | FBO structures remain viable only with adequate governance, control, and recordkeeping | Day-to-day tasks can be distributed, but accountability should not be ambiguous | Require documented controls and records before launch |

In bank-fintech arrangements, unclear accountability can be where failures start. Current governance expectations emphasize independent control and visibility over customer funds, even when operations are spread across multiple partners.

The FBO model has existed for more than a decade. It can still work, but only when governance, control, and recordkeeping are durable.

Why U.S. pressure can slow program changes#

Program changes can slow when ownership and control are not clearly documented. In the post-Synapse environment, tolerance is lower for opaque ledgers, fragmented ownership of critical controls, and unclear accountability when failures occur.

This does not make bank-fintech programs off limits. It does mean expansions and control changes can face tighter scrutiny unless ownership, visibility, and recordkeeping are clear before launch.

What to verify before signing#

Before you sign, ask for evidence on three points:

- Who legally holds customer funds.

- Who maintains the system of record and can provide real-time or near-real-time visibility into balances, fund location, and proof of ownership.

- How independent control, reconciliation, and failure accountability work if a critical middleware or ledger provider fails.

Use this decision rule. If your team cannot show explicit ownership of funds, explicit ownership of the ledger, and a tested reconciliation path, do not treat the model as launch-ready. When accountability is vague, customers can lose access to funds and reconciliation can break down.

Build effort and launch timing by function#

Plan launch timing across functions, not only around how quickly engineering gets API access. For integrated payments, splitting implementation into five tracks early can help teams avoid assuming the integration is done once the API calls work:

- API integration

- Event and operations handling

- Finance and reporting mapping

- Compliance scope and controls

- Exception handling

Where build effort usually concentrates#

Build effort usually spills beyond API integration into event handling, finance mapping, and exception management. In BaaS, bank services are delivered through APIs, either directly by a bank or through a platform partner that interfaces with the bank.

Build effort and timing can shift by model. In one thin API-layer example, a debit card product launches in weeks, with the bank retaining risk decisions, account terms, and compliance policies. Fuller-stack BaaS can include core banking, ledger, compliance automation, and lending infrastructure. That gives the fintech more control and more operational responsibility. Some providers position licensing, KYC/AML, and transaction processing as managed components, but exact scope is contract-defined.

For MoR, this guide does not define one standard technical scope. Treat MoR effort as contract-defined. Confirm exactly which events, statuses, reports, and exception paths you will receive before you lock your plan.

| Function | BaaS | MoR |

|---|---|---|

| Integration surface | Bank services via API, directly or through a platform partner | Scope is provider-specific and must be documented |

| Testing depth | Validate API behavior and your internal handling of operational and finance workflows | Validate only the functions and handoffs explicitly included in the contract |

| Go-live dependency | Technical readiness plus clear ownership for the responsibilities in your chosen model | Provider-delivered scope and documented handoff readiness |

| Production checkpoint | Agreed ownership, tested operational handling, and clear escalation paths | Confirmed scope, reporting outputs, and escalation contacts |

Order of operations to reduce launch risk#

A lower-risk sequence is to lock ownership before technical design hardens around assumptions.

- Commercial terms

Confirm pricing logic, reporting access, support coverage, and exception handling responsibilities.

- Compliance scope

Confirm who owns approvals, reviews, and exception handling before design decisions harden around assumptions.

- Technical design

Define how APIs and operational outputs map into your product and operations.

- Sandbox validation

Test the real launch paths end to end and confirm ops and finance can use the outputs.

- Controlled rollout

Start narrow, with named escalation contacts and a manual path for unsupported or unclear cases.

If you are deciding between BaaS and MoR, use one practical rule: choose the path whose production checkpoints you can evidence before go-live.

Failure modes that create expensive rework#

Expensive rework can come from mis-scoping, not API access alone. Before launch, define whether a program is full BaaS or another fintech partnership, because many institutions blur that line.

This is a lifecycle issue, not a one-time diligence step. If scope classification is weak early, it can resurface later under supervisory scrutiny.

Where "live" often breaks#

Partnerships can look live on the happy path while still carrying structural risk. Check these pressure points before launch:

| Area | What looks live | What fails in practice | What to verify before launch |

|---|---|---|---|

| Scope classification | A bank-fintech product is live and processing activity | Teams do not clearly differentiate certain fintech partnerships from full BaaS | Written classification for each product or flow and rationale for that label |

| Partnership model design | One operating model is documented for everything | Bank-fintech partnerships are a continuum, and one-size assumptions can leave gaps | Model-by-model operating map and decision log |

| Supervisory signal readiness | No immediate regulatory blockers appear | Consent-order examples indicate heightened scrutiny of bank-fintech partnerships | A documented process to track, assess, and act on supervisory signals |

| Policy trade-offs | Decisions emphasize efficiency and competition | Trade-offs with stability, integrity, and consumer or privacy outcomes are not explicit | Explicit trade-off record and governance signoff |

A common mistake is assuming every partnership carries the same risk profile. Partnership type and scope vary, so map decisions line by line instead of using one blanket label.

Red flags in vendor conversations#

Treat these as warning signs before launch:

- They cannot clearly distinguish full BaaS from other fintech partnership models.

- They describe one fixed model and cannot explain where they sit on the partnership continuum.

- They emphasize efficiency and competition but cannot explain stability, integrity, and consumer or privacy trade-offs.

- They treat consent-order scrutiny signals as isolated events instead of governance inputs.

The practical fix#

The fix is simple: require a pre-launch evidence pack, not just contract language. At minimum, ask for a written scope classification, partnership-model map, and a governance record of policy trade-offs.

That pack should show how the team distinguishes full BaaS from other fintech partnerships, how model choices are documented across the partnership continuum, and how supervisory signals are monitored and escalated. If a provider cannot produce those artifacts, treat post-launch rework risk as higher. Evidence is the safer decision signal.

Which option fits your platform stage and risk appetite#

Pick the model your team can run cleanly after launch, not the one with the best demo. For many early platforms, that means staying narrower first and moving deeper into BaaS when product-level control of funds flow and onboarding becomes core.

The split is practical. Stay narrower while you validate demand and keep operating scope light. Move toward BaaS when you need direct control over funds movement and onboarding and can handle bank-approval dependency and slower approval cycles.

Stage recommendations by platform model#

Use this as a working guide, not a rulebook. Treat MoR references as contract-scope checks rather than legal conclusions.

| Stage | Contractor platform | Creator platform | Marketplace platform |

|---|---|---|---|

| Early | If you use a narrow outsourced model (including MoR), keep scope simple and verify contract coverage for your transaction types. Revisit BaaS when control of funds movement or onboarding becomes core. | Keep scope narrow while flows are standard and funds movement is not a core differentiator. Revisit BaaS if onboarding and money movement begin driving product value. | Stay narrow first if custom funds movement is not yet central. Start BaaS diligence when payout logic or onboarding complexity becomes core. |

| Growth | If narrow scope still works operationally, keep it while you evaluate BaaS tradeoffs for deeper control. | Stay narrow while provider scope still fits; start BaaS diligence when you need more direct control of onboarding or funds movement. | This is often an inflection point. If you need finer control of onboarding or funds movement, compare BaaS with adjacent models before signing. If structure is still shifting, compare MoR against payfac and marketplace models. |

| Scaled | Choose BaaS when financial features are central and the team can run ongoing bank-partner approval processes. Stay narrower if that operating load is not yet justified. | Choose BaaS when financial tooling is central to the creator experience. If not, stay narrower and negotiate stronger reporting and change terms before taking on bank-partner complexity. | BaaS can fit when money-movement design is a competitive feature and your team can run ongoing approvals and controls. If that operating model is still unsettled, wait. |

A quick decision filter#

Use these four checks before deciding:

| Check | Grounded guidance |

|---|---|

| Launch velocity | Timelines vary by provider and model. One source says many bank-partnered programs take about 9-11 months to go live once diligence, integration, and approvals are included. |

| Compliance operating capacity | If you cannot support ongoing approval and compliance workflows, BaaS is usually premature. |

| Operating dependency | BaaS coverage varies by provider, so confirm exact ownership boundaries and the reporting/reconciliation outputs you will actually receive. |

| Need for product-level funds-flow control | If core product value depends on controlling funds movement and onboarding, the tradeoffs of staying narrow increase, and BaaS may be worth the added operating load. |

Tradeoffs that matter in practice#

BaaS coverage varies by provider, so category labels are not enough. Verify exact ownership boundaries, approval paths for new flows, reporting outputs, and production responsibilities.

A core BaaS risk is dependency. Teams report slow and uncertain approvals, and unapproved features can stall. One cited scenario describes offboarding with as little as 30 days' notice, with potential customer-fund disruption, so confirm offboarding terms, data return, and records handling in writing.

For MoR, base decisions on contract scope and operating reality. Verify covered transaction types, refund and dispute boundaries, support responsibilities, and reporting detail explicitly.

When not now is the right answer#

A deliberate "not now" is often the lower-risk decision. Defer signing if the added operating burden is still unclear.

If bank-approval dependency is already constraining you, direct licensing can be a later-stage path, but it is not a shortcut. One source says initial MTL approvals can come in as little as 3-4 months in some states, often starting with 5-10 states. It also cites about $1 million in starting capital to begin applications. These are not universal minimums, and requirements vary by state. The same source explicitly lists funds-flow information and an organizational or management chart as licensing artifacts.

The practical question is simple: which model can your team operate reliably for the next 12 months? If you need funds-flow control now and can staff ownership, go deeper on BaaS diligence. If you still need speed or cleaner scope, stay narrower for now and make that decision explicitly.

For a step-by-step walkthrough, see Choosing a Fintech Platform for Consumer Subscription Billing and Recurring Revenue.

The minimum evidence pack before signing anything#

Treat a missing written evidence pack as execution risk before you sign a BaaS partner deal. If a sponsor bank or key provider cannot provide concrete operating evidence before contract close, that is a warning sign. A practical checkpoint is having that package ready before onboarding discussions.

In U.S. bank-fintech arrangements, start with a written ownership matrix reflected in contracts and SLAs. It should name who owns reconciliation across programs and who is responsible for identifying and resolving breaks. Vague ownership can make launch speed, scaling confidence, and regulator navigation harder to assess.

| Evidence area | What to request | What to verify | Red flag |

|---|---|---|---|

| Ownership | Written matrix across the sponsor bank and key partners | Roles and responsibilities are explicit in contracts and SLAs, with named owners | "Shared" ownership with no named approver |

| Operations | Reconciliation artifacts, break-resolution process details, and relevant public consent-order history | Reconciliation ownership is clear; break identification and resolution owners are named; consent orders are reviewed at a high level | Poor ledgering or loose reconciliation controls |

| Technical | Architecture and API documentation, regulatory-readiness and security-operations materials, SLA terms, and data-portability plans | Architecture and API expectations are clear; security and SLA ownership are explicit; portability is defined | Slides only, with no concrete operating evidence |

Two checks can surface gaps quickly. First, review any public consent orders at a high level and ask how related issues are managed today.

Second, test reconciliation ownership before onboarding. Ask how ledger reconciliation is handled across fintech programs and who is responsible for identifying and resolving breaks. If that answer is fuzzy, weak diligence tends to show up later as incidents, audit findings, or stalled roadmaps. For adjacent dispute and recovery issues, see Chargeback Management for Marketplaces and MoR Dispute Recovery.

Integration and operations design that prevents month-end chaos#

Design for month-end close from day one, but do not confuse technical integration with launch readiness. In Q4 2023 commentary on bank-fintech programs, fewer new products were launching as partner banks became more cautious, and scrutiny plus enforcement risk were described as very high.

Launch checkpoints, not API-success first#

Treat API success as an input, not proof that a launch can proceed. In bank-fintech partnerships spanning payments, banking, and lending infrastructure, regulatory and partner-bank approvals can still gate go-live.

| Layer | What must exist | What to verify before launch | What breaks if missing |

|---|---|---|---|

| Partner evaluation | Clear criteria for integration ease, product customization, and speed to market | The team agrees on tradeoffs instead of optimizing for speed alone | Late vendor rework and launch drift |

| Approval dependencies | A written map of required approvals for the exact client or product scope | Whether your program needs non-objection before adding new clients or products | Launch-ready work that cannot be released |

| Product gating | Product-specific go or no-go conditions | Whether new lending is approval-gated in your case | Month-end plans stall at signoff |

| Timeline assumptions | A plan that separates integration pace from compliance checkpoints | Which steps can move in weeks and which remain approval-bound | Missed close dates from unrealistic sequencing |

Use one fast checkpoint before launch. Confirm owners, status, and fallback for every external approval dependency tied to this release.

Speed claims and compliance reality#

Some vendors market implementations in weeks, not months. That can help with planning, but it does not remove approval dependencies, and Q4 2023 commentary still described elevated scrutiny and enforcement risk in bank-fintech programs.

Plan for both conditions at once: technical work may move quickly while launch authorization still depends on regulator or partner-bank signoff.

Finance-ops checks that matter in production#

Define escalation ownership before launch. For each dependency, assign who handles internal investigation, third-party handoff, and regulator-facing follow-up if approvals stall.

Treat readiness as a combined operations and compliance decision. Check partner fit against integration, customization, and speed criteria. Then confirm a clear approval map and go-live clearance for the specific products and client scope in this release.

The 30-day decision checklist teams can run immediately#

Use this example four-week cycle as a structured selection process, not a sales cycle. Treat it as a practical operating framework, not a complete legal checklist. Proceed only when ownership, controls, and evidence are clear enough to run in production.

| Week | Decision goal | What you need to see | Red flag |

|---|---|---|---|

| 1 | Lock decision criteria and ownership boundaries | Written ownership for compliance tasks, audit evidence, ongoing monitoring, and termination planning | Team says "the provider handles that" without naming the entity or document |

| 2 | Run standardized diligence across options | The same question set for sponsor-bank, partner-program, and intermediary candidates, including mission-fit and regulatory-readiness checks | Vendors judged on different standards, so comparison becomes sales-led |

| 3 | Pressure-test operating readiness | Evidence that monitoring, escalation, control checks, and cross-functional review can run under real conditions | A strong demo, but no evidence the team can run controls consistently after launch |

| 4 | Decide and set launch guardrails | Chosen path, controlled rollout rules, escalation owners, rollback steps, and an evidence pack stored for audit and ops | Contract moves forward before operational staffing and escalation paths are named |

Set decision criteria in week 1#

Set decision criteria before more vendor conversations. The first decision is responsibility and regulatory readiness. In bank-fintech partnerships, banks can face significant regulatory pressure and expectations, and many are highly reliant on third parties.

Produce a one-page ownership matrix that names owners for onboarding rules, monitoring, policy exceptions, audit evidence, reconciliations, incident review, and termination planning. Use a simple lifecycle structure: selection, launch readiness, ongoing monitoring, and termination. If ongoing monitoring or termination is still undefined, you are likely not ready to compare pricing.

Run comparable diligence in week 2#

Run one standardized diligence questionnaire across every option. This keeps comparisons objective and helps prevent a sales-led decision. Keep questions directly comparable:

- How does this partnership fit your mission and customer strategy?

- What regulatory and compliance expectations apply before and after launch?

- Who owns ongoing monitoring, incident escalation, and audit evidence?

- How will both sides handle growth if demand outpaces compliance capacity?

- What are termination and migration expectations if the relationship stops working?

Ask for sample operating artifacts that show how controls run in practice. If a vendor can describe the process but cannot show usable evidence, treat that as a launch risk.

Prove the flow in week 3#

Run a production-like operating proof, not a demo. Review the same evidence across product, risk and compliance, finance, and engineering so governance and operations stay aligned. Use these minimum test cases:

- Escalation paths are clear and staffed.

- Monitoring and issue management can run continuously, not just at launch.

- A small-volume pilot can run without bypassing controls.

- Growth assumptions are realistic for both fintech and bank operating constraints.

Also verify resilience under disruption. Your proof should show the team can pause safely, investigate quickly, and resume with documented decisions when control issues appear.

Make the call in week 4#

Make the decision only after the evidence pack is complete. Then document launch guardrails: rollout scope, stop conditions, first-look incident owner, escalation path, including bank or intermediary where relevant, and rollback steps.

Do not approve launch on commercial terms and demo results alone. Guardrails should explicitly cover control breaks, monitoring gaps, and policy gates that block live activity.

Use a clear go or no-go gate#

Proceed only if all four are true:

- Ownership boundaries are written and accepted by product, finance, ops, and compliance.

- Diligence produced usable evidence, not just assurances.

- Operating proof showed the team can run controls and escalation under real conditions.

- Staffing matches the operating burden and expected growth pace of the chosen model.

If any one is missing, the right decision is no go for now.

If your checklist leans toward shifting transaction-side operations, review how a MoR setup may affect ownership boundaries before contracting: See Gruv Merchant of Record for businesses.

Conclusion#

Choose the model your team can operate responsibly after launch, not the one that is most popular. In practice:

- Choose Banking-as-a-Service (BaaS) when your team is prepared for explicit operational and compliance ownership in the program.

- Choose Merchant of Record (MoR) only after you verify, in contract and in operations, which responsibilities are actually owned by the provider versus your team.

Treat this as an operating-capability decision. In U.S. bank-third-party arrangements, recent guidance and joint agency messaging point in the same direction: third-party use can add risk, and banks still remain responsible for compliance and safe operation.

Ask a day 2 question before signing: what can your team actually own once volume, exceptions, and audits begin? MoR responsibilities are not established in the evidence here and can be provider-specific and contract-specific, so do not assume a zero-obligation shortcut for your platform. BaaS can work, but only when ownership is explicit and staffed.

Use evidence, not promises. Require a written ownership matrix for day-to-day operational, financial, and compliance responsibilities, plus clear change and dispute governance. Confirm what must be approved before production, who signs off, what evidence is retained, and how record access and contingency plans are handled.

Launch in stages with named owners for monitoring, exceptions, and rollback. If ownership, change control, or production-readiness evidence is vague, pause before go-live.

When you have a draft responsibility matrix and want a practical fit check, use this as a scoping conversation for your team: Talk to Gruv.

Frequently Asked Questions

What is Banking-as-a-Service (BaaS) in a fintech partnership context?

BaaS is a way to embed bank-provided accounts and payment services in your product while operating alongside a bank. In the grounded model here, the bank provides the account and payment services, while customers interact day to day with the fintech brand. What to verify: clear documentation of who owns onboarding, monitoring, escalation, and evidence retention.

What is Merchant of Record (MoR), and how is it different from BaaS for a non-bank entity?

Treat MoR as contract-defined until scope is explicitly documented. The sources here support BaaS role boundaries, but they do not establish MoR legal-seller scope or liability allocation. What to verify: contract scope for refunds, disputes, tax handling, and the customer-facing counterparty; if useful, see MoR vs. PayFac vs. Marketplace Model for Platform Teams.

When should a marketplace platform choose MoR instead of a direct partner bank program?

Make that decision based on your ability to operate the model after launch, not on sales demos. For bank-partner programs, grounded evidence shows bank-level review and account-opening controls tied to KYC and AML, so governance and staffing needs are real from day one. What to verify: whether your team can support cross-functional implementation, contingency planning, and named escalation owners before launch.

What tradeoff matters most in practice: launch speed, control, or compliance ownership?

Compliance ownership matters most because it determines whether the model is workable in production. In BaaS partnerships, a common tension is UX friction versus strict rule adherence, and regulatory missteps are a known risk. What to verify: who approves exceptions, who reviews monitoring outcomes, and whether reconciliation evidence is usable.

Can a fintech start with MoR and move to BaaS later?

Potentially. Moving into a bank partnership can require bank-level due diligence and operating changes tied to ongoing oversight. What to verify: whether contracts allow migration and whether product and finance can keep a clean reconciliation history through the transition.

Which risks increase when working with a regional bank, community bank, or credit union program in the United States?

Do not use institution type as a shortcut for operational risk. The grounded requirement is consistent across partnership types: strong third-party risk management, cross-disciplinary implementation, technical staff to maintain the solution, and lifecycle contingency planning. What to verify: review expectations, staffing depth, and escalation ownership if controls fail after go-live.

What documents and technical evidence should teams request before signing?

Ask for operating evidence, not summaries. Request responses to structured diligence questions, third-party risk controls, implementation checkpoints, technical ownership, and contingency planning artifacts. What to verify: that the evidence is current, matches contract scope, and is reviewable by product, ops, finance, and compliance.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- brooklynworks.brooklaw.edu/cgi/viewcontent.cgitrusted

- documents1.worldbank.org/curated/en/099735304212236910/pdf/P17300608c...trusted

- federalreserve.gov/apps/proposals/comments/FR-0000-0134-01-C137trusted

- occ.gov/topics/charters-and-licensing/public-comment...trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC7861282trusted

- pmc.ncbi.nlm.nih.gov/articles/PMC12939948trusted

- scholarship.claremont.edu/cgi/viewcontent.cgitrusted

- supremecourt.gov/DocketPDF/22/22-7044/259488/2023032210182749...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: