Quick Answer

A payment gateway is the secure front end of online payment processing. It captures payment details at checkout, encrypts and routes the data, and returns an authorization result, while the processor handles fund movement. For service businesses, the main implementation choice is hosted checkout for faster setup and lower direct security burden or API integration for more control and more responsibility.

A payment gateway is the secure front end of online payment processing#

A payment gateway is the secure front end of online payment processing. One of the first practical decisions is hosted checkout or API integration. That choice affects how payment data is captured and transmitted, how much control you keep over the product experience, and how much security responsibility your team takes on.

This guide is for teams that have to live with that decision after launch. A gateway sits between your customer, your business, banks, and processors, so implementation choices can affect more than checkout alone.

| Approach | What it means | Main upside | Main tradeoff |

|---|---|---|---|

| Hosted checkout | Customer is redirected to a provider-hosted payment page | Faster implementation and lower merchant security-compliance burden | Less control over the on-site payment experience |

| Integrated (API-based) | Payment flow stays on your site or app | More control and a smoother on-site experience | More stringent security measures and greater security responsibility |

Checkout friction is not theoretical. In the cited Stripe survey context, 18% of abandoned carts were tied to checkout that felt too long or complicated. That does not prove one architecture will always improve conversion, but it does show how checkout UX friction can affect revenue. By the end, you should have clear answers to three questions:

- Should you start hosted for speed and compliance simplicity, or invest early in API integration for tighter control?

- Which costs matter beyond headline transaction pricing, including setup fees, monthly fees, and transaction fees?

- What must be verified before go-live so ownership and controls are clear?

Treat provider claims as inputs to verify, not assumptions. Confirm the checkout model, what part of the flow is hosted, what data touches your systems, and the full fee structure in writing. Verify compliance expectations before you commit.

Related: A Canadian Freelancer's Guide to Setting Up a US Stripe Account.

Payment gateway means and what it does not do#

A payment gateway is the front end of online payment processing. It captures payment details at checkout, encrypts and routes that data, and triggers transaction authorization. It is not the component that moves funds into your bank account.

The payment processor plays a different role. The processor executes the transfer of funds with banking partners, while the gateway handles payment data and the authorization flow. In operations, treat status labels carefully:

- Authorized means the transaction was approved to proceed, often in real time.

- Authorization does not mean funds have already completed movement.

If approval is denied, the transaction is paused and the customer is notified immediately. That is an authorization outcome, not a funds-movement outcome.

When you evaluate providers, get the flow in writing: where payment data is entered, what part of checkout is hosted, and whether your app touches card details. Those answers can affect PCI-DSS scope and who handles card-data security.

This pairs well with our guide on Bulk Payment Processing Platforms for Thousands of Payouts.

How online payment processing moves from checkout to settlement#

Treat authorized and finalized funds as separate states from day one. If your systems collapse both into one "paid" label, reconciliation and support decisions become less reliable.

A common card flow starts when a customer enters card details at online checkout and submits payment. The gateway securely transmits encrypted payment data and sends an authorization request. The gateway then returns an approval or decline to your checkout flow. In this model, a processor alone is not the secure authorization layer.

The flow you should model#

Payment processing is a lifecycle, not a single event. It includes authorization, clearing, and settlement. The checkout result is an authorization outcome, not confirmation that funds have fully moved.

| Stage | What is happening | What your team should record |

|---|---|---|

| Checkout submitted | Customer enters card details and confirms payment | Internal payment ID, checkout/session ID, timestamp |

| Authorization | Gateway sends the approval request; checks can include billing address and CVV | Auth outcome, decline reason if present, gateway/provider reference |

| Post-approval handling | Payment moves onward through clearing and settlement based on provider flow | Clearing/settlement status if exposed, amount, currency, linked order or invoice |

| Settlement complete | Funds movement completes on provider timing | Final status, provider reference, reconciliation marker |

A payment can be approved at checkout and still sit outside "cash received" reporting until later phases complete. Reconcile against provider fund-movement data, not raw authorization success counts.

What to verify in the authorization step#

Do not stop at pass or fail. Confirm what evidence came back with the decision. In card flows, authorization can include checks such as billing address and CVV. Verify whether your provider returns those signals and where they appear in logs, admin views, or exports.

Declines are a normal outcome, including cases tied to available funds or other factors. When a decline happens, make sure the customer message, support view, and payment record all map to the same event.

Build one source of truth for every payment event#

Your payment record needs full status history, not just the latest state. At minimum, store status transitions, provider references, and an audit trail for each state-changing event.

| Record area | Include |

|---|---|

| Identifiers | Internal payment ID and linked order or invoice ID |

| Status history | Current status and prior status transitions with timestamps |

| Provider references | Provider event or reference IDs from authorization and later stages |

| Audit trail | Audit trail entries showing who or what changed payment state |

If finance or support cannot answer "what happened, when, and according to which provider event?" from one record, the model is too thin. This record becomes the backbone for reconciliation, disputes, and incident review.

You might also find this useful: Shopify Payouts Explained for Sellers Choosing Alternatives.

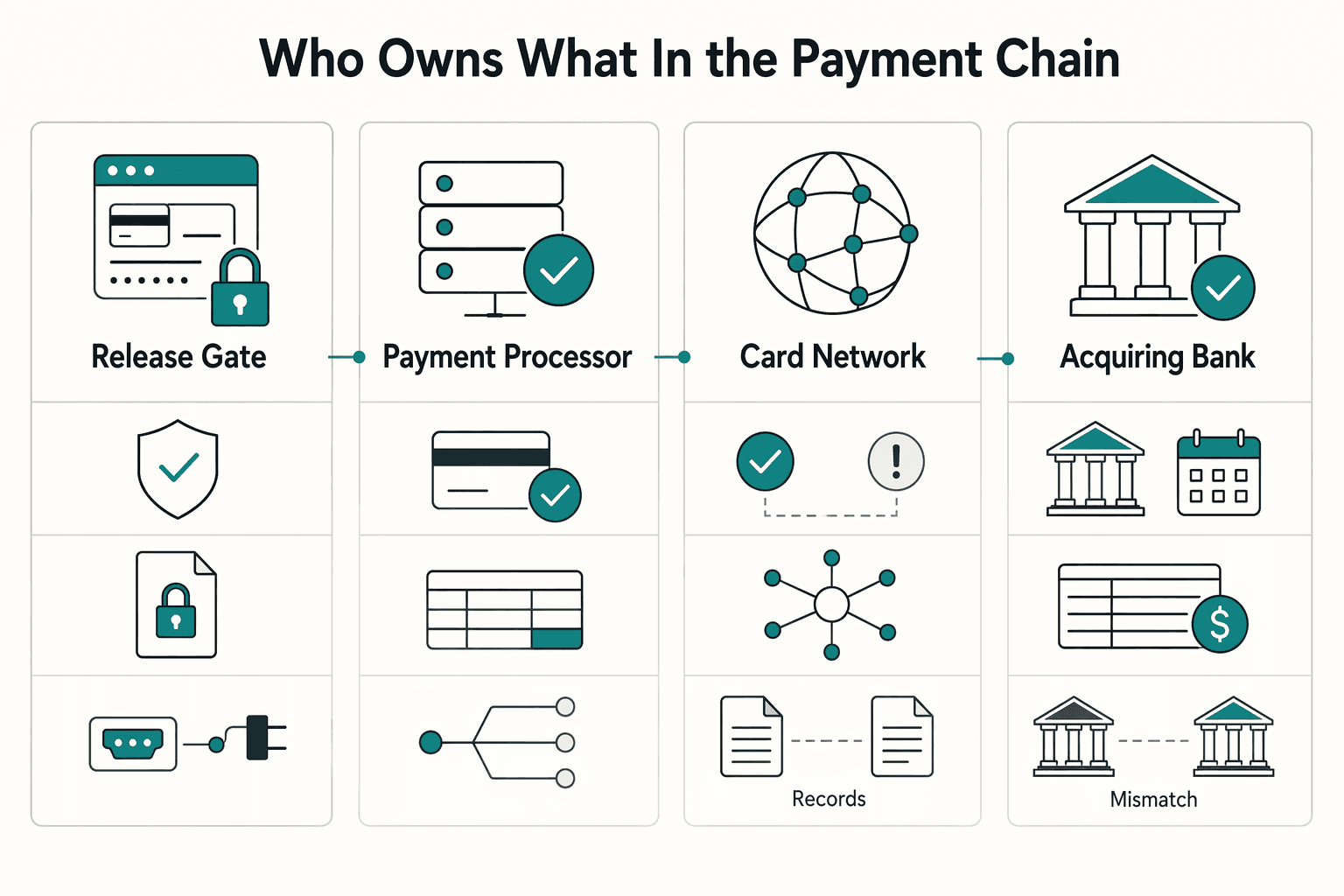

Who owns what in the payment chain#

No single party typically owns the full payment path, even when one provider sells it as a single product. In practice, the gateway handles secure payment data and passes authorization requests. The processor handles charging the card. The card network receives the authorization request for approval, and the acquiring bank receives the funds after settlement.

Some providers bundle gateway and processor functions, but separating responsibilities still helps during incident triage. When something breaks, you need to identify whether the failure sits in data capture, charging flow, network authorization, or final fund movement to the acquiring bank.

| External party | Core responsibility | Internal owner to name | Failure symptom | Evidence to pull first |

|---|---|---|---|---|

| Payment gateway | Securely captures checkout payment data and passes authorization requests onward | Define internally | Checkout state is unclear or inconsistent with customer report | Gateway transaction record for reconciliation |

| Payment processor | Charges the card in the transaction flow | Define internally | Approval or decline outcomes are unclear across systems | Authorization outcome and processor/provider transaction reference |

| Card network (scheme) | Receives authorization requests for approval | Define internally | Authorization outcomes are inconsistent or unclear | Network-related response data returned by provider |

| Acquiring bank | Receives settled funds for the merchant | Define internally | Payment was approved earlier but cash is not yet reflected in finance views | Reconciliation record tied to settlement/deposit reporting |

What to confirm before incidents force the answer#

Set named internal owners for each failure point and required evidence, then test that handoff before you need it. At minimum, confirm you can trace one payment from checkout through authorization and into final fund-movement records.

Keep authorization and cash movement separate in your operating language. Approval holds funds but does not move them. The later funds step runs separately, usually once per business day, and funds can reach the acquiring bank in one to three business days.

If you want a deeper dive, read The best alternatives to Stripe for international businesses.

Hosted checkout or API integration#

Choose based on ownership. Start with hosted checkout when speed and limited team capacity matter most. Choose API integration when payment experience is core to your product logic and you can take on more engineering and compliance work.

Operationally, the key question stays the same: when payment flow breaks, does your provider own most of the experience, or does your team?

When hosted checkout is the better call#

Hosted checkout redirects customers to a provider-hosted payment page. It is generally faster to implement, often requires minimal coding, and reduces your direct payment-data handling burden.

This is usually the better starting point when launch speed is the constraint. One grounded example suggests teams under 1,000 transactions per month may accept higher per-transaction pricing for easier setup, but that is a planning reference, not a universal threshold. The tradeoff is lower control. With a provider-hosted page, branding flexibility is usually more limited.

When API integration is worth the extra burden#

API integration keeps payment on your site or app, which gives you more control over UX and branding. It can be a stronger fit when payment flows need a tighter connection to your product behavior.

The cost is higher implementation complexity and more security and compliance responsibility. Checkout quality and security execution are directly tied to conversion and risk. Some sources also frame API integration as potentially lowering fees at scale, but that depends on your volume and operating maturity.

| Dimension | Hosted checkout | API integration |

|---|---|---|

| Launch speed | Often fastest; can be hours or days | Slower due to build and testing |

| UX and branding control | Lower | Higher |

| Security/compliance burden | Lower direct handling burden | Higher technical/compliance responsibility |

| Ops ownership | Simpler early, less edge-case control | More control, more team responsibility |

A practical decision rule#

Start hosted if your priority is accepting payments quickly with limited technical resources. Prioritize API integration if you need tighter control over checkout UX and on-site payment flow.

What to lock before go-live#

Before launch, set explicit acceptance criteria so teams agree on what must work on day one, including:

- Launch monitoring for checkout and payment success

- Timeout handling with a clear customer state and internal triage path

- Clear ownership for security and compliance issues

Then run test payments and confirm you can track each transaction from checkout attempt to final status.

Before you lock architecture, map your flow against the Gruv docs so product, engineering, and finance are signing off on the same flow.

Security and compliance controls that actually matter#

After you decide who owns checkout, lock down who owns payment risk. The practical standard is simple: minimize where card data can appear, assign clear owners for incident response, and verify controls with real evidence.

Draw the PCI boundary early#

Start with system boundaries, not a yes or no PCI question. Map where cardholder data could enter or appear across your transaction flow and connected systems.

Hosted checkout, API integrations, and tokenization services can all remain in cardholder-data scope, so the integration choice is also a compliance choice. If you go deeper on API control, review what your implementation captures across customer-facing flows and operational tooling.

Tokenization helps, but it is not a blanket exemption. A stronger setup keeps private card numbers out of day-to-day systems so teams work from tokens or masked references instead.

Focus controls on predictable incident paths#

Build controls around known payment-chain risk areas, including breach and incident response. The key is clear ownership before incidents happen. Set named owners for monitoring, alert routing, and investigation workflows. If ownership is vague, response quality drops and reconstruction gets harder.

As a practical checkpoint, confirm you can retrieve the records needed for a payment investigation and maintain a usable audit trail.

Treat gateway model choice as a compliance tradeoff#

Hosted, self-hosted, and API-based gateways offer different tradeoffs between speed, control, compliance burden, and customization. Plan against the exact model and product variant you will deploy, not generic assumptions.

Ask for proof, not promises#

Use an evidence-first review when you evaluate providers:

| Evidence item | Specific focus |

|---|---|

| PCI and security documentation | The specific product variant you will use |

| Security certifications and compliance documentation | Used in partner evaluation |

| Incident-readiness practices | Breach scenarios |

| Data-segmentation documentation | Shared infrastructure models |

This matters most in shared, multi-merchant environments, where strict segmentation and incident readiness are critical. If a provider cannot show clear compliance artifacts, segmentation controls, and concrete incident-readiness practices, treat that as a real risk signal.

Failure modes and recovery paths without duplicate charges#

The recovery goal is simple: keep one customer intent from turning into two debits when failures happen. You will still see timeouts, retries, and other intermittent technical issues. What matters is whether your recovery path is safe and traceable.

The breakpoints worth designing for first#

Some failures are technical and intermittent, and teams can misread them as customer behavior. When that happens, the wrong retry action can create a duplicate-charge incident.

| Breakpoint | What may have happened | First recovery check |

|---|---|---|

| Timeout or latency spike | A prior attempt's final outcome may be unclear | Query the provider by transaction reference before creating a new payment |

| Duplicate-transaction prevention trigger | A valid follow-up attempt was flagged as a possible duplicate | Check inquiry or transaction history before creating a fresh charge |

| Retry after unclear outcome | A follow-up attempt is sent before the first outcome is confirmed | Reuse the same idempotency key and return the original result if it exists |

| Hard vs soft decline | The failure is either permanent (hard) or potentially temporary (soft) | Avoid blind retries on hard declines; retry or adjust only for soft declines |

If you use payment failover or automatic traffic rerouting, include transaction safety in the same design. Failover can keep checkout running when a gateway, processor, or network path goes down, but weak idempotency can still increase duplicate-debit risk across paths.

A practical operator rule is simple: if you cannot prove the prior attempt's final state, do not create a fresh charge blindly. Investigate first. Provider inquiry-style endpoints are useful here, and gateway docs may explicitly include inquiry transaction actions and transaction-history retrieval after a given transaction ID.

Put idempotent retry protection in three places#

Idempotency should cover initial payment creation, retry handling, and failover rerouting, not just the initial create call. One intent should resolve to one payment outcome, and retries should return the existing result when it already exists.

Use the same discipline in retry logic. A hard decline is a permanent failure, so retrying is usually not useful. A soft decline can recover after retry or adjustment.

Give finance and support a state model they can actually use#

Finance, support, and product should use the same internal triage model so they are not describing the same payment in different ways:

- pending auth

- authorized-not-settled

- settled

- reversed

- disputed (chargeback)

Treat this as your internal operating model, not an industry-standard taxonomy. Its value is consistent mapping and faster incident handling.

The minimum investigation pack for every payment#

Open duplicate-charge or unmatched-debit cases with these four artifacts attached:

- provider transaction ID

- internal payment ID

- ledger journal reference

- current reconciliation status

These records let teams compare provider history with internal state quickly and consistently. As a control check, confirm your data model avoids duplicate cardholder data across multiple records, and confirm teams can trace one payment through its lifecycle without ambiguity.

How to evaluate cost beyond headline fees#

If you evaluate a gateway only by the rate card, you can undercount total cost. Compare total payment cost per successful order and per month, not just the quoted 2%-3.5% + a fixed fee.

A gateway connects checkout to institutions that authorize and settle transactions, but your real spend can sit across gateway fees, processor fees, merchant account terms, compliance work, operations, and integration upkeep. Include monthly and per-transaction charges, then add costs created by declined payments, delayed fund movement, and manual work.

Start with the rate card, then break it apart#

Start by identifying the pricing model: flat-rate, interchange-plus, or tiered. These three models can produce very different total outcomes. For direct costs, model your expected transaction mix instead of a single blended bucket. Separate processor markup from interchange and assessment fees so you can see whether cost changes come from payment mix, network costs, or provider margin.

Use one monthly control: reconcile gross processed volume, provider payout reporting, and cash received in the merchant account. Fees are often deducted before funds arrive, so those numbers will not match automatically.

Hidden costs usually show up in ops, finance, and engineering#

Most hidden costs are operational, not just pricing line items.

| Cost line item | Owner | Measurement source | Monthly review cadence |

|---|---|---|---|

| Monthly fees and platform charges | Finance | Contract and provider invoices | Monthly |

| Per-transaction charges | Finance and product | Rate card and payout report | Monthly |

| Declined or failed payment handling | Support and product | Support tickets, retry volume, decline logs | Monthly |

| Manual reconciliation work | Finance ops | Reconciliation backlog, unmatched transactions | Monthly |

| Chargeback labor and fees | Finance ops and support | Dispute queue, handling time, provider reports | Monthly |

| Engineering maintenance for API integration | Engineering | Incident tickets, release work, webhook and retry errors | Monthly |

Pay extra attention to declined-payment handling and chargebacks. They add both fee exposure and labor load. Also account for PCI and compliance overhead, possible delays in fund movement, and merchant account terms such as reserves or payout holds, since each can affect cash flow.

Compare cost by business shape, not just provider#

Run scenario views for your operating model. A low-volume, high-touch business may prioritize lower operational drag. A high-volume flow with payout dependencies may be more sensitive to markup, dispute load, reconciliation effort, and funding timing.

Choose the option that minimizes total operating cost and cash-flow friction for your business shape, not the option with the lowest headline rate card.

Need the full breakdown? Read Gateway Routing for Platforms: How to Use Multiple Payment Gateways to Maximize Approval Rates.

Payment methods and channels you should support first#

Support the payment methods you need for launch first, then expand. An initial mix can include credit cards, debit cards, and digital wallets, with additional rails added when audience demand is clear.

The goal is to reduce checkout friction, not to enable every option in a provider catalog. A poor gateway choice can increase payment friction and lost purchases, so start with a method mix that balances coverage with manageable product and ops load.

Pick channels deliberately#

A gateway can support online, in-app, and in-person acceptance, and it may connect to your website or your point-of-sale (POS) system. Do not assume a provider's payment terminal setup is automatically the right fit for your online stack, or vice versa.

Before you decide, confirm required channel support explicitly for your launch scope:

- Online checkout

- In-app acceptance

- In-person POS or terminal acceptance

If you only sell online today, avoid adding in-person complexity early. If in-person is already in scope, confirm the POS connection fits your online integration and support workflow.

Treat QR and NFC as demand-led features#

For in-person acceptance, QR code and Near Field Communication (NFC) support can help, but they are not automatic requirements. Add them when they match real customer behavior and your operating context, not because they appear on a feature checklist.

Related reading: Global Payment Processing Infrastructure Choices for Platforms.

Cross-border realities for service platforms#

For service platforms, cross-border expansion is not a checkout add-on. It is a merchant account, authorization, and fund-movement decision from day one. Before you commit market launch dates, confirm supported countries, currencies, and payment methods for the exact provider program you plan to use.

In cross-border checkout, buyers may choose a currency such as USD or GBP, and the gateway may show the final amount with any exchange rate applied. Validate that flow end to end: what the buyer sees, what your payment records store, and what support can retrieve later. If those views do not line up, refunds, disputes, and customer explanations get harder.

Coverage is where plans often break. A provider can support global cards, wallets, and overseas banking systems overall, while availability can vary by market and program. Get explicit market-by-market confirmation for country coverage, customer currency support, and payment-method support, and keep it with product signoff.

Authorization also deserves extra attention across borders. The merchant bank may forward transaction details to the customer's card issuer for authorization, and each handoff can introduce another failure point. Track authorized and finalized amounts separately, because authorization is not the same as received funds.

If your platform also runs payouts, tie payment intake states to your internal payout and finance reconciliation workflows from the start. Keep one shared record across support, ops, and finance that links the provider payment reference, your internal booking or order ID, payout reference, and current reconciliation status.

For a step-by-step walkthrough, see Multi-Currency Payment Processing for Platforms: How to Accept and Disburse in 50+ Currencies.

Implementation checkpoints before launch#

Do not launch on happy-path approvals alone. Before live traffic, gather test evidence across product, engineering, finance, and ops for normal flows, failure flows, and record traceability.

| Team | Primary checks | Evidence to confirm |

|---|---|---|

| Product | Success criteria for online checkout and payment link | Approvals, declines, interrupted sessions, and recovery after failure; support can map the customer-facing message to the internal payment record |

| Engineering | Normal and failure paths your provider and architecture can produce | Observed behavior against prepared test data |

| Finance and ops | Reporting and reconciliation end to end | Trace one payment across the internal booking or order ID, provider payment reference, and the report used for reconciliation; include refunds and chargebacks |

If you chose a custom integration, keep extra testing time in plan. Prebuilt checkout can ship in days, while API-led builds can take weeks, and flexibility usually increases testing burden.

Product checks that protect conversion#

Start with clear success criteria for online checkout and payment link, including what customers see when payments fail, stay pending, or need another attempt.

Use a dedicated payment-gateway checklist that covers test environment setup, test data preparation, and error handling and messaging. Include named scenarios for approvals, declines, interrupted sessions, and recovery after failure. For each failure state, confirm support can map the customer-facing message to the internal payment record.

Engineering checks for event reliability#

Engineering should validate that the integration behaves reliably across the normal and failure paths your provider and architecture can produce. Test those paths against prepared test data, and keep launch evidence focused on observed behavior, not only design intent.

Finance and ops checks for money movement#

Before the first live charge, validate reporting and reconciliation end to end. You should be able to trace one payment across the internal booking or order ID, provider payment reference, and the report used for reconciliation.

Include refunds and chargebacks in the same scope, and confirm operations can find the original payment and related records.

Go-live gate#

Use a go-live gate based on documented test evidence, not verbal readiness. If key test artifacts are missing, delay launch until those gaps are closed.

For ACH-specific collection and payout controls, use ACH Payment Processing Platforms for U.S. Collections and Payouts.

Conclusion#

The right choice is the payment setup your team can run reliably when transactions fail, not the provider with the best pitch. A gateway can encrypt and transmit payment data and support real-time authorization between the merchant, acquiring bank, and issuing bank. Your operating model determines whether that setup works in practice.

Start with ownership capacity. Hosted and API integrations are both common options. Choose the option your team can operate clearly day to day, especially when payment states need investigation.

Keep role boundaries explicit. Gateway and processor terms are often used inconsistently, so your contract and implementation plan should make this unambiguous: who owns payment data capture and authorization flow, and who owns network-facing processing and clearing or capture.

Before signing, test observable states, not just checkout success. Confirm both that the payment was approved and that the charge was submitted for settlement, because those are different states with different support and finance implications.

Use a one-page scorecard to force decision clarity before final selection:

- Integration option: hosted, API, or both

- Role split: gateway responsibilities vs processor responsibilities

- Observable states: authorization result and settlement-submission status

- Transaction checkpoints: payment submit trigger, approval status, and settlement-submission status

- Channel fit: online only or online plus POS

Then run a launch-readiness review with product, engineering, finance, and ops before committing dates. If one owner cannot clearly support monitoring, exception handling, and payment-state tracing, treat that as a blocker.

Turn your vendor scorecard into numbers by running your own mix of methods and volumes in the payment fee comparison tool before final selection.

Frequently Asked Questions

What does a payment gateway do in online payment processing?

A payment gateway is the secure front end of online payment processing. It captures payment data at checkout, encrypts and routes that data, and triggers authorization. It does not move funds into your bank account.

What is the difference between a payment gateway and a payment processor?

The gateway handles payment data capture, encryption, and the authorization flow. The processor executes fund movement with banking partners. If a provider bundles both, confirm which component owns each role.

Do service businesses always need a payment gateway for online payments?

Not always as a separate product. What matters is that your setup still covers secure payment data capture and encryption. It also needs to match your channels and PCI-DSS posture.

How does payment processing work step by step from checkout to settlement?

The customer enters payment details and submits checkout, then the gateway sends an authorization request and returns an approval or decline. After approval, the payment moves through clearing and settlement based on the provider flow. Your team should track authorization and final fund movement as separate states.

How much does a payment gateway cost beyond transaction fees?

Headline transaction pricing is only the starting point. Compare monthly fees, per transaction charges, compliance work, operations, integration upkeep, declined payment handling, reconciliation effort, and chargeback labor and fees. Review total cost per successful order and per month, not just the rate card.

Can one setup support online checkout and in-person POS payments?

Yes, some setups support both online checkout and physical POS transactions. The key check is whether those channels line up in reporting and reconciliation. Confirm the POS connection fits your online integration and support workflow before rollout.

What should platform teams verify before selecting a gateway provider?

Start by verifying country and currency support for the exact provider program you plan to use. Then confirm the checkout model, what part of the flow is hosted, whether your systems touch card data, the full fee structure, and average go live time. If you plan geography based routing or acceptance testing, confirm multi gateway support and whether your team can handle the added operational complexity.

Researched and edited by the Gruv editorial team. Gruv builds cross-border billing, payouts, and finance-operations software for global businesses.

Sources

Includes 5 external sources outside the trusted-domain allowlist.

- paypal.com/us/brc/article/what-is-a-payment-gatewaytrusted

- stripe.com/resources/more/payment-gateways-101trusted

- stripe.com/resources/more/payment-failovertrusted

- adyen.com/knowledge-hub/payment-gatewayexternal

- aspireapp.com/us/blog/payment-gatewayexternal

- bigcommerce.com/articles/ecommerce/payment-gatewaysexternal

- bill.com/learning/payment-gatewaysexternal

- decta.com/company/media/how-to-choose-between-hosted-c...external

Educational content only. Not legal, tax, or financial advice.

Related Posts

The Freelance Payment Penalty: A Modeled Audit of Platform Fees, FX Spreads, and Payout Delays

The money rarely disappears through a single, easy-to-spot fee. The real loss is stacked. A marketplace takes its commission, a processor adds a charge for international cards, a bank or payment company converts the currency at a spread, a platform holds the funds before release, and a wire sheds a little to intermediaries on the way in. Each layer looks defensible on its own, but the worker feels the combined result as a smaller deposit and a later payday.

How to Respond to a Subpoena for Business Records

Move fast, but do not produce records on instinct. If you need to **respond to a subpoena for business records**, your immediate job is to control deadlines, preserve records, and make any later production defensible.

A US Expat's Guide to Investing in UCITS ETFs to Avoid PFIC Issues

The real problem is a two-system conflict. U.S. tax treatment can punish the wrong fund choice, while local product-access constraints can block the funds you want to buy in the first place. For **us expat ucits etfs**, the practical question is not "Which product is best?" It is "What can I access, report, and keep doing every year without guessing?" Use this four-part filter before any trade: