Quick Answer

A platform tax compliance calendar should function as a control system that ties every IRS-facing task to a named owner, required data and documentation, approvals, evidence, and a due date. To reduce missed filings, run the year in fixed phases, keep intake, reporting, and support lanes separate, log exceptions and escalation triggers, and route post-issuance changes through a documented correction path.

Build the Calendar Backward from IRS Deadlines#

A useful platform tax compliance calendar is a control system, not just a list of dates. For each IRS-facing item, it should make four things explicit: what must be done, who owns it, what documentation is required, and when it is due.

Missed deadlines often come from coordination gaps, not a missing date alone. When ownership or dependencies are unclear, issues can stay hidden until the reporting window is already open.

The IRS's timeliness guidance supports that operating mindset. It points to Roles and Responsibilities, Critical Dates, and timing effects such as Holiday or Weekend Impact. In practice, your job is not only to track deadlines, but to confirm the work behind them is actually ready.

This article treats the calendar as shared control design for compliance, legal, finance, and risk teams managing payout flows. The focus is execution: clear ownership, dated checkpoints, retained evidence, and defined escalation when facts are unclear or obligations vary.

That discipline matters even more when you operate across entities or markets, where complexity rises fast. A centralized view helps only if each item still shows the owner, the dependency state, and proof that the task is on track.

This is operational guidance, not legal advice. Missing compliance deadlines can lead to penalties and reputational harm, and coordination gaps or missing evidence can also become costly when they surface late.

Define the calendar as a control system not a reminder system#

Treat your calendar as a control map, not a reminder list. For each Internal Revenue Service item, define the owner, required data or documentation, approval point, and retained evidence.

That structure matches IRS procedural logic. Processing timeliness guidance separates Roles and Responsibilities from Program Controls. A line that only says "file by X date" does not tell you whether the filing is actually ready.

Keep intake quality tied to reporting readiness. Tax documentation collection should feed downstream work, not sit in a separate admin queue. If records are incomplete or unresolved, the related filing item is not truly on track.

Treat missing ownership as a risk. If a task has no accountable owner, treat it as not on track until ownership is assigned. That is a control decision, not an IRS mandate, and it reduces hidden deadline and exception risk.

A practical calendar entry can include:

- deadline or period

- legal entity

- form or obligation type

- dependency state

- escalation trigger

- retained evidence location

Before marking anything complete, verify status integrity. The document should exist, the correct entity should be attached, approval should be logged, and evidence should be retrievable. Manual date tracking can still leave fragmented records, increasing the risk of fines, interest, and audit exposure. Tie calendar status to reconciled accounting data so filing readiness reflects actual readiness.

For multi-country operations, Build a Global Contractor Payment Compliance Calendar for Monthly, Quarterly, and Annual Obligations shows how to extend the same discipline beyond IRS dates.

Map the IRS obligations that matter for platform payout models#

Once ownership is clear, scope becomes the next control decision. Keep intake records, payer reporting outputs, and payee-facing context in separate lanes so a status does not look complete when only one lane moved.

For this section, treat Form W-8, Form W-9, Form 1099, Form 1099-NEC, Form 1099-MISC, and Schedule SE as mapping labels that still require rule verification from current IRS instructions. 1099, W-8, W-9, and Schedule SE deadlines, thresholds, and filing mechanics are not established here, so your calendar should show "verified" versus "pending tax review" instead of assumed rules.

| Item | Payer-facing place in the map | Payee-facing context | Verification status |

|---|---|---|---|

| Form W-8 | Intake dependency lane | Record-quality context for downstream handling | IRS mechanics not established here; verify before use as a filing rule |

| Form W-9 | Intake dependency lane | Record-quality context for downstream handling | IRS mechanics not established here; verify before use as a filing rule |

| Form 1099 | Reporting-output lane | Recipient document context | Payer obligations, thresholds, and deadlines not established here |

| Form 1099-NEC | Reporting-output lane | Recipient document context | Payer obligations, thresholds, and deadlines not established here |

| Form 1099-MISC | Reporting-output lane | Recipient document context | Payer obligations, thresholds, and deadlines not established here |

| Schedule SE | Support-routing context lane | Recipient tax-filing context | Filing rules and platform obligations not established here |

Add cross-border watch items without merging unlike obligations#

Cross-border items belong in the same map, but on a separate watch layer. FATCA is relevant because it is part of the IRS context around Form 8938.

The grounded checkpoints for Form 8938 are specific:

- Use Form 8938 to report specified foreign financial assets when the filer is above the applicable threshold.

- Attach Form 8938 to the annual return and file by that return's due date, including extensions.

- Form 1065 is explicitly listed in this filing context.

- If no income tax return is required for the year, Form 8938 is not required even if asset value is above threshold.

- For specified domestic entities, instructions cite more than $50,000 on the last day of the tax year or more than $75,000 at any time during the tax year.

- Higher thresholds can apply for joint filers or taxpayers residing abroad.

- Confirm each filer-category threshold with the relevant authority.

- Certain accounts are excluded, including an account maintained by a U.S. payer.

Track FBAR (FinCEN Form 114) in the same watch layer. Filing Form 8938 does not replace FBAR when FBAR is otherwise required.

Include IGA in the map only as "verify locally." Assign ownership and escalation rather than adding unstated rules.

Escalate classification disputes before filing#

Late classification disputes should go through a formal decision path, not a quick cleanup pass. Preserve the original classification, log who challenged it, and require tax or legal approval before you finalize outputs. Any late change that could affect form selection should move out of routine cleanup and into a documented filing-decision process.

Related: How to Expand Your Subscription Platform to Europe: Payment Methods Tax and Compliance.

Assign ownership and escalation across legal tax finance and ops#

This calendar is only reliable when each control step has a named decider, a named doer, and a clear escalation path. Define that ownership before payout release and before filing work starts.

The prior section separated intake, reporting outputs, and support context. This section makes those lanes ownable. Cross-functional handoffs can break down, so treat ownership clarity as a control, not as a formality.

Put one accountable owner on each step#

Use a compact RACI and keep it in the same tracker as form status, payout status, and exceptions. If a row has no accountable owner and fallback, it is not ready for green status.

| Activity | Compliance or Tax | Legal | Finance | Ops |

|---|---|---|---|---|

| Form W-8 and Form W-9 intake | A | C | I | R |

| Taxpayer data and form validation | A | C | I | R |

| Information return filing prep | A | I | R | C |

| Filing sign-off and release approval | R | A | C | I |

| Corrections and post-issuance disputes | A | R | C | C |

A = accountable, R = responsible, C = consulted, I = informed.

This is a failure-prevention control. Date tracking alone is not enough. Ownership, blocker status, and decision evidence need to live in one record.

Make risk gates visible before money moves#

If you already run separate compliance checks, show those statuses next to tax profile status before payout release. That is an internal control choice, not an IRS requirement.

Use a payout view that shows the current tax form on file, validation status, exception count, and latest compliance-check result for each payee or seller. If statuses conflict, keep the lane blocked until the named owner clears it or escalates it.

False-green states happen: one team sees onboarded, another sees funded, while an unresolved Form W-8 or Form W-9 issue is still open.

Set cutoffs and freeze rules before filing season#

Set a hard internal cutoff for unresolved taxpayer-data exceptions so decisions do not drift into filing week. That reduces avoidable cost, time, and operational burden from late exceptions.

One internal rule is simple: if a W-form mismatch, taxpayer name conflict, or similar issue is unresolved by cutoff, consider freezing the affected payout lane and routing it to tax counsel or legal for a decision. Apply that rule consistently so one team is not editing records while another prepares reporting outputs.

For each escalation, keep an audit-ready evidence log with the submitted form, conflicting values, validation notes, reviewer, cutoff-breach date, payout-hold decision, and final approval.

If ownership is unclear, stop the lane, name the decider, and document the exception before money or forms go out.

If your escalation policy includes payout freezes, align those triggers with compliance-gated status tracking and audit trails in Gruv Payouts.

Run the year in fixed phases with dated checkpoints#

Run the year in fixed phases, not as a loose deadline list. Each phase should close only when its evidence is complete. If unresolved exceptions exceed your internal tolerance, shift from filing execution to incident mode with a defined leadership review cadence.

| Phase | When to run it | Minimum artifacts before moving on | Decision checkpoint |

|---|---|---|---|

| Setup | Start of cycle and after prior-year close | Entity scope, owner list, prior-year issue carryforward, phase dates, approver sign-off on calendar | Confirm in-scope entities, payout products, and reporting populations |

| Intake hardening | Ongoing, with recurring checkpoints before year end | Validated tax-profile data set, open exception log, validation notes, payout-hold decisions where needed | If validation backlog grows, route new exceptions into named queues and escalate unresolved identity or tax-profile conflicts |

| Pre-filing review | Before draft generation becomes final work | Draft variance report, exception log with aging, unresolved edge-case record, approver sign-off to enter filing window | If exception volume or severity exceeds tolerance, declare incident mode instead of pushing ahead |

| Filing window | During final prep, submission, and recipient delivery | Final approved output set, filing-readiness checklist, distribution evidence, submission approvals | Release only files that match approved scope and locked source data |

| Correction window | Immediately after issuance and filing | Correction case log, cause category, changed taxpayer data or payment record, approver sign-off per correction | Separate true corrections from support questions to avoid reopening stable populations |

| Retention | After filings and corrections stabilize | Archived evidence pack, approval history, exception history, copies of reports and correction records | Verify archive completeness before access or staffing changes break traceability |

The pre-filing control that usually catches real risk is the draft variance report. Keep it plain: payee-count shifts, payout-total shifts, entity-mix shifts, exception-count shifts, and records that moved into or out of reportable populations since the last lock.

Use the same checkpoint to test Form 1099-K logic before deadline pressure builds. IRS guidance says payment card companies, payment apps, and online marketplaces are required to file Form 1099-K and send recipient copies by January 31. It also says direct card payments do not depend on payment count or amount, and payment apps or online marketplaces may still issue Form 1099-K below the stated over $20,000 and more than 200 transactions condition. If your rule set assumes a single threshold path, treat that as a readiness gap.

When you cross your internal unresolved-exception tolerance, change operating mode immediately. In incident mode, review on a set cadence: open exception count, blocker age, records tied to recipient deadlines, and whether source data is still changing. Repeated draft regeneration without a signed treatment decision for the same exception class is a stop signal.

Add FinCEN timing as a linked support lane so deadline-week issues do not get improvised. For affected persons, FBAR is FinCEN Form 114 filed through BSA E-Filing. For threshold routing, use maximum account value: if a single-account maximum or aggregate maximum exceeds $10,000 at any time during the year, an FBAR must be filed; if not, FBAR is not required. The annual due date is April 15th, with an automatic extension to October 15th. FinCEN can also post relief notices that change timing for affected filers, so include notice monitoring as a checkpoint. If post-filing errors are found, route them for amendment handling and capture the Prior Report BSA Identifier needed for an amended FBAR.

Harden onboarding and payout intake before money moves#

Before payouts, treat tax intake as an internal control gate. A received form is not the same as a validated tax profile. If you gate unrestricted payouts on unresolved tax-profile or identity issues, frame that as your internal policy choice, not as a rule stated in the IRS Form 8938 materials.

A practical baseline is to keep "document received" and "profile validated" as separate states, with a named exception path and owner when records do not clear review.

Validate the profile, not just the form#

Your intake check should confirm more than file upload. Keep the profile structured enough to support later tax decisions and audits:

| Profile area | Fields to keep |

|---|---|

| Form record | form type, receipt date, review date, and reviewer |

| Taxpayer details | legal name, tax identifier status, country, and entity type |

| Payer mapping | payer legal entity and payout product tied to the profile |

| Cross-border review | jurisdiction flags for cross-border review |

| Decision trail | decision status, exception reason, and any payout restriction applied |

Keep those fields structured rather than scattered across attachments or free-text notes.

For cross-border cases, keep the flag traceable. IRS FATCA technical guidance describes IDES as the system used to exchange taxpayer information with foreign tax authorities, and structured records are generally easier to review later than free-text-only notes.

Form 8938 is a useful routing check, not a substitute for intake design. Filing starts only if the filer is a specified person, including certain specified domestic entities, and published triggers include aggregate value thresholds such as over $50,000 for some taxpayers and $50,000 year-end or $75,000 anytime for certain specified domestic entities; higher thresholds can apply for other groups. If no income tax return is required for the year, Form 8938 is not required.

Protect sensitive data without losing traceability#

As an internal security practice, mask and encrypt sensitive fields in normal operations, but preserve a clear audit trail. The goal is to limit access for day-to-day teams while still showing what was reviewed, approved, changed, and when payout status changed.

A clean archive should answer, without querying live systems:

- which record version was approved

- which payer entity it applied to

- which tax year it covered

- who approved it

If Form 8938 becomes relevant, it must be attached to the annual return and filed by that return's due date, including extensions, and it must state the applicable calendar or tax year. Keep FBAR review separate as well. Filing Form 8938 does not remove potential FinCEN Form 114 obligations.

Split intake by legal payer entity#

If your model includes a Merchant of Record entity, keep payer-entity mapping explicit from onboarding onward as an internal reporting control. Do not let one approved profile flow across multiple payer populations without a recorded decision and owner.

That separation can keep reporting populations clearer at year end and reduce avoidable scope disputes during filing and correction work.

For a step-by-step walkthrough, see Brazil Platform Operator Tax Controls for CIDE, ISS, and CBS/IBS Transition.

Control monthly and quarterly close so filing season is boring#

Make monthly and quarterly close your early warning system for reporting risk, not just an accounting routine. If a close miss can change what you report to the IRS, treat it as a compliance issue and resolve it with clear ownership.

| Close check | What to verify |

|---|---|

| Expected Form 1099-Ks | from payment card companies, payment apps, and online marketplaces |

| Forms received | including whether recipient copies arrive by January 31 |

| Amount matching | Form 1099-K amounts matched with the other records you use to figure and report taxable income |

| Platform aggregation | payments accepted on different platforms are aggregated |

| Same-year reconciliation | multiple Form 1099-Ks for the same tax year are reconciled |

| Threshold monitoring | threshold-based monitoring is not your only control |

Reconcile the same Form 1099-K population each period so issues surface before filing season. If you run monthly closes and quarterly year-to-date reviews, keep the same scope each time so variances are comparable and explainable.

Before sign-off, check completeness as well as totals.

For Form 1099-K exposure, do not wait until year end. Form 1099-K reports payments received for goods or services. Direct card payments can generate Form 1099-K regardless of count or amount, and payment apps or marketplaces may still issue forms below the stated threshold.

Track unresolved exceptions as open risk, with a named owner and due date. That dashboard design is an internal control choice, but it makes filing season more predictable and easier to defend.

If foreign payees are part of the workflow, FATCA and W-8 Tax Compliance for Platforms: When to Release, Hold, or Withhold Foreign Payouts covers the hold, release, and withholding decisions that sit behind the calendar.

Execute filing season with explicit correction paths#

Filing season should run as a controlled issuance process. Finalize what is still in draft, and treat any post-issuance edit as a tracked correction instead of a quiet overwrite.

| Control record | Included detail |

|---|---|

| Generation snapshot | exact data snapshot used to generate each form |

| Variance review | draft variance summary |

| Recipient data | recipient data snapshot used for generation |

| Approval record | approver and approval date |

| Distribution record | distribution version and timestamp |

| Held or excluded records | exceptions list for held or excluded records |

| Correction case | why the case exists, who approved the next action, and the expected resolution date |

For Form 1099-NEC and Form 1099-MISC, a clear internal sequence can help: draft generation, internal review, issuer approval, distribution, then correction handling. That sequence is an internal control choice, not an IRS-mandated five-step method, but it creates a clean boundary between "under review" and "already issued."

Before approval, lock the exact data snapshot used to generate each form and retain the evidence listed above.

Define correction triggers in advance. If recipient or reportable data changes after issuance, open a correction case rather than editing records silently. Consider capturing why the case exists, who approved the next action, and the expected resolution date. Those fields are internal control choices here, but they create a usable audit trail.

Set a final review cutoff for structural changes so late edits cannot bypass governance. After cutoff, route high-impact changes through designated approvers (for example, tax or legal) and document the decision: issue and correct afterward, or hold the affected records pending approval.

This discipline matters because policy discussions have called for earlier third-party data access before filing deadlines and faster matching before refunds. The same materials also note uncertainty about which IRS compliance actions follow detected mismatches, so unresolved discrepancies should be escalated, not patched informally.

Support teams also need visible correction status. Recipients may receive more than one Form 1099-K across platforms, which can create confusion when records are out of sync.

Handle cross-border overlap without overextending the IRS calendar#

Keep the IRS calendar narrow and authoritative. Run IRS filing controls there, and track cross-border regimes as linked items with clear owners so the calendar does not imply false completeness.

| Item | Keep in the IRS calendar | What to record |

|---|---|---|

| Core IRS return filing tasks | Yes | Deadline, legal entity, approver, evidence pack, correction path |

| Form 8938 context | Linked IRS-adjacent item | Applicability decision owner, taxpayer context used, link to return filing owner |

| FBAR (FinCEN Form 114) | Linked external tracker | Separate owner, separate tracker, escalation contact |

| FATCA and IGA flags | Adjacent watch item only | Verify locally, owner, status, linked analysis |

| DAC7 and VAT | External country tracker | Jurisdiction, local owner, applicability review status |

The key boundary is Form 8938 versus FBAR. Form 8938 is attached to the annual income tax return and filed by that return's due date, including extensions. FBAR is a separate obligation, and filing Form 8938 does not remove any FinCEN Form 114 requirement.

For Form 8938, do not hardcode a single threshold into your calendar. IRS materials show that thresholds vary by taxpayer context, including joint filers and taxpayers residing abroad, include example triggers such as aggregate value exceeding $50,000 for some taxpayers, and include exclusions such as some financial accounts maintained by a U.S. payer. The control point is to record who verified applicability, what taxpayer context they used, and whether an income tax return is required, because if no return is required for the year, Form 8938 is not required.

For DAC7, VAT, FATCA, and IGA-dependent rules, keep the status at verify locally until a named owner confirms applicability. If a rule is country-program specific and unconfirmed, it should not appear as complete.

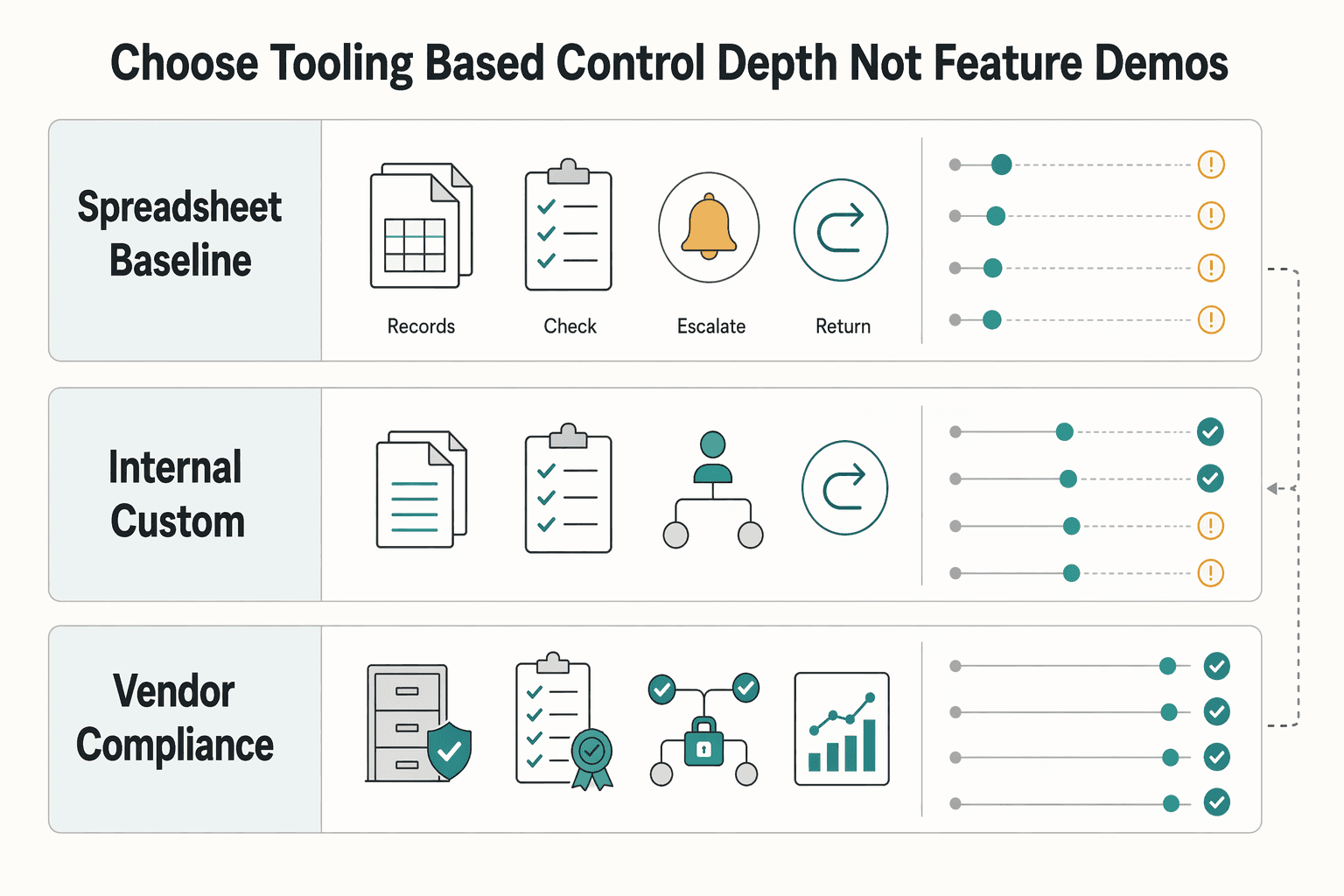

Choose tooling based on control depth not feature demos#

Choose the option that can prove control outcomes in your actual workflow, not the one with the best demo. If entity count and jurisdiction variance are low, a lightweight setup can be enough. If corrections, handoffs, and approvals are frequent, move to controls that enforce the process and preserve evidence.

| Option | Best fit | Control depth to test for | Main risk |

|---|---|---|---|

| Spreadsheet baseline | One or a few entities, limited filing types, low correction volume | Named owner, due date, dependency status, link to evidence, manual sign-off fields | Drift into email threads, weak versioning, and incomplete correction history |

| Internal custom stack | You need tailored integrations and can support implementation effort internally | Configurable dependencies, automated escalations, stored approval logs, queryable evidence records, exception views | Overbuilding before process rules are stable, or creating a filing-season bottleneck |

| Vendor compliance suite | You want a centralized compliance platform without building everything from scratch | Demonstrable evidence retention, approval routing, exception handling, and reporting on demand | Buying on demo flow without proving escalation and correction cases |

The real comparison is not spreadsheet versus software in the abstract. It is whether the tool helps you track obligations, manage evidence, and demonstrate compliance on demand.

Judge the tool by the control outcome#

Start with audit traceability. You should be able to answer, without reconstruction: who changed the task, when it changed, what was approved, what evidence was attached, and what happened after a correction request. If that history is unclear, it is a reporting surface, not a control surface.

Then test dependency logic. Tasks should not close while prerequisites remain open, such as missing sign-off or an unresolved correction case. A polished dashboard that turns items green without dependency proof is a red flag.

Approval and exception workflows are the practical separator. Confirm that late changes trigger a distinct correction path, exceptions age visibly, and escalation moves beyond passive notes. Also weigh implementation effort and ease of use alongside features, because a poor tool decision can become a filing-season bottleneck.

Use a simple selection rule#

Use a lightweight option when all three are true:

- low entity count

- low jurisdiction variance

- low correction and handoff volume

Prioritize workflow-enforced controls when these rise: frequent data changes, multiple approvers, cross-team ownership, or recurring exceptions.

What to require in a live proof#

Before adoption, require a live test using one of your real failure cases. Ask the team to show a blocked task, route it to the correct approver, miss a due date, trigger escalation, and preserve the evidence trail after resolution.

If they cannot show timestamps, approval identity, attached records, and correction history in one place, keep looking. Do not buy on dashboard quality alone. Buy when escalation paths and evidence retention work under real operating conditions.

Keep an evidence pack ready for audits and leadership#

You should be able to prove control performance quickly, so keep a standing evidence pack for each IRS reporting period instead of rebuilding one after questions arrive.

Keep five items current in one place: control matrix, owner list, exception register, approval logs, and filing history. This structure is an operating choice, not an IRS-required format, but it makes it easier to show what the control was, who owned it, what changed, and how issues were resolved.

What to verify every cycle#

Anchor at least one checkpoint to a fixed IRS date. For Form 1099-K populations, payment card companies, payment apps, and online marketplaces file annually and must send recipients a copy by January 31. Your evidence should show how the population was identified, who approved the filing set, and how late changes were documented.

Include a small end-to-end sample record. It can start with intake data, show validation or exception handling, and end at the Form 1099-K reporting output. Where Form 1099-K is in scope, keep related transaction records with it, since Form 1099-K is used with other records to report taxable income.

What usually fails#

The common breakdown is loss of traceability when data is messy or workloads spike. Rule-only setups get brittle under that pressure, so pair automated assistance with human review and immutable logging, and preserve approval timestamps and change notes.

Add a one-page risk brief each cycle with open issues, mitigations, filed versus held items, and decisions deferred to counsel. This helps leadership review status quickly.

Related reading: Gruv Platform Payments for Global B2B Payouts and Compliance.

Conclusion#

The core pattern is straightforward: a common risk is ownership gaps, weak intake, and missing evidence, not the date itself. A credible calendar works as a control record that ties each obligation to a named owner, prerequisite data, required documentation, and a clear approval point.

That structure matters because tax compliance is operationally complex, not routine admin. The IRS Taxpayer Advocate describes return preparation and filing as too difficult, costly, and time-consuming, and points to a Code with 9,834 sections plus a six-volume set of regulations. In practice, that complexity can create confusion and errors unless your calendar surfaces exceptions early and assigns ownership.

A practical way to reduce surprises is phased execution, not a full redesign. Tighten intake controls first, add recurring reconciliation checkpoints next, and then document filing and correction decision rules. Before any filing cycle moves to final review, confirm that the reporting dataset is complete and the accounting data is reconciled and finalized.

If you need a minimum enforceable model, build these three pieces first:

- a single owner list with fallback owners for intake, validation, filing prep, sign-off, and corrections

- a standing evidence pack with the control matrix, exception register, approval logs, and filing or correction history

- written decision rules for what happens when data is late, conflicting, or changed after issuance

That is enough to expose a common failure mode: a task appears covered on a shared deadline sheet, but no one owns data quality or approval to proceed. Without a structured calendar, teams struggle to track responsibilities effectively.

Add tooling only after the control works in plain language. If a spreadsheet plus disciplined review gives you traceable ownership, documented evidence, and reliable exception handling, use it. Add systems only when they clearly improve control quality and audit traceability. Keep adjacent regimes linked but clearly labeled, and verify current scope from the governing source before relying on older trackers, especially where guidance may not be fully updated.

When you are ready to implement this calendar as enforceable controls, use the integration and operations guides in Gruv Docs.

Frequently Asked Questions

What is a platform tax compliance calendar and how is it different from a normal deadline tracker?

It is a control record that ties each deadline to required data, decision points, approvals, and retained evidence. A normal tracker shows dates. A compliance calendar also shows ownership, dependencies, and how the filing can be defended.

Which IRS deadlines matter most for platforms paying contractors, sellers, and creators?

The deadlines that matter most are the ones tied to the forms and reporting outputs actually in scope for your payout model. This article does not provide a complete schedule for Forms 1099, 1099-NEC, or 1099-MISC, so use current IRS instructions for exact dates and set internal cutoffs before them.

Who should own each deadline across legal, tax, finance, and operations?

No single ownership model is required here. What matters is a named decider, a named doer, documented handoffs, and a named final approver for each filing cycle so exceptions do not stall.

What controls reduce missed filings and penalty exposure in practice?

Use recurring checks that surface incomplete or conflicting reporting data early, with documented approvals, exception handling, and retained evidence. For some international information reporting obligations, missed requirements can trigger significant penalties and can extend the IRS time to assess related tax, so unresolved exceptions should be escalated.

When should we pause payouts because of W-8 or W-9 issues?

Pause payouts when your documented internal policy says unresolved documentation or identity issues require a hold. This article does not set the hold rules, so tax and legal should define the trigger, the owner, and the evidence needed to release the lane.

How should we handle late data changes after Form 1099 issuance?

Treat late changes as tracked correction cases, not silent record edits. Keep approvals and traceable change history, and confirm form-specific correction requirements in current IRS instructions.

Where do FATCA, DAC7, VAT, FBAR, and Form 8938 fit relative to the IRS calendar?

Form 8938 belongs on the IRS-facing calendar because it is attached to the annual return and due with that return, including extensions. If no income tax return is required for the year, Form 8938 is not required. FBAR should stay in a separate tracker because filing Form 8938 does not remove any FinCEN Form 114 requirement. FATCA, DAC7, VAT, and IGA-dependent rules should be tracked as separate jurisdiction-specific items or marked verify locally until applicability is confirmed.

Try a related tool

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

- fincen.gov/system/files/shared/FBAR%20Line%20Item%20Fil...trusted

- fincen.gov/reporting-maximum-account-valuetrusted

- irs.gov/businesses/international-businesses/foreign-...trusted

- irs.gov/businesses/understanding-your-form-1099-ktrusted

- taxpayeradvocate.irs.gov/wp-content/uploads/2020/11/Fundamental-Chang...trusted

- taxpayeradvocate.irs.gov/wp-content/uploads/2023/01/ARC22_MSP_02_Comp...trusted

Educational content only. Not legal, tax, or financial advice.

Related Posts

Gig Worker Tax Compliance at Scale: How Platforms Handle 1099s W-8s and DAC7 for 50000+ Contractors

At scale, the hard part is not the acronyms. It is deciding sequence, ownership, and evidence when Form 1099-K, Form 1099-NEC, Form W-8BEN/W-8BEN-E, and DAC7 do not line up cleanly. If you run a high-volume marketplace, put controls in the right order and define clear stop points where legal or tax takes over.

How to Expand Your Subscription Platform to Europe for Payment and VAT Readiness

Treat a European launch as an operations sequencing decision first. Lock VAT, payments, and compliance ownership before you scale localization or acquisition.

Music Royalty Tax Compliance: How Platforms Handle 1099-MISC vs. 1099-NEC for Artist Payments

This is an operating-model decision, not a year-end form choice. A team can ship quickly and still end up with misclassified payouts, correction cycles, and filing risk if the classification logic is weak. If you run creator payouts, you need the classification rule before your first batch, not after your first correction cycle.