Quick Answer

Start by splitting bank-presentment status from debt status, then route each item through owned internal states until final disposition. A stale cheque uncashed payment policy uncollected funds platform teams can defend should require outreach logs, a maintained jurisdiction matrix, and ledger evidence that the obligation stayed open until reissue or remittance. Add explicit escalation triggers for ownership disputes, compliance holds, and unclear governing jurisdiction.

What this article will help you decide#

This article helps you choose the minimum controls needed to handle stale and uncollected payouts in a way that is defensible, traceable, and hard to duplicate.

1) Whether you are the intended reader#

You are in scope if you own payout risk across markets in compliance, legal, finance, or risk, especially for contractor, seller, or creator disbursements. If you set policy, approve reissues, review aged liabilities, or answer audit questions, this is built for your decisions.

A practical fit check: do you already have clear ownership for program controls, inventory management, and issue escalation? That ownership split matches the structure in IRS IRM 11.3.41, specifically Program Controls, Inventory Management Requirements, and Guidelines for Improving Issues.

2) When this is more process than you need#

If you operate in one country, handle occasional checks, and do not have meaningful unclaimed property exposure, a lighter documented process may be enough. Do not overbuild. When exceptions are rare and one team can review them end to end, extra layers often add overhead without reducing much risk.

3) What a defensible review process usually includes#

At minimum, you need an inventory-management focus and a defined escalation path for disputed facts or adverse decisions. That lines up with the IRM 11.3.41 inventory-management focus and issue-elevation guidance.

For due-process design, use baseline principles reflected in Colorado Initiative 2025-2026 #273. Before adverse action, those principles include written digital notice with the factual and legal basis, a reasonable chance to respond with evidence, neutral decision-making, and appeal or judicial review where provided by law. Treat that baseline as conditional, not universal, because the text says it applies unless a more specific procedure is provided.

4) What you should expect from the rest of the article#

What follows is a decision framework for what to implement now versus later. The goal is not to build every possible control. It is to prioritize the controls that close real exposure without creating unnecessary process.

If you want a deeper dive, read Airline Delay Compensation Payments: How Aviation Platforms Disburse Refunds at Scale.

1) Define your liability boundary before you write policy text#

If you are replacing ad hoc SOPs with one written standard, define this boundary first: a check outcome and a liability outcome are not the same decision. Your policy should say what changes when a check is declined or flagged as stale, and what stays open until a separate review is complete.

Treat this as an operational control boundary, not a one-step legal determination.

Keep these decisions separate in every case record:

- instrument status, for example accepted, declined, returned

- liability status in the ledger

- assigned owner for the next decision step

What to put in the policy#

Write the boundary in operational language. For each uncashed item, require at least:

- check issue date and amount

- bank decline or return evidence, if present

- current ledger treatment

- payee contact details and outreach history

- next owner and next action, for example reissue review or legal/compliance review

This helps prevent a failure mode where one team marks an item closed after a bank event while another still carries it as payable, or no team owns it at all.

The control standard to anchor on#

Use the OCC Payment Systems control lens to keep this boundary auditable and testable: documented Policies and Procedures, Internal Controls, Risk Assessment, and management and board reports, plus explicit handling for Checks and Other Monetary Instruments. The point is discipline, not a one-size-fits-all legal conclusion.

In practice, an item can be declined while the amount remains open in your liability process until the next disposition is documented and assigned.

For a step-by-step walkthrough, see Liquidity Management for Payment Platforms With Funds Ready to Pay.

2) Separate stale status from true dormancy status#

A stale-dated check is not automatically a closed obligation. "Stale" is a bank presentment status tied to checks presented more than six months after the check date, and a bank or credit union may still choose to honor the check. That decision does not, by itself, end your liability.

Keep stale status and dormancy status as separate control states so uncashed items do not disappear before unclaimed-property handling is complete.

Use a four-state model as an internal control#

| State | Definition | Notes |

|---|---|---|

| Issued | check sent | liability stays open |

| Stale-dated check | check is more than six months old | stale keys off check age |

| Dormant | abandonment period has run under the applicable state rule | may depend on last owner activity or last documented owner contact |

| Remittable | required reporting, notice, and transfer steps are due or completed | depends on required filing and notice steps, not just an old check date |

The trigger logic matters more than the labels. "Stale" keys off check age. "Dormant" keys off abandonment timing, which may depend on last owner activity or last documented owner contact. "Remittable" depends on required filing and notice steps, not just an old check date.

A key control field. Track the last documented owner contact or activity date in every case. If you start dormancy timing from issue date alone, you can mis-age cases and move items too early.

That is why stale items should usually stay in a tracked liability account until final disposition. A check can be stale for payment handling while the underlying obligation remains open in your records.

Payroll checks show why this matters. Payroll checks make the gap obvious. A check may be stale after more than six months, while some guidance sets payroll abandonment at one year rather than three years for other checks. Stale status and unclaimed-property timing can diverge.

If a payroll check goes stale, keep it assigned and tracked through outreach, reissue review, or unclaimed-property processing. Move it only when the required timing and notice steps are actually met.

Evidence required before advancing status#

Before you move an item from stale to dormant, or dormant to remittable, confirm:

- check date and whether it is more than six months old

- property type, including whether it is payroll

- last known owner address and last documented owner contact or activity date

- outreach record, including due diligence notice where required

- ledger evidence that liability remained open until claim, reissue, or remittance

If this evidence is missing, the item is not finished. Keep the uncashed check open, owned, and visible until disposition is documented.

Related reading: How to Expand Your Subscription Platform to APAC: Payment Methods Currency and Regulatory Market.

3) Use one jurisdiction matrix to avoid one-size-fits-all mistakes#

If you handle uncollected funds across multiple markets, a counsel-owned jurisdiction matrix can help keep handlers from relying on ad hoc judgment for state escheatment law decisions.

A single matrix may improve consistency and legal review, but only if someone maintains it with counsel-approved updates.

What to standardize in the matrix#

The provided materials do not establish state-by-state dormancy periods, due-diligence timing or content, or remittance triggers, so those entries should come from counsel-approved jurisdiction research.

Use the table below as an internal template, not a statutory list of required fields.

| Jurisdiction | Owner state rule | Due-diligence requirement | Remittance trigger | Documentation needed for escheatment process | Last legal review |

|---|---|---|---|---|---|

| State A | Counsel-approved summary | Required notice step or "none identified" | Counsel-approved trigger | Counsel-specified evidence and legal source copy | YYYY-MM-DD |

| State B | Counsel-approved summary | Required notice step or "none identified" | Counsel-approved trigger | Counsel-specified evidence and legal source copy | YYYY-MM-DD |

| State C | Counsel-approved summary | Required notice step or "none identified" | Counsel-approved trigger | Counsel-specified evidence and legal source copy | YYYY-MM-DD |

Keep checkpoint discipline visible. The matrix only works if handlers use it case by case. Before you move a case forward, require the handler to attach the exact matrix row used and confirm that the row is current.

This aligns with the unclaimed-royalties checkpoint model. The Copyright Office's July 2021 report describes formal checkpoints, including a report due not later than 2 years after initial designation and submission to both Senate and House Judiciary Committees, and it says the collective should give substantial weight to the recommendations when setting procedures.

One caveat: if Securities and Exchange Commission (SEC) material comes up in review, treat it as background context here, not as a replacement for the applicable state-level unclaimed property determination.

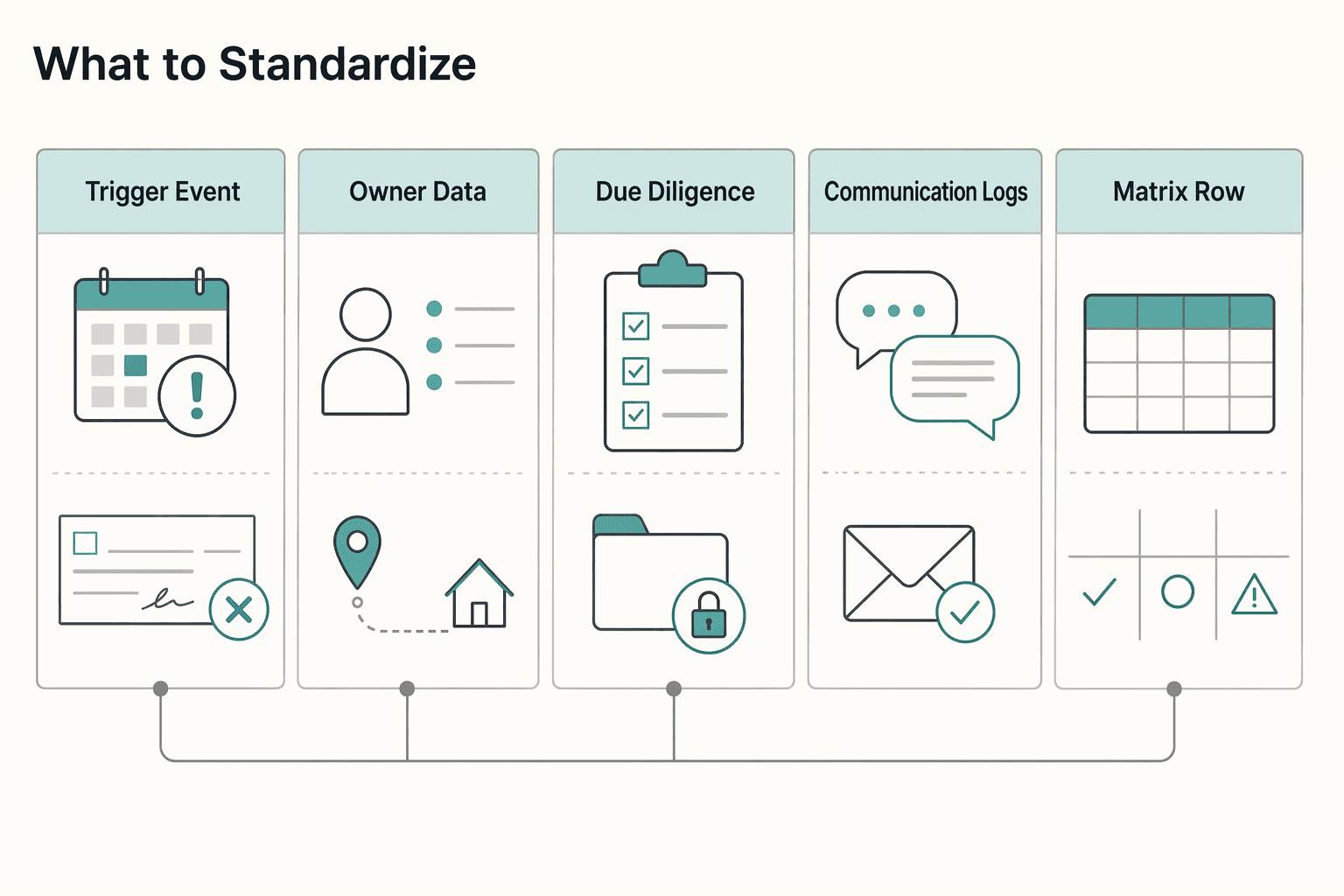

4) Standardize owner outreach before you reissue or remit#

Before you reissue funds or move a case toward remittance review, require one standardized outreach record. Otherwise, handlers can improvise contact steps on failed payouts or uncashed checks, and the case history gets harder to defend over time.

The control pattern is straightforward: organize the case, keep the electronic record coherent, and define when escalation is required by policy. That aligns with the checkpoint structure in 11.3.41.2.3 Inventory Management Requirements, 11.3.41.2.4.1 Electronic Inventory Case Organization, and 11.3.41.2.5 Guidelines for Improving Issues.

What to standardize#

For each failed payout or uncashed-check case, keep one outreach file that includes:

| Outreach file element | Required detail |

|---|---|

| Trigger event | the trigger event that opened the case |

| Owner data | the exact owner data used for contact |

| Due diligence letter | a copy of the due diligence letter, if your policy uses one |

| Communication logs | timestamped communication logs for each outreach attempt |

| Matrix row and next action | the current jurisdiction-matrix row and proposed next action |

If those items are not visible in one place, the case is not ready for reissue or remittance routing.

Where teams can fail. A common operational risk is fragmented evidence across systems and inboxes, which makes review and escalation decisions harder to defend. Another risk is skipping escalation when outreach reveals unclear ownership or contactability.

Set a clear elevation rule under 11.3.41.2.5 for those cases. If ownership and contactability are resolved, proceed on the defined next path. If not, keep the case open and escalate.

Need the full breakdown? Read How to Evaluate PCI DSS, SOC 2, and ISO 27001 for Payment Platforms.

5) Pick the right action path for each stale payment type#

Once outreach is complete, route each case through one of four paths: reissue, stop-payment order, unclaimed property review, or human override. Reissue only when reachability and entitlement are clear, use a stop-payment to control instrument risk, and move to remittance review only when the matrix supports it.

Reissue when the owner is reachable#

Reissue is appropriate when the payee can receive funds and the file shows no entitlement dispute. Before you send a replacement, confirm that the original liability is still open and that the case file includes the trigger event, current contact data, communication history, and any due diligence letter your policy requires.

A key operational risk is duplicate disbursement. If the original check could still clear, do not reissue until treasury has evidence that the first item is voided, blocked, or otherwise controlled.

Place a stop-payment order when the original item is still a bank risk#

Use a stop-payment order when an uncashed check may still be presented and may create bank exposure. Treat this as a bank-side control, not final legal disposition of the funds.

Keep the bank confirmation, check number, order date, and linked liability record in one file. Do not mark the case closed based on bank action alone. The next step still has to be decided as reissue, hold, or remittance review.

Route to unclaimed property only when the jurisdiction row supports it#

If the payee is not reachable and your matrix shows that the legal trigger is met, move to remittance review. Do not apply a single national rule. State unclaimed-property statutes are not identical, and even where core procedures overlap, some state processes differ.

Use the matrix row as the control point. The case file should document owner-state analysis, outreach timeline, and notice record before it moves forward.

Hold for human review when identity or entitlement is disputed#

If identity or entitlement is unclear, keep the liability open and escalate under 11.3.41.2.5 Guidelines for Improving Issues. This override path prevents forced automation in cases that do not fit cleanly into reissue or remittance logic.

A similar caution appears in the narrower ERISA context. The 2019 Advisory Council examined voluntary transfers of uncashed distribution checks, but its report was not official Department of Labor policy and did not set detailed locator-step standards. When facts are contested, preserve the file and require legal or compliance review before funds move.

For related context, see What Is a Payment Facilitator (PayFac)? And Should Your Platform Become One.

6) Tie payout controls to compliance gates, not just bank outcomes#

Once you have chosen the action path, do not let an operational outcome act as your only release signal.

Set a documented compliance gate with a clear last-acceptance date before final action. If your process includes a required public comment window, treat that timing as hard: keep comments open through the stated deadline, extend to the next workday if the date lands on a holiday, keep at least five days after the last required hearing, and do not adopt final action until the day after the window expires.

7) Design ledger-first controls so retries cannot duplicate liability#

After a payout clears the compliance gate, duplicate risk becomes the next control point. Your ledger journal should be the record that shows what liability is open, replaced, or closed.

That is an internal design choice, not a rule established in the source materials. The same is true for idempotency: useful for retries, but not standalone proof that duplicates cannot occur. Use retry keys as guardrails, then verify outcomes against ledger state.

Make one record the liability anchor#

Keep the obligation record separate from payment-rail outcomes. A provider can report failed or accepted outcomes, and your internal process may classify cases as stale, but those signals should not open or close liability by themselves when your internal books show otherwise.

The support here is structural, not jurisdictional. IRS IRM 11.3.41 separates work into Inventory Management System, Electronic Inventory Case Organization, and Guidelines for Improving Issues. It does not govern platform payout liability, but it can support the control pattern of one inventory, organized case records, and explicit escalation for exceptions.

Use a status model that preserves evidence#

These labels are not mandated by the source materials. They are an internal model for keeping a single liability trail from issuance through final disposition.

| Step | Internal status fields to keep | Ledger evidence to retain |

|---|---|---|

| issued | payout reference, beneficiary ID, amount, currency, issue date, rail, compliance gate result | original liability entry, linked to the payout attempt |

| failed | failure reason, failure timestamp, provider or bank response, retry hold flag | liability remains open, with no close entry based only on failure |

| stale | stale flag, stale-date basis, outreach state, action freeze, jurisdiction note if relevant | open liability remains, plus dated review evidence |

| reissued | replacement payout reference, approval record, link to prior attempt, payee verification state | linked adjustment chain showing replacement, not duplication |

| remitted | remittance date, jurisdiction, filing/reference number, owner-contact record, close reason | closing entry tied to remittance support |

Keep status and date-bound exceptions in separate fields. The TX-RAMP table in the source pack uses distinct fields like Certification Status, Certification Expiration Date, and Provisional Certification Expiration Date. One provisional row shows 1/22/2026 while the standard certification expiration field is blank. The control takeaway is separation of meaning by field, not a legal analogy.

Follow a fixed order when stale status appears. The source pack does not prescribe a required stale-payment retry checklist, so treat this as internal operating discipline:

- Detect the exception signal. Record the trigger and match it to the original payout reference before acting.

- Freeze conflicting actions. Pause automated retries, reissues, and closure steps while the case is reviewed.

- Verify ledger state. Confirm whether one open obligation exists, whether a replacement already exists, and whether any closeout was posted.

- Apply the approved action. Reissue, continue outreach, or move to remittance only after the compliance gate is satisfied, and link the action to the original obligation.

- Reconcile before closure. Match provider outcome, internal status, and ledger postings, then close the case.

Retain the action-time evidence pack: original issue record, stale review note, approval or escalation record, outreach history, any reissue reference, and final provider confirmation or remittance support. Related: International EFT Payments: How Platforms Can Send Electronic Funds Transfers Across Borders.

When you turn this checklist into workflow rules, map each stale-to-remit transition to one payout status and one ledger event so retries stay deterministic. Use Gruv Payouts as your implementation reference.

8) Set escalation triggers that compliance and legal can defend#

Once your ledger confirms an open obligation, treat escalation as a governance decision, not just an ops judgment call. Define trigger-based escalation with a named owner and a documented record so decisions can withstand supervisory, audit, and internal review.

This fits the OCC payment-systems framework. It is examiner-oriented, includes Compliance Risk, and points to governance artifacts such as Management and Board Reports and Internal Audit. Your trigger design should create a defensible review trail, not just move cases out of queue.

1. Outreach failure with unresolved ownership#

Escalate when outreach is complete but you still cannot confirm who is entitled to the funds. Silence alone is not the trigger. Unresolved ownership is.

Before you route the case, confirm that the outreach log is complete, time-stamped, and linked to the original obligation record. If the evidence is informal or incomplete, escalate rather than reissue or close.

2. Disputed ownership or conflicting payee instructions#

Escalate when multiple parties claim the same payment, beneficiary details change after issuance, or redirection is requested without clean support. At that point, the risk is no longer purely operational.

Package the case with the original payee record, change requests, supporting documentation, and the ledger link to the initial issue. Avoid parallel decision paths that allow action before ownership is resolved.

3. AML/KYC findings that block reissue beyond your policy window#

Escalate when screening, sanctions review, or unresolved KYC/KYB findings keep a reissue on hold past your internal window. The obligation may remain open even when compliance cannot clear disbursement.

Record the hold reason, hold start date, current screening state, and any document requests to the payee. If the case is frozen because ownership of the next decision is unclear, treat that as a control gap.

4. Jurisdiction ambiguity that changes the disposition path#

Escalate when the team cannot determine which jurisdiction governs next steps for the funds. The issue is whether the uncertainty could change the disposition path, not just that rules differ across places.

The OCC warns against one-size-fits-all application by emphasizing institution-specific risk and circumstances. Capture candidate jurisdictions, the basis for each, and the precise legal question to be answered. Do not assume state unclaimed-property dormancy, filing, or remittance rules from this framework; treat those legal specifics as jurisdiction-specific decisions for counsel.

Make the authority boundary explicit. Use one primary decider per trigger and one clear escalation destination. Publish these triggers with the required case fields and include them in management reporting so escalation becomes a controlled exception process.

| Trigger type | Primary decider | Required checkpoint |

|---|---|---|

| outreach failed, ownership unclear | legal | outreach log complete and liability still open |

| disputed ownership | legal with compliance input | beneficiary evidence and change history attached |

| AML/KYC block | compliance | screening hold reason and review start date recorded |

| jurisdiction ambiguity | legal | jurisdiction memo or case note attached |

9) Keep an audit evidence set ready before regulators or auditors ask#

Keep one exportable evidence packet per open escalated case so you can answer audit, board, or partner questions quickly and show how the decision was controlled. The main risk is retrofitting documentation after the fact, when key records are harder to reconstruct.

What the packet should contain#

- Policy snapshot

Keep the policy version that was in force when the decision was made, with the effective date or version ID tied to the case date.

- Case transaction evidence

Include records for the original obligation, any hold or reversal, and final disposition, linked to the case ID or payment reference where available.

- Communication record

Retain timestamped outreach logs and related correspondence so another reviewer can see who was contacted, when, and what response was received.

- Tax-document steps (if used in your process)

Keep receipt or status records for any tax-document handling that was part of payout review.

- FBAR support where applicable

For foreign account reporting cases, identify the filing as FinCEN Form 114 and keep the support file: maximum account value workpaper, statements used where they fairly reflect the yearly maximum, U.S.-dollar conversion basis, and filing status. FinCEN guidance says amounts are recorded in U.S. dollars and rounded up to the next whole dollar. For non-U.S.-currency accounts, use the Treasury rate for the last day of the calendar year, or another verifiable rate with its source if a Treasury rate is unavailable. FBAR filing is required when a single-account maximum or aggregate maximum exceeds $10,000 during the calendar year. The annual due date is April 15, with an automatic extension to October 15. If corrected, keep the prior report identifier because an amended filing is submitted as a new complete FBAR with the Amend box checked.

If you cannot export this packet in one pass within a day, your documentation process still depends too much on memory. This pairs well with our guide on How to Build a Finance Tech Stack for a Payment Platform: Accounts Payable, Billing, Treasury, and Reporting.

What to implement first in the next 30 days#

In the first 30 days, implement a minimum defensible control baseline. Publish how instrument status maps to payable status (validated with counsel), define operating states, build an institution-and-jurisdiction matrix with outreach steps, and lock in escalation plus retry controls before adding automation.

- Adopt one documented liability-boundary rule and publish the state definitions.

Document one clear rule for how payment-instrument status should be handled alongside the underlying payable, and confirm that rule with legal or compliance counsel. Then publish your operating states and transition owners so teams apply the same logic every time. Keep this as a formal control artifact, not an informal thread. As design context, the OCC Payment Systems booklet (Version 1.0, October 2021) explicitly organizes risk management into policies and procedures, internal controls, risk assessment, and management/board reporting.

- Build the jurisdiction matrix and outreach sequence before new tooling.

Document, per entity and jurisdiction, who reviews the item, what outreach your team will perform, and what evidence you require before reissue, hold, or remittance. Pair that with a simple outreach log: date, channel, response status, and stop-payment status. Do this manually first. If the matrix cannot resolve edge cases, automation will scale confusion. Avoid one-size-fits-all design, because risk profiles differ across institutions.

- Prioritize two controls with the highest downside if they fail.

Set explicit escalation triggers for disputed ownership, exhausted outreach, or unclear jurisdiction outcomes. Add ledger-level idempotent retry handling before any reissue path to reduce duplicate-processing risk from repeated provider events. Test against check-specific exceptions, not only generic payout failures. The OCC booklet includes supplemental procedures for "Checks and Other Monetary Instruments" (p. 78).

- Validate coverage with counsel, then map controls to your payout stack and owners.

Review the rule set, state definitions, matrix, and priority controls with legal or compliance counsel, then assign accountable owners across finance, operations, compliance, and engineering. Include a practical review packet: policy version, sample ledger entries, outreach evidence, and a control checklist. For audit-readiness discipline, use the OCC Internal Control Questionnaire (p. 83) and Appendix A 12 CFR 7.1026 Compliance Worksheet (p. 88) as structure models, and keep materials current. The booklet notes that reputation-risk references were removed as of March 20, 2025.

You might also find this useful: What Is a Balance Sheet? How Payment Platforms Account for Held Funds Reserves and Liabilities.

Once your 30-day plan is drafted, pressure-test market coverage, compliance gates, and ownership boundaries with your real operating model by talking with Gruv.

Frequently Asked Questions

What is a stale cheque in policy terms, and how is it different from a dormant obligation?

A stale cheque is generally a check older than 6 months, after which a bank may still pay it or decline it. In policy terms, that is an instrument-status issue, not a liability conclusion. A dormant obligation is the still-open amount you continue to track and manage, often across an active-management window such as 1 to 3 years.

Does a stale-dated check cancel the underlying debt, or do we still owe the funds?

No. Stale status does not extinguish the underlying obligation, and the funds remain owed until they are resolved through reissuance or escheatment. Treating “stale” as “closed” too early creates avoidable accounting and compliance risk.

When does an uncashed check become unclaimed property under state escheatment law?

Not at the 6-month stale point. The support here is that timing is state-dependent and is often described as roughly 3 to 5 years. Treat stale status and unclaimed-property status as separate timelines.

What must be documented before remitting funds through an escheatment process?

At minimum, document the payment details, the unresolved liability history, and all outreach attempts to the payee. Keep reconciliation evidence, and records showing funds stayed in the trust account while unresolved, so the item was actively monitored before remittance.

When should we reissue a payment versus place a stop-payment order?

The grounding here is limited: a bank may still honor a stale item when no stop-payment order exists. Use your internal policy and applicable state rules to decide reissue timing, and confirm the obligation is still unresolved before taking action.

How do idempotency and ledger journal controls reduce duplicate-payout risk during retries?

The grounding pack does not provide direct evidence on idempotency mechanics or ledger-journal controls. Treat these as internal control practices, and rely on consistent records and reconciliation checks to reduce duplicate-payout risk during retries.

Try a related tool

Fatima covers payments compliance in plain English—what teams need to document, how policy gates work, and how to reduce risk without slowing down operations.

Priya specializes in international contract law for independent contractors. She ensures that the legal advice provided is accurate, actionable, and up-to-date with current regulations.

Sources

- bsaefiling.fincen.gov/docs/XMLUserGuide_FinCENFBAR.pdftrusted

- claimittexas.gov/app/dormancytrusted

- consumerfinance.gov/ask-cfpb/the-bankcredit-union-refused-to-cas...trusted

- copyright.gov/policy/unclaimed-royalties/unclaimed-royalti...trusted

- dol.gov/sites/dolgov/files/ebsa/pdf_files/2019-permi...trusted

- dol.gov/sites/dolgov/files/EBSA/about-ebsa/about-us/...trusted

- dor.wa.gov/education/industry-guides/hospital-industry/...trusted

- dos.ny.gov/june-15-2022vol-xliv-issue-24trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Airline Delay Compensation Payments for Customer Experience and Control

If you are evaluating an `airline compensation payments customer experience delays platform`, split the work into three lanes first: legally owed refunds, discretionary compensation, and outsourced claims recovery. Vendor pages often blur these together, but they lead to different policy choices, ledger treatment, and customer outcomes.

How Platforms Choose International EFT Payments Across Borders

---

What Is a Balance Sheet? How Payment Platforms Account for Held Funds Reserves and Liabilities

If you own payouts, the core question is not what sits on the balance sheet. It is what obligation you can prove, what amount should stay held, and what can safely move. For finance, ops, and product teams dealing with balance sheet treatment for payment platforms - held funds, reserves, and liabilities - that distinction matters more than tidy labels. If your team cannot explain that distinction at release time, your close process is weaker than it looks.